financial services

Auto Added by WPeMatico

Auto Added by WPeMatico

Business, now more than ever before, is going digital, and today a startup that’s building a vertically integrated solution to meet business banking needs is announcing a big round of funding to tap into the opportunity. Airwallex — which provides business banking services directly to businesses themselves as well as via a set of APIs that power other companies’ fintech products — has raised $200 million, a Series E round of funding that values the Australian startup at $4 billion.

Lone Pine Capital is leading the round, with new backers G Squared and Vetamer Capital Management, and previous backers 1835i Ventures (formerly ANZi), DST Global, Salesforce Ventures and Sequoia Capital China also participating.

The funding brings the total raised by Airwallex — which has head offices in Hong Kong and Melbourne, Australia — to $700 million, including a $100 million injection that closed out its Series D just six months ago.

Airwallex will be using the funding both to continue investing in its product and technology as well as to continue its geographical expansion and to focus on some larger business targets. The company has started to make some headway into Europe and the U.K. and that will be one big focus, along with the U.S.

The quick succession of funding and rising valuation underscore Airwallex’s traction to date around what CEO and co-founder Jack Zhang describes as a vertically integrated strategy.

That involves two parts. First, Airwallex has built all the infrastructure for the business banking services that it provides directly to businesses with a focus on small and medium enterprise customers. Second, it has packaged up that infrastructure into a set of APIs that a variety of other companies use to provide financial services directly to their customers without needing to build those services themselves — the so-called “embedded finance” approach.

“We want to own the whole ecosystem,” Zhang said to me. “We want to be like the Apple of business finance.”

That seems to be working out so far for Airwallex. Revenues were up almost 150% for the first half of 2021 compared to a year before, with the company processing more than US$20 billion for a global client portfolio that has quadrupled in size. In addition to tens of thousands of SMEs, it also, via APIs, powers financial services for other companies like GOAT, Papaya Global and Stake.

Airwallex got its start like many of the strongest startups do: It was built to solve a problem that the founders encountered themselves. In the case of Airwallex, Zhang tells me he had actually been working on a previous startup idea. He wanted to build the “Blue Bottle Coffee” of Asia Pacific out of Australia, and it involved buying and importing a lot of different materials, packaging and, of course, coffee from all around the world.

“We found that making payments as a small business was slow and expensive,” he said, since it involved banks in different countries and different banking systems, manual efforts to transfer money between them and many days to clear the payments. “But that was also my background — payments and trading — and so I decided that it was a much more fascinating problem for me to work on and resolve.”

Eventually one of his co-founders in the coffee effort came along, with the four co-founders of Airwallex ultimately including Zhang, along with Xijing Dai, Lucy Liu and Max Li.

It was 2014, and Airwallex got attention from VCs early on in part for being in the right place at the right time. A wave of startups building financial services for SMBs were definitely gaining ground in North America and Europe, filling a long-neglected hole in the technology universe, but there was almost nothing of the sort in the Asia Pacific region, and in those earlier days solutions were highly regionalized.

From there it was a no-brainer that starting with cross-border payments, the first thing Airwallex tackled, would soon grow into a wider suite of banking services involving payments and other cross-border banking services.

“In the last six years, we’ve built more than 50 bank integrations and now offer payments across 95 countries, payments through a partner network,” he added, with 43 of those offering real-time transactions. From that, it moved on to bank accounts and “other primitive stuff” with card issuance and more, he said, eventually building an end-to-end payment stack.

Airwallex has tens of thousands of customers using its financial services directly, and they make up about 40% of its revenues today. The rest is the interesting turn the company decided to take to expand its business.

Airwallex had built all of its technology from the ground up itself, and it found that — given the wave of new companies looking for more ways to engage customers and become their one-stop shop — there was an opportunity to package that tech up in a set of APIs and sell that on to a different set of customers, those who also provided services for small businesses. That part of the business now accounts for 60% of Airwallex’s business, Zhang said, and is growing faster in terms of revenues. (The SMB business is growing faster in terms of customers, he said.)

A lot of embedded finance startups that base their business around building tech to power other businesses tend to stay at arm’s length from offering financial services directly to consumers. The explanation I have heard is that they do not wish to compete against their customers. Zhang said that Airwallex takes a different approach, by being selective about the customers they partner with, so that the financial services they offer would not be in direct competition with those of its customers. The GOAT marketplace for sneakers, or Papaya Global’s HR platform are classic examples of this.

However, as Airwallex continues to grow, you can’t help but wonder whether one of those partners might like to gobble up all of Airwallex and take on some of that service provision role itself. In that context, it’s very interesting to see Salesforce Ventures returning to invest even more in the company in this round, given how widely the company has expanded from its early roots in software for salespeople into a massive platform providing a huge range of cloud services to help people run their businesses.

For now, it’s been the combination of its unique roots in Asia Pacific, plus its vertical approach of building its tech from the ground up, plus its retail acumen that has impressed investors and may well see Airwallex stay independent and grow for some time to come.

