EC Fintech

Auto Added by WPeMatico

Auto Added by WPeMatico

Jen Young and Jeff Cavins were sitting in a beige conference room at a downtown Vancouver hotel, wasting away under fluorescent lights, an endless PowerPoint and a pair of sad Styrofoam cups of coffee between them. Young was there on a marketing contract. Cavins was a board member. They shared one of those looks that only couples can understand. It said: There’s got to be something better than this.

With 40 years of running technology companies under Cavins’ belt and a successful ad agency career under Young’s, the two decided to craft a business around their shared passion of being out in nature. When they realized there are more than 20 million recreational vehicles all across the U.S., most of which are used only a handful of days, they saw an opportunity. They asked themselves: How do we create memorable outdoor experiences and make them available to everybody?

For seven months, the couple traveled across the U.S. to do market research on travelers and RV owners to form the basis of their company.

The sharing economy of Uber, Lyft and Airbnb had already laid the groundwork. Why not open it up to RVs?

In 2014, Young and Cavins invested their life savings into Outdoorsy, sold their homes and jumped into an Airstream Eddie Bauer trailer. For seven months, the couple traveled across the U.S. to do market research on travelers and RV owners to form the basis of their company.

In June, Outdoorsy raised $90 million in a Series D led by ADAR1 Partners, as well as an additional $30 million in debt financing from Pacific Western Bank. The money will be used in large part to accelerate the growth of Outdoorsy’s insurtech business, Roamly. In the same month, the company announced a partnership with glamping company Collective Retreats to expand its outdoor offerings.

The following interview, part of an ongoing series with founders who are building transportation companies, has been edited for length and clarity.

You’ve taken a personal approach to your business, spending months in the research phase actually living in an RV and interviewing RV owners and their families around the country. How do you think that’s shaped your business?

Jen Young: When we lived on the road, we had to experience that customer experience every day for hundreds of days. So this is where we were able to pick up and identify what the biggest pain points were on the renter and the owner side and start tackling those first.

For example, we understood what was most important from an insurance perspective because we could hear the voices of renters and owners — they consider these things their babies in many cases.

The owners that are more entrepreneurial-minded, they consider them more of a business asset, but both of them want to know, “What am I going to get for liability insurance? Comp and collision? Interior damage?” The detailed list of those things became the beginning of the product roadmap, as well as itemizing what things have to occur for a good guest experience.

In what ways have you had to pivot your model based on how people have used your platform?

Cavins: One of the things we learned is most renters don’t want to drive these things, so owners started to do delivery, which became very popular on our platform. Sixty percent of all owners now will just deliver and set up for you so you can arrive at your campsite and everything’s just done. Your chairs are out, your barbecue is out, your awning is out and maybe a bottle of champagne in your fridge for you.

When Jen and I were traveling last year, we saw that most of the American landscape of campgrounds and campsites were overbooked. People couldn’t get their reservations closed the way that you would expect in a world of technologically evolved industries, and we thought there had to be something better in terms of the customer experience for camping, which really catalyzed our investment in glamping company Collective Retreats.

Powered by WPeMatico

News broke this morning that Revolut, a U.K.-based consumer fintech player, raised a Series E round of funding worth $800 million at a valuation of $33 billion. Those figures are breathtaking not only due to their sheer scale, but also thanks to their radical divergence from Revolut’s preceding funding event.

At times, The Exchange, TechCrunch’s markets-and-startups column, runs into two topics worth exploring in a single day. Today is such a day. You can check out our earlier notes on the buy now, pay later startup market and Apple’s entrance into the BNPL space here. Now, let’s talk about neobanks.

As TechCrunch’s Ingrid Lunden wrote earlier today concerning the news:

This latest Series E is being co-led by Softbank Vision Fund 2 and Tiger Global, who appear to be the only backers in this round. It comes on the heels of rumors earlier this month Revolut was raising big. Revolut last raised about a year ago, when it closed out a Series D at $580 million, but what is stunning is how much its valuation has changed since then, growing 6x (it was $5.5 billion last year).

Stunning indeed.

Lunden also went on to report on the company’s changing financial picture based on Revolut’s recently released 2020 results. In this entry, we’re digging more deeply into those financial results and usage metrics detailed by the fintech megacorn.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The picture that emerges is one of a company with a rapidly improving financial image, albeit with some blank spaces regarding recent customer growth.

