corporate finance

Auto Added by WPeMatico

Auto Added by WPeMatico

Startups are raising record sums around the world, thanks to several contributing factors. As The Exchange explored yesterday, historically low interest rates have helped venture capitalists raise more capital than ever, to pick an example.

Low rates have helped startups in another manner: As yields fell for certain assets, investors chased returns by betting on growth. And in recent years, the investing classes turned their attention to public software companies, bidding up the value of their revenue to record highs.

This raised the worth of startups in general terms, and private tech companies’ comps enjoyed a steady, upward climb in the value of their revenues. If the value of a dollar of SaaS revenue was worth $1 one year and $2 the next, the repricing was good for private companies even if we were tracking the metrics from the perspective of public companies.

The free ride could be ending.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

I’ve held back from covering the value of software (SaaS, largely) revenues for a few months after spending a bit too much time on it in preceding quarters — when VCs begin to point out that you could just swap out numbers quarter to quarter and write the same post, it’s time for a break. But the value of software revenues posted a simply incredible run, and I can’t say “no” to a chart.

The pace at which software revenues were repriced upwards in the last few years is simply astounding. Per the Bessemer Cloud Index, back in 2016, the median revenue multiple for public SaaS companies was around 5x. When 2018 began, median SaaS multiples had expanded to around 7x.

The pace at which software revenues were repriced upwards in the last few years is simply astounding. Per the Bessemer Cloud Index, back in 2016, the median revenue multiple for public SaaS companies was around 5x. When 2018 began, median SaaS multiples had expanded to around 7x.

That’s a 40% climb in pricing, but it proved to be just a foretaste of the feast to come.

By the end of 2019, the median figure had appreciated to around the 9x mark. And today it has shot to just under 18x. That is why software companies have been able to raise so much money, earlier, and in larger chunks. Every dollar of recurring revenue they sold was worth $5 in market cap in mid-2016. At the end of 2019, that same dollar of revenue was worth $9. And today, for the median public software company, it’s valued at around $18.

There are nuances to the data, but we care less about exacting definitions than the directional change it describes: The median value of SaaS revenues more than tripled from 2016 to 2021. That’s an insane amount of growth.

Powered by WPeMatico

As a startup founder, there will be three scenarios in which you’ll need to understand how to properly do a quality of earnings (QofE) if you want to maximize value.

The first scenario will be when you decide to raise a Series A and subsequent VC rounds, followed by when you do a strategic acquisition, and lastly, when you sell your company.

This post is a framework for how to think and organize your QofE and go through the most common items that you’ll want to keep top of mind for every M&A and private equity transaction you may be part of.

The goal of a QofE is to adjust the reported EBITDA to calculate a restated EBITDA that best reflects the current state of the company on an ongoing basis. It also presents a historical adjusted EBITDA that is comparable throughout the last two or three years.

QofE can have a significant impact on a company valuation for three main reasons:

With that in mind, every entrepreneur must understand how to properly form a view of what is the proper adjusted EBITDA and adjusted revenue of your company. It is common for founders in an M&A process to be unfamiliar with the notion of QofE and leave value on the table.

When performed by a professional transaction service advisory team, the quality of earnings is a result of a thorough review of all the documents generally available in a data room.

This breakdown aims to ensure that you won’t be that founder and that you’ll be armed to negotiate your company valuation on equal ground with your investors. If you are in the seller’s shoes, you will get the advantage of understanding how an experienced investor or buyer thinks. If you’re in the buyer’s shoes, you’ll benefit from understanding and valuing your acquisitions better.

When performed by a professional transaction service advisory team, the quality of earnings is a result of a thorough review of all the documents generally available in a data room. These include, but are not limited to: Legal documentation, financial statements (P&L, balance sheet, cash flow), audit reports, management presentation and contracts.

When doing a QofE analysis, it’s key to consistently ask yourself: “Can or should this information translate into an adjustment of revenue or EBITDA, net working capital (NWC) or net debt?”

Why did we include NWC and net debt? That is because they often have an indirect impact on adjusted EBITDA. Think of an adjustment to the historical level of inventory. Less inventory likely means fewer storage costs. So if you adjust historical inventory, you’ll want to also impact your adjusted EBITDA.

On top of reviewing all the aforementioned documents, your QofE analysis will heavily rely on interviewing management. No matter how long you look at the financials, if you can’t have management confirm information or explain trends, you won’t be able to draw proper conclusions and understand the numbers.

Powered by WPeMatico

On Tuesday, the Open Cap Table Coalition announced its launch through an inaugural Medium post. The goal of this project is to standardize startup capitalization table data as well as make it far more accessible, transparent and portable.

For those unfamiliar with a cap table, it’s a list of who owns your company’s securities, which includes your company shares, options and more. A clear and simple cap table should quickly indicate who owns what and how much of it they own. For a variety of reasons (sometimes inexperience or bad advice) too many equity holders often find companies’ capitalization information to be opaque and not easily accessible.

This is particularly important for the small percentage of startups that survive in the long term, as growth makes for far more complicated cap tables.

A critical part of good startup hygiene is to always have a clean and updated cap table. Since there is no set format and cap tables are generally not out in the open, they are often siloed rather than collaborative.

