EC Fintech

Auto Added by WPeMatico

Auto Added by WPeMatico

What happens to hot fintech startups that have benefited from a rise in consumer trading activity if regular folks lose interest in financial wagers?

That’s the question facing Robinhood, Coinbase and other trading platforms that have ridden an upward cycle. Each has performed well in recent quarters: Robinhood by securing huge payment-for-order-flow revenues, while Coinbase’s trading fees have proven incredibly lucrative, something we learned when it filed to go public.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

According to recent reporting, the consumer trading frenzy could be slowing: Bloomberg recently noted that options trading volume is slipping, Robinhood’s app store ranking is falling, and some alternative assets are also losing steam. Other reporting from the publication notes that many SPAC shares are underwater while Google trends data indicates falling consumer trading interest, perhaps limiting the inflow of new users for equities-focused apps.

There are other indications that the red-hot speculative consumer market is cooling. Bitcoin is off around 10% in the last week after a blistering rise in recent quarters. Hot stocks like Peloton, once a darling of traders, fell more than 10% yesterday alone.

But looking past price declines and other signals of market chop, volume itself at some well-known exchanges could be falling.

But looking past price declines and other signals of market chop, volume itself at some well-known exchanges could be falling.

There’s a historical precedent for such declines. Coinbase’s historical revenues, to pick an example, have proved variable based on consumer interest in cryptocurrencies, with the company benefiting from rising demand and trading activity and seeing its top line decline in periods of restrained enthusiasm.

Robinhood and its fellow free trading apps have yet to undergo a similar rise-and-fall in trading volume, I’d reckon. At least of the sort of extreme up-and-down that Coinbase endured after the 2017-2018 bitcoin boom. Our question is, what would happen to Robinhood and its cohorts if the apparent cooling in consumer trading demand continues? Let’s talk about it.

Coinbase was a famously lucrative organization during the 2017-2018 bitcoin boom.

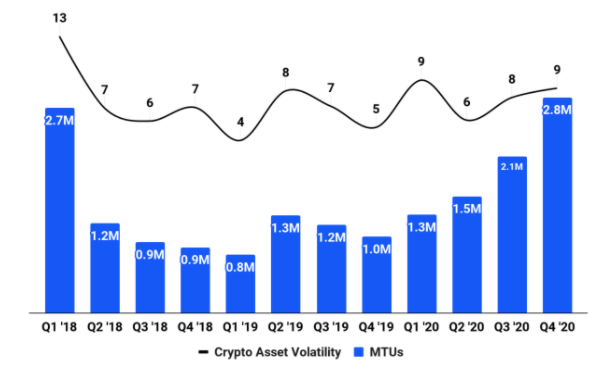

Indeed, we can see from the following chart from its S-1 filing that the company’s monthly transacting users (MTUs) dropped sharply into 2018. The percentage decline from 2.7 million to 800,000 is just over 70%.

Image Credits: Coinbase

And in case you think we’re being rude, we have a related chart from the same SEC filing that shows trading volume falling over the same period, not merely MTUs. We’re not picking a loose proxy to merely infer that trading revenue dipped at Coinbase. We can show it:

Powered by WPeMatico

Covering YC Demo Day yesterday was good fun, but I missed a few items while watching several hundred startup pitches. A few years ago, these stories might have been the biggest news of the week.

But with the venture capital market redlining its engines while public markets remain sympathetic to growing, unprofitable companies, there’s lots going on. So, as a follow-up to our first late-stage roundup that we published yesterday morning, here’s another.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

This time we’re discussing IPO news from DigitalOcean (context), Kaltura (context), Robinhood (context) and Zymergen, and big rounds for Lattice and goPuff. That’s a lot to chew on, but I’ll be brief and to the point.

We’ll commence with the IPO news and then pivot into the late-stage rounds, just in case more drops this morning while we’re typing our way through yesterday’s news. Let’s go!

We’ll commence with the IPO news and then pivot into the late-stage rounds, just in case more drops this morning while we’re typing our way through yesterday’s news. Let’s go!

Today’s most pressing news is that DigitalOcean, a provider of cloud services to small businesses, priced its IPO at $47 per share last night. That was right at the top of its public-offering price range of $44 to $47. Before counting shares reserved for its underwriters, DigitalOcean is worth just under $5 billion.

And the company raised a gross $775.5 million in the offering, giving DigitalOcean a massive war chest to pursue its vision. As the company has proved increasingly unprofitable on a GAAP basis in recent years, the extra cash isn’t a problem: DigitalOcean plans to reduce its aggregate debt load with some of the proceeds, which will improve its profitability.

