corporate finance

Auto Added by WPeMatico

Auto Added by WPeMatico

Demetrius Curry has spent the last couple years chasing a dream.

His startup, College Cash, allows brands to petition users to create photo and video marketing content highlighting their product or service, with the wrinkle being that content creators are paid by the brands in the form of credits that go directly toward paying down their student loan debt. This model awards the brands involved a level of social good will and tax benefits.

The Dallas-area founder was inspired to tackle the student loan debt crisis after talking with his daughter about the prospect of eventually paying down her own loan debt. Curry has spent the past two years building out the nascent platform, tracking down brand partners, navigating accelerator programs, enticing users and pounding the pavement to find investors willing to bet on his vision.

College Cash has raised $105,000 to date, and is hoping to eventually wrap the funding into a $1 million seed round.

Filling out the round has been its own challenge for Curry, who has struggled at times to find opportunity, even among historic levels of capital flowing into the startup ecosystem, a distinction that has been less noticeable for black founders that still make up just a small percentage of VC allocation. In the aftermath of last summer’s protests against police brutality, a number of venture capital firms issued statements decrying institutional racism and pledging to back more underserved founders, spinning up new programs for diverse founders.

Demetrius Curry, CEO of College Cash

While Curry says he appreciates the scope of the problem and the good intentions of those making the statements, he believes that venture capital networks still have a lot to learn about what being an “underserved” founder means, and that plenty of the existing efforts feel like “lip service.” He says that even as Silicon Valley continues to idolize dropouts from prestigious universities, stakeholders have less interest in recognizing the accomplishments of founders who fought their way through poverty or found opportunity in geographies where opportunities are harder to come by.

“You can’t look for something different if you’re looking in the same places,” Curry tells TechCrunch. “When you look at the topic of ‘underserved founders,’ it’s not only a skin color thing, it’s also about where they came from and what they’ve been through.”

Curry says that it can be frustrating to compete for early-stage opportunities when investors aren’t willing to meaningfully adjust their parameters. Of particular frustration to Curry has been navigating the world of “warm introductions” to even get a foot in the door for programs meant for diverse founders, or applying for early-stage programs geared toward the “underserved” only to be told that they weren’t far enough along to qualify.

“Think about how much we had to go through to even get in the room with you,” Curry says. “I’ve sold plasma to pay a web hosting fee, nothing is going to stop me.”

College Cash’s mission of expanding opportunities for people struggling to manage their student loan debt is personal to Curry, who saw his life turn around after going back to school.

Decades ago, fresh out of the military, Curry said he had a random conversation with a stranger while eating at a Hardee’s — the discussion about what more he wanted from life ended up pushing him to to go back and get his GED and later a business degree. What followed was a career in finance that eventually led toward his recent entrepreneurial pursuits with College Cash.

The platform is firmly an early-stage venture at the moment, but Curry has big ambitions he’s building toward. His next effort is building out a College Cash tipping integration with gig economy platforms, with the aim that users of those platforms could ultimately opt to tip a worker and route that money directly toward paying down that person’s student loan debt.

Curry says the team at College Cash has been working with a “national gig economy platform” to run a pilot of the integration and has run focus groups showing that users are more likely to tip when they know that money goes toward erasing loan debt.

Powered by WPeMatico

Shell’s plan to roll out 500,000 electric charging stations in just four years is the latest sign of an EV charging infrastructure boom that has prompted investors to pour cash into the industry and inspired a few companies to become public companies in search of the capital needed to meet demand.

Since the beginning of the year, three companies have been acquired by special purpose acquisition vehicles and are on a path to go public, while a third has raised tens of millions from some of the biggest names in private equity investing for its own path to commercial viability.

The SPAC attack began in September when an electric vehicle charging network ChargePoint struck a deal to merge with special purpose acquisition company Switchback Energy Acquisition Corporation, with a market valuation of $2.4 billion. The company’s public listing will debut February 16 on the New York Stock Exchange.

In January, EVgo, an owner and operator of electric vehicle charging infrastructure, agreed to merge with the SPAC Climate Change Crisis Real Impact I Acquisition for a valuation of $2.6 billion — a huge win for the company’s privately held owner, the power development and investment company LS Power. LS Power and EVgo management, which today own 100% of the company, will be rolling all of its equity into the transaction. Once the transaction closes in the second quarter, LS Power and EVgo will hold a 74% stake in the newly combined company.

