EC Fintech

Auto Added by WPeMatico

Auto Added by WPeMatico

Both as a term and as a financial product, “buy now, pay later” has become mainstream in the past few years. BNPL has evolved to assume various forms today, from small-ticket offerings by fintechs on consumer checkout platforms and marketplaces, to closed-loop products offered on marketplaces such as Amazon Pay Later (which they are now extending for outside use as well). You can also see some variants offered by companies that want to expand the scope of consumption and consumer credit.

Globally, BNPL has seen the most growth in the consumer segment and has driven retail consumption and lending over the past few years. Consumer BNPL offerings are a good alternative to credit cards, especially for people who do not have a credit history and can’t get credit from banks. That said, a specific vertical of BNPL products is gaining traction — one targeted toward small and medium enterprises (SMEs). This new vertical is known as “SME BNPL.”

BNPL can be particularly useful when flow-based underwriting or transaction-based underwriting is used to offer credit to small businesses.

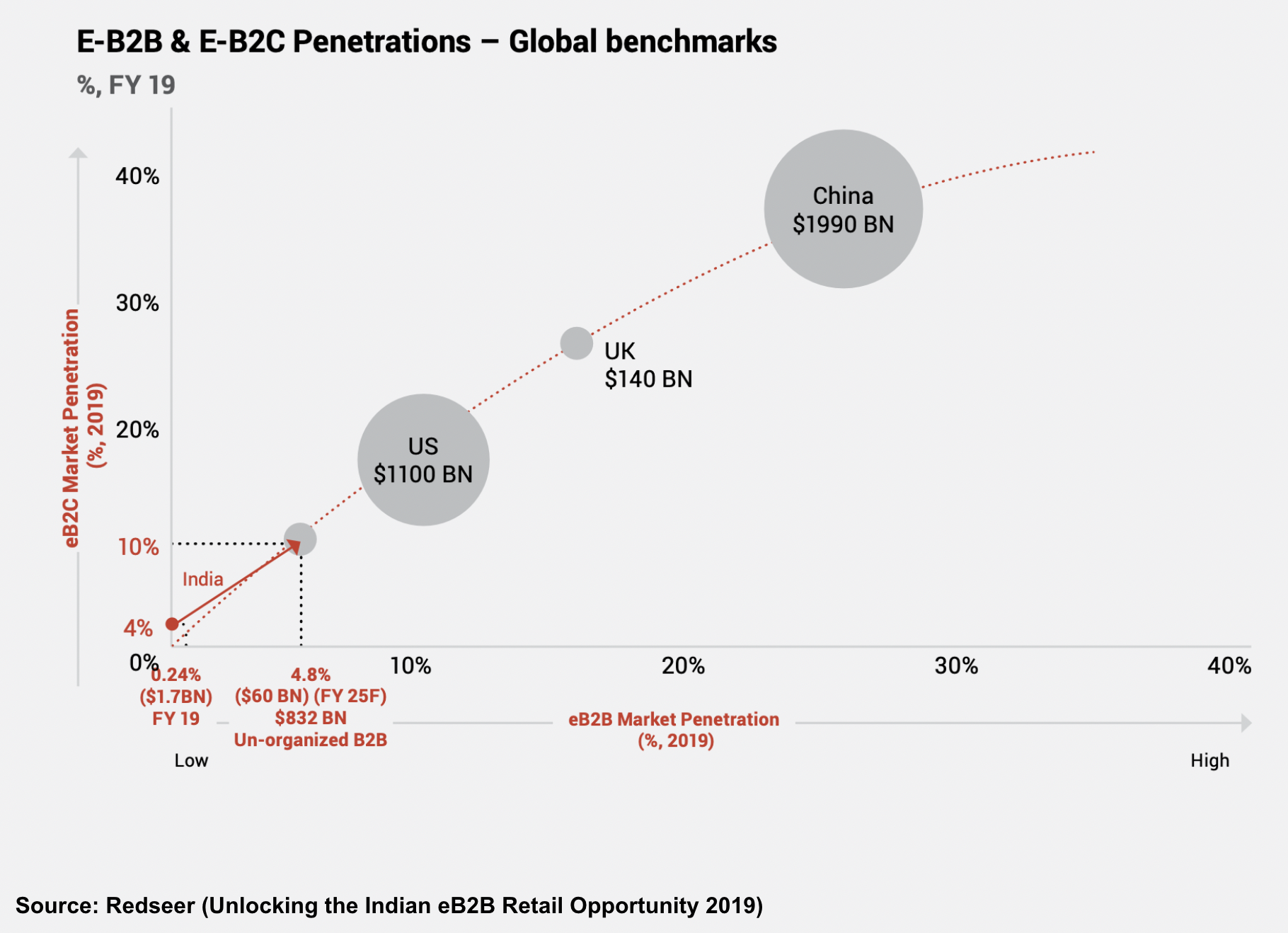

E-commerce has seen tremendous growth in India over the past decade. Skyrocketing smartphone and internet penetration led to rapid growth in e-commerce across large cities and smaller towns alike. Consumer credit has also taken off in parallel as credit cards and digital lending spurred credit-based consumption across offline and online stores.

