EC Column

Auto Added by WPeMatico

Auto Added by WPeMatico

If money is the ultimate commodity, how can fintechs — which sell money, move money or sell insurance against monetary loss — build products that remain differentiated and create lasting value over time?

And why are so many software companies — which already boast highly differentiated offerings and serve huge markets— moving to offer financial services embedded within their products?

A new and attractive hybrid category of company is emerging at the intersection of software and financial services, creating buzz in the investment and entrepreneurial communities, as we discussed at our “Fintech: The Endgame” virtual conference and accompanying report this week.

These specialized companies — in some cases, software companies that also process payments and hold funds on behalf of their customers, and in others, financial-first companies that integrate workflow and features more reminiscent of software companies — combine some of the best attributes of both categories.

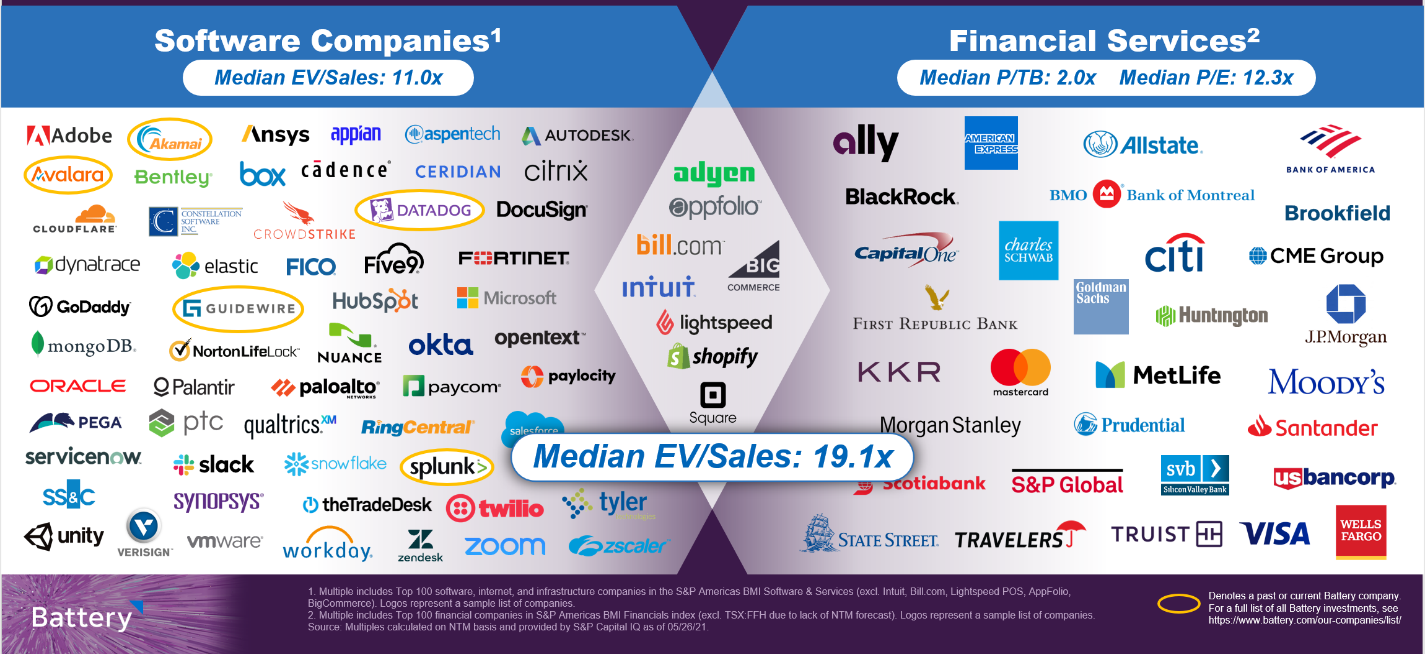

Image Credits: Battery Ventures

From software, they design for strong user engagement linked to helpful, intuitive products that drive retention over the long term. From financials, they draw on the ability to earn revenues indexed to the growth of a customer’s business.

Fintech is poised to revolutionize financial services, both through reinventing existing products and driving new business models as financial services become more pervasive within other sectors.

The powerful combination of these two models is rapidly driving both public and private market value as investors grant these “super” companies premium valuations — in the public sphere, nearly twice the median multiple of pure software companies, according to a Battery analysis.

