entrepreneurship

Auto Added by WPeMatico

Auto Added by WPeMatico

Many companies will not see the uncertainty of a global pandemic as the perfect moment to go international, but for others (particularly in healthcare, online communications, and workplace mobility) the market is stronger than ever and companies are having to respond quickly internationally to both service existing clients and take advantage of the growth in demand.

We and our team at Taylor Wessing advise 50 to 75 venture-backed North American companies each year on setting up in Europe or Asia. We’ve helped companies such as TaskRabbit, Lime, Glossier, InVision and many others translate their domestic success to new jurisdictions and cultures and to thrive as global businesses.

This is a practical guide to international expansion with the challenges of the current time in mind. It’s a quick-read providing some practical tips and sharing best practices from peer companies to help you come out of the pandemic with a strong international presence. A great deal of this advice is evergreen and will serve you well whatever the circumstances may be.

In particular, we’ll cover the rise (and risks) of distributed workforces — a way for CEOs to hire the best talent anywhere in the world. This has taken on new significance with the boom in remote working as one of several options for CEOs looking for strategic growth during and after COVID.

Ten years ago, the timing question was much simpler. Founders would first of all focus on developing a product and winning over their domestic market, funded through their Series A and B rounds, and then go on to raise their Series C round, which investors would expect to be used to push into new markets.

Since then, with the age of the smartphone in full swing and international direct ordering ubiquitous, opportunities to sell into new markets appeared far earlier in a company’s growth and there is no longer a canned strategy for timing your international expansion.

The current circumstances have exaggerated this trend. There are many challenges in traditional sectors, but also many new market opportunities quickly appearing in healthcare and other technology sectors with founders wanting to move quickly into new markets.

Although it may be tempting to just get a few sales people on the ground to go for it, we would still recommend laying some groundwork and making some key decisions before diving in. For example: ensuring management can give sufficient time and attention to the new market; tweaking your product to comply with local regulations; reworking your sales approach.

If you are early-stage, tread carefully. Our belief is that the Series B round is still the earliest a founder or board should consider international expansion.

If you are early-stage, tread carefully. Our belief is that the Series B round is still the earliest a founder or board should consider international expansion. The companies we’ve worked with who have moved earlier than the B round will generally end up realizing it’s too early. They’ll end up pressing pause, or making a full strategic exit, tail between legs.

International expansion is a matter of focus, as well as financial resources. Once you’re selling into a new market, everyone in the business needs to be thinking internationally, including the CEO, CFO, general counsel, the board, engineers and staff. It can stretch everyone before there are the necessary resources in place to cope.

Even in the best of times our advice would be to not experiment or push the boundaries when it comes to your international strategy, do that elsewhere in your business. You should follow the path most travelled at this stage. This is especially true in the current climate. If you’re thinking of doing something new, something your peers haven’t done before, we should have a conversation first.

Whichever market you’ve chosen, there are some universal first steps (although they might vary slightly between jurisdictions). For example:

Powered by WPeMatico

VCs expect the companies they invest in to use data to improve their decision-making. So why aren’t they doing that when evaluating startup teams?

Sure, venture capital is a people business, and the power of gut feeling is real. But using an objective, data-backed process to evaluate teams — the same way we do when evaluating financial KPIs, product, timing and market opportunities — will help us make better investment decisions, avoid costly mistakes and discover opportunities we might have otherwise overlooked.

An objective assessment process will also help investors break free from patterns and back someone other than a white male for a change. Is looking at how we have always done things the best way to build for the future?

Sixty percent of startups fail because of problems with the team. Instinct matters, but a team is too big a risk to leave to intuition. I will use myself as an example. I have founded two companies. I know what it takes to build a company and to achieve a successful exit. I like to think I can sense when someone has that special something and when a team has chemistry. But I am human. I am limited by bias and thought patterns; data is not.

You can (and should) take a scientific approach to evaluating a startup team. A “strong” team isn’t a vague concept — extensive research confirms what it takes to execute a vision. Despite what people expect, soft skills can be measured. VCVolt is a computerized selection model that analyzes the performance of companies and founding teams developed by Eva de Mol, Ph.D., my partner at CapitalT.

