corporate finance

Auto Added by WPeMatico

Auto Added by WPeMatico

The venture capital industry is less transparent today than at any time in recent memory.

For all the talk about expanding access and improving its sordid record on diversity, in reality, it has never been harder for founders to figure out who can even write a check to their startups in the first place.

When I first returned to TechCrunch after my second stint in venture capital, my first piece was entitled “The loss of first check investors.” While working in the venture capital industry, it was maddening to see — particularly at the pre-seed and seed stages — how few investors were really willing to go out on a limb and invest in founders before another VC had committed a check.

It’s only gotten worse in the past two years since that article, and the complexity comes from a number of different places. As our investigation showed more than a year ago, fewer and fewer venture rounds are being announced through SEC Form D filings.

There are almost no publicly accountable datasets left indicating who is writing checks in the venture industry and which companies are receiving those checks. While stealthiness is valid in the early days of a startup, the excuse wears thin after years.

Powered by WPeMatico

Corporate venture capital (CVC) is booming, with more than $50 billion of CVC capital deployed in 2018. The rise in capital expenditures by CVCs between 2013 and 2018 was an impressive 400%, according to Corporate Venturing Research Data. There are currently more than a hundred active CVC investors, and some sources suggest that almost half of all venture rounds include a strategic investor.

This rise has been driven by two factors: 1) the tech landscape is moving at a faster pace and bigger companies know they need to innovate quicker to meet market demand; and 2) the number of startups seeking CVC capital is growing as founders look beyond traditional venture funds to help grow their businesses.

Kruze Consulting and Goodwin have worked with hundreds of startups through the funding process, including those working with CVCs. Together, the two firms and their principals have decades of experience advising founders during and after their capital raises.

To help startups navigate CVC transactions, we’ve created a guide to working with CVCs. In this segment, we’ll discuss the types of CVCs, the best way to approach each type and the key things to keep in mind during initial discussions.

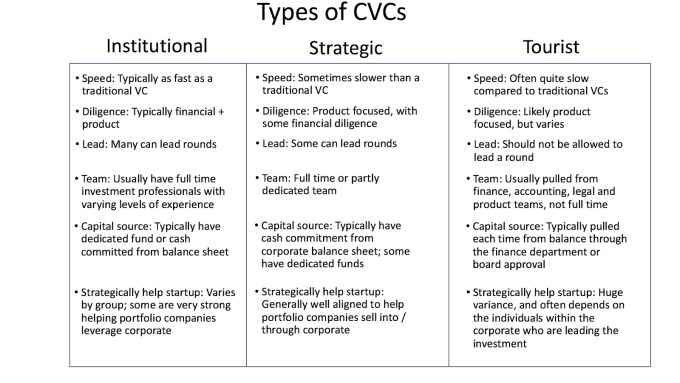

Roughly put, CVCs fall into three categories:

As the realm of CVCs becomes increasingly professionalized, more and more CVCs fall into the first category. For entrepreneurs seeking CVC investors, those in the institutional or strategic category can provide tremendous value — though it’s important that a startup know which type of CVC they’re speaking to, and have clear objectives going in that align with the CVC’s goals and strengths.

Before engaging with a CVC, or any potential investor for that matter, the most important step is to do your research. Who is the individual you’re meeting with? What’s his/her background and what deals has he/she done with this venture group? These are Must Knows before walking into the initial meeting.

Once you’re in early discussions, ask the CVC whether he or she has carry in the fund and whether the venture arm is autonomous. The answers to these questions will help you clarify whether you’re dealing with institutional versus strategic CVCs.

“With corporate-backed venture funds, it’s really key up front to know who you’re talking to,” says Allen. “It’s dangerous to call all groups that are nontraditional investors ‘CVCs’ since some are far more serious than others. Most have some degree of strategic mandate but many are increasingly investing for financial gain.”

The next question is: Are you dealing with a financially driven CVC or a strategically driven one? From a founder’s standpoint, you’ll need to know whether you’re meeting with an investor who views deals through the lens of, “I’m looking for a great team, huge market and a chance to bring in funding and connections to make a business as strong as it can be” or, “I’m looking for a solution/product/platform that I can bring into my company or use to expose my company to a brand new marketplace or technology.”

Once again, the way to determine which type of CVC you’re dealing with is to ask the right questions. In the first meeting, ask about their investment process, how investments are made and whether strategic business unit sponsorship is required for a given deal. The answers will tell you whether the CVC falls into Group 1 or 2, and you’ll be in a strong position to then make choices about whether this potential investor is right for you.