The near-perfect example of this phenomenon is Shopify, the company that made its name selling software to help business owners launch and manage online stores. Despite achieving notable scale with this original SaaS product, Shopify today makes twice as much revenue from payments as it does from software by enabling those business owners to accept credit card payments and acting as its own payment processor.

The combination of a software solution indexed to e-commerce growth, combined with a profitable payments stream growing even faster than its software revenues, has investors granting Shopify a 31x multiple on its forward revenues, according to CapIQ data as of May 26.

Before even talking about how investors should value these hybrid companies, it’s worth making the point that in both private and public markets, fintechs have been notoriously hard to value, fomenting controversy and debate in the investment community.

Powered by WPeMatico

On Earth Day, April 22, SOSV published the SOSV Climate Tech 100, a list of the best startups that we’ve supported from their earliest stages to address climate change. There are always valuable insights embedded in a list like the 100. A TechCrunch story captured the investment perspective, and an SOSV post went deeper into the companies’ category breakdown and founder profiles.

But what can founders learn from the list about climate tech investors? In other words, who invested in the Climate Tech 100? We dug into the “who’s who” of the list, which had more than 500 investors, and here’s what we found.

If you think 500 investors in 100 companies is a lot of investors, you’re right. There are clearly a lot of investors interested in climate tech, and most are generalists just testing the waters. For the Climate Tech 100, about 10% of investors put their money in more than one startup and only seven (less than 2%) wrote a check to four or more. These included Blue Horizon, CPT Capital, EF, Fifty Years, Hemisphere Ventures and Horizons Ventures.