We use it to inform every investment decision we make and to demystify a common hurdle to entrepreneurial success. (The technology also evaluates the company, market opportunity, timing and other factors, but since most investors aren’t taking a structured, data-backed approach to analyzing teams, let’s focus on that.)

VCVolt allows us to reduce team risk early on in the selection and due diligence process, thereby reducing confirmation bias and fail rates, discovering more winning teams and driving higher returns.

I will keep this story brief for privacy reasons, but you will get the point. While testing the model, we advised another VC firm not to move forward with an investment based on the model’s findings. The firm moved forward anyway because they were in love with the deal, and everything the model predicted transpired. It was a big loss for the investors, and a reminder that hunch and gut feeling can be wrong — or at least blind you to some serious risk factors.

The platform uses a validated model that is based on more than five years of scientific research, data from more than 1,000 companies and input from world-class experts and scientists. Its predictive validity is noted in top-tier scientific journals and other publications, including Harvard Business Review. By asking the right questions — science-based questions validated by more than 80,000 datapoints — the platform analyzes the likelihood that a team will succeed. It considers:

Powered by WPeMatico

When a friend forwarded this tweet from Paul Graham, it hit close to home:

Startups are subject to something like infant mortality: before they’re established, one thing going wrong can kill the company. Hardware companies seem to be subject to infant mortality their whole lives.

I think the reason is that the evolution of the product is so discontinuous. The company has to keep shipping, and customers to keep buying, new products. Which in practice is like relaunching the company each time.

I don’t know if there is an answer to this, but if there were a way for hardware companies to evolve more the way software companies do, they’d be a lot more resilient.

Looking back on our startup journey at Minut, I remember several moments when we could have died. However, surviving several near misses we learned to tackle these challenges and have become more resilient over time. While there will never be one fully exhaustive answer, here are some of the lessons we learned over the years:

While you can sell hardware with a margin and make important early revenue, it’s not a sustainable business model for a company that requires both software and hardware. You can’t cover an indefinite commitment with a finite amount of money.

Many hardware companies don’t consider subscriptions early enough. While it can be hard to command a subscription from the start (if you can, you might have waited too long to launch), it needs to be in the plan from the beginning. Look for markets where paying subscriptions is the norm rather than markets that operate on a one-time sale model.

It’s tempting to set low prices for hardware to attract customers, but in the beginning you should do the opposite. Margins allow for mistakes to be rectified. A missed deadline might mean you have to opt for freight by air rather than boat. You might have to scrap components or buy them expensively in a supply crunch. Surprises are seldom positive, and you don’t want to use your venture capital to pay for them.

Healthy margins can also be used to cover marketing costs while you learn what kind of messaging works and what channels you can sell through. If that wasn’t enough reason, starting with relatively high prices will help you avoid another common mistake, selling too much at launch.

This might seem counterintuitive — why wouldn’t you want great success out of the gate? The reason is that you will inevitably make mistakes with your early launches, and the bigger the launch, the bigger the blow. There are plenty of companies who achieved amazing crowdfunding success and then failed to deliver even the first units. Startups tend to chase growth at all costs, but for hardware startups in the first few years there is such a thing as too much of a good thing.

Powered by WPeMatico

Welcome, the HR software that helps organizations make and close offers to new candidates, announced the close of a $6 million seed round today, led by FirstMark Capital. Participating investors include Ludlow Ventures, Nat Turner and Zach Weinberg, and Keenan Rice and Ben Porterfield (which were existing investors), as well as a wide array of angels.

TechCrunch last covered Welcome in August, when it announced a $1.4 million funding round. That the startup was able to raise more as quickly as it has is testament to how hot the early-stage venture capital market is today, and likely an endorsement of Welcome’s economic profile and recent growth.

