corporate finance

Auto Added by WPeMatico

Auto Added by WPeMatico

Spotify did it. Slack did it. Many other late-stage private technology companies are reported to be seriously considering it. Should yours?

If you are a board member of a late-stage, venture-backed company or part of its management team, you likely have heard of the term “direct listing.” Or you may have attended one or all of the slew of recent conferences being hosted by big-name investment banks and others, including tech investor guru Bill Gurley, who recently debated the pros and cons of choosing a direct listing over a traditional IPO.

Before you decide what’s right for your company, here are a few things you need to know about direct listings.

For people not familiar with the term, a direct listing is an alternative way for a private company to “go public,” but without selling its shares directly to the public and without the traditional underwriting assistance of investment bankers.

In a traditional IPO, a company raises money and creates a public market for its shares by selling newly created stock to investors. In some instances, a select number of pre-IPO investors, usually very large stockholders or management, may also sell a portion of their holdings in the IPO. In an IPO, the company engages investment bankers to help promote, price and sell the stock to investors. The investment bankers are paid a commission for their work that is based on the size of the IPO—usually seven percent for a traditional technology company IPO.

In a direct listing, a company does not sell stock directly to investors and does not receive any new capital. Instead, it facilitates the re-sale of shares held by company insiders such as employees, executives and pre-IPO investors. Investors in a direct listing buy shares directly from these company insiders.

Does this mean that a company doing a direct listing doesn’t need investment banks? Not quite. Companies still engage investment banks to assist with a direct listing and those banks still get paid quite well (to the tune of $35 million in Spotify and $22 million in Slack).

However, the investment banks play a very different role in a direct listing. Unlike a traditional IPO, in a direct listing, investment banks are prohibited under current law from organizing or attending investor meetings and they do not sell stock to investors. Instead, they act purely in an advisory capacity helping a company to position its story to investors, draft its IPO disclosures, educate a company’s insiders on process and strategize on investor outreach and liquidity.

The concept of a direct listing is actually not a new one. Companies in a variety of industries have used similar structures for years. However, the structure has only recently received a lot of investor and media attention because high-profile technology companies have started to use it to go public. But why have technology companies only recently started to consider direct listings?

The rise of massive pre-IPO fundraising rounds

With an abundance of investor capital, especially from institutional investors that historically hadn’t invested in private technology companies, massive pre-IPO fundraising rounds have become the norm. Slack raised over $400 million in August 2018—just over a year prior to its direct listing. Because of this widespread availability of capital, some technology companies are now able to raise sufficient capital before their actual IPO to either become profitable or put them on a path to profitability.

Criticism of current IPO process

There has been increasing negative sentiment, especially amongst well-known venture capitalists, about certain aspects of the traditional IPO process—namely IPO lock-up agreements and the pricing and allocation process.

IPO lock-up agreements. In a traditional IPO, investment bankers require pre-IPO investors, employees and the company to sign a “lock-up agreement” restricting them from selling or distributing shares for a specified period of time following the IPO—usually 180 days. The bankers put these agreements in place in order to stabilize the stock immediately after the IPO. While the merits of a lock-up agreement can certainly be debated, by the time VCs (and other insiders) are allowed to sell following an IPO, oftentimes the stock price has fallen significantly from its highs (sometimes to below the IPO price) or the post lock-up flood of selling can have an immediate negative impact on the trading price.

In a direct listing, there is no lock-up agreement, which allows for equal access to the offering to all of the company’s pre-IPO investors, including rank-and-file employees and smaller pre-IPO stockholders.

IPO pricing and allocation: In a traditional IPO, shares are often allocated directly by a company (with the assistance of its underwriters) to a small number of large, institutional investors. Traditional IPOs are often underpriced by design to provide large institutional investors the benefit of an immediate 10-15% “pop” in the stock price. Over the last few years, some of these “pops” have become more pronounced. For example, Beyond Meat’s stock soared from $25 to $73 on its first day of trading, a 163% gain. This has fueled a concern, particularly shared amongst the VC community, that investment banks improperly price and allocate shares in an IPO in order to benefit these institutional investors, which are also clients of the same investment banks that are underwriting the IPO. While the merits of this concern can also be debated, in instances where there is a large price discrepancy between the trading price of the stock following the IPO and the price of the IPO, there is often a sense that companies have left money on the table and that pre-IPO investors have suffered unnecessary dilution. If the IPO had been priced “correctly,” the company would have had to sell fewer shares to raise the same amount of proceeds.

