EC Fintech

Auto Added by WPeMatico

Auto Added by WPeMatico

The U.S. insurance technology market is hot and has been for years now. Back in early 2020, to pick an example, TechCrunch reported on a wave of funding events among domestic insurtech marketplaces. Those companies have since gone on to raise hundreds of millions of dollars more.

And after a long period of incubation, we’ve seen neoinsurance players from the U.S. like Root and Metromile go public. Hippo is working to join the cohort.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

So from the perspective of venture capital activity, startup growth and exits, insurtech is proving itself in the States. Even if growth remains the name of the game in insurance tech and profits are often scarce.

What about other markets? The recent Wefox round caught The Exchange’s eye. A $650 million insurtech round would have commanded our attention regardless of its location. But to see a European insurance technology startup raise that amount of cash made us wonder if there’s as much money present for the EU market’s insurtech startups as we’ve seen here in the U.S.

After all, with business-focused neoinsurance provider Embroker raising a big round this week in the United States, to pick an example, it seems that attacking the massive and antiquated insurance market is good startup sport. Why wouldn’t that concept apply to Europe?

After all, with business-focused neoinsurance provider Embroker raising a big round this week in the United States, to pick an example, it seems that attacking the massive and antiquated insurance market is good startup sport. Why wouldn’t that concept apply to Europe?

To find out more, we got in touch with a number of VCs from Europe to hear their perspectives on what’s happening on the ground, including folks from Accel, Astorya.vc and Insurtech Gateway. To ground us, we collated the biggest recent rounds from the EU insurance technology market. Let’s go!

Venture capitalists and startup founders get paid when they generate an exit. Lately, exits in the space have featured a number of IPOs.

The older a startup gets, the more it has to deal with public-market investors. Crossover funds and the like make their appearance before unicorns go public. And then former startups have to pitch not the venture capital market, but the public markets. It’s a different game.

That’s the impression that The Exchange got chatting with the CEO of Root, Alex Timm, this earnings cycle. He noted that public tech-focused investors don’t always grok the insurance elements of his business, while insurance investors don’t always grok the tech side of Root.

