Column

Auto Added by WPeMatico

Auto Added by WPeMatico

Most founders fall into an extremely common trap: Just because you produced outstanding results for the last round of investors doesn’t mean new investors will believe you. This new cohort hasn’t seen that performance firsthand, and they have no reason to trust you yet.

As a founder approaching your next round, it’s common to wonder, “How do I get this new group of investors to trust that I will perform?”

In our experience, founders who fundraise successfully are great at building relationships, and they usually deliver what we call “the pre-pitch.” This is the “we actually aren’t looking for money; we just want to be friends for now” pitch that gets you on an investor’s radar so that when it’s time to raise your next round, they’ll be far more likely to answer the phone because they actually know who you are.

But the concept of the pre-pitch goes deeper than just having potential investors be aware of your existence. Building relationships with potential future investors requires you to think less like a founder and more like a marketer — much of the relationship heavy lifting comes long before it’s time to ask for a capital commitment.

If an investor has made a deal in your space, there’s a good chance they know an earlier-round investor who could potentially be a good fit for you today.

There’s a host of advantages to the pre-pitch approach:

Now you’re probably wondering, “What the heck do I say to build a good relationship with that next-round investor?” Here are a few notes on how to approach the pre-pitch:

Acknowledge you’re early, but mention that you think it could potentially be a good fit later on. State it up front that you’re seeking a relationship and want to find out if you could eventually be a good fit for one another. Don’t sneak in an ask; let the relationship blossom organically.

Here’s an example: “We’re actually not raising yet, and we’re probably too early for you. But I think this is something you might be very interested in, and thought it made sense to reach out, open up a relationship and see if there might be a fit.”

Powered by WPeMatico

Which terms come to mind when you think about SaaS?

“Solutions,” “cutting-edge,” “scalable” and “innovative” are just a sample of the overused jargon lurking around every corner of the techverse, with SaaS marketers the world over seemingly singing from the same hymn book.

Sadly for them, new research has proven that such jargon-heavy copy — along with unclear features and benefits — is deterring customers and cutting down conversions. Around 57% of users want to see improvements in the clarity and navigation of websites, suggesting that techspeak and unnecessarily complex UX are turning customers away at the door, according to The SaaS Engine.

That’s not to say SaaS marketers aren’t trying: Seventy percent of those surveyed have been making big adjustments to their websites, and 33% have updated their content. So how and why are they missing the mark?

They say there’s no bigger slave to fashion than someone determined to avoid it, and SaaS marketing is no different. To truly stand out, you need to do thorough competitor analysis.

There are three common blunders that most SaaS marketers make time and again when it comes to clarity and high-converting content:

We’re going to unpack what the research suggests and the steps you can take to avoid these common pitfalls.

It’s a jungle out there. But while camouflage might be key to surviving in the wild, in the crowded SaaS marketplace, it’s all about standing out. Let’s be honest: How many SaaS homepages have you visited that look the same? How many times have you read about “innovative tech-driven solutions that will revolutionize your workflow”?

The research has found that of those using SaaS at work, 76% are now on more platforms or using existing ones more intensively than last year. And as always, with increased demand comes a boom in competition, so it’s never been more important to stand out. Rather than imitating the same old phrases and copy your competitors are using, it’s time to reach your audience with originality, empathy and striking clarity.

But how do you do that?

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

Extra Crunch members receive access to weekly “Dear Sophie” columns; use promo code ALCORN to purchase a one- or two-year subscription for 50% off.

Dear Sophie,

I received a conditional green card after my wife and I got married in 2019. Recently, we have made the difficult decision to end our marriage. I want to continue living and working in the United States.

Is it still possible for me to complete my green card based on my marriage through the I-751 process or do I need to do something else, like ask my employer to sponsor me for a work visa?

— Better to Have Loved and Lost

Dear Better,

I’m sorry to hear your marriage didn’t work out. Rest assured, you can still proceed with getting a full-fledged green card even though you and your wife are divorcing. Listen to my recent podcast with Anita Koumriqian, my law partner, in which we discuss the removal of conditions on permanent residence for people who got two-year green cards through marriage.

As you know, since you were married for less than two years when you applied for your green card through marriage, you were issued a conditional green card that is only valid for two years rather than a 10-year green card. The purpose of the I-751 is to show that the couple entered into a genuine, good faith marriage. Usually, couples must file an I-751 petition together. However, an individual may file a petition without a spouse if any of the following apply:

If your divorce is not yet finalized and you don’t have a family law attorney yet, I do recommend that you work with a family law attorney, who is necessary to help streamline the process. I also recommend consulting an immigration attorney as soon as possible to prepare the I-751 filing since it can get tricky for an individual in divorce proceedings. Both need to work together and in parallel to ensure that everything goes smoothly for you with U.S. Citizenship and Immigration Services.

Image Credits: Joanna Buniak / Sophie Alcorn (opens in a new window)

The I-751 should be filed within the 90-day period before your conditional green card is set to expire. I recommend filing as soon as you can within that window. Keep in mind that, if you file your I-751 petition too early, it may be returned to you. And if you file it after your conditional green card expires, you not only face having to leave the U.S., but USCIS could also deny your petition if you fail to provide a compelling reason. If you are in this situation, definitely let your immigration attorney know.

Powered by WPeMatico

The pandemic has highlighted some of the brightest spots — and greatest areas of need — in America’s healthcare system. On one hand, we’ve witnessed the vibrancy of America’s innovation engine, with notable contributions by U.S.-based scientists and companies for vaccines and treatments.

On the other hand, the pandemic has highlighted both the distribution challenges and cost inefficiencies of the healthcare system, which now accounts for nearly a fifth of our GDP — far more than any other country — yet lags many other developed nations in clinical outcomes.

