CRM

Auto Added by WPeMatico

Auto Added by WPeMatico

As the biggest sales and marketing technology firms mature, they are all turning to AI and machine learning to advance the field. This morning it was Oracle’s turn, announcing several AI-fueled features for its suite of sales tools.

Rob Tarkoff, who had previous stints at EMC, Adobe and Lithium, and is now EVP of Oracle CX Cloud says that the company has found ways to increase efficiency in the sales and marketing process by using artificial intelligence to speed up previously manual workflows, while taking advantage of all the data that is part of modern sales and marketing.

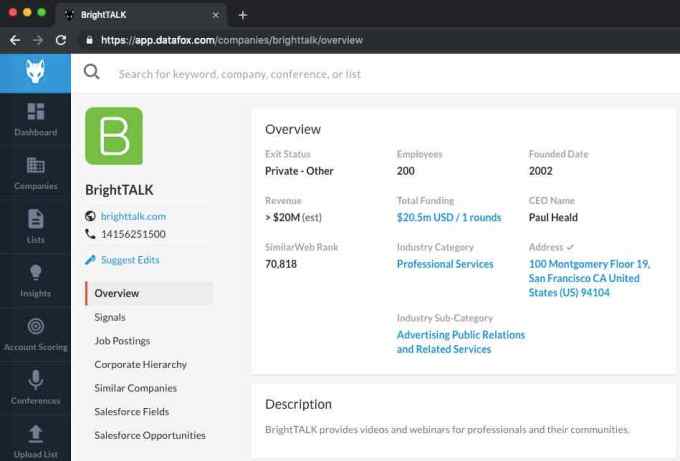

For starters, the company wants to help managers and salespeople understand the market better to identify the best prospects in the pipeline. To that end, Oracle is announcing integration with DataFox, the company it purchased last fall. The acquisition gave Oracle the ability to integrate highly detailed company profiles into their Customer Experience Cloud, including information such as SEC filings, job postings, news stories and other data about the company.

DataFox company profile. Screenshot: Oracle

“One of the things that DataFox helps you you do better is machine learning-driven sales planning, so you can take sales and account data and optimize territory assignments,” he explained.

The company also announced an AI sales planning tool. Tarkoff says that Oracle created this tool in conjunction with its ERP team. The goal is to use machine learning to help finance make more accurate performance predictions based on internal data.

“It’s really a competitor to companies like Anaplan, where we are now in the business of helping sales leaders optimize planning and forecasting, using predictive models to identify better future trends,” Tarkoff said.

Sales forecasting tool. Screenshot: Oracle

The final tool is really about increasing sales productivity by giving salespeople a virtual assistant. In this case, it’s a chatbot that can help handle tasks like scheduling meetings and offering task reminders to busy sales people, while allowing them to use their voices to enter information about calls and tasks. “We’ve invested a lot in chatbot technology, and a lot in algorithms to help our bots with specific dialogues that have sales- and marketing-industry specific schema and a lot of things that help optimize the automation in a rep’s experience working with sales planning tools,” Tarkoff said.

Brent Leary, principal at CRM Essentials, says that this kind of voice-driven assistant could make it easier to use CRM tools. “The Smarter Sales Assistant has the potential to not only improve the usability of the application, but by letting users interact with the system with their voice it should increase system usage,” he said.

All of these enhancements are designed to increase the level of automation and help sales teams run more efficiently with the ultimate goal of using data to more sales and making better use of sales personnel. They are hardly alone in this goal as competitors like Salesforce, Adobe and Microsoft are bringing a similar level of automation to their sales and marketing tools

The sales forecasting tool and the sales assistant are generally available starting today. The DataFox integration will GA in June.

Powered by WPeMatico

Salesforce is celebrating its 20th anniversary today. The company that was once a tiny irritant going after giants in the 1990s Customer Relationship Management (CRM) market, such as Oracle and Siebel Systems, has grown into a full-fledged SaaS powerhouse. With an annual run rate exceeding $14 billion, it is by far the most successful pure cloud application ever created.

Twenty years ago, it was just another startup with an idea, hoping to get a product out the door. By now, a legend has built up around the company’s origin story, not unlike Zuckerberg’s dorm room or Jobs’ garage, but it really did all begin in 1999 in an apartment in San Francisco, where a former Oracle executive named Marc Benioff teamed with a developer named Parker Harris to create a piece of business software that ran on the internet. They called it Salesforce .com.

None of the handful of employees who gathered in that apartment on the company’s first day in business in 1999 could possibly have imagined what it would become 20 years later, especially when you consider the start of the dot-com crash was just a year away.

It all began on March 8, 1999 in the apartment at 1449 Montgomery Street in San Francisco, the site of the first Salesforce office. The original gang of four employees consisted of Benioff and Harris and Harris’s two programming colleagues, Dave Moellenhoff and Frank Dominguez. They picked the location because Benioff lived close by.

March 8th 1999 Parker Harris, Dave Moellenhoff, Frank Dominguez, & I showed up at 1449 Montgomery Street & we started a company called https://t.co/GcJjXaxGXz & introduced the end of software (now called the the cloud). Congratulations @parkerharris on 20 amazing years! pic.twitter.com/qIbpbBl2C6

— Marc Benioff (@Benioff) March 5, 2019

It would be inaccurate to say Salesforce was the first to market with Software as a Service, a term, by the way, that would not actually emerge for years. In fact, there were a bunch of other fledgling enterprise software startups trying to do business online at the time, including NetLedger, which later changed its name to NetSuite and was eventually sold to Oracle for $9.3 billion in 2016.

Other online CRM competitors included Salesnet, RightNow Technologies and Upshot. All would be sold over the next several years. Only Salesforce survived as a standalone company. It would go public in 2004 and eventually grow to be one of the top 10 software companies in the world.

Co-founder and CTO Harris said recently that he had no way of knowing that any of that would happen, although having met Benioff, he thought there was potential for something great to happen. “Little did I know at that time, that in 20 years we would be such a successful company and have such an impact on the world,” Harris told TechCrunch.

It wasn’t entirely a coincidence that Benioff and Harris had connected. Benioff had taken a sabbatical from his job at Oracle and was taking a shot at building a sales automation tool that ran on the internet. Harris, Moellenhoff and Dominguez had been building salesforce automation software solutions, and the two visions meshed. But building a client-server solution and building one online were very different.

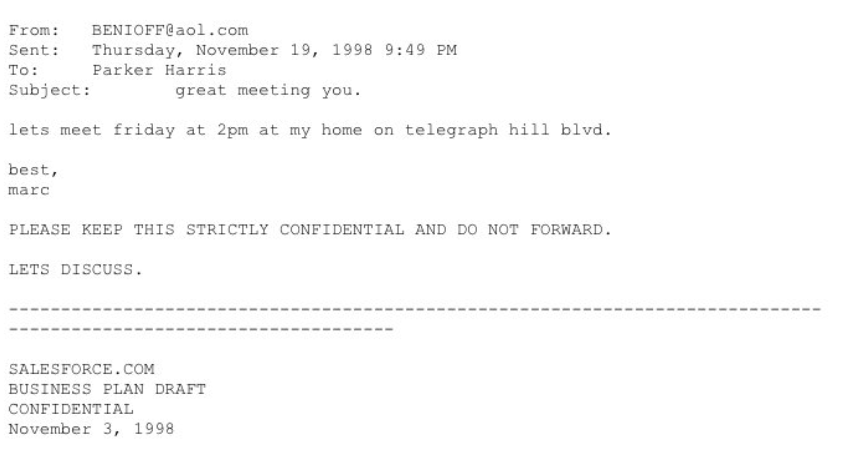

Original meeting request email from Marc Benioff to Parker Harris from 1998 (Email courtesy of Parker Harris)

You have to remember that in 1999, there was no concept of Infrastructure as a Service. It would be years before Amazon launched Amazon Elastic Compute Cloud in 2006, so Harris and his intrepid programming team were on their own when it came to building the software and providing the servers for it to scale and grow.

“I think in a way, that’s part of what made us successful, because we knew that we had to, first of all, imagine scale for the world,” Harris said. It wasn’t a matter of building one CRM tool for a large company and scaling it to meet that individual organization’s demand, then another, it was really about figuring out how to let people just sign up and start using the service, he said.

“I think in a way, that’s part of what made us successful because we knew that we had to, first of all, imagine scale for the world.” Parker Harris, Salesforce

That may seem trivial now, but it wasn’t a common way of doing business in 1999. The internet in those years was dominated by a ton of consumer-facing dot-coms, many of which would go bust in the next year or two. Salesforce wanted to build an enterprise software company online, and although it wasn’t alone in doing that, it did face unique challenges being one of the early adherents.

“We created a software that was what I would call massively multi-tenant where we couldn’t optimize it at the hardware layer because there was no Infrastructure as a Service. So we did all the optimization above that — and we actually had very little infrastructure early on,” he explained.

From the beginning, Benioff had the vision and Harris was charged with building it. Tien Tzuo, who would go on to be co-founder at Zuora in 2007, was employee number 11 at Salesforce, starting in August of 1999, about five months after the apartment opened for business. At that point, there still wasn’t an official product, but they were getting closer when Benioff hired Tzuo.

As Tzuo tells it, he had fancied a job as a product manager, but when Benioff saw his Oracle background in sales, he wanted him in account development. “My instinct was, don’t argue with this guy. Just roll with it,” Tzuo relates.