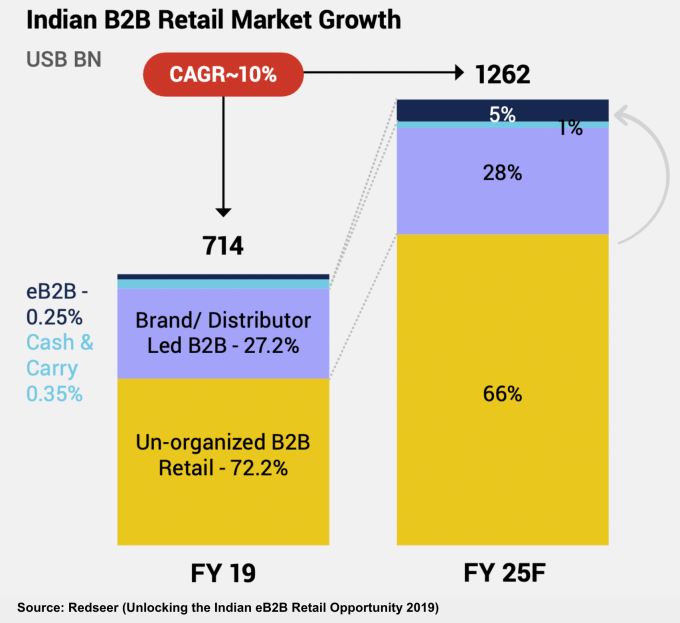

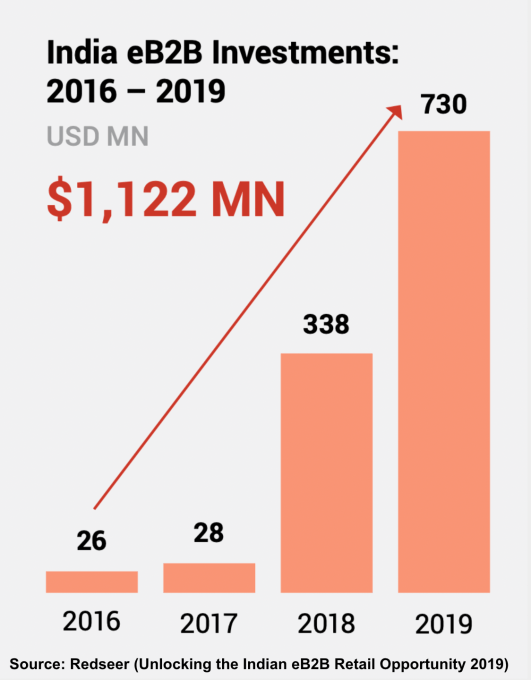

However, the large B2B supply chain enabling the burgeoning retail market was plagued by bottlenecks and inefficiencies because it involved a plethora of intermediaries and streamlining became a big problem. A number of tech players responded by organizing the previously disorganized B2B commerce market at various touch points, inserting convenience, pricing and easier product access through tech-enabled logistics and a modern supply chain.

Image Credits: Redseer

India’s B2B e-commerce space has developed rapidly since 2020. Small businesses have moved from using paper to smartphone apps for running a significant part of their day-to-day business, leading to widespread disruption in how businesses transact today. The COVID-19 pandemic also forced small businesses, which were earlier using physical means to procure goods and services, to try new and online models to conduct their affairs.

Image Credits: Redseer

Moreover, the Indian government’s widespread promotion of an instant payments system in the form of the Unified Payments Interface (UPI) has changed how people send money to each other or pay merchants for their goods and services. The next step for solving the digital B2B puzzle is to embed credit inside every transaction and invoice.