Many of these challenges stem from a lack of alignment between payment and incentive models, as well as an overreliance on hospitals as centers for care delivery. A third of healthcare costs are incurred at hospitals, though at-home models can be more effective and affordable. Furthermore, most providers rely on fee for service instead of preventive care arrangements.

These factors combine to make care in this country reactive, transactional and inefficient. We can improve both outcomes and costs by moving care from the hospital back to the place it started — at home.

Right now in-home care accounts for only 3% of the healthcare market. We predict that it will grow to 10% or more within the next decade.

In-home care is nothing new. In the 1930s, over 40% of physician-patient encounters took place in the home, but by the 1980s, that figure dropped to under 1%, driven by changes in health economics and technologies that led to today’s hospital-dominant model of care.

That 50-year shift consolidated costs, centralized access to specialized diagnostics and treatments, and created centers of excellence. It also created a transition from proactive to reactive care, eliminating the longitudinal relationship between patient and provider. In today’s system, patients are often diagnosed by and receive treatment from individual doctors who do not consult one another. These highly siloed treatments often take place only after the patient needs emergency care. This creates higher costs — and worse outcomes.

That’s where in-home care can help. Right now in-home care accounts for only 3% of the healthcare market. We predict that it will grow to 10% or more within the next decade. This growth will improve the patient experience, achieve better clinical outcomes and reduce healthcare costs.

To make these improvements, in-home healthcare strategies will need to leverage next-generation technology and value-based care strategies. Fortunately, the window of opportunity for change is open right now.

Over the last few years, five significant innovations have created new incentives to drive dramatic changes in the way care is delivered.

Powered by WPeMatico

Investors and politicians embracing a vision of an all-electric car future believe that path will significantly reduce global carbon dioxide emissions. That’s far from clear.

A growing body of research points to the likelihood that widespread replacement of conventional cars with EVs would likely have a relatively small impact on global emissions. And it’s even possible that the outcome would increase emissions.

The issue is not primarily about the emissions resulting from producing electricity. Instead, it’s what we know and don’t know about what happens before an EV is delivered to a customer, namely, the “embodied” emissions arising from the labyrinthine supply chains to obtain and process all the materials needed to fabricate batteries.

All products entail embodied emissions that are ‘hidden’ upstream in production processes, whether it’s a hamburger, a house, a smartphone, or a battery. To see the implications at the macro level, credit France’s High Climate Council for a study issued last year. The analysis found that France’s claim of achieving a national decline in carbon dioxide emissions was illusory. Emissions had in fact increased and were some 70% higher than reported once the embodied emissions inherent in the country’s imports were counted.

Embodied emissions can be devilishly difficult to accurately quantify, and nowhere are there more complexities and uncertainties than with EVs. While an EV self-evidently emits nothing while driving, about 80% of its total lifetime emissions arise from the combination of the embodied energy in fabricating the battery and then in ‘fabricating’ electricity to power the vehicle. The remaining comes from manufacturing the non-fuel parts of the car. That ratio is inverted for a conventional car where about 80% of lifecycle emissions come directly from fuel burned while driving, and the rest comes from the embodied energy to make the car and fabricate gasoline.

Virtually every feature of the fuel-cycle for conventional cars is well-understood and narrowly bounded, significantly monitored if not tightly regulated, and largely assumption-free. That’s not the case for EVs.

For example, one review of fifty academic studies found estimates for embodied emissions to fabricate a single EV battery ranged from a low of about eight tons to as high as 20 tons of CO2. Another recent technical analysis put the range at about four to 14 tons. The high end of those ranges is nearly as much CO2 as is produced by the lifetime of fuel burned by an efficient conventional car. Again, that’s before the EV is delivered to a customer and driven its first mile.

The uncertainties come from inherent—and likely unresolvable—variabilities in both the quantity and type of energy used in the battery fuel cycle with factors that depend on geography and process choices, many often proprietary. Analyses of the embodied energy show a range from two to six barrels of oil (in energy-equivalent terms) is used to fabricate a battery that can store the energy-equivalent of one gallon of gasoline. Thus, any calculation of embodied emissions for an EV battery is an estimate based on myriad assumptions. The fact is, no one can measure today’s or predict tomorrow’s EV carbon dioxide ‘mileage.’

As more dollars flood into government programs and climate-tech funds — 2021 is on track to blow past record 2020 climate-tech investments, with three firms alone, BlackRock, General Atlantic and TPG, each announcing new $4 to $5 billion cleantech funds — we’re overdue for paying serious attention to embodied emissions of EVs and other presumed technological panaceas for reducing carbon dioxide emissions. As we will see shortly, the attention may not reveal the expected outcomes.

The goal for any vehicle is to have the fuel system take as small a share of total weight as possible, leaving room for passengers or cargo. Lithium batteries, as revolutionary and Nobel-prize worthy as they are, still constitute a distant second place in the metric of merit for powering untethered machines: energy density.

The inherent energy density of lithium-class chemicals (i.e., not a battery cell, but the raw chemical) can be theoretically as high as about 700 watt-hours per kilogram (Wh/kg). While that’s roughly five-fold greater than the energetics of lead-acid battery chemistry, it’s still a small fraction of the 12,000 Wh/kg available in petroleum.

To achieve the same driving range as 60 pounds of gasoline, an EV battery weighs about 1,000 pounds. Not much of that gap is closed by the lower weight of an electric versus gasoline motor because the former is typically only about 200 pounds lighter than the latter.

Manufacturers offset some of a battery’s weight penalty by lightening the rest of the EV using more aluminum or carbon-fiber instead of steel. Unfortunately, those materials are respectively 300% and 600% more energy intensive per pound to produce than steel. Using a half ton of aluminum, common in many EVs, adds six tons of CO2 to the non-battery embodied emissions (a factor most analyses ignore.) But it’s with all the other elements, the ones needed to fabricate the battery itself, where the emissions accounting gets messy.