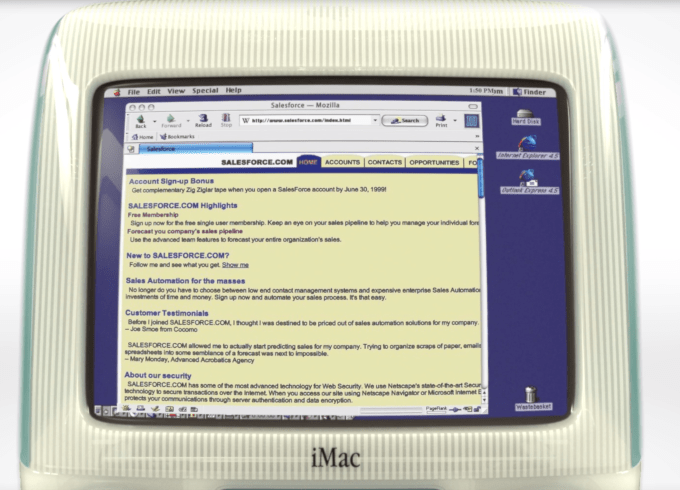

Early prototype of Salesforce.com (Photo: Salesforce)

As Tzuo pointed out, in a startup with a handful of people, titles mattered little anyway. “Who cares what your role was. All of us had that attitude. You were a coder or a non-coder,” he said. The coders were stashed upstairs with a view of San Francisco Bay and strict orders from Benioff to be left alone. The remaining employees were downstairs working the phones to get customers.

“Who cares what your role was. All of us had that attitude. You were a coder or a non-coder.” Tien Tzuo, early employe

The first Wayback Machine snapshot of Salesforce.com is from November 15, 1999, It wasn’t fancy, but it showed all of the functionality you would expect to find in a CRM tool: Accounts, Contacts, Opportunities, Forecasts and Reports, with each category represented by a tab.

The site officially launched on February 7, 2000 with 200 customers, and they were off and running.

Every successful startup needs visionary behind it, pushing it, and for Salesforce that person was Marc Benioff. When he came up with the concept for the company, the dot-com boom was in high gear. In a year or two, much of it would come crashing down, but in 1999, anything was possible, and Benioff was bold and brash and brimming with ideas.

But even good ideas don’t always pan out for so many reasons, as many a failed startup founder knows only too well. For a startup to succeed it needs a long-term vision of what it will become, and Benioff was the visionary, the front man, the champion, the chief marketer. He was all of that — and he wouldn’t take no for an answer.

Paul Greenberg, managing principal at The 56 Group and author of multiple books about the CRM industry, including CRM at the Speed of Light (the first edition of which was published in 2001), was an early user of Salesforce, and says that he was not impressed with the product at first, complaining about the early export functionality in an article.

A Salesforce competitor at the time, Salesnet, got wind of Greenberg’s post, and put his complaint on the company website. Benioff saw it, and fired off an email to Greenberg: “I see you’re a skeptic. I love convincing skeptics. Can I convince you?” Greenberg said that being a New Yorker, he wrote back with a one-line response. “Take your best shot.” Twenty years later, Greenberg says that Benioff did take his best shot — and he did end up convincing him.

“I see you’re a skeptic. I love convincing skeptics. Can I convince you?” Early Marc Benioff email

Laurie McCabe, who is co-founder and partner at SMB Group, was working for a consulting firm in Boston in 1999 when Benioff came by to pitch Salesforce to her team. She says she was immediately impressed with him, but also with the notion of putting enterprise software online, effectively putting it within reach of many more companies.

“He was the ringmaster I believe for SaaS or cloud or whatever we want to call it today. And that doesn’t mean some of these other guys didn’t also have a great vision, but he was the guy beating the drum louder. And I just really felt that in addition to the fact that he was an exceptional storyteller, marketeer and everything else, he really had the right idea that software on prem was not in reach of most businesses,” she said.

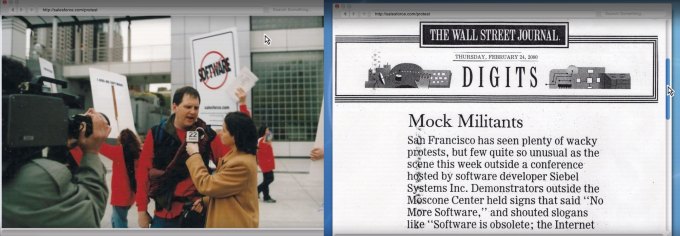

One of the ways that Benioff put the company in the public eye in the days before social media was guerrilla marketing techniques. He came up with the idea of “no software” as a way to describe software on the internet. He sent some of his early employees to “protest” at the Siebel Conference, taking place at the Moscone Center in February, 2000. He was disrupting one of his major competitors, and it created enough of a stir to attract a television news crew and garner a mention in The Wall Street Journal. All of this was valuable publicity for a company that was still in its early stages.

Photos: Salesforce

Brent Leary, who had left his job as an industry consultant in 2003 to open his current firm, CRM Essentials, said this ability to push the product was a real differentiator for the company and certainly got his attention. “I had heard about Salesnet and these other ones, but these folks not only had a really good product, they were already promoting it. They seemed to be ahead of the game in terms of evangelizing the whole “no software” thing. And that was part of the draw too,” Leary said of his first experiences working with Salesforce.

Leary added, “My first Dreamforce was in 2004, and I remember it particularly because it was actually held on Election Day 2004 and they had a George W. Bush look-alike come and help open the conference, and some people actually thought it was him.”

Greenberg said that the “no software” campaign was brilliant because it brought this idea of delivering software online to a human level. “When Marc said, ‘no software’ he knew there was software, but the thing with him is, that he’s so good at communicating a vision to people.” Software in the 1990s and early 2000s was delivered mostly in boxes on CDs (or 3.5-inch floppies), so saying no software was creating a picture that you didn’t have to touch the software. You just signed up and used it. Greenberg said that campaign helped people understand online software at a time when it wasn’t a common delivery method.

One of the big differentiators for Salesforce as a company was the culture it built from Day One. Benioff had a vision of responsible capitalism and included their charitable 1-1-1 model in its earliest planning documents. The idea was to give one percent of Salesforce’s equity, one percent of its product and one percent of its employees’ time to the community. As Benioff once joked, they didn’t have a product and weren’t making any money when they made the pledge, but they have stuck to it and many other companies have used the model Salesforce built.

Image: Salesforce

Bruce Cleveland, a partner at Wildcat Ventures, who has written a book with Geoffrey Moore (of Crossing the Chasm fame) called Traversing the Traction Gap, says that it is essential for a startup to establish a culture early on, just as Benioff did. “A CEO has to say, these are the standards by which we’re going to run this company. These are the things that we value. This is how we’re going to operate and hold ourselves accountable to each other,” Cleveland said. Benioff did that.

Another element of this was building trust with customers, a theme that Benioff continues to harp on to this day. As Harris pointed out, people still didn’t trust the internet completely in 1999, so the company had to overcome objections to entering a credit card online. Even more than that though, they had to get companies to agree to share their precious customer data with them on the internet.

“We had to not only think about scale, we had to think about how do we get the trust of our customers, to say that we will protect your information as well or better than you can,” Harris explained.

The company was able to overcome those objections, of course, and more. Todd McKinnon, who is currently co-founder and CEO at Okta, joined Salesforce as VP of Engineering in 2006 as the company began to ramp up becoming a $100 million company, and he says that there were some growing pains in that time period.

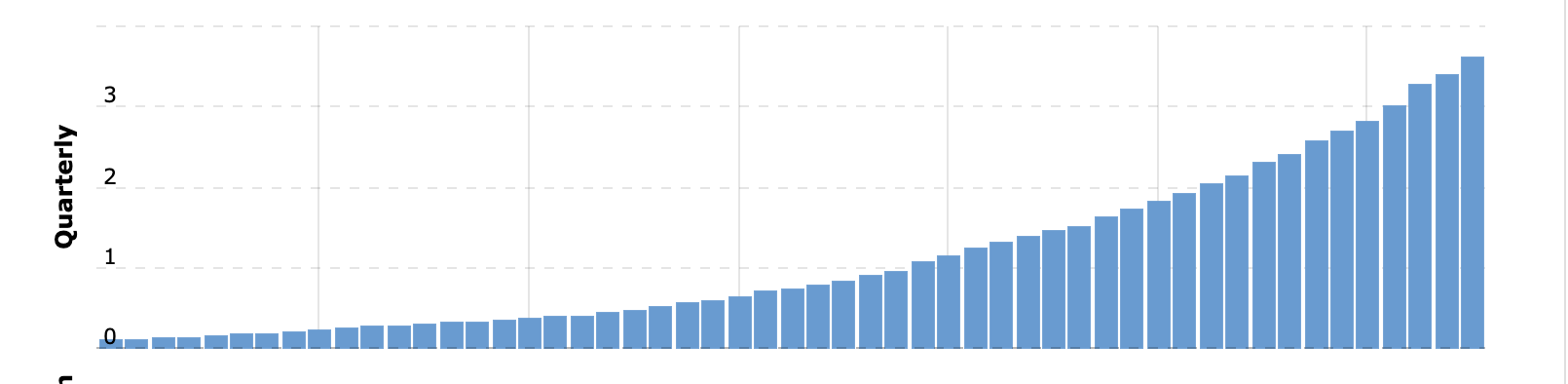

Salesforce revenue growth across the years, from 2006-present (Chart: Macro Trends)

When he arrived, they were running on three mid-tier Sun servers in a hosted co-location facility. McKinnon said that it was not high-end by today’s standards. “There was probably less RAM than what’s in your MacBook Pro today,” he joked.

When he came on board, the company still had only 13 engineers and the actual infrastructure requirements were still very low. While that would change during his six-year tenure, it was working fine when he got there. Within five years, he said, that changed dramatically as they were operating their own data centers and running clusters of Dell X86 servers — but that was down the road.

Before they did that, they went back to Sun one more time and bought four of the biggest boxes they sold at the time and proceeded to transfer all of the data. The problem was that the Oracle database wasn’t working well, so, as McKinnon tells it, they got on the phone with Larry Ellison from Oracle, who upon hearing about the setup, asked them straight out why they were doing that? The way they had it set up simply didn’t work.

They were able to resolve it all and move on, but it’s the kind of crisis that today’s startups probably wouldn’t have to deal with because they would be running their company on a cloud infrastructure service, not their own hardware.