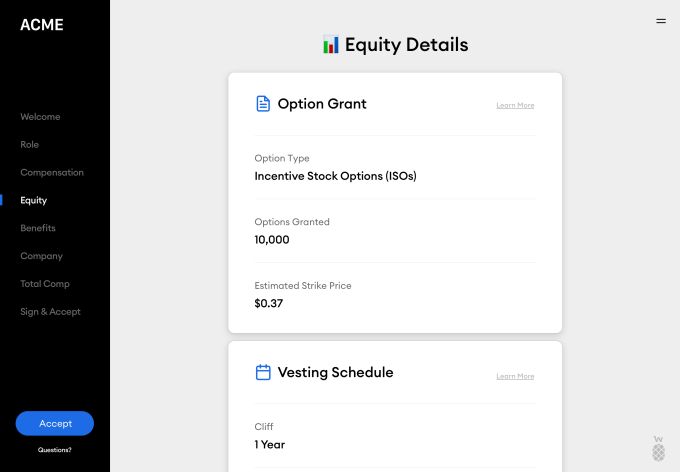

Past the new capital, Welcome is also launching a new product today called Total Rewards, which helps not just new candidates but also existing employees get a complete, easy-to-understand picture of their compensation, across salary, benefits, equity, etc.

But let’s back up.

Welcome was founded in 2019 by Nick Gavronsky and Rick Pereira, with a mission to help organizations close offers on candidates by providing a much clearer picture of compensation, particularly around equity. Co-founder and CEO Nick Gavronsky explained that many candidates don’t truly understand the value of the equity they’re offered, or how it works.

“A lot of recruiting teams aren’t well-equipped to use it as a selling tool and explain it effectively and showcase the value to candidates to help them think about their ownership at the company,” he added.

Image Credits: Welcome

Welcome allows companies to organize their compensation offers based on level and position, and deliver that information digitally to candidates in a way that makes sense.

The startup integrates with a variety of other software providers, including Slack, Lever, Greenhouse, ADP and Justworks to name a few, simplifying onboarding for Welcome clients and bringing a broad array of information into one place.

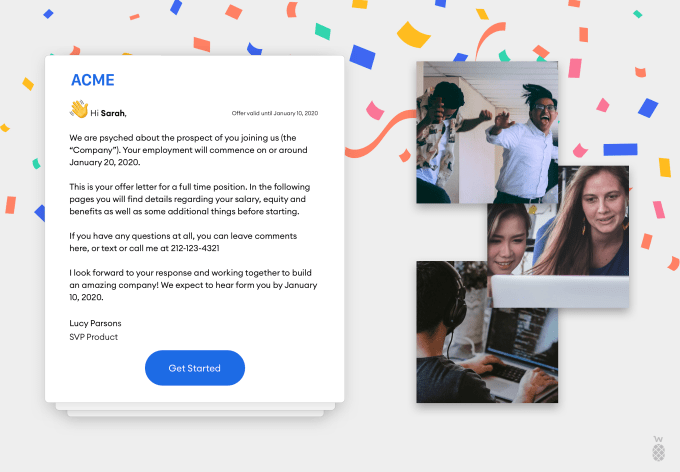

Offers sent through Welcome show a description of the role, equity details, total compensation and even include a welcome note and video. This is in stark contrast to the black and white legal PDF often sent to candidates.

Image Credits: Welcome

The next phase for the company comes in the form of the launch of Total Rewards, which is meant to help retain existing employees, helping them understand their compensation value and their potential at the company.

“Painting a better picture becomes a pre-retention tool,” said Gavronsky. “An employee will sometimes leave thousands of dollars on the table because they don’t understand what they’re walking away from. A lot of times companies will wait until that person is going to resign. Let me now bring up all the things that are great about our company and talk through your stock options. But the decision’s already made. So we wanted something that we can kind of put in with performance reviews.”

Welcome also has plans to offer a third product pillar in the form of real-time accurate industry-wide compensation data, helping companies understand where they fit into the larger ecosystem with regards to compensation.

Thus far, Welcome has 40 companies on the platform, including Uncork and Betterment, with hundreds on the waitlist, according to the co-founders. The company plans to use the funding to build out the team and the product.

Powered by WPeMatico

If I were to pick one thing that unites the global tech scene in terms of culture I would point to the respect and reverence accorded to startup founders.

