entrepreneurship

Auto Added by WPeMatico

Auto Added by WPeMatico

The world has spent most of 2020 adapting to ever-changing guidelines and restrictions (with no end in sight, even as the vaccines start to roll out). Board meetings are quickly increasing in their significance to foster consistent and vital interactions as an organization. It’s essential for companies to capitalize on the essential time together during these uncertain times.

While we might look like the Brady Bunch while sharing a Zoom window, are you actually communicating more like the family from “Succession?”

Are your meetings organized? Do people talk over one another? Do you usually run over time? Are you giving people time to digest information?

As we move into 2021 and Q1 meetings are being put onto calendars, take some time to modernize how you conduct your board meetings.

Board meetings are quickly increasing in their significance to foster consistent and vital interactions as an organization.

Having served on public company boards, growth-stage businesses and Series A startups, an observation I have made in boards that are later stage are more about financial analysis and governance. Whereas earlier-stage board discussions hinge more on product strategy, key partnerships, sharing best practices to help develop founders as executives and important hiring decisions.

Since the nature of the discussions is more, let’s call it … creative in earlier-stage businesses, where the focus is on where they’ve been particularly impacted by reduced bandwidth for collaboration while meeting remotely.

As said best by Mike Maples and paraphrased by Jeff Bonforte — there are only four things a board really needs to consider:

Collecting data around those points is the job. In the meeting, the team can add color.

Remember the board works for you, so be sure to put them to work. Sharing materials with participants about three days ahead of time tends to be the best. Any later and they may not get enough time to digest, send earlier and the information might be out of date by the time you meet. It’s most common to format as a deck, but lately I’m seeing more written format and even magazine-style.

The number one request I get from early-stage companies is “help find me more customers.”

Other common requests are “help me find or land this type of talent, help me with industry benchmarks for this type of business deal or compensation structure, connect me to people that have experience with X so I can learn ways we could structure our process.” It’s helpful to put these asks in the materials you send ahead because sometimes board members might not be able to react quickly and now “homework” comes up spontaneously in the discussions.

Another purpose of these meetings is to build working relationships so when strategic decisions need to be made, board members are used to working together. Sometimes it is a forum for executives to gain exposure to board members and for board members to have the opportunity to evaluate and provide input on executives. For that reason execs are often invited to participate in certain discussions.

Like the product person who presents a roadmap or a market analysis, the head of sales should give color on pipeline and competitive deals, the marketing person may lead a discussion on ABM or channel marketing tactics, the engineering lead might ask for feedback on their metrics versus other companies, etc. Generally, CEOs also bring forth an interesting topic to have a discussion, such as channel strategy, market mapping/sizing, hiring plan and related issues.

As far as logistics, we reserve two hours in calendars but we try to hit 90 minutes. I suggest something like this for a 90-minute session:

Powered by WPeMatico

Demetrius Curry has spent the last couple years chasing a dream.

His startup, College Cash, allows brands to petition users to create photo and video marketing content highlighting their product or service, with the wrinkle being that content creators are paid by the brands in the form of credits that go directly toward paying down their student loan debt. This model awards the brands involved a level of social good will and tax benefits.

The Dallas-area founder was inspired to tackle the student loan debt crisis after talking with his daughter about the prospect of eventually paying down her own loan debt. Curry has spent the past two years building out the nascent platform, tracking down brand partners, navigating accelerator programs, enticing users and pounding the pavement to find investors willing to bet on his vision.

College Cash has raised $105,000 to date, and is hoping to eventually wrap the funding into a $1 million seed round.

Filling out the round has been its own challenge for Curry, who has struggled at times to find opportunity, even among historic levels of capital flowing into the startup ecosystem, a distinction that has been less noticeable for black founders that still make up just a small percentage of VC allocation. In the aftermath of last summer’s protests against police brutality, a number of venture capital firms issued statements decrying institutional racism and pledging to back more underserved founders, spinning up new programs for diverse founders.

Demetrius Curry, CEO of College Cash

While Curry says he appreciates the scope of the problem and the good intentions of those making the statements, he believes that venture capital networks still have a lot to learn about what being an “underserved” founder means, and that plenty of the existing efforts feel like “lip service.” He says that even as Silicon Valley continues to idolize dropouts from prestigious universities, stakeholders have less interest in recognizing the accomplishments of founders who fought their way through poverty or found opportunity in geographies where opportunities are harder to come by.

“You can’t look for something different if you’re looking in the same places,” Curry tells TechCrunch. “When you look at the topic of ‘underserved founders,’ it’s not only a skin color thing, it’s also about where they came from and what they’ve been through.”

Curry says that it can be frustrating to compete for early-stage opportunities when investors aren’t willing to meaningfully adjust their parameters. Of particular frustration to Curry has been navigating the world of “warm introductions” to even get a foot in the door for programs meant for diverse founders, or applying for early-stage programs geared toward the “underserved” only to be told that they weren’t far enough along to qualify.

“Think about how much we had to go through to even get in the room with you,” Curry says. “I’ve sold plasma to pay a web hosting fee, nothing is going to stop me.”

College Cash’s mission of expanding opportunities for people struggling to manage their student loan debt is personal to Curry, who saw his life turn around after going back to school.

Decades ago, fresh out of the military, Curry said he had a random conversation with a stranger while eating at a Hardee’s — the discussion about what more he wanted from life ended up pushing him to to go back and get his GED and later a business degree. What followed was a career in finance that eventually led toward his recent entrepreneurial pursuits with College Cash.

The platform is firmly an early-stage venture at the moment, but Curry has big ambitions he’s building toward. His next effort is building out a College Cash tipping integration with gig economy platforms, with the aim that users of those platforms could ultimately opt to tip a worker and route that money directly toward paying down that person’s student loan debt.

Curry says the team at College Cash has been working with a “national gig economy platform” to run a pilot of the integration and has run focus groups showing that users are more likely to tip when they know that money goes toward erasing loan debt.

Powered by WPeMatico

Fundraising is challenging, especially for deep tech founders who need to get investors excited about a complex technology, a complex sales cycle and a complex risk profile.

As a former investor and current angel investor, I have met thousands of founders, many in the deep tech space.

Based on my experience, here’s how to avoid making the most common mistakes deep tech founders make when pitching investors:

Early-stage investors are in the business of funding dreams. They chose to be early-stage investors because they love hearing about new ideas and enthralling futures. They deliberately are not investment bankers or accountants because they do not want to constantly pour over endless spreadsheets or dive deep into financial models. Similarly, they are not operators because they do not want to spend time figuring out the intricacies of a supply chain or a marketing campaign or the configuration of a product component.

Make your pitch tailored to what excites venture capital investors and avoid what does not.

So make your pitch tailored to what excites venture capital investors and avoid what does not. Keep the financial model details and the warehouse system logistics information to your Appendix. You have it in case anyone wants to dive in deeper, but your core presentation should be focused on your biggest, most bullish hopes for the company seven to 10 years from now. Dedicate multiple slides to painting the picture of what society would look like should you meet all your intended milestones as a company.