Powered by WPeMatico

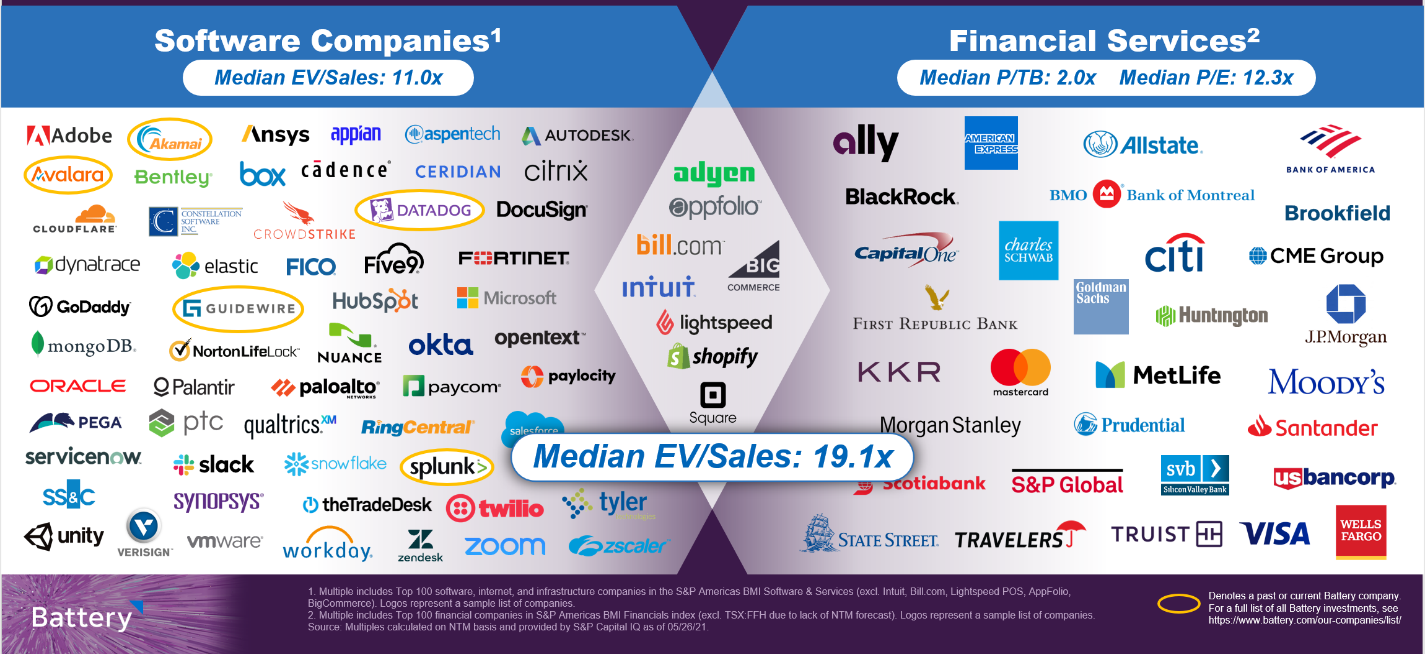

If money is the ultimate commodity, how can fintechs — which sell money, move money or sell insurance against monetary loss — build products that remain differentiated and create lasting value over time?

And why are so many software companies — which already boast highly differentiated offerings and serve huge markets— moving to offer financial services embedded within their products?

A new and attractive hybrid category of company is emerging at the intersection of software and financial services, creating buzz in the investment and entrepreneurial communities, as we discussed at our “Fintech: The Endgame” virtual conference and accompanying report this week.

These specialized companies — in some cases, software companies that also process payments and hold funds on behalf of their customers, and in others, financial-first companies that integrate workflow and features more reminiscent of software companies — combine some of the best attributes of both categories.

Image Credits: Battery Ventures

From software, they design for strong user engagement linked to helpful, intuitive products that drive retention over the long term. From financials, they draw on the ability to earn revenues indexed to the growth of a customer’s business.

Fintech is poised to revolutionize financial services, both through reinventing existing products and driving new business models as financial services become more pervasive within other sectors.

The powerful combination of these two models is rapidly driving both public and private market value as investors grant these “super” companies premium valuations — in the public sphere, nearly twice the median multiple of pure software companies, according to a Battery analysis.

The near-perfect example of this phenomenon is Shopify, the company that made its name selling software to help business owners launch and manage online stores. Despite achieving notable scale with this original SaaS product, Shopify today makes twice as much revenue from payments as it does from software by enabling those business owners to accept credit card payments and acting as its own payment processor.

The combination of a software solution indexed to e-commerce growth, combined with a profitable payments stream growing even faster than its software revenues, has investors granting Shopify a 31x multiple on its forward revenues, according to CapIQ data as of May 26.

Before even talking about how investors should value these hybrid companies, it’s worth making the point that in both private and public markets, fintechs have been notoriously hard to value, fomenting controversy and debate in the investment community.

Powered by WPeMatico

An estimated 41 million Americans say they need life insurance but have yet to purchase coverage. Despite this awareness among consumers, the Life Insurance Marketing and Research Association estimates a $12 trillion coverage gap, with about 50% of millennials planning to purchase coverage within the next year.

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution. It’s imperative for companies to consider product lines and partnerships to expand markets, create new revenue streams and provide added value to their customers.

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution.

Connecting consumers with products they need through channels they already know and trust is both a massive revenue opportunity and a social good, providing financial resilience to families at a time when they need it most.

The concept of digitally bundling financial products in a packaged offering to a customer is certainly not new — but it is for the life insurance space.

Embedded finance uses technology and operations infrastructure to offer products and services through entities that may not be financial institutions at all. Think of embedded finance like on-demand shopping; customers benefit from both the transaction (buying financial protection for their families) and the convenience it provides (from whatever platform they are currently engaging with).