After all, creating your own company is an ambition many of us harbor. It can bring with it unparalleled freedom, a lasting legacy, prestige, wealth and the ability to do good. Across social and traditional media the feats of founders big and small are lauded for their genius on a daily basis. Many entrepreneurs go to great lengths to showcase their backbreaking hard work and eye-popping success. An outsider would be forgiven for believing that every founder is living the dream as a result of their talent and toil.

Of course, as with nearly every image projected online, the reality is quite different. There is a seldom talked about price of being a founder — the impact on one’s mental health.

A recent study by the National Institute of Mental Health found that 72% of entrepreneurs are directly or indirectly impacted by mental health issues. This compares to 48% of the general population. The damage can also affect loved ones — 23% of entrepreneurs report that they have family members with problems, which is 7% higher than the relations of nonentrepreneurs.

I am in no way a mental health expert. But what I do know from both my own experience and speaking to scores of business owners I work with is that being a founder is an inherently lonely job. Pressure is high and uncertainty pervades every decision. Fear of failure is ever present. Unaddressed, these issues can take a serious toll.

The unpalatable truth is that the situation appears to be getting worse. A similar study conducted in 2015 by Dr. Michael A. Freeman found the rate of mental health issues among founders to be lower — at 50%. While comparing different research pieces is inexact, we only need to look at how the global recession has damaged many companies and how working from home has contributed to feelings of isolation, to know that the environment for startups has got harder this year. Added to this mix is how social media continues to promote an unhealthy fetishization of hustle culture and founding myths.

A number of founders have told me that they have constant feelings of inadequacy and guilt when they compare themselves to the startup gurus who celebrate working 24/7, are constantly selling, raising money or making their millions. They feel they should be working harder or be doing better — just like all the people they read about.

So how do we address this? The first step is talking about it. This means having an environment where we can be honest that not everything is always fine. Speaking to a fellow founder, not about commercial concerns, but about personal worries can be revelatory. I’ve seen it happen in our community. It’s like an “Emperor’s New Clothes” moment.

The myth of the bulletproof, genius, hustling founder can disappear in a puff of smoke as people suddenly realize they are not alone. They find that the concerns, anxieties and uncertainties they feel are almost universal.

Experienced founders can provide invaluable support to people new to the startup scene. They can share their experiences, both failures and success, and reveal some of their coping mechanisms. I would strongly advise founders who are experiencing some of the worries I’ve outlined to actively seek out advice from both their peers and potential mentors — much in the way they may seek out commercial guidance.

Next, we need to address how we tackle the culture and myths around being a founder. Business owners need to know that many of the extraordinary “success stories” they see celebrated online are exactly that — extraordinary.

Similarly, those that promote the principle that working all hours is the only way to be successful are at best talking about what works for them, and are at worst, engaging in a performance to achieve attention. We need to think carefully about how we respond to these posts. There is a fine line between being supportive and enabling unhealthy or damaging behavior and philosophy.

After all, success in the startup scene is all relative. For some owning a small business that makes them a decent income with a good work-life balance is the goal. For others, it is simply being able to do what they love in the way that they want. Very few will get the exit that makes them a millionaire, and an infinitesimally small minority will build the next Facebook . I cannot stress enough how important it is for founders to keep their aims and ambitions in perspective and ignore the noise they hear online.

More broadly, the industry, including the media, does need to get wiser about how it views and represents founders. For example, a pervasive myth is that some of the biggest tech companies in the world started in garages with no money, then through the genius and sheer bloodymindedness of their founder they were grown into a massive corporation.

The reality is that the vast majority of these tech companies benefited from substantial seed capital from family or connections almost from day one. These founders were also quickly surrounded by highly talented people who did a lot of the heavy lifting and, whisper it, a truckload of good luck. In short, the idea of the superhuman founder perpetuated in the industry is, in nearly all cases, nonsense.

In a similar vein, there are also issues around how we frame success and failure.