The company won’t trade for hours, so we’re done with DigitalOcean for now. File it in your mind as a win, as the company raised $50 million last year at a $1.1 billion valuation (PitchBook data). That’s a quick 5x.

Next up from the IPO treadmill is Kaltura, which released a first guess of its market value as a public company. Targeting $14 to $16 per share in its impending debut, the video software company is worth around $2 billion at the top end of its range, not counting shares reserved for its underwriting banks or other shares tied up in vested options and recruited stock units (RSUs).

Powered by WPeMatico

It’s that time again! Today is Demo Day for Y Combinator’s latest accelerator batch — its largest to date, with more than 300 teams getting a minute each to pitch their companies to an audience of investors.

This is the third time YC has held its Demo Day via a Zoom livestream and the second time the entire program was entirely virtual. YC president Geoff Ralston outlined their thinking for this latest batch — and how/why they’ve expanded the program to over 300 companies — in a post this morning.

Want to see all of the companies? YC has a catalog of the entire Winter 2021 batch here (minus those that haven’t publicly launched), filterable by industry and region.

If you don’t have time to skim through it all, we’ve aggregated some of the companies that really managed to catch our eye. This is part one of two, covering our favorites from the companies that launched in the first half of the day.

As Alex Wilhelm put it last time we did one of these, “we’re not investors, so we’re not pretending to sort the unicorns from the goats.” But we do spend a lot of time talking with startups, hearing pitches and telling their stories; if you’re curious about which companies stood out, read on.

Prospa is building a neobank for small companies in Nigeria. The startup charges customers $7 per month and has reached $50,000 in monthly recurring revenue. That’s some pretty darn good traction. We found Prospa notable because Nigeria’s economy and population are rapidly growing, neobanks have succeeded in a number of markets thus far, and the company’s clear business model and early traction stood out.

And Prospa isn’t targeting a small market. It said during its presentation that there are 37 million so-called “microbusinesses” in its target country. That’s a lot of scale to grow into, and it’s really nice to hear from a neobank that isn’t going to merely pray that interchange revenues will eventually stack to the moon.

— Alex

Image Credits: Blushh

Blushh, built by a team of ex-Google, Amazon, Harvard and BCG professionals, is creating a directory of short, sensual audio stories for women in Asia. The startup believes that there is a massive unmet need for adult content created for women, instead of men, signing up 100 paying subscribers within its first month on the market.

During their pitch, co-founder Soy Hwang said Blushh wants to do for sexual wellness what “Spotify and Audible did for music and audio books.” This startup stands out because it is taking on an untapped market ridden with stigma and lack of innovation. It’s a risk on several levels, and considering the fact that many venture capitalists today still have a “vice” clause that prevents them from investing in sex tech, it will be key to see how Blushh funds itself to keep growing.

— Natasha

TechCrunch caught up with BrioHR a few weeks ago when the startup announced that it had closed a $1.3 million round. During its presentation, the company announced that it had reached $13,000 in monthly recurring revenue (MRR), or $156,000 in annual recurring revenue (ARR).

The company is building human resources software for companies in Southeast Asia, a market it considers fraught with old software and outdated business processes. The company is doing two things. First, building software to help manage and pay workers. The latter part of its work requires lots of localization, so it’s rolling out more slowly than the rest of its software.

If Southeast Asia is as fertile ground for modern HR software as the United States has been shown to be, BrioHR could find more than enough room to grow. I’m excited to see how far the company can scale its ARR with the round that we recently covered.

— Alex

Strava walked so Charge Running could, well, run. The startup, founded by a former Navy SEAL, app connoisseur and kinesiology specialist, is an app that offers live virtual running classes. The consumer play is being framed by the team as a “Peloton for running” with motivation and social engagement during the run.

Powered by WPeMatico

A big story in the finance world this morning is that the Nasdaq composite index lost ground in pre-market trading while bond yields rose. The concern is that inflation could rise, which led to bonds selling off and falling valuations for expensive stocks. So, tech stocks were broadly lower this morning.

Unlike last night, when New York-based restaurant software company Olo priced its IPO at $25 per share, sharply above its raised IPO target price range.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Today, we’re checking in on the price investors paid for a block of Olo shares before it began trading. The resulting valuation and its new revenue multiples will help us answer several questions.

First, how hot is the market for high-growth tech shares that also feature profitability? And, second, is Olo pricing ahead of, or behind, known comps? If the latter is true, it could point to a cooling enthusiasm among public investors for tech IPOs, even if the headline numbers coming from the Olo IPO are impressive.