As a deep tech company, your differentiation is in your intellectual property. However, investors care less about the “what” and much more about the “so what.” Investors are less interested in the intricacies of your technology and more interested in what impact it can create.

Formulate your slides to focus on answering questions like, “What can people or companies do as a result of your technology?” and “How will people save time, money and lives with your product?”

Put your presentation to the “grandma” test. Would your grandmother be able to understand and be excited about everything you share? Investor pitch meetings are not dissertation defenses. You are being evaluated on your potential for impact rather than the intricate details of your research. The best way to succeed in this evaluation framework is to ensure that everything you share is relevant and exciting to a diverse audience of even nontechnical folks.

Five million people are a statistic, but one person is a story. When people read data on massive populations of people, they conceptually understand the implications but only on a logical level, not an emotional one. When pitching, you want to reach the hearts of investors.

Powered by WPeMatico

The wave of venture capital interest in geographies other than Silicon Valley has been building momentum over the past 5+ years. If you measure capital flow by Twitter chatter alone, you may assume the tidal wave is about to break and checks are being doled out via T-shirt launchers repurposed from hockey games.

Meanwhile, VCs will approach founders saying, “We are now looking into markets beyond Silicon Valley.”

When Mucker launched back in 2011, our founding partners, who had left Silicon Valley for LA, set out to prove that high-growth companies can be built anywhere. Our portfolio from this past decade is a testament to this very narrative. With offices in LA, Austin and Nashville — and investments all over North America, we are seeing a marked increase in receptivity to an idea we had over a decade ago to invest across the U.S. and into Canada.

As of late, I’m receiving more and more outreach from VCs based in San Francisco, New York and beyond interested in deal flow here in Nashville and the Southeast.

When we think about the opportunity beyond Silicon Valley, we are really speaking of America.

In reality, there will be some lag time before the checks being written by these same VCs are consistent with both the outward hype and existing market opportunity. The broadened geographic focus of VCs for marketing purposes and FOMO is not adequately capturing the real narrative.

In short: When we think about the opportunity beyond Silicon Valley, we are really speaking of America.

“We” is a loaded declaration. I write this as a venture capitalist and also as the biracial daughter of a first-generation immigrant, with both of my parents growing up poor by most people’s standards. One branch of my family immigrated to the U.S. from Mexico during the Mexican Revolution, the other harkens back to rural Oklahoma. The founders I meet day in and day out in the Southeast oftentimes tell a similar story.

My story is that of the average American, and yet feels light years apart from what people perceive as the “innovation economy.” Many of the people I’ve met in venture capital this past decade come from prestigious lineages with parents and grandparents who may have never associated with mine. And yet, here we are. This is America.

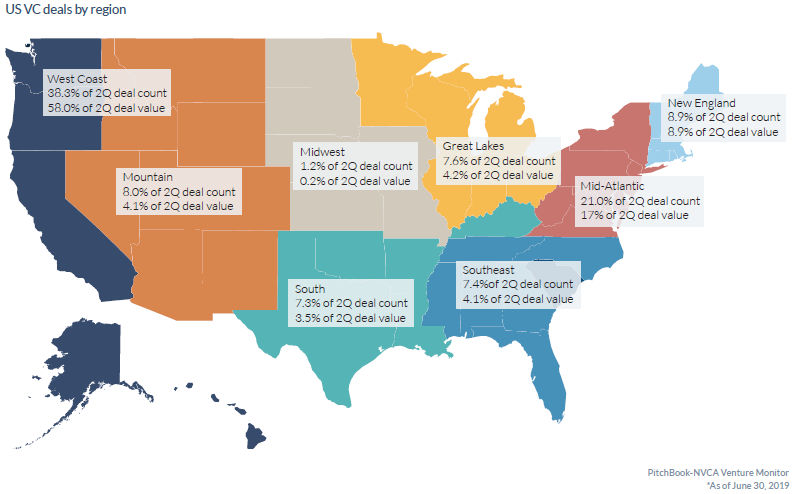

While Silicon Valley’s origins and climb to international stardom center around a collection of innovators, attracting more innovators and capital as the decades passed, one critical element arguably fell by the wayside — America as an expansive and diverse collection of states and people. Annual reporting on where venture capital dollars flow supports this discrepancy, with the majority of funds being funneled into companies based in and around Silicon Valley.

U.S. VC deals by region, as of June 2019. Image Credits: PitchBook/NVCA Venture Monitor

We find ourselves at the threshold of a decade where America will be rightfully recast as the land of opportunity for VC dollars to flow into the products and services fueling America’s future. And, at the helm of such innovations needs to be the people closest to these market opportunities, in full alignment with their customers and the nuances to best serve them.

In a post-COVID world, customers have never demanded more transparency into supply chains, workplace culture and equity ownership. Customers are more informed than ever before, with a 24/7 info line on brands and a growing scrutiny on where to place their hard-earned dollars. In short, they demand to be seen, and the founders who recognize this are the ones thriving in this new climate.

Where do the customers live? I’ll give you a hint: They are largely not in Silicon Valley.