“Airwallex has a clear competitive advantage in the digital payments market,” said David Craver, MD at Lone Pine Capital, in a statement. “Its unique Asia-Pacific roots, coupled with its innovative infrastructure, products and services, speak volumes about the business’ global growth opportunities and its impressive expansion in the competitive payment providers space. We are excited to invest in Airwallex at this dynamic time, and look forward to helping drive the company’s expansion and success worldwide.”

Updated to note that the coffee business was in Australia, not Hong Kong.

Powered by WPeMatico

When Anik Khan graduated from college, his first job was working on credit cards and business expenses at Accenture. There, he found that someone could bring in a couple of thousand dollars just by having the right credit cards and following the rewards and promotions.

It was back in 2017 when he and David Gao got the idea for his company MaxRewards, a digital wallet app that manages credit cards and automatically activates benefits like rewards, cashback offers and monthly credits. It also makes recommendations at the point of purchase on which card would yield the best reward for that purchase.

Going after the some 83% of Americans that have a credit card, the app version was officially launched in 2019, and now the Atlanta-based company is announcing a $3 million seed round co-led by Dundee Venture Capital and Calano Ventures. Also backing the company are Techstars, Fintech Ventures Fund, Service Provider Capital and Fleetcor president Nick Izquierdo.

Tracking his own credit cards manually prior to MaxRewards, Khan recalled in one year, getting $16,000 in rewards. However, utilizing those benefits was time-consuming and difficult, because the rewards and savings aren’t always made evident by the credit card companies.

“Other companies have tried to do something similar, but the issue is you don’t have the reward information or the offers,” Khan told TechCrunch. “If you were to aggregate this information, you still would have to activate all of these things and use them before they expired.”

Users connect their accounts and when they make a purchase, their location is cross-referenced with the merchant and an algorithm is applied to tell the user which card to use. The average app user has six credit cards.

MaxRewards is free to download and use, and the majority of the app’s functionalities are free. Users who want additional features, like the auto activation or rewards, can join MaxRewards Gold and are given the opportunity to choose their own monthly price — the average is over $25 per month — based on the value they expect to gain, Khan said.

MaxRewards offers and benefits. Image Credits: MaxRewards

Ron Watson, partner at Dundee, said his firm invests in seed-stage companies between the coasts and is interested in consumer and e-commerce companies. Watson said he was impressed with what MaxRewards has been able to do with a team of three. He also relates to the company’s mission, having grown up in a lower, middle-class family that did not frequently go on vacations.

When he got his first job and was suddenly flying everywhere, he recalls building up so many rewards to the point where he was able to go on a vacation to Hawaii and only spend maybe $100, he said.

“I used to put my points into a spreadsheet, but as I got older and had kids, I realized how hard it was for the average person to do that and how important it is to have automation,” Watson said. “I downloaded the app, and on the first day, saved $20.”

The company is often compared to NerdWallet or Mint, but in terms of functionality, Khan said he feels MaxRewards is unique due to its credit card system connectors. Rather than rely on third-party aggregators to discover the rewards, MaxRewards leverages its own proprietary connectors to card systems.

There are hundreds of thousands of offers to be discovered, and consumers are asking for even more features, so Khan decided it was time to go after seed funding. He had raised a small seed, about $200,000, from his time at Techstars, but the new funding will enable him to add to his team of three people. He expects to be at 20 by the end of the year. Khan also wants to accelerate its user acquisition, product improvement and compliance.

Next up, the company is going to automate rewards and savings across additional platforms like debit cards, payment apps and cashback apps, as well as create browser extensions and a web app. Khan also wants to do more on the education side with regard to using credit cards in a smart manner.

Arron Solano, managing partner at Calano, met Khan through Techstars and said he is an advocate for using credit cards in the right way. His firm was looking for a company like MaxRewards.

“During our first call, I remember telling my partner that Anik was a bulldog who knew what he was talking about, especially at that stage,” Solano added. “He had strong team members, his vision lined up well and that checked off a massive box for us. He energized us and showed he could find a market with insanely high ‘super users.’ ”

Powered by WPeMatico

A Canadian startup called Nuula that is aiming to build a super app to provide a range of financial services to small and medium businesses has closed $120 million of funding, money that it will use to fuel the launch of its app and first product, a line of credit for its users.

The money is coming in the form of $20 million in equity from Edison Partners, and a $100 million credit facility from funds managed by the Credit Group of Ares Management Corporation.

The Nuula app has been in a limited beta since June of this year. The plan is to open it up to general availability soon, while also gradually bringing in more services, some built directly by Nuula itself but many others following an embedded finance strategy: business banking, for example, will be a service provided by a third party and integrated closely into the Nuula app to be launched early in 2022. Alongside that, the startup will also be making liberal use of APIs to bring in other white-label services, such as B2B and customer-focused payment services, starting first in the U.S. and then expanding to Canada and the U.K. before expanding further into countries across Europe.

Current products include cash flow forecasting, personal and business credit score monitoring, and customer sentiment tracking; and monitoring of other critical metrics including financial, payments and e-commerce data are all on the roadmap.