“Look for someone who will understand your business, meet with you and decide that there’s something beyond just capital that will form the basis for that relationship,” says Rick Prostko, managing director at Comcast Ventures. “In today’s venture market, founders want money AND value. Seek out a CVC who has valuable experience to provide, and look for someone who’s been an operator in this segment previously or who has valuable insight and experience to offer.”

Once you’ve done your initial diligence, developed a relationship and determined that a CVC could be a strong investor in your business, there are important factors to be aware of as you move into the next stage of discussions. These include:

Expect deeper product and technical diligence. CVCs can call on technical, product and market experts within their corporation during the due diligence process. As such, their level of product diligence is typically more rigorous than traditional VCs. Be prepared for some grilling by subject matter experts. On the flip side, this diligence process provides you with exposure to potential customers and partners inside the corporation, so use this time to your advantage.

Be aware that you’re going to share confidential information with a large company. “CVCs know that you’re only as good as your reputation,” says Eric Budin, director at Touchdown Ventures . “As such, there are very few examples of CVCs abusing confidential information, because news of it would get around so quickly.”

Still, for a founder, the goal is to be thoughtful and strategic with what you share, and to determine whether the CVC is truly interested in doing a deal before you hand over financial, technical and competitive information. It’s possible that commercial teams at the CVC sponsor could gain unfair advantage from seeing your information, or use their CVC to gain valuable intel on the competition.

On the other hand, sharing your intel could be a fantastic way to get in front of an internal team at the parent company. The key is to think carefully about what you are being asked to share and with whom, and set ground rules with the CVC before they begin diligence.

“It’s important to understand how the corporate fund is structured and how they handle any information that’s shared,” says Prostko. “It might be in your interest to loop in a business unit [within the parent company] that could benefit from learning about your business. On the flip side, if the CVC is a potential competitor, you’ll want to be more careful about what you reveal.”

There will be a risk of regime change. Large companies operate like, well, large companies. People leave, management changes happen and priorities shift. At the outset, ask questions such as: Who will support your company if the commercial manager leading your investment leaves? What will happen to the CVC if the person leading the venture arm is fired? Will they do their pro-rata if the person leading your deal is gone? What happens to any commercial relationships that you might be working on? It’s important to have a keen understanding of internal dynamics before you enter the relationship.

“In general, the more successful a firm is, the more likely the CVC will stick around,” says Allen. “Be sure to look at the individual’s history at the firm, how long he or she has been there, and whether he or she has jumped from fund to fund. If the investing partner has come out of the corporate ‘mother ship,’ and lacks any credible venture experience, buyer beware.”

The CVC may be subject to regulatory rules. Depending on the industry, government regulations may impact how your deal is structured. Banks, for example, are subject to rules that can restrict the percentage of voting stock they can own. Foreign investors may need to comply with CFIUS regulations if your company provides certain specified technologies. Generally, the CVCs will understand the regulations that apply to them. They may not, however, bring them up until late in the process, which could lead to delays.

Commercial transactions with the corporate arm can slow things down. Purely strategic CVCs (Group 2) often require a commercial transaction to happen in connection with a venture deal. The process involved in these transactions often takes longer than the financing process, which can cause issues if the CVC is a key (but not sole) investor in the round. If you’re dealing with a Group 2 CVC, discuss this issue ahead of time to see if you can decouple the two transactions and close the investment prior to inking the commercial deal.

CVCs offer a wealth of capital, human resources and corporate partnerships for startups. But whether you choose to take CVC capital or not, you can benefit from merely approaching CVCs if you have business units operating in either the same space or a tangential space. An initial meeting both gives you an opportunity to do a sales pitch and offers the CVC a chance to vet a product or team and gain some deal insight. For founders, you gain a powerful sales opportunity that might have otherwise taken months or years to obtain.

“Even if you’re told ‘no’ by a CVC, the meeting could result in a good business relationship that could turn into a sales opportunity for you in the near future,” says Prostko.

The WRONG way to think about approaching CVC investors is something along the lines of, “I can’t raise what I want from financial VCs so I’ll go to CVCs as my second choice, since they’re more likely to say ‘yes’ and/or give me better terms.” This attitude will shut doors and cut you off from valuable partners, capital and opportunities to strategically grow your business.

Above all, stay informed as you choose whom to bring in as a partner. Ultimately, it’s your business and the responsibility to ensure that you bring in the right capital partners lies with you.