One more deal soon followed. Volta Industries agreed to merge this month with Tortoise Acquisition II, a tie-up that would give the charging company named after battery inventor Alessandro Volta a $1.4 billion valuation. The deal sent shares of the SPAC company, trading under the ticker SNPR, rocketing up 31.9% in trading earlier this week to $17.01. The stock is currently trading around $15 per share.

Not to be outdone, private equity firms are also getting into the game. Riverstone Holdings, one of the biggest names in private equity energy investment, placed its own bet on the charging space with an investment in FreeWire. That company raised $50 million in a new round of funding earlier this year.

“The writing is on the wall and the investors have to take the time. There’s been a flight out of the traditional investment opportunities in markets,” said FreeWire chief executive Arcady Sosinov, in an interview. “There’s been a flight out of the oil and gas companies and out of the traditional utilities. You have to look at other opportunities… This is going to be the largest growth opportunity of the next 10 years.”

FreeWire deploys its infrastructure with BP currently, but the company’s charging technology can be rolled out to fast food companies, post offices, grocery stores or anywhere people go and spend somewhere between 20 minutes and an hour. With the Biden administration’s plan to boost EV adoption in federal fleets, post offices actually represent another big opportunity for charging networks, Sosinov said.

“One of the reasons we find electrification of mobility so attractive is because it’s not if or how, it’s when,” said Robert Tichio, a partner at Riverstone in charge of the firm’s ESG efforts. “Penetration rates are incredibly low… compare that to Norway or Northern Europe. They have already achieved double-digit percentages.”

A recent Super Bowl commercial from GM featuring Will Farrell showed just how far ahead Norway is when it comes to electric vehicle adoption.

“The demands on capital in the electrification of transport will begin to approach three quarters of a trillion annually,” Tichio said. “The short answer to your question is that the needs for capital now that we have collectively, politically, socially economically come to a consensus in terms of where we’re going and we couldn’t say that 18 months ago is going to be at a tipping point.”

Shell already has electric vehicle charging infrastructure that it has deployed in some markets. Back in 2019 the company acquired the Los Angeles-based company Greenlots, an EV charging developer. And earlier this year Shell made another move into electric vehicle charging with the acquisition of Ubitricity in the U.K.

“As our customers’ needs evolve, we will increasingly offer a range of alternative energy sources, supported by digital technologies, to give people choice and the flexibility, wherever they need to go and whatever they drive,” said Mark Gainsborough, executive vice president, New Energies for Shell, in a statement at the time of the Greenlots acquisition. “This latest investment in meeting the low-carbon energy needs of US drivers today is part of our wider efforts to make a better tomorrow. It is a step towards making EV charging more accessible and more attractive to utilities, businesses and communities.”

Powered by WPeMatico

Welcome to 2021, a year that could extend 2020’s startup market disruptions and excesses — or change patterns that previously performed well for early-stage tech companies and their investors.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

As we turn the page, I have a number of questions worth raising as we muck into 2021.

Each relates to a 2020 change that is expected to persist, by either the general market or those bullish on startups. I want to know what would need to change to shake up what became the new normal last year. After all, it’s precisely when it feels like nothing could shake up a downturn (or a boom) that things often do.

Today, let’s discuss seed deals, venture investing cadence, the resulting valuation pressures from rapid-fire bets, current IPO expectations and what happens to software sales when remote work begins to fade.

Today, let’s discuss seed deals, venture investing cadence, the resulting valuation pressures from rapid-fire bets, current IPO expectations and what happens to software sales when remote work begins to fade.

As 2020 came to a close, Natasha Mascarenhas and I reported on seed investing’s strong year and its especially strong second half. How long can that pace keep up?

Nearly all our questions today deal with the endurance of certain conditions, namely: how long the market can keep parts of startup land red-hot.

When it comes to seed deal-making, Q1 and Q2 2020 saw similar levels of investment in the United States. But Q3 proved explosive, with money invested into domestic seed deals rising from around $1.5 to $1.6 billion during the first two quarters to $2.2 billion in the July-September period.

Q4 numbers are yet to fully come in, but it’s clear that private investors were incredibly bullish on early-stage startups in the second half of 2020. How long can that keep up? I think the answer is for a while yet, as investors have shown scant enthusiasm for slowing down their dealmaking cadence.