“We’re building tools to work in a complementary fashion in the app,” CEO Mark Ruddock said in an interview. “Today, businesses can project if they are likely to run out of money, and monitor their credit scores. We keep an eye on customers and what they are saying in real time. We think it’s necessary to surface for SMBs the metrics that they might have needed to get from multiple apps, all in one place.”

Nuula was originally a side-project at BFS, a company that focused on small business lending, where the company started to look at the idea of how to better leverage data to build out a wider set of services addressing the same segment of the market. BFS grew to be a substantial business in its own right (and it had raised its own money to that end, to the tune of $184 million from Edison and Honeywell). Over time, it became apparent to management that the data aspect, and this concept of a super app, would be key to how to grow the business, and so it pivoted and rebranded earlier this year, launching the beta of the app after that.

Nuula’s ambitions fall within a bigger trend in the market. Small and medium enterprises have shaped up to be a huge business opportunity in the world of fintech in the last several years. Long ignored in favor of building solutions either for the giant consumer market, or the lucrative large enterprise sector, SMBs have proven that they want and are willing to invest in better and newer technology to run their businesses, and that’s leading to a rush of startups and bigger tech companies bringing services to the market to cater to that.

Super apps are also a big area of interest in the world of fintech, although up to now a lot of what we’ve heard about in that area has been aimed at consumers — just the kind of innovation rut that Nuula is trying to get moving.

“Despite the growth in services addressing the SMB sector, overall it still lacks innovation compared to consumer or enterprise services,” Ruddock said. “We thought there was some opportunity to bring new thinking to the space. We see this as the app that SMBs will want to use everyday, because we’ll provide useful tools, insights and capital to power their businesses.”

Nuula’s priority to build the data services that connect all of this together is very much in keeping with how a lot of neobanks are also developing services and investing in what they see as their unique selling point. The theory goes like this: banking services are, at the end of the day, the same everywhere you go, and therefore commoditized, and so the more unique value-added for companies will come from innovating with more interesting algorithms and other data-based insights and analytics to give more power to their users to make the best use of what they have at their disposal.

It will not be alone in addressing that market. Others building fintech for SMBs include Selina, ANNA, Amex’s Kabbage (an early mover in using big data to help loan money to SMBs and build other financial services for them), Novo, Atom Bank, Xepelin and Liberis, biggies like Stripe, Square and PayPal, and many others.

The credit product that Nuula has built so far is a taster of how it hopes to be a useful tool for SMBs, not just another place to get money or manage it. It’s not a direct loaning service, but rather something that is closely linked to monitoring a customers’ incomings and outgoings and only prompts a credit line (which directly links into the users’ account, wherever it is) when it appears that it might be needed.

“Innovations in financial technology have largely democratized who can become the next big player in small business finance,” added Gary Golding, General Partner, Edison Partners. “By combining critical financial performance tools and insights into a single interface, Nuula represents a new class of financial services technology for small business, and we are excited by the potential of the firm.”

“We are excited to be working with Nuula as they build a unique financial services resource for small businesses and entrepreneurs,” said Jeffrey Kramer, Partner and Head of ABS in the Alternative Credit strategy of the Ares Credit Group, in a statement. “The evolution of financial technology continues to open opportunities for innovation and the emergence of new industry participants. We look forward to seeing Nuula’s experienced team of technologists, data scientists and financial service veterans bring a new generation of small business financial services solutions to market.”

Powered by WPeMatico

Itamar Jobani was a software developer working for a medical company and “hated that time of the month” when he had to use the company’s chosen reimbursement tool.

“It was full of friction and as part of the company’s wellness team, I felt an urge to take care of the employee experience and find a better tool,” Jobani told TechCrunch. “I looked for something, but didn’t find it, so I tried to build it myself.”

What resulted was PayEm, an Israeli company he founded with Omer Rimoch in 2019 to be a spend and procurement platform for high-growth and multinational organizations. Today, it announced $27 million in funding that includes $7 million in seed funding, led by Pitango First and NFX, with participation by LocalGlobe and Fresh Fund, as well as $20 million in Series A funding led by Glilot+.

The company’s technology automates the reimbursement, procurement, accounts payable and credit card workflows to manage all of the requests and invoices, while also creating bills and sending payments to over 200 territories in 130 currencies.

It gives company finance teams a real-time look at what items employees are asking for funds to buy, and what is actually being spent. For example, teams can submit a request and go through an approval flow that can be customized with purchasing codes tied to a description of the transaction. At the same time, all transactions are continuously reconciled versus having to spend hours at the end of the month going through paperwork.

“Organizations are running in a more democratized way with teams buying things on behalf of the organization,” Jobani said. “We built a platform to cater to those needs, so it’s like a disbursement platform instead of a finance team always being in charge.”

The global B2B payments market is valued at $120 trillion annually and is expected to reach $200 trillion by 2028, according to payment industry newsletter Nilson Report. PayEm is among many B2B payments startups attracting venture capital — for example, last month, Nium announced a $200 million in Series D funding at a $1 billion valuation. Paystand raised $50 million in Series C funding to make B2B payments cashless, while Dwolla raised $21 million for its API that allows companies to build and facilitate fast payments.