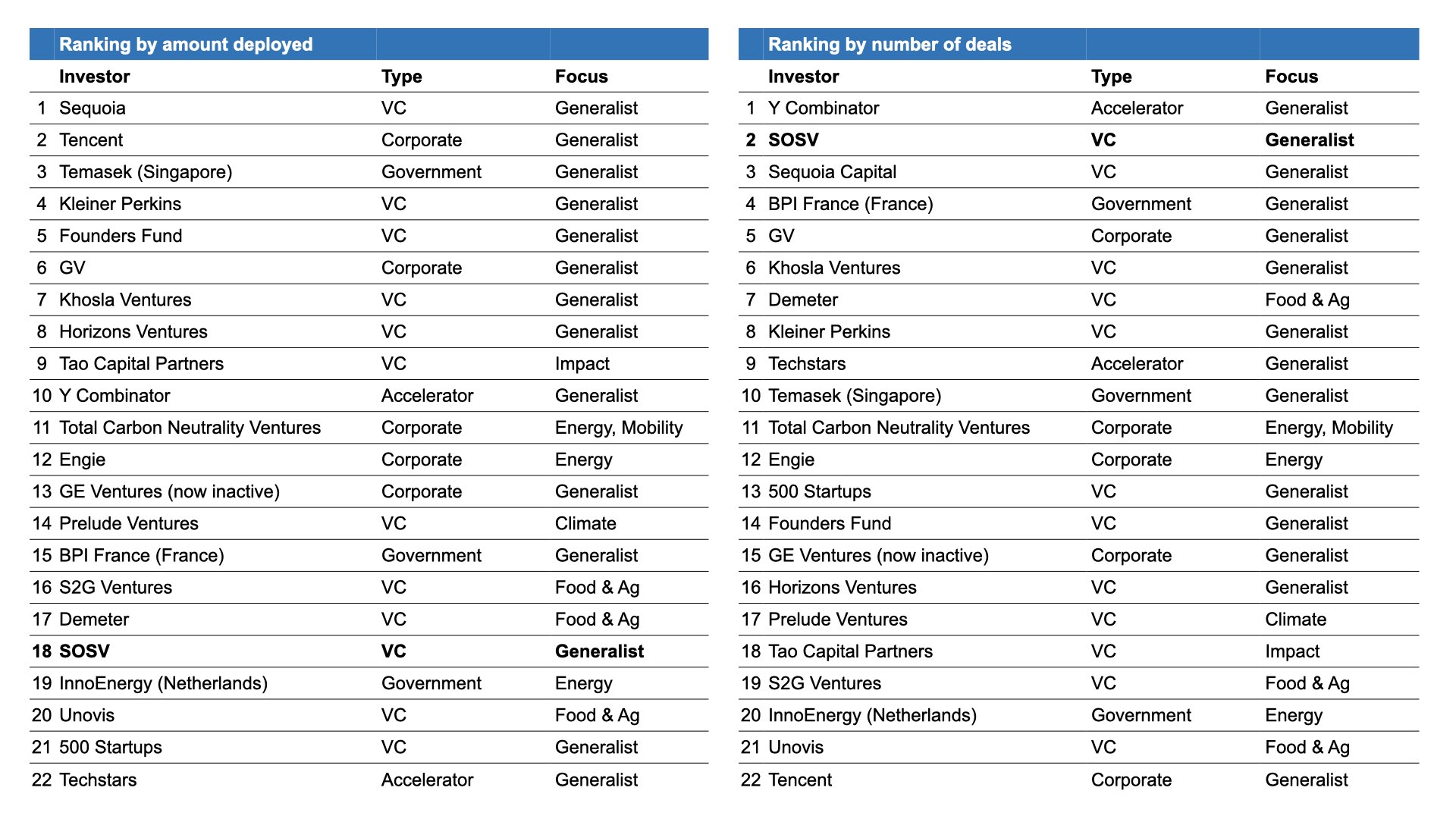

That pattern tracks well with data from PwC, which found that 2,700 unique investors had backed 1,200 startups in its State of Climate Tech 2020 report covering the 2013-2019 period. The report found that only 10 firms out of 2,700 made four or more climate tech deals per year, on average, over the 2013-2019 period. The most active firms are listed in the table below.

Image Credits: PwC, 2020; additional research by SOSV

Capital deployed in climate tech grew at five times the venture capital overall growth rate over the 2013-2019 period.

There is reason to believe that the fragmentation will diminish with the launch of more funds focused on climate tech. Four funds worth more than a billion dollars each have launched since 2020 that fit the description (see chart below).

It’s also encouraging to see that capital deployed in climate tech grew at five times the venture capital overall growth rate over the 2013-2019 period.

Even so, climate tech still only represented 6% of total venture capital deployed in 2019, so there is plenty of room to grow.

Powered by WPeMatico

Running a startup can be a complicated, difficult process fraught with pitfalls and ample opportunities to make mistakes. But the logistics of setting up a startup should be simple, because over the long run, complicated equity setups and cap tables cost more money in legal fees and administration time.

The logistics of setting up a startup should be simple, because over the long run, complicated equity setups and cap tables cost more money in legal fees and administration time.

My company, Pulley, has helped more than a thousand founders build their cap table and equity structure.

Here’s a tactical guide to get your startup running in just four days.

It is now standard to incorporate your company at the seed stage itself. In the U.S., startups incorporate as Delaware C Corporations with 10 million authorized shares. This is the standard setup when you use services like Stripe Atlas or Clerky.

Post incorporation, you need to answer a few questions on how to grant equity to founders and future employees.

First, you should determine how you want to split the equity between the founders. There is no standard for doing so — some founders split shares equally, while others do 49/51 splits for control. Some founders even may have an 80/20 equity split because one founder spent an extra year on the idea.

At the end of the day, a good equity split is one that all founders find fair. If you can’t agree on a structure, you should have a deeper discussion on whether this is the right team to work with for the next decade or more.

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

Extra Crunch members receive access to weekly “Dear Sophie” columns; use promo code ALCORN to purchase a one- or two-year subscription for 50% off.

Dear Sophie,

I started a tech company about two years ago, and ever since I’ve dreamed of expanding my company in the United States.

I would love to have a green card. Someone mentioned that I should apply for a diversity green card. Would you please provide me with more details about it and how to apply?

— Technical in Tanzania

Dear Technical,

As a startup founder from Tanzania, you have several immigration options available to you, including the Diversity Immigrant Visa (green card) Program.

My law partner, Anita Koumriqian, and I recently discussed the Diversity Immigrant Visa Program (DV Program) on a podcast episode. Take a listen for how to apply and tips for applying. Each year, the U.S. Department of State, which oversees the DV Program, reserves 50,000 green cards for individuals born in countries that have low rates of immigration to the United States. The State Department publishes instructions each year, which includes the countries whose natives are eligible to register for the annual diversity lottery. Here is the latest version.

You must register online in the fall — usually from early October through early November — for the annual random lottery by completing the Electronic Diversity Visa Entry Form (DS-5501). There is no cost to register for the lottery, but be aware that you will be automatically disqualified if you register yourself more than once, and incomplete forms will not be accepted.

