entrepreneurship

Auto Added by WPeMatico

Auto Added by WPeMatico

The business world has a love-hate relationship with coaching. Founders are visionaries: They start with an idea, a talent, a dream, but not necessarily the business know-how. Because being an entrepreneur doesn’t require a license or training — Jeff Bezos is an engineer and computer scientist; Elon Musk is an economist and physicist, and so on.

In any other industry, when someone with raw talent — an athlete, a singer, an actor — furthers their career, the first thing they receive is a coach. And it doesn’t stop once they get their first Olympic gold or Grammy.

Coaches don’t leave their side until they hang up their gloves. Tiger Woods is famous for having worked with many coaches to switch up his tactics and keep exceeding in his performance.

In any other industry, when someone with raw talent — an athlete, a singer, an actor — furthers their career, the first thing they receive is a coach.

Despite a culture that pushes founders to the edge of their physical, mental and personal limits as they build their company, we insist that they fly solo. They’re led to believe that reaching out for support is a sign of weakness.

That stigma is a huge part of the problem. We look up to business magnates, believing that they sailed from a college dorm to the C-suite without breaking a sweat. But we don’t see the vigorous kicking that goes on beneath the surface. As a client of mine once mused, even the best leaders are self-sabotaging themselves at least 30% of the time. I know for a fact that top Silicon Valley billionaires have nutrition, parenting, meditation and life coaches, but they — like half of my own clients — are reluctant to embrace this out in the open.

VCs know that they don’t invest in the business; they invest in the person. Record amounts of money are being funneled into mental wellness startups right now, but investors also need to direct that awareness toward their founders’ well-being. By offering access to a coach to all your portfolio founders, you’ll be tackling the real problems stopping them from pouring their energy into their business, and you’ll without a doubt improve your returns.

I coach founders and CEOs of startups, and more than half their main life challenges are not work related. They’re getting pulled in multiple directions — some have cancer, others are having an affair, a few are going through IVF, others still are dealing with past grief and traumas.

And when a problem is work related, it’s often a communication or psychological issue: How do I face my fear of failure? How do I lead a team of 50 for the first time? Should I trust my gut?

All this is happening in the midst of Series A raises, hiring and firing employees, acquisitions, and deciding whether to bridge or shut down the business. Imagine how much emotional energy and hours it takes for founders — or anyone, really — to face those intimate issues in isolation while putting on a brave face with investors or at board meetings.

One of the most recurring concerns founders share with me is that they feel alone.

VCs, when you choose to fund someone, you’re also marrying into their past, their family, their personal issues. The full package. Ask yourself — do you currently know the major distractions in the lives of all your portfolio founders? If you don’t, start with the assumption that something is going on in their life other than work and make coaching available to them at any time.

If you commit to helping founders manage their fears, limiting beliefs and blind spots, you’re committing to their potential as a company and industry leader. A healthy leadership is a healthy company.

As with elite soccer coaches, the benefits of business coaching are highly visible, without the million-dollar expense. Founders start to make better decisions the first time around. They hire the right talent, rather than hiring, onboarding and firing someone within a month.

They have more honest conversations with stakeholders, avoiding conflict and allowing more people to contribute meaningfully to the business’ growth. They have the proper mindset to fundraise, and their attitude matches the money they’re asking for.

That’s before getting to the physical improvements. My founders have lost weight, stopped smoking and drinking, and have more energy to build a business. If a founder works with chronic fatigue, which many are, it won’t be long before their body cracks. I get calls from clients caught in panic attacks before big meetings, struggling to steady their frayed nerves.

You can fund your founders’ well-being in a variety of ways. In the same way your firm might offer marketing or PR services to portfolio companies, coaching should be part of the package. Firms can make executive coaches available on retainer. You may choose to have a full-time resident coach, available whenever someone needs them.

At the very least, firms should make available a list of recommended coaches. Some coaches specialize in leadership coaching, female founders or health specifically, while others cover various personal and professional skills.

Investors will sometimes offer a handful of free sessions to their founders, but if they want to continue, they are then forced to decide between their personal health and the health of the business — which other people (including your firm) have staked millions of dollars on. It should never be a case of one or the other.

My hope is that in the future, VCs will set aside a percentage of their funds exclusively for mental wellness for founders and executives.

A few VCs have already taken a 1% pledge, but it’s the Europeans who are leading the charge here, with funds from Estonia to Ireland generously covering all founder coaching fees and other support programs. Those I know talk about how 10x growth is possible without burnout.

Founders are resistant to hiring a coach themselves because they’re worried about what their investors and board will think of them. They tell themselves: “If I were normal, and good enough, I wouldn’t need one.”

It’s not just their inner voice talking. When a client of mine joined a Silicon Valley startup, he asked his superiors if coaching could be part of his comp package. They wondered why he needed a coach.

