EC Column

Auto Added by WPeMatico

Auto Added by WPeMatico

Netflix has two CEOs: Co-founder Reed Hastings oversees the streaming side of the company, while Ted Sarandos guides Netflix’s content.

Warby Parker has co-CEOs as well — its co-founders went to college together. Other companies like the tech giant Oracle and luggage maker Away have shifted from having co-CEOs in recent years, sparking a wave of headlines suggesting that the model is broken.

It’s impossible to be in two places at once or clone yourself. With co-CEOs, you can effectively do just that.

While there isn’t a lot of research on companies with multiple CEOs, the data is more promising than the headlines would suggest. One study on public companies with co-CEOs revealed that the average tenure for co-CEOs, about 4.5 years, was comparable to solitary CEOs, “suggesting that this arrangement is more stable than previously believed.”

The study’s authors also found that co-CEOs were spread across industry types and that splitting the role can “complement each other in terms of educational background or executive responsibilities.”

I serve as co-CEO of an organic meal delivery company with my sister Laureen. Having two CEOs has helped us take Fresh n’ Lean to new heights. We closed 2020 with $87 million in revenue, more than double from the year before, and project similar growth this year.

We complement each other well, and the results bear that out. During the decade that we’ve served as co-CEOs, the company has grown from a very small team to 475 full-time employees and 40 part-time employees. We’ve delivered more than 17 million meals, launched four different meal lines, expanded our retail offerings, partnered with some great names in sports and fitness, and saw our annual revenues climb exponentially.

The leadership structure isn’t for every company, but it’s been a great fit for Fresh n’ Lean. Here’s why.

Laureen launched the company in 2010 out of her one-bedroom apartment.

“Those early years were especially tough,” she said. “I consistently worked 20-hour days as I performed just about every role — cooking dishes, preparing labels, making deliveries and performing customer service duties. I was devoting so much energy into product, packaging and logistics, but in order for the company to grow, I needed help with marketing, tech and finance.”

Those areas happened to be my strengths. There was too much for one person to oversee as CEO and not enough hours in the day. But given the equal challenges that both sides of the company presented and the trust we shared, it made sense for us to be side by side on the organizational chart.

Powered by WPeMatico

Venture capitalists add value in a number of ways. For example, one of my business’ backers has a deep tech “pod” that generates events and content we are always welcomed to be a part of. Another one of our investors gives us full commercial support through its network of mentors that are there to support the business, not the VC.

Due diligence works both ways, and entrepreneurs shouldn’t be in a rush to take investment from anyone that offers it.

I might not expect that from every VC, but if they promise those “assets” by saying that they are here to drive innovation and growth, then I expect them to deliver, just as I have to back up the claim of having a team of supersmart machine learning researchers.

They might know the forks in the road, directions to take, and who to speak to based on having been through the process with similar companies. They might have venture partners that can mentor you and a network of investors that can participate in follow-on rounds. That is where they add value.

The best ones will seek to connect with you personally. They’ll have prepared thoroughly beforehand and are brimming with questions. While they may have preconceived and potentially ill-informed ideas, they demonstrate enthusiasm by starting sentences with “what if,” and they leave me emboldened but contemplative. I fully expect to be provoked in the right way.

However, some also play God. One experience offered up a major warning sign, one that would make me walk on by.

I’m pleased to say my business has some outstanding investors who totally get it. Our investors’ head of investment told representatives at one of New York’s top funds that one of their leading deep tech portfolio companies was coming to town for a “blitz meeting session.” They announced that they were committing to the round I was raising and that we were looking for a new lead investor.

So, put it this way: I wasn’t a guy who walked off the street with a crazy idea, but you might have thought otherwise, given the experience that followed. To be clear, I don’t expect all VCs to open their arms and embrace everyone, but there are rules of engagement.

After a very positive morning meeting, I’d scheduled a couple of hours for a quick chance to grab a breather at my hotel. Flicking through my phone, an email from the associate at the VC I was due to meet next pinged into my inbox.