Meanwhile, PayEm itself saw accelerated growth in the second quarter of 2021, including increasing its transaction volume by four times over the previous quarter and generating millions of dollars in revenue. It now boasts a list of hundreds of customers like Fiverr, JFrog and Next Insurance. It also launched new features like the ability to create corporate cards.

The company, which also has an office in New York, has 40 employees currently, and the new funds will enable the company to triple its headcount, focusing on hiring in the United States, and to bring additional features and payment capabilities to market.

“Each person can have a budget and a time frame for making the purchase, while accounting still feels in control,” Jobani added. “Everyone now has the full context and the right budget line item.”

Powered by WPeMatico

On the heels of Heroes announcing a $200 million raise earlier today, to double down on buying and scaling third-party Amazon Marketplace sellers, another startup out of London aiming to do the same is announcing some significant funding of its own. Olsam, a roll-up play that is buying up both consumer and B2B merchants selling on Amazon by way of Amazon’s FBA fulfillment program, has closed $165 million — a combination of equity and debt that it will be using to fuel its M&A strategy, as well as continue building out its tech platform and to hire more talent.

Apeiron Investment Group — an investment firm started by German entrepreneur Christian Angermayer — led the Series A equity round, with Elevat3 Capital (another Angermayer firm that has a strategic partnership with Founders Fund and Peter Thiel) also participating. North Wall Capital was behind the debt portion of the deal. We have asked and Olsam is only disclosing the full amount raised, not the amount that was raised in equity versus debt. Valuation is also not being disclosed.

Being an Amazon roll-up startup from London that happens to be announcing a fundraise today is not the only thing that Olsam has in common with Heroes. Like Heroes, Olsam is also founded by brothers.

Sam Horbye previously spent years working at Amazon, including building and managing the company’s business marketplace (the B2B version of the consumer marketplace); while co-founder Ollie Horbye had years of experience in strategic consulting and financial services.

Between them, they also built and sold previous marketplace businesses, and they believe that this collective experience gives Olsam — a portmanteau of their names, “Ollie” and “Sam” — a leg up when it comes to building relationships with merchants; identifying quality products (versus the vast seas of search results that often feel like they are selling the same inexpensive junk as each other); and understanding merchants’ challenges and opportunities, and building relationships with Amazon and understanding how the merchant ecosystem fits into the e-commerce giant’s wider strategy.

Olsam is also taking a slightly different approach when it comes to target companies, by focusing not just on the usual consumer play, but also on merchants selling to businesses. B2B selling is currently one of the fastest-growing segments in Amazon’s Marketplace, and it is also one of the more overlooked by consumers. “It’s flying under the radar,” Ollie said.

“The B2B opportunity is very exciting,” Sam added. “A growing number of merchants are selling office supplies or more random products to the B2B customer.”

Estimates vary when it comes to how many merchants there are selling on Amazon’s Marketplace globally, ranging anywhere from 6 million to nearly 10 million. Altogether those merchants generated $300 million in sales (gross merchandise value), and it’s growing by 50% each year at the moment.

And consolidating sellers — in order to achieve better economies of scale around supply chains, marketing tools and analytics, and more — is also big business. Olsam estimates that some $7 billion has been spent cumulatively on acquiring these businesses, and there are more out there: Olsam estimates there are some 3,000 businesses in the U.K. alone making more than $1 million each in sales on Amazon’s platform.

(And to be clear, there are a number of other roll-up startups beyond Heroes also eyeing up that opportunity. Raising hundreds of millions of dollars in aggregate, others that have made moves this year include Suma Brands [$150 million], Elevate Brands [$250 million], Perch [$775 million], factory14 [$200 million], Thrasio [currently probably the biggest of them all in terms of reach and money raised and ambitions], Heyday, The Razor Group, Branded, SellerX, Berlin Brands Group [X2], Benitago, Latin America’s Valoreo and Rainforest and Una Brands out of Asia.)

“The senior team behind Olsam is what makes this business truly unique,” said Angermayer in a statement. “Having all been successful in building and selling their own brands within the market and having worked for Amazon in their marketplace team – their understanding of this space is exceptional.”

Powered by WPeMatico

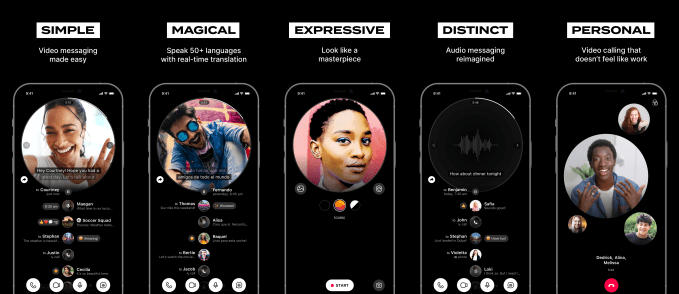

A London-headquartered startup called LOVE, valued at $17 million following its pre-seed funding, aims to redefine how people stay in touch with close family and friends. The company is launching a messaging app that offers a combination of video calling as well as asynchronous video and audio messaging, in an ad-free, privacy-focused experience with a number of bells and whistles, including artistic filters and real-time transcription and translation features.