Success, as I’ve mentioned earlier, is nearly always couched in the most basic numerical terms. The “unicorn” label is bandied about so often that many people fail to realize that it’s simply a valuation that a few investors have given a company. It does not reflect whether the business is actually successful in the traditional sense, i.e., making money. Generally, the startup scene celebrates and idolizes founders who make big exits or achieve “unicorn status” — less is spoken about the thousands of SMEs that employ people, develop and patent new tech, make a tidy profit and pay taxes.

With failure, there is an altogether different problem. The startup scene downplays failure as par for the course. It is, on the face of it, one of the industry’s great virtues. It enables people to try without fear of embarrassment. However, in practice, it can actually minimize real-world fears nearly all founders have. Failure cannot just be brushed off if you’ve devoted years of your life, spent a lot of money and have staff who rely on you. By simply thinking of failure as part of the process we cannot address and talk about this real source of concern in an open way. “Fail fast” only works for those who can afford it.

Individually, these issues may seem like nothing but white noise and the cure for suffering founders may simply be to get off social media. Unfortunately, it isn’t that simple. Social and traditional media is amplifying startup culture, not creating it. The same tropes are on display at every tech conference and meetup. To fit in, the founder is expected to be a fearless, genius visionary. Deviation from this norm, such as by displaying vulnerability around mental health, is by inference, failure.

Despite its shortcomings in relation to diversity, the startup scene is generally one of the most progressive, collaborative and open industries in the world. These virtues are ideally suited to tackling the reluctance to discuss mental health and creating the network of support that ensures people don’t suffer alone.

To make this happen, we need to dispense with the myths and hagiography around being a founder and be more honest about what the reality of running a business actually entails.

Powered by WPeMatico

A few years ago, building a bottom-up SaaS company – defined as a firm where the average purchasing decision is made without ever speaking to a salesperson – was a novel concept. Today, by our count, at least 30% of the Cloud 100 are now bottom-up.

For the first time, individual employees are influencing the tooling decisions of their companies versus having these decisions mandated by senior executives. Self-serve businesses thrive on this momentum, leveraging individuals as their evangelists, to grow from a single use-case to small teams, and ultimately into whole company deployments.

In a truly self-service model, individual users can sign up and try the product on their own. There is no need to get compliance approval for sensitive data or to get IT support for integrations — everything can be managed by the line-level users themselves. Then that person becomes an internal champion, driving adoption across the organization.

Today, some of the most well-known software companies such as Datadog, MongoDB, Slack and Zoom, to name a few, are built with a primarily bottom-up product-led sales approach.

In this piece, we will take a closer look at this trend — and specifically how it has fundamentally altered pricing — and at a framework for mapping pricing to customer value.

In a bottom-up SaaS world, pricing has to be transparent and standardized (at least for the most part, see below). It’s the only way your product can sell itself. In practice, this means you can no longer experiment as you go, with salespeople using their gut instinct to price each deal. You need a concrete strategy that aligns customer value with pricing.

To do this well, you need to deeply understand your customers and how they use your product. Once you do, you can “MAP” them to help align pricing with value.

The MAP customer value framework requires deeply understanding your customers in order to clearly identify and articulate their needs across Metrics, Activities and People.

Not all elements of MAP should determine your pricing, but chances are that one of them will be the right anchor for your pricing model:

Metrics: Metrics can include things like minutes, messages, meetings, data and storage. What are the key metrics your customers care about? Is there a threshold of value associated with these metrics? By tracking key metrics early on, you’ll be able to understand if growing a certain metric increases value for the customer. For example:

Activity: How do your customers really use your product and how do they describe themselves? Are they creators? Are they editors? Do different customers use your product differently? Instead of metrics, a key anchor for pricing may be the different roles users have within an organization and what they want and need in your product. If you choose to anchor on activity, you will need to align feature sets and capabilities with usage patterns (e.g., creators get access to deeper tooling than viewers, or admins get high privileges versus line-level users). For example:

Powered by WPeMatico

BuildBuddy, whose software helps developers compile and test code quickly using a blend of open-source technology and proprietary tools, announced a funding round today worth $3.15 million.