There are many combinations of elements possible for lithium battery chemistries. Choices are dictated by compromises to meet a battery’s mix of performance metrics: safety, density, charge rate, lifespan, etc. Depending on the specific formulation chosen, the embodied energy associated with the key battery chemicals themselves can vary by as much as 600%.

Consider the key elements in the widely used nickel-cobalt formulation. A typical 1,000-pound EV battery contains about 30 pounds of lithium, 60 pounds of cobalt, 130 pounds of nickel, 190 pounds of graphite, and 90 pounds of copper. (The balance of the weight is with steel, aluminum, and plastic.)

Uncertainties in the embodied energy begin with the ore grade, or share of rock that contains each target mineral. Ore grades can range from a few percent to as little as 0.1 percent depending on the mineral, the mine, and over time. Using today’s averages, the quantity of ore mined—necessarily using energy-intensive heavy equipment—for one single EV battery is about: 10 tons of lithium brines to get to the 30 pounds of lithium; 30 tons of ore to get 60 pounds of cobalt; 5 tons for the 130 pounds of nickel; 6 tons for the 90 pounds of copper; and about one ton of ore for the 190 pounds of graphite.

Aerial view of trucks loading brine from the evaporation pools of the new state-owned lithium extraction complex, in the southern zone of the Uyuni Salt Flat, Bolivia, on July 10, 2019. Image Credits: PABLO COZZAGLIO/AFP via Getty Images

Then, one must add to that tonnage the “over-burden,” the amount of earth that’s first removed in order to access the mineral-bearing ore. That quantity also varies widely, depending on ore type and geology, typically from about three to seven tons excavated to access one ton of ore. Putting all the factors together, fabricating a single half-ton EV battery can entail digging up and moving a total of about 250 tons of earth. After that, an aggregate total of roughly 50 tons of ore are transported and processed to separate out the targeted minerals.

Embodied energy is also impacted by a mine’s location, something that is in theory knowable today but is a guessing-game regarding the future. Remote mining sites typically involve more trucking and depend on more off-grid electricity, the latter commonly supplied by diesel generators. As it stands today, the mineral sector alone accounts for nearly 40% of global industrial energy use. And over one-half of the world’s batteries or the key battery chemicals are produced in Asia with its coal-dominated electric grids. Despite hopes for more factories in Europe and North America, every forecast sees Asia utterly dominating that supply chain for a long time.

Most analyses of EV emissions don’t ignore the embodied carbon debt in batteries. But that factor is typically, and simplistically, assigned a single value in order to calculate the variabilities arising from using EVs on different electric grids.

A recent analysis from the International Council on Clean Transportation (ICCT) is usefully illustrative. The ICCT, using a fixed carbon debt for a battery, focused on how the EV carbon footprint varies depending on where it’s driven in Europe. The calculations showed that, compared to a fuel-efficient conventional car, an EV’s lifecycle emissions can range from as much as 60% lower when driven in Norway or France, to about 25% lower when driven in the U.K., to tiny emissions reduction if driven in Germany. (Germany’s grid has roughly the same average carbon emissions per kilowatt-hour as does America’s.)

Their analysis used average grid emissions data that don’t necessarily represent emissions that occur when plugged in. But the specific time, not the average, determines the actual source of electricity used for ‘fueling.’ No such ambiguities attend to the location and time of gasoline use; it’s always the same anytime and anywhere on the planet. While the EV time factor has minimal variability in Norway and France where most electricity comes around the clock from hydro and nuclear respectively, it can vary wildly elsewhere from, say, 100% solar to 100% coal depending on the time of day, month and location.

The lignite-fired power station of Boxberg in Germany. The region of Lusatia in the east of Germany and its economic infrastructure is heavily dependent on the coal-fired power plants in Jaenschwalde, Schwarze Pumpe and Boxberg. Image Credits: Florian Gaertner/Photothek via Getty Images

Another recent ICCT analysis also used annualized grid averages and calculated that, compared to an average car, lifecycle emissions reductions range from about 25% for EVs in India to 70% in Europe. But, as with the similar exercise for intra-European comparisons, a single, fixed carbon debt for battery fabrication was assumed, and a low value at that.

There is good reason to consider the implications of the range of embodied battery emissions, rather than a single, low average value, because the IEA (amongst others) reports that most mineral production today entails processes at the higher end of emissions “intensity.” Adjusting the ICCT outcomes for that reality lowers the calculated lifecycle EV emissions savings to about 40% (instead of 60%) driving in Norway, to little or no reduction in the U.K. or the Netherlands, and about a 20% increase for EVs driven in Germany.

That’s not the end of the real-world uncertainties. The ICCT, again typical of many similar analyses, made calculations based on batteries 30% to 60% smaller than the size required to replicate the 300-mile range needed for widespread replacement of conventional cars. The larger batteries are common on high-end EVs today. Doubling the size of the battery leads to a straightforward doubling of its carbon debt which, in turn, dramatically erodes or eliminates lifecycle emissions savings in many, maybe most places.

Similarly problematic, one finds forecasts of future emissions savings often explicitly assume that the future battery supply chain will be located in the country where the EVs operate. One widely cited analysis assumed aluminum demand for U.S. EVs would be met by domestic smelters and powered mainly from hydro dams. While that may be theoretically possible, it doesn’t reflect reality. The United States, for example, produces just 6% of global aluminum. If one assumes instead the industrial processes are located in Asia, the calculated lifecycle emissions are 150% higher.