Powered by WPeMatico

If you’ve been lucky enough to keep your job or business, you almost certainly know someone who wasn’t so fortunate.

Thousands have lost their jobs as companies significantly reduce workforces to adjust to uncertainties and economic challenges created by COVID-19. Many of these people in tech are now faced with a number of questions, from how they’ll pay next month’s rent to whether they’re eligible for unemployment. One area that is particularly confusing is what to do if your compensation package was tied to equity.

Here are some ways I suggest approaching the issue.

Layoffs have become part and parcel of the current economic crisis with unemployment figures skyrocketing to record highs as a result of COVID-19. From multinational conglomerates to mom-and-pop stores, everyone is feeling the impact, and the startup sector is no different.

Despite difficult circumstances, the silver lining for employees is that we have seen many management teams go the extra mile to help their teams, especially when it comes to equity. Compared to traditional layoff situations, companies in the COVID-19 era are offering generous extensions and accelerated vesting on their options, which is undeniably good news for employees with equity.

Typically, equity plans come with a 90-day exercise window after employment termination. That means that if you leave the company, you will have to exercise your options within 90 days or they go back to the company. However, lots of management teams have decided to extend these deadlines many years out given the circumstances.

While layoffs are not easy, it’s been great to see management teams doing the right thing when it comes to equity for their employees who have been laid off. Offering extensions is a benefit that employers should be offering their employees who have helped build the company.

If your company is not offering this, consider negotiating and asking for an extension. This is the right thing to do for employees who are now out of work and a paycheck for the foreseeable future. Both options do not require the company to pay cash at the moment, so there are few reasons a company should deny this request in this environment.

Even if you are granted an extension to exercise your options, employees that hold incentive stock options (ISOs) should look into exercising their options now to maximize their equity’s value.

Many companies are offering extensions for option exercises. While this is great in that it gives employees more time to figure out their exercise situation, waiting past the 90-day window may have much bigger tax consequences that employees need to consider.

ISOs are much more tax advantageous compared to non-qualified stock options (NSOs). They are not taxed under standard income tax and if you sell the stock two years after grant date and one year after exercise date, you sell them as part of a qualifying disposition. In short, this allows you to effectively convert everything north of your strike price to preferential long-term capital gain rates.

As part of offering these tax advantages, the tax code has limitations on ISOs. Most relevant to us at this point is that the fact that you cannot have ISOs past 90 days after you are no longer an employee. This means that even if your company allows an extension on your stock options past the typical 90-day expiration window, your ISOs will convert to NSOs and lose their tax benefit.

This creates a potential planning opportunity that employees who have been laid off need to consider. If you feel good about the upside of the company, then you should consider exercising your ISOs today to capture the potential tax benefits rather than letting them convert to NSOs. Employees who wait risk putting themselves in the same difficult situation once the extension ends at typically less favorable conditions due to an increased 409A valuation.

In light of the economic slowdown many companies have begun to cut costs. Reduced pay or furloughing employees has become the new norm as businesses of all sizes struggle to navigate these changing times.

It can obviously be concerning if you find yourself in this situation. But for startup employees, the COVID-19 crisis could provide an opportunity to negotiate your compensation package to make up for this decrease, and even set yourself up to prosper in the future.

Startups typically offer equity as a means of deferred compensation and as a way to incentivize employees to own a piece of the company they are building. The compensation is deferred as most startups are cash-strapped and cannot afford to pay you what a larger company may be able to.

If your company is now asking you to take a pay cut, or even take no pay during this time, you should consider asking for additional equity to make up for the lost compensation. While not all companies may be amenable to offering more equity, there is no cash outlay from the company’s standpoint, so it’s an efficient way for your company to compensate you for your sacrifice while preserving their cash.

In addition, offering more equity shows a commitment from management to their employees during this difficult time. It may be the win-win scenario for your company and yourself in the long-run so it’s worth having the conversation with management to discuss if this is available for you.

If your company does offer you more equity, make sure you ask whether the 409A (or fair market value) of the company is being updated. With revised forecasts given the COVID-19 situation, it may be possible for your company to issue your stock at a lower strike price if the company revalues its 409A.

I can sympathize with startup employees right now because I faced a similar situation when I left a startup that I had joined as employee number four and was forced to wave goodbye to the equity I had banked on.