Image Credits: Redseer

If we compare online B2B transactions to the offline world, there is only one missing link: The terms offered to small businesses by their supplier/distributor or vendor. Businesses, unlike consumers, must buy goods and services to eventually trade them, or add value and sell to consumers or others down the value chain. This process is not immediate and has a certain time cycle attached.

The longer sales cycle means many small businesses require credit payment terms when buying inventory. As B2B commerce scales and grows through digital means, a BNPL product that caters to the needs of SMEs can support their growth and alleviate the burden on their cash flows.

An SME BNPL product is a purchase financing product for small businesses transacting with suppliers, distributors, aggregator platforms or B2B marketplaces.

Powered by WPeMatico

Earlier today, spend management startup Ramp said it has raised a $300 million Series C that valued it at $3.9 billion. It also said it was acquiring Buyer, a “negotiation-as-a-service” platform that it believes will help customers save money on purchases and SaaS products.

The round and deal were announced just a week after competitor Brex shared news of its own acquisition — the $50 million purchase of Israeli fintech startup Weav. That deal was made after Brex’s founders invested in Weav, which offers a “universal API for commerce platforms.”

From a high level, all of the recent deal-making in corporate cards and spend management shows that it’s not enough to just help companies track what employees are expensing these days. As the market matures and feature sets begin to converge, the players are seeking to differentiate themselves from the competition.

But the point of interest here is these deals can tell us where both companies think they can provide and extract the most value from the market.

These differences come atop another layer of divergence between the two companies: While Brex has instituted a paid software tier of its service, Ramp has not.

Let’s start with Ramp. Launched in 2019, the company is a relative newcomer in the spend management category. But by all accounts, it’s producing some impressive growth numbers. As our colleague Mary Ann Azevedo wrote:

Since the beginning of 2021, the company says it has seen its number of cardholders on its platform increase by 5x, with more than 2,000 businesses currently using Ramp as their “primary spend management solution.” The transaction volume on its corporate cards has tripled since April, when its last raise was announced. And, impressively, Ramp has seen its transaction volume increase year over year by 1,000%, according to CEO and co-founder Eric Glyman.

Ramp’s focus has always been on helping its customers save money: It touts a 1.5% cash back reward for all purchases made through its cards, and says its dashboard helps businesses identify duplicitous subscriptions and license redundancies. Ramp also alerts customers when they can save money on annual versus monthly subscriptions, which it says has led many customers to do away with established T&E platforms like Concur or Expensify.

All told, the company claims that the average customer saves 3.3% per year on expenses after switching to its platform — and all that is before it brings Buyer into the fold.

Powered by WPeMatico

Oh, how the tables have turned.

It used to be that if you were a fintech startup or, for lack of a better term, a digitally native financial services business, you might be eyeing an acquisition from an incumbent in the industry.

It used to be that if you were a fintech startup or, for lack of a better term, a digitally native financial services business, you might be eyeing an acquisition from an incumbent in the industry.

But lately, fintech upstarts are the ones doing the acquiring. Over just the last year or so, we’ve seen:

So what’s going on here? Why are fintechs now acquiring legacy financial services businesses, instead of the other way around?

Powered by WPeMatico

The Chinese government’s crackdown on its domestic technology industry continues, with Tencent under fresh pressure despite the company’s efforts to follow changing regulatory expectations.

News broke over the weekend that Beijing filed a civil suit against Tencent “over claims its messaging-app WeChat’s Youth Mode does not comply with laws protecting minors,” per the BBC. And NetEase, a major Chinese technology company, will delay the IPO of its music arm in Hong Kong. Why? Uncertain regulations, per Reuters.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The latest spate of bad news for China’s technology industry follows a raft of regulatory changes and actions by the nation’s government that have deleted an enormous quantity of equity value. After a period of relatively light-touch regulatory oversight, domestic Chinese technology companies have found themselves on defense after the Chinese Communist Party (CCP) came after their market power in antitrust terms — and some of their business operations from other perspectives. Sectors hit the hardest include fintech and edtech.

Gaming is also in the CCP crosshairs.

After state media criticized the gaming industry as providing the digital equivalent of drugs to the nation’s youth last week, shares of companies like Tencent and NetEase fell. Tencent owns Riot Games, makers of the popular League of Legends title. NetEase generated $2.3 billion in gaming revenue out of total revenues of $3.1 billion in its most recent quarter.