Cap tables are near and dear to me as someone who has advised hundreds of startups over the past two decades as the founder of an accelerator, a venture partner and a senior adviser at a government-funded startup launchpad. I have been on the shareholder side of the equation as well and can assure you that pretty much nothing destroys trust between shareholders and startups quicker than poor communication, especially around issues such as the current status of the cap table.

A critical part of good startup hygiene is to always have a clean and updated cap table.

I really like the idea of a cap table being an open corporate record, because the value proposition to the companies is clear. From the time a startup creates a cap table, it’s prone to inaccuracy, friction and mistakes. What this means in practice is that startups may spend money on cap-table-related issues that they should be spending on other things. From a legal process perspective, the law firm that is brought in to help with these issues has to deal with tedious back-end work, so the legal time isn’t high value for either the startup or the law firm.

The value proposition for equity holders is equally clear. All equity holders have a general and legal interest in a company’s capitalization information. They have the right to this information, which they may need for a variety of reasons (including, if things ever get really bad, an aggrieved shareholder action). So making this information clear and easily accessible is a service to equity holders and can also encourage more investment, especially from less experienced investors.

When I imagine what this project could become in the next couple of years, I think back to late 2013, when Y Combinator announced the SAFE (simple agreement for future equity). I think the SAFE is a good analogy here, as no one knew what it was and people wondered if this was a nice-to-have rather than a must-have for startups. But the end result was a dramatic improvement in the early-stage capital-raising process.

While the coalition’s founders include Morgan Stanley’s Shareworks, LTSE Software and Carta, it’s also heavy on Big Law, with Cooley, Goodwin Procter, Wilson Sonsini Goodrich & Rosati, Orrick, Gunderson Dettmer, Latham & Watkins, and Fenwick & West rounding out the group of 10 founding members.

So what’s the real motivation of seven law firms, which together saw revenue of over $10 billion in 2020 to collaborate on an open cap table product for startups? Deal flow.

Big Law has been trying for a couple of decades to build relationships with startups at the stage where it makes no sense for a startup to be dealing with a massive and expensive law firm. Their efforts to build startup programs have often fallen short and received mixed reviews. They have also been far too heavy on the self-serve and too light on the “we’re going to give you our regular Big Law level of services at a small fraction of the costs just in case you make it big and can one day pay our regular fees.” So these firms are trying to separate themselves from the rest of the Big Law pack by building this entrepreneur-friendly tech.

The coalition has already produced its initial version of the open cap table. The real question is whether this is going to be a big deal, as the SAFE was, or whether it’s going to be a vanity solution in search of a real problem. My best guess is that if this coalition gets all the relationships right, doesn’t get greedy and understands that there is a social good component at play here, this could be, reasonably quickly, as impactful as the SAFE was.

Powered by WPeMatico

Meetings should have a clear purpose, but instead, they’ve become a way to measure status and reinforce what is colloquially referred to as CYA culture.

There’s a kernel of truth in every joke, so whenever someone quips, “This meeting could have been an email!” you can bet that some small part of them meant it sincerely.

Few people know how to run meetings effectively and keep conversations on track. Making matters worse, attendees often don’t bother to prepare, which makes a boring session even less productive.

And then there’s the complication of workplace politics: How secure do you feel declining an invitation from a co-worker — or a manager?

“Every time a recurring meeting is added to a calendar, a kitten dies,” says Chuck Phillips, co-founder of MeetWell. “Very few employees decline meetings, even when it’s obvious that the meeting is going to be a doozy.”

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Changing your meeting culture is difficult, but given that 26% of workers plan to look for a new job when the pandemic ends, startups need to do all they can to retain talent.

Aimed at managers, this post offers several testable strategies that will help you boost productivity and say goodbye to poorly run, lazily planned meetings.

“Declining a bad meeting should never be taboo, and you should reiterate your trust in the team and challenge them to spend their and others’ time with more intention,” Phillips says. “Help them feel empowered to decline a bad meeting.”

Thanks very much for reading Extra Crunch, and have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Shein

In the last year, online apparel shopping app Shein grew active daily users by 130%, reports Apptopia.

Each day, thousands of new products arrive on the app’s virtual shelves. Items are rapidly designed and prototyped before Shein’s contractors put them into production in Guangzhou factories — two weeks later, those SKUs arrive in fulfillment centers around the globe.

TechCrunch reporter Rita Liao examined how the company’s agile supply chain has become hot talk among e-commerce experts, but beyond a strong logistics game and data-driven product development, Shein’s close relationships with suppliers are integral to its success.

She also tried to answer a question many are asking: Is Shein a Chinese company?

“It’s hard to pin down where Shein is from,” answered Richard Xu from Grand View Capital, a Chinese venture capital firm.

“It’s a company with operations and supply chains in China targeting the global market, with nearly no business in China.”

Image Credits: Chevrolet

GM Vice President of Innovation Pam Fletcher is in charge of the company’s startups that tackle “electrification, connectivity and even insurance — all part of the automaker’s aim to find value (and profits) beyond its traditional business of making, selling and financing vehicles,” Kirsten Korosec writes.

Fletcher joined TechCrunch at a virtual TC Sessions: Mobility 2021 event to discuss what it’s like to launch a slew of startups under the umbrella of a 113-year-old automaker.