“Hey Ofri, it’s Jessica [not her real name], really sorry, I’m not feeling great so am thinking I might cut the day short. I know you’re only in New York the next two days, so let’s catch up later on a call and next time you’re over I’m sure we can revisit.”

I started composing a polite response: “Really sorry to hear that. Absolutely fine to reschedule. Let me know your availability, etc., etc.” In truth, I was irritated — this had been in the diary for two months and was one of six meetings scheduled. I was not sorry; I was annoyed.

Powered by WPeMatico

Every company wants to be innovative, but innovation comes with its share of difficulties. One key challenge for early-stage companies that are disrupting a particular space or creating a new category is figuring out how to sell a unique product to customers who have never bought such a solution.

This is especially the case when a solution doesn’t have many reference points and its significance may not be obvious.

My view is simple — some buyers could use a walkthrough of the buying process. If you are building a singular product in a nascent market that necessitates forward-looking customers and want to drastically shorten sales cycles, I have a proposal: Create a buyer’s guide.

A buyer’s guide is essentially a prescriptive summary that provides an understandable overview of how a customer may buy your solution.

A buyer’s guide is essentially a prescriptive summary that provides an understandable overview of how a customer may buy your solution. What does your product actually do? Is it secure? How would you implement the technology? What does it replace, if anything? It should be short, simple and speak the customer’s language. It also acts as a sales-enabling tool. Sales teams, especially at smaller startups, can review the guide quarterly and analyze what is and isn’t working as the company goes to market.

Here is how to put together a buyer’s guide, including what to sort out before you type a single word.

From the start, it’s important to think about who the stakeholders are for your product’s buying cycle. One typical issue with early-stage startups is they meet with an enthusiastic buyer — a CIO, CTO or VP of product — but neglect to include the other stakeholders who should be part of the conversation. More importantly, a lot of companies don’t realize the impact of their product on a group or team that they would not typically sell to.

For example, target the security team as an early stakeholder, because they’re probably going to review your product. If the solution is focused toward, say, integration, then hone in on who would be owning the integration process on the buyer’s team.

If you’re selling a martech solution, on a business level, you have to consider a finance business partner for marketing. Think about the problems your customers face and also how others in their company relate to them.

Powered by WPeMatico

An estimated 41 million Americans say they need life insurance but have yet to purchase coverage. Despite this awareness among consumers, the Life Insurance Marketing and Research Association estimates a $12 trillion coverage gap, with about 50% of millennials planning to purchase coverage within the next year.

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution. It’s imperative for companies to consider product lines and partnerships to expand markets, create new revenue streams and provide added value to their customers.

There’s latent demand for life insurance currently unaddressed by much of the financial services industry, and embedded finance can be the solution.

Connecting consumers with products they need through channels they already know and trust is both a massive revenue opportunity and a social good, providing financial resilience to families at a time when they need it most.

The concept of digitally bundling financial products in a packaged offering to a customer is certainly not new — but it is for the life insurance space.

Embedded finance uses technology and operations infrastructure to offer products and services through entities that may not be financial institutions at all. Think of embedded finance like on-demand shopping; customers benefit from both the transaction (buying financial protection for their families) and the convenience it provides (from whatever platform they are currently engaging with).

Similar to how Amazon saves shoppers 75 hours a year, bundling life insurance gives consumers back time in their day and can improve their financial health.