Once you complete the online registration form, you will get a confirmation number. Do not lose this number! It is the only way to access the online system that will tell you whether you were selected in the lottery and are eligible to submit a green card application. In May, registrants can log into the online system to find out whether they’ve been selected. No notification will be sent by email or snail mail; checking online by entering your confirmation code is the only way to find out. After you enter your confirmation code online, you will receive a diversity visa number, which you will use to determine when you can file your green card application.

Powered by WPeMatico

Hey, founders between gigs: What now?

If you exited your last company for airplane money and are now independently wealthy, congratulations! If you want to build another company, just self-fund. If you want outside capital, VCs will chase after you to invest.

Unfortunately, most founders are not in that position: nine out of 10 startups fail. Even if you achieve a high valuation, you might end up like FanDuel’s founders: Their investors got the benefit of a $465 million exit; the founders got zero.

As someone with “founder” on your resume, you face a greater challenge when trying to get a traditional salaried job. You’ve already shown that you really want to lead a company and not just rise up the ladder, which means some employers are less likely to hire you. One research paper found:

[F]ormer founders receive fewer callbacks than non-founders; however, all founders are not disadvantaged similarly. Former founders of successful ventures receive even fewer [emphasis added] callbacks than former founders of failed ventures. Through 20 interviews with technical recruiters, we highlight the mechanisms driving this founder-experience discount: concerns related to the applicant’s capability and ability to fit into and remain committed to the wage employment and the hiring firm.

At my prior firm, ff Venture Capital, we invested in a company co-founded by Nate Jenkins, who had a successful exit, but not quite enough to buy a private plane. He’s now researching his next opportunity and interviewing for some jobs. At the end of a recent interview, the interviewer summarized, “I’ll hire you, but is this what you really want to do?”

That said, Samuel Sabin, CEO of HireBlue, observed, “Some founders who work better with more resources at their disposal may be tapped for intrapreneurship roles. Also, some companies value a self-starter mentality.”

So what should you do? Especially if your life partner and/or bank account are burnt out on the income volatility of startups?

I’ve been in this situation myself when I shut down one startup and exited two others. I think you have six main options:

At Versatile VC, our new VC fund, we’re creating an online community just for founders who are in transition, Founders’ Next Move. We hope you will join us!

If you want to work on your startup idea, the bar for starting a company should always be very high. VCs have a diversified portfolio and most of their investments die. You don’t have a diverse portfolio and so you’re taking far more risk than the VCs. For free resources to help research your ideas, see What startup will you build? Identifying market white space.

Powered by WPeMatico

The pandemic forced companies around the world to adjust to a “new normal,” which caused many leaders to pivot their business strategies and adopt new technologies to continue operations. In a time of chaos and change, there is no senior leader that can navigate this sort of change better than a CTO.

Not only do CTOs understand the ever-changing tech landscape, they also provide invaluable insights to help organizations go beyond traditional IT conversations and leverage technology to successfully scale businesses.

Boards are facing pressure to be strategic and thoughtful on how to evolve in the rapidly iterating world of technology, and a CTO is uniquely positioned to address specific challenges.

There are now more reasons than ever to consider adding a CTO to your board. As a CTO myself, I know how important and impactful it can be to have technical-minded leaders on a company’s board of directors. At a time when companies are accelerating their digital transformation, it’s critical to have diverse technical perspectives and people from varying backgrounds, as transformations are a mix of people, process and technology.

Drawing on my experience on Lightbend’s board of directors, here are five hidden benefits of making space at the table for a CTO.

Currently, most boards of directors are composed of former CEOs, CFOs and investors. While such executives bring vast experience, they have very specific expertise, and that frequently does not include technical proficiency. In order for a company to be successful, your board needs to have people with different backgrounds and expertise.

Inviting different perspectives forces companies out of the groupthink mentality and find new, creative solutions to their problems. Diverse perspectives aren’t just about the title –– racial ethnicity and gender diversity are clearly a play here as well.

For a product-led company, having a CTO who has been close to product development and innovation can bring deep insights and understanding to the boardroom. Boards are facing pressure to be strategic and thoughtful on how to evolve in the rapidly iterating world of technology, and a CTO is uniquely positioned to address specific challenges.

Powered by WPeMatico

Software as a service has been thriving as a sector for years, but it has gone into overdrive in the past year as businesses responded to the pandemic by speeding up the migration of important functions to the cloud. We’ve all seen the news of SaaS startups raising large funding rounds, with deal sizes and valuations steadily climbing. But as tech industry watchers know only too well, large funding rounds and valuations are not foolproof indicators of sustainable growth and longevity.