Because a company is not selling stock in a direct listing, the trading price after listing is purely market driven and is not “set” by the company and its investment bankers. Moreover, since no new shares are issued in a direct listing, insiders do not suffer any dilution.

The Spotify effect

Before Spotify’s direct listing, technology companies hadn’t used the direct listing structure to go public. Spotify was, in many ways, the perfect test case for a direct listing. It was well known, didn’t need any additional capital and was cash flow positive. In addition, prior to its direct listing, Spotify had entered into a debt instrument that penalized the company so long as it remained private. As a result, it just needed to go public. After clearing some regulatory hurdles, Spotify successfully executed its direct listing in April 2018. After Spotify’s direct listing, Slack (relatively) quickly followed suit. Slack’s direct listing was notable because it represented the first traditional Silicon Valley-based VC-backed company to use the structure. It was also an enterprise software company, albeit one with a consumer cult following.

While a direct listing offers many benefits, the structure does not make sense for every company. Below is a list of key benefits and drawbacks:

Powered by WPeMatico

Founders, entrepreneurs, and tech executives in the know realize they may be able to avoid paying tax on all or part of the gain from the sale of stock in their companies — assuming they qualify.

If you’re a founder who’s interested in exploring this opportunity, put careful consideration put into the formation, operation and selling of your company.

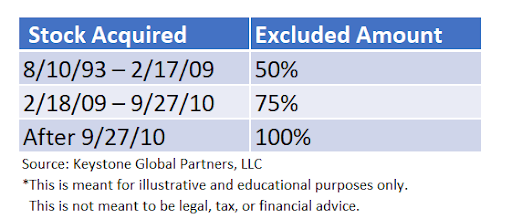

Qualified Small Business Stock (QSBS) presents a significant tax savings opportunity for people who create and invest in small businesses. It allows you to potentially exclude up to $10 million, or 10 times your tax basis, whichever is greater, from taxation. For example, if you invested $2 million in QSBS in 2012, and sell that stock after five years for $20 million (10x basis) you could pay zero federal capital gains tax on that gain.

These tax savings can be so significant, that it’s one of a handful of high-priority items we’ll first discuss, when working with a founder or tech executive client. Surprisingly, most people in general either:

Founders who are scaling their companies usually have a lot on their minds, and tax savings and personal finance usually falls to the bottom of the list. For example, I recently met with someone who will walk away from their upcoming liquidity event with between $30-40 million. He qualifies for QSBS, but until our conversation, he hadn’t even considered leveraging it.

Instead of paying long-term capital gains taxes, how does 0% sound? That’s right — you may be able to exclude up to 100% of your federal capital gains taxes from selling the stake in your company. If your company is a venture-backed tech startup (or was at one point), there’s a good chance you could qualify.

In this guide I speak specifically to QSBS on a federal tax level, however it’s important to note that many states such as New York follow the federal treatment of QSBS, while states such as California and Pennsylvania completely disallow the exclusion. There is a third group of states, including Massachusetts and New Jersey, that have their own modifications to the exclusion. Like everything else I speak about here, this should be reviewed with your legal and tax advisors.

My team and I recently spoke with a founder whose company was being acquired. She wanted to do some financial planning to understand how her personal balance sheet would look post-acquisition, which is a savvy move.