If you want to take action on equity but don’t know where to start, now might be a good time to brush up on how your stock options work. As the economy begins to reopen, there’s a good chance we’ll see a rush for candidates in tech as companies compete to bring in some of the extremely talented folks who lost their jobs this week.

Those who have a good understanding of equity may be positioned for a big payday down the line.

Powered by WPeMatico

When we launched in 2016, we took the unusual approach of saying we’d buy common stock in startups. We believed then, and still do, that alignment with founders was more important than covering our downside in investments that didn’t work as planned. Said differently, we wanted to enhance our upside through alignment, rather than maximizing our downside through terms.

The world has changed a lot since that time. While we are actively making investments, and still buying common stock, we know that many entrepreneurs may be trying to raise money now — and it is very hard.

Fred Destin wrote a great piece about the ugly terms that can creep into term sheets during difficult times. If you have a choice between a good term sheet and a bad one, of course, you’ll take the good one. But what if you have no choice? And how can you compare term sheets in the first place?

To this end, we developed the term-sheet grader, a simple way to compare different term sheets or help characterize whether a term sheet is good or evil.

Let me first point out that none of this has anything to do with the valuation of the round (share price), the amount of capital, the likelihood of reaching a closing, the quality of the firm or the trust you have with the individual leading the investment, all absolutely critical pieces of the puzzle. Here, we are just looking at the terms and conditions, the legal structure of the investment.

We’ve listed nine key terms below — five that have to do with economics and four that relate to control and decision-making:

FWIW, the Pillar common stock standard deal earns a +8 (shown below).

Powered by WPeMatico

Despite all evidence to the contrary, there’s more to building a startup than raising venture capital.

Founders are finding success without overly relying on VC dollars; some are even sharing profits with their respective employees and customers without the help of traditional funding and Silicon Valley power dynamics.

As some investors slow down their funding pace, it has become clear that profitability trumps funding and venture capital can only take a startup so far when the economy tanks and outside cash streams dry up.

In the Indie.vc portfolio, profitability is its driving force. In fact, its main criterion for funding is that a startup must be on a clear path to profitability with durable fundamentals like high gross margins or the ability to start charging for a product right away, as opposed to companies that need a significant amount of upfront investment for research and development.

Profitability, Indie.vc founder Bryce Roberts tells TechCrunch, needs to be a habit, and founders need to recognize that it’s not a switch they can just turn on. Startups looking to prioritize profitability need to start out as revenue-driven businesses that replace funding milestones with profitability goals.

“Genuinely, it’s not rocket science,” he says. “Profitability isn’t this crazy, elusive thing. It’s literally more achievable than a Series A round. It’s way more achievable than a Series B round. If you look at the kind of fall-off between those rounds, most entrepreneurs would be better off finding their path to profitability and scale.”

Indie.vc, which recently announced its latest batch of investments, advises founders to make sure they have what they need to be stable and then to create and measure value, Roberts says. That value, which differs depending on the company, must be quantifiable as some metric or revenue.

To do that, Roberts says founders should adopt a mindset where they’re focused on creating revenue opportunities, rather than cost savings. Indie.vc’s model also does not prioritize hiring ahead of growth, a strategy that seems to be working for its portfolio during the pandemic.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Today we’re taking a look at a bit of data on the European venture capital scene in Q1. As with our looks at other locales like Silicon Valley and other bits of the United States, we’re taking stock of what happened in the first quarter. Q1 2020 includes pre-COVID-19 results, though as some European countries began to lock-down before the United States, there may be more pandemic-impact in the following results than we’ve seen domestically thus far.

Today’s grip of data is via the folks over at PitchBook, who compiled a venture-focused dig through the continent’s first three months of the year. Let’s parse the top numbers, make a comparison or two and then look to what’s next.

Despite COVID-19, China’s broad shuttering and an aged bull market deep, Europe’s venture capital activity in Q1 2020 was mostly fine. It wasn’t great, and there were some less-than-winsome results that could be chalked up to the pandemic, but the first quarter provided an alright start to the year.

Powered by WPeMatico

As silently and swiftly as it has devastated families and communities around the world, COVID-19 has also left many startups gasping for air. Emerging companies with strong 2020 revenue forecasts have seen their high-confidence plans reduced by 60%-80% in a matter of days. Even in the best of times, startups must reach value-unlocking milestones to successfully raise new capital. But today, a globally synchronized halt to business activity has made irrelevant normal benchmarks for financing rounds.