Failing to come across as a unique, differentiated company will likely mean settling for an exit that feels mediocre instead of incredible.

To scale sustainably, grow its customer base and mature to the point of an exit, a SaaS startup needs to stand apart from the herd at every phase of development. Failure to do so means a poor outcome for founders and investors.

As a founder who pivoted from on-premise to SaaS back in 2016, I have focused on scaling my company (most recently crossing 145,000 customers) and in the process, learned quite a bit about making a mark. Here is some advice on differentiation at the various stages in the life of a SaaS startup.

Differentiation is crucial early on, because it’s one of the only ways to attract customers. Customers can help lay the groundwork for everything from your product roadmap to pricing.

The more you know about your target customers’ pain points with current solutions, the easier it will be to stand out. Take every opportunity to learn about the people you are aiming to serve, and which problems they want to solve the most. Analyst reports about specific sectors may be useful, but there is no better source of information than the people who, hopefully, will pay to use your solution.

The key to success in the SaaS space is solving real problems. Take DocuSign, for example — the company found a way to simply and elegantly solve a niche problem for users with its software. This is something that sounds easy, but in reality, it means spending hours listening to the customer and tailoring your product accordingly.

Powered by WPeMatico

It was August 2019, and the fundraising process was not going well.

My co-founder and I had left our product management jobs at New Relic several months prior, deciding to finally plunge into building Reclaim after nearly a year of late nights and weekends spent prototyping and iterating on ideas. We had bits and pieces of a product, but the majority of it was what we might call “slideware.”

When you can’t raise big on the vision, you need to raise big on the proof. And the proof comes from building, learning, iterating and getting traction with your first few hundred users.

When we spoke to many other founders, they all told us the same thing: Go raise, raise big, and raise now. So we did that, even though we were puzzled as to why anyone would give us money with little more than a slide deck to our names. We spent nearly three months pitching dozens of VCs, hoping to raise $3 million to $4 million in a seed round to hire our founding team and build the product out.

Initially, we were excited. There was lots of inbound interest, and we were starting to hear a lot of crazy numbers getting thrown around by a lot of Important People. We thought for sure we were maybe a week away from term sheets. We celebrated preemptively. How could it possibly be this easy?

Then in July, almost in an instant, everything started to dry up. The verbal offers for term sheets didn’t materialize into real offers. We had term sheets, but they were from investors that didn’t seem to care much about what we were building or what problems we wanted to solve. We quickly realized that we hadn’t really built momentum around the product or the vision, but were instead caught up in what we later learned to be “deal flow.”

Basically, investors were interested because other investors were interested. And once enough of them weren’t, nobody was.

Fortunately, as I write this today, Reclaim has raised a total of $6.3 million on great terms across a group of incredible investors and partners. But it wasn’t easy, and it required us to embrace our failure and learn three important lessons that I believe every founder should consider before they decide to go out and pitch investors.

In 2019, we were hunting for what some referred to as a “mango seed” — that is, a seed round that was large enough that it was perceptibly closer to a light Series A financing. Being pre-product at the time, we had to lean on our experience and our vision to drive conviction and urgency among investors. Unfortunately, it just wasn’t enough. Investors either felt that our experience was a bad fit for the space we were entering (productivity/scheduling) or that our vision wasn’t compelling enough to merit investment on the terms we wanted.

When we did get offers, they involved swallowing some pretty bitter pills: We would be forced to take bad terms that were overly dilutive (at least from our perspective), work with an investor who we didn’t think had high conviction in our product strategy, or relinquish control in the company from an extremely early stage. None of these seemed like good options.

Powered by WPeMatico

Would you like to work with private equity and venture capital funds?