For EV carbon accounting, the problem is that there are no reporting mechanisms or standards even remotely equivalent to the transparency with which petroleum is obtained, refined, and consumed. The challenges in having accurate data are not lost on the researchers, even if those concerns don’t percolate up into executive summaries and media claims. In the technical literature one often finds cautionary statements such as a “greater understanding of the energy required to manufacture Li-ion battery cells is crucial for properly assessing the environmental implications of a rapidly increasing use of Li-ion batteries.” Or in another recent research paper: “Unfortunately, industry data for the rest of the battery materials remain meager to nonexistent, forcing LCA [lifecycle analysis] researchers to resort to engineering calculations or approximations to fill the data gaps.”

Those “data gaps” become chasms when it comes to expanding the world’s mineral supply chain to support the production of tens of millions of more EVs.

Perhaps the most important wildcard is the expected rise in energy costs associated with obtaining the necessary quantities of “energy transition minerals,” (ETMs) as the International Energy Agency (IEA) terms them.

Earlier this year, the agency issued a major report on the challenges of supplying ETMs to build batteries as well as solar and wind machines. The report reinforces what others have earlier pointed out. Compared to conventional cars, EVs require using, overall, about 500% more critical minerals per vehicle. Thus, the IEA concludes that current plans for EVs, along with plans for wind and solar, will require a 300% to 4,000% increase in global mine output for the necessary suite of key minerals.

The fact that an EV uses, for example, about 300 to 400% more copper than a conventional car has yet to impact global supply chain because EVs still account for less than 1% of the total global auto fleet. Producing EVs at scale, along with plans for grid batteries as well as for wind and solar machines, will push the “clean energy” sector up to consuming over half of all global copper (from today’s 20% level). For nickel and cobalt, to note two other relevant minerals, “transition” aspirations will push clean energy use of those two metals to 60% and 70%, respectively of global demand, up from a negligible share today.

Tesla Inc. vehicles in a parking lot after arriving at a port in Yokohama, Japan, on Monday, May 10, 2021. Image Credits: Toru Hanai/Bloomberg via Getty Images

To illustrate the ultimate scale of demand that EV mandates alone will place on mining, consider that a world with 500 million electric cars—which would still constitute under half of all vehicles—would require mining a quantity of energy minerals sufficient to build batteries for about 3 trillion smartphones. That’s equal to over 2,000 years of mining and production for the latter. For the record, that many EVs would eliminate only about 15% of world oil use.

Set aside the environmental, economic, and geopolitical implications of such a staggering expansion of global mining. The World Bank cautions about “a new suite of challenges for the sustainable development of minerals and resources.” Such an increase in mining has direct relevance for predictions about the future carbon intensity for minerals because acquiring raw materials already accounts for nearly one half of the life-cycle carbon dioxide emissions for EVs.

As the IEA report also observes, ETMs not only have a “high emissions intensity,” but trends show that the energy-use-per-pound mined has been rising because of long-standing declines in ore grades. If mineral demands accelerate, miners will necessarily chase ever lower grade ores, and increasingly in more remote locations. The IEA sees, for example, a 300% to 600% increase in emissions to produce each pound of lithium and nickel respectively.

Nickel mine, Thio, New Caledonia, French Overseas Collectivity, France. Image Credits: DeAgostini/Getty Images

Trends with copper are illustrative of the challenge. From 1930 to 1970, advances in the post-mining chemical processes led to a 30% drop in energy use to produce a ton of copper even though ore grades slowly declined. But those were one-time gains as optimized processes approached physics limits. Thus, during the four decades after 1970, as ore grade continued to decline, energy use per ton of copper increased, and returned to the same level as in 1930. That will be the pattern for the near future as ore grades continue to decline for other minerals.

Nonetheless, the IEA, like others, uses today’s putative average supply-chain emissions intensity to assert that EVs in the future will reduce emissions. But the data in the IEA’s own report point to rising embodied emissions for ETMs. Add to this the implications of far more solar and wind construction, which the IEA notes require 500% to 700% more minerals compared to building a natural gas power plant, and we’ll see even more pressure on the mining supply chain — which, in the commodity world, points to a dramatic rise in prices.

If the EV share of vehicles rises from today’s less than 1% and begins to approach a 10% share, the resource experts at Wood Mackenzie see untenable material demands: “Unless battery technology can be developed, tested, commercialised, manufactured and integrated into EVs and their supply chains faster than ever before, it will be impossible for many EV targets and ICE (internal combustion engine) bans to be achieved – posing issues for current EV adoption rate projections.”

There’s no evidence of capabilities to accelerate industry-class chemical development and manufacturing, or mining, in the short time-periods common in policy aspirations. Nearly three decades passed after the discovery of lithium battery chemistry before the first Tesla sedan.

There are, of course, ways to ameliorate some of the factors that are dragging the world toward a future with increasing EV supply-chain emissions: better battery chemistry (reducing materials needed per kilowatt-hour of stored energy), more efficient chemical processes, electrifying mining equipment, and recycling. All of these are often offered as “inevitable” or “necessary” solutions. But none can have a significant impact in the time frames contemplated for rapid EV expansion.

Even though popular news stories frequently claim some “breakthrough,” there are no commercially viable alternative battery chemistries that significantly change the order-of-magnitude of the physical materials needed per electric-vehicle-mile. In most cases, changing chemistry formulations merely shifts burdens.

For example, reducing the use of cobalt is generally achieved by increasing nickel content. As for chemistries that eliminate the use of energetic atoms of, say, carbon or nickel, using instead, for example, more prosaic and low-energy-intensity elements like iron (e.g., the lithium-iron-phosphate battery), such formulations have lower energy density. The latter means a bigger, heavier battery is needed to maintain vehicle range. Still, it is reasonable to imagine the eventual discovery of a foundationally superior classes of battery chemistries. But once validated, it then takes many years to safely scale-up industrial chemical systems. Batteries put into cars today, and for the near future, will necessarily use technologies available now and not theoretically available someday.