While cadence remains hot generally, seed deals should stay heated as the number of investors who are willing to invest early has increased.

Which brings us to our second question:

A theme that cropped up in the second half of 2020 was the pace at which investors were conducting venture capital deals. This was for a few reasons. To start, venture capitalists have raised larger funds in recent years, meaning that they need larger returns to make the math work out. This led to many investors putting money to work in younger and younger companies, hoping to get in early on a big win. That setup led to more deal competition and faster deal-making.

How? Two things. Investors who were already on a startup’s cap table — already part-owners, in other words — led preemptive rounds, in part to get ahead of other investors who might want to poach the succeeding deal. Other investors, knowing this, seemed to do the same math and move even faster, and earlier, to get around the defense.

So how long can the trend keep up? Given that many big VC firms raised in 2020, many startups picked up some tailwinds from the COVID-19 economy and exits have been strong, forever? Until something stops things? Think of it as Newton’s First Law of startup investing.

What could be the sudden impact to shake up the current set of conditions boosting the pace at which seed and later deals occur? An asteroid strike is probably too extreme, but inertia is one hell of a drug and markets love to stay happy.

Moving along, all the competition to get money to work in hot startups now has had another effect than the mere speed of deal-making; it has also pushed prices higher.

Powered by WPeMatico

Welcome, the HR software that helps organizations make and close offers to new candidates, announced the close of a $6 million seed round today, led by FirstMark Capital. Participating investors include Ludlow Ventures, Nat Turner and Zach Weinberg, and Keenan Rice and Ben Porterfield (which were existing investors), as well as a wide array of angels.

TechCrunch last covered Welcome in August, when it announced a $1.4 million funding round. That the startup was able to raise more as quickly as it has is testament to how hot the early-stage venture capital market is today, and likely an endorsement of Welcome’s economic profile and recent growth.

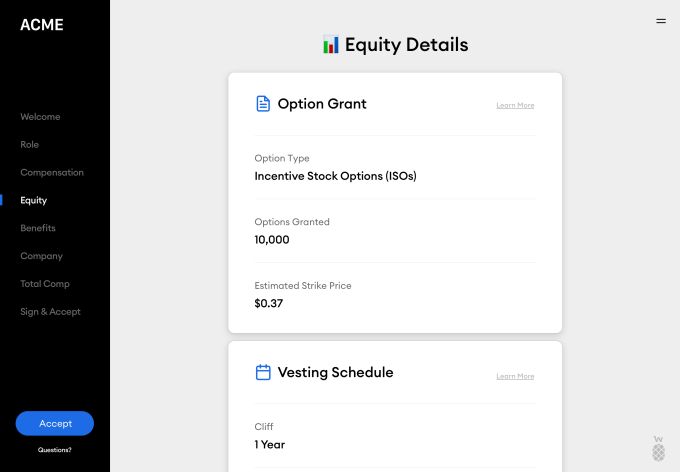

Past the new capital, Welcome is also launching a new product today called Total Rewards, which helps not just new candidates but also existing employees get a complete, easy-to-understand picture of their compensation, across salary, benefits, equity, etc.

But let’s back up.

Welcome was founded in 2019 by Nick Gavronsky and Rick Pereira, with a mission to help organizations close offers on candidates by providing a much clearer picture of compensation, particularly around equity. Co-founder and CEO Nick Gavronsky explained that many candidates don’t truly understand the value of the equity they’re offered, or how it works.

“A lot of recruiting teams aren’t well-equipped to use it as a selling tool and explain it effectively and showcase the value to candidates to help them think about their ownership at the company,” he added.

Image Credits: Welcome

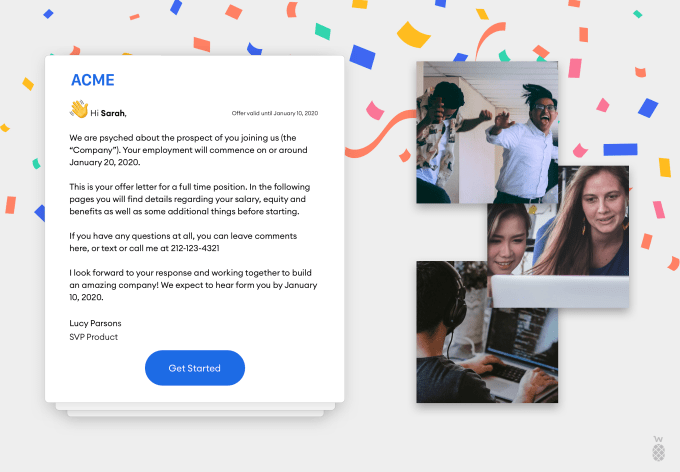

Welcome allows companies to organize their compensation offers based on level and position, and deliver that information digitally to candidates in a way that makes sense.