In other industries, connecting someone with a coach is proof of their worth. That’s the conversation investors should be having: You’re good enough for us to give you money, so we’re going to give you someone to accompany you on your journey, so you don’t pretend you can figure it out at every step.

There’s also a negative connotation around the term “mental health” that we should be reframing. Those two words tend to make people think about depression, suicidal thoughts or addiction. Which is mental unhealth. Let’s talk more about mental wellness and founder well-being, which focuses us on the goal we’re working toward.

Eliminating the stigma can start with open conversations about well-being between investors and executives, as well as inviting a coach to talk to your founders about what these sessions entail, and why everyone has something to gain. By shattering the taboo, you’ll enable founders to make the absolute most of that experience, rather than hold back to keep up appearances.

If we start making coaching mainstream today, we might eventually see it as obligatory for all founders.

Finally, business leaders and investors need to set an example for the startup community, and especially people at the start of their journeys, that it’s OK to ask for assistance in bettering yourself.

Many VCs, like top CEOs, have coaches. If more simply owned it, they’d have so much power to normalize coaching, and even make #IHaveACoach fashionable. After all, we’re talking about the same industry that made meditation rooms trendy and kombucha an office feature.

Why not make coaching a central topic in future investor conferences, or, as a VC firm, publish a study on how portfolio founders who followed a coaching program saw greater business success?

For example: For years, Union Square Ventures has invested in providing value to their founders and has built a team whose responsibilities include developing leadership training, fostering mentorship circles and connecting founders to coaches. If you let founders see your commitment to human issues, it won’t occur to them that being human is being weak.

These approaches are also important self-promotion for VCs positioning themselves as the next generation of ethical investors. With so many alternative funding options becoming available, founders are seeking VCs who give them more than just capital and who see wellness and diversity and inclusion as inextricable from success.

Founder health and startup health can’t be separated from each other. On some level, all investors know this. So let’s give the people shaping tomorrow’s world the tools to be more comfortable in their own skin and more masterful in leading teams to achieve greatness and incredible returns.

Powered by WPeMatico

Holberton, the education startup that started out as a coding school in San Francisco and today works with partners to run schools in the U.S., Europe, LatAm and Europe, today announced that it has raised a $20 million Series B funding round led by Redpoint eventures. Existing investors Daphni, Imaginable Futures, Pearson Ventures, Reach Capital and Trinity Ventures also participated in this round, which brings Holberton’s total funding to $33 million.

Today’s announcement comes after a messy 2020 for Holberton, and not only because the pandemic put a stop to in-person learning.

The original promise of Holberton was that it provided students — which it selects through a blind admissions process — with a well-rounded software development education akin to a college education for free. In return, students provide a set amount of their salary for the next few years to the school as part of a deferred tuition agreement, up to a maximum of $85,000.

But early last year, California’s Bureau for Private Postsecondary Education (BPPE) directed the school to immediately cease operation, in part because the agency found that Holberton had started offering a new, unapproved program. This program, a nine-month training program augmented by six months of employment, required students to pay the full $85,000 cost of its approved programs. After a hearing, the BPPE allowed Holberton to continue to operate its other programs. A number of students also accused the school of not giving them the education it had promised.

Throughout this period, Holberton continued expanding, though. It opened campuses in Mexico and Peru, for example. Indeed, it doubled the number of schools in its system from nine to 18 in 2020.

But on December 17, 2020, Holberton voluntarily surrendered its operating license in California. The day before, Holberton announced that it would not re-open its campus in San Francisco, which had been shut down since March because of the pandemic. Holberton co-founder Sylvain Kalache argued that the school would be best positioned to achieve its mission by “working with amazing local partners who operate the campuses and deeply understand their markets’ unique needs” and not by operating its own campuses.

It now thinks of itself more as an “OS of Education” that offers franchised campuses and education tools.

In January, California’s attorney general struck down the fraud allegations against the school. “California was the only market in which Holberton faced any regulatory challenges,” Kalache wrote in the company’s first public acknowledgment of the lawsuits. “With this now behind us, we are excited to move forward with our original mission of providing affordable and accessible education to prospective software engineers around the world.”

Clearly, that’s how Holberton’s funders feel about this, too.

“They’ve proven successful in breaking down barriers of cost and access while delivering a world-class curriculum,” said Manoel Lemos, managing partner at Redpoint eventures. “With the concept of ‘OS of Education’ as a service, they provide customers with all the tools they need for success. Customers can be nonprofit impact investors who want to improve local economies, education institutions who want to fill gaps in how they teach in a post-COVID learning environment, or corporations who want to provide the best training possible as education providers themselves or as employee development programs.”

Holberton founder and CEO Julien Barbier tells me that, today, “for the first time since our creation, we have started working with universities to help them create a better experience and add hands-on education on top of their traditional methodology. Everyone’s happy: the school, the students, and the teachers — because they prefer to focus on teaching and not spend huge amounts of time correcting projects.”