Then we’re going to chat about Coinbase’s latest S-1/A filing, which helps provide a bit of guidance regarding how its direct listing is scooting along.

Ready to get caught up on the public-private divide that the most successful startups cross? Let’s get into it!

As a quick reminder, Olo initially targeted a $16 to $18 per-share IPO price interval. That was raised, as expected, to $20 to $22 per share. Pricing at $25, then, is a strong 56.25% greater per-share value than the low end of the company’s first estimate.

As Olo featured rapid growth (an acceleration in year-over-year revenue from 59.4% in 2019 to 94.2% in 2020), and GAAP profits (a 2019-era net loss of $8.3 million became 2020 net income of $3.1 million) in its IPO filings, the first price range it rolled out felt a bit light. The second, however, felt more appropriate.

At $25 per share, we have to do new math. Using a simple share count inclusive of the company’s underwriters’ option, Olo is worth $3.62 billion. That figure swells to $4.6 billion when a fully diluted valuation is calculated, per IPO watch group Renaissance Capital.

Powered by WPeMatico

We’re putting aside the IPO news cycle this morning to check in on the venture capital world and the fintech market in particular.

As we all know, fintech is booming: Between Robinhood and Public and M1 Finance raising competing rounds, payment-tech startup Finix moving to diversify its cap table, and ideas that work in one market finding purchase and capital in others, it’s a damn good time to build financial technology.

But perhaps even with all that recent knowledge, we’re still missing the point.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

A provisional report from data and research group CB Insights indicates that we’re not merely in a warm period for fintech funding — we are in a period of all-time record investment for so-called mega-rounds, or investments of $100 million or more inside the fintech realm.

The first quarter of 2020 had stiff competition to overcome to set a mega-round record. The preceding period, Q4 2020, for example, saw 30 fintech rounds across the globe that were worth nine figures. But, to date, Q1 2021 is ahead and is thus guaranteed to set a new record, having already bested the preceding all-time high.

This morning we’re talking big money and fintech, with a splash of early-stage digging. I asked a CB Insights analyst about what appears to be falling fintech seed deal volume. Is this the result of data reporting delays inherent to seed data, the impact of SAFEs and other sorts of notes limiting visibility into the earliest stages of venture, or just a plain-old slowdown? Let’s find out.

Per the interim CB Insights dataset, there have been some 33 fintech mega-rounds so far in 2021. For context, it’s more than 50% more such rounds in Q1 2020 and Q1 2019. Via the preliminary report, here’s the data:

Powered by WPeMatico

Olo, the New York-based fintech startup that provides order processing software to restaurants, shared its initial IPO price range this morning. The company’s debut comes ahead of the expected IPO of Toast, a Boston-based unicorn with a similar market remit.

Targeting $16 to $18 per share, Olo could raise as much as $372.6 million in its public offering.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Unlike most companies going public in recent quarters that we’ve tracked, Olo has a history of growth and profitability, making its impending pricing all the more interesting. It’s unknown if Toast is profitable, but because most venture-backed IPOs aren’t, we’re presuming it isn’t.

This morning, we’re doing our usual work: parsing the company’s pricing interval to get a valuation range for Olo. We’ll calculate both simple and fully diluted pricing and then do some quick work on its revenue scale to come to grips with its total scale.

Are investors willing to pay more for profits? And, if so, how much? This is a niche question because most IPOs look a bit more like Coursera than Olo, but it’s still worth answering.

If you’d like to follow along, you can read the new S-1 filing here. Our first look at Olo is here, and its fundraising history is here, per Crunchbase.

The company is targeting $16 to $18 per share with an expected sale of 18 million shares. The company is also reserving 2.7 million shares for its underwriters. At the upper end of its range, not counting shares reserved for its bankers, Olo could raise $324 million in its debut.

Per the company, its total number of Class A and B shares outstanding after its IPO would come to 142,012,926, or what we calculate to be 144,712,926 shares, including its underwriters’ option. Using the latter — because we tend to look for valuation extremes — Olo would be worth $2.32 billion to $2.6 billion.

But what about its fully diluted valuation? Adding in shares that are currently tied to unexercised but vested stock options bring Olo to around 188,085,714 shares. Add in the underwriters’ option and the total rises to 190,785,714 shares.

Using the latter figure, at $16 and $18 per share Olo could be worth $3.05 billion to $3.43 billion on a fully diluted basis.