But LOVE’s bigger differentiator may not be its product alone, but rather the company’s mission.

LOVE aims for its product direction to be guided by its user base in a democratic fashion as opposed to having the decisions made about its future determined by an elite few at the top of some corporate hierarchy. In addition, the company’s longer-term goal is ultimately to hand over ownership of the app and its governance to its users, the company says.

These concepts have emerged as part of bigger trends towards a sort of “Web 3.0,” or next phase of internet development, where services are decentralized, user privacy is elevated, data is protected and transactions take place on digital ledgers, like a blockchain, in a more distributed fashion.

LOVE’s founders are proponents of this new model, including serial entrepreneur Samantha Radocchia, who previously founded three companies and was an early advocate for the blockchain as the co-founder of Chronicled, an enterprise blockchain company focused on the pharmaceutical supply chain.

As someone who’s been interested in emerging technology since her days of writing her anthropology thesis on currency exchanges in “Second Life’s” virtual world, she’s now faculty at Singularity University, where she’s given talks about blockchain, AI, Internet of Things, Future of Work, and other topics. She’s also authored an introductory guide to the blockchain with her book “Bitcoin Pizza.”

Co-founder Christopher Schlaeffer, meanwhile, held a number of roles at Deutsche Telekom, including chief product & innovation officer, corporate development officer and chief strategy officer, where he along with Google execs introduced the first mobile phone to run Android. He was also chief digital officer at the telecommunication services company VEON.

The two crossed paths after Schlaeffer had already begun the work of organizing a team to bring LOVE to the public, which includes co-founders Chief Technologist Jim Reeves, also previously of VEON, and Chief Designer Timm Kekeritz, previously an interaction designer at international design firm IDEO in San Francisco, design director at IXDS and founder of design consultancy Raureif in Berlin, among other roles.

Image Credits: LOVE

Explained Radocchia, what attracted her to join as CEO was the potential to create a new company that upholds more positive values than what’s often seen today — in fact, the brand name “LOVE” is a reference to this aim. She was also interested in the potential to think through what she describes as “new business models that are not reliant on advertising or harvesting the data of our users,” she says.

To that end, LOVE plans to monetize without any advertising. While the company isn’t ready to explain its business model in full, it would involve users opting in to services through granular permissions and membership, we’re told.

“We believe our users will much rather be willing to pay for services they consciously use and grant permissions to in a given context than have their data used for an advertising model which is simply not transparent,” says Radocchia.

LOVE expects to share more about the model next year.

As for the LOVE app itself, it’s a fairly polished mobile messenger offering an interesting combination of features. Like any other video chat app, you can video call with friends and family, either in one-on-one calls or in groups. Currently, LOVE supports up to five call participants, but expects to expand that as it scales. The app also supports video and audio messaging for asynchronous conversations. There are already tools that offer this sort of functionality on the market, of course — like WhatsApp, with its support for audio messages, or video messenger Marco Polo. But they don’t offer quite the same expanded feature set.

Image Credits: LOVE

For starters, LOVE limits its video messages to 60 seconds, for brevity’s sake. (As anyone who’s used Marco Polo knows, videos can become a bit rambling, which makes it harder to catch up when you’re behind on group chats.) In addition, LOVE allows you to both watch the video content as well as read the real-time transcription of what’s being said — the latter which comes in handy not only for accessibility’s sake, but also for those times you want to hear someone’s messages but aren’t in a private place to listen or don’t have headphones. Conversations can also be translated into 50 languages.

“A lot of the traditional communication or messenger products are coming from a paradigm that has always been text-based,” explains Radocchia. “We’re approaching it completely differently. So while other platforms have a lot of the features that we do, I think that…the perspective that we’ve approached it has completely flipped it on its head,” she continues. “As opposed to bolting video messages on to a primarily text-based interface, [LOVE is] actually doing it in the opposite way and adding text as a sort of a magically transcribed add-on — and something that you never, hopefully, need to be typing out on your keyboard again,” she adds.

The app’s user interface, meanwhile, has been designed to encourage eye-to-eye contact with the speaker to make conversations feel more natural. It does this by way of design elements where bubbles float around as you’re speaking and the bubble with the current speaker grows to pull your focus away from looking at yourself. The company is also working with the curator of Serpentine Gallery in London, Hans Ulrich-Obrist, to create new filters that aren’t about beautification or gimmicks, but are instead focused on introducing a new form of visual expression that makes people feel more comfortable on camera.

For the time being, this has resulted in a filter that slightly abstracts your appearance, almost in the style of animation or some other form of visual arts.

The app claims to use end-to-end encryption and the automatic deletion of its content after seven days — except for messages you yourself recorded, if you’ve chosen to save them as “memorable moments.”