He expects to see 5,000 students join this year, up from 500 in 2019, and see the network expand with new schools in the U.S., Europe, LatAm and Africa. He also noted that the company already has customers for its “OS of Education” tools for auto-grading projects and its online programs. Just this week, Holberton Tulsa announced plans to more than double its physical campus in the city.

“Raising funds is helping us support and accelerate our vision of creating this ‘OS of education.’ Many educational entities need help and tools to better support their students and their staff. It is now that they need our help. Again, COVID has accelerated the digital transformation, and clearly, there are a lot of gaps that need to be filled,” he said. “[…] We are now a SaaS company which charges other businesses, universities or non-profits to use our tools and/or contents so that they can run their education/training programs at scale, with a better experience, while increasing the quality of education.”

Powered by WPeMatico

All successful companies start off as a great idea, scribbled on the back of a cocktail napkin during a late-night meeting of the minds or gleaned from a fleeting inspiration that leaves you with a feeling of “I could do that better.”

For most, that’s as far as entrepreneurship ever goes, because, unfortunately, a great idea can’t raise money, develop a product or disrupt an industry.

It’s only an idea.

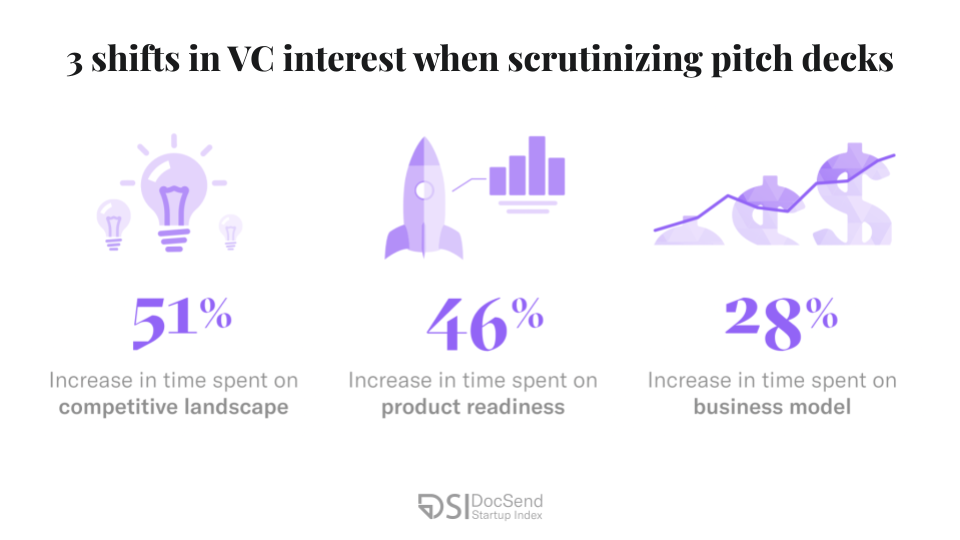

Investors’ heightened expectations for monetization potential and a company’s positioning within its competitive landscape are unlikely to lessen in the years to come, even in a post-COVID economy.

New data from the DocSend Startup Index show that for early-stage fundraising, particularly in the pre-seed round, founders need to approach VCs with much more than a great idea to secure funding. Our newest report on the state of pre-seed fundraising shows that investors became laser-focused on sections of the pitch deck that address monetization and business viability — signs that founders need to come to the table with better-defined businesses in order to succeed.

According to the data, overall founder and VC activity took a nosedive in early 2020 once the serious nature of the pandemic became apparent. But as the year progressed and investors adjusted to the new market conditions and remote dealmaking, overall activity quickly surpassed pre-pandemic levels.

Despite this flurry of activity and an unprecedented appetite for new startup pitches, investors made it very clear that strong positioning in three sections of the pitch deck was nonnegotiable.

Image Credits: DocSend(opens in a new window)

Powered by WPeMatico

When it comes to fast-moving technology, mobility zooms ahead of the pack — both literally and figuratively. Early-stage startup founders and investors need to keep their fingers on the sector’s very rapid pulse and the best place to do that is, you guessed it, TC Sessions: Mobility 2021 on June 9.

If you’re eager to introduce your early-stage startup to the top leaders, investors, experts and policy makers across the mobility tech community, don’t just attend TC Sessions: Mobility — exhibit there. Double down on essential exposure and increase your opportunities.

Budget-friendly tip: The early-bird price remains active until May 5 at 11:59 pm (PST). Buy your Startup Exhibitor Package before the deadline hits and save 35 percent.

Talk about a rapt audience. One big reason people attend the show is to see and meet exciting, innovative new startups. A Startup Exhibitor Package lets you showcase your tech, build your network and expand your opportunities for growth and success. Here’s what your package includes (Note: They’re available only to pre-Series A, early-stage startups).