Then there’s the prospect for improving the efficiency of the various chemical processes used in the mineral refining and conversion processes. Improvements there are inevitable, in no small part because that’s what engineers always do, and in the digital era they will more often find success. But there are no known “step function” changes on the horizon in the well-trod field of physical chemistry where processes already operate near physics limits. Put differently, lithium batteries are now well past the early stages where one sees rapid improvements in process (and cost) efficiencies and have entered the stage of incremental gains.

As for electrifying mining trucks and equipment, Caterpillar, Deere and Case (and others) all have such projects, and even a few production machines for sale. Promising designs are on the horizon for a few specific applications, but batteries are not up to the 24×7 performance demands to power heavy equipment in most uses. Moreover, the turnover rate in mining and industrial equipment is measured in decades. Mines will use a lot of oil-fired equipment for a very long time.

Finally, there’s recycling, commonly proposed to mitigate new demands. Even if all batteries were entirely recycled, it couldn’t come close to meeting the enormous increase in demand that will arise from the proposed (or mandated) growth path for EVs. In any case, there are unresolved technical challenges regarding the efficacy and economics of recycling critical minerals from complex machines, especially batteries. While one might imagine someday having automated recycling capabilities, nothing like that exists now. And given the variety of present and future battery designs, there’s no clear path to such capabilities in the timeframes policymakers and EV proponents have in mind.

The unavoidable fact is that there are so many assumptions, guesses, and ambiguities that any claims of EV emissions reductions will be subject to manipulation if not fraud. Much of the necessary data may never be collectable in any normal regulatory fashion given the technical uncertainties, the variety and opacity of geographic factors, as well as the proprietary nature of many of the processes. Even so, the Securities and Exchange Commission is apparently considering such disclosure requirements. The uncertainties in the EV ecosystem could lead to legal havoc if European and U.S. regulators enshrine “green disclosures” in legally binding ways, or enforce “responsible” ESG metrics regarding carbon dioxide emissions.

For policymakers eager to reduce automotive oil use, engineers have already invented an easier and more certain way to achieve that goal while awaiting revolutions in battery chemistry and mining. Commercially viable combustion engines already exist that can cut fuel use by as much as 50%. Capturing just half that potential by providing incentives for consumers to purchase more efficient engines would be cheaper, faster—and transparently verifiable—than adding 300 million EVs to the world’s roads.

Powered by WPeMatico

Facebook is a monopoly. Right?

Mark Zuckerberg appeared on national TV today to make a “special announcement.” The timing could not be more curious: Today is the day Lina Khan’s FTC refiled its case to dismantle Facebook’s monopoly.

To the average person, Facebook’s monopoly seems obvious. “After all,” as James E. Boasberg of the U.S. District Court for the District of Columbia put it in his recent decision, “No one who hears the title of the 2010 film ‘The Social Network’ wonders which company it is about.” But obviousness is not an antitrust standard. Monopoly has a clear legal meaning, and thus far Lina Khan’s FTC has failed to meet it. Today’s refiling is much more substantive than the FTC’s first foray. But it’s still lacking some critical arguments. Here are some ideas from the front lines.

To the average person, Facebook’s monopoly seems obvious. But obviousness is not an antitrust standard.

First, the FTC must define the market correctly: personal social networking, which includes messaging. Second, the FTC must establish that Facebook controls over 60% of the market — the correct metric to establish this is revenue.

Though consumer harm is a well-known test of monopoly determination, our courts do not require the FTC to prove that Facebook harms consumers to win the case. As an alternative pleading, though, the government can present a compelling case that Facebook harms consumers by suppressing wages in the creator economy. If the creator economy is real, then the value of ads on Facebook’s services is generated through the fruits of creators’ labor; no one would watch the ads before videos or in between posts if the user-generated content was not there. Facebook has harmed consumers by suppressing creator wages.

A note: This is the first of a series on the Facebook monopoly. I am inspired by Cloudflare’s recent post explaining the impact of Amazon’s monopoly in their industry. Perhaps it was a competitive tactic, but I genuinely believe it more a patriotic duty: guideposts for legislators and regulators on a complex issue. My generation has watched with a combination of sadness and trepidation as legislators who barely use email question the leading technologists of our time about products that have long pervaded our lives in ways we don’t yet understand. I, personally, and my company both stand to gain little from this — but as a participant in the latest generation of social media upstarts, and as an American concerned for the future of our democracy, I feel a duty to try.

According to the court, the FTC must meet a two-part test: First, the FTC must define the market in which Facebook has monopoly power, established by the D.C. Circuit in Neumann v. Reinforced Earth Co. (1986). This is the market for personal social networking services, which includes messaging.