Obtaining payroll support from the recently enacted special government programs for small businesses will not resolve the cascading problems startups are grappling with, regardless of whether or not they are VC-backed.

Product development roadmaps in many innovation-driven industries are changing in ways that may permanently alter a company’s future strategic direction. Merger and acquisition discussions are being shelved. Normal financing rounds, in process and contemplated, are contracting or being abandoned altogether. Many venture funds, including corporate venture programs, have unilaterally “taken a pause” to reevaluate the radically changing landscape for their early-stage company portfolios.

I last experienced this phenomenon in the aftermath of the Great Technology Bubble: 2002-2003. And all signs show that we are at the beginning of a new round of punitive “incentives” for venture investors to keep their companies alive.

Several of my current portfolio companies have recently proposed “emergency bridge” convertible note financings of between $5 million and $15 million, each featuring a painful feature for non-participants: multiple liquidation preferences benefiting only the new money above 3x, with discounts greater than 20% on conversion in a new equity financing. Of course, these financings are open to both existing and new investors. But the likelihood of another round is actually diminished by this type of structure.

Powered by WPeMatico

Today after the bell, Zoom reported its Q4 earnings. The company’s recorded revenue of $188.3 million and its adjusted per-share profit of $0.15 were ahead of expectations, including $176.55 million in revenue and earnings per share of $0.07, according to Yahoo Finance averages.

Down several points during a broad market rally, Zoom has been a hot company to track in recent months. Its profile was heightened due to its position as an incidental benefactor of the world’s grappling with the novel coronavirus — as more countries and companies stressed staying home and working remotely, respectively, Zoom’s video conferencing tool was expected to see rising usage and demand.

The company’s shares were down sharply after reporting its earnings.

What follows is a dive into Zoom’s Q4 earnings, its expectations for the coming period and what those figures may have to say about the infection and its impacts. We’ll wrap with notes from startups that are building remote-work friendly products, sharing what they are seeing on the ground regarding demand for their services during this bleakly fascinating period of history.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This week we had TechCrunch’s Alex Wilhelm and Danny Crichton on hand to dig into the news, with Chris Gates on the dials and more news than we could possibly cram into 30 minutes. So we went a bit over; sorry about that.

We kicked off by running through a few short-forms to get things going, including:

Turning to longer cuts, the team dug into the latest from SoftBank, its Vision Fund and the successes and struggles of its enormous startup bets. Leading the news cycle this week were layoffs at Zume, a robotic pizza delivery venture that is no longer pursuing robotic pizza delivery. Now it’s working on sustainable packaging. Cool, but it’s going to be hard for the company to grow into its valuation while pivoting.

Other issues have come up — more here — that paint some cracks onto the Vision Fund’s sunny exterior. Don’t be too beguiled by the bad news, Danny says; venture funds run like J-Curves, and there are still winners in that particular portfolio.

After that, we turned to China, in particular its venture slowdown. The bubble, in Danny’s view, has burst. The story discussed is here, if you want to read it. The short version for the lazy is that not only has China’s venture scene slowed down dramatically, but startups — even those with ample capital raised — are dying by the hundred. But one highly caffeinated Chinese startup continues to find growth in the world’s greatest tea market.

Finally we hit on the Sam Altman wager and the latest from Sisense, which is now a unicorn. All that and we had some fun.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Venture capital investment exploded across a number of geographies in 2019 despite the constant threat of an economic downturn.

San Francisco, of course, remains the startup epicenter of the world, shutting out all other geographies when it comes to capital invested. Still, other regions continue to grow, raking in more capital this year than ever.

In Utah, a new hotbed for startups, companies like Weave, Divvy and MX Technology raised a collective $370 million from private market investors. In the Northeast, New York City experienced record-breaking deal volume with median deal sizes climbing steadily. Boston is closing out the decade with at least 10 deals larger than $100 million announced this year alone. And in the lovely Pacific Northwest, home to tech heavyweights Amazon and Microsoft, Seattle is experiencing an uptick in VC interest in what could be a sign the town is finally reaching its full potential.

Seattle startups raised a total of $3.5 billion in VC funding across roughly 375 deals this year, according to data collected by PitchBook. That’s up from $3 billion in 2018 across 346 deals and a meager $1.7 billion in 2017 across 348 deals. Much of Seattle’s recent growth can be attributed to a few fast-growing businesses.