Similar to how Amazon saves shoppers 75 hours a year, bundling life insurance gives consumers back time in their day and can improve their financial health.

Powered by WPeMatico

As expected, Bill.com is buying Divvy, the Utah-based corporate spend management startup that competes with Brex, Ramp and Airbase. The total purchase price of around $2.5 billion is substantially above the company’s roughly $1.6 billion post-money valuation that Divvy set during its $165 million, January 2021 funding round.

Divvy’s growth rate tells us that the company did not sell due to performance weakness.

Per Bill.com, the transaction includes $625 million in cash, with the rest of the consideration coming in the form of stock in Divvy’s new parent company.

Bill.com also reported its quarterly results today: Its Q1 included revenues of $59.7 million, above expectations of $54.63 million. The company’s adjusted loss per share of $0.02 also exceeded expectations, with the street expecting a sharper $0.07 per share deficit.

The better-than-anticipated results and the acquisition news combined to boost the value of Bill.com by more than 13% in after-hours trading.

Luckily for us, Bill.com released a deck that provides a number of financial metrics relating to its purchase of Divvy. This will not only allow us to better understand the value of the unicorn at exit, but also its competitors, against which we now have a set of metrics to bring to bear. So, this afternoon, let’s unpack the deal to gain a better understanding of the huge exit and the value of Divvy’s richly funded competitors.

The following numbers come from the Bill.com deck on the deal, which you can read here. Here are the core figures we care about:

This lets us price the company somewhat. Divvy sold for around 25x its current revenue rate. That’s a software-level multiple, implying that the company has either incredibly strong gross margins, or Bill.com had to pay a multiples-premium to buy the company’s future growth today. I suspect the latter more than the former, but we’ll have to scout for more data when Divvy shows up in Bill.com results after the deal closes; that data is a few quarters away.

Powered by WPeMatico

Domm Holland, co-founder and CEO of e-commerce startup Fast, appears to be living a founder’s dream.

His big idea came from a small moment in his real life. Holland watched as his wife’s grandmother tried to order groceries, but she had forgotten her password and wasn’t able to complete the transaction.

“I just remember thinking it was preposterous,” Holland said. “It defied belief that some arbitrary string of text was a blocker to commerce.”

So he built a prototype of a passwordless authentication system where users would fill out their information once and would never need to do so again. Within 24 hours, tens of thousands of people had used it.

Nothing beats building human networks. That’s the way that you’re going to get this done in terms of fundraising.

Shoppers weren’t the only ones on board with this idea. In less than two years, Holland has raised $124 million in three rounds of fundraising, bringing on partners like Index Ventures and Stripe.

Although the success of Fast’s one-click checkout product has been speedy, it hasn’t been effortless.

For one thing, Holland is Australian, which means he started out as a Silicon Valley outsider. When he arrived in the U.S. in the summer of 2019, he had exactly one Bay Area contact in his phone. He built his network from the ground up, a strategic process he credits to one thing: hard work.

On an episode of the “How I Raised It” podcast, Holland talks about how he built his network, why it’s important — not just for fundraising but for building the entire business — and how to avoid the mistakes he sees new founders make.

Holland’s primary strategy in building networks sounds like an obvious one — reach out to relevant people.

“When I first got to the States, I wanted to build networks,” Holland said, “but I didn’t really know anyone here in the Bay Area. So I spent a lot of time reaching out to relevant people — people working in payments, people working in technology, people working in identity authentication — just really relevant people in the space working in Big Tech who were building large-scale networks.”

One of the people Holland connected with was Allison Barr Allen, then the head of global product operations at Uber. Barr Allen managed her own angel investment fund, but Holland wasn’t actually looking for money when he reached out to her. He was much more interested in her perspective as the leader of an enormous financial services operation.

Powered by WPeMatico

It’s a big morning for fintech startups today: Flywire, a Boston-based magnet for venture capital, has filed to go public.