Powered by WPeMatico

Technology plays a huge role in nearly every aspect of financial services today. As the world moved online, tools and infrastructure to help people manage their money and make payments have burgeoned the world over in the past decade.

With much of the finance world now leveraging technology to conduct business, predict trends and deliver services, financial services regulators are also developing new technologies to monitor markets, supervise financial institutions and conduct other administrative activities. The emergence of purpose-built technologies to facilitate regulator oversight has, over the past few years, garnered its own moniker of supervisory technology, or suptech.

Interest in suptech is proliferating across the globe thanks to a diverse set of prudential and conduct regulators. A sampling of regulators developing suptech include the FDIC, CFPB, FINRA and Federal Reserve in the U.S.; the U.K.’s FCA and Bank of England; the National Bank of Rwanda in Africa; as well as the ASIC, HKMA and MAS in Asia. Several “super regulators” are also engaged in suptech efforts such as the Bank of International Settlements, the Financial Stability Board and the World Bank.

The strides in suptech demonstrate that creative thinking coupled with experimentation and scalable, easily accessible technologies are jump-starting a new approach to regulation.

In this post, we’ll examine a few core suptech use cases, consider its future and explore the challenges facing regulators as the market matures. The uses are diverse, so we’ll focus on three key areas: regulatory reporting, machine-readable regulation, and market and conduct oversight.

A quick general note: Nearly every financial services regulator is engaged in some type of suptech activity and the use cases discussed in this article are intended as a sample, not a comprehensive list.

As a preliminary matter, we should quickly survey a few definitions of suptech to frame our understanding. Both the World Bank and BIS have offered definitions that provide useful outlines for this discussion. The World Bank states that suptech “refers to the use of technology to facilitate and enhance supervisory processes from the perspective of supervisory authorities.” It’s a little circular, but helpful.

The BIS defines suptech as “the use of technology for regulatory, supervisory and oversight purposes.” This is a similarly loose definition that describes the broader scope better.

Regardless of differences on the margins, the “sup” in these suptech definitions acknowledges the primacy of the idea that regulators’ objectives are to oversee the conduct, structure, and health of the financial system. Suptech technologies facilitate related regulatory supervision and enforcement processes.

Regulatory reporting refers to a broad swath of activities such as financial firms providing trading data to regulatory authorities and regulators’ analysis of financial data or corporate information to determine the projected health or potential risks facing an institution or the market.

The MAS and FDIC are incorporating transactional and financial data reported by firms as a means to assess their financial viability. The MAS, in conjunction with BIS, has run tech sprints soliciting new ideas relating to regulatory reporting, while the FDIC has “a regulatory reporting solution that would allow ‘on-demand’ monitoring of banks as opposed to being constrained by ‘point-in-time’ reporting. This project is particularly targeted at smaller, community banks that provide only aggregated data on their financial health on a quarterly basis.”

The HKMA recently outlined its three-year plan for the development of suptech, which includes developing an approach to “network analysis.” The HKMA will analyze reporting data related to corporate shareholding and financial exposure to bring them “to life as network diagrams, so that the relationships between different entities become more apparent. Greater transparency of the connections and dependencies between banks and their customers will enable HKMA supervisors to detect early warning signals within the entire credit network.”

These reporting initiatives touch on a theme regulators have continuously struggled with: How to regulate markets and firms based on a reactive approach to historical data. Regulation and enforcement are often retrospective activities — examining past behavior and data to decide how to sanction an organization or develop a regulatory framework to govern a particular type of activity or financial product. This can result in an approach to regulation too rooted in past failures, which might lack the flexibility to anticipate or adapt to emerging risks or financial products.

Powered by WPeMatico

In the wake of Coinbase’s direct listing earlier this year, other crypto companies may be looking to go public sooner than later. That appears to be the case with Circle, a Boston-based technology company that provides API-delivered financial services and a stablecoin.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Circle will not direct list or pursue a traditional IPO. Instead, the company is combining with Concord Acquisition Corp., a SPAC, or blank-check company. The transaction values the crypto shop at an enterprise value of $4.5 billion and an equity value of around $5.4 billion.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

Circle’s SPAC presentation details a company whose core business deals with a stablecoin — a crypto asset pegged to an external currency, in this case, the U.S. dollar — and a set of APIs that provide crypto-powered financial services to other companies. It also owns SeedInvest, an equity crowdfunding platform, though Circle appears to generate the bulk of its anticipated revenues from its other businesses.