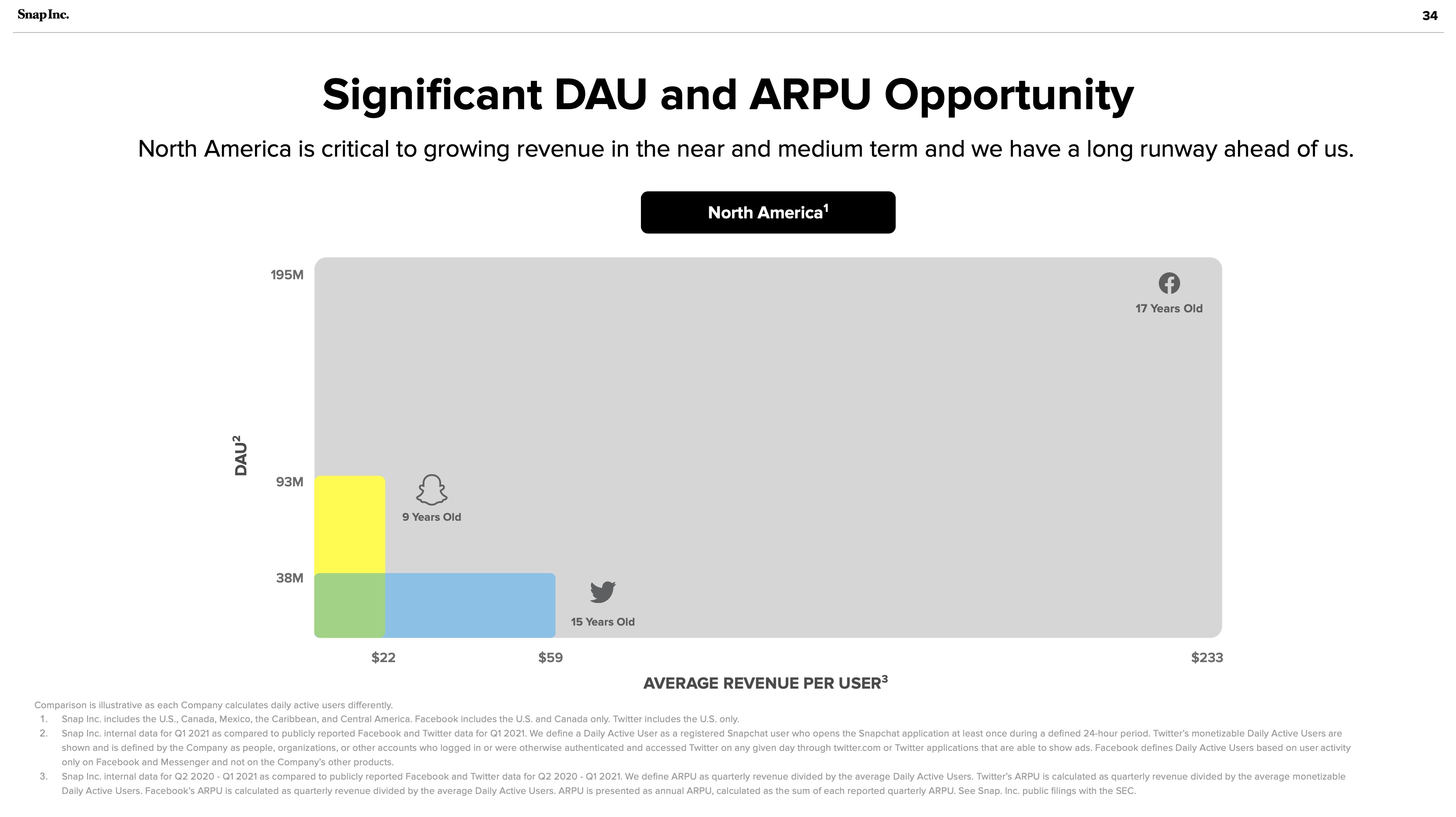

Second, the FTC must establish that Facebook controls a dominant share of that market, which courts have defined as 60% or above, established by the 3rd U.S. Circuit Court of Appeals in FTC v. AbbVie (2020). The right metric for this market share analysis is unequivocally revenue — daily active users (DAU) x average revenue per user (ARPU). And Facebook controls over 90%.

The answer to the FTC’s problem is hiding in plain sight: Snapchat’s investor presentations:

Snapchat July 2021 investor presentation: Significant DAU and ARPU Opportunity. Image Credits: Snapchat

This is a chart of Facebook’s monopoly — 91% of the personal social networking market. The gray blob looks awfully like a vast oil deposit, successfully drilled by Facebook’s Standard Oil operations. Snapchat and Twitter are the small wildcatters, nearly irrelevant compared to Facebook’s scale. It should not be lost on any market observers that Facebook once tried to acquire both companies.

The FTC initially claimed that Facebook has a monopoly of the “personal social networking services” market. The complaint excluded “mobile messaging” from Facebook’s market “because [messaging apps] (i) lack a ‘shared social space’ for interaction and (ii) do not employ a social graph to facilitate users’ finding and ‘friending’ other users they may know.”

This is incorrect because messaging is inextricable from Facebook’s power. Facebook demonstrated this with its WhatsApp acquisition, promotion of Messenger and prior attempts to buy Snapchat and Twitter. Any personal social networking service can expand its features — and Facebook’s moat is contingent on its control of messaging.

The more time in an ecosystem the more valuable it becomes. Value in social networks is calculated, depending on whom you ask, algorithmically (Metcalfe’s law) or logarithmically (Zipf’s law). Either way, in social networks, 1+1 is much more than 2.

Social networks become valuable based on the ever-increasing number of nodes, upon which companies can build more features. Zuckerberg coined the “social graph” to describe this relationship. The monopolies of Line, Kakao and WeChat in Japan, Korea and China prove this clearly. They began with messaging and expanded outward to become dominant personal social networking behemoths.

In today’s refiling, the FTC explains that Facebook, Instagram and Snapchat are all personal social networking services built on three key features:

Unfortunately, this is only partially right. In social media’s treacherous waters, as the FTC has struggled to articulate, feature sets are routinely copied and cross-promoted. How can we forget Instagram’s copying of Snapchat’s stories? Facebook has ruthlessly copied features from the most successful apps on the market from inception. Its launch of a Clubhouse competitor called Live Audio Rooms is only the most recent example. Twitter and Snapchat are absolutely competitors to Facebook.

Messaging must be included to demonstrate Facebook’s breadth and voracious appetite to copy and destroy. WhatsApp and Messenger have over 2 billion and 1.3 billion users respectively. Given the ease of feature copying, a messaging service of WhatsApp’s scale could become a full-scale social network in a matter of months. This is precisely why Facebook acquired the company. Facebook’s breadth in social media services is remarkable. But the FTC needs to understand that messaging is a part of the market. And this acknowledgement would not hurt their case.

Boasberg believes revenue is not an apt metric to calculate personal networking: “The overall revenues earned by PSN services cannot be the right metric for measuring market share here, as those revenues are all earned in a separate market — viz., the market for advertising.” He is confusing business model with market. Not all advertising is cut from the same cloth. In today’s refiling, the FTC correctly identifies “social advertising” as distinct from the “display advertising.”