Let’s find out! Digging back into Olo’s growth, we can see a business with rapidly expanding software incomes. And the same software revenues are improving in quality over time. From 2019 to 2020, for example, Olo’s “platform” revenues — a mix of subscription and transaction top line from software — grew from $45.1 million to $92.8 million. Over the same time, the company’s platform revenue saw its gross margin improve from 73.6% to 84.5%.

Powered by WPeMatico

Amidst all the hype that Lemonade (IPO), Root (IPO), Metromile (SPAC-led debut) and other insurtech players have generated in the last year, it’s been easy to forget about Oscar Health. But now that the company founded in 2012 is approaching the public markets, one of the early tech-themed insurance companies is catching up on the attention front.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

So this morning we’re digging into Oscar Health’s first IPO pricing interval, hoping to understand how the market is valuing its unprofitable health-insurance enterprise.

Recall that Oscar Health was valued at around $3.2 billion in March of 2018. That datapoint, via PitchBook, is dated. Oscar Health raised hundreds of millions since (per several venture-capital tracking databases, including Crunchbase) but we lack a final private valuation for the company.

Recall that Oscar Health was valued at around $3.2 billion in March of 2018. That datapoint, via PitchBook, is dated. Oscar Health raised hundreds of millions since (per several venture-capital tracking databases, including Crunchbase) but we lack a final private valuation for the company.

Regardless, with Oscar Health now targeting a $32 to $34 per-share IPO range, we can get our hands dirty.

Let’s get some valuation numbers and then decide if Oscar Health feels cheap or expensive at that price.

Oscar Health is looking to reap as much as $1.21 billion in its IPO, a huge sum. The company is selling 30,350,920 shares, with 4,650,000 additional shares reserved for its underwriters. Existing shareholders are selling another 649,080 shares.

This means that after the IPO, Oscar Health will have 197,037,445 Class A and B shares in circulation, or 201,687,445 after counting shares reserved for its underwriters.

Using the company’s $32 to $34 per-share range, we can calculate a valuation minimum of $6.31 billion for the company (lower share count, low-end of price range) and $6.86 billion (higher share count, high-end of price range). That’s the company’s simple IPO valuation.

Oscar Health may also sell up to $375 million of its shares at its IPO price to three different funds. The company advises that the “indication of interest is not a binding agreement or commitment to purchase,” so we can ignore it for now.

Powered by WPeMatico

Mere days after we discussed Coinbase at $77 billion and Stripe at $115 billion in the private markets, those same semi-liquid exchanges have provided a new valuation for the cryptocurrency company. It’s now $100 billion, per Axios’ reporting.

Good thing we argued last week that there could be some merit to Coinbase’s $77 billion secondary market valuation from a particular perspective. We’d look silly today if we’d mocked the $77 billion figure only for it to go up by about a third in just a few days.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Luckily for us, Axios also got its hands on a few numbers regarding Coinbase’s 2019 and 2020 financial performance, so we can get into all sorts of trouble this morning. We’ll look at the data, which stretches to the end of Q3 2020, and then do some creative extrapolating into Q1 2021 to decide whether Coinbase at $100 billion makes no sense, a little sense or perfect sense.

As always, we’re riffing, not giving investment advice. So read on if you want to noodle on Coinbase with me; its impending direct listing will be one of the year’s most watched financial events.

We’ll drag Stripe back in at the end. Given that the companies now nearly share private-market valuations, we’d be remiss to not unfairly stack them against one another. Into the breach!

Axios’ Dan Primack, a good egg in my experience, got the goods on Coinbase’s historical performance. Summarizing the bits we need, here’s what the crypto exchange got up to recently:

It’s simple to take the 2020 data that we have and extrapolate it into full-year data. Indeed, you get revenues of $921.33 million and net income of $188 million. Compared to its 2019 data, Coinbase would have managed around 74% growth while swinging steeply into the profitable domain.

That’s a killer year. But it’s actually a bit better than we are giving Coinbase credit for. Poking around volume data compiled by Bitcoinity.org, Coinbase had its biggest period of 2020 in terms of bitcoin trading volume in the fourth quarter. Thinking about Coinbase’s 2020 from a trading perspective using the same dataset, it had a great Q1, more staid Q2 and Q3, and a blockbuster Q4 that ramped to record highs at the end.

Powered by WPeMatico

If we are not careful, every entry of this column could consist of SPAC news.

Special purpose acquisition companies, or blank-check companies, whatever you prefer to call them, are enormous business today. But they aren’t the only thing going on, and we’ll get to other things shortly. Consider this an apology for having written about SPACs twice in two days.