About this same time, Salesforce began a strategy to grow through acquisitions. In 2006, it acquired the first of 55 companies when it bought a small wireless technology company called Sendia for $15 million. As early as 2006, the year before the first iPhone, the company was already thinking about mobile.

Last year it made its 52nd acquisition, and the most costly so far, when it purchased MuleSoft for $6.5 billion, giving it a piece of software that could help Salesforce customers bridge the on-prem and cloud worlds. As Greenberg pointed out, this brought a massive change in messaging for the company.

“With the Salesforce acquisition of MuleSoft, it allows them pretty much to complete the cycle between back and front office and between on-prem and the cloud. And you notice, all of a sudden, they’re not saying ‘no software.’ They’re not attacking on-premise. You know, all of this stuff has gone by the wayside,” Greenberg said.

No company is going to be completely consistent as it grows and priorities shift, but if you are a startup looking for a blueprint on how to grow a successful company, Salesforce would be a pretty good company to model yourself after. Twenty years into this, they are still growing and still going strong and they remain a powerful voice for responsible capitalism, making lots of money, while also giving back to the communities where they operate.

One other lesson you could learn is that you’re never done. Twenty years is a big milestone, but it’s just one more step in the long arc of a successful organization.

Powered by WPeMatico

Clari started as a company that wanted to give sales teams more information about their sales process than could be found in the CRM database. Today, the company announced a much broader platform, one that can provide insight across sales, marketing and customer service to give a more unified view of a company’s go-to-market operations, all enhanced by AI.

Company co-founder and CEO Andy Byrne says this involves pulling together a variety of data and giving each department the insight to improve their mission. “We are analyzing large volumes of data found in various revenue systems — sales, marketing, customer success, etc. — and we’re using that data to provide a new platform that’s connecting up all of the different revenue departments,” Byrne told TechCrunch.

For sales, that would mean driving more revenue. For marketing it would it involve more targeted plans to drive more sales. And for customer success it would be about increasing customer retention and reducing churn.

Screenshot: ClariThe company’s original idea when it launched in 2012 was looking at a range of data that touched the sales process, such as email, calendars and the CRM database, to bring together a broader view of sales than you could get by looking at the basic customer data stored in the CRM alone. The Clari data could tell the reps things like which deals would be most likely to close and which ones were at risk.

“We were taking all of these signals that had been historically disconnected from each other and we were connecting it all into a new interface for sales teams that’s very different than a CRM,” Byrne said.

Over time, that involved using AI and machine learning to make connections in the data that humans might not have been seeing. The company also found that customers were using the product to look at processes adjacent to sales, and they decided to formalize that and build connectors to relevant parts of the go-to-market system like marketing automation tools from Marketo or Eloqua and customer tools such as Dialpad, Gong.io and Salesloft.

With Clari’s approach, companies can get a unified view without manually pulling all this data together. The goal is to provide customers with a broad view of the go-to-market operation that isn’t possible looking at siloed systems.

The company has experienced tremendous growth over the last year, leaping from 80 customers to 250. These include Okta and Alteryx, two companies that went public in recent years. Clari is based in the Bay Area and has around 120 employees. It has raised more than $60 million. The most recent round was a $35 million Series C last May led by Tenaya Capital.

Powered by WPeMatico

Compass, the real estate tech platform that is now worth $4.4 billion, has made an acquisition to give its agents a boost when it comes to looking for good leads on properties to sell. It is acquiring Contactually, an AI-based CRM platform designed specifically for the industry, which includes features like linking up a list of homes sold by a brokerage with records of sales in the area and other property indexes to determine which properties might be good targets to tap for future listings.

Contactually had already been powering Compass’s own CRM service that it launched last year, so there is already a degree of integration between the two.

Terms of the deal are not being disclosed. Crunchbase notes that Contactually had raised around $18 million from VCs that included Rally Ventures, Grotech and Point Nine Capital, and it was last valued at around $30 million in 2016, according to PitchBook. From what I understand, the startup had strong penetration in the market, so it’s likely that the price was a bit higher than this previous valuation.

The plan is to bring over all of Contactually’s team of 32 employees, led by Zvi Band, the co-founder and CEO, to integrate the company’s product into Compass’s platform completely. They will report to CTO Joseph Sirosh and head of product Eytan Seidman. It will also mean a bigger operation for Compass in Washington, DC, which is where Contactually had been based.

“The Contactually team has worked for the past 8 years to build a best-in-class CRM that aggregates relationships and automatically documents every touchpoint,” said Band in a statement “We are proud that our investment into machine learning has resulted in new features like Best Time to Email and other data-driven, follow-up recommendations which help agents be more effective in their day-to-day. After working extensively with the Compass team, it was apparent that joining forces would accelerate our missions of building the future of the industry.”

For the time being, customers who are already using the product — and a large number of real estate brokers and agents in the U.S. already were, at prices that ranged from $59/month to $399/month depending on the level of service — will continue their contracts as before.

I suspect that the longer-term plan, however, will be a little different: You have to wonder if agents who compete against Compass would be happy to use a service where their data is being processed by it, and for Compass itself. I would suspect that having this tech for itself would give it an edge over the others.

Compass, I understand from sources, is on track to make $2 billion in revenues in 2019 (its 2018 targets were $1 billion on $34 billion in property sales, and it had previously said it would be doubling that this year). Now in 100 cities, it’s come a long way from its founding in 2012 by Ori Allon and Robert Reffkin.

The bigger picture beyond real estate is that, as with many other analog industries, those who are tackling them with tech-first approaches are sweeping up not only existing business, but in many cases helping the whole market to expand. Contactually, as a tool that can help source potential properties for sale that owners hadn’t previously considered putting on the market, could end up serving that very end for Compass.

The focus on using tech to storm into a legacy industry is also coming at an interesting time. As we’ve pointed out before, the housing market is predicted to cool this year, and that will put the squeeze on agents who do not have strong networks of clients and the tools to maximise whatever opportunities there are out there to list and sell properties.

The likes of Opendoor — which appears to be raising money and inching closer to Compass in terms of valuation — is also trying out a different model, which essentially involves becoming a middle part in the chain, buying properties from sellers and selling them on to buyers, to speed up the process and cut out some of the expenses for the end users. That approach underscores the fact that, while the infusion of technology is an inevitable trend, there will be multiple ways of applying that.

This appears to be Compass’s first full acquisition of a tech startup, although it has made partial acqui-hires in the past.

Powered by WPeMatico

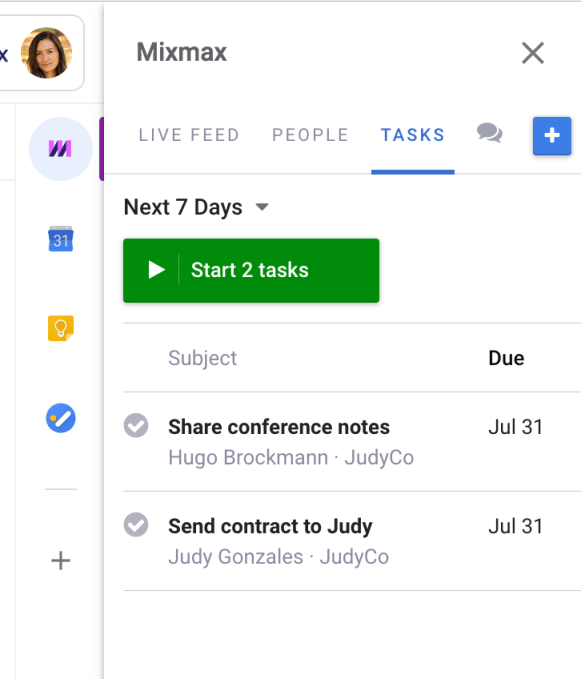

Mixmax today introduced version 2.0 of its Gmail-based tool and plugin for Chrome that promises to make your daily communications chores a bit easier to handle.

With version 2.0, Mixmax gets an updated editor that better integrates with the current Gmail interface and that gets out of the way of popular extensions like Grammarly. That’s table stakes, of course, but I’ve tested it for a bit and the new version does indeed do a better job of integrating itself into the current Gmail interface and feels a bit faster, too.

What’s more interesting is that the service now features a better integration with LinkedIn . There’s both an integration with the LinkedIn Sales Navigator, LinkedIn’s tool for generating sales leads and contacting them, and LinkedIn’s messaging tools for sending InMail and connection requests — and sees info about a recipient’s LinkedIn profile, including the LinkedIn Icebreakers section — right from the Mixmax interface.

Together with its existing Salesforce integration, this should make the service even more interesting to sales people. And the Salesforce integration, too, is getting a bit of a new feature that can now automatically create a new contact in the CRM tool when a prospect’s email address — maybe from LinkedIn — isn’t in your database yet.

Also new in Mixmax 2.0 is something the company calls “Beast Mode.” Not my favorite name, I have to admit, but it’s an interesting task automation tool that focuses on helping customer-facing users prioritize and complete batches of tasks quickly and that extends the service’s current automation tools.

Finally, Mixmax now also features a Salesforce-linked dialer widget for making calls right from the Chrome extension.

Finally, Mixmax now also features a Salesforce-linked dialer widget for making calls right from the Chrome extension.

“We’ve always been focused on helping business people communicate better, and everything we’re rolling out for Mixmax 2.0 only underscores that focus,” said Mixmax CEO and co-founder Olof Mathé. “Many of our users live in Gmail and our integration with LinkedIn’s Sales Navigator ensures users can conveniently make richer connections and seamlessly expand their networks as part of their email workflow.”

Whether you get these new features depends on how much you pay, though. Everybody, including free users, gets access to the refreshed interface. Beast Mode and the dialer are available with the enterprise plan, the company’s highest-level plan which doesn’t have a published price. The dialer is also available for an extra $20/user/month on the $49/month/user Growth plan. LinkedIn Sales Navigator support is available with the growth and enterprise plans.

Sadly, that means that if you are on the cheaper Starter and Small Business plans ($9/user/month and $24/user/month respectively), you won’t see any of these new features anytime soon.