Flywire is a global payments company that attracted more than $300 million as a startup, according to Crunchbase, most recently raising a $60 million Series F last month. We don’t have its most recent valuation, but PitchBook data indicates that the company’s February 2020, $120 million round valued Flywire at $1 billion on a post-money basis.

So what we’re looking at here is a fintech unicorn IPO. A great way to kick off the week, to be honest, though I’d thought that Robinhood would be the next such debut.

Fintech venture capital activity has been hot lately, which makes the Flywire IPO interesting. Its success or failure could dictate the pace of fintech exits and fintech startup valuations in general, so we have to care about it.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Regardless, we’re doing our regular work this morning. First, what does Flywire do and with whom does it compete? Then, a closer look at its financial results as we hope to get our hands around its revenue quality, aggregate economics and growth prospects.

After that, we’ll discuss valuations and which venture capital groups are set to do well in its flotation. The company had a number of backers, but Spark Capital, Temasek, F-Prime Capital and Bain Capital Ventures made the major shareholder list, along with Goldman Sachs. So, a number of firms and funds are hoping for a big Flywire exit. Let’s dig in.

Flywire is a global payments company. Or, as it states in its S-1 filing, it’s “a leading global payments enablement and software company.” And it thinks that its market, and by extension itself, has lots of room to grow. While “substantial strides [have been] made in payments technology in the retail and e-commerce industries,” the company wrote, “massive sectors of our global economy—including education, healthcare, travel, and business-to-business, or B2B, payments—are still in the early stages of digital transformation.”

That’s the same logic behind Stripe’s epic valuation and the rising value of payments-focused companies like Finix.

Powered by WPeMatico

To close out the week, a short meditation on value, or, more precisely, how assets are valued in today’s markets.

Do you recall the pre-direct-listing hype Coinbase enjoyed? After reporting its estimated first-quarter financial performance, interest in the domestic cryptocurrency trading giant ran red-hot.

When Coinbase set a $250 per-share direct listing reference price, it was broadly viewed as modest, if not downright low. Of course, a reference price is just that — a reference — so it wasn’t too big a deal. But it also wasn’t surprising that Coinbase shares traded as high as $429.54 on their first day, according to Yahoo Finance data.

Coinbase equity hasn’t topped $400 in any following day and is now under the $300 mark, with more declines set to arrive as trading commences. Its reference price looms, and suddenly a price that felt intensely conservative before Coinbase began to trade is starting to look nearly reasonable.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

There have been other notable declines in value among some recently public, more technologically differentiated companies. The Exchange has watched with something akin to polite confusion as the value of Root, a neoinsurance company, fell to a third of its public-market highs after going public, even though it beat growth expectations in its most recent quarterly report.

We could toss UiPath into our trend of wildly meandering value. The company’s initial IPO price range targeted a price as low as $43 per share. Today it’s worth $76.75 per share in pre-market trading.

No one knows what anything is worth, again. This is the feeling I get while watching the markets work to determine how to value assets as diverse as startups crossing the private-public divide to the value of Bitcoin, which was supposed to keep going up. Until it suddenly reversed gear.

Frankly, we’re still dealing with new-enough models — or big-enough guesses about the future baked into business models — that it’s hard to really value the most uncertain (and therefore most exciting) companies, let alone cryptocurrencies. Let’s discuss.

Powered by WPeMatico

The investment landscape for insurtech startups is off to a hot start in Q2 2021. Since the end of the first quarter, we’ve seen several players in the broad startup category announce new capital, including Clearcover, Alan, Next Insurance and The Zebra.

But, as anyone who’s familiar with startups that offer insurance-related products and services knows, the sector is enough of a mixed bag that one needs to segment down to get clarity on how constituent companies are performing. So while Clearcover’s $200 million round from last week, Next Insurance’s $250 million round from the first of the month and Alan’s $220 million round from yesterday are interesting, this morning we’re going to focus a bit more on The Zebra’s side of the insurtech house.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The Exchange divides insurtech startups into three categories: neoinsurance providers, insurtech marketplaces and insurtech enablers. (You can see why we need to segment the insurtech genre!)