Yesterday, we considered the rise of the VC-led SPAC and whether venture capital groups that offer seed-through-SPAC money will wind up with advantage in the market over firms that specialize on any particular startup stage. Sticking to the blank-check theme, this morning we’re looking into two SPAC-led deals, namely those involving Rover and MoneyLion.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

We’re doubling up to prevent more SPAC-related posts. And we’ve selected Rover because Chewy, another pet-themed entity, is an already-public company. As both were venture-backed, we may be able to contrast their trading performance post-debut. Sadly, Chewy is focused on pet e-commerce while Rover is more centered around pet services, but they may prove close enough for some loose comparisons.

And why chat about MoneyLion? Because it’s a heavily venture-backed fintech startup, one that TechCrunch has covered extensively. If its SPAC-assisted vault into the public markets goes well, it could smooth the same path forward for myriad other yet-private fintechs sitting atop a mountain of raised capital.

So this is a SPAC post, but as we’ll largely be looking at the financial health of two companies that we’ve heard about for ages and never got to see inside of, I hope you join me all the same.

We’re starting with the Rover investor presentation, before zipping over to MoneyLion’s own.

Rover is merging with Nebula Caravel Acquisition Corp., which is affiliated with True Wind Capital. The deal gives Rover an anticipated market cap of around $1.6 billion, with around $300 million in cash on its books.

So, how attractive is this new unicorn? You can find its investor deck here, if you want to read along as we peek.

First up, the company stresses rising use of digital services in the last year thanks to the pandemic and the fact that pet ownership is growing. Both of which are true. We’ve seen the accelerating digital transformation for both companies and consumers. And if you’ve tried to adopt a pet lately, you’ve seen how few are left waiting for forever homes.

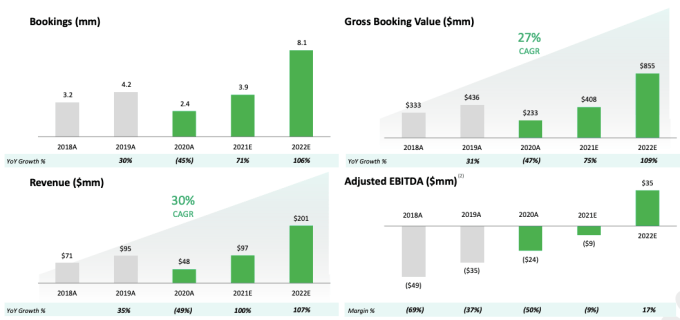

With those things behind it, you might be wondering why Rover is pursuing a SPAC-led debut as well. If its market is hot and it has previously raised venture capital, why not just go public via an IPO? Because 2020 was tough on the company.

Image Credits: Rover

Revenue dipped from $95 million in 2019 to just $48 million last year. Bookings fell from 4.2 million to 2.4 million over the same time frame, leading to gross booking value falling from $436 million in 2019 to $233 million in 2020. Why? Because everyone was stuck at home. With their pets. A situation that limited demand for Rover-delivered pet services.

Powered by WPeMatico

Metromile began trading as a public company yesterday. Its exit from the private market was accelerated by its decision to combine with a special purpose acquisition company, or SPAC.

Such transactions have exploded in popularity in recent years, bridging the gap between a host of richly valued private companies and endless bored capital. SPACs raise cash, go public and then merge with a private entity. The SPAC then dissolves itself into the combined entity, a process that often includes an additional slug of money (PIPE) for good measure.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

SPAC-led debuts can move faster than a traditional IPO, making them attractive to companies in a hurry. And with more visibility into how much capital might be raised than during a traditional public-offering pricing run, they can smooth worries amongst target-companies regarding how much cash they can attract by leaving the private-market fold.

Metromile is hardly the final company we expect to debut this year via a SPAC. The list is long and may include fellow neoinsurance company Hippo. (Hippo declined to comment on the matter.)

Metromile is hardly the final company we expect to debut this year via a SPAC. The list is long and may include fellow neoinsurance company Hippo. (Hippo declined to comment on the matter.)

But with many more SPACs coming our way, we took Metromile’s debut as a learning moment. To that end, we got on the horn with CEO Dan Preston to chat about what the day meant for his company, and to elicit a note or two on the SPAC process for our own enjoyment.

TechCrunch asked Preston about the SPAC world and how his combination came about. He said his firm started by dipping its toe into the blank-check waters, kicking off with a small set of conversations, chats that quickly gathered traction.

But don’t take that to mean that any company will elicit a similar market response. Preston said SPACs are designed for a specific class of company; namely those that want or need to share a bit more story when they go public. Younger companies, in other words, for whom a traditional S-1 filing might not be provide a sufficient summation of its potential.

Powered by WPeMatico