Powered by WPeMatico

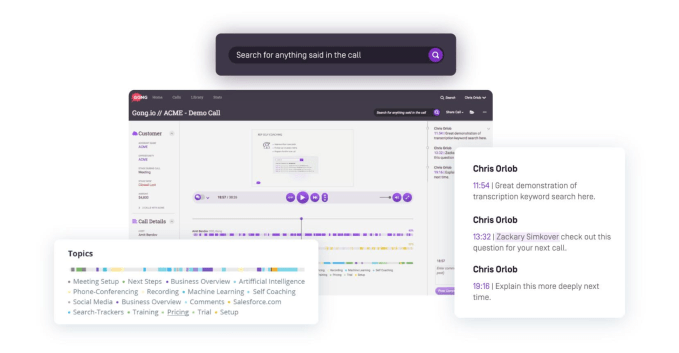

With traditional CRM tools, sales people add basic details about the companies to the database, then a few notes about their interactions. AI has helped automate some of that, but Gong.io wants to take it even further using voice recognition to capture every word of every interaction. Today, it got a $40 million Series B investment.

The round was led by Battery Ventures, with existing investors Norwest Venture Partners, Shlomo Kramer, Wing Venture Capital, NextWorld Capital and Cisco Investments also participating. Battery general partner Dharmesh Thakker will join the startup’s board under the terms of the deal. Today’s investment brings the total raised so far to $68 million, according to the company.

Indeed, $40 million is a hefty Series B, but investors see a tool that has the potential to have a material impact on sales, or at least give management a deeper understanding of why a deal succeeded or failed using artificial intelligence, specifically natural language processing.

Company co-founder and CEO Amit Bendov says the solution starts by monitoring all customer-facing conversation and giving feedback in a fully automated fashion. “Our solution uses AI to extract important bits out of the conversation to provide insights to customer-facing people about how they can get better at what they do, while providing insights to management about how staff is performing,” he explained. It takes it one step further by offering strategic input like how your competitors are trending or how are customers responding to your products.

Screenshot: Gong.io

Bendov says he started the company because he has had this experience at previous startups where he wants to know more about why he lost a sale, but there was no insight from looking at the data in the CRM database. “CRM could tell you what customers you have, how many sales you’re making, who is achieving quota or not, but never give me the information to rationalize and improve operations,” he said.

The company currently has 350 customers, a number that has more than tripled since the end of 2017 when it had 100. He says it’s not only that it’s adding new customers, existing ones are expanding, and he says that there is almost zero churn.

Today, Gong has 120 employees, with headquarters in San Francisco and a 55-person R&D team in Israel. Bendov expects the number of employees to double over the next year with the new influx of money to keep up with the customer growth.

Powered by WPeMatico

Young founders who want to start companies while still in school have an increasing number of resources to tap into that exist just for them. Students that want to learn how to build companies can apply to an increasing number of fast-track programs that allow them to gain valuable early stage operating experience. The energy around student entrepreneurship today is incredible. I’ve been immersed in this community as an investor and adviser for some time now, and to say the least, I’m continually blown away by what the next generation of innovators are dreaming up (from Analytical Space’s global data relay service for satellites to Brooklinen’s reinvention of the luxury bed).

Bill Gates in 1973

First, let’s look at student founders and why they’re important. Student entrepreneurs have long been an important foundation of the startup ecosystem. Many students wrestle with how best to learn while in school —some students learn best through lectures, while more entrepreneurial students like author Julian Docks find it best to leave the classroom altogether and build a business instead.

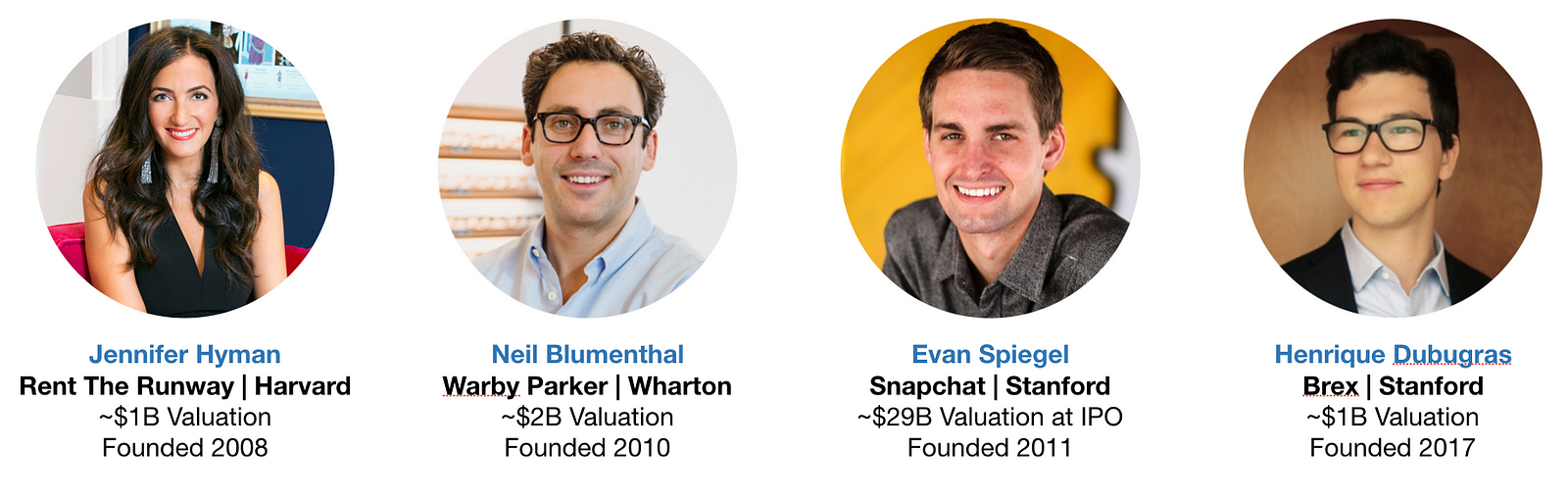

Indeed, some of our most iconic founders are Microsoft’s Bill Gates and Facebook’s Mark Zuckerberg, both student entrepreneurs who launched their startups at Harvard and then dropped out to build their companies into major tech giants. A sample of the current generation of marquee companies founded on college campuses include Snap at Stanford ($29B valuation at IPO), Warby Parker at Wharton (~$2B valuation), Rent The Runway at HBS (~$1B valuation), and Brex at Stanford (~$1B valuation).

Some of today’s most celebrated tech leaders built their first ventures while in school — even if some student startups fail, the critical first-time founder experience is an invaluable education in how to build great companies. Perhaps the best example of this that I could find is Drew Houston at Dropbox (~$9B valuation at IPO), who previously founded an edtech startup at MIT that, in his words, provided a: “great introduction to the wild world of starting companies.”

Student founders are everywhere, but the highest concentration of venture-backed student founders can be found at just 5 universities. Based on venture fund portfolio data from the last six years, Harvard, Stanford, MIT, UPenn, and UC Berkeley have produced the highest number of student-founded companies that went on to raise $1 million or more in seed capital. Some prospective students will even enroll in a university specifically for its reputation of churning out great entrepreneurs. This is not to say that great companies are not being built out of other universities, nor does it mean students can’t find resources outside a select number of schools. As you can see later in this essay, there are a number of new ways students all around the country can tap into the startup ecosystem. For further reading, PitchBook produces an excellent report each year that tracks where all entrepreneurs earned their undergraduate degrees.

Student founders have a number of new media resources to turn to. New email newsletters focused on student entrepreneurship like Justine and Olivia Moore’s Accelerated and Kyle Robertson’s StartU offer new channels for young founders to reach large audiences. Justine and Olivia, the minds behind Accelerated, have a lot of street cred— they launched Stanford’s on-campus incubator Cardinal Ventures before landing as investors at CRV.

StartU goes above and beyond to be a resource to founders they profile by helping to connect them with investors (they’re active at 12 universities), and run a podcast hosted by their Editor-in-Chief Johnny Hammond that is top notch. My bet is that traditional media will point a larger spotlight at student entrepreneurship going forward.

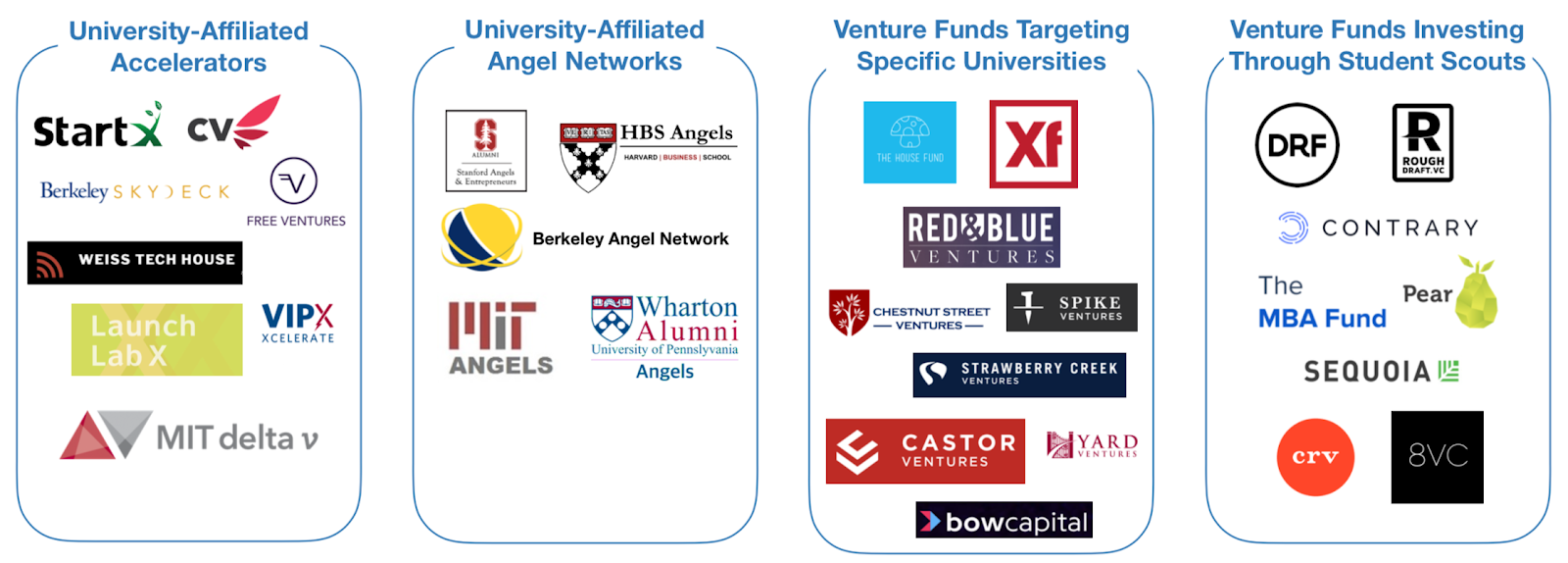

New pools of capital are also available that are specifically for student founders. There are four categories that I call special attention to:

While it is difficult to estimate exactly how much capital has been deployed by each, there is no denying that there has been an explosion in the number of programs that address the pre-seed phase. A sample of the programs available at the Top 5 universities listed above are in the graphic below — listing every resource at every university would be difficult as there are so many.