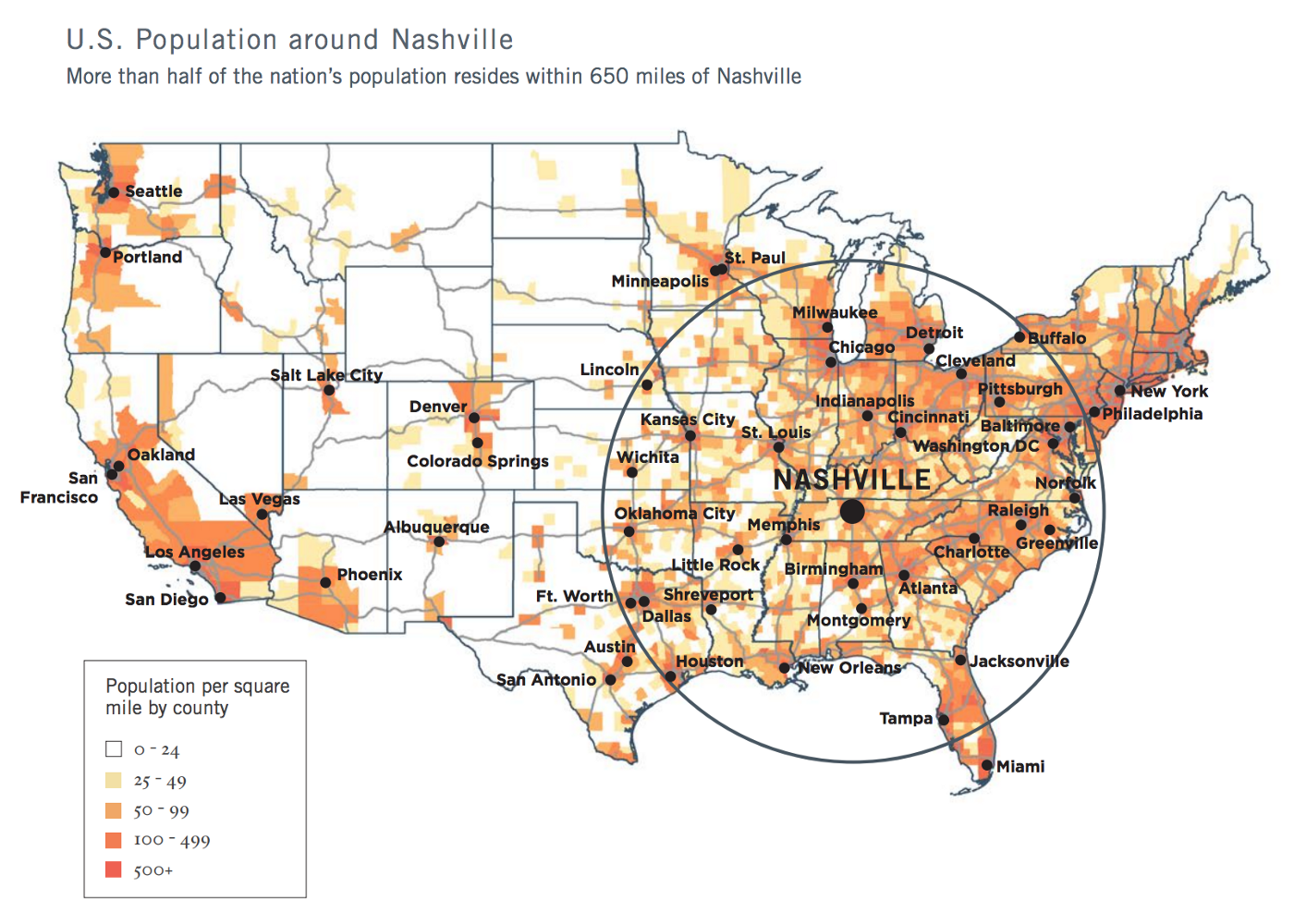

U.S. population around Nashville, TN. Image Credits: Nashville 2018 Regional Economic Development Guide

I wrote about the unfair advantage of Nashville back in 2018 when I announced the launch of Build In SE, a community I co-founded to support founders choosing to build their companies in the Southeast. Nashville is at the center of over half of the United States population within a radius of 650 miles, and within a two-hour flight of 75% of the U.S. market.

Customers come in all shapes and sizes, and founders with boots on the ground in these markets, wearing the same brand of proverbial boots as these customers, carry an unfair advantage. These same founders historically bootstrapped their companies out of need, as access to early-stage, high-risk capital can be scarce and vary widely city by city, state by state, industry by industry.

These same founders still built household name companies in the tech and innovation economy, including the likes of Mailchimp, Calendly, Lynda.com, and GoFundMe (their Series A valued them at $600 million pre-money). All of these companies have another thing in common — they were founded “beyond Silicon Valley.”

Another macrotrend at play is that of the increasing distribution of talent beyond traditional metropolitan strongholds like San Francisco and New York. Entrepreneurs, technologists and operational talent are lifestyle-seeking at a time in history when life feels all the more precious. Moving to cities like Nashville, Austin, Atlanta, Denver, Durham, Miami, et. al. means proximity to aging family members, affordable childcare and outdoor activities.

These simple pleasures were the tradeoffs people made when “pursuing their dreams” in coastal cities, picking up to move in pursuit of money (sometimes better weather). Seemingly overnight, capital abounds in the private markets just as talent becomes increasingly scarce and therefore valuable. The pendulum swung, and capital became the weaker of the two magnets; Wall Street began moving up Manhattan island toward coffee shops and dog parks when talent began to pose the question, “How long do I want my commute to be?” and “How much time do I want to reclaim for my family, and myself?”

2020 was the match to ignite this dry hillside. People trapped inside of cramped quarters with resources left to invest in a new life (or in other cases, left with nothing to lose) packed their bags for a new, up-and-coming metro.

For some, this comes with a newfound sense of community and belonging, as I experienced in 2017 when I moved from my lifelong home of Los Angeles to Nashville. In LA, my local neighborhood hardly knew one another due to the transient nature of the town. In Nashville, I became part of something greater than myself.

One of the big frustrations expressed by founders I know in markets like Nashville, Atlanta, the Research Triangle, Cincinnati and Toronto, is, “I keep hearing there is more capital available, but I’m not seeing it.” They will meet with investors, then be told they are too early, raising too little money, or too much, or not going after a “big enough market.”

Sometimes, one or more of these may be true. However, there are instances where these investor responses may be thinly veiled criticism of the perceived ability of the founders who might not sound, look or behave like Silicon Valley entrepreneurs.

Closing this gap of understanding between pattern-matching VCs of varying skill and startup CEOs across the country will require hard work in the coming decade. A big piece of this will require breaking bread as neighbors, with kids in the same schools, a shared affinity for the local greasy spoon and a mutual trust. This will be step one. Though really, it will require much more alignment and rigor around the very definition of America.

It is up to investors to capture this opportunity in the next decade. In fact, it is our job.

Powered by WPeMatico

Edtech is so widespread, we already need more consumer-friendly nomenclature to describe the products, services and tools it encompasses.

I know someone who reads stories to their grandchildren on two continents via Zoom each weekend. Is that “edtech?”

Similarly, many Netflix subscribers sought out online chess instructors after watching “The Queen’s Gambit,” but I doubt if they all ran searches for “remote learning” first.

Edtech needs to reach beyond underfunded public school systems to become more sustainable, which is why more investors and founders are focusing on lifelong learning.

Besides serving traditional students with field trips and art classes, a maturing sector is now branching out to offer software tutors, cooking classes and singing lessons.

For our latest investor survey, Natasha Mascarenhas polled 13 edtech VCs to learn more about how “employer-led up-skilling and a renewed interest in self-improvement” is expanding the sector’s TAM.

Here’s who she spoke to:

Full Extra Crunch articles are only available to members

Use discount code ECFriday to save 20% off a one- or two-year subscription

In other news: Extra Crunch Live, a series of interviews with leading investors and entrepreneurs, returns next month with a full slate of guests. This year, we’re adding a new feature: Our guests will analyze pitch decks submitted by members of the audience to identify their strengths and weaknesses.

If you’d like an expert eye on your deck, please sign up for Extra Crunch and join the conversation.

Thanks very much for reading! I hope you have a fantastic weekend — we’ve all earned it.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Bryce Durbin

Image Credits: Nigel Sussman (opens in a new window)

After falling into yesterday’s wild news cycle, Alex Wilhelm returned to The Exchange this morning with a close look at venture capital activity across Africa in 2020.

“Comparing aggregate 2020 figures to 2019 results, it appears that last year was a somewhat robust year for African startups, albeit one with fewer large rounds,” he found.