Image Credits: MaC Venture Capital / Wonderschool

MaC Venture Capital founding managing partner Marlon Nichols and Wonderschool CEO Chris Bennett joined Extra Crunch Live to tear down the company’s early deck.

“The first thing that jumped out at all of us was just how bare-bones the presentation is: white text on a blue background, largely made up of bullet points,” Brian Heater writes before noting the CEO admitted that “not much changed aesthetically between that first pitch and the Series A deck.”

“It aligned with what we were valuing at the time,” Bennett says. “We were really focused on getting the product-market fit and really trying to understand what our customers needed. And we’re really focused on building the team.”

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

I’ve been working on an H-1B in the U.S. for nearly two years.

While I’m grateful to have made it through the H-1B lottery and to be working, I’m feeling unhappy and frustrated with my job.

I really want to start something of my own and work on my own terms in the United States. Are there any immigration options that would allow me to do that?

— Seeking Satisfaction

Image Credits: Nigel Sussman (opens in a new window)

Alex Wilhelm calls SentinelOne’s looming debut “fascinating.”

“Why? Because the company sports a combination of rapid growth and expanding losses that make it a good heat check for the IPO market,” he writes. “Its debut will allow us to answer whether public investors still value growth above all else.”

Alex delves into an early dataset from SentinelOne and why public market investors still appear to value growth above anything else.

Image Credits: Jenny Dettrick (opens in a new window) / Getty Images

Guest columnist Rob Hudock, a litigator who focuses on helping companies recruit the best talent available while avoiding distracting workplace issues or lawsuits, lays out the importance of putting out any employment-related fires before an exit.

“Inattention to employment issues can have a significant impact on deals — from preventing closings and reducing the deal value to altering the deal terms or significantly limiting the pool of potential buyers,” he writes.

“Fortunately, such issues typically can be resolved well in advance with a little forethought and legal guidance.”

Image Credits: John M Lund Photography Inc (opens in a new window) / Getty Images

Building an excellent product and a standout company culture require the same process, Heap CEO Ken Fine writes in a guest column.

“At Heap, the analytics solution provider I lead, a defining principle is that good ideas should not be lost to top-down dictates and overrigid hierarchies,” he writes. “The best results come when you approach leadership like you would create a great product — you hypothesize, you test and iterate, and once you get it right, you grow it.”

Here, he lays out his method that argues in favor of iterative change, not “one-and-done decrees.”

Image Credits: Nigel Sussman (opens in a new window)

The big news on Thursday was the announcement of Andreessen Horowitz’s new cryptocurrency-focused fund. Most focused on the eye-popping $2.2 billion figure, but Alex Wilhelm dug a bit deeper into the announcement to note that a16z isn’t just pumping a ton of money into the crypto space, it’s putting on gloves to fight for it.

Alex writes that “a16z intends to run defense for crypto in the American, and perhaps global, market. Crypto-focused startups are likely unable to tackle the regulation of their market on their own because they’re more focused on product work in a particular region of the larger crypto economy. The wealthy and connected investment firm that backs them will take on the task for its chosen champions.”

Image Credits: Nicholas Kamm / AFP / Getty Images

Alex Wilhelm dives headfirst into BuzzFeed’s announcement that it plans to go public via a blank check company.

He looked at its historical and anticipated revenue growth (the latter is very sunny, which is not atypical for SPAC presentations), what makes up that revenue (more “commerce” as time goes on), its long-term profitability projections, as well as fun stuff, like the Pulitzer Prize-winning BuzzFeed News.

Admit it. You’re curious.

Image Credits: SaskiaAcht (opens in a new window) / Getty Images

Moving from a pay-as-you-go model to a subscription service is more than just putting a monthly or yearly price tag on a product, CloudBlue’s Jess Warrington writes in a guest column.

“Executives cannot just layer a subscription model on top of an existing business,” Warrington writes. “They need to change the entire operation process, onboard all stakeholders, recalibrate their strategy and create a subscription culture.”

Warrington says that in his role at CloudBlue, companies often approach him for “help with solving technology challenges while shifting to a subscription business model, only to realize that they have not taken crucial organizational steps necessary to ensure a successful transition.”

Here’s how to avoid that situation.

Image Credits: Bryce Durbin

Rebecca Bellan interviewed Veo CEO Candice Xie about the micromobility startup’s “old-fashioned way” of doing business.

“I understand people are eager to prove their unit economics, their scalability and also improve their matrix to the VC to raise another round,” Xie says. “I would say that’s OK in the consumer industry, like consumer electronics or SaaS.

“But we are in transportation. It is a different business, and transportation takes years of collaboration and building between private and public partners. … So I don’t see it happening from day one, turning over a billion-dollar company, while simultaneously having it all make sense for the cities and users.”

Image Credits: jayk7 (opens in a new window) / Getty Images

All companies want more or less the same thing: growth. But how do you accomplish it?

Ideally, don’t start from scratch.

The race to grow faster is more pressing than ever before. … “[F]orward-thinking entrepreneurs and growth marketers simply must make time to study their competition, learn best practices and apply them to their own business growth,” Mark Spera, the head of growth marketing at Minted, writes in a guest column.

“Of course, you should still run your own experiments, but it’s just more capital-efficient to emulate than to trial-and-error from scratch. Here are five companies with growth strategies worth emulating — including the most important lessons you can begin applying to your business today.”