For more on the deal itself, TechCrunch’s Romain Dillet has a piece focused on the transaction. Here, we’ll dig into the company’s investor presentation, talk about its business model, and riff on its historical and anticipated results and valuation multiples.

In short, we get to have a little fun. Let’s begin.

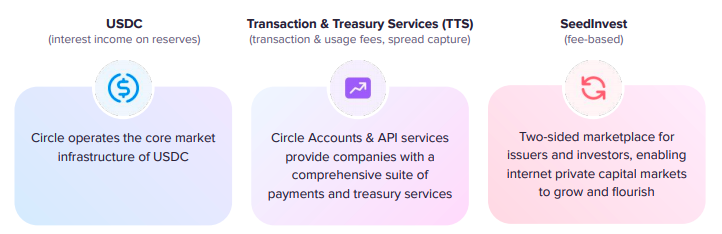

As noted above, Circle has three main business operations. Here’s how it describes them in its deck:

Image Credits: Circle investor presentation

Let’s consider each one, starting with USDC.

Stablecoins have become popular in recent quarters. Because they are pegged to an external currency, they operate as an interesting form of cash inside the crypto world. If you want to have on-chain buying power, but don’t want to have all your value stored in more volatile, and tax-inducing, cryptos that you might have to sell to buy anything else, stablecoins can operate as a more stable sort of liquid currency. They can combine the stability of the U.S. dollar, say, and the crypto world’s interesting financial web.

Powered by WPeMatico

This afternoon Robinhood filed to go public. TechCrunch’s first look at its results can be found here. Now that we’ve done a first dig, we can take the time to dive into the company’s filing more deeply.

Robinhood’s IPO has long been anticipated not only because there are billions of dollars in capital riding on its impending liquidity, but also because the company became something of a poster child for the savings and investing boom that 2020 saw and the COVID-19 pandemic helped engender.

The consumer trading service’s products became so popular and enmeshed in popular culture thanks to both the “stonks” movement and the larger GameStop brouhaha, that the company’s public offering carries much more weight than that of a more regular venture-backed entity. Robinhood has fans, haters, and many an observer in Congress.

Regardless of all that, today we are digging into the company’s business and financial results. So, if you want to better understand how Robinhood makes money, and how profitable or not it really is, this is for you.

We will start with a more in-depth look at growth and profitability, pivot to learning about the company’s revenue makeup, discuss a risk factor or two, and close on its decision to offer some of its own shares to its users. Let’s go!

Before we get into the how of Robinhood’s growth, let’s discuss how big the company has become.

The fintech unicorn’s revenue grew from $277.5 million in 2019 to $958.8 million in 2020, which works out to growth of around 245%. Robinhood expanded even more quickly in the first quarter of 2021, scaling from year-ago revenue of $127.6 million to $522.2 million, a gain of around 309%.

Those are numbers that we frankly do not see often amongst companies going public; 300% growth is a pre-Series A metric, usually.

Powered by WPeMatico

Brazil is a country riven with economic contradictions. It has one of the largest and most profitable banking industries in Latin America, and is among the world’s most developed financial markets. Financial transactions that would take days to process in the United States through ACH happen instantaneously in Brazil. This sophistication, however, masks a backward state of affairs plagued by appalling customer service, exorbitant fees and lack of banking access for many.

The country’s financial system is volatile and often leaves its citizens with few or no alternatives. According to an HBS case study, “in December 2018 the interest rate in Brazil for corporate loans was 52.3%, for consumer loans it was 120.0% and for credit card indebtedness it was 272.42%.” Those rates are many multiples higher compared to figures in neighboring countries.

Brazil’s banking system is a massive market, and one ill-served by incumbents. If someone could thread the needle of product development, strategy and political horse trading required to build a bank in a country where it is nearly impossible for foreigners to own or invest in a bank, it would be one of the great startup and economic success stories of this century.

Nubank is on its way to realizing that objective. Its story is one of unmitigated success, even by the standards of our EC-1 series on high-flying companies and their hard-learned lessons. Just last week, this Brazilian credit card and banking fintech raised a $750 million round led by Berkshire Hathaway at a $30 billion valuation, becoming one of the most valuable startups in the world. It has 40 million users across Brazil, as well as Mexico and Colombia.