The company was part of the Winter 2020 Y Combinator batch, which saw its traditional demo day in March turned into an all-virtual affair. The startups from the cohort then had to raise capital as the public markets crashed around them and fear overtook the startup investing world.

BuildBuddy’s funding round makes it clear that choppy market conditions and a move away from in-person demos did not fully dampen investor interest in YC’s March batch of startups, though it’s far too soon to tell if the group will perform as well as others, given how long it takes for startup winners to mature into exits.

BuildBuddy has foundations in how Google builds software. To get under the skin of what it does, I got ahold of co-founder Siggi Simonarson, who worked at the Mountain View-based search giant for a little over a half decade.

During that time he became accustomed to building software in the Google style, namely using its internal tool called Blaze to compile his code. It’s core to how developers at Google work, Simonarson told TechCrunch. “You write some code,” he added, “you run Blaze build; you write some code, you run Blaze test.”

What sets Blaze apart from other developer tools is that “opposed to your traditional language-specific build tools,” Simonarson said, it’s code agnostic, so you can use it to “build across [any] programming language.”

Google open-sourced the core of Blaze, which was named Bazel, an anagram of the original name.

So what does BuildBuddy do? In product terms, it’s building the pieces of Blaze that Google engineers have access to inside the company, for other developers using Bazel in their own work. In business terms, BuildBuddy wants to offer its service to individual developers for free, and charge companies that use its product.

Simonarson and his co-founder Tyler Williams started small, building a “results UI” tool that they shared with a Bazel user group. The members of that group picked up the tool, rapidly bringing it inside a number of sizable companies.

This origin story underlines something that BuildBuddy has that early-stage startups often lack, namely demonstrable enterprise market appetite. Lots of big companies use Bazel to help create software, and BuildBuddy found its way into a few of them early in its life.

Simply building a useful tool for a popular open-source project is no guarantee of success, however. Happily for BuildBuddy, early users helped it set direction for its product development, meaning that over the summer the startup added the features that its current users most wanted.

Simonarson explained that after BuildBuddy was initially used by external developers, they demanded additional tools, like authentication. In the words of the co-founder, the response from the startup was “great!” The same went for a request for dashboarding, and other features.

Even better for the YC graduate, some of the features requested were the sort that it intends to charge for. That brings us back to money and the round itself.

BuildBuddy closed its round in May. But like with most venture capital tales, it’s not a simple story.

According to Simonarson, his startup started raising the round during one of those awful early-COVID days when the stock market dropped by double-digit percentage points in a single trading session.

BuildBuddy’s goal was to raise $1.5 million. Simonarson was worried at the time, telling TechCrunch that it was his first time fundraising, and that he wasn’t sure if his startup was going to “raise anything at all” in that climate.

But the nascent company secured its first $100,000 check. And then a $300,000 check, over time managing to fill out its round.

So what happened that got the company from $1.5 million to just over $3 million? The investor that put in $300,000 wanted to put in another $2 million. The company talked them down to $1.5 million at a higher cap (BuildBuddy raised its round using a SAFE), and the deal was done at those terms.

The startup initially didn’t want to raise the extra cash, but Simonarson told TechCrunch that at the time it was not clear where the fundraising environment was heading; BuildBuddy raised back when startup layoffs were a leading story, and a return to high-cadence VC rounds was months away.

So BuildBuddy wound up securing $3.15 million to support a current headcount of four. It intends to hire, naturally, lower its comically long runway and keep building out its Bazel-focused service.

Picking a few names from the investor spreadsheet that BuildBuddy sent over — points for completeness to the startup — Y Combinator, Addition, Scribble and Village Global, among others put capital into the round.

Dev tools are hot at the moment. Given that, as soon as BuildBuddy’s ARR starts to get moving, I expect we’ll hear from them again.

Powered by WPeMatico

Floww — a data-driven marketplace designed to allow founders to pitch investors, with the whole investment relationship managed online — says it has raised $6.7 million (£5 million) to date in seed funding from angels and family offices. Investors include Ramon Mendes De Leon, Duncan Simpson-Craib, Angus Davidson, Stephane Delacote and Pip Baker (Google’s head of Fintech U.K.) and multiple family offices. The cash will be used to build out the platform designed to give startups access to more than 500 VCs, accelerators and angel networks.