Image Credits: ChrisChrisW (opens in a new window) / Getty Images

With more than 50 million Americans suffering from chronic pain and musculoskeletal (MSK) medical problems, a number of startups are offering patients new products “that don’t resemble the cookie-cutter status quo,” reports Natasha Mascarenhas.

Startups hoping to enter this space have an uphill climb. Setting aside regulations that cover aspects like product packaging and marketing, they must compete with well-entrenched competition from Big Pharma as they try to partner with health insurance companies.

Natasha profiles three companies that are each taking a different approach to personalized health: Clear, Hinge Health and PeerWell.

Image Credits: Nigel Sussman (opens in a new window)

In the second part of an Exchange series looking at the global early-stage venture capital market, Alex Wilhelm and Anna Heim unpacked the scene in Latin America, discovering it looked a lot like the situation in the United States: slow Series A rounds, fast B rounds.

“Mega-rounds are no longer an exception in Latin America; in fact, they have become a trend, with ever-larger rounds being announced over the last few months,” they write.

Despite that, the funds aren’t being equitably distributed, and the region still lags behind its peers: Brazil has the most $1 billion startups in Latin America, with 12. The U.S., meanwhile, has 369, and China has 159.

But the Latin American market remains hot, if not quite as scorching as the U.S. and China.

Powered by WPeMatico

Early-stage startups are increasingly looking for alternative ways to access capital, meaning not every company wants to raise money from VCs or take on debt.

In recent years, a flurry of startups have emerged to give companies other options. (Think Pipe, for example.)

And today, San Francisco-based Architect Capital is a new firm that is launching with over $100 million in funds to serve as an “asset-based lender” to “high-growth,” early-stage tech companies. Specifically, the new firm aims to provide non-dilutive or less-dilutive financing options to asset-rich fintech, e-commerce and SaaS companies in the U.S. and Latin America, but with an emphasis on the latter. The region, Architect maintains, does not have a plethora of institutional financing available against assets.

The firm is not out to replace traditional venture capital or venture debt, emphasizes founder and CEO James Sagan, but rather to offer asset-based products that will complement them.

For some context, Sagan is no stranger to the startup world, having co-founded and served as managing partner of Arc Labs, an early-stage credit fund focused on lending to technology-enabled businesses. He’s been investing in Latin America for years, and recognized the need for new forms of financing to fund “novel and underappreciated assets.”

Also, he believes the region is home to “the most prominent fintech ecosystem in the world.”

To Sagan, traditional forms of equity and debt financing in the venture world are vital for things like growing headcount, but he believes they are “not engineered to support the growth of a company’s underlying financial products.”

“VC is highly dilutive and should be used for ROI activities such as hiring engineers and building great teams,” Sagan told TechCrunch. “It’s expensive to use equity to fund assets. Equity should not be put in a loan book. We’ll fund the loan book.”

Image Credits: Architect Capital founder James Sagan / Architect Capital

Architect’s goal is to provide “tailored and less dilutive funding,” especially to companies that produce repeatable revenues, such as SaaS and subscription businesses.

Sagan said he first discovered the strategy in 2015 when he was working for a multifamily office that was lending against a bunch of traditional assets.

“A colleague and good friend of mine started a business and raised some equity and venture debt, but he couldn’t find the asset-specific financing for the receivables he was generating,” Sagan recalls. “He was lending to small businesses and needed asset-specific financing against those receivables.”

Venture debt doesn’t really work for receivables-based lending because venture debt shops typically are underwriting assets, or rather, underwriting the quality of the investors in the company, Sagan believes.

“So we really tailor our underwriting towards those assets themselves right and those assets range from unsecured consumer receivables to secure small business receivables to real estate,” he told TechCrunch. “Essentially, we’re providing an additional instrument for asset-heavy businesses that will allow them to scale in a way that venture debt will not.”

Architect’s LPs are mostly large institutions, as opposed to traditional high net worth individuals. The firm’s average check size will land at around $10 million to $15 million.

“Our portfolio allocation is more concentrated in general,” Sagan said. “We expect to grow our AUM (assets under management) pretty precipitously.”

Architect Capital has invested in six companies since inception, including PayJoy, a company that delivers consumer financing and smartphone technology to customers in emerging markets; Forum Brands, a U.S.-based e-commerce marketplace aggregator; and ADDI, a fintech that aims to give Colombian consumers access to fair and affordable credit through point-of-sale-financing that recently raised $65 million.

Powered by WPeMatico

Every company wants to be innovative, but innovation comes with its share of difficulties. One key challenge for early-stage companies that are disrupting a particular space or creating a new category is figuring out how to sell a unique product to customers who have never bought such a solution.

This is especially the case when a solution doesn’t have many reference points and its significance may not be obvious.

My view is simple — some buyers could use a walkthrough of the buying process. If you are building a singular product in a nascent market that necessitates forward-looking customers and want to drastically shorten sales cycles, I have a proposal: Create a buyer’s guide.

A buyer’s guide is essentially a prescriptive summary that provides an understandable overview of how a customer may buy your solution.

A buyer’s guide is essentially a prescriptive summary that provides an understandable overview of how a customer may buy your solution. What does your product actually do? Is it secure? How would you implement the technology? What does it replace, if anything? It should be short, simple and speak the customer’s language. It also acts as a sales-enabling tool. Sales teams, especially at smaller startups, can review the guide quarterly and analyze what is and isn’t working as the company goes to market.