Briefly, neoinsurance providers are companies like Root, Metromile and Next Insurance, which use technology to underwrite and sell insurance in an updated manner; these companies also often have optimized mobile experiences.

Marketplaces like The Zebra, Gabi, Insurify and others provide a way for consumers to better identify their insurance options. And, finally, there are companies like AgentSync, which fit neatly into our third category of firms that help other companies in the insurance business digitize their operations or otherwise modernize.

Insurtech marketplaces came back into our view when The Zebra put together a $150 million Series D earlier this month and released a host of metrics regarding its growth, and Insurify dropped the news that it is partnering with Toyota.

Insurtech marketplaces came back into our view when The Zebra put together a $150 million Series D earlier this month and released a host of metrics regarding its growth, and Insurify dropped the news that it is partnering with Toyota.

This morning, let’s discuss insurtech’s 2020 as a whole, peek at some preliminary 2021 venture data and then dive deep into what we’ve collected regarding growth among insurtech marketplace players. The Exchange has data and other details from The Zebra, Insurify, Wefox and more.

Covering longitudinal progress of specific startup categories is one of our favorite things to do. So, please, walk with us!

PitchBook data regarding the insurtech category in 2020 underscores how large the startup niche has grown. Per the data company, $18.3 billion was spent last year on insurtech startups across venture capital, private equity and M&A activity. That was a billion dollars under its 2019 result, but given the pandemic’s onset, 2020’s final result is somewhat impressive — who expected insurance investing to hold up during an unprecedented global catastrophe?

This year is proving lucrative for the insurtech market, at least from a venture capital perspective. Normally I’d make a joke about how unprofitable some neoinsurance providers are at this juncture, but because our focus is elsewhere, bringing up the fact that, say, Lemonade’s adjusted losses in the final quarter of 2020 were around 150% of its revenue is kind of irrelevant. So we won’t!

Powered by WPeMatico

Coinbase’s direct listing was a massive finance, startup and cryptocurrency event that impacted a host of public and private investors, early employees, and crypto-enthusiasts. Regardless of where one sits in the broader tech and venture world, Coinbase storming north of a $100 billion valuation during its first day of trading was the biggest startup happening of the year.

The transaction’s effects will be felt for some time in the public market, but also among the startups and capital that comprise the private market.

In the buildup to Coinbase’s flotation — and we’d argue especially after it released its blockbuster Q1 2021 results — there was a general expectation that the unicorn’s direct listing would provide a halo effect for other startups in the space. Anthemis’ Ruth Foxe Blader told The Exchange, for example, that “the Coinbase listing shows this great inflection point for crypto,” with another “wave” of startup work in the space coming up.

The widely held perspective raised two questions: Will the success of Coinbase’s direct listing bolster private investment in crypto-focused startups, and will that success help other areas of financially focused startup work garner more investor attention?

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Presuming that Coinbase’s listing will positively impact its niche and others around it is not a stretch. But to make sure we weren’t misreading sentiment, and to get deeper into the why of the concept, The Exchange reached out to venture capitalists who invest in the broader fintech world to get their take. We even roped in an analyst or two to round out our panel.

The answer is not a simple yes. There are several ways to approach investing in the cryptocurrency space — from buying coins themselves, to investing in mainstream-ish institutions like legal exchanges, to the more exotic, like supporting efforts on the forefront of the decentralized blockchain world. And while it is somewhat clear that most folks expect more capital to be available for crypto projects, it’s not clear where it may end up inside the market.

We’ll wrap by considering what impact Coinbase’s direct listing will have, if any, on non-crypto fintech venture capital investing.

We’ll wrap by considering what impact Coinbase’s direct listing will have, if any, on non-crypto fintech venture capital investing.

After yesterday’s examination of how blazingly hot the venture capital market looked in the first quarter, we’re again trying to gauge the private market’s temperature. Let’s talk to some folks on the ground and hear what they are seeing.