Keeping with the networking theme, this is how Karin Maake, senior director of communications at FlashParking, described her experience.

“TC Sessions: Mobility isn’t just an educational opportunity, it’s a real networking opportunity. Everyone was passionate and open to creating pilot programs or other partnerships. That was the most exciting part. And now — thanks to a conference connection — we’re talking with Goodyear’s Innovation Lab.”

Don’t miss your chance to sashay your superior stuff in front of the mobility industry’s leading mover, shakers and makers. Buy a Startup Exhibitor Package now, save 35 percent and get ready for TC Sessions Mobility 2021.

Is your company interested in sponsoring or exhibiting at TC Sessions: Mobility 2021? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico

Extra Crunch publishes a variety of article types, but how-tos are my favorite category.

For many entrepreneurs, the startup they are trying to get off the ground might be only the second entry on their resume. As a result, they don’t have much experience to draw from when it comes to basics like hiring, fundraising and growth marketing.

Last week, Natasha Mascarenhas interviewed experts who had some strategic advice for finding the right time to bring a product manager on board. This afternoon, we published a guest post by growth marketer Jessica Li with tips for “how nontechnical talent can build relationships with deep tech companies.”

We’ve also received great feedback on a recent guest post about bootstrapping options for SaaS founders written by a founder who’s actually done it.

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

If you have some startup-related “how” and “why” questions, please browse our Extra Crunch How To stories. They’re aimed squarely at early-stage founders and workers trying to solve long-term problems.

Thanks very much for reading Extra Crunch this week! I hope you have a relaxing weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Steve Jennings / Getty Images

As Roblox began to trade Wednesday, the company’s shares shot above its reference price of $45 per share. Roblox, a gaming company aimed at children, has had a tumultuous if exciting path to the public markets.

Seeing Roblox trade so very far above its direct listing reference price and final private valuation appears to undercut the argument that this sort of debut can sort out pricing issues inherent in more traditional IPOs.

Image Credits: Zastrozhnov (opens in a new window) / Getty Images

Trained on trillions of words, GPT-3 is a 175-billion parameter transformer model — the third of such models released by OpenAI.

GPT-3 is remarkable in its ability to generate human-like text and responses, able to return coherent and topical emails, tweets, trivia and much more. In 2021, this technology will power the launch of a thousand new startups and applications.

Image Credits: Nigel Sussman (opens in a new window)

We are in a period of all-time record investment for so-called mega-rounds, or investments of $100 million or more inside the fintech realm.

To date, Q1 2021 is ahead and is thus guaranteed to set a new record, having already bested the preceding all-time high. What’s going on?

Image Credits: Nigel Sussman (opens in a new window)

Global-e, an e-commerce platform that helps online sellers reach global consumers, filed to go public on Tuesday. Global-e’s business exploded amid the pandemic in 2020, and the company expects that the COVID-fueled shift to e-commerce will only lead to future growth.

Image Credits: Alistair Berg (opens in a new window) / Getty Images

Have you ever popped into a meeting because you overheard a snippet of a conversation and wanted to share your perspective?

That’s passive collaboration — low-friction ways to invite new ideas. But it’s only when we’re able to fully realize passive collaboration virtually that we’ll have unlocked the full potential of remote and hybrid work situations.

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie:

I’m an entrepreneur who wants to expand my startup to the U.S. What are the benefits and drawbacks of various types of visas and green cards?

The ones I’ve heard the most about are the H-1B, O-1 and EB-1A.

— Intelligent in India

Image Credits: Sean Gladwell (opens in a new window) / Getty Images

Many investors will encourage CEOs to remain U.S.-centric this year and perhaps expand their product offering or move into new market segments. But 95% of the world’s population lives outside the U.S., making an expansion into Europe your best growth lever.

Image Credits: Bloomberg (opens in a new window)/ Getty Images

After Roblox debuted on Wednesday, Coupang followed, with shares shooting above the South Korean e-commerce giant’s IPO price range. Quick math shows Coupang is worth around $92 billion at the moment, a huge number that nearly zero companies will ever reach.

Image Credits: Francesco Carta Fotografo (opens in a new window) / Getty Images

Because product managers and founders often have overlapping skill sets, it can be tricky to find the right candidate.

While it’s different for every company, hiring a PM ensures companies aren’t “chasing the shiny object” but rather building the things that create enduring value for customers.

Image Credits: Alashi / Getty Images (Image has been modified)

AI isn’t confined to the tech sphere; machine learning is applicable across disciplines, from music and the “computational unfolding” of ancient letters to figuring out where EV charging stations need to be built.

Image Credits: Bryce Durbin / TechCrunch

The SEC filing offers a glimpse into the finances of how an edtech company, accelerated by the pandemic, performed over the past year.