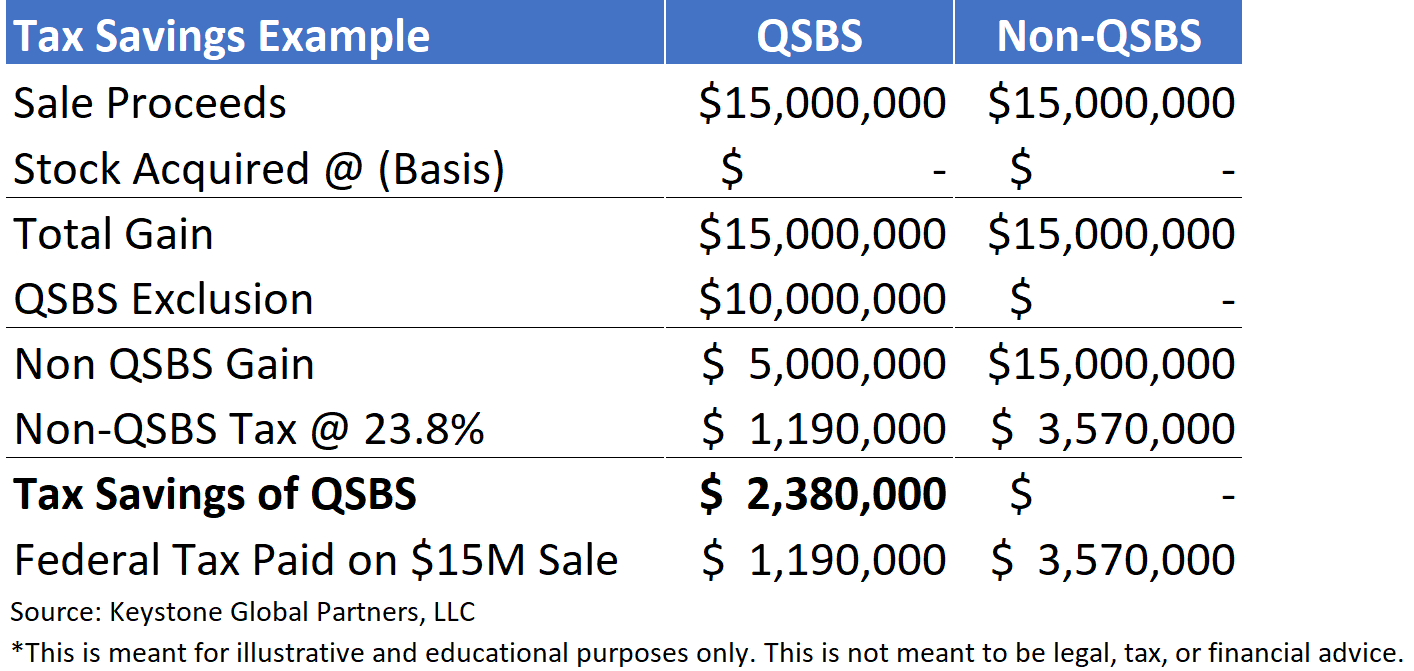

We worked with her corporate counsel and accountant to obtain a QSBS representation from the company and modeled out the founder’s effective tax rate. She owned equity in the form of company shares, which met the criteria for qualifying as Section 1202 stock (QSBS). When she acquired the shares in 2012, her cost basis was basically zero.

A few months after satisfying the five-year holding period, a public company acquired her business. Her company shares, first acquired for basically zero, were now worth $15 million. When she was able to sell her shares, the first $10 million of her capital gains were completely excluded from federal taxation — the remainder of her gain was taxed at long-term capital gains.

This founder saved millions of dollars in capital gains taxes after her liquidity event, and she’s not the exception! Most founders who run a venture-backed C Corporation tech company can qualify for QSBS if they acquire their stock early on. There are some exceptions.

A frequently asked question as we start to discuss QSBS with our clients is: how do I know if I qualify? In general, you need to meet the following requirements:

When in doubt, follow this flowchart to see if you qualify:

Powered by WPeMatico

Harlem Capital has upgraded from angel syndicate to full-fledged venture capital fund, closing its debut effort on an oversubscribed $40.3 million.

The firm was launched by managing partners Henri Pierre-Jacques and Jarrid Tingle in New York City’s Harlem neighborhood in 2015. The pair have since graduated from Harvard Business School and hired two venture partners, Brandon Bryant and John Henry, and two senior associates to help expand their portfolio. The over-arching goal: invest in 1,000 diverse founders over the next 20 years.

“We fundamentally believe we are a venture fund with impact, not an impact fund,” Pierre-Jacques tells TechCrunch. “The way we generate impact is to give women and minority entrepreneurs ownership.”

Capital from Harlem Capital Partners Venture Fund I, an industry-agnostic vehicle that invests in post-revenue businesses across the U.S., will be used to lead, co-lead or participate in $250,000 to $1 million-sized seed or Series A financings. To date, the team has backed 14 companies, including B2B feminine hygiene product Aunt Flow, gig economy marketplace Jobble and pet wellness platform Wagmo. Harlem Capital plans to add another 22 businesses to Fund 1.

You need diversity funds like ourselves to get this market anywhere close to parity. Harlem Capital managing partner Jarrid Tingle

With its first fund close, Harlem Capital becomes one of the largest venture capital funds with a diversity mandate. Despite an increasing amount of punishing data exposing the gender and race gap in venture capital, minority founders continue to rake in just a small percentage of funding each year. According to a RateMyInvestor and Diversity VC report released earlier this year, most VC dollars are invested in companies run by white men with a university degree. Other recent data indicates startups founded exclusively by women raised just 2.2% of overall VC funding in 2018, with numbers on pace to increase only slightly in 2019. Meanwhile, the median amount of funding raised by black female founders, as of 2018, was $0.