Powered by WPeMatico

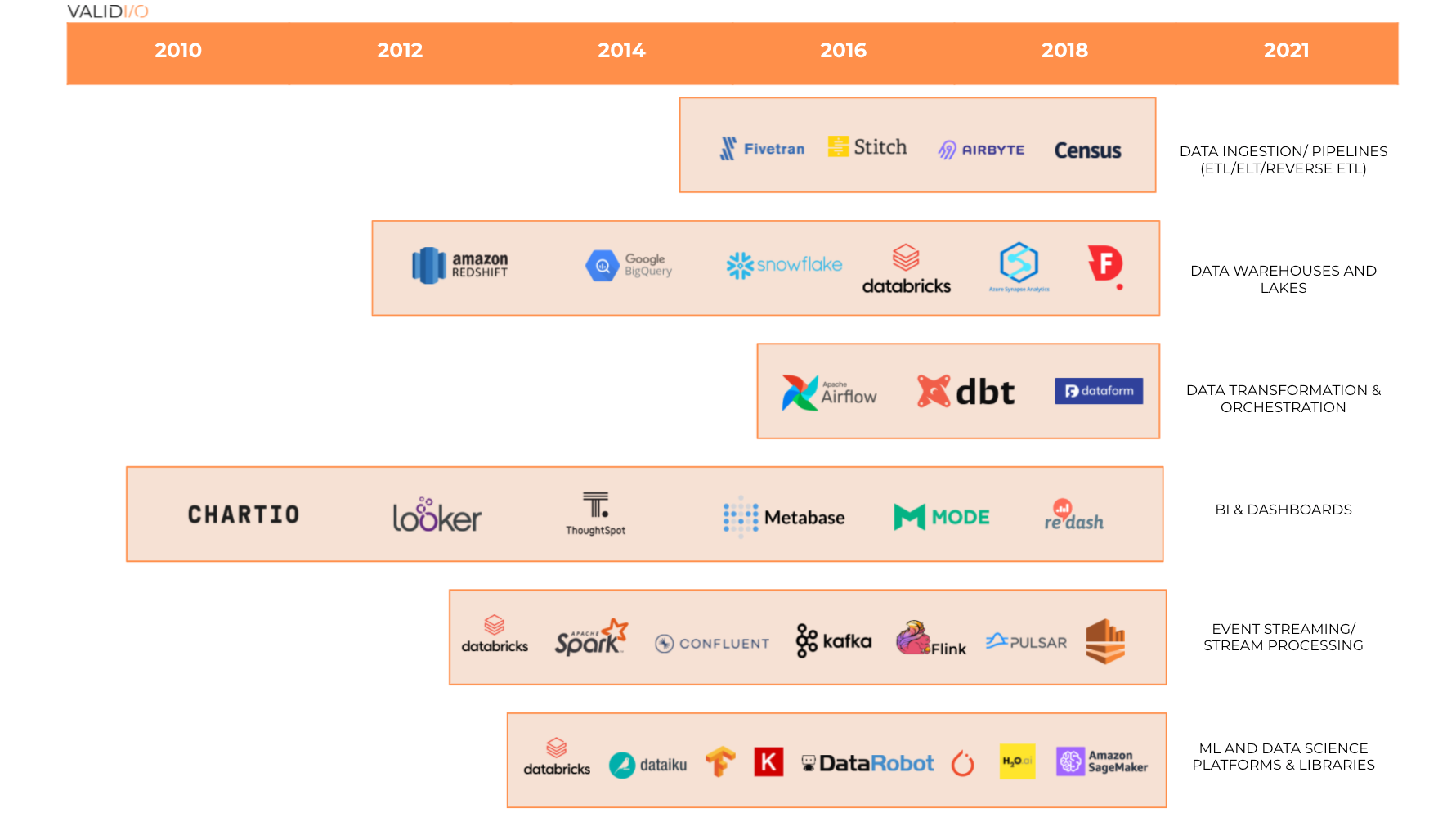

A little over a decade has passed since The Economist warned us that we would soon be drowning in data. The modern data stack has emerged as a proposed life-jacket for this data flood — spearheaded by Silicon Valley startups such as Snowflake, Databricks and Confluent.

Today, any entrepreneur can sign up for BigQuery or Snowflake and have a data solution that can scale with their business in a matter of hours. The emergence of cheap, flexible and scalable data storage solutions was largely a response to changing needs spurred by the massive explosion of data.

Currently, the world produces 2.5 quintillion bytes of data daily (there are 18 zeros in a quintillion). The explosion of data continues in the roaring ‘20s, both in terms of generation and storage — the amount of stored data is expected to continue to double at least every four years. However, one integral part of modern data infrastructure still lacks solutions suitable for the Big Data era and its challenges: Monitoring of data quality and data validation.