The startup integrates with a variety of other software providers, including Slack, Lever, Greenhouse, ADP and Justworks to name a few, simplifying onboarding for Welcome clients and bringing a broad array of information into one place.

Offers sent through Welcome show a description of the role, equity details, total compensation and even include a welcome note and video. This is in stark contrast to the black and white legal PDF often sent to candidates.

Image Credits: Welcome

The next phase for the company comes in the form of the launch of Total Rewards, which is meant to help retain existing employees, helping them understand their compensation value and their potential at the company.

“Painting a better picture becomes a pre-retention tool,” said Gavronsky. “An employee will sometimes leave thousands of dollars on the table because they don’t understand what they’re walking away from. A lot of times companies will wait until that person is going to resign. Let me now bring up all the things that are great about our company and talk through your stock options. But the decision’s already made. So we wanted something that we can kind of put in with performance reviews.”

Welcome also has plans to offer a third product pillar in the form of real-time accurate industry-wide compensation data, helping companies understand where they fit into the larger ecosystem with regards to compensation.

Thus far, Welcome has 40 companies on the platform, including Uncork and Betterment, with hundreds on the waitlist, according to the co-founders. The company plans to use the funding to build out the team and the product.

Powered by WPeMatico

Since 2007, the number of publicly listed companies in Brazil has decreased from 400 to just a little over 300.

In the past six years there were only 21 IPOs — an average of just 3.5 public exits per year; by 2019, even Iran had more listed companies than Brazil. Global capital markets are heated given pandemic stimulus packages and low interest rates worldwide, but in Brazil the boom comes with a special feature: in Q3 2020, there were 25 primary and secondary equity offerings, and this year is on track to be the most active in history both in number of deals and dollar volume.

The most important event, however, is not necessarily the reversal of a shrinking public market but the fact that startups are issuing stocks for the first time, a dramatic change for a market previously dominated by industries like commodities and utilities.

Not only is Brazil’s IPO market roaring, the waitlist is even more impressive: More than 47 companies have filed at CVM (equivalent to the the Securities and Exchange Commission) to issue equity and are waiting for approval. In other words, the IPO is equivalent to more than 15% of the number of publicly listed companies. In the first half of October, six companies were approved to issue equity. Obviously construction and retail names are still predominant as they take advantage of the lower rates, but the main novelty are new entrants in internet and technology.

In the past decade, there were 56 IPOs in Brazil and only two were in the software space, both in 2013. That is a reflection of the profile of the investors who dominate local markets, which are used to allocating assets to companies in sectors like oil, paper and cellulose, mining or utilities. Historically, publicly listed companies in the country were value plays, as few of them had significant exposure to the domestic market and derived a significant share of revenue from commodities and exports.

As a result, companies that focused on the domestic market or on growth were never quite embraced by local investors. Many investors deploying capital in Brazil were mostly foreign and very risk-averse to the dynamics of the domestic market; in 2007, when Brazil went through a similar IPO boom, 70 percent of the demand for equity offerings came from foreign investors.

Along with an undervalued currency, growth companies struggled to find attractive valuations on the local exchange. As a result, growth companies such as Stone Payments, Netshoes, PagSeguro, Arco Educação and XP Investimentos did their IPOs in New York where they attained higher valuations. It’s ironic that there were three times more IPOs of Brazilian growth companies in the U.S. in the past five years than there were in the domestic market in the last decade.

Powered by WPeMatico

When you’re running your own venture — especially if it’s your first — it’s unlikely you will find the time to deep dive into how venture capital firms work. Fundraising is distracting for founders and can even hurt their company in the early days. But if you only start learning about VCs when you’re already down the fundraising path, you’ll already be too late.