Yet, it’s a startup with a CEO and co-founder who isn’t Brazilian, didn’t speak the local language of Portuguese, hadn’t started a company before, and didn’t really know a lot about banking to begin with. This is a story of how raw execution, a “faster, faster” mentality and a fanaticism for making customer experience as enjoyable as a trip to Disney World can completely change the history of an industry — and country — forever.

Our lead writer for this EC-1 is Marcella McCarthy. McCarthy, who spent significant time in Brazil growing up and is trilingual in English, Spanish and Portuguese, has been covering the LatAm and Miami ecosystems for TechCrunch with an eye to the disruption underway in these interconnected regions. The lead editor for this package was Danny Crichton, the assistant editor was Ram Iyer, the copy editor was Richard Dal Porto, and illustrations were drawn by Nigel Sussman.

Nubank had no say in the content of this analysis and did not get advance access to it. McCarthy has no financial ties to Nubank or other conflicts of interest to disclose.

The Nubank EC-1 comprises four main articles numbering 9,200 words and a reading time of 37 minutes. Here’s what’s in the bank:

We’re always iterating on the EC-1 format. If you have questions, comments or ideas, please send an email to TechCrunch Managing Editor Danny Crichton at danny@techcrunch.com.

Powered by WPeMatico

For most startups, the hardest early challenge is identifying a market and a product to serve it. That wasn’t the case for Nubank CEO David Velez, who understood the massive potential for success if he could break into Latin America’s most valuable economy with even a moderately modern banking offering.

Instead, the challenge was how to rebuild the concept of a bank in a country where banking is widely hated, all while the incumbents heavily entrenched with the state worked to block every move.

Nubank knew its market and geography, and through tenacious fundraising, inventive marketing and product development, and a series of contrarian hires, Velez and his team stripped bare the morass of Brazilian banking to build one of the world’s great fintech companies.

The challenge was how to rebuild the concept of a bank in a country where banking is widely hated, all while the incumbents heavily entrenched with the state worked to block every move.

In the first part of this EC-1, I’ll look at how Velez brought his skills and experience to bear on this market, how Nubank was founded in 2013, and how the team brought a Californian rather than Brazilian vibe to their first office on — no joke — California Street, in a neighborhood called Brooklin in the city of São Paulo.

The idea of being his own boss was ingrained in Velez from his earliest days in Colombia, where he grew up in an entrepreneurial family, with a father who owned a button factory. “I heard from my dad over and over again that you need to start your own company,” Velez said.

But years would pass and Velez still had no idea what he wanted to do. To “kill time,” and also to surround himself with entrepreneurial energy, Velez attended Stanford University — partially financed by the sale of some livestock — and then worked as an analyst at Goldman Sachs and Morgan Stanley before switching to venture capital at General Atlantic and Sequoia.

Powered by WPeMatico

As we mentioned in part 1 of this EC-1, David Velez had two key co-founding roles he needed to fill to get started building Nubank. For one, he needed a CTO to lead the engineering side of the business, as Velez didn’t have an engineering background.

Edward Wible, an American computer science graduate who spent most of his career in private equity, would take that responsibility. He didn’t bring years of coding experience, but he had qualities that Velez considered more important: A strong belief in the potential of the product and an equally intense commitment to working on it.

Given the occasionally hostile reaction of most incumbent banks to their customers in Brazil, Nubank’s starkly contrasting openness and transparency has garnered a huge following.

That left an even more important role to fill — one that was much harder to define. This other co-founder would need to blend knowledge of the Brazilian market and local savvy with expertise in banking, all while embodying a Silicon Valley ethos of focusing on customers. This person would also have to work in São Paulo for minimal wages out of a small office with just one bathroom, all in the belief that their equity (both stock and sweat) would one day be worth it.

Velez would eventually stumble upon Cristina Junqueira, who was qualified to do all this, and much, much more.

“Once someone said I was the glue of the operation, and that someone else was the brains. And I said, ‘No, I’m the glue and the brains, and I bet my brain is even better than his,”’ Junqueira said.

Junqueira didn’t just lead Nubank’s drive into the Brazilian market, she also upended age-old notions of what it means to be a 21st-century bank. Her inspiration was nothing short of Disney, and her mission was to create a bank as popular as the magical kingdom itself.

A bank. As popular as Disney. Sounds like a fairy tale, frankly.

Unlike her co-founders Velez and Wible, Junqueira grew up in Nubank’s home market of Brazil. The eldest of four sisters, she remembers her parents — both dentists — always assiduously working to maintain their practice.