Let me go through how we got here and the challenges ahead for data quality.

In 2005, Tim O’Reilly published his groundbreaking article “What is Web 2.0?”, truly setting off the Big Data race. The same year, Roger Mougalas from O’Reilly introduced the term “Big Data” in its modern context — referring to a large set of data that is virtually impossible to manage and process using traditional BI tools.

Back in 2005, one of the biggest challenges with data was managing large volumes of it, as data infrastructure tooling was expensive and inflexible, and the cloud market was still in its infancy (AWS didn’t publicly launch until 2006). The other was speed: As Tristan Handy from Fishtown Analytics (the company behind dbt) notes, before Redshift launched in 2012, performing relatively straightforward analyses could be incredibly time-consuming even with medium-sized data sets. An entire data tooling ecosystem has since been created to mitigate these two problems.

The emergence of the modern data stack (example logos and categories). Image Credits: Validio

Scaling relational databases and data warehouse appliances used to be a real challenge. Only 10 years ago, a company that wanted to understand customer behavior had to buy and rack servers before its engineers and data scientists could work on generating insights. Data and its surrounding infrastructure was expensive, so only the biggest companies could afford large-scale data ingestion and storage.

The challenge before us is to ensure that the large volumes of Big Data are of sufficiently high quality before they’re used.

Then came a (Red)shift. In October 2012, AWS presented the first viable solution to the scale challenge with Redshift — a cloud-native, massively parallel processing (MPP) database that anyone could use for a monthly price of a pair of sneakers ($100) — about 1,000x cheaper than the previous “local-server” setup. With a price drop of this magnitude, the floodgates opened and every company, big or small, could now store and process massive amounts of data and unlock new opportunities.

As Jamin Ball from Altimeter Capital summarizes, Redshift was a big deal because it was the first cloud-native OLAP warehouse and reduced the cost of owning an OLAP database by orders of magnitude. The speed of processing analytical queries also increased dramatically. And later on (Snowflake pioneered this), they separated computing and storage, which, in overly simplified terms, meant customers could scale their storage and computing resources independently.

What did this all mean? An explosion of data collection and storage.

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

Extra Crunch members receive access to weekly “Dear Sophie” columns; use promo code ALCORN to purchase a one- or two-year subscription for 50% off.

Dear Sophie,

Our startup employs several individuals who are on work visas or have employment authorization. Many of them have been waiting for quite a while for the government to tell them their applications have been received.

Why? When will things be back on track? We have a few employees who are waiting for green cards, and a few F-1 visa holders who will be extending their OPT to STEM OPT.

Is there anything we can do?

— Patient in Pasadena

Dear Patient,

Thanks for your questions. Last September, an increase in applications submitted to U.S. Citizenship and Immigration Services (USCIS) amid COVID-19-related staff reductions created a substantial backlog and subsequent delay in USCIS sending out receipt notices.

My law firm partner, Anita Koumriqian, and I provided an update on receipt notices on a recent podcast. Dedicating an entire episode to receipt notices was unthinkable a year ago because applicants usually received receipt notices within one to three weeks after USCIS received their application.

For those who don’t know, USCIS sends a letter called a receipt notice to applicants when it receives an application. The receipt notice — also known as a Notice of Action or Form I-797 — contains information about:

Before the pandemic, applicants would typically be notified in less than one month after USCIS received their application. Currently, applicants are receiving their receipt notice as long as eight to nine weeks after USCIS received their application, and sometimes longer.