One alumni-centric fund to highlight is the Alumni Ventures Group, which pools LP capital from alumni at specific universities, then launches individual venture funds that invest in founders connected to those universities (e.g. students, alumni, professors, etc.). Through this model, they’ve deployed more than $200M per year! Another highlight has been student scout programs — which vary in the degree of autonomy and capital invested — but essentially empower students to identify and fund high-potential student-founded companies for their parent venture funds. On campuses with a large concentration of student founders, it is not uncommon to find student scouts from as many as 12 different venture funds actively sourcing deals (as is made clear from David Tao’s analysis at UC Berkeley).

Investment Team at Rough Draft Ventures

In my opinion, the two institutions that have the most expansive line of sight into the student entrepreneurship landscape are First Round’s Dorm Room Fund and General Catalyst’s Rough Draft Ventures. Since 2012, these two funds have operated a nationwide network of student scouts that have invested $20K — $25K checks into companies founded by student entrepreneurs at 40+ universities. “Scout” is a loose term and doesn’t do it justice — the student investors at these two funds are almost entirely autonomous, have built their own platform services to support portfolio companies, and have launched programs to incubate companies built by female founders and founders of color. Another student-run fund worth noting that has reach beyond a single region is Contrary Capital, which raised $2.2M last year. They do a particularly great job of reaching founders at a diverse set of schools — their network of student scouts are active at 45 universities and have spoken with 3,000 founders per year since getting started. Contrary is also testing out what they describe as a “YC for university-based founders”. In their first cohort, 100% of their companies raised a pre-seed round after Contrary’s demo day. Another even more recently launched organization is The MBA Fund, which caters to founders from the business schools at Harvard, Wharton, and Stanford. While super exciting, these two funds only launched very recently and manage portfolios that are not large enough for analysis just yet.

Over the last few months, I’ve collected and cross-referenced publicly available data from both Dorm Room Fund and Rough Draft Ventures to assess the state of student entrepreneurship in the United States. Companies were pulled from each fund’s portfolio page, then checked against Crunchbase for amount raised, accelerator participation, and other metrics. If you’d like to sift through the data yourself, feel free to ping me — my email can be found at the end of this article. To be clear, this does not represent the full scope of investment activity at either fund — many companies in the portfolios of both funds remain confidential and unlisted for good reasons (e.g. startups working in stealth). In fact, the In addition, data for early stage companies is notoriously variable in quality, even with Crunchbase. You should read these insights as directional only, given the debatable confidence interval. Still, the data is still interesting and give good indicators for the health of student entrepreneurship today.

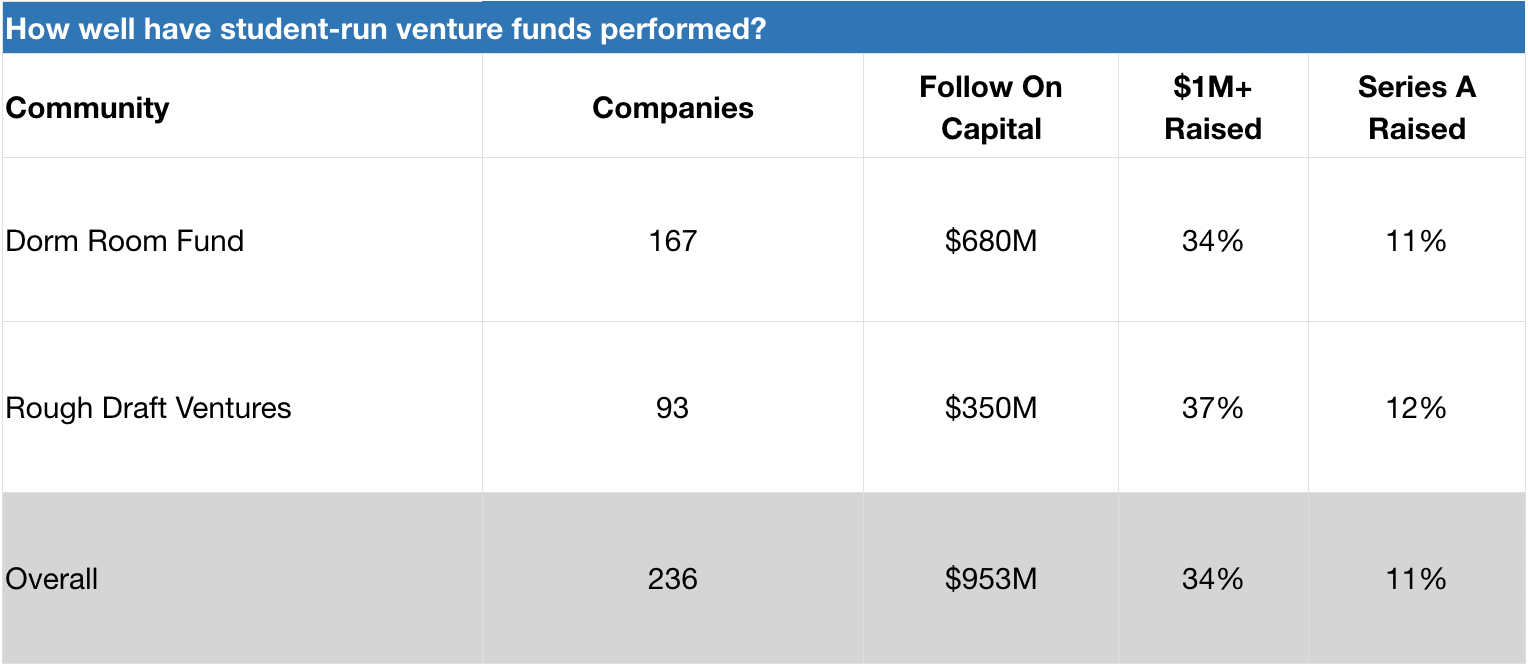

Dorm Room Fund and Rough Draft Ventures have invested in 230+ student-founded companies that have gone on to raise nearly $1 billion in follow on capital. These funds have invested in a diverse range of companies, from govtech (e.g. mark43, raised $77M+ and FiscalNote, raised $50M+) to space tech (e.g. Capella Space, raised ~$34M). Several portfolio companies have had successful exits, such as crypto startup Distributed Systems (acquired by Coinbase) and social networking startup tbh (acquired by Facebook). While it is too early to evaluate the success of these funds on a returns basis (both were launched just 6 years ago), we can get a sense of success by evaluating the rates by which portfolio companies raise additional capital. Taken together, 34% of DRF and RDV companies in our data set have raised $1 million or more in seed capital. For a rough comparison, CB Insights cites that 40% of YC companies and 48% of Techstars companies successfully raise follow on capital (defined as anything above $750K). Certainly within the ballpark!

Dorm Room Fund and Rough Draft Ventures companies in our data set have an 11–12% rate of survivorship to Series A. As a benchmark, a previous partner at Y Combinator shared that 20% of their accelerator companies raise Series A capital (YC declined to share the official figure, but it’s likely a stat that is increasing given their new Series A support programs. For further reading, check out YC’s reflection on what they’ve learned about helping their companies raise Series A funding). In any case, DRF and RDV’s numbers should be taken with a grain of salt, as the average age of their portfolio companies is very low and raising Series A rounds generally takes time. Ultimately, it is clear that DRF and RDV are active in the earlier (and riskier) phases of the startup journey.