Founders tend to make a series of classic mistakes when raising funding. Error number one (and two) is to raise the wrong amount of money and to do it at the wrong time. This double whammy results in founders being very diluted too early or not raising enough money to reach the next funding stage.

They can also put all their eggs in one basket too early. I made that mistake. I had signed a term-sheet (a nonbinding agreement) for a €2.5 million Series A round, passed the due diligence process, and the investment committee had approved the deal. But at the very last minute, a claim from one of the angels on my cap table made the prospect investor change his mind. In a Point Nine Capital survey, founders said that the two most stressful elements of raising venture capital are not knowing where in the fundraising process they are and not understanding why VCs have rejected their proposal.

On the other hand, if you know what VCs all about, you’ll be geared up for the ride, know the kind of investor personality you’re aiming for, and crucially — you’ll optimize the value of your equity in the long run. Founders who manage to raise more VC funds end up having a greater value stake in their company when the time comes to IPO, according to statistical research. The learning curve is steep; you’re not just studying VC as an industry, but the individual investors themselves. So, I’ve decided to share the main lessons about VC that I wish I’d known when I was a startup founder chasing venture capital.

Startups are all about reaching two milestones: (a) product/market fit and (b) a profitable, repeatable and scalable growth model. Once those two corners are turned, the risk of a startup decreases enormously, which is normally reflected in the valuation. As an early-stage founder, if you want to protect your ownership, make sure you’re raising small amounts of money while your valuations are low.

Save your cash until you de-risk your early-stage startup. Then, raise aggressively when you finally have hard evidence that you have a strong product/market fit and a clear growth model. Be sure you understand when your company reaches that stage and becomes a scaleup. You don’t want to be a founder that has successfully raised a Series A round but has very little ownership and a very long road ahead.

Sometimes, the timing is out of your hands. The price of equity in startups is governed by the supply and demand of capital. Investors themselves have to raise money from another type of investor called Limited Partners (LPs), who may hold stakes in a variety of assets. If LPs have a strong interest in VC assets, there is more supply of capital and the price of startup equity will rise. But the opposite is also true. If you take a look at the last two recessions in the United States (2000 and 2008), you will see that the stock market crash coincided with corrections to valuations in the VC market.

So, be strategic and raise when “the market” has a strong appetite for your equity; otherwise, stretch your runway and wait for the right time. Right now, it’s common to see startups postponing their next raise to 2021, looking for stronger winds.

I see two conditions for startups to raise a large round: (a) a large market that can justify a sizable exit, and (b) a large VC fund (small funds don’t need super sizable exits to be successful).

Assuming the first condition is met, where can we find those large VC funds? Typically, they’ll be in locations close to large markets, with a track record of sizable exits.

Powered by WPeMatico

Year-in, year-out, the gender gap in venture capital investment continues to be a problem women founders face. While the gender gap in other areas (such as the number of women entering tech in general) may be on the right path, this disparity in funding seems to be stagnant. There has been little movement in the amount of VC dollars going to women-founded companies since 2012.

In fintech, the problem is especially prominent: Women-founded fintechs have raised a meager 1% of total fintech investment in the last 10 years. This should come as no surprise, given that fintech combines two sectors traditionally dominated by men: finance and technology. Though by no means does this mean that women aren’t doing incredible work in the field and it’s only right that women founders receive their fair share of VC investment.

In the short term, women founders can take action to boost their chances at VC success in the current investment climate, including leveraging their community and support network and building the necessary self-belief to thrive. In the long term, there needs to be foundational change to level the playing field for women entrepreneurs. VC funds must look at ways they can bring in more women decision-makers, all the way up to the top.

Let’s dive into the state of gender bias in VC investing as it stands, and what founders, stakeholders and funds themselves can do to close the gap.

In 2019, less than 3% of all VC investment went to women-led companies, and only one-fifth of U.S. VC went to startups with at least one woman on the founder team. The average deal size for female-founded or female co-founded companies is less than half that of only male-founded startups. This is especially concerning when you consider that women make up a much bigger portion of the founder community than proportionately receive investment (around 28% of founders are women). Add in the intersection of race and ethnicity, and the figures become bleaker: Black women founders received 0.6% of the funding raised since 2009, while Latinx female founders saw only 0.4% of total investment dollars.