As I mentioned earlier, coronavirus-related staffing reductions at USCIS coupled with a substantial jump in the number of applications submitted prompted huge delays that began in September. Application submissions surged primarily due to:

Powered by WPeMatico

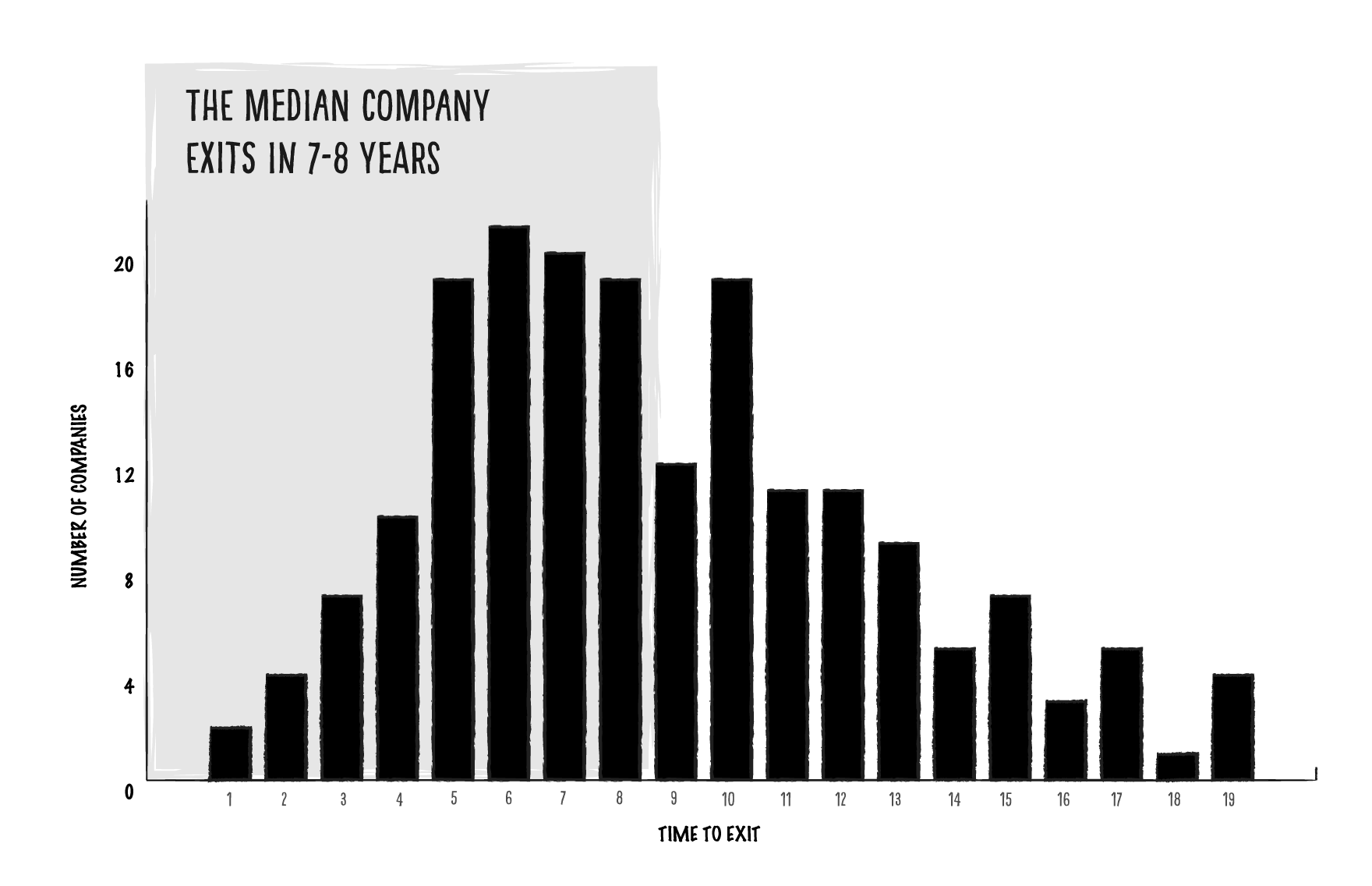

Does it really take an average of seven to eight years for a successful startup to exit? What can early-stage founders do to accelerate outcomes?