The stark contrast in funding for female versus male entrepreneurs or white women versus black women founders is in part a result of a lack of diversity amongst general partners at venture capital funds and amongst the limited partners that choose which venture capital funds to provide capital. While there’s little data available on diversity of LPs, 81% of VC firms didn’t have a single black investor as of 2018.

“There’s no rational reason why this problem exists,” Tingle tells TechCrunch. “It persists because VC funds in general have been closely held and clustered around Silicon Valley. They come from particular schools with particular networks with a small head count that doesn’t turn over frequently. Some firms have strategically added a few partners here and there, but not enough to change the organization. You need diversity funds like ourselves to get this market anywhere close to parity.”

“A lot of investors are frankly missing out on opportunities,” Tingle adds.

Having met through the Management Leadership for Tomorrow Program, a nonprofit organization identifying a new generation of leadership, Tingle and Pierre-Jacques have built a prolific internship program at the firm. With as many as six interns admitted each quarter, the goal is to train future investors of color.

Limited partners in Harlem Capital Partners Fund I include TPG Global, State of Michigan Retirement Systems, the Consumer Technology Association and Dorm Room Fund .

Powered by WPeMatico

Why raise venture capital when you can raise debt and keep your equity?

That’s the question a whole slew of new financial technology companies are hoping entrepreneurs will ask themselves as they begin to think about collecting outside capital for their businesses. Clearbanc made waves with its “20-Minute Term Sheet” campaign, with a goal of backing 2,000 businesses with $1 billion in non-dilutive capital by the end of 2019. Now, Capital is launching to educate founders about the possibility of debt funding.

Founded by former Draper Fisher Jurvetson (now known as Threshold Ventures) investor Blair Silverberg, Csaba Konkoly and Chris Olivares, Capital is launching today with $5 million from Future Ventures, Greycroft, Wavemaker and others. Additionally, it’s raised from “prominent institutional pools of capital” to invest between $5 million and $50 million in promising companies, determined using “The Capital Machine.”

Capital co-founder Blair Silverberg.

Capital’s underwriting technology, dubbed The Capital Machine, determines if businesses have the growth potential necessary for an infusion of debt (by analyzing revenue and other financial considerations), then delivers term sheets within 24 hours. The expedited process cuts out the time-consuming elements of pitching venture capitalists, the company says, allowing businesses to go from zero to $5 million — or more — in a matter of hours.

For companies that are’t ready for a debt round, or that don’t meet Capital’s qualification, the company is offering access to a free calculator that determines the cost of a company’s capital based on their fundraising and valuation data.

“We are trying to create a business that is the place that all founders go to start their fundraising process,” Silverberg tells TechCrunch. “We just want entrepreneurs to understand that step one in building a balance sheet is to understand your cost of capital. Step two is you can now use that to compare your financing options. We hope we can make this process simpler and more transparent.”

Capital charges a 5% to 15% flat fee on its capital, investing a maximum of $50 million over time. The company has ambitions of becoming a holistic investment bank of sorts, says Silverberg, ready and willing to advise companies on fundraising possibilities and connect them with VCs for future deals.

Historically, Silverberg explains, venture capital dollars went to risky upstarts poised to disrupt a category. Today, loads of equity funding is funneled into predictable business models that could be funded entirely with non-dilutive capital: “I saw what the venture process was like,” Silverberg said, referencing his stint at DFJ. “Tech companies do not utilize debt … this is extremely expensive for founders.”

There’s a culture surrounding venture capital fundraising in Silicon Valley and beyond. One in which startups seek to become “unicorns,” hoping for stories on this very site to laud their accomplishments — including the loads of venture capital dollars they’ve pulled in. In reality, much of that capital is plowed into things like Facebook and Google to fuel digital ad campaigns, which is not how VC is intended to be used and can result in founders taking a company public with just a few percentage points of ownership.

Solutions like Capital, Clearbanc, Lighter Capital and others should remind entrepreneurs that venture capital isn’t the only route to getting a company off the ground and can be raised in addition to venture debt.

“There’s no excuse for not knowing your cost of capital,” Silverberg adds.

Powered by WPeMatico