It paints a picture of growth, albeit one that came at steep expense.

Image Credits: Nigel Sussman (opens in a new window)

Olo has a history of growth and profitability, making its impending pricing all the more interesting.

But are investors willing to pay more for profits? And, if so, how much?

Image Credits: Andrew Ferraro — Handout/Jaguar Racing / Getty Images

InMotion’s investment in Circulor, a company that monitors supply chains from raw material inputs to finished outputs with an eye toward sustainable sourcing, shows the firm’s dedication to backing companies across the mobility space broadly.

Image Credits: maxkabakov (opens in a new window) / Getty Images

Americans are bored, housebound and screened out, driving roughly 128 million Americans to use a voice assistant at least once a month.

This has created a golden opportunity for audio as consumers turn to podcasts, voice assistants and smart speakers.

Image Credits: Nigel Sussman (opens in a new window)

One of the first recurring features Alex Wilhelm established at Extra Crunch was the “$100M ARR Club,” ongoing coverage of startups that have reached scale.

“Forget a $1 billion valuation — $100 million in annual recurring revenue is the cool kids’ club,” he wrote in December 2019. Since then, he expanded it to cover companies that attained $50M ARR.

The concept is a useful lens for studying the market. I can say this with confidence because it’s been widely copied by other tech news outlets. But this morning, Alex surprised me — he’s shelving the ARR Club, at least for now.

“In the end it became a pre-IPO list that was fun but not entirely educational, by my reckoning,” he told me. “The $50M ARR club evolution was supposed to help shake loose more interesting operational details, but just didn’t.”

Before putting the format on hiatus, Alex’s last ARR Club roundup looks at in-office display and kiosk startup AppSpace, data backup unicorn Druva, and Synack, which makes security software.

From April 1-2, some of the most successful founders and VCs will explain how they build their businesses, raise money and manage their portfolios.

At TC Early Stage, we’ll cover topics like recruiting, sales, legal, PR, marketing and brand building. Each session includes ample time for audience questions and discussion.

Use discount code ECNEWSLETTER to take 20% off the cost of your TC Early Stage ticket!

Powered by WPeMatico

Venture capitalists love to talk investment theses: on Twitter, Medium, Clubhouse, at conferences. And yet, when you take a closer look, theses are often meaningless and/or misleading.

OpenVC is a new, open-source initiative to collect and analyze all publicly available VC theses to help founders more efficiently find the right investors — and vice-versa. For the first time, we are sharing here our initial conclusions. We hope you’ll upload your own thesis to benchmark yourself. We’ve identified six common patterns of how VCs articulate their theses and some best practices in doing so.

Our analysis is based on two complementary datasets:

Our four primary conclusions:

For the sake of simplicity, we will consider “investment thesis” and “investment criteria” as equivalent terms moving forward, although we argue that the thesis leads to the investment criteria. We summarize how they interrelate in the table below.

A typical VC thesis: “We invest in tech startups in Europe at an early stage.” However, our experience shows that in many cases “Europe” means a handful of countries, for instance, France, U.K. and Germany; and “tech” means B2B SaaS/fintech or consumer apps.

Thirty-four VC firms in OpenVC call themselves “early stage.” Yet 30% of those don’t actually invest in pre-revenue startups. The phrase is quite ambiguous; we suggest quantifying check size so that your investment preference is clearer.

Almost every VC says that they invest in the “best” founders. However, according to PitchBook Data, since the beginning of 2016, companies with women founders have received only 4.4% of venture capital deals. Those companies have garnered only about 2% of all capital invested. This is despite the fact that the data show you’re better off investing in women.

This lack of transparency results in confused founders who chase the wrong investors. In turn, investors are overwhelmed with poorly qualified opportunities.

Christoph Janz from Point Nine Capital wrote on Twitter:

The modal VC thesis is: “We invest in great teams addressing large markets with disruptive solutions.” Who invests in lousy teams addressing tiny markets with outdated solutions? Theses also tend to use the same words across many firms, e.g., “daring” and “bold.”

In particular, in our second dataset, we found a disproportionate number of theses focused on “technical” companies (vaguely defined) and focused on companies attacking “problems of the future rather than the present,” in various permutations of that language.

| Top Visible Heuristics (in dataset of 36 U.S. VCs) | Occurrences |

| “Technical” companies (i.e., any mention of a focus on tech companies) | 26 |

| Local affinity or bias | 10 |

| Attack problems of the future rather than the present (or some variant) | 9 |

| Technical founders | 7 |

Why are the investment criteria so imprecise on the VC websites? We have three theories, in descending order of importance:

Powered by WPeMatico

You have just 170 seconds. Weeks or even months of working on your pitch deck could come down to the 170 seconds (on average) that investors spend looking at it.