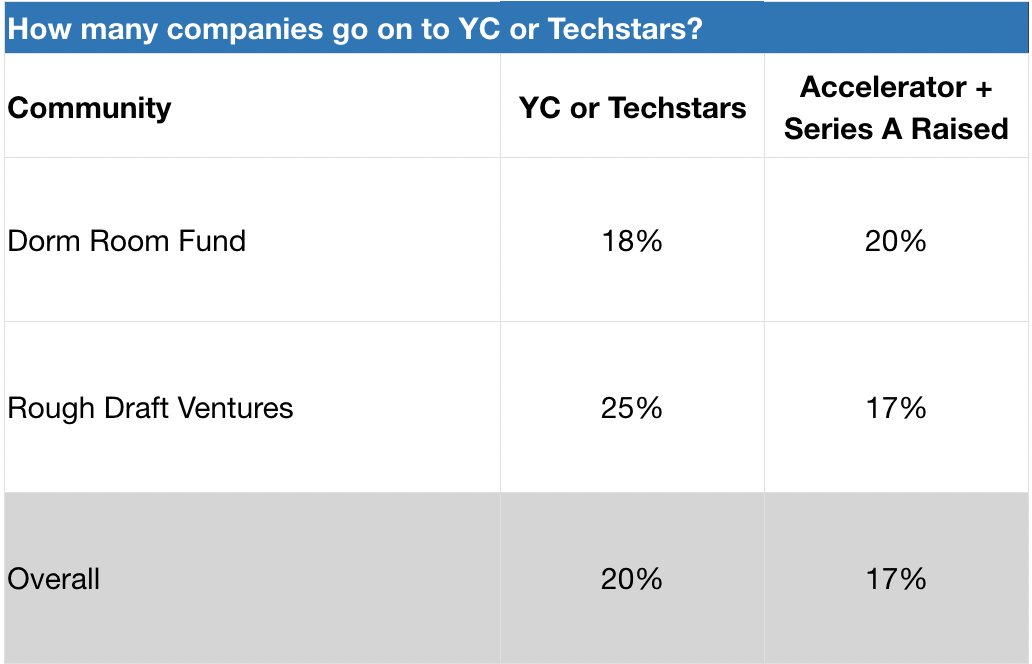

Dorm Room Fund and Rough Draft Ventures send 18–25% of their portfolio companies to Y Combinator or Techstars. Given YC’s 1.5% acceptance rate as reported in Fortune, this is quite significant! Internally, these two funds offer founders an opportunity to participate in mock interviews with YC and Techstars alumni, as well as tap into their communities for peer support (e.g. advice on pitch decks and application content). As a result, Dorm Room Fund and Rough Draft Ventures regularly send cohorts of founders to these prestigious accelerator programs. Based on our data set, 17–20% of DRF and RDV companies that attend one of these accelerators end up raising Series A venture financing.

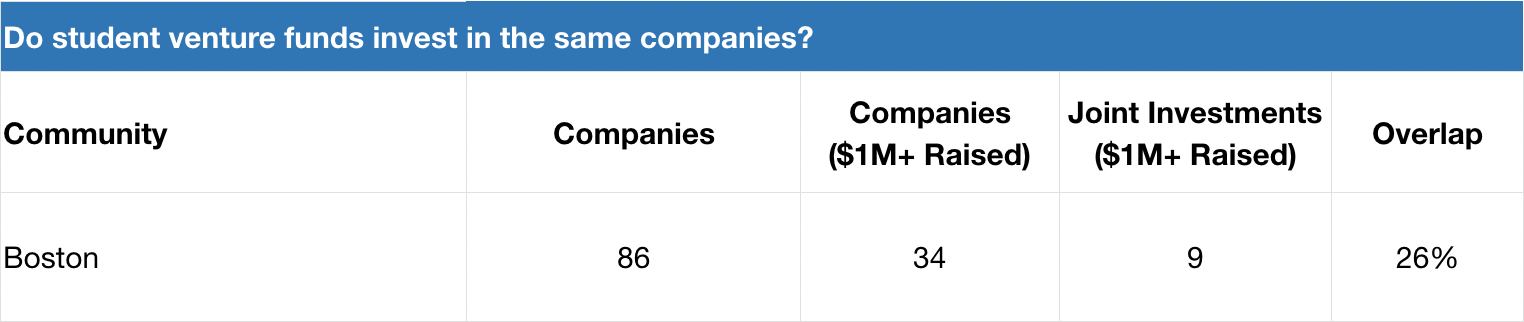

Dorm Room Fund and Rough Draft Ventures don’t invest in the same companies. When we take a deeper look at one specific ecosystem where these two funds have been equally active over the last several years — Boston — we actually see that the degree of investment overlap for companies that have raised $1M+ seed rounds sits at 26%. This suggests that these funds are either a) seeing different dealflow or b) have widely different investment decision-making.

Dorm Room Fund and Rough Draft Ventures should not just be measured by a returns-basis today, as it’s too early. I hypothesize that DRF and RDV are actually encouraging more entrepreneurial activity in the ecosystem (more students decide to start companies while in school) as well as improving long-term founder outcomes amongst students they touch (portfolio founders build bigger and more successful companies later in their careers). As more students start companies, there’s likely a positive feedback loop where there’s increasing peer pressure to start a company or lean on friends for founder support (e.g. feedback, advice, etc).Both of these subjects warrant additional study, but it’s likely too early to conduct these analyses today.

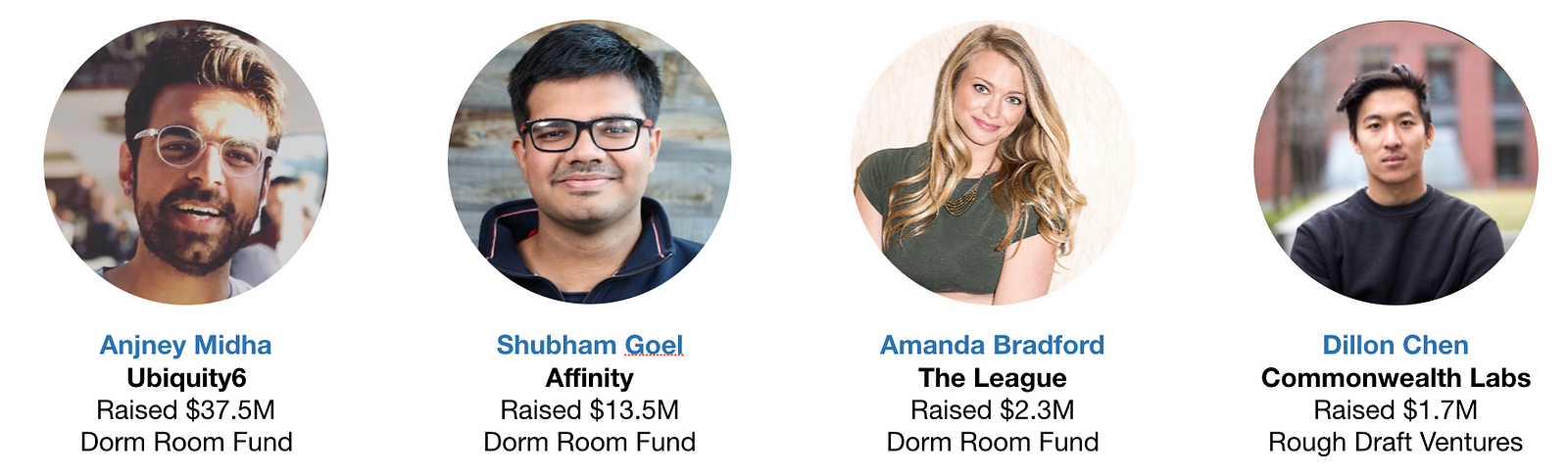

Dorm Room Fund and Rough Draft Ventures have impressive alumni that you will want to track. 1 in 4 alumni partners are founders, and 29% of these founder alumni have raised $1M+ seed rounds for their companies. These include Anjney Midha’s augmented reality startup Ubiquity6 (raised $37M+), Shubham Goel’s investor-focused CRM startup Affinity (raised $13M+), Bruno Faviero’s AI security software startup Synapse (raised $6M+), Amanda Bradford’s dating app The League (raised $2M+), and Dillon Chen’s blockchain startup Commonwealth Labs (raised $1.7M). It makes sense to me that alumni from these communities that decide to start companies have an advantage over their peers — they know what good companies look like and they can tap into powerful networks of young talent / experienced investors.