The team consists of Martijn De Wever, founder and CEO of London-based VC Force Over Mass; Lee Fasciani, co-founder of Territory Projects (the firm behind film graphics and design including “Guardians of the Galaxy” and “BladeRunner 2049”); and CTO Alex Pilsworth, of various fintech startups.

Having made more than 160 investments himself, De Wever says he recognized the need for a platform connecting investors and startups based on merit, clean data and transparency, rather than a system built on “warm introductions,” which can have inherent cultural and even racial biases.

Floww’s idea is that it showcases startups based on merit only, allowing founders to raise capital by providing investors with data and transparency. Startups are given a suite of tools and materials to get started, from cap table templates to “How To” guides. Founders can then “drag and drop” their investor documents in any format. Floww’s team of accountants then cross-checks the data for errors and processes key performance metrics. A startup’s digital profile includes dynamic charts and tables, allowing prospective investors to see the company’s business potential.

Floww charges a monthly fee to VCs, accelerators, family offices and PE firms. Startups have free access to the platform, and a premium model to contact and send their deal to multiple VCs.

Floww’s pitch is that VCs can, in turn, manage deal-sourcing, CRM, as well as reporting to their investors and LPs. Quite a claim, given all VCs to date handle this kind of thing in-house. However, Floww claims to have processed 3,000 startups and says it is rolling out to more than 500 VCs.

In a statement, De Wever said: “In an age of virtual meetings and connections, the need for coffee meetings on Sand Hill Road or Mayfair is gone. What we need now are global connections, allowing VCs to engage in merit-based investing using data and metrics.” He says the era of the coronavirus pandemic means many deals will have to be sourced remotely now, so “the time for a platform like this is now.”

AngelList is perhaps its closest competitor from the startup perspective. And the VC application incorporates the kind of functionality seen in Affinity, Airtable, Efront and DocSend. But AngeList doesn’t provide data or metrics.

Powered by WPeMatico

Sequoia Capital, the renowned Silicon Valley venture capital firm that has backed companies like Apple, Google, Dropbox, Airbnb and Stripe, recently disclosed that it had opened its first office in Europe. To staff up, it hired partner Luciana Lixandru away from rival Accel Partners.

Even without an official European presence, Sequoia has quietly operated in the region for more than a decade, first investing in Klarna in 2010. Other Europe-founded companies in its portfolio include Baaima, CEGX, Charlotte Tilbury, Dashlane, Evervault, FON Wireless, Front, Graphcore, Mapillary, Metaswitch Networks, n8n, Remote, Skyscanner, Songkick, Tessian, Tourlane, UiPath, Unity and 6Winderkinder (Wunderlist).

Yet, it is only now that the VC firm is putting people on the ground here in Europe, starting with an office in London that has a remit to invest across the continent.

Working alongside Lixandru is a more junior investor, George Robson, who joined from Revolut. Most recently, Sequoia recruited Zoe Jervier Hewitt from EQT as head of talent in Europe. And finally, Matt Miller, a Sequoia U.S. veteran, is also part of the European efforts and plans to relocate next year, while I also understand that Sequoia’s Doug Leone will be spending a lot of his time in Europe.

Last week at the virtual “Node by Slush” event, I interviewed Lixandru and Miller and teased out some important details about Sequoia’s plans.

“There has been this evolution and maturity of the tech ecosystem that has been really meaningful, that has attracted us to want to put down boots on the ground and be more invested in Europe than ever before,” said Sequoia partner Matt Miller.

“One change is in the attitudes of young people. Europe has always been this place where there’s been incredible talent coming out of the computer science programs, across the universities across the continent and the U.K., and these young people previously, were going into careers in investment banking and consulting are bigger conglomerates. And now that those young people are interested in startups and technology careers, that’s fueling a lot of great ideas and a lot of great talent.

“There was a long time this question of, when will there be a $10 billion plus startup, and now there’s multiple of them across the continent. And now the question has really changed: When will there be the next hundred billion dollar startup in Europe, and I think it’s just an evolution over time.