Coinbase’s direct listing floated a company that is worth more than all but two major blockchains, namely Ethereum and Bitcoin. Several other chains have aggregate coin values in the 11-figure range, but a 12-digit worth is still rare among crypto assets.

The scale of Coinbase’s valuation post-listing matters, according to Chainalysis Chief Economist Phillip Gradwell. Gradwell told The Exchange that “Coinbase’s $100 billion valuation today demonstrates that venture investors can make great returns from putting money into crypto companies, not just cryptocurrencies. That proof point is good for the entire ecosystem.”

More simply, it is now eminently reasonable to invest in the companies working in the crypto space instead of merely putting capital to work hard-buying coins themselves. The other way to consider the comment is to realize that Coinbase’s share price appreciation is steep enough since its 2012 founding to rival the returns of some coins over the same time frame.

Cleo Capital‘s Sarah Kunst expanded on the point, telling The Exchange in an email that “it’s now credible to say you’re a crypto startup and plan to IPO [versus] having acquisition or ICO be the only proven exit paths in the U.S.”

Powered by WPeMatico

It appears that the slowdown in tech debuts is not a complete freeze; despite concerning news regarding the IPO pipeline, some deals are chugging ahead. This morning, we’re adding Alkami Technology to a list that includes Coinbase’s impending direct listing and Robinhood’s expected IPO.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

We are playing catch-up, so let’s learn about Alkami and its software, dig into its backers and final private valuation, and pick apart its numbers before checking out its impending IPO valuation. After all, if Kaltura and others are going to hit the brakes, we must turn our attention to companies that are still putting the hammer down.

We are playing catch-up, so let’s learn about Alkami and its software, dig into its backers and final private valuation, and pick apart its numbers before checking out its impending IPO valuation. After all, if Kaltura and others are going to hit the brakes, we must turn our attention to companies that are still putting the hammer down.

Frankly, we should have known about Alkami’s IPO sooner. One of a rising number of large tech companies based in nontraditional areas, the bank-focused software company is based in Texas, despite having roots in Oklahoma. The company raised $385.2 million during its life, per Crunchbase data. That sum includes a September 2020 round worth $140 million that valued the company at $1.44 billion on a post-money basis, PitchBook reports.

So, into the latest SEC filing from the software unicorn we go!

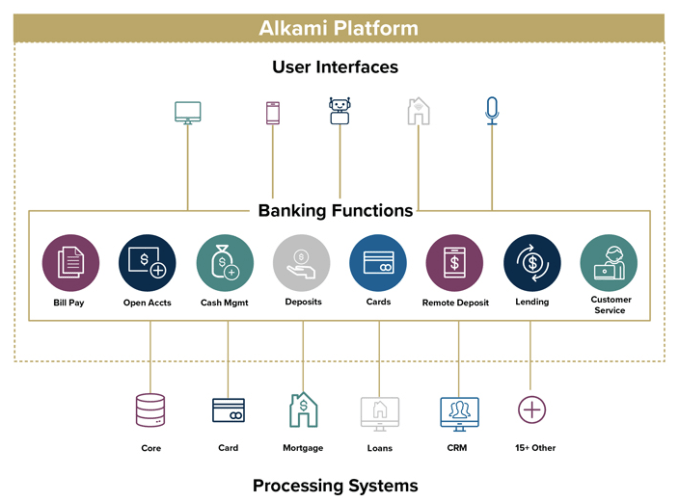

Alkami Technology is a software company that delivers its product to banks via the cloud, so it’s not a legacy player scraping together an IPO during boom times. Instead, it is the sort of company that we understand; it’s built on top of AWS and charges for its services on a recurring basis.

The company’s core market is all banks smaller than the largest, it appears, or what Alkami calls “community, regional and super-regional financial institutions.” Its service is a software layer that plugs into existing financial systems while also providing a number of user interface options.

In short, it takes a bank from its internal systems all the way to the end-user experience. Here’s how Alkami explained it in its S-1/A filing:

Image Credits: Alkami S-1

Simple enough!

Powered by WPeMatico