Their work ethic trickled down, but so did responsibility. As the oldest at home, she was forced to grow up quickly and take on responsibilities from an early age. “I remember being 11 years old and doing grocery shopping for the month,” she said. “I did everything very young.”

Powered by WPeMatico

As we saw in parts 1 and 2 of this EC-1, by mid-2013, Nubank CEO David Velez had most of what he needed to get started. He’d brought on two co-founders, assembled ambitious engineering and operations teams, raised $2 million in seed funding from Sequoia and Kaszek, rented a tiny office in São Paulo, and was armed with a mission to deliver the kind of banking services that customers in a market as large and lucrative as Brazil’s should expect.

Despite being named Nubank, however, the startup couldn’t actually be a bank: Brazil’s laws made it illegal at the time for a foreigner-run company to operate a bank. That restriction required the team to develop an inventive product strategy to find a foothold in the market while they waited for a license directly from the country’s president.

Nubank was so adamant about differentiating itself from other banks that it chose Barney purple for its brand color and first credit card.

Nubank therefore pursued a credit card as its first offering, but it had to race against a clock counting quickly down to zero. At the time, Brazil didn’t have ownership restrictions on this product segment like it did with banking, but new rules were coming into force in just a few months in May 2014 that would block a company like Nubank from launching.

The company needed to execute rapidly over the next eight months if it wanted to be grandfathered into the existing regulations. The speed of operations was frantic to say the least, and the company would go on to work even faster, ultimately propelling itself into the stratosphere of fintech startups.

It’s easy to assume that the name Nubank refers to “new bank,” but that’s not really what the founders were going for. The word “nu” in Portuguese means “naked,” and Velez and his team wanted the name to reflect their vision: To build a 21st-Century bank without any of the shackles imposed by the traditional banks in Brazil.

The team wanted to offer services to as many people as possible, as there is a huge wealth gap in Brazil, where the minimum wage is around $200 a month.

Launching with just a credit card was both a strategic and practical business decision. Credit cards were widely used in the country, and everyone understood how they worked. Additionally, you could only use credit cards to shop online in Brazil, because debit cards weren’t accepted.

Powered by WPeMatico

Nubank’s first office, on California Street in the Brooklin neighborhood of São Paulo, makes for a great beginning to the company’s story. It wasn’t a Silicon Valley garage, but this tiny, one-bathroom rented house, where 30 people worked insane hours to push out the company’s debut credit card, lends just as well to an image of entrepreneurial spirit and drive.

As Nubank continues to make international waves, more and more VC investors are taking a look at the Brazilian ecosystem and could potentially fund other upstarts in the years to come.

But as Nubank’s story continued, the team eventually had to move out of that early office, and the next several offices, too. Eventually Nubank had to relocate to an eight-story building in São Paulo, which houses a large part of the company’s now 3,000-person team.

The startup reached decacorn status in far less than a decade, and it is growing faster than ever. When I interviewed CEO David Velez back in January to discuss Nubank’s $400 million Series G, he said, “We’ve gone from 12 million customers in 2019 to 34 million solely based on word of mouth.” By September last year, the company was onboarding 41,000 new customers per day.

In the five months since our interview, Nubank has managed to rope in a whopping 6 million customers to reach 40 million. It’s now valued at $30 billion.

Nubank’s present day headquarters in São Paulo, Brazil. Image Credits: NELSON ALMEIDA/AFP / Getty Images

Getting there hasn’t been easy. The company’s three co-founders, Velez, Edward Wible and Cristina Junqueira, had to make key strategic decisions about how to scale themselves to retain the company’s lead in the neobanking market. That lead is getting tougher to sustain every day. Nubank’s proliferating offerings and broader geographical remit has painted a massive target on its back, and a wide number of competitors have cropped up to run on the paths it pioneered.

Like most Disney films, a fairy-tale ending seems in order, but it’ll take a few more rotations of the film wheel to get to the ending.

For the co-founding trio, it became increasingly clear that Nubank’s growing scale demanded critical strategic decisions on how to bring order to the company.

By 2018, the company had thousands of employees, millions of customers, and they still didn’t have a head of HR. Growth until then had been somewhat unstructured. According to Junqueira, waiting so long to hire a head of HR was one of their early mistakes, because it stunted their ability to grow. “[Good] people continue to be our biggest bottleneck,” she says.

Powered by WPeMatico