We wanted to know if founding teams can execute faster with a higher degree of success if they’re able to take advantage of relevant executive expertise. After all, that’s the thesis we built our venture model around — we purposefully designed M13 so that early-stage founders get access to experienced executives they wouldn’t otherwise have the money to hire or the time to vet, onboard and manage.

Even if companies are doing everything right, they still reduce time to exit when they have multiple founders with prior relevant experience as a senior leader or operator.

We looked at years of data from hundreds of successful startups. As it turns out, the impact of relevant executive expertise is even greater than we had anticipated — to the tune of doubling the rate of return on a venture investment.

When it comes to measuring leadership experience, information about an individual executive’s experience — for example, how long they’ve been an exec — is publicly available. Unfortunately, there isn’t readily available structured data around a founding team’s seniority and how early the founders bring on people with more experience as an operator or leader.

To find out if leadership experience significantly impacts startups’ success, we analyzed nearly 800 executives at more than 200 companies that reached a sizable exit (greater than or equal to a $500 million valuation) via an IPO on a U.S. exchange or an exit via M&A from 2004-2019. About 70% of the companies in our dataset exited between 2016-2019, including notable IPOs like Spotify, Zoom, Uber and Peloton. We decided to exclude companies in the biotech/life sciences space because these companies follow a different growth trajectory than consumer tech and B2B tech and traditionally exit via IPO or M&A at a much earlier stage.

Here’s what our analysis of startups with successful exits revealed.

While there are other intangible variables for startup success, the basic equation is the time and capital required to achieve an exit and the size of that exit.

Our dataset validates the widely accepted statement that successful exits take about seven to eight years:

Image Credits: M13

But could a variable like relevant leadership experience actually accelerate the time to exit? We wondered: Beyond time and capital, are there any factors — like experience as a leader or operator — that can have an exponential impact on the exit outcome? And when is the right time for those human capital resources to be introduced to make that impact?

Powered by WPeMatico

Whether you’re building a company or thinking about investing, it’s important to understand your strategic advantage. In order to determine one, you should ask fundamental questions like: What’s the long-term, sustainable reason that the company will stay in business?

The most important elements for founders to consider when figuring out their strategic advantage(s) include one-sided or “direct” network effects (e.g., with social media sites like Facebook), marketplace network effects (e.g., with two-sided marketplaces like Uber), data moats, first mover and switching costs.

Let’s take a quick look at an example of one-sided network effects. At the very earliest stages of Facebook’s existence, it was just Mark Zuckerberg, a few friends and their basic profiles. The nascent social media platform wasn’t useful beyond a few dorm rooms. They needed a strategic advantage or the company would not make it beyond the edge of campus.

A successful startup without a strategic advantage is just a validated business model vulnerable to copycat companies looking for a market entry point.

In fact, Facebook only truly became a useful platform — and accelerated as a business — when more users came into the fold and more types of email addresses were accepted. Add to that the introduction of an ad marketplace revenue model and you have a clear strategic advantage — based on one-sided network effects — that gave Facebook a strategic edge over other early social media sites like MySpace.

These one-sided network effects are different from two-sided network effects.

Image Credits: Canvas Ventures

Two-sided network effects are most common in marketplace business models. In a two-sided network, supply and demand are matched, like Uber riders (demand) being matched with Uber drivers (supply). The Uber product is not necessarily more valuable just because more users (riders) join, the way Facebook is more valuable when more users join.

In fact, when more users (riders) join the demand side of the Uber network, it might actually be worse for the user experience — it’s harder to find a driver and wait times get longer. The demand side (riders) gets value from more supply (drivers) joining the platform and vice-versa. That’s why it’s called a two-sided network, or a marketplace.

Regardless of industry, a successful startup without a strategic advantage is just a validated business model vulnerable to copycat companies looking for a market entry point. Copycats can range in size from startups with similar grit to large companies like Facebook or Google that have limitless resources to drive competition into the market, and potentially run the startup with the original idea out of business. This vulnerability can prove fatal unless a startup’s founding team explores and embraces one or more strategic advantages.