“Investors see a lot of pitches,” VC and LinkedIn co-founder Reid Hoffman noted. “In a single year, the classic general partner in a venture firm is exposed to around 5,000 pitches … and ends up doing between zero and two deals.”

With all that pressure to make an impact quickly, founders spend an incredible amount of time on the design of their slides. Less consideration, however, is usually spent on the words on the slide. That’s a mistake, especially when you only have 170 seconds.

Founders spend an incredible amount of time on the design of their slides. Less consideration, however, is usually spent on the words on the slide. That’s a mistake.

When not used intentionally, the words in your deck can be distracting or downright off-putting. We used what we know about language and healthy communication from the millions of documents we’ve processed at Writer to come up with 11 words and phrases to remove from your VC pitch deck.

Pitching VCs is a balancing act: You want to position your idea in the best light, but also show that you’ve thought things through. However, volunteering certain types of information can have the opposite effect. Don’t write: I’m seeking $X in funding to provide Y months of runway. You certainly need to show how you’re going to use the funding you’re asking for, but you don’t want to frame things in terms of runway in a pitch deck. The word is associated with a looming cash-out date, which can put an investor in a negative state of mind.

This HappySignal slide is a solid example of keeping your messaging positive and using uplifting language.

Don’t write: Our exit strategy is … . Yes, thinking through your business means knowing how you’ll handle worst-case and best-case scenarios. But putting exit strategy in your deck can only get investors thinking about the inherent risks. You want them focused on the opportunity. You need to know what to say when the topic comes up — just don’t volunteer the information on a slide.

A pitch deck is a tool to show VCs why your idea merits investment. Using clichés can work against that goal. Don’t write: If we could capture X percent of the market … . It’s not only a cliché, it’s wishful thinking — not a plan. Keep the text on your slides grounded in relevant facts and figures. Other clichés to cut include: the Amazon of X, imagine a future and moving Y to blockchain.

Powered by WPeMatico

Over the past decade, venture capital has become synonymous with entrepreneurship. Founders from around the world arrive in Silicon Valley with visions of record-setting A rounds and billion-dollar valuations. But what if you don’t have unicorn dreams — or you don’t want to pursue VC money?

Bootstrapping a SaaS company is not only possible — I believe it’s a saner, more sustainable way to build and scale a business. To be clear, bootstrapping isn’t always easy. It requires patience and focus, but the freedom to create a meaningful product, on your terms, is worth more than even the biggest VC check.

The freedom to create a meaningful product, on your terms, is worth more than even the biggest VC check.

I started my company, JotForm, in 2006. We’ve grown steadily from a simple web tool into a product that serves more than 8 million users — without taking a dime in outside funding. We’re profitable in an industry with big-name competitors like Google.

Most importantly, I still love this company and its mission, and I want the same for my fellow entrepreneurs. If you’re a SaaS founder who’s wary of VC funding, here are my best bootstrapping tips.

Success stories from founders who leap blindly into business without resources or relevant experience are compelling, but they’re the exception, not the rule. Working inside another organization can build your skills, your network and even inspire great product ideas.

After finishing college with a computer science degree, I worked as a developer for a New York media company. The editors always needed custom web forms, which were tedious and time consuming to build. I kept thinking, “There has to be a better way.”

That daily frustration led me to start JotForm — but I didn’t leave my job right away. I stayed with the media firm for five years and worked on my product on the side. By the time I was ready to go all in, I had the confidence, experience and savings I needed.

Many of the world’s biggest companies began as side projects, including Twitter, Craigslist, Slack, Instagram, Trello, and a little venture called Apple. If your day job doesn’t pay enough to fund the early stages of your business, consider a side gig or consulting work. There are so many ways to set yourself up for success without the pressure of VC cash or selling a chunk of your business.

The exact numbers shift every year, but data compiled by Fundable show that only 0.05% of U.S. startups are backed by VCs. Another 0.91% are funded by angel investors. The vast majority, at 57%, are funded by credit and personal loans, while 38% get funding from friends and family.

It may feel like most founders raise multimillion-dollar rounds, but that’s simply not the case. It’s also good to remember that securing VC money is complicated and time consuming. You can spend months taking meetings and presenting the perfect deck — and still leave empty handed. Be patient and stick to your own path.

SaaS founders often emphasize vanity metrics, like user acquisitions and total downloads. These numbers can measure short-term popularity, but they don’t reveal how users and customers feel about your product — or your long-term potential.

Powered by WPeMatico

I’m a Black man in America — that’s hard. Black founders, and uniquely Black founders in tech, are facing insurmountable odds.

As the recipients of less than 1% of venture capital raise, institutionalized systems are visibly at play. Within almost 10 years of my entrepreneurial journey, I have encountered just as many setbacks and failures as I have successes.

However, I have pressed forward despite the disparities that often plague the Black entrepreneurial community. From imbalances in fundraising to minimal capital and access, Black brilliance and its cloak of resilience continues to rise.