For more context, he interviewed Dario Giuliani, the director of research firm Briter Bridges, which focuses on emerging markets in Africa, Asia and Latin America.

Image Credits: MCCAIG (opens in a new window) / Getty Images

New cybersecurity ecosystems are popping up in different parts of the world.

Some of of that growth has been fueled by an exodus from the Bay Area, but many early-stage security startups already have deep roots in East Coast cities like Boston and New York.

In the United Kingdom and Europe, government innovation programs have helped entrepreneurs close higher numbers of Series A and B rounds.

Investor interest and expertise is migrating out of Silicon Valley: This post will help you understand where it’s going.

Image Credits: NurPhoto (opens in a new window) / Getty Images

Today’s smartphones are unfathomably feature-rich and durable, so it’s logical that sales have slowed.

A phone purchased 18 months ago is probably “good enough” for many consumers, especially in times of economic uncertainty.

Then again, of the record $111.4 billion in revenue Apple earned last quarter, $65.68 billion came from phone sales, largely driven by the release of the iPhone 12.

Even though “Apple’s success this quarter was kind of a perfect storm,” writes Hardware Editor Brian Heater, “it’s safe to project a rebound for the industry at large in 2021.”

Image Credits: Randy Faris (opens in a new window) / Getty Images

Finmark co-founder and CEO Rami Essaid wrote a post for Extra Crunch that candidly describes the traps he laid for himself that made him a less-effective entrepreneur.

As someone who’s worked closely with founders at several startups, each of the points he raised resonated deeply with me.

In my experience, many founders have a hard time delegating, which can quickly create cultural and operational problems. Rami’s experience bears this out:

“I became a human GPS: People could follow my directions, but they struggled to find the way themselves. Independent thinking suffered.”

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie:

I just got my U.S. citizenship! My husband and I want to bring my mom and her husband to the U.S. to help us take care of our preschooler and toddler.

My biological dad passed away several years ago when I was an adult and my mom has since remarried.

— Appreciative in Aptos

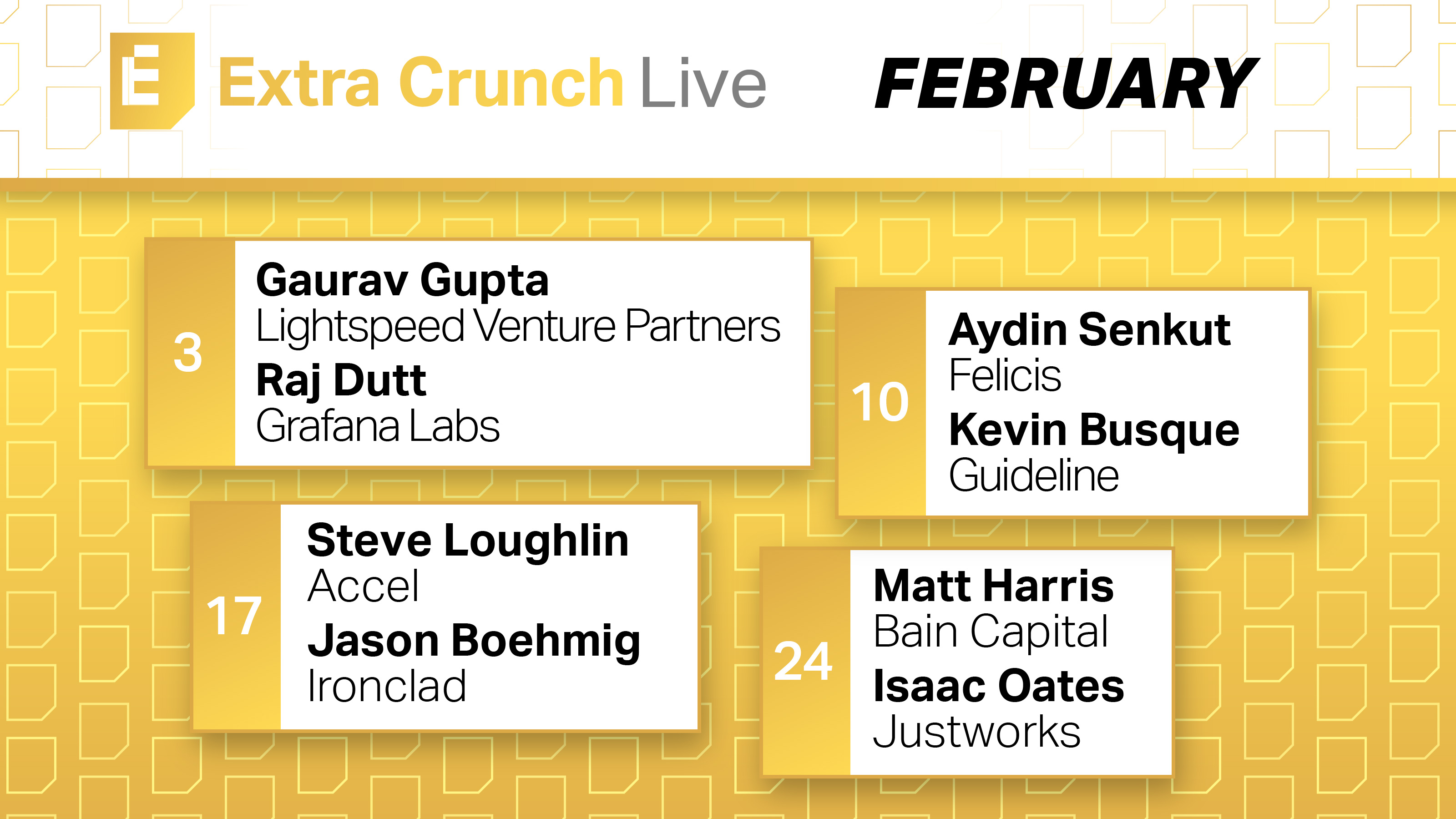

Next month, Extra Crunch Live returns with a lineup of guests who are extremely well-qualified to discuss early-stage startups.

Each Wednesday at noon PPST/3 p.m. EST, join a conversation with founders and the investors who backed their companies:

February 3:

Gaurav Gupta (Lightspeed Venture Partners) + Raj Dutt (Grafana Labs)

February 10:

Aydin Senkut (Felicis Ventures) + Kevin Busque (Guideline)

February 17:

Steve Loughlin (Accel) + Jason Boehmig (Ironclad)

February 24:

Matt Harris (Bain Capital) + Isaac Oates (Justworks)

Also, we’re adding a new feature to Extra Crunch Live — our guests will offer advice and feedback on pitch decks submitted by Extra Crunch members in the audience!

Image Credits: Aleksandar Nakic (opens in a new window) / Getty Images

Since the pandemic disrupted the social rhythms of work and school, many of us have compensated by changing our relationship to digital media.

For instance, I purchased a new sofa and thicker living room curtains several months ago when I realized we have no idea when movie theaters will reopen.