The statistics paint a stark picture, but it’s a disparity that I’ve faced on a personal level too. I have been faced with VC investors who ask my co-founder — in front of me — why I was doing the talking instead of him. On another occasion, a potential investor asked my co-founder who he was getting into business with, because “he needed to know who he’d be going to the bar with when the day was up.”

This demonstrates a clear expectation on the part of VC investors to have a male counterpart within the founding team of their portfolio companies, and that they often — whether subconsciously or consciously — value men’s input over that of the women on the leadership team.

So, if you’re a female founder faced with the prospect of pitching to VCs — what steps can you take to set yourself up for success?

Women founders looking to receive VC investment can take a number of steps to increase their chances in this seemingly hostile environment. My first piece of advice is to leverage your own community and support network, especially any mentors and role models you may have, to introduce you to potential investors. Contacts that know and trust your business may be willing to help — any potential VC is much more likely to pay you attention if you come as a personal recommendation.

If you feel like you’re lacking in a strong support network, you can seek out female-founder and startup groups and start to build your community. For example, The Next Women is a global network of women leaders from progress-driven companies, while Women Tech Founders is a grassroots organization on a mission to connect and support women in technology.

Confidence is key when it comes to fundraising. It’s essential to make sure your sales, pitch and negotiation skills are on point. If you feel like you need some extra training in this area, seek out workshops or mentorship opportunities to make sure you have these skills down before you pitch for funding.

When talking with top male VCs and executives, there may be moments where you feel like they’re responding to you differently because of your gender. In these moments, channeling your self-belief and inner strength is vital: The only way that they’re going to see you as a promising, credible founder is if you believe you are one too.

At the end of the day, women founders must also realize that we are the first generation of our gender playing the VC game — and there’s something exciting about that, no matter how challenging it may be. Even when faced with unconscious bias, it’s vital to remember that the process is a learning curve, and those that come after us won’t succeed if we simply hand the task over to our male co-founder(s).

While there are actions that women can take on an individual level, barriers cannot be overcome without change within the VC firms themselves. One of the biggest reasons why women receive less VC investment than men is that so few of them make up decision-makers in VC funds.

A study by Harvard Business Review concluded that investors often make investment decisions based on gender and ask women founders different questions than their male counterparts. There are countless stories of women not being taken seriously by male investors, and subsequently not being seen as a worthwhile investment opportunity. As a result of this disparity in VC leadership teams, women-focused funds are emerging as a way to bridge the funding gender gap. It’s also worth noting that women VCs are not only more likely to invest in women-founded companies, but also those founded by Black entrepreneurs. In addition to embracing women and minority-focused investors, the VC community as a whole should ensure they’re bringing in more women leaders into top positions.

From day one, the Prometeo team has made concerted efforts to have both men and women in decision-maker roles. Having women in the founding team and in leadership positions has been crucial in not only helping to fight the unconscious bias that might take place, but also in creating a more dynamic work environment, where diversity of thought powers better business decisions.

Striving for gender equality, both within the walls of VC funds and in the founder community, is also better for businesses’ bottom line. In fact, a study by Boston Consulting Group found that women-founded startups generate 78% for every dollar invested, compared to 31% from men-founded companies.

Here in Latin America, women founders receive a higher proportion of VC investment than anywhere else in the world, so it’s no surprise that women are leading the region’s fintech revolution. Having more women in leadership positions is ultimately a better bet for business.

Closing the gender gap in VC funding is no simple task, but it’s one that must be undertaken. With the help of internal VC reform and external initiatives like community building, training opportunities and women-focused support networks, we can work toward finally making the VC game more equitable for all.

Powered by WPeMatico

According to industry reports, venture capital deal-making has notably rebounded since dropping off briefly in March as shelter-in-place orders gripped much of the country.

As seed-stage fintech investors, this has certainly been our experience: “Hot” deals are getting funded faster than ever, and we increasingly see the large multistage global funds competing for the earliest access to companies. However, in our experience and anecdotal conversations with other early-stage investors, that excitement has not been translating to the Series A stage.

We’ve increasingly wondered if the Series A market in fintech is really as hot as it seems. As pre-seed and seed-stage investors, we know that the health of the Series A market is of critical importance.

In early October 2020, the Financial Venture Studio put together a brief survey of the Series A market in fintech and shared it with more than 100 investors with whom we work closely. Despite the high-level numbers indicating a healthy market, our research indicates a market that remains in flux, with significant ramifications for early-stage founders.