Now, as a CEO who has ambitiously raised nearly $13 million for my current venture, against the odds, I posit that it is not the Black founders who are missing out the most — it is the investors who are at a loss, not comprehending that they have underestimated the power of these founders’ Black brilliance.

Black founders need to own their resiliency and leverage the power that has resulted from their unique experiences.

When you think about the intersection of venture capital and technology, and specifically how it works — it is being led from an engineering perspective. Developers and coders historically go to specific schools and colleges, entering a funnel that guides them to success.

Historically, many Black students (more so Black male students), are influenced by sports as a vehicle to higher education and not necessarily the institutions recognized for technological prowess.

Their parents and community encourage athleticism because that is the only thing they know — as an institutionalized mindset reinforced over time. Unless they are guided into the accepted foundations for technology, or get into a Cal Berkeley, Stanford or Harvard, where many of the technology companies are built, they are immediately funneled outside of the “circle,” which sets the first of many ongoing obstacles for a Black tech founder.

I offer, however, that these “obstacles” are not in fact barriers but the crucial catalyst for these founders’ superpowers.

Admittedly, there were no entrepreneurs in my family. I did not have access to information about the best colleges. Despite having great grades and graduating with honors, I was completely unaware of how valuable an Ivy League education could be.

As a star basketball player, with my skills and grades, I could have played and graduated from somewhere like Yale, Brown, Columbia or even a school like Southern Methodist University where I was offered a full scholarship. But because of the lack of knowledge that I could actually do so and benefit from being inside the Ivy League “circle,” I didn’t.

I was in college from 2000 to 2004. A lot of great companies were started at elite schools during that period. It is this institutional blocking of information from myself and many other Black students that molded our overall perspective and created our glass ceilings.

Breaking through that glass ceiling, overcoming these odds to press forward relentlessly, with unyielding focus, and to hold conversations with the types of investors I have had to sit in front of, with the type of company that I have built, takes a different level of brilliance that only the Black experience can provide. For 2021 and beyond, Black founders need to not only recognize, but unlock that power as they look to fundraise and catapult their tech companies to success. It would be smart, and incredibly beneficial for investors, venture capitalists and the entire entrepreneurial ecosystem to take heed.

For Black founders, a paradigm shift is evident, but it can only manifest if implemented in these five ways.

Black founders and specifically Black tech founders are fed a monotonous script of how to raise money “the right way,” in light of disparaging statistics highlighting a lack of funding — so much that there is a robotic approach to the process. They try to become this cookie-cutter entrepreneur that is designed to raise money from investors, with their playbook and by their rules.

Black founders capitulate and conform to what society has dictated as appropriate fundraising, often glorifying the investor with the fate of their startup in their hands, without realizing that they hold the negotiating power. Their playbook hasn’t won us any games. As of today, own your power.

Set the playbook aside and lean more into your expertise and uniqueness.

Years ago, Mark Cuban delivered a keynote address at Dallas Startup Week that chronicled his road to success. One of his main points was to “Know your business, and know your business cold.” It was so simple, yet so impactful.

Early on in my career, I learned about venture capital from my experiences working for a startup. While I did not know the area in depth, I referenced what little knowledge I had as I raised for my own company years later. Although I was limited in my dealings with venture capitalists, I was confident in my background and expertise (at that time as a payroll technology sales professional) to truly stake my claim and seat at the table.

So while they may have sold a company for $7 billion or have $35 billion AUM (assets under management), I knew that they were not as well-versed in payroll or payroll technology than I was. It was this tenacious mindset that made me look at investors, rather than up to them, thereby positioning us on equal footing.

As a Black founder in tech, I have encountered many injustices — from networking to fundraising to the game of business as a whole. Even among those sitting at the table, there is a plethora of worldviews, political preferences, religious propensities and more that create a melting pot of divisiveness. However, recognizing that the common thread between all of the players in the game is the desire to be part of the brilliant business opportunity at hand is what will ultimately prevail.

It served me well not to overindex whether the venture capitalists liked me or on our differences. Locking in on the ambition of my entrepreneurial spirit and focusing on my brilliance — my Black brilliance — made them want to invest in me. Simplistically, investors want to give their money to founders who will make them money — passionately and ambitiously. Be you and find the investor that appreciates you.

Black founders are not getting in front of enough investors. Systemically, the venture capital landscape has marginalized this community and has failed to expand their network for inclusiveness. Currently, ethnic minorities are severely underrepresented in the venture capital industry. Eighty percent of investment partners are white, with only a staggering 3% being Black or African-American.

Regardless, Black entrepreneurs must press forward and still show up. The sheer number of people that entrepreneurs must face during the fundraising process is astronomical, so one must not be swayed by the disillusionment of opportunity.