Here is how to put together a buyer’s guide, including what to sort out before you type a single word.

From the start, it’s important to think about who the stakeholders are for your product’s buying cycle. One typical issue with early-stage startups is they meet with an enthusiastic buyer — a CIO, CTO or VP of product — but neglect to include the other stakeholders who should be part of the conversation. More importantly, a lot of companies don’t realize the impact of their product on a group or team that they would not typically sell to.

For example, target the security team as an early stakeholder, because they’re probably going to review your product. If the solution is focused toward, say, integration, then hone in on who would be owning the integration process on the buyer’s team.

If you’re selling a martech solution, on a business level, you have to consider a finance business partner for marketing. Think about the problems your customers face and also how others in their company relate to them.

Powered by WPeMatico

Fintech startup StudentFinance — which allows educational institutions to offer success-based financing for students — has raised a $5.3 million (€4.5 million) seed round co-led by Giant Ventures and Armilar Venture Partners. It’s now raised $6.6 million total, to date.

StudentFinance launched in Spain first, followed by Germany and Finland, with the U.K. planned this year. Existing investors Mustard Seed Maze and Seedcamp, along with Sabadell Venture Capital, also participated.

The startup, which launched at the beginning of 2020, provides the tech back end for institutions to offer flexible payment plans in the form of ISAs (income-share agreements). It also provides data intelligence on the employment market to predict job demand.

It now has 35 education providers signed up, managing over €5 million worth of ISAs. It also works with upskilling platforms including Ironhack and Le Wagon. StudentFinance’s competitors include (in the USA) Blair, Leif, Vemo Education, Chancen (Germany-based) and EdAid (U.K.-based).

As for why StudentFinance stands out from those companies, Mariano Kostelec, co-founder and CEO of StudentFinance, said: “StudentFinance is the only platform in this space providing the full end-to-end, cross-border infrastructure to deliver ISAs for students whilst helping to plug the growing skills gap. Not only do we provide the infrastructure to support the ISA financing model, but we also provide data intelligence on the employment market and a career-as-a-service platform that focuses on placing students in the right job. We are creating an equilibrium between supply and demand.”

With an ISA, students only start paying back tuition once they are employed and earning above a minimum income threshold, with payments structured as a percentage of their earnings. This makes it a “success-based model”, says StudentFinance, which shifts the risk away from the students. They are likely to be popular as workers need to reskill with the onset of digitization and the pandemic’s effects.

The startup was founded in 2019 by Kostelec, Marta Palmeiro, Sergio Pereira and Miguel Santo Amaro. Kostelec and Santo Amaro previously built Uniplaces, which raised $30 million as a student housing platform in Europe.

Cameron Mclain, managing partner of Giant Ventures, commented: “What StudentFinance has built empowers any educational institution to offer ISAs as an alternative to upfront tuition or student loans, broadening access to education and opportunity.”

Duarte Mineiro, partner at Armilar Venture Partners, commented: “StudentFinance is a great opportunity to invest in because aside from its very compelling core purpose, this is a sound business where its economics are backed by a solid proprietary software technology.”

Sia Houchangnia, partner at Seedcamp, commented: “The need for reskilling the workforce has never been as acute as it is today and we believe StudentFinance has an important role to play in tackling this societal challenge.”

Angel backers include investors, which includes: Victoria van Lennep (founder of Lendable); Martin Villig (founder of Bolt); Ed Vaizey (the U.K.’s longest-serving Culture & Digital Economy Minister); Firestartr (U.K.-based early-stage VC); Serge Chiaramonte (U.K. fintech investor); and more.

Powered by WPeMatico

A U.S./Israeli startup, Sorbet — which is tackling what companies do with the financial risks as employees accrue paid time off (PTO) — has raised $6 million in a seed funding round led by Viola Ventures, with participation by Global Founders Capital and Meron Capital.

The economics of paid time off is relatively hidden in the business world, but essentially, Sorbet takes on the burden of this PTO from employers and then allows employees to spend it. This gives the employers far more control over the whole process and the ability to forecast its impact on the business.

Sorbet says that in the U.S., employees use only 72% of PTO balances, even though it’s the most sought-after benefit. But this, effectively, comes out at 768 million unused days off a year, worth around $224 billion. This creates a difficult problem for CFOs and accountants because its creates balance sheet liabilities on the company’s books, says Sorbet. If the employee doesn’t use all of their PTO, the employer can end up owing them a lot of money, which creates a cash flow liability on the company’s books. So Sorbet buys out these PTO liabilities from employees, then loads the cash value of the PTO on prepaid credit cards for the employees.

Speaking to me on a call, CEO and co-founder Veetahl Eilat-Raichel, said: “We researched this whole idea of paid time off and found this huge, massive market failure and inefficiency around the way that PTO is constructed. It’s kind of one of those things where, on the face of it, there’s this boring bureaucratic payroll item that turns into a boring balance sheet item. But under it is a $224 billion problem for U.S. businesses… If you think about it, employers are borrowing money from their employees at the worst terms possible and employees aren’t benefitting either. So everyone’s hurting here.”