Convoy, the digital freight network that connects truckers with shippers, closed a $400 million round last month bringing its valuation to $2.75 billion. The deal was remarkable for a number of reasons. Firstly, it was the largest venture round for a Seattle-based company in a decade, PitchBook claims. And it pushed Convoy to the top of the list of the most valuable companies in the city, surpassing OfferUp, which raised a sizable Series D in 2018 at a $1.4 billion valuation.

Convoy has managed to attract a slew of high-profile investors, including Amazon’s Jeff Bezos, Salesforce CEO Marc Benioff and even U2’s Bono and the Edge. Since it was founded in 2015, the business has raised a total of more than $668 million.

Remitly, another Seattle-headquartered business, has helped bolster Seattle’s startup ecosystem. The fintech company focused on international money transfer raised a $135 million Series E led by Generation Investment Management, and $85 million in debt from Barclays, Bridge Bank, Goldman Sachs and Silicon Valley Bank earlier this year. Owl Rock Capital, Princeville Global, Prudential Financial, Schroder & Co Bank AG and Top Tier Capital Partners, and previous investors DN Capital, Naspers’ PayU and Stripes Group also participated in the equity round, which valued Remitly at nearly $1 billion.

Up-and-coming startups, including co-working space provider The Riveter, real estate business Modus and same-day delivery service Dolly, have recently attracted investment too.

A number of other factors have contributed to Seattle’s long-awaited rise in venture activity. Top-performing companies like Stripe, Airbnb and Dropbox have established engineering offices in Seattle, as has Uber, Twitter, Facebook, Disney and many others. This, of course, has attracted copious engineers, a key ingredient to building a successful tech hub. Plus, the pipeline of engineers provided by the nearby University of Washington (shout-out to my alma mater) means there’s no shortage of brainiacs.

There’s long been plenty of smart people in Seattle, mostly working at Microsoft and Amazon, however. The issue has been a shortage of entrepreneurs, or those willing to exit a well-paying gig in favor of a risky venture. Fortunately for Seattle venture capitalists, new efforts have been made to entice corporate workers to the startup universe. Pioneer Square Labs, which I profiled earlier this year, is a prime example of this movement. On a mission to champion Seattle’s unique entrepreneurial DNA, Pioneer Square Labs cropped up in 2015 to create, launch and fund technology companies headquartered in the Pacific Northwest.

Boundless CEO Xiao Wang at TechCrunch Disrupt 2017

Operating under the startup studio model, PSL’s team of former founders and venture capitalists, including Rover and Mighty AI founder Greg Gottesman, collaborate to craft and incubate startup ideas, then recruit a founding CEO from their network of entrepreneurs to lead the business. Seattle is home to two of the most valuable businesses in the world, but it has not created as many founders as anticipated. PSL hopes that by removing some of the risk, it can encourage prospective founders, like Boundless CEO Xiao Wang, a former senior product manager at Amazon, to build.

“The studio model lends itself really well to people who are 99% there, thinking ‘damn, I want to start a company,’ ” PSL co-founder Ben Gilbert said in March. “These are people that are incredible entrepreneurs but if not for the studio as a catalyst, they may not have [left].”

Boundless is one of several successful PSL spin-outs. The business, which helps families navigate the convoluted green card process, raised a $7.8 million Series A led by Foundry Group earlier this year, with participation from existing investors Trilogy Equity Partners, PSL, Two Sigma Ventures and Founders’ Co-Op.

Years-old institutional funds like Seattle’s Madrona Venture Group have done their part to bolster the Seattle startup community too. Madrona raised a $100 million Acceleration Fund earlier this year, and although it plans to look beyond its backyard for its newest deals, the firm continues to be one of the largest supporters of Pacific Northwest upstarts. Founded in 1995, Madrona’s portfolio includes Amazon, Mighty AI, UiPath, Branch and more.

Voyager Capital, another Seattle-based VC, also raised another $100 million this year to invest in the PNW. Maveron, a venture capital fund co-founded by Starbucks mastermind Howard Schultz, closed on another $180 million to invest in early-stage consumer startups in May. And new efforts like Flying Fish Partners have been busy deploying capital to promising local companies.

There’s a lot more to say about all this. Like the growing role of deep-pocketed angel investors in Seattle have in expanding the startup ecosystem, or the non-local investors, like Silicon Valley’s best, who’ve funneled cash into Seattle’s talent. In short, Seattle deal activity is finally climbing thanks to top talent, new accelerator models and several refueled venture funds. Now we wait to see how the Seattle startup community leverages this growth period and what startups emerge on top.

Powered by WPeMatico