Last year, podcast sponsors spent almost $800 million to reach listeners, but ad revenue is estimated to surpass $1 billion this year. Clearly, I’m not the only person who used a discount code to buy a new product in 2020.

At this point, I can scarcely keep track of the multiple streaming platforms I’m subscribed to, but a new voice-activated remote control that comes with my basic cable plan makes it easier to browse my options.

Media reporter Anthony Ha spoke to10 VCs who invest in media startups to learn more about where they see digital media heading in the months ahead. For starters, how much longer can we expect traditional advertising models to persist?

And in a world with hundreds of channels, how are creators supposed to compete for our attention? What sort of discovery tools can we expect to help us navigate between a police procedural set in a Scandinavian village and a 90s sitcom reboot?

Here’s who Anthony interviewed:

Normally, we list each investor’s responses separately, but for this survey, we grouped their responses by question. Some readers say they use our surveys to study up on an individual VC before pitching them, so let us know which format you prefer.

Image Credits: Nigel Sussman (opens in a new window)

Data analytics platform Databricks is reportedly raising new capital that could value the company between $27 billion and $29 billion.

By the end of Q3 2020, Databricks had surpassed a $350 million run rate — a $150 million YoY increase, reports Alex Wilhelm.

At the time, he described the company as “an obvious IPO candidate” with “broad private-market options.”

Which begs the question: “Can we come up with a set of numbers that help make sense of Databricks at $27 billion?”

Image Credits: Natalia Timchenko (opens in a new window) / Getty Images

Rapid shifts in the way we buy goods and services disrupted old-school marketplaces like local newspapers and the Yellow Pages.

Today, I can use my phone to summon a plumber, a week’s worth of groceries or a ride to a doctor’s office.

End-to-end operators like Netflix, Peloton and Lemonade take a lot of time and energy to reach scale, but “the additional capital required is often outweighed by the value captured from owning the entire experience.”

Image Credits: Nigel Sussman (opens in a new window)

On January 25, Social Capital CEO Chamath Palihapitiya tweeted that he was making two blank-check deals.

Enterprise SaaS company Latch makes keyless entry systems; Sunlight Financial helps consumers finance residential solar power installations.

“There are nearly 300 SPACs in the market today looking for deals,” noted Alex Wilhelm, who unpacked both transactions.

“There’s no escaping SPACs for a bit, so if you are tired of watching blind pools rip private companies into the public markets, you are not going to have a very good next few months.”

Image Credits: dan tarradellas (opens in a new window) / Getty Images

On Monday, we published the Matrix Fintech Index, a three-part study that weighs liquidity, public markets and e-commerce trends to create a snapshot of an industry in perpetual flux.

For four years running, the S&P 500 and incumbent financial services companies have been outperformed by companies like Afterpay, Square and Bill.com.

In light of steady VC investment, increasing consumer adoption and a crowded IPO pipeline, “fintech represents one of the most exciting major innovation cycles of this decade.”

Image Credits: Acquia

On January 15, 2001, then-college student Dries Buytaert released Drupal 1.0.0, an open-source content-management platform. At the time, about 7% of the world’s population was online.

After raising more than $180 million, Buytaert exited to Vista Equity Partners for $1 billion in 2019.

Enterprise reporter Ron Miller interviewed Buytaert to learn more about his 18-year journey.

“His story is compelling, but it also offers lessons for startup founders who also want to build something big,” says Ron.

Powered by WPeMatico

June 4, 2019 should have been one of the happiest days of my life.

At 11:30 a.m., a press release hit the wire announcing that the cybersecurity company I had spent more than eight years building was being acquired by a larger cybersecurity player.

What’s not to love about a successful exit? I’d be set financially, the investors who had given us $70 million would make money, and the technology we created would get new legs in an organization with broader reach and resources.

Still, I had regrets. For one thing, I initially hadn’t wanted to sell. (More on that later.) For another, I was nagged by the feeling that our company had fallen short of its true potential, and that the reason was me — specifically, several rookie mistakes I made as a first-time entrepreneur.

I don’t stew about those errors any longer. In fact, I believe my miscues at my first startup will help define my career from here on out. That’s why, as I grow my next company, I’m thinking about not only the things I want to do but those I’d never do again.

Here are five of them.

In management theory terms, I was a “pacesetter.” I’d be the first to jump into any project or task, I’d execute it as quickly as possible and I expected everyone else to keep up. I thought that was how a startup leader acted — super helpful and scrappy.

But it came at a big price: disempowerment of the team. I was hoarding not only control — nobody felt like they personally owned anything — but also the institutional knowledge that needs to be spread around as a company grows. I became a human GPS: People could follow my directions, but they struggled to find the way themselves. Independent thinking suffered.

I became a human GPS: People could follow my directions, but they struggled to find the way themselves. Independent thinking suffered.

After a few years, I had a frustrating sense that I had all the answers and no one else did. Well, no wonder.

I’m now leaving the pacesetting to NASCAR and marathons.

I believed all I had to do was say something once and everyone would get it. I became irritated when that didn’t happen. “We talked about this three months ago,” I’d bark. Intimidated team members would say to themselves, “Yeah, but we really only got 50% of it.”

Powered by WPeMatico

Previously, we introduced the concept of flexible VC: structures that allow founders to access immediate risk capital while preserving exit and ownership optionality. We list here all the active flexible VCs we have identified, broken into these categories:

These investors are paid back primarily based on a percentage of revenues.

Chattanooga, TN-based Capacity Capital was launched in 2020 with a primary focus on the southeastern U.S. Jonathan Bragdon, its CEO, describes Capacity as “a team of founders-turned-funders making non-dilutive, founder-aligned investments of $50,000-$300,000 in post-startup, post-revenue businesses planning to 2x revenues in 12-24 months. Investments are typically in exchange for a capped, single-digit revenue share and a right to equity under certain circumstances.

If the company sells or raises enough capital, the investment converts into an agreed-upon percentage of equity. If the company grows without raising additional equity funding, founders redeem most of the equity right, based on a pre-agreed return amount. With a portfolio that includes food, tech and services, the fund is industry-agnostic and focused on the overlooked and underrepresented with high-margin business models.”

Jonathan sometimes refers to their investments as “micro-mezzanine” because “mezz is typically structured as a contractual periodic payment, with some equity-like upside, but subordinate to other debt … so most lenders look at it like equity. But, it is typically shorter term with fewer control mechanisms than equity (i.e., not VC). I wanted [a term for] something similar (between debt and equity) but on an extremely small scale.”

In addition to a fund, the overall Capacity organization provides direct mentorship, consulting and connects founders to a broad network of talent, diverse forms of capital and existing resources focused on the post-startup stage of growth. The founders, LPs and venture partners have a long history in local startup ecosystems in the Southeast including LaunchTN, The Company Lab, CO.STARTERS and several other regional funds and resources.