Although the seed and pre-seed fintech market continues to attract substantial entrepreneurial and investor interest, it is also in some ways one of the easiest parts of the market to fund. The check size is smaller, the velocity of new deals is highest, and while the potential returns are also the highest, this is also the part of the market where information is most scarce. Perhaps counterintuitively, the fact that there is so little information on a business — aside from a plan, a team and maybe some early anecdotal evidence to support the vision — actually makes it easier to “pull the trigger” on deals where those data points align. There just often isn’t a lot more to dig into.

Similarly, by the time a company is raising Series B capital, they typically have some objective evidence that the idea is working. Companies are typically generating revenue, small teams have grown and become more sophisticated in how they operate, and importantly, the governance functions of a company have (hopefully) begun to take shape. The simple existence of a board member with invested capital at stake means that some of the more existential risks of the earliest stage have been mitigated.

In contrast, one of the big milestones for any startup has been to raise a Series A from an institutional investor. Besides an infusion of capital (which is often 2-3x the aggregate capital a company may have raised since its inception), this “stamp of approval” lends credibility to a small company that is trying to hire talent, sell to customers, and, in most cases, raise substantial subsequent capital.

Thus, it’s critical that Series A investors remain active; if not, many of these upstart companies may fail due to a lack of investment, even if they are able to demonstrate early market traction. The Series A funding market is one of — if not the most — critical funding stage in the innovation economy because it acts as a bridge between scrappy early innovation and commercialization at scale.

It stands to reason, then, that dollar amounts invested may not be the best barometer of the ecosystem’s health. What really matters is the volume of companies being funded and the variety of product approaches being pursued.

Once the initial shock of the pandemic wore off, the VC community had to get back to business, which admittedly is harder to do for funds that write $10 million+ checks and like getting to know founders in person. Still, Series A investors made it a point to let entrepreneurs know they were, and continue to be, “open for business.”

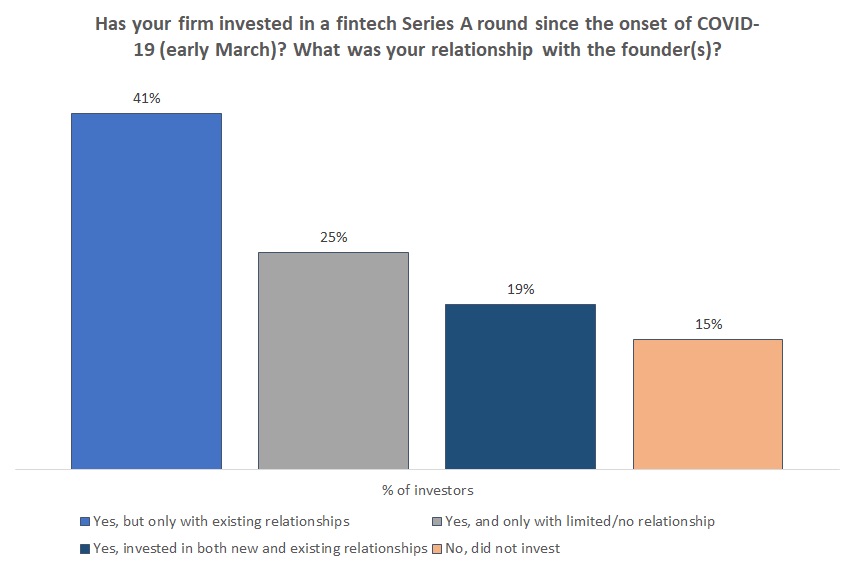

As investors have gotten more comfortable with the new normal, they have been more open to a virtual diligence process. Of the firms we surveyed, only 15% stated they have not completed a Series A investment during COVID-19 work restrictions. Of the firms who completed a Series A investment during COVID-19 (~85%), about half invested in a company whose founder(s) they had a limited or no relationship with prior to the onset of shelter-in-place orders.

Image Credits: Financial Venture Studio (opens in a new window)

The shift to a virtual environment means that process is more important than ever. Numerous investors have cited their renewed focus on following a structured approach to sourcing and diligence. The interpersonal aspect remains important to close a deal, but customer references, referrals from trusted seed-stage investors and a heightened scrutiny of metrics are all at the forefront of investors’ evaluations.