But it goes off the deep end trying to avoid naming revenue as the distinguishing market share metric. Instead the FTC cites “time spent, daily active users (DAU), and monthly active users (MAU).” In a world where Facebook Blue and Instagram compete only with Snapchat, these metrics might bring Facebook Blue and Instagram combined over the 60% monopoly hurdle. But the FTC does not make a sufficiently convincing market definition argument to justify the choice of these metrics. Facebook should be compared to other personal social networking services such as Discord and Twitter — and their correct inclusion in the market would undermine the FTC’s choice of time spent or DAU/MAU.

Ultimately, cash is king. Revenue is what counts and what the FTC should emphasize. As Snapchat shows above, revenue in the personal social media industry is calculated by ARPU x DAU. The personal social media market is a different market from the entertainment social media market (where Facebook competes with YouTube, TikTok and Pinterest, among others). And this too is a separate market from the display search advertising market (Google). Not all advertising-based consumer technology is built the same. Again, advertising is a business model, not a market.

In the media world, for example, Netflix’s subscription revenue clearly competes in the same market as CBS’ advertising model. News Corp.’s acquisition of Facebook’s early competitor MySpace spoke volumes on the internet’s potential to disrupt and destroy traditional media advertising markets. Snapchat has chosen to pursue advertising, but incipient competitors like Discord are successfully growing using subscriptions. But their market share remains a pittance compared to Facebook.

The FTC has correctly argued for the smallest possible market for their monopoly definition. Personal social networking, of which Facebook controls at least 80%, should not (in their strongest argument) include entertainment. This is the narrowest argument to make with the highest chance of success.

But they could choose to make a broader argument in the alternative, one that takes a bigger swing. As Lina Khan famously noted about Amazon in her 2017 note that began the New Brandeis movement, the traditional economic consumer harm test does not adequately address the harms posed by Big Tech. The harms are too abstract. As White House advisor Tim Wu argues in “The Curse of Bigness,” and Judge Boasberg acknowledges in his opinion, antitrust law does not hinge solely upon price effects. Facebook can be broken up without proving the negative impact of price effects.

However, Facebook has hurt consumers. Consumers are the workers whose labor constitutes Facebook’s value, and they’ve been underpaid. If you define personal networking to include entertainment, then YouTube is an instructive example. On both YouTube and Facebook properties, influencers can capture value by charging brands directly. That’s not what we’re talking about here; what matters is the percent of advertising revenue that is paid out to creators.

YouTube’s traditional percentage is 55%. YouTube announced it has paid $30 billion to creators and rights holders over the last three years. Let’s conservatively say that half of the money goes to rights holders; that means creators on average have earned $15 billion, which would mean $5 billion annually, a meaningful slice of YouTube’s $46 billion in revenue over that time. So in other words, YouTube paid creators a third of its revenue (this admittedly ignores YouTube’s non-advertising revenue).

Facebook, by comparison, announced just weeks ago a paltry $1 billion program over a year and change. Sure, creators may make some money from interstitial ads, but Facebook does not announce the percentage of revenue they hand to creators because it would be insulting. Over the equivalent three-year period of YouTube’s declaration, Facebook has generated $210 billion in revenue. one-third of this revenue paid to creators would represent $70 billion, or $23 billion a year.

Why hasn’t Facebook paid creators before? Because it hasn’t needed to do so. Facebook’s social graph is so large that creators must post there anyway — the scale afforded by success on Facebook Blue and Instagram allows creators to monetize through directly selling to brands. Facebooks ads have value because of creators’ labor; if the users did not generate content, the social graph would not exist. Creators deserve more than the scraps they generate on their own. Facebook suppresses creators’ wages because it can. This is what monopolies do.

Facebook has long been the Standard Oil of social media, using its core monopoly to begin its march upstream and down. Zuckerberg announced in July and renewed his focus today on the metaverse, a market Roblox has pioneered. After achieving a monopoly in personal social media and competing ably in entertainment social media and virtual reality, Facebook’s drilling continues. Yes, Facebook may be free, but its monopoly harms Americans by stifling creator wages. The antitrust laws dictate that consumer harm is not a necessary condition for proving a monopoly under the Sherman Act; monopolies in and of themselves are illegal. By refiling the correct market definition and marketshare, the FTC stands more than a chance. It should win.

A prior version of this article originally appeared on Substack.

Powered by WPeMatico

The Pareto principle, also known as the 80-20 rule, asserts that 80% of consequences come from 20% of causes, rendering the remainder way less impactful.

Those working with data may have heard a different rendition of the 80-20 rule: A data scientist spends 80% of their time at work cleaning up messy data as opposed to doing actual analysis or generating insights. Imagine a 30-minute drive expanded to two-and-a-half hours by traffic jams, and you’ll get the picture.

As tempting as it may be to think of a future where there is a machine learning model for every business process, we do not need to tread that far right now.

While most data scientists spend more than 20% of their time at work on actual analysis, they still have to waste countless hours turning a trove of messy data into a tidy dataset ready for analysis. This process can include removing duplicate data, making sure all entries are formatted correctly and doing other preparatory work.

On average, this workflow stage takes up about 45% of the total time, a recent Anaconda survey found. An earlier poll by CrowdFlower put the estimate at 60%, and many other surveys cite figures in this range.

None of this is to say data preparation is not important. “Garbage in, garbage out” is a well-known rule in computer science circles, and it applies to data science, too. In the best-case scenario, the script will just return an error, warning that it cannot calculate the average spending per client, because the entry for customer #1527 is formatted as text, not as a numeral. In the worst case, the company will act on insights that have little to do with reality.