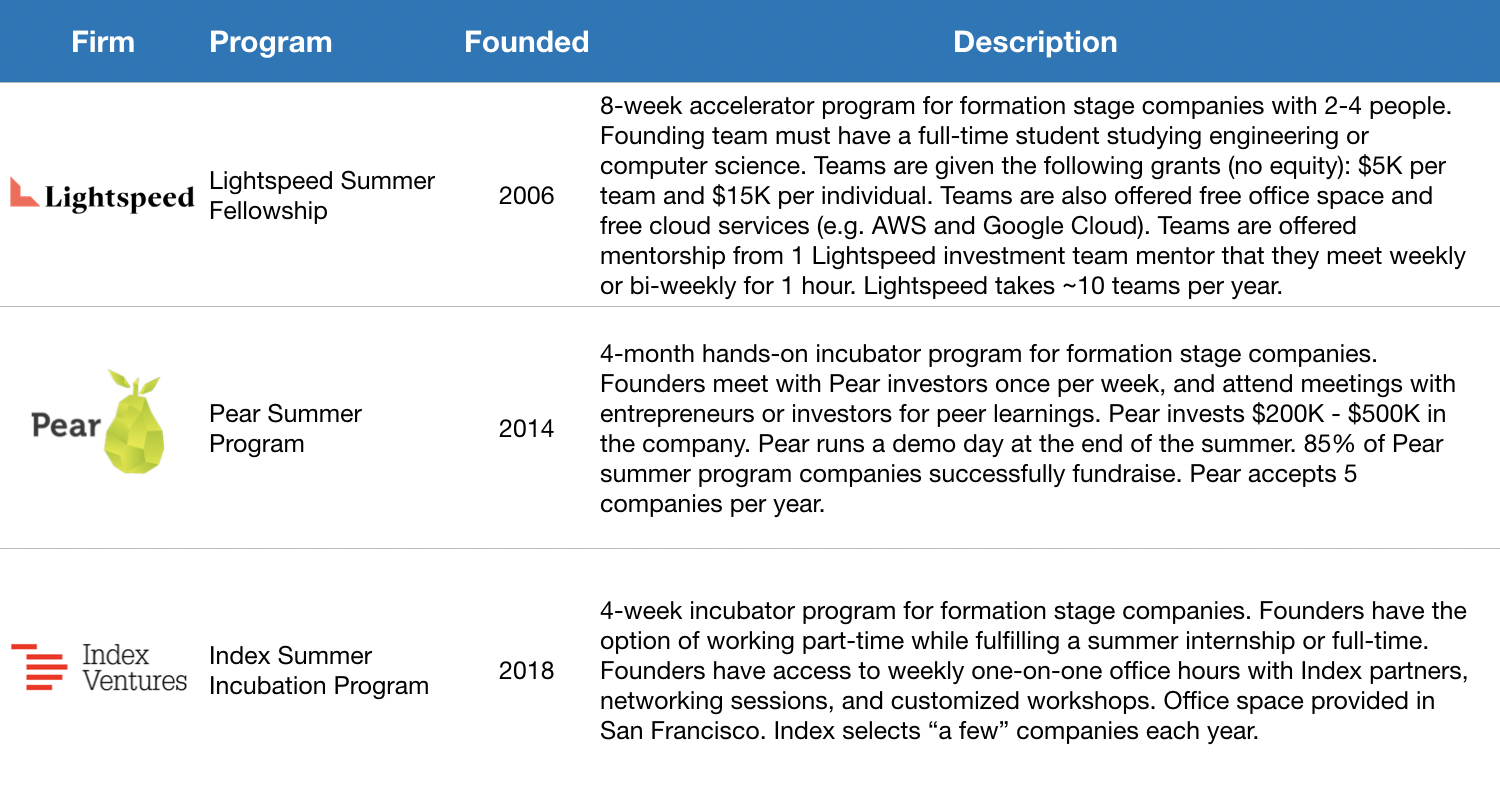

Beyond Dorm Room Fund and Rough Draft Ventures, some venture capital firms focus on incubation for student-founded startups. Credit should first be given to Lightspeed for producing the amazing Summer Fellows bootcamp experience for promising student founders — after all, Pinterest was built there! Jeremy Liew gives a good overview of the program through his sit-down interview with Afterbox’s Zack Banack. Based on a study they conducted last year, 40% of Lightspeed Summer Fellows alumni are currently active founders. Pear Ventures also has an impressive summer incubator program where 85% of its companies successfully complete a fundraise. Index Ventures is the latest to build an incubator program for student founders, and even accepts founders who want to work on an idea part-time while completing a summer internship.

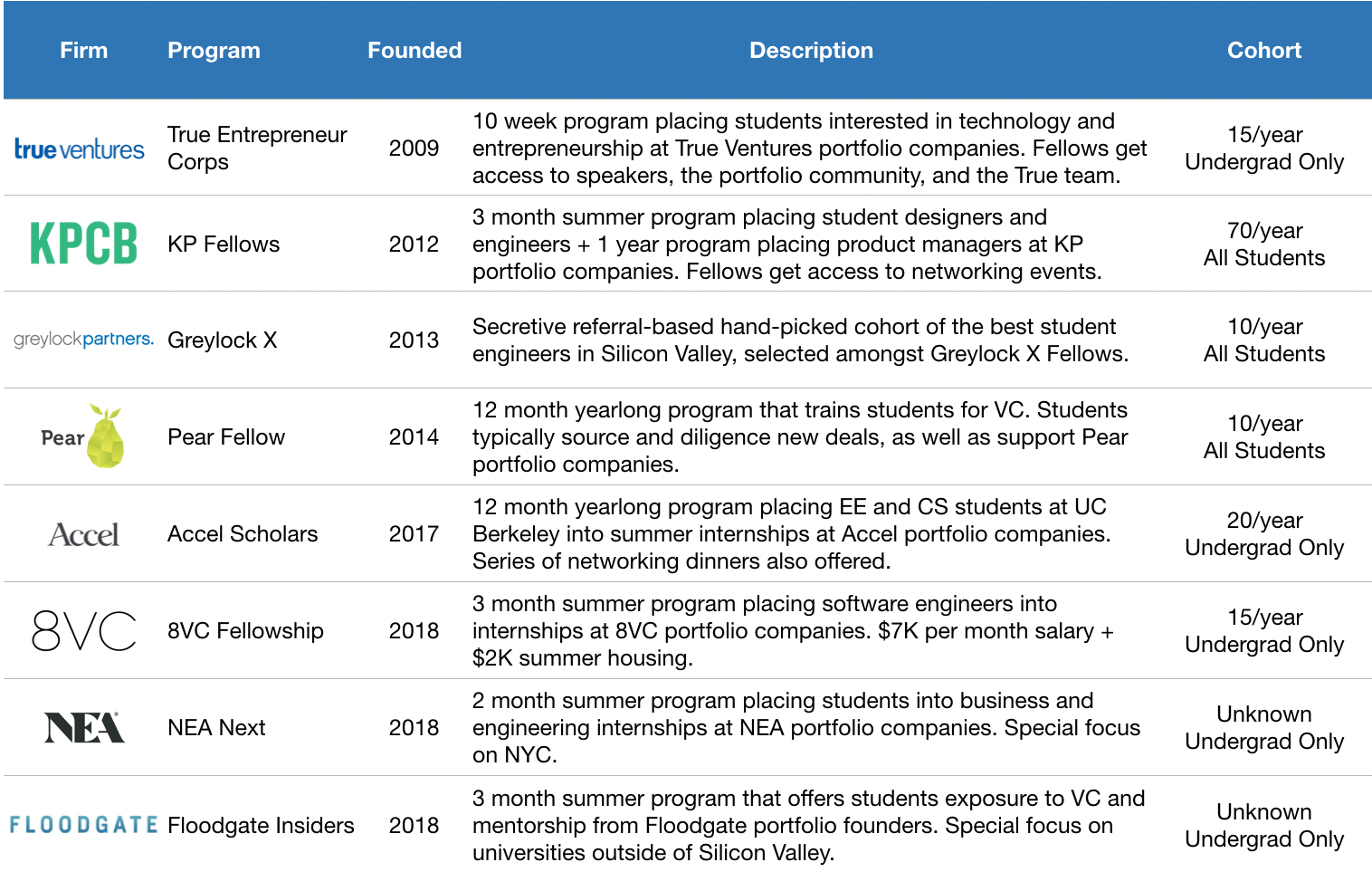

Let’s now look at students who want to join a startup before founding one. Venture funds have historically looked to tap students for talent, and are expanding the engagement lifecycle. The longest running programs include Kleiner Perkins’ class=”m_1196721721246259147gmail-markup–strong m_1196721721246259147gmail-markup–p-strong”> KP Fellows and True Ventures’ TEC Fellows, which focus on placing the next generation’s most promising product managers, engineers, and designers into the portfolio companies of their parent venture funds.

There’s also the secretive Greylock X, a referral-based hand-picked group of the best student engineers in Silicon Valley (among their impressive alumni are founders like Yasyf Mohamedali and Joe Kahn, the folks behind First Round-backed Karuna Health). As these programs have matured, these firms have recognized the long-run value of engaging the alumni of their programs.

More and more alumni are “coming back” to the parent funds as entrepreneurs, like KP Fellow Dylan Field of Figma (and is also hosting a KP Fellow, closing a full circle loop!). Based on their latest data, 10% of KP Fellows alumni are founders — that’s a lot given the fact that their community has grown to 500! This helps explain why Kleiner Perkins has created a structured path to receive $100K in seed funding to companies founded by KP Fellow alumni. It looks like venture funds are beginning to invest in student programs as part of their larger platform strategy, which can have a real impact over the long term (for further reading, see this analysis of platform strategy outcomes by USV’s Bethany Crystal).

KP Fellows in San Francisco

Venture funds are doubling down on student talent engagement — in just the last 18 months, 4 funds have launched student programs. It’s encouraging to see new funds follow in the footsteps of First Round, General Catalyst, Kleiner Perkins, Greylock, and Lightspeed. In 2017, Accel launched their Accel Scholars program to engage top talent at UC Berkeley and Stanford. In 2018, we saw 8VC Fellows, NEA Next, and Floodgate Insiders all launch, targeting elite universities outside of Silicon Valley. Y Combinator implemented Early Decision, which allows student founders to apply one batch early to help with academic scheduling. Most recently, at the start of 2019, First Round launched the Graduate Fund (staffed by Dorm Room Fund alumni) to invest in founders who are recent graduates or young alumni.

Given more time, I’d love to study the rates by which student founders start another company following investments from student scout funds, as well as whether or not they’re more successful in those ventures. In any case, this is an escalation in the number of venture funds that have started to get serious about engaging students — both for talent and dealflow.

Student entrepreneurship 2.0 is here. There are more structured paths to success for students interested in starting or joining a startup. Founders have more opportunities to garner press, seek advice, raise capital, and more. Venture funds are increasingly leveraging students to help improve the three F’s — finding, funding, and fixing. In my personal view, I believe it is becoming more and more important for venture funds to gain mindshare amongst the next generation of founders and operators early, while still in school.

I can’t wait to see what’s next for student entrepreneurship in 2019. If you’re interested in digging in deeper (I’m human — I’m sure I haven’t covered everything related to student entrepreneurship here) or learning more about how you can start or join a startup while still in school, shoot me a note at sxu@dormroomfund.com. A massive thanks to Phin Barnes, Rei Wang, Chauncey Hamilton, Peter Boyce, Natalie Bartlett, Denali Tietjen, Eric Tarczynski, Will Robbins, Jasmine Kriston, Alicia Lau, Johnny Hammond, Bruno Faviero, Athena Kan, Shohini Gupta, Alex Immerman, Albert Dong, Phillip Hua-Bon-Hoa, and Trevor Sookraj for your incredible encouragement, support, and insight during the writing of this essay.

Powered by WPeMatico

Infor, a NYC-based enterprise software company, announced a massive $1.5 billion investment today that could be the precursor to an IPO in the next 12-24 months. One analyst is estimating that the valuation could be at least $60 billion.

The investment is being led by Koch Industries’ investment arm, Koch Equity Development, and Golden Gate Capital. Today’s investment comes on top of a $2 billion+ cash infusion from Koch in 2017, bringing the total raised to at least more than $3.5 billion along with a hefty $6.1 billion in debt. That’s a lot of cash.

In fact, the company plans to use a large portion of today’s investment to pay down part of that debt, including $500 million in senior secured notes due in 2020, which it plans to pay off next month, and $750 million in HoldCo senior contingent cash pay notes due in 2021, which it plans to pay off in May. The thinking is that the company wants to reduce its debt load ahead of its IPO.