After state media criticized the gaming industry as providing the digital equivalent of drugs to the nation’s youth last week, shares of companies like Tencent and NetEase fell. Tencent owns Riot Games, makers of the popular League of Legends title. NetEase generated $2.3 billion in gaming revenue out of total revenues of $3.1 billion in its most recent quarter.

NetEase stock traded around $110 per share in late July. It’s now worth around $90 per share after expectations shifted in light of the gaming news, indicating that investors are concerned about its future performance. Tencent’s Hong Kong-listed stock has also fallen, from HK$775.50 to HK$461.60 this morning.

Tencent tried to head off regulatory pressure, announcing changes to how it controls access to its games after the government’s shot across the bow. The effort doesn’t appear to have worked. That Tencent is being sued by the government despite its publicly announced changes implies that its proposed curbs to youth gaming were either insufficient or perhaps moot from the beginning.

Powered by WPeMatico

The global venture capital bet on neobanks is massive. London-based Starling Bank has raised more than $900 million, per Crunchbase. The same data source indicates that Chime has raised $1.5 billion. Monzo has raised nearly $650 million. And the list goes on: E-commerce-focused neobank Juni raised $21.5 million last month. Novo, an SMB-focused neobank, raised $41 million in June. Nubank has raised $2.3 billion. And FairMoney has locked down more than $50 million.

On and on and on.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

But despite our general inclination to lump banking-focused fintech providers that serve consumers, business customers or both into a single bucket, there’s wide divergence in how the various neobank players are performing in the market.

Back in August 2020, The Exchange noted that many neobanks were racking up steep losses. Our read at the time was that the capital being poured into the fintech category was being invested aggressively in the name of growth. Based on recent results, that view is holding up.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

And Starling Bank reached what it describes as profitable territory in October 2020. Things have changed since our first look into neobank results.

The trend of positive neobank news continued this June, when Revolut reported its recent financial performance. The company did post rather negative aggregate results for the 2020 period. But when we drilled down into its quarterly results, we saw the picture of a fintech company scaling its gross margins and revenues while nearly reaching adjusted net income neutrality by Q4 2020. We were impressed.

This morning, let’s add to our running dig into neobank results by parsing recently released data from Starling Bank and Monzo. As we’ll see, although some neobanks are managing to clean up their ledgers and work toward profits — or reach profitability — not all are in the black.

Powered by WPeMatico

Shares of Square are up this morning after the company announced its second-quarter earnings and that it will buy Afterpay, an Australian buy now, pay later (BNPL) player in a $29 billion deal. As TechCrunch reported this morning, Afterpay shareholders will receive 0.375 shares of Square in exchange for their existing equity.

Shares of Afterpay are sharply higher after the deal was announced thanks to its implied premium, while shares of Square are up 7% in early-morning trading.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Over the past year, we’ve written extensively about the BNPL market, usually from the perspective of earnings from companies in the space. Afterpay has been a key data source, along with the yet-private Klarna and U.S. public BNPL outfit Affirm. Recall that each company has posted strong growth in recent periods, with the United States arising as a prime competitive market.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

From that landscape, let’s explore the Square-Afterpay deal. We want to know what Afterpay brings to Square in terms of revenue, growth and reach. We also want to do some math on the price Square is willing to pay for the company — and what that might tell us about the value of BNPL and fintech revenues more broadly. Then we’ll eyeball the numbers and try to decide if Square is overpaying for Afterpay.

As with most major deals these days, Square and Afterpay released an investor presentation detailing their argument in favor of their combination. Let’s dig through it.

Square is a two-part company. It has a large consumer business via Cash App, and it has a large business division that offers payments tech and other fintech services to corporate customers. Recall that Square is also building out banking services for its business customers and that Cash App also serves some banking and investing functionality for consumers.

Powered by WPeMatico

Robinhood priced at $38 per share this week, opened flat and closed its first day’s trading yesterday worth $34.82 per share, or a bit more than 8% underwater. The company posted a mixed picture today, falling early before recovering to breakeven in late-morning trading.

It wasn’t the debut that some expected Robinhood to have.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

To close out the week, we’re not going to noodle on banned Chinese IPOs or do a full-week mega-round discussion. Instead, let’s parse some notes from a chat The Exchange had with Robinhood’s CFO about his company’s IPO and go over a few reasonable guesses as to why we’re not wondering how much money Robinhood left on the table by pricing its public offering lower than it closed on its first day.