The real question to ask here is whether re-formatting the data for customer #1527 is really the best way to use the time of a well-paid expert. The average data scientist is paid between $95,000 and $120,000 per year, according to various estimates. Having the employee on such pay focus on mind-numbing, non-expert tasks is a waste both of their time and the company’s money. Besides, real-world data has a lifespan, and if a dataset for a time-sensitive project takes too long to collect and process, it can be outdated before any analysis is done.

What’s more, companies’ quests for data often include wasting the time of non-data-focused personnel, with employees asked to help fetch or produce data instead of working on their regular responsibilities. More than half of the data being collected by companies is often not used at all, suggesting that the time of everyone involved in the collection has been wasted to produce nothing but operational delay and the associated losses.

The data that has been collected, on the other hand, is often only used by a designated data science team that is too overworked to go through everything that is available.

The issues outlined here all play into the fact that save for the data pioneers like Google and Facebook, companies are still wrapping their heads around how to re-imagine themselves for the data-driven era. Data is pulled into huge databases and data scientists are left with a lot of cleaning to do, while others, whose time was wasted on helping fetch the data, do not benefit from it too often.

The truth is, we are still early when it comes to data transformation. The success of tech giants that put data at the core of their business models set off a spark that is only starting to take off. And even though the results are mixed for now, this is a sign that companies have yet to master thinking with data.

Data holds much value, and businesses are very much aware of it, as showcased by the appetite for AI experts in non-tech companies. Companies just have to do it right, and one of the key tasks in this respect is to start focusing on people as much as we do on AIs.

Data can enhance the operations of virtually any component within the organizational structure of any business. As tempting as it may be to think of a future where there is a machine learning model for every business process, we do not need to tread that far right now. The goal for any company looking to tap data today comes down to getting it from point A to point B. Point A is the part in the workflow where data is being collected, and point B is the person who needs this data for decision-making.

Importantly, point B does not have to be a data scientist. It could be a manager trying to figure out the optimal workflow design, an engineer looking for flaws in a manufacturing process or a UI designer doing A/B testing on a specific feature. All of these people must have the data they need at hand all the time, ready to be processed for insights.

People can thrive with data just as well as models, especially if the company invests in them and makes sure to equip them with basic analysis skills. In this approach, accessibility must be the name of the game.

Skeptics may claim that big data is nothing but an overused corporate buzzword, but advanced analytics capacities can enhance the bottom line for any company as long as it comes with a clear plan and appropriate expectations. The first step is to focus on making data accessible and easy to use and not on hauling in as much data as possible.

In other words, an all-around data culture is just as important for an enterprise as the data infrastructure.

Powered by WPeMatico

When you enter the health tech industry as a new startup, an advisory board is a crucial foundational step. A board can guide you through industry-specific nuances, help you make important decisions and prove your legitimacy to investors looking for a strong industry background.

An advisory board will be able to give you strategic insights about both your company and the wider healthcare and technology industries.

In my experience of raising capital, the unpredictable financial situation at the beginning of the pandemic meant we nearly lost our $2 million round, but came through with a committed $250,000, which we used to bring in about $500,000 in revenue.

Something that helped this process was building our advisory board and starting small — we didn’t go for all of healthcare but instead focused on two healthcare verticals. This allowed us to prove our concept, build case studies and win contracts with specific teams in our customers’ companies.

It pays off to stay focused and prove your worth so that your advisory board members can champion you in niche markets, with the potential to expand in the future. For this reason, it’s important to identify the main intention behind your board, and exactly who should be on it.

Three to five people is an ideal starting point for an advisory board, depending on the size and stage of your company. In health tech, you need more than just the healthcare perspective — you also need the insight of those who have already grown technology companies, perhaps outside of the industry. Our company’s board is an even split of two healthcare and two technology advisers, and, ideally, you want to find a fifth who is well versed in both industries.

It pays off to stay focused and prove your worth so that your advisory board members can champion you in niche markets, with the potential to expand in the future.

An M.D., a Ph.D. from a respected institution or a thought leader in your relevant field of healthcare is the most important asset to an advisory board. These are the highly decorated physicians who have strong connections and act as a reference for their peers.

They provide instant credibility for your company, help you get into the minds of both patients and healthcare providers, and can outline how various health systems work.

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

Extra Crunch members receive access to weekly “Dear Sophie” columns; use promo code ALCORN to purchase a one- or two-year subscription for 50% off.

Dear Sophie,

I’m on an H-1B living and working in the U.S. I want to apply for a green card on my own. I’m concerned about only relying on my current employer and I want to be able to easily change jobs or create a startup. I’ve been looking at the EB-1A and EB-2 NIW.

I’m not sure if I would qualify for an EB-1A, but since I was born in India, I face a much longer wait for an EB-2 NIW. Any tips on how to proceed?

— Inventive from India

Dear Inventive,

Thanks for your question. Take a listen to my podcast episode in which I discuss the latest tech immigration news and delve into the benefits and requirements of the EB-1A green card for individuals of extraordinary ability and the EB-2 NIW (National Interest Waiver) green card, which as you know are the main employment-based green cards for which individuals can self-sponsor.

I recommend you consult an experienced immigration attorney who can evaluate your abilities and accomplishments and assess your prospects for each green card. After an initial consultation with new clients, we’re able to provide a lot more detail to folks on their specific options since these are such individualized pathways.

There are some groups of people who might need every advantage. Those can include folks born in India or China, who might face long green card backlogs. Another such group includes people whose skills and accomplishments might be borderline for an EB-1A green card for extraordinary ability. In some cases — if eligible and to have every opportunity for green card security and to mitigate wait times as much as possible — our clients choose to file both the EB-1A and EB-2 NIW in parallel.

Image Credits: Joanna Buniak / Sophie Alcorn (opens in a new window)

The EB-1A is the highest priority green card and the standard for qualifying is much higher than for the EB-