“One of our commitments is to privacy and the right-to-forget,” says Radocchia. “We don’t want to be or need to be storing any of this information.”

LOVE has been soft-launched on the App Store, where it’s been used with a number of testers and is working to organically grow its user base through an onboarding invite mechanism that asks users to invite at least three people to join. This same onboarding process also carefully explains why LOVE asks for permissions — like using speech recognition to create subtitles.

LOVE says its valuation is around $17 million USD following pre-seed investments from a combination of traditional startup investors and strategic angel investors across a variety of industries, including tech, film, media, TV and financial services. The company will raise a seed round this fall.

The app is currently available on iOS, but an Android version will arrive later in the year. (Note that LOVE does not currently support the iOS 15 beta software, where it has issues with speech transcription and in other areas. That should be resolved next week, following an app update now in the works.)

Powered by WPeMatico

Earlier today, spend management startup Ramp said it has raised a $300 million Series C that valued it at $3.9 billion. It also said it was acquiring Buyer, a “negotiation-as-a-service” platform that it believes will help customers save money on purchases and SaaS products.

The round and deal were announced just a week after competitor Brex shared news of its own acquisition — the $50 million purchase of Israeli fintech startup Weav. That deal was made after Brex’s founders invested in Weav, which offers a “universal API for commerce platforms.”

From a high level, all of the recent deal-making in corporate cards and spend management shows that it’s not enough to just help companies track what employees are expensing these days. As the market matures and feature sets begin to converge, the players are seeking to differentiate themselves from the competition.

But the point of interest here is these deals can tell us where both companies think they can provide and extract the most value from the market.

These differences come atop another layer of divergence between the two companies: While Brex has instituted a paid software tier of its service, Ramp has not.

Let’s start with Ramp. Launched in 2019, the company is a relative newcomer in the spend management category. But by all accounts, it’s producing some impressive growth numbers. As our colleague Mary Ann Azevedo wrote:

Since the beginning of 2021, the company says it has seen its number of cardholders on its platform increase by 5x, with more than 2,000 businesses currently using Ramp as their “primary spend management solution.” The transaction volume on its corporate cards has tripled since April, when its last raise was announced. And, impressively, Ramp has seen its transaction volume increase year over year by 1,000%, according to CEO and co-founder Eric Glyman.

Ramp’s focus has always been on helping its customers save money: It touts a 1.5% cash back reward for all purchases made through its cards, and says its dashboard helps businesses identify duplicitous subscriptions and license redundancies. Ramp also alerts customers when they can save money on annual versus monthly subscriptions, which it says has led many customers to do away with established T&E platforms like Concur or Expensify.

All told, the company claims that the average customer saves 3.3% per year on expenses after switching to its platform — and all that is before it brings Buyer into the fold.

Powered by WPeMatico

Oh, how the tables have turned.

It used to be that if you were a fintech startup or, for lack of a better term, a digitally native financial services business, you might be eyeing an acquisition from an incumbent in the industry.

It used to be that if you were a fintech startup or, for lack of a better term, a digitally native financial services business, you might be eyeing an acquisition from an incumbent in the industry.

But lately, fintech upstarts are the ones doing the acquiring. Over just the last year or so, we’ve seen:

So what’s going on here? Why are fintechs now acquiring legacy financial services businesses, instead of the other way around?

Powered by WPeMatico

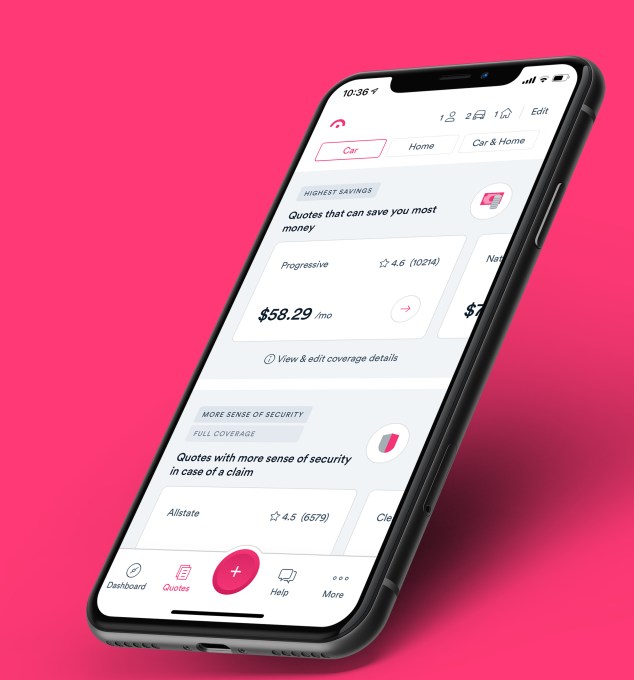

Just months after raising $28 million, Jerry announced today that it has raised $75 million in a Series C round that values the company at $450 million.

