EC Column

Auto Added by WPeMatico

Auto Added by WPeMatico

The world has spent most of 2020 adapting to ever-changing guidelines and restrictions (with no end in sight, even as the vaccines start to roll out). Board meetings are quickly increasing in their significance to foster consistent and vital interactions as an organization. It’s essential for companies to capitalize on the essential time together during these uncertain times.

While we might look like the Brady Bunch while sharing a Zoom window, are you actually communicating more like the family from “Succession?”

Are your meetings organized? Do people talk over one another? Do you usually run over time? Are you giving people time to digest information?

As we move into 2021 and Q1 meetings are being put onto calendars, take some time to modernize how you conduct your board meetings.

Board meetings are quickly increasing in their significance to foster consistent and vital interactions as an organization.

Having served on public company boards, growth-stage businesses and Series A startups, an observation I have made in boards that are later stage are more about financial analysis and governance. Whereas earlier-stage board discussions hinge more on product strategy, key partnerships, sharing best practices to help develop founders as executives and important hiring decisions.

Since the nature of the discussions is more, let’s call it … creative in earlier-stage businesses, where the focus is on where they’ve been particularly impacted by reduced bandwidth for collaboration while meeting remotely.

As said best by Mike Maples and paraphrased by Jeff Bonforte — there are only four things a board really needs to consider:

Collecting data around those points is the job. In the meeting, the team can add color.

Remember the board works for you, so be sure to put them to work. Sharing materials with participants about three days ahead of time tends to be the best. Any later and they may not get enough time to digest, send earlier and the information might be out of date by the time you meet. It’s most common to format as a deck, but lately I’m seeing more written format and even magazine-style.

The number one request I get from early-stage companies is “help find me more customers.”

Other common requests are “help me find or land this type of talent, help me with industry benchmarks for this type of business deal or compensation structure, connect me to people that have experience with X so I can learn ways we could structure our process.” It’s helpful to put these asks in the materials you send ahead because sometimes board members might not be able to react quickly and now “homework” comes up spontaneously in the discussions.

Another purpose of these meetings is to build working relationships so when strategic decisions need to be made, board members are used to working together. Sometimes it is a forum for executives to gain exposure to board members and for board members to have the opportunity to evaluate and provide input on executives. For that reason execs are often invited to participate in certain discussions.

Like the product person who presents a roadmap or a market analysis, the head of sales should give color on pipeline and competitive deals, the marketing person may lead a discussion on ABM or channel marketing tactics, the engineering lead might ask for feedback on their metrics versus other companies, etc. Generally, CEOs also bring forth an interesting topic to have a discussion, such as channel strategy, market mapping/sizing, hiring plan and related issues.

As far as logistics, we reserve two hours in calendars but we try to hit 90 minutes. I suggest something like this for a 90-minute session:

Powered by WPeMatico

Fundraising is challenging, especially for deep tech founders who need to get investors excited about a complex technology, a complex sales cycle and a complex risk profile.

As a former investor and current angel investor, I have met thousands of founders, many in the deep tech space.

Based on my experience, here’s how to avoid making the most common mistakes deep tech founders make when pitching investors:

Early-stage investors are in the business of funding dreams. They chose to be early-stage investors because they love hearing about new ideas and enthralling futures. They deliberately are not investment bankers or accountants because they do not want to constantly pour over endless spreadsheets or dive deep into financial models. Similarly, they are not operators because they do not want to spend time figuring out the intricacies of a supply chain or a marketing campaign or the configuration of a product component.

Make your pitch tailored to what excites venture capital investors and avoid what does not.

So make your pitch tailored to what excites venture capital investors and avoid what does not. Keep the financial model details and the warehouse system logistics information to your Appendix. You have it in case anyone wants to dive in deeper, but your core presentation should be focused on your biggest, most bullish hopes for the company seven to 10 years from now. Dedicate multiple slides to painting the picture of what society would look like should you meet all your intended milestones as a company.

As a deep tech company, your differentiation is in your intellectual property. However, investors care less about the “what” and much more about the “so what.” Investors are less interested in the intricacies of your technology and more interested in what impact it can create.

Formulate your slides to focus on answering questions like, “What can people or companies do as a result of your technology?” and “How will people save time, money and lives with your product?”