Let’s not be dicks about it. The time for Twitter jokes was yesterday. We’ll put our thinking caps on this morning.

Let’s not be dicks about it. The time for Twitter jokes was yesterday. We’ll put our thinking caps on this morning.

Chatting with Robinhood CFO Jason Warnick earlier this week, we wanted to know why this was the right time for Robinhood to go public.

Now, no public company CEO or CFO will come out and directly say that they are going public because they think that they can defend — or extend — their most recent private valuation thanks to current market conditions.

Instead, execs on IPO day tend to deflect the question, pivoting to a well-oiled bon mot about how their public offering is a mere milestone on their company’s long-term trajectory. For some reason in our capitalist society, during an arch-capitalist event, by a for-profit company, leaders find it critical to downplay their IPO’s importance.1

With that in mind, Warnick did not say Robinhood went public because the IPO market has recently rewarded big-brand consumer tech companies like Airbnb and DoorDash with strong debuts. And he didn’t say that with tech shares near all-time highs and a taste for high-growth concerns, the company was likely set to enter a market that would be willing to price it at a valuation that it found attractive.

Powered by WPeMatico

Anomaly detection is one of the more difficult and underserved operational areas in the asset-servicing sector of financial institutions. Broadly speaking, a true anomaly is one that deviates from the norm of the expected or the familiar. Anomalies can be the result of incompetence, maliciousness, system errors, accidents or the product of shifts in the underlying structure of day-to-day processes.

For the financial services industry, detecting anomalies is critical, as they may be indicative of illegal activities such as fraud, identity theft, network intrusion, account takeover or money laundering, which may result in undesired outcomes for both the institution and the individual.

There are different ways to address the challenge of anomaly detection, including supervised and unsupervised learning.

Detecting outlier data, or anomalies according to historic data patterns and trends can enrich a financial institution’s operational team by increasing their understanding and preparedness.

Anomaly detection presents a unique challenge for a variety of reasons. First and foremost, the financial services industry has seen an increase in the volume and complexity of data in recent years. In addition, a large emphasis has been placed on the quality of data, turning it into a way to measure the health of an institution.

To make matters more complicated, anomaly detection requires the prediction of something that has not been seen before or prepared for. The increase in data and the fact that it is constantly changing exacerbates the challenge further.

There are different ways to address the challenge of anomaly detection, including supervised and unsupervised learning.

Powered by WPeMatico

Is the trading boom of 2020 and 2021 slowing?

That’s a question The Exchange has had on its mind since Robinhood released its latest IPO filing. The popular U.S. consumer-focused investing app told investors in the document that it expects revenues to decline in the third quarter compared to its Q2 performance. The company highlighted historically strong crypto volumes in preceding quarters as part of the reason for its anticipated revenue decline.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Naturally, we got to thinking about Coinbase.

It’s likely fair to say that Coinbase and Robinhood are bullish enough about the cryptocurrency market to be unbothered by short-term changes to crypto trading volumes. Coinbase discussed rising and falling consumer interest in trading cryptos in its own IPO filings, for example.

The now-public unicorn has lived through crypto ups and crypto downs. A decline in consumer interest in the next few months or quarters is not a huge deal, assuming one keeps a long enough perspective and the crypto-infused future that its fans expect comes to pass.

The boom in crypto demand among U.S. consumers lifted many a boat in recent quarters. Coinbase posted insanely good early-2021 results thanks to a bull run in cryptocurrency prices that drove retail interest and trading fees. Robinhood also saw a rush of crypto demand, something that TechCrunch explored here. And Square itself has seen crypto revenues explode.

Sure, equities interest and demand for options also elevated the fortune of many consumer fintechs during the COVID-19 savings and investing boom. But crypto revenues had a big part to play. Let’s examine both situations through the lens of the latest from Robinhood.

There are some 316 mentions of “cryptocurrency” in Robinhood’s latest IPO filing. We’re going to stick to those we consider the most important.

As context, Robinhood shared preliminary Q2 data. We discussed it here if you want to go deeper into the aggregate figures. But after its disclosure of hard numbers, Robinhood had some interesting notes about the current quarter (emphasis TechCrunch):

Trading activity was particularly high during the first two months of the 2021 period, returning to levels more in line with prior periods during the last few weeks of the quarter ended June 30, 2021, and remained at similar levels into the early part of the third quarter. We expect our revenue for the three months ending September 30, 2021 to be lower, as compared to the three months ended June 30, 2021, as a result of decreased levels of trading activity relative to the record highs in trading activity, particularly in cryptocurrencies, during the three months ended June 30, 2021, and expected seasonality.