Existing backer Goodwater Capital doubled down on its investment in Jerry, leading the “oversubscribed” round. Bow Capital, Kamerra, Highland Capital Partners and Park West Asset Management also participated in the financing, which brings Jerry’s total raised to $132 million since its 2017 inception. Goodwater Capital also led the startup’s Series B earlier this year. Jerry’s new valuation is about “4x” that of the company at its Series B round, according to co-founder and CEO Art Agrawal.

“What factored into the current valuation is our annual recurring revenue, growing customer base and total addressable market,” he told TechCrunch, declining to be more specific about ARR other than to say it is growing “at a very fast rate.” He also said the company “continues to meet and exceed growth and revenue targets” with its first product, a service for comparing and buying car insurance. At the time of the company’s last raise, Agrawal said Jerry saw its revenue surge by “10x” in 2020 compared to 2019.

Jerry, which says it has evolved its model to a mobile-first car ownership “super app,” aims to save its customers time and money on car expenses. The Palo Alto-based startup launched its car insurance comparison service using artificial intelligence and machine learning in January 2019. It has quietly since amassed nearly 1 million customers across the United States as a licensed insurance broker.

“Today as a consumer, you have to go to multiple different places to deal with different things,” Agrawal said at the time of the company’s last raise. “Jerry is out to change that.”

The new funding round fuels the launch of the company’s “compare-and-buy” marketplaces in new verticals, including financing, repair, warranties, parking, maintenance and “additional money-saving services.” Although Jerry also offers a similar product for home insurance, its focus is on car ownership.

Image Credits: Jerry

“Access to reliable and affordable transportation is critical to economic empowerment,” said Rafi Syed, Jerry board member and general partner at Bow Capital, which also doubled down on its investment in the company. “Jerry is helping car owners make the most of every dollar they earn. While we see Jerry as an excellent technology investment showcasing the power of data in financial services, it’s also a high-performing investment in terms of the financial inclusion it supports.”

Goodwater Capital Partner Chi-Hua Chien said the firm’s recurring revenue model makes it stand out from lead generation-based car insurance comparison sites.

CEO Agrawal agrees, noting that Jerry’s high-performing annual recurring revenue model has made the company “attractive to investors” in addition to the fact that the startup “straddles” the auto, e-commerce, fintech and insurtech industries.

“We recognized those investment opportunities could drive our business faster and led to raising the round earlier than expected,” he told TechCrunch. “We’re eager to launch new categories to save customers time and money on auto expenses and the new investment shortens our time to market.”

Agrawal also believes Jerry is different from other auto-related marketplaces out there in that it aims to help consumers with various aspects of car ownership (from repair to maintenance to insurance to warranties), rather than just one. The company also believes it is set apart from competitors in that it doesn’t refer a consumer to an insurance carrier’s site so that they still have to do the work of signing up with them separately, for example. Rather, Jerry uses automation to give consumers customized quotes from more than 45 insurance carriers “in 45 seconds.” The consumers can then sign on to the new carrier via Jerry, which can then cancel former policies on their behalf.

Jerry makes recurring revenue from earning a percentage of the premium when a consumer purchases a policy on its site from carriers such as Progressive.