Greater Colorado Venture Fund (GCVF) is a $17 million seed fund that invests in high-growth startups in rural Colorado using equity and flexible VC structuring.

A typical GCVF flexible VC investment is $100,000-$250,000 for up to 10% ownership, of which 9% is redeemable, with a sub-10% revenue share and 12-month-plus holiday period. GCVF specializes in providing critical support to founders based in small communities, while connecting them to an unfair network well-beyond their small-town headquarters.

GCVF is pioneering the future of venture capital and high-growth startups for all small communities. With Colorado as an ideal pilot community, the GCVF team (which includes Jamie Finney, a co-author of this article) has helped grow multiple staple initiatives in the rural Colorado startup ecosystem, including West Slope Startup Week, Telluride Venture Accelerator, Startup Colorado, Energize Colorado Gap Fund and the Greater Colorado Pitch Series.

Recognizing the need for creative investment structures in their Colorado market, they co-founded the Alternative Capital Summit, creating the first community of flexible VCs and alternative startup investors.

They share their learnings on flexible VC and pioneering rural startup ecosystems on the GCVF blog.

Powered by WPeMatico

Of the Inc. 5000 companies, only 6.5% raised money from VCs and 7.7% raised from angels. Where else can fast-growing companies get funding?

More and more startups are pursuing revenue-based VCs, but it’s not a good fit for everyone. A new category of investors has emerged offering a hybrid between VC and revenue-based investment (RBI), which we call “flexible VC.”

From RBI, flexible VCs borrow the ability to reap meaningful returns without demanding founders build for an exit. From traditional equity VC, flexible VC borrows the option to pursue and reap the rewards of an outsized exit. Every flexible VC structure allows founders to access immediate risk capital while preserving exit, growth trajectory and ownership optionality.

Before raising capital, we encourage founders to dig into the nuances between different flexible VC structures.

Our categorization is not a technical one. Rather, we want to accommodate the wide variety of instruments currently offered by flexible VC investors, detailed below. As two fund managers employing flexible VC, we think it is a healthy addition to the ecosystem and will yield more predictable and stable healthy returns for investors.

This is currently the most common investment structure: The flexible VC investor purchases either equity ownership, or a convertible right to equity, and a right to regularly scheduled payments based on a percentage of revenues.

By tying payments to actual revenues, founders and investors remain aligned around the company’s real-time performance, good or bad.

“Too often, investment structures force the management team to make decisions between misaligned growth and investment (return) objectives. This structure allows for alignment on the front end, and real-time flexibility for performance metrics,” says Samira Salman, a family office investor and advisor.

Payments are commonly delayed for a grace period of 12-36 months. John Berger, director of Operations and Impact Solutions at Toniic, observed that this has clear investor benefits: “The grace period became a feature because it benefits investors in regions like the U.S. where there can be tax differences between short- and long-term gains. It has moved from its origins as a tax benefit and can be viewed as a feature that benefits founders.” After the grace period, the return payments begin, often lasting until a return cap is hit, such as 2-5 times the original investment.

To account for these revenue share payments, the investor’s ownership (or convertible right to ownership) is simultaneously reduced. Once the return cap is reached, the investor is typically left with a residual stake — a fraction of the pre-revenue share ownership. At any point, should the founder wish to pursue a traditional equity VC round, or get bought, the revenue share is paused, and the investor’s then-current ownership converts to equate to a traditional equity VC investor.

Flexible VCs have created structures based on other company performance metrics than revenues, such as profits or founder salaries. These different company performance metrics provide a slight variation in how the investor and founder relationship is defined. For example, profit-sharing structures ensure payments do not begin until the company is profitable, though likely delaying returns to the investor and complicating payment calculations.

Similarly, when flexible VC structures are based off of the founder’s own compensation (often via salary or dividends), investors are specifically tying their returns to the financial success of the founder. This translates less directly to company performance compared to a revenue or profit share, but offers uniquely personal alignment. These variations in founder alignment allow flexible VCs to specialize in the types of companies they work with.

In all these cases, capital is provided to fuel forecasted growth without creating a commitment to a particular vision for future funding rounds, exit goals and associated blitzscaling. The founder retains full control over whether they want to optimize for hypergrowth (usually at the expense of profitability) or for organic, profitable growth. Flexible VC opens up a new risk capital option for bootstrappers, minorities, family-owned and countless other founder segments left out by the traditional funding landscape.

A range of small VCs are deploying with flexible VC structures, but we believe the total amount of AUM deployed with this strategy is well under $50 million. Similar to the explosion of seed funds in the past decade, we (and some limited partners too) believe these Flexible VCs are on the forefront of what will become a major segment of the venture ecosystem.

We detail below the major categories of VC:

| Funder category | Equity ownership | Returns primarily based on | Composition of returns | Example VC |

| Equity VC | Yes, typically preferred equity.

15%-20% sold per round. On average, founders own just 43% of equity by Series B, declining thereafter. |

The value ascribed by subsequent investors (in a secondary); buyers (acquisition); or the public markets (IPO). | Volatile, uncapped. | Andressen Horowitz, ff Venture Capital, HOF Capital, Sequoia. |

| Flexible VC: Revenue-based | Yes, nonvoting common shares (if converted).

5%-20% initial stake, with 50%-90% of this redeemable. |

Gross revenues (generally 2%-8%). | 2x-5x return cap + path to uncapped equity returns. | Capacity Capital, Greater Colorado Venture Fund, Indie.VC, Reformation Partners, UP Fund, Versatile VC. |

| Flexible VC: Compensation-based | Yes, via conversion rights at a valuation cap. | “Founder earnings” (Founder salaries + dividends + retained earnings). | 2x-5x return cap + path to uncapped equity returns. | Chisos. |

| Flexible VC: Blended Return | Yes, via conversion rights at a valuation cap. | Profits, founder salaries, and/or dividends declared. | Typically ~3x+ return cap + path to uncapped equity returns. Discretionary dividends and salary share built in. | Collab Capital, Earnest Capital, TinySeed. |

| Revenue-share investing | No. | Gross revenues (generally 2%-8%). | 1.35x-2.2x return cap. | Novel Growth Partners, Lighter Capital, Rev Up, Corl. |

Flexible VC investors offer founders some of the same advantages as equity VCs:

Flexible VCs also offer investors some of the same advantages as RBI:

Flexible VC also offers some unique advantages:

That said, nothing is cost-free. The unique disadvantages of flexible VC include:

Powered by WPeMatico

In 2020, venture capitalists unceremoniously broke up with D2C brands and product-based businesses.

Many watched as the consumer brands in their portfolios rushed to make hefty layoffs and eke out more runway and grew more concerned with their business models.

Some simply monitored the “lackluster” Casper IPO or skimmed articles about Brandless and others “imploding” and started pulling a slow fade on D2C brands — not taking pitches, not following up.

Many product-based brands, as it turns out, are no longer interested in chasing venture capital.

Last year, investors adopted a wait-and-see approach to all new investments and prayed portfolio brands could cut their burn significantly enough, stay relevant and ride things out.