Put your presentation to the “grandma” test. Would your grandmother be able to understand and be excited about everything you share? Investor pitch meetings are not dissertation defenses. You are being evaluated on your potential for impact rather than the intricate details of your research. The best way to succeed in this evaluation framework is to ensure that everything you share is relevant and exciting to a diverse audience of even nontechnical folks.

Five million people are a statistic, but one person is a story. When people read data on massive populations of people, they conceptually understand the implications but only on a logical level, not an emotional one. When pitching, you want to reach the hearts of investors.

Powered by WPeMatico

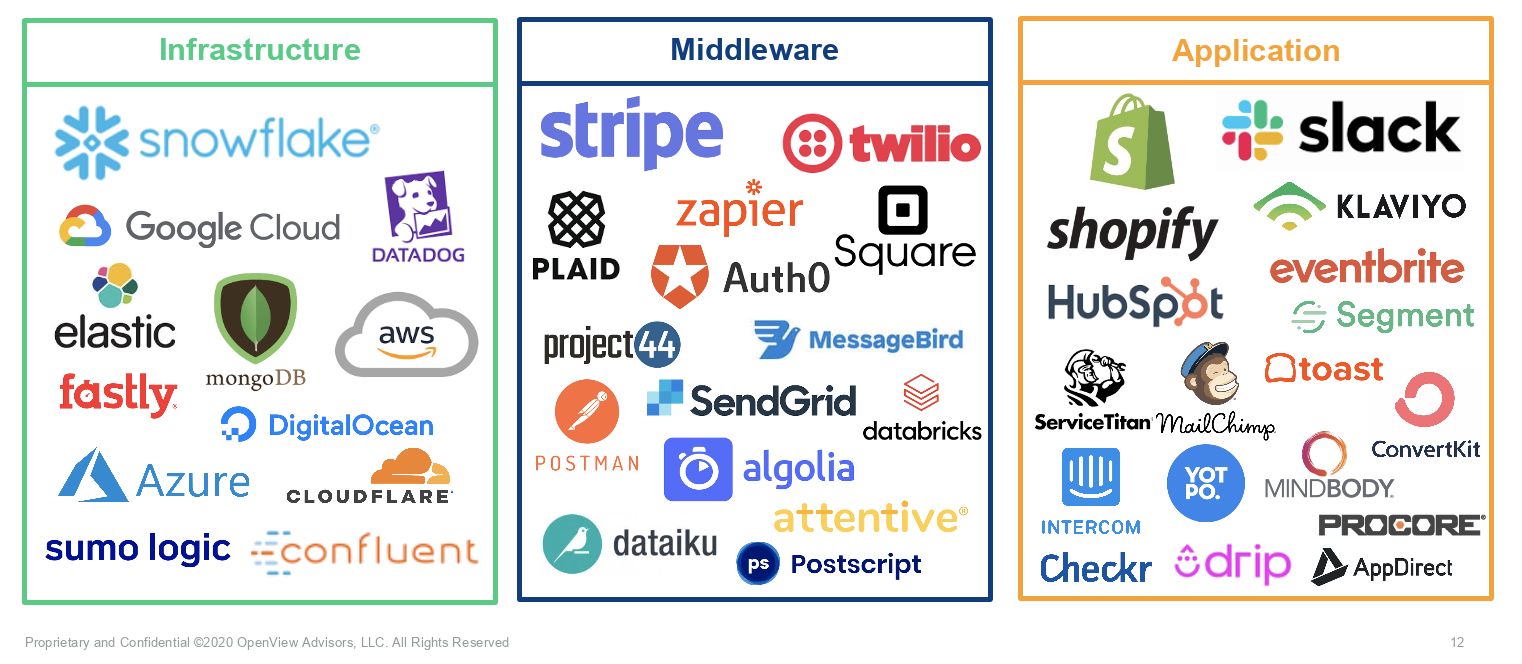

Software buying has evolved. The days of executives choosing software for their employees based on IT compatibility or KPIs are gone. Employees now tell their boss what to buy. This is why we’re seeing more and more SaaS companies — Datadog, Twilio, AWS, Snowflake and Stripe, to name a few — find success with a usage-based pricing model.

The usage-based model allows a customer to start at a low cost, while still preserving the ability to monetize a customer over time.

The usage-based model allows a customer to start at a low cost, minimizing friction to getting started while still preserving the ability to monetize a customer over time because the price is directly tied with the value a customer receives. Not limiting the number of users who can access the software, customers are able to find new use cases — which leads to more long-term success and higher lifetime value.