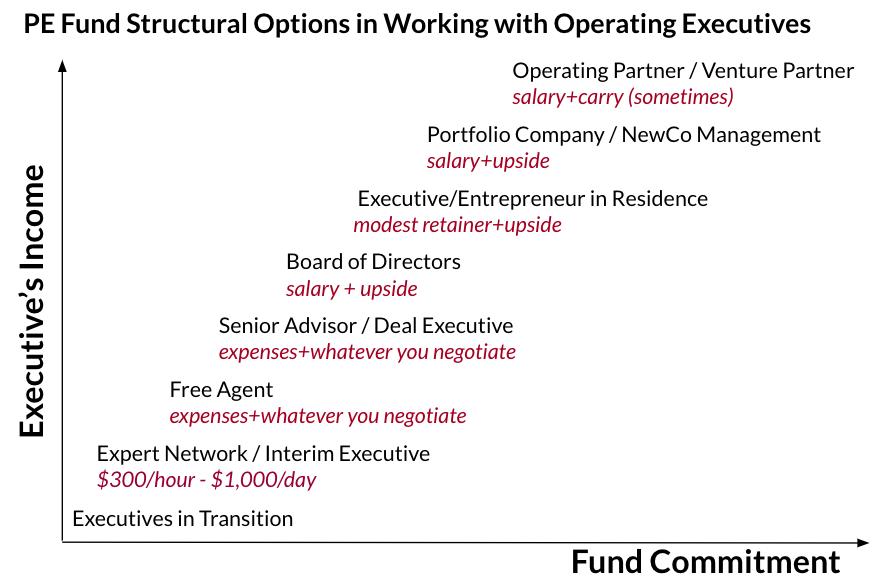

There are relatively few jobs directly inside private equity and venture capital funds, and those jobs are highly competitive. However, there are many other ways you can work and earn money within the industry — as a consultant, an interim executive, a board member, a deal executive partnering to buy a company, an executive in residence or as an entrepreneur in residence.

Venture capitalists often have an operations background. However, historically most private equity professionals were former investment bankers and other finance professionals. Then private equity players gradually realized that value cannot be created through financial engineering alone. A BCG study of 121 investments found that operational improvement drives 48% of value creation in PE-backed companies. PE funds now almost always require an upgrade in management and change management teams if necessary.

Not surprisingly, the tighter your relationship with the firm, the more money you will earn:

Image Credits: David Teten

At Versatile VC, we’ve used all these models. We are soon launching Founders’ Next Move, a selective, free community for founders researching their next move, which will be a key tool for working with outside talent.

The simplest path forward is to identify funds in your industry of expertise and reach out. You can explore all of the models below with them. First, start by identifying the firms that invest in companies that you’ve worked with. Then, more broadly, look for investors in the industries in which you have expertise. You can identify institutional investors through one of multiple online databases:

| All investors | Private equity | Venture capital |

| Preqin (free demo)

Grey House (free demo) |

PitchBook (free trial)

PrivateEquityFirms.com |

AngelList (free)

CrunchBase (free) PWC MoneyTree (free) VentureDeal (free trial) Asian Venture Capital Journal (free trial) |

Let’s take a look at the different ways you can work with the investment community.

Expert network firms source subject matter experts from various domains and pair them with clients seeking topical or industry insights. They typically charge clients up to $1,200 per hour, and pay the expert $100 to $500 an hour. I founded Circle of Experts, an expert network that I sold to Evalueserve.

The expert network industry has grown an average 4.5% annually between 2015 and 2020, its market size topping $1.3 billion in 2020. While the major clients were initially hedge funds and private equity firms, consulting firms now comprise 32% of total demand for expert network services.