Product-based businesses fell out of favor and venture capitalists, if they did invest last year, mainly focused on AI startups, or companies focused on data collaboration, data privacy and healthcare (mostly founded by men, might I add).

From a distance, it sounds like direct-to-consumer founders were left destitute and desperate for financing, wounded by every slow fade or hard pass, beholden as ever to the whims of Silicon Valley.

But as Hal Koss so eloquently shared in his “DTC playbook” post-mortem, this wasn’t a one-way breakup; this parting of ways is actually mutual. Many product-based brands, as it turns out, are no longer interested in chasing venture capital, playing the “grow-at-all-costs” game and relinquishing partial control to investors, despite the pandemic and the uncertain circumstances many founders find themselves facing.

Through my work running and scaling Bulletin, I’ve followed thousands of product-based businesses ranging from indie beauty brands selling clean serums and cleansers to sex tech companies making couples’ vibrators and foreplay accessories. I’ve followed them on Instagram, in the press and across various platforms, and in many cases, I’ve spoken to their founders directly.

Over the past two years, I interviewed executives at more than 30 women-owned businesses for my upcoming book, “How to Build a Goddamn Empire,” and had long phone calls with dozens of independent brands and makers as Bulletin got a handle on how the pandemic was impacting customers. And I noticed something new and remarkable about what founders want now, in 2021, compared to what they wanted in years past.

Back then, I’d get dozens of cold emails and DMs asking how I successfully raised VC and what the unspoken rules might be. I’d hear from business owners who were considering a raise or gearing up for one. Product-based entrepreneurs approached me at panels or Bulletin events and say they wanted to be the “Glossier for X” or the “Away for Y.” Many younger founders didn’t even know what venture capital really was, but they saw it as symbolic validation for the business, or the only way to get “big.”

Now, brands would rather scrape by than pursue an injection of funding on someone else’s terms; just ask the Gorjana founders or Scott Sternberg. Many brands that saw astronomical growth in 2020, like Rosen, Golde, Entireworld and others that spurred similar growth for Etsy and Shopify are fully bootstrapped businesses, and proudly so.

Some founders I’ve spoken to have even outright rejected offers for investment. A lot of D2C brands are interested in learning about alternative forms of financing like bank loans, lines of credit and crowdfunding, and ask about iFundWomen or Kickstarter, observing the success of other fully crowdfunded brands like Dame and Pepper.

Venture capital, from my vantage point, has lost its sheen for a lot of product-based brands. They’re not destitute and desperate for financing. They’re actually scoffing at the prospect and trusting they can succeed, scale and maintain long-term profitability without swapping equity for cash. They’re tripped up by what they’ve been reading in the media, or they’ve survived or even thrived during COVID, as a fully bootstrapped company, and feel more conviction than ever that the “grow slow” approach is the right move.

They’re reading the same stories about layoffs and tenuous unit economics at massive D2C companies and agreeing with Sam Kaplan that the old playbook — pricey customer acquisition practices, rapid scale, endless rounds of funding — is out of date. It’s 2021 and we’re midpandemic. These brands want to turn a profit.

Powered by WPeMatico

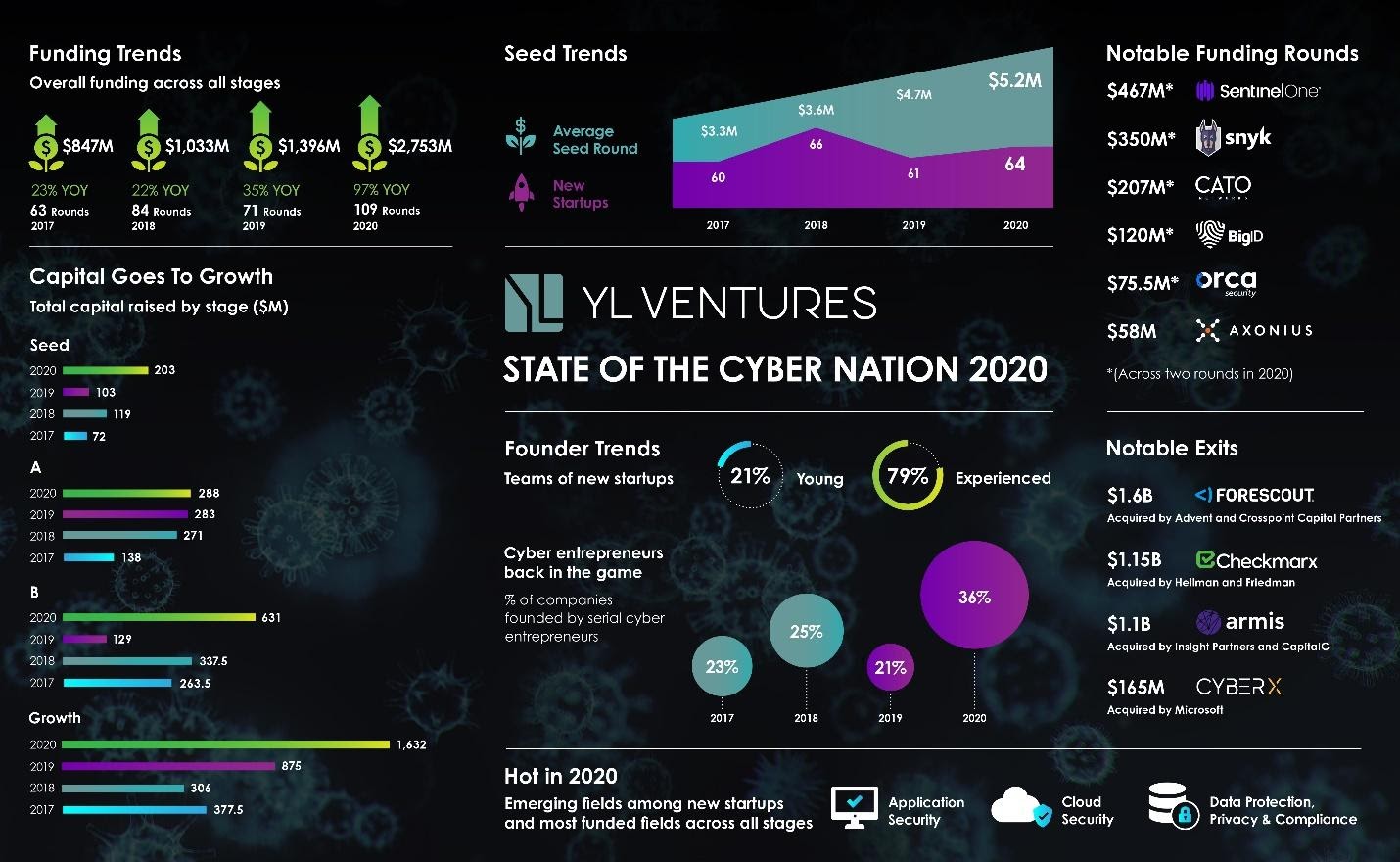

From COVID-19’s curve to election polls, public temperature checks to stimulus checks, 2020 was dominated by numbers — the guiding compass of any self-respecting venture capital investor.