“We expect this paydown, in combination with cash flows and estimated IPO proceeds, will provide Infor with leverage levels consistent with other successful IPOs over the past few years,” Infor CFO Kevin Samuelson explained during an investor call today.

The company wouldn’t rule out additional investments before going public, but it was looking firmly toward an IPO. “We’ve spoken for some time about the many advantages that we believe Infor will receive if the company goes public, including improved brand recognition, a broader employee equity program, additional currency for M&A and more financial clarity for our customers and prospects,” Samuelson said.

Infor may be the largest company you never heard of, with more than 17,000 employees and 68,000 customers in more than 100 countries worldwide. All of those customers generated $3 billion in revenue in 2018. That’s a significant presence.

Ray Wang, founder and principal analyst at Constellation Research, told TechCrunch that based on that revenue, he believes the valuation could be in the neighborhood of $60 billion. He based that on $3 billion in revenue, while using Oracle and SAP as similar industry comparisons. These companies have a 20X price/earnings ratio. He adds, that would make it the largest tech IPO ever for a NYC tech company if that comes to pass. Infor would not confirm this number with a spokesperson telling TechCrunch, “We cannot comment on value at this time.”

What does this company do to achieve this size and scope? It’s not unlike many other large enterprise companies, says Wang. It produces cloud software solutions around typical enterprise needs such as CRM, ERP and supply chain asset management.

Daniel Newman, principal analyst at Futurum Research, says that Infor has grown rapidly through a series of acquisitions and an unusual approach to enterprise software. “What makes its approach to enterprise software unique is that rather than building software and then attempting to customize it for the unique [customer] needs, Infor takes an industry-based approach that incorporates both subtle and material capabilities to address specific industry needs that more generic ERP tools aren’t capable of out of the box,” Newman told TechCrunch.

He adds that this difference is attractive to many companies seeking ERP and enterprise asset management tools that are built with their business in mind, rather than completely customizing a software designed for any business in any industry.

As it turns out, Koch isn’t just an investor, it’s an Infor customer. “Koch was a customer of Infor before we became an investor in the company, and Koch Industries’ companies continue to move their most mission critical applications to Infor CloudSuites,” Jim Hannan, executive vice president and CEO for Enterprises at Koch Industries said in a statement.

The company, which was founded way back in 2002, has been shifting to the cloud over the last five years. It reports that more than 70 percent of its revenue is now derived from cloud products, fueled in part by an aggressive acquisition strategy.

Powered by WPeMatico

Chatbots and other AI-based tools have firmly found footing in the world of customer service, used either to augment or completely replace the role of a human responding to questions and complaints, or (sometimes, annoyingly, at the same time as the previous two functions) sell more products to users.

Today, an Israeli startup called TechSee is announcing $16 million in funding to help build out its own twist on that innovation: an AI-based video service, which uses computer vision, augmented reality and a customer’s own smartphone camera to provide tech support to customers, either alongside assistance from live agents, or as part of a standalone customer service “bot.”

Led by Scale Venture Partners — the storied investor that has been behind some of the bigger enterprise plays of the last several years (including Box, Chef, Cloudhealth, DataStax, Demandbase, DocuSign, ExactTarget, HubSpot, JFrog and fellow Israeli AI assistance startup WalkMe), the Series B also includes participation from Planven Investments, OurCrowd, Comdata Group and Salesforce Ventures. (Salesforce was actually announced as a backer in October.)

The funding will be used both to expand the company’s current business as well as move into new product areas like sales.

Eitan Cohen, the CEO and co-founder, said that the company today provides tools to some 15,000 customer service agents and counts companies like Samsung and Vodafone among its customers across verticals like financial services, tech, telecoms and insurance.

The potential opportunity is big: Cohen estimates there are about 2 million customer service agents in the U.S., and about 14 million globally.

TechSee is not disclosing its valuation. It has raised around $23 million to date.

While TechSee provides support for software and apps, its sweet spot up to now has been providing video-based assistance to customers calling with questions about the long tail of hardware out in the world, used for example in a broadband home Wi-Fi service.

In fact, Cohen said he came up with the idea for the service when his parents phoned him up to help them get their cable service back up, and he found himself challenged to do it without being able to see the set-top box to talk them through what to do.

So he thought about all the how-to videos that are on platforms like YouTube and decided there was an opportunity to harness that in a more organised way for the companies providing an increasing array of kit that may never get the vlogger treatment.

“We are trying to bring that YouTube experience for all hardware,” he said in an interview.

The thinking is that this will become a bigger opportunity over time as more services get digitised, the cost of components continues to come down and everything becomes “hardware.”

“Tech may become more of a commodity, but customer service does not,” he added. “Solutions like ours allow companies to provide low-cost technology without having to hire more people to solve issues [that might arise with it.]”

The product today is sold along two main trajectories: assisting customer reps; and providing unmanned video assistance to replace some of the easier and more common questions that get asked.

In cases where live video support is provided, the customer opts in for the service, similar to how she or he might for a support service that “takes over” the device in question to diagnose and try to fix an issue. Here, the camera for the service becomes a customer’s own phone.

Over time, that live assistance is used in two ways that are directly linked to TechSee’s artificial intelligence play. First, it helps to build up TechSee’s larger back catalogue of videos, where all identifying characteristics are removed with the focus solely on the device or problem in question. Second, the experience in the video is also used to build TechSee’s algorithms for future interactions. Cohen said there are now “millions” of media files — images and videos — in the company’s catalogue.

The effectiveness of its system so far has been pretty impressive. TechSee’s customers — the companies running the customer support — say they have on average seen a 40 percent increase in customer satisfaction (NPS scores), a 17 percent decrease in technician dispatches and between 20 and 30 percent increase in first-call resolutions, depending on the industry.

TechSee is not the only company that has built a video-based customer engagement platform: others include Stryng, CallVU and Vee24. And you could imagine companies like Amazon — which is already dabbling in providing advice to customers based on what its Echo Look can see — might be interested in providing such services to users across the millions of products that it sells, as well as provide that as a service to third parties.

According to Cohen, what TechSee has going for it compared to those startups, and also the potential entry of companies like Microsoft or Amazon into the mix, is a head start on raw data and a vision of how it will be used by the startup’s AI to build the business.

“We believe that anyone who wants to build this would have a challenge making it from scratch,” he said. “This is where we have strong content, millions of images, down to specific model numbers, where we can provide assistance and instructions on the spot.”

Salesforce’s interest in the company, he said, is a natural progression of where that data and customer relationship can take a business beyond responsive support into areas like quick warranty verification (for all those times people have neglected to do a product registration), snapping fender benders for insurance claims and of course upselling to other products and services.

“Salesforce sees the synergies between the sales cloud and the service cloud,” Cohen said.

“TechSee recognized the great potential for combining computer vision AI with augmented reality in customer engagement,” said Andy Vitus, partner at Scale Venture Partners, who joins the board with this round. “Electronic devices become more complex with every generation, making their adoption a perennial challenge. TechSee is solving a massive problem for brands with a technology solution that simplifies the customer experience via visual and interactive guidance.”

Powered by WPeMatico

Ryan Smith of Qualtrics speaks onstage during TechCrunch Disrupt SF 2015

Enterprise software giant SAP announced today that it has agreed to acquire Qualtrics for $8 billion in cash, just before the survey and research software company was set to go public. The deal is expected to be completed in the first half of 2019. Qualtrics last round of venture capital funding in 2016 raised $180 million at a $2.5 billion valuation.

This is the second-largest ever acquisition of a SaaS company, after Oracle’s purchase of Netsuite for $9.3 billion in 2016.

In a conference call, SAP CEO Bill McDermott said Qualtrics’ IPO was already oversubscribed and that the two companies began discussions a few months ago. SAP claims its software touches 77 percent of the world’s transaction revenue, while Qualtrics’ products include survey software that enables its 9,000 enterprise users to gauge things like customer sentiment and employee engagement.

McDermott compared the potential impact of combining SAP’s operational data with Qualtrics’ customer and user data to Facebook’s acquisition of Instagram. “The legacy players who carried their ‘90s technology into the 21st century just got clobbered. We have made existing participants in the market extinct,” he said. (SAP’s competitors include Oracle, Salesforce.com, Microsoft, and IBM.)

SAP, whose global headquarters is in Walldorf, Germany, said it has secured financing of €7 billion (about $7.93 billion) to cover acquisition-related costs and the purchase price, which will include unvested employee bonuses and cash on the balance sheet at close.

Ryan Smith, who co-founded Qualtrics in 2002, will continue to serve as its CEO. After the acquisition is finalized, the company will become part of SAP’s Cloud Business Group, but retain its dual headquarters in Provo, Utah and Seattle, as well as its own branding and personnel.

According to Crunchbase, the company raised a total of $400 million in VC funding from investors including Accel, Sequoia, and Insight Ventures. It had intended to sell 20.5 million shares in its debut for $18 to $21, which could have potentially grossed up to about $495 million. This would have put its valuation between $3.9 billion to $4.5 billion, according to CrunchBase’s Alex Wilhelm.

This year, Qualtrics’ revenue grew 8.5 percent from $97.1 million in the second-quarter to $105.4 million in the third-quarter, according to its IPO filing. It reported third-quarter GAAP net income of $4.9 million. That represented an increase from the $975,000 it reported in the previous quarter, as well as its net profit in the same period a year ago of $4.7 million. Qualtrics grew its operating cash flow to $52.5 million in the first nine months of 2018, compared to $36.1 million during the same period in 2017.

In today’s announcement, Qualtrics said it expects its full-year 2018 revenue to exceed $400 million and forecasts a forward growth rate of more than 40 percent, not counting the potential synergies of its acquisition by SAP.

Qualtrics’ main competitors include SurveyMonkey, which went public in September.

Powered by WPeMatico