Powered by WPeMatico

Yaw Aning named Malomo, the service he launched for small businesses to turn their order-tracking services into branded customer experiences, as a tribute to his mother, who was a small business owner herself.

“Malomo” means flowers in Swahili and it was the name of Aning’s mother’s small soap-making business which she built over the years — even as she was battling the cancer to which she would eventually succumb.

The small Indianapolis startup has just raised $2.8 million to expand its services providing a new marketing channel for the Shopify retailers of the world who can always use more ways to reach new customers, Aning said.

The financing came from the San Francisco-based firm, Base 10, and New York’s Harlem Capital, along with commitments from previous investors Hyde Park and High Alpha.

Aning came to entrepreneurship as an Orr Fellow, an Indiana program that takes 10 graduates and places them in high-growth companies. While Aning worked in corporate finance, he was always interested in the startup world, and started is first company, Pocket Tales, an online reading game for children.

That business was followed by Sticks and Leaves, a web design agency that gave Aning his first view into the opportunity that order tracking presented as a space for a better customer experience.

Along with co-founder Anthony Smith, Aning built a service that connects with a single click to the Shopify platform and creates custom, branded tracking pages for each brand. “It’s a landing page for a brand. They use it like they would use any marketing asset,” Aning said. “The strategy is to build up integrations to the other tools merchants use to create rich experiences leveraging those tools.”

Powered by WPeMatico

Marco Financial, a new Miami-based startup, is looking to take a piece of the roughly $350 billion trade finance market for Latin American exporters with its novel factoring services business.

Small and medium-sized businesses in Latin America can have trouble getting the financing they need to launch export operations to the U.S. and Marco said it aims to bridge that gap with new risk modeling and management tools that can make better decisions on who should receive loans.

“For smaller businesses in Latin America, accessing trade finance to export their goods is a major concern and a top reason why many don’t succeed,” said Javier Urrutia, director of Foreign Investments at PROCOLOMBIA, an organization that promotes foreign investment and non-traditional exports in Colombia, in a statement from the company. “In Colombia alone, a 1% increase in exporter productivity in our textile industry would result in 500,000 new jobs for the country.”

The company is backed by a small seed round from Struck Capital and Antler and over $20 million in a credit facility underwritten by Arcadia Funds.

“As a former owner of a small business in Latin America, I saw firsthand how difficult it is for SMEs in this region to access trade financing that will let them export their goods while retaining enough capital to keep their business running,” said Peter D. Spradling, COO and co-founder of Marco, in a statement. “Access to trade finance is one of the greatest hurdles in business operations and the traditional system dominated by banks is simply not working anymore, disproportionately hurting SMEs and further restricting economic mobility and job creation in emerging markets. Equity funding and a material credit facility let us serve this underserved market in Latin America and help build a healthier, more equitable trade ecosystem reflective of an increasingly borderless global economy.”

Spradling met his co-founder Jacob Shoihet through the Antler accelerator, a Singapore and New York-based early-stage investment and advisory services program that connects entrepreneurs and tech operators to launch new businesses.

Shoihet, a classically trained musician who fell in with the startup scene in New York through work at Yelp, was eager to launch his own company and connected with Spradling over shared interests in intermittent fasting and sports.

Small and medium businesses have a hard time receiving loans from traditional lenders thanks to tighter regulations and capital controls dating back to the 2008 financial crisis, according to Marco’s founders. And the long periods that companies have to wait between when goods are shipped and orders are payed can put undue pressure on business operations. Factoring solves the gap by lending to merchants based on their receivables.

Marco said that it can reduce the length of the loan origination process from over two months to one week and provide funding to approved exporters within 24 hours.

The company is initially focused on Mexico, Uruguay, Chile, Colombia and Peru, and chose those markets because of Spradling’s previous experience as an importer and exporter across the region.

“We look for companies that not only target massive, sleepy industries but also for ones that are led by management teams with fresh perspectives and asymmetric information that position them to upend incumbents,” said Yida Gao, partner at Struck Capital, in a statement. “In short order, Marco has assembled a world-class team to tackle the multi trillion-dollar trade finance market in a post-Covid time when SMEs around the world need, more than ever, reliable capital to fund operations and growth. We are excited to be part of Marco’s journey to support the suppliers that are the backbone of global trade.”

Powered by WPeMatico

{kind=link}