And in a discussion of some other performance metrics, including funded accounts and the like, Robinhood had this to say (emphasis TechCrunch):

We anticipate the rate of growth in these Key Performance Metrics will be lower for the period ended September 30, 2021, as compared to the three months ended June 30, 2021, due to the exceptionally strong interest in trading, particularly in cryptocurrencies, we experienced in the three months ended June 30, 2021, and seasonality in overall trading activities.

Falling revenue and slowing KPM growth is not really the world’s best set of metrics to flash up during an IPO run. But a quick scan of Robinhood’s 2020 revenues indicates it’s unlikely that the unicorn will be able to post year-over-year growth in the final two quarters of 2021. Still, its period of rapid-fire revenue growth appears to have come to an end after Robinhood posted top-line expansion in every quarter since Q4 2019.

Powered by WPeMatico

Today, Tractable is worth $1 billion. Our AI is used by millions of people across the world to recover faster from road accidents, and it also helps recycle as many cars as Tesla puts on the road.

And yet six years ago, Tractable was just me and Raz (Razvan Ranca, CTO), two college grads coding in a basement. Here’s how we did it, and what we learned along the way.

In 2013, I was fortunate to get into artificial intelligence (more specifically, deep learning) six months before it blew up internationally. It started when I took a course on Coursera called “Machine learning with neural networks” by Geoffrey Hinton. It was like being love struck. Back then, to me AI was science fiction, like “The Terminator.”

Narrowly focusing on a branch of applied science that was undergoing a paradigm shift which hadn’t yet reached the business world changed everything.

But an article in the tech press said the academic field was amid a resurgence. As a result of 100x larger training data sets and 100x higher compute power becoming available by reprogramming GPUs (graphics cards), a huge leap in predictive performance had been attained in image classification a year earlier. This meant computers were starting to be able to understand what’s in an image — like humans do.

The next step was getting this technology into the real world. While at university — Imperial College London — teaming up with much more skilled people, we built a plant recognition app with deep learning. We walked our professor through Hyde Park, watching him take photos of flowers with the app and laughing from joy as the AI recognized the right plant species. This had previously been impossible.

I started spending every spare moment on image classification with deep learning. Still, no one was talking about it in the news — even Imperial’s computer vision lab wasn’t yet on it! I felt like I was in on a revolutionary secret.

Looking back, narrowly focusing on a branch of applied science undergoing a breakthrough paradigm shift that hadn’t yet reached the business world changed everything.

I’d previously been rejected from Entrepreneur First (EF), one of the world’s best incubators, for not knowing anything about tech. Having changed that, I applied again.

The last interview was a hackathon, where I met Raz. He was doing machine learning research at Cambridge, had topped EF’s technical test, and published papers on reconstructing shredded documents and on poker bots that could detect bluffs. His bare-bones webpage read: “I seek data-driven solutions to currently intractable problems.” Now that had a ring to it (and where we’d get the name for Tractable).

That hackathon, we coded all night. The morning after, he and I knew something special was happening between us. We moved in together and would spend years side by side, 24/7, from waking up to Pantera in the morning to coding marathons at night.

But we also wouldn’t have got where we are without Adrien (Cohen, president), who joined as our third co-founder right after our seed round. Adrien had previously co-founded Lazada, an online supermarket in South East Asia like Amazon and Alibaba, which sold to Alibaba for $1.5 billion. Adrien would teach us how to build a business, inspire trust and hire world-class talent.

Tractable started at EF with a head start — a paying customer. Our first use case was … plastic pipe welds.

It was as glamorous as it sounds. Pipes that carry water and natural gas to your home are made of plastic. They’re connected by welds (melt the two plastic ends, connect them, let them cool down and solidify again as one). Image classification AI could visually check people’s weld setups to ensure good quality. Most of all, it was real-world value for breakthrough AI.

And yet in the end, they — our only paying customer — stopped working with us, just as we were raising our first round of funding. That was rough. Luckily, the number of pipe weld inspections was too small a market to interest investors, so we explored other use cases — utilities, geology, dermatology and medical imaging.

Powered by WPeMatico