She said: “Sorbet assumes the liability on ourselves and so then we can allow the company to control their cash flow and decide when they want to pay us back. They gain a lot of financial value because we are able to be very, very attractive on our funding. So it saves costs, it provides them with complete control of their cash flow and it allows them to give out amazing financial benefits to employees at a time where we can all use some extra cash right now.”

The platform Sorbet has built will, it says, sync with calendars, HR and payroll systems, identify habits and then proactively suggest personalized, pre-approved 3-6 hour “Micro Breaks”, 1-4 day “Micro Vacations” and +1 week Vacations. This, says the startup, increases PTO used by as much as 15%.

Employers can constantly renegotiate the terms of the loan with Sorbet, thus matching future cash flow, insulating themselves against salary raises (wage inflation), and take advantage of other benefits.

The co-founders are Eilat-Raichel, who previously worked at L’Oréal, Lockheed Martin and a fintech entrepreneur; Eliaz Shapira, co-founder and CPO; and Rami Kasterstein, co-founder and board member.

Powered by WPeMatico

Casa Blanca, which aims to develop a “Bumble-like app” for finding a home, has raised $2.6 million in seed funding.

Co-founder and CEO Hannah Bomze got her real estate license at the age of 18 and worked at Compass and Douglas Elliman Real Estate before launching Casa Blanca last year.

She launched the app last October with the goal of matching home buyers and renters with homes using an in-app matchmaking algorithm combined with “expert agents.” Buyers get up to 1% of home purchases back at closing. Similar to dating apps, Casa Blanca’s app is powered by a simple swipe left or right.

Samuel Ben-Avraham, a partner and early investor of Kith and an early investor in WeWork, led the round for Casa Blanca, bringing its total raise to date to $4.1 million.

The New York-based startup recently launched in the Colorado market and has seen some impressive traction in a short amount of time.

Since launching the app in October, Casa Blanca has “made more than $100M in sales” and is projected to reach $280 million this year between New York and its Denver launch.

Bomze said the app experience will be customized for each city with the goal of creating a personalized experience for each user. Casa Blanca claims to streamline and sort listings based on user preferences and lifestyle priorities.

Image Credits: Casa Blanca

“People love that there is one place to book, manage feedback, schedule and communicate with a branded agent for one cohesive experience,” Bomze said. “We have a breadth of users from first time buyers to people using our platform for $15 million listings.”

Unlike competitors, Casa Blanca applies a direct-to-consumer model, she pointed out.

“While our agents are an integral part of the company, they are not responsible for bringing in business and have more organizational support, which allows them to focus on the individual more and creates a better end-to-end experience for the consumer,” Bomze said.

Casa Blanca currently has over 38 agents in NYC and Colorado, compared to about 15 at this time last year.

“We are in a growth phase and finding a unique opportunity in this climate, in particular, because there are many women exploring new, more flexible job opportunities,” Bomze noted.

The company plans to use its new capital to continue expanding into new markets, nationally and globally; as well as enhancing its technology and scaling.

“As we continue to grow in new markets, the app experience will be curated to each city — for example, in Colorado you can edit your preferences based on access to ski areas — to make sure we’re offering a personalized experience for each user,” Bomze said.

Powered by WPeMatico

For this morning’s column, Alex Wilhelm looked back on the last few months, “a busy season for technology exits” that followed a hot Q4 2020.

We’re seeing signs of an IPO market that may be cooling, but even so, “there are sufficient SPACs to take the entire recent Y Combinator class public,” he notes.

Once we factor in private equity firms with pockets full of money, it’s evident that late-stage companies have three solid choices for leveling up.

Seeking more insight into these liquidity options, Alex interviewed:

After recapping their deals, each executive explains how their company determined which flashing red “EXIT” sign to follow. As Alex observed, “choosing which option is best from a buffet’s worth of possibilities is an interesting task.”

Thanks very much for reading Extra Crunch! Have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Image Credits: Nigel Sussman