Powered by WPeMatico

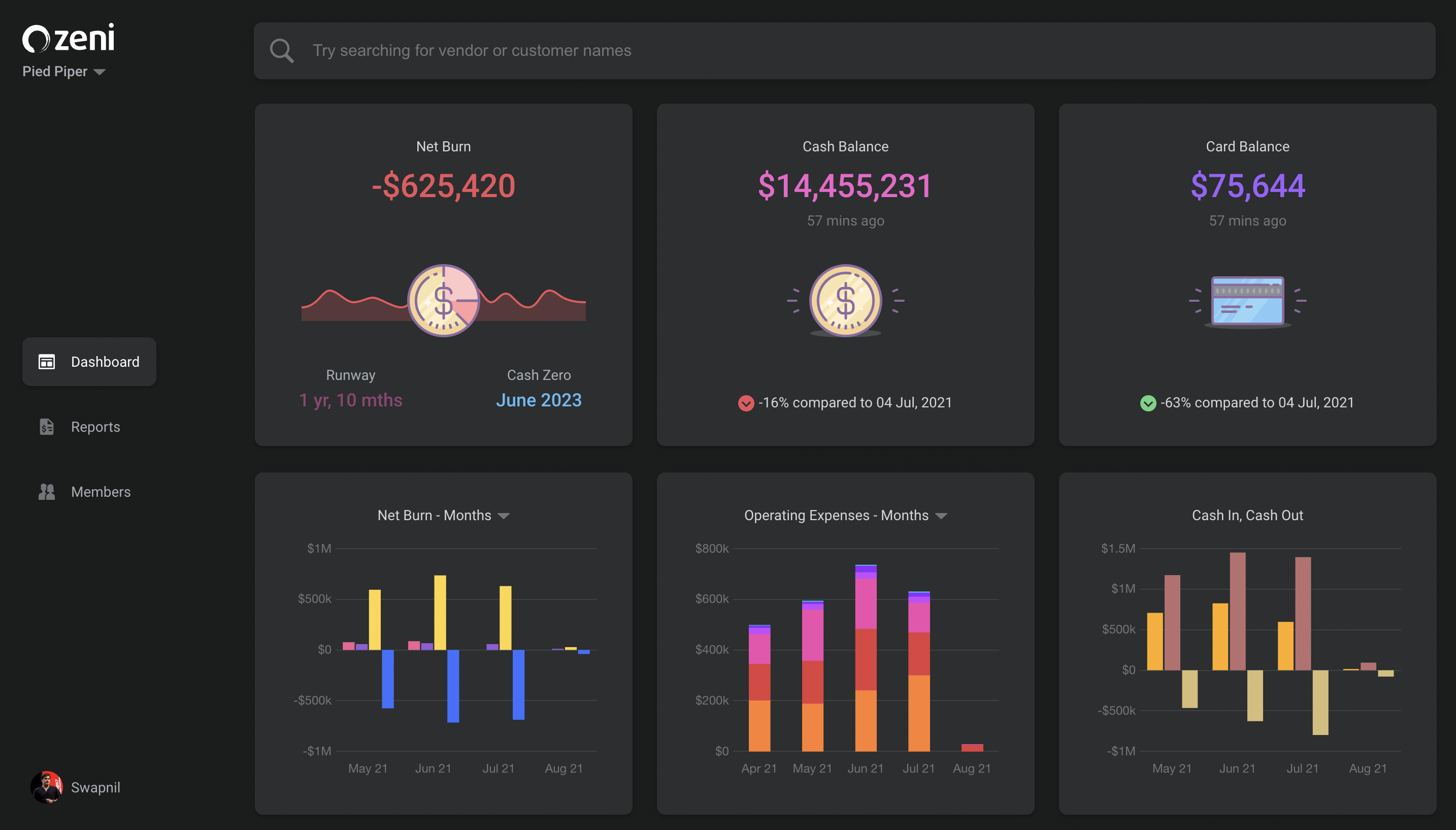

Zeni, a Palo Alto fintech company providing real-time financial services data to venture-backed startups, raised $34 million in Series B funding led by Elevation Capital.

The new investment comes just five months after Zeni announced $13.5 million in a combined seed and Series A round. The company has now raised $47.5 million in total since it was co-founded in 2019 by twin brothers Swapnil Shinde and Snehal Shinde.

Elevation was joined in the new round by new investors Think Investments and Neeraj Arora, as well as existing investors Saama Capital, Amit Singhal, Sierra Ventures, Twin Ventures, Dragon Capital and Liquid 2 Ventures. As part of the investment, Ravi Adusumalli, founder and managing partner at Elevation Capital, will join Zeni’s board.

The Shinde siblings started the company after selling their last company, Mezi, a travel concierge, to American Express in 2018. Zeni’s AI-powered finance concierge platform offers bookkeeping, accounting, tax and CFO services, managing these for a flat monthly fee starting at $299 per month. Founders have real-time access to financial insights via the Zeni Dashboard, including cash in and out, operating expenses, yearly taxes and financial projections. They can also download the financial data in the “slice” that they want.

At the time of its seed/Series A round, the company was managing more than $200 million in funds each month, and that has ballooned to more than $500 million, CEO Swapnil Shinde told TechCrunch. Its customers range from pre-revenue startups to businesses generating more than $100 million in annual revenue.

In addition to the cash in and cash out analysis, the company also created a search function for transactions and spend and income trends on every customer and vendor, Snehal Shinde, chief product officer, said.

Zeni’s dashboard

Zeni experienced 550% revenue growth year-over-year, while the company’s customer base grew 375%, driven by referrals and organic growth, Swapnil Shinde said.

Despite the growth, the Series B came as a surprise to the siblings. The company was already “very well capitalized,” with a majority of the previous round still around, Swapnil Shinde said.

However, Zeni began receiving so many inbound inquiries that he said it was too exciting to pass on. Especially with the addition of Elevation Capital as an investor. Shinde said that was appealing because the firm was an investor in Paytm, and “knows how to partner and build unicorns.”

The new funding will be used to continue scaling and building the bookkeeping and accounting functions and to accelerate hiring, particularly in the engineering, sales and finance team verticals. Shinde expects to double or triple the finance team in the next year.

“As our customers scale through to their Series B, the more you can use our solution in real time to see what is happening with your finances, especially with startups and businesses having more of a remote workforce,” Swapnil Shinde added. “Zeni fits with that.”

Ash Lilani, managing partner at Saama Capital, one of Zeni’s earliest and largest investors, said he knew how big the total addressable market was — $200 billion — and how much these kinds of financial services were a giant pain point for startup companies.

“To know where you stand financially in real time is hard to do, usually, you get that information at month-end,” Lilani said. “I believe we have the opportunity to build a large company. Though Zeni is going after startups today, the small and medium markets can be leveraged. As they grow, Zeni will become their controller on the back end, while companies can just hire a CFO for the strategic decisions.”

Powered by WPeMatico