While we aren’t going 100% usage-based overnight, looking at some of the megatrends in software — automation, AI and APIs — the value of a product normally doesn’t scale with more logins. Usage-based pricing will be the key to successful monetization in the future. Here are four top tips to help companies scale to $100+ million ARR with this model.

Usage-based pricing is in all layers of the tech stack. Though it was pioneered in the infrastructure layer (think: AWS and Azure), it’s becoming increasingly popular for API-based products and application software — across infrastructure, middleware and applications.

Image Credits: Kyle Povar / OpenView

Some fear that investors will hate usage-based pricing because customers aren’t locked into a subscription. But, investors actually see it as a sign that customers are seeing value from a product and there’s no shelf-ware.

In fact, investors are increasingly rewarding usage-based companies in the market. Usage-based companies are trading at a 50% revenue multiple premium over their peers.

Investors especially love how the usage-based pricing model pairs with the land-and-expand business model. And of the IPOs over the last three years, seven of the nine that had the best net dollar retention all have a usage-based model. Snowflake in particular is off the charts with a 158% net dollar retention.

Powered by WPeMatico

June 4, 2019 should have been one of the happiest days of my life.

At 11:30 a.m., a press release hit the wire announcing that the cybersecurity company I had spent more than eight years building was being acquired by a larger cybersecurity player.

What’s not to love about a successful exit? I’d be set financially, the investors who had given us $70 million would make money, and the technology we created would get new legs in an organization with broader reach and resources.

Still, I had regrets. For one thing, I initially hadn’t wanted to sell. (More on that later.) For another, I was nagged by the feeling that our company had fallen short of its true potential, and that the reason was me — specifically, several rookie mistakes I made as a first-time entrepreneur.

I don’t stew about those errors any longer. In fact, I believe my miscues at my first startup will help define my career from here on out. That’s why, as I grow my next company, I’m thinking about not only the things I want to do but those I’d never do again.

Here are five of them.

In management theory terms, I was a “pacesetter.” I’d be the first to jump into any project or task, I’d execute it as quickly as possible and I expected everyone else to keep up. I thought that was how a startup leader acted — super helpful and scrappy.

But it came at a big price: disempowerment of the team. I was hoarding not only control — nobody felt like they personally owned anything — but also the institutional knowledge that needs to be spread around as a company grows. I became a human GPS: People could follow my directions, but they struggled to find the way themselves. Independent thinking suffered.

I became a human GPS: People could follow my directions, but they struggled to find the way themselves. Independent thinking suffered.

After a few years, I had a frustrating sense that I had all the answers and no one else did. Well, no wonder.

I’m now leaving the pacesetting to NASCAR and marathons.

I believed all I had to do was say something once and everyone would get it. I became irritated when that didn’t happen. “We talked about this three months ago,” I’d bark. Intimidated team members would say to themselves, “Yeah, but we really only got 50% of it.”

Powered by WPeMatico

Three years ago, we released the first edition of the Matrix Fintech Index. We believed then, as we do now, that fintech represents one of the most exciting major innovation cycles of this decade. In 2020, all the long-term trends forcing change in this sector continued and even accelerated.

The broad movement away from credit toward debit, particularly among younger consumers, represents one such macro shift. However, the pandemic also created new, unforeseen drivers. Among them, millennials decamped from their rentals in crowded cities to accelerate their first home purchases to the benefit of proptech companies and challenger mortgage players alike.

E-commerce saw an enormous acceleration in growth rates, furthering adoption of online payments platforms. Lastly, low interest rates and looming inflation helped pave the way for the price of Bitcoin to charge toward $30,000. In short, multiple tailwinds combined to produce a blockbuster year for the category.

In this year’s refresh of the Matrix Fintech Index, we’ll divide our attention into three parts. First, a look at the public stocks’ performance. Second, liquidity. Third, we highlight one major trend in the sector: Buy Now Pay Later, or BNPL.

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index. While the underlying performance of these companies was strong, the pandemic further bolstered results as consumers avoided appearing in-person for both shopping and banking. Instead, they sought — and found — digital alternatives.