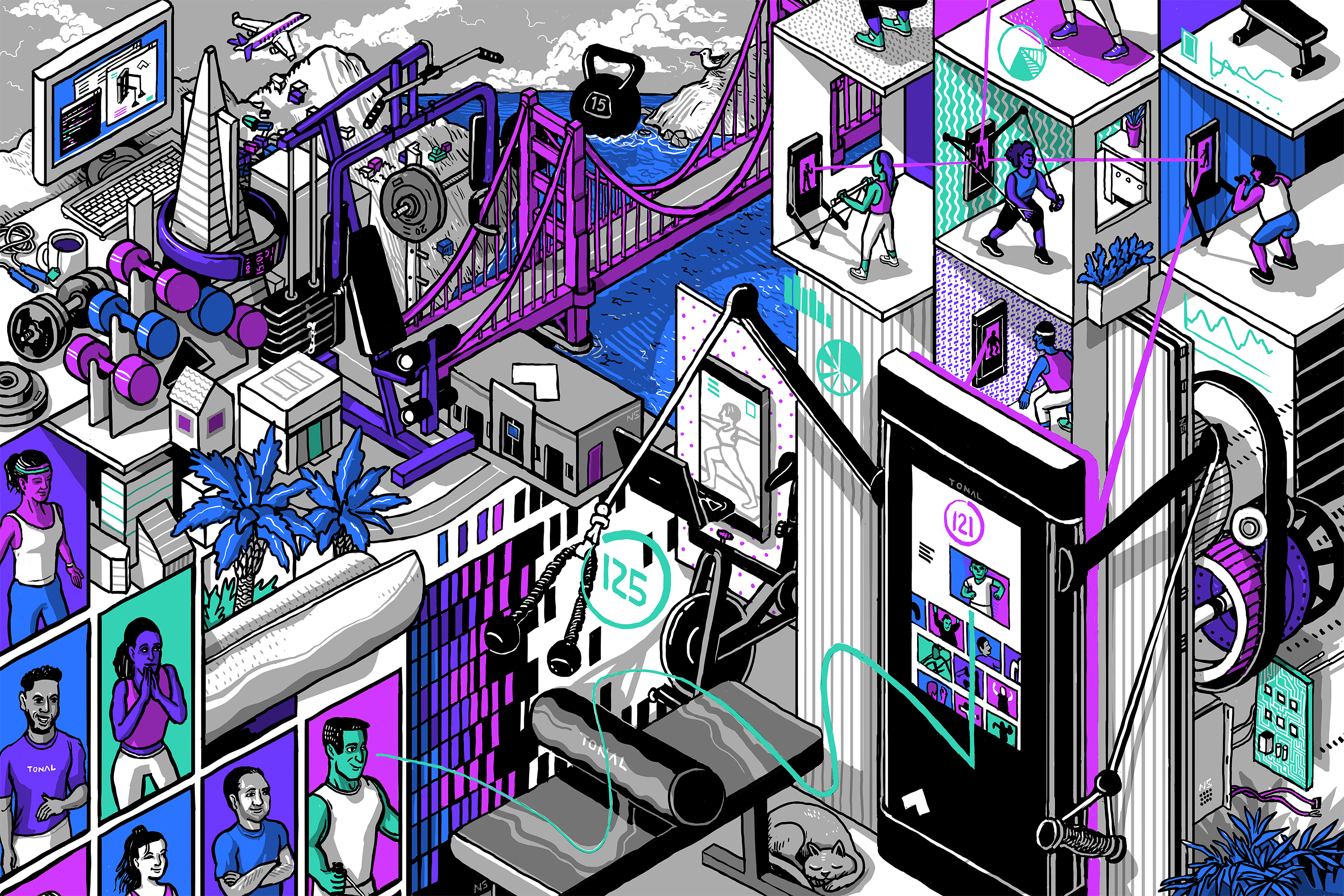

On Tuesday, we published a four-part series on Tonal, a home fitness startup that has raised $200 million since it launched in 2018. The company’s patented hardware combines digital weights, coaching and AI in a wall-mounted system that sells for $2,995.

By any measure, it is poised for success — sales increased 800% between December 2019 and 2020, and by the end of this year, the company will have 60 retail locations. On Wednesday, Tonal reported a $250 million Series E that valued the company at $1.6 billion.

Our deep dive examines Tonal’s origins, product development timeline, its go-to-market strategy and other aspects that combined to spark investor interest and customer delight.

We call this format the “EC-1,” since these stories are as comprehensive and illuminating as the S-1 forms startups must file with the SEC before going public.

Here’s how the Tonal EC-1 breaks down:

We have more EC-1s in the works about other late-stage startups that are doing big things well and making news in the process.

Image Credits: Nigel Sussman (opens in a new window)

Why did Deliveroo struggle when it began to trade? Is it suffering from cultural dissonance between its high-growth model and more conservative European investors?

Let’s peek at the numbers and find out.

Image Credits: Nigel Sussman (opens in a new window)

The Exchange doubts many folks expected the IPO climate to get so chilly without warning. But we could be in for a Q2 pause in the formerly scorching climate for tech debuts.

Image Credits: Nigel Sussman (opens in a new window)

A $65 million Series B is remarkable, even by 2021 standards. But the fact that a16z is pouring more capital into the alt-media space is not a surprise.

Substack is a place where publications have bled some well-known talent, shifting the center of gravity in media. Let’s take a look at Substack’s historical growth.

Image Credits: Visual Generation / Getty Images

Robotic process automation came to the fore during the pandemic as companies took steps to digitally transform. When employees couldn’t be in the same office together, it became crucial to cobble together more automated workflows that required fewer people in the loop.

RPA has enabled executives to provide a level of automation that essentially buys them time to update systems to more modern approaches while reducing the large number of mundane manual tasks that are part of every industry’s workflow.

Image Credits: Javier Zayas Photography (opens in a new window) / Getty Images

This year is all about the roll-ups, the aggregation of smaller companies into larger firms, creating a potentially compelling path for equity value. The interest in creating value through e-commerce brands is particularly striking.

Just a year ago, digitally native brands had fallen out of favor with venture capitalists after so many failed to create venture-scale returns. So what’s the roll-up hype about?

Image Credits: TarikVision (opens in a new window) / Getty Images

The cyber world has entered a new era in which attacks are becoming more frequent and happening on a larger scale than ever before. Massive hacks affecting thousands of high-level American companies and agencies have dominated the news recently. Chief among these are the December SolarWinds/FireEye breach and the more recent Microsoft Exchange server breach.

Everyone wants to know: If you’ve been hit with the Exchange breach, what should you do?

Image Credits: David Malan (opens in a new window) / Getty Images

Machine learning has become the foundation of business and growth acceleration because of the incredible pace of change and development in this space.