Powered by WPeMatico

There’s a lot of noise out there. The ability to effectively communicate can make or break your launch. It will play a role in determining who wins a new space — you or a competitor.

Most people get that. I get emails every week from companies coming out of stealth mode, wanting to make a splash. Or from a Series B company that’s been around for a while and hopes to improve their branding/messaging/positioning so that a new upstart doesn’t eat their lunch.

You have to stop thinking that what you are up to is interesting.

How do you make a splash? How do you stay relevant?

Worth noting is that my area of expertise is in the DevOps space and that slant may crop up occasionally. But these five specific tips should be applicable to virtually any startup.

This is especially important if you are a small startup that not many people know about. Journalists don’t want to hear opinions from your head of marketing or product — they want to hear from the founders. What problems are they solving? What unique opinions do they have about the market? These are insights that mean the most coming from the people that started the company. So if you don’t have at least one founder that can dedicate time to being the face, then PR is going to be an uphill battle.

That doesn’t mean there isn’t plenty to do to support these efforts. Create a list of all the journalists that have written about your competitors. Read those articles. How can your founder add value to these conversations? Where should you be contributing thought leadership? What are the most interesting perspectives you can offer to those audiences?

This is legwork and research you can do before looping founders into the conversation. Getting your PR going can be like trying to push a broken-down car up the road: If the founders see you exerting effort to get things moving on your own, they’re more likely to get beside you and help.

Here’s an example: It may be unreasonable to ask a founder to sit down and write a 1,000-word thought leadership piece by the end of the week, but they very likely have 20 minutes to chat, especially if you make it clear that the contents of the conversation will make for great thought leadership pieces, social media posts, etc.

The flow looks like:

Powered by WPeMatico

Search engine optimization, PR, paid marketing, emails, social — marketing and communications is crowded with techniques, channels, solutions and acronyms. It’s little wonder that many startups strapped for time and money find defining and executing a sustainable marketing campaign a daunting prospect.

The sheer number of options makes it difficult to determine an effective approach, and my view is that this complexity often obscures the obvious answer: A startup’s best marketing asset is its story. The knowledge and expertise of its team, together with the why and the how of its offering provides the most compelling content.

Leveraging this material with best practice techniques enables any startup, no matter how limited its budget, to run an effective marketing campaign.

Many startups make the mistake of choosing systems and employing procedures to solve the immediate needs of the department that requires them.

I know this approach works, because this is exactly what I did with my co-founder Alex Feiglstorfer when we set up Storyblok. To be clear, we are developers not marketers. However, our previous experience building CMS systems taught us that the main driver of organic engagement for most businesses was customer conversations around content.

Specifically, sharing experiences, expertise and what we learned. We had committed nearly all of our available cash to developing our product, so we knew that the only way to market Storyblok was to do it all ourselves.

As a result, we focused solely on problem-solving content. This took the form of tutorials on web development and opinion pieces on headless CMS and other topics within our areas of expertise. The trick was that what we published wasn’t made just for marketing, it was based on our own internal documentation of problems we encountered as we developed our product. In essence, we were “learning in public.” Through this approach we were able to acquire thousands of customers in our first year.

Retelling this story isn’t to blow my own trumpet, it’s to make clear that you don’t have to be a marketer by training or commit a huge amount of time and resources to successfully market your startup. So, how do you get started?

Although there’s no one-size-fits-all approach to how you organize your startup’s marketing function, there are some basic principles that apply in nearly every situation. A recent survey of 400+ executives from CMS Wire helpfully identified the following factors as the “top digital customer experience challenges” for businesses:

Challenges two to four are the pitfalls that we can focus on avoiding. They are directly related to how a startup produces, organizes and distributes its content.

With regard to the siloing of systems and fragmentation of customer data, the overriding goal is to ensure all your systems are integrated and speak to one another. In practice, this means that the data gathered in different departments — whether its feedback from sales, engagement on your website, customer service responses or product development information — is collected in a uniform and methodical manner and is readily accessible across the business.

Powered by WPeMatico