As a VC exclusively focused on investments in Israeli cybersecurity, the numbers that guide us have become some of the most interesting to watch over the course of the past year.

The start of a new year presents the perfect opportunity to reflect on the annual performance of Israel’s cybersecurity ecosystem and prepare for what the next twelve months of innovation will bring. With the global cybersecurity market outperforming this year’s panic-stricken expectations, we carefully combed through the figures to see how Israel’s market, its strongest performer, compared — and predict what it has in store.

The cybersecurity market continues to draw the confidence of investors, who appear to recognize its heightened importance during times of crisis.

The “cyber nation” not only remained strong throughout the pandemic, but even saw a rise in fundraising, especially around application and cloud security, following the emergence of remote workflow security gaps brought on by social distancing. Encouraged by this, investors have demonstrated committed enthusiasm to its growth and M&A landscape.

Emboldened by the sector’s overall strength and new opportunities, today’s Israeli visionaries are developing stronger convictions to build larger companies; many of them, already successful entrepreneurs, are making their own bets in the industry as serial entrepreneurs and angel investors.

Image Credits: YL Ventures (opens in a new window)

The numbers also reveal how investors are increasingly concentrating their funds on larger seed rounds for serial entrepreneurs and the foremost industry trends. More than $2.75 billion was poured into the industry this year to back companies across all stages, a 97% increase from last year’s $1.39 billion. If its long-term slope is any indication, we can only expect it to continue to grow.

However, though they clearly indicate progress, the numbers still make the need for a demographic reset clear. Like the rest of the industry, Israel’s cybersecurity ecosystem must adapt to the pace of change set out by this year’s social movements, and the time has long passed for true diversity and gender representation in cybersecurity leadership.

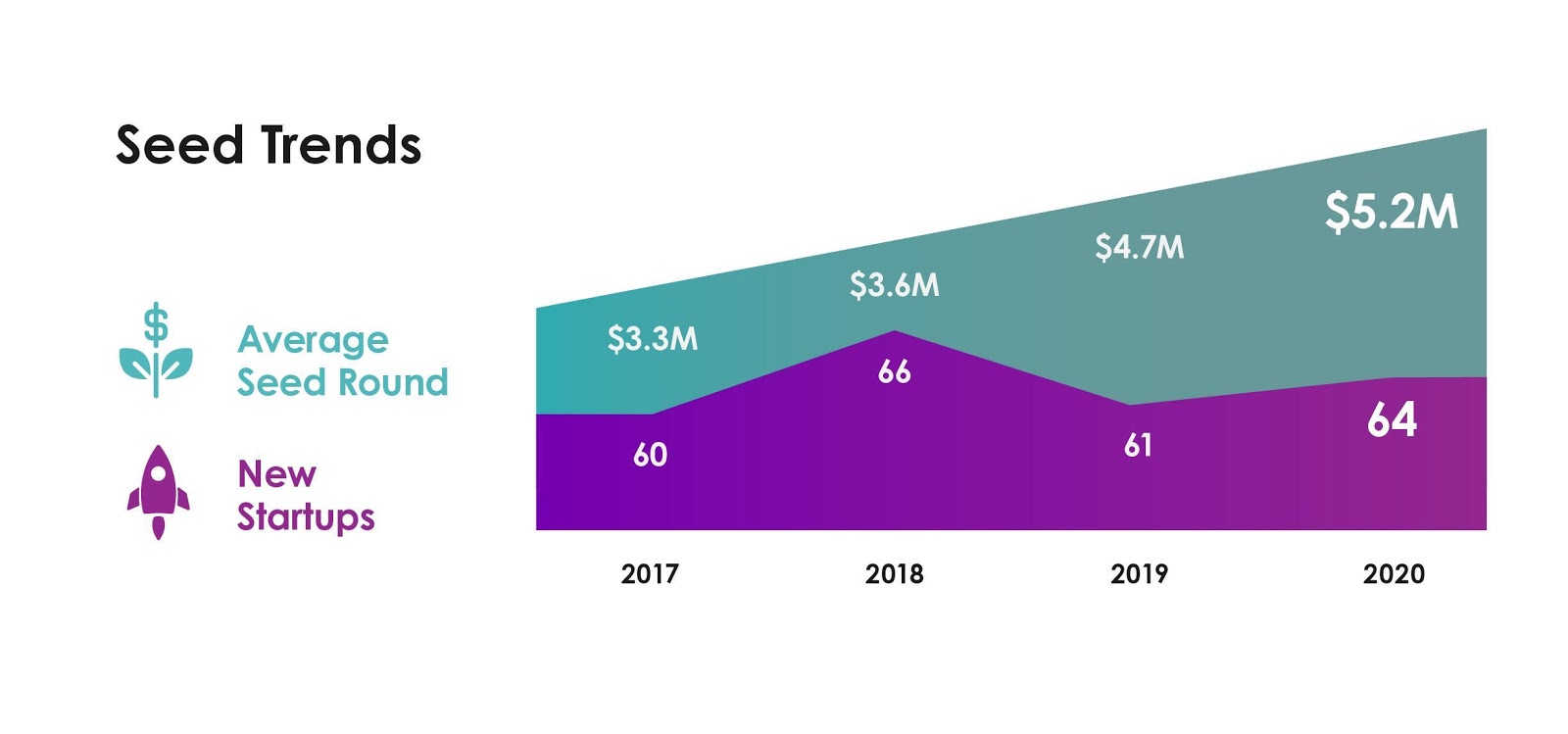

As the market’s biggest leaders garner experience and expertise, the bar for entry to Israel’s cybersecurity startup ecosystem has gradually risen over the years. However, this did not appear to impact this year’s entrepreneurial breakthroughs. 58% of Israel’s newly founded cybersecurity companies received seed rounds this year, totaling 64 seeded companies in 2020 compared with last year’s 61. The total number of newly founded companies increased by 5%, reversing last year’s downward trend.

The amount invested at seed hit an all-time high as average deal size in 2020 increased by 11%, amounting to an average of $5.2 million per deal. This continues an upward trend in average seed rounds, which have surged over the last four years due to sizable year-on-year increases. It also provides further support for a shift toward higher caliber seed rounds with a strategically focused and “all-in” approach. In other words, founders that meet the new bar for entry are raising bigger rounds for more ambitious visions.

Image Credits: YL Ventures

2020 proved an exceptional year for application security and cloud security startups. Perhaps the runaway successes of Snyk and Checkmarx left strong impressions. This year saw an explosive 140% increase in application security company seed investments (such as Enso Security, build.security and CloudEssence), as well as a whopping 200% increase in cloud security seed investments (like Solvo and DoControl), from last year.

Powered by WPeMatico