Realistically speaking, it takes a long time to raise money. Period. I have talked to thousands of potential investors to raise nearly $13 million for my current company. If you are a Black founder, it is going to take you longer to fundraise and you are going to have to get in front of more people. So I ask, “Do you have enough oxygen in the tank to withstand the obstacles, for a long enough period of time, to attract the venture capital that you need?” The wealth gap says no.

When I first started Gig Wage, the number one question I received from investors is, “How much runway do you have?” I would answer, “Until I get to where I need to get.” They would then rephrase, “How much money do you have in the bank? How long is your wife going to let you do this?” I would reply, “It does not matter how much money I have in the bank because I’m going to keep going until this happens.”

Discriminatively, there was this unspoken expectation that I lacked the financial wherewithal and stamina to withstand the fundraising process, and at times it was extremely discouraging — because to be honest, when I looked in the bank account, I realistically had about nine to 12 months of runway.

The reason Black people raise less than 1% of venture capital is because the racism weaved into the fabric of American society bleeds over into the entrepreneurial ecosystem. Despite it all, I took thousands of meetings. I was willing to endure with an ambitious conviction that I was going to win. Again, this is Black brilliance.

As a Black man, I have personally endured challenges to build resiliency — mirroring similar realities of other Black men in America. Whether it was dealing with the police or witnessing men in my family struggle with drugs, violence, poverty or the like — I often think, “Why would I be intimidated by an investor meeting or a term sheet?” The construct of America has dealt me much worse.

Black founders need to own their resiliency and leverage the power that has resulted from their unique experiences. The victory mentality that ensues thereafter is the type of mindset that venture capitalists should want to invest in, and if they do not, they are undoubtedly missing out.

The unyielding focus of “The world is stacked against me but I’m not going to quit. I’m going to pivot. I’m going to be resourceful. I’m going to figure it out — even if I’m scared,” is a person you need to invest in. It is not necessarily that they have a groundbreaking business idea, but culturally, Black people have a passion and a perspective that is unmatched, with limitless possibilities that venture capitalists are overlooking.

So for 2021 and well beyond, Black founders, and those especially in tech, need to shift their respective paradigms, own their place within the entrepreneurial space, take back their power and continue to operate at the utmost in Black brilliance. It is the investors, not the founders, that are missing out. Be bold. Be courageous. Be audacious.

As for me, the best thing that I can do right now is to continue to drive the conversation, illuminate the disparities and be as successful for Black entrepreneurs, Black professionals and the world at large as possible. I am owning my power and I’m committed to epitomizing and evangelizing Black brilliance.

Powered by WPeMatico

This morning Citadel ID announced a combined $3.5 million raise for its income and employment verification service. The startup provides an API to customer companies, allowing them to rapidly verify details of consumer employment.

The capital came from a blend of venture firms and angels. On the firm side, Abstract and Soma VC were in there, along with ChapterOne. Brianne Kimmel put capital in as well, according to the startup. And denizens with work histories at companies like Zynga (Mark Pincus), Stripe (Lachy Groom), Carta (Henry Ward) and others also put cash into the fundraise. (The company reached out to add that Fathom Capital also put a good amount in the round.)

Citadel was founded back in June of 2020, before raising capital, snagging its first customer and shipping its product all inside of the same year.

The idea for Citadel ID came when co-founder Kirill Klokov worked at Carta, the cap-table-as-a-service startup that recently built an exchange for the trading of private stock. Klokov discovered while working on the tech side of the company how hard it was to verify certain data, like employment and income and identity.

As Carta deals with money, stock and the collection and distribution of both, you can imagine why having a quick way to verify who worked where, and since when, mattered to the company. But Klokov came to realize that there wasn’t a good solution in the market for what Carta needed, sans building integrations to a host of payroll managers by hand and dealing with lots of data with varying taxonomies. That or using an in-the-market product, like Equifax’s The Work Number, which the founder described as expensive and offering relatively low coverage.

To fill the market void Klokov helped found Citadel ID, quickly building integrations into payroll managers where there were hooks for code, and working around older login systems when needed. Citadel ID’s service allows regular folks to provide access to their employment data to others, allowing for the verification of their income (a rental group, perhaps), or employment (Carta, perhaps) quickly.

Per the startup the market demand for such verifications is in the hundreds of millions every year in the United States. So, Citadel should have plenty of market space to grow into. Citadel ID has around 20 customers today, it told TechCrunch, and charges on a per verification basis.

Finally, while Citadel also offers data via its website and not merely through its API, the startup still fits inside the growing number of startups we’ve seen in recent quarters foregoing traditional SaaS, and instead offering their products via a developer hook (sometimes referred to as a “headless” approach). API-delivered startups are not new, after all Twilio went public years ago. But their model of product delivery feels like it’s gaining momentum over managed software offerings.

Let’s see how quickly Citadel ID can scale before it raises its Series A.

Powered by WPeMatico