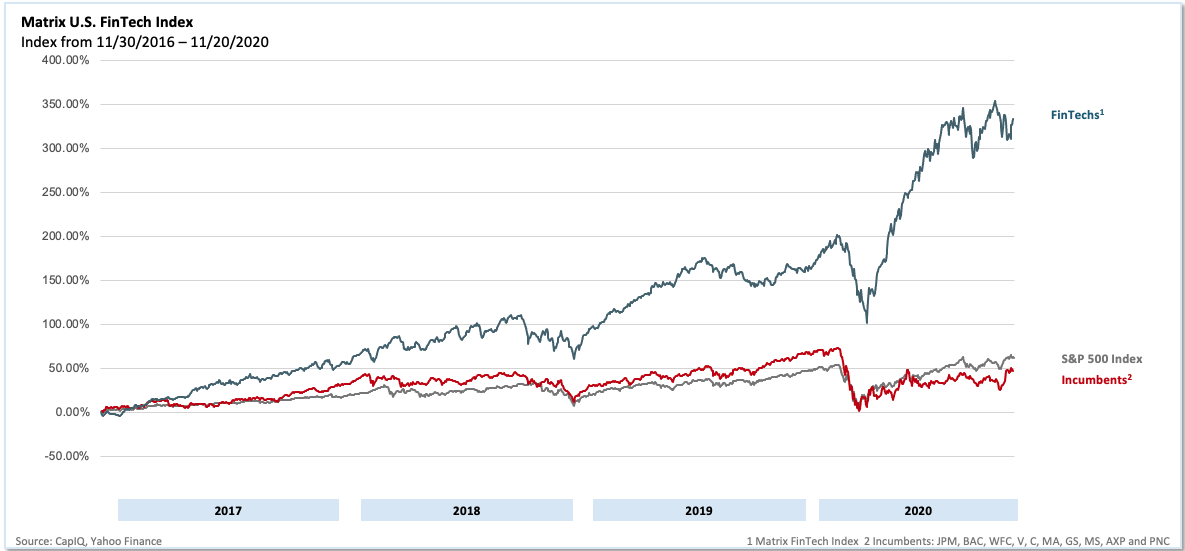

For the fourth straight year, the publicly traded fintechs massively outperformed the incumbent financial services providers as well as every mainstream stock index.

Our own representation of the public fintechs’ performance is the Matrix Fintech Index — a market cap-weighted index that tracks the progress of a portfolio of 25 leading public fintech companies. The Matrix fintech Index rose 97% in 2020, compared to a 14% rise in the S&P 500 and a 10% drop for the incumbent financial service companies over the same time period.

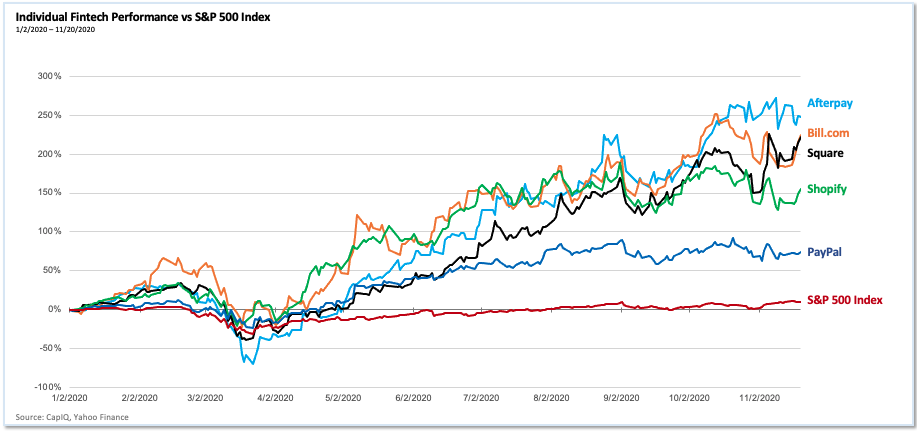

2020 performance of individual fintech companies vs. SPX Image Credits: CapiQ, Yahoo Finance

Matrix U.S. Fintech Index, 2016 -2020 Image Credits: CapiQ, Yahoo Finance

E-commerce undoubtedly stood out as a major driver. As a category, retail e-commerce grew 35% YoY as of Q3, propelling PayPal and Shopify to add over $160 billion of market capitalization over the year. For its part, PayPal in the third quarter signed up 15 million net new active accounts (its highest ever).

Powered by WPeMatico