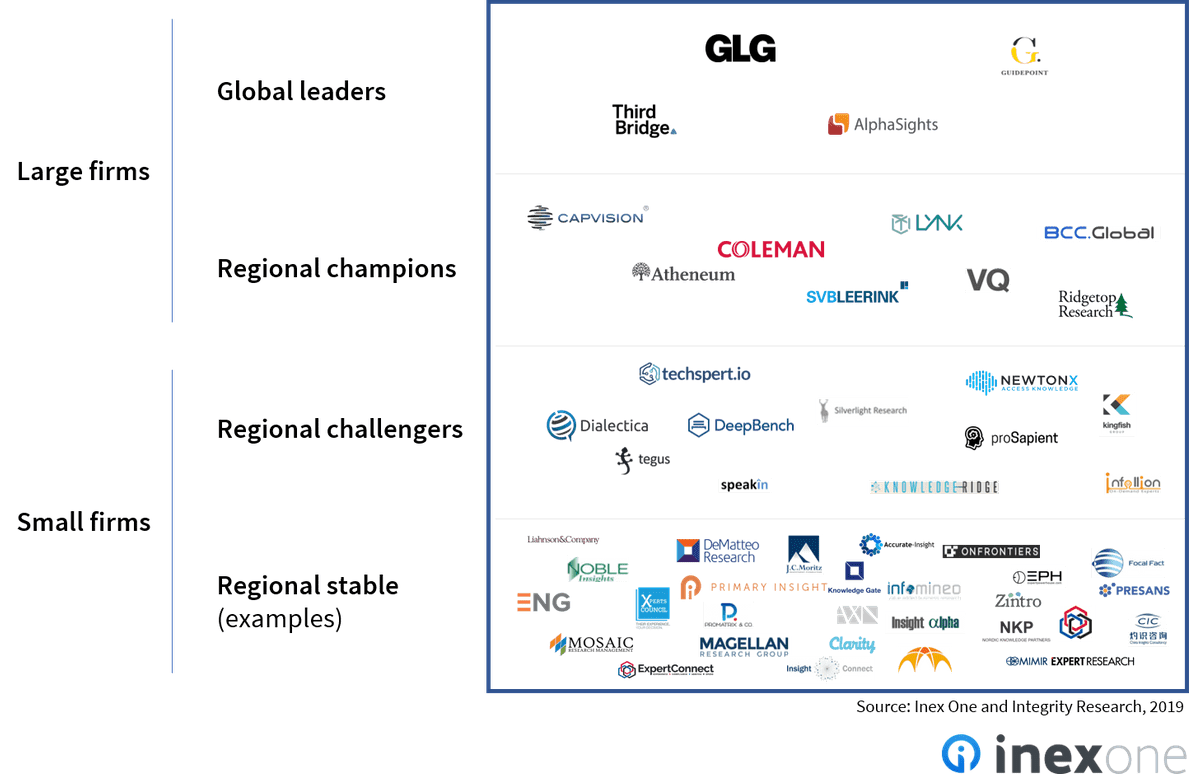

Inex One, an expert network marketplace, has compiled a list of 80 expert networks, summarized in the graphic below:

Image Credits: Inex One and Integrity Research

The largest expert networks include: GLG, which accounts for approximately 50% of the industry’s revenue; AlphaSights is the second biggest generalist expert network; Guidepoint services six major categories of clients globally across several industries; and Third Bridge hires and retains talent to “democratize the world’s human insights and upend the traditional research model.”

Other notable expert networks include Atheneum Partners, Coleman Research Group, Dialectica, ENG, Lynk Global, Mosaic, PreScouter, ProSapient and Tegus. There are also expert networks with sector or geography specialization. For example, SERMO is a global social media network for physicians to exchange knowledge and share challenging patient cases, and Clarity.fm connects startups to experts in building new businesses.

Powered by WPeMatico

Customers have been “experiencing” business since the ancient Romans browsed the Forum for produce, pottery and leather goods. But digitization has radically recalibrated the buyer-seller dynamic, fueling the rise of one of the most talked-about industry acronyms: CX (customer experience).

Part paradigm, part category and part multibillion-dollar market, CX is a broad term used across a myriad of contexts. But great CX boils down to delighting every customer on an emotional level, anytime and anywhere a business interaction takes place.

Great CX boils down to delighting every customer on an emotional level, anytime and anywhere a business interaction takes place.

Optimizing CX requires a sophisticated tool stack. Customer behavior should be tracked, their needs must be understood, and opportunities to engage proactively must be identified. Wall Street, for one, is taking note: Qualtrics, the creator of “XM” (experience management) as a category, was spun-out from SAP and IPO’d in January, and Sprinklr, a social media listening solution that has expanded into a “Digital CXM” platform, recently filed to go public.

Thinking critically about customer experience is hardly a new concept, but a few factors are spurring an inflection point in investment by enterprises and VCs.

Firstly, brands are now expected to create a consistent, cohesive experience across multiple channels, both online and offline, with an ever-increasing focus on the former. Customer experience and the digital customer experience are rapidly becoming synonymous.

The sheer volume of customer data has also reached new heights. As a McKinsey report put it, “Today, companies can regularly, lawfully, and seamlessly collect smartphone and interaction data from across their customer, financial, and operations systems, yielding deep insights about their customers … These companies can better understand their interactions with customers and even preempt problems in customer journeys. Their customers are reaping benefits: Think quick compensation for a flight delay, or outreach from an insurance company when a patient is having trouble resolving a problem.”

Moreover, the app economy continues to raise the bar on user experience, and end users have less patience than ever before. Each time Netflix displays just the right movie, Instagram recommends just the right shoes, or TikTok plays just the right dog video, people are being trained to demand just a bit more magic.

Powered by WPeMatico