But for engineering and team leaders without an ML background, this can also feel overwhelming and intimidating.

Here are best practices and must-know components broken down into five practical and easily applicable lessons.

Image Credits: Busakorn Pongparnit / Getty Images

Embedded procurement is the natural evolution of embedded fintech.

In this next wave, businesses will buy things they need through vertical B2B apps, rather than through sales reps, distributors or an individual merchant’s website.

Image Credits: twomeows / Getty Images

There’s a persistent fallacy swirling around that any startup growing pain or scaling problem can be solved with business development.

That’s frankly not true.

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie:

I’m a founder of a startup on an E-2 investor visa and just got engaged! My soon-to-be spouse will sponsor me for a green card.

Are there any minimum salary requirements for her to sponsor me? Is there anything I should keep in mind before starting the green card process?

— Betrothed in Belmont

Image Credits: RichVintage / Getty Images

Many organizations perceive data management as being akin to data governance, where responsibilities are centered around establishing controls and audit procedures, and things are viewed from a defensive lens.

That defensiveness is admittedly justified, particularly given the potential financial and reputational damages caused by data mismanagement and leakage.

Nonetheless, there’s an element of myopia here, and being excessively cautious can prevent organizations from realizing the benefits of data-driven collaboration, particularly when it comes to software and product development.

Image Credits: Jetta Productions Inc (opens in a new window) / Getty Images

Cyber strategy and company strategy are inextricably linked. Consequently, chief information security officers in the C-suite will be just as common and influential as CFOs in maximizing shareholder value.

Image Credits: Tetra Images (opens in a new window) / Getty Images

Edtech unicorns have boatloads of cash to spend following the capital boost to the sector in 2020. As a result, edtech M&A activity has continued to swell.

The idea of a well-capitalized startup buying competitors to complement its core business is nothing new, but exits in this sector are notable because the money used to buy startups can be seen as an effect of the pandemic’s impact on remote education.

But in the past week, the consolidation environment made a clear statement: Pandemic-proven startups are scooping up talent — and fast.

Image Credits: Orbon Alija (opens in a new window)/ Getty Images

Knowledge transfer is not the only trend flowing in the U.S.-Asia-LatAm nexus. Competition is afoot as well.

Because of similar market conditions, Asian tech giants are directly expanding into Mexico and other LatAm countries.

Image Credits: Steven Puetzer (opens in a new window) / Getty Images

There’s certainly no shortage of SaaS performance metrics leaders focus on, but NRR (net revenue retention) is without question the most underrated metric out there.

NRR is simply total revenue minus any revenue churn plus any revenue expansion from upgrades, cross-sells or upsells. The greater the NRR, the quicker companies can scale.

Image Credits: SOPA Images (opens in a new window) / Getty Images

Even the most experienced and talented game designers from the mobile F2P business usually fail to understand what features matter to Robloxians.

For those just starting their journey in Roblox game development, these are the most common mistakes gaming professionals make on Roblox.

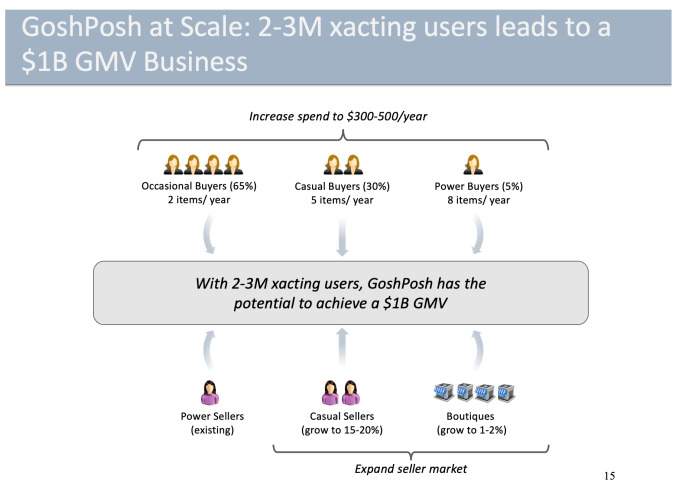

Image Credits: Poshmark

“Lead with love, and the money comes.” It’s one of the cornerstone values at Poshmark. On the latest episode of Extra Crunch Live, Chandra and Chaddha sat down with us and walked us through their original Series A pitch deck.

Image Credits: hopsalka (opens in a new window) / Getty Images

Cities are bustling hubs where people live, work and play. When the pandemic hit, some people fled major metropolitan markets for smaller towns — raising questions about the future validity of cities.

But those who predicted that COVID-19 would destroy major urban communities might want to stop shorting the resilience of these municipalities and start going long on what the post-pandemic future looks like.

Image Credits: Gearstd (opens in a new window) / Getty Images

There’s plenty of uncertainty surrounding copyright issues, fraud and adult content, and legal implications are the crux of the NFT trend.

Whether a court would protect the receipt-holder’s ownership over a given file depends on a variety of factors. All of these concerns mean artists may need to lawyer up.

Image Credits: Nigel Sussman (opens in a new window)

It’s a reasonable question: Why would anyone pay that much for Cazoo today if Carvana is more profitable and whatnot? Well, growth. That’s the argument anyway.

Powered by WPeMatico