“We find ourselves getting pulled more and more. So when … we want to invest in the best AI semiconductor company in the world, we looked at them in China, Israel and Europe. And the one we wanted to invest in was Graphcore, in Bristol [in the U.K.]. And when we looked … [to] invest in the best process automation company in the world, we looked at automation anywhere in California … and we looked at companies all over the world, and the one we wanted to invest in was UiPath in Romania. And that is increasingly becoming the case.”

“To some extent, success breeds success, too,” said Lixandru. “I think role models are really powerful. And the fact that there have been these category-leading companies created out of Europe, but that are winning on a global scale, like Spotify, Adyen and UiPath … I think that’s really inspirational to the next generation of founders. And I think that has helped a lot.”

“We work as one partnership across two geographies, and we invest from the same pool of capital across both geographies,” explained Lixandru. “And the rationale behind that is exactly what Matt talked about. We want to be able to partner with category leading companies, and if they start in Paris, or in Stockholm, or in San Francisco, for us, it does not make a difference. We want to partner with them early. And we want to be able to help them on the ground early … whether they start here in Europe or in the U.S.”

Related to this, Sequoia will share carry — the fund’s profits — with partners across the U.S. and Europe, regardless of where partners reside or where the deal was sourced.

“One of the things that I love the most about Sequoia having been here close to nine years now is the way that we operate is very, very team centric, and that everybody is compensated the same amount in a fund, whether or not it is the investment that they lead or the investment that their partner led,” said Miller. “So when we make an investment, we lock arms together as a team, and we work collectively to help that company be successful.”

Miller said portfolio companies in Europe also get to work with Sequoia’s operational supporting partners in the U.S., too. “And the economic model is one that supports that,” he said.

Powered by WPeMatico

Milana Lewis, CEO and co-founder of music tech startup Stem, started the fundraising process long before she actually asked any investors for money (dig the well before you’re thirsty — it’s the best way). She recommends that other founders do the same.

Ten years ago, Milana started working at United Talent Agency (UTA), one of the world’s leading talent agencies. When tasked with finding the best tools and technologies that UTA’s clients could use to self-distribute their work, she discovered a glaring gap.

“There were all these tools built for the distribution of content, monetization of content and audience development,” she says. “The last piece missing was the financial aspect.” The entertainment industry desperately needed a platform that would help artists manage the financial side of their business — and that’s how the idea for Stem was born.

Because UTA had its own investment branch, called UTA Ventures, Milana’s job also introduced her to some brilliant investors. Years later, when it was time to fundraise for Stem, those connections played a pretty big role.

In an episode of How I Raised It, Milana shared how Stem has landed some superstar investors and raised a little under $22 million.

Milana’s involvement with UTA Ventures exposed her to the investor experience and put her in the same room as people like Gary Vaynerchuk, Jonathon Triest from Ludlow Ventures, Anthony Saleh from Wndrco and Scooter Braun.

After meeting them the first time, she made sure to nurture those relationships, and she was “honest and vulnerable” about the fact that she wanted to be an entrepreneur one day.

“It’s amazing how much people will help and support you along in that journey,” Milana says. Investors “get excited about making early-stage investments because they want to identify that person before anyone else does.”

As her idea for Stem came together, she shared that with them, too. Over the course of a year, she provided regular updates on her vision, like how she was building out her team, and she also called them for occasional advice.

By the time she approached some of them for funding, she didn’t even need to present a full pitch. By then, they already knew enough about Stem, and about Milana as a businesswoman. Her pitch meeting with Gary Vaynerchuk — the first person to invest — ended up being just 15 minutes long.

“I brought people on my entrepreneurial journey in the beginning,” Milana says. “The biggest piece of advice I could give is to start raising a year before you start raising. Start building relationships and data points.”

Image Credits: Nathan Beckord (opens in a new window)

For each round, Milana put together a lead list — a list of potential investors who she either met socially or through business. Each time, she wanted to have at least 100 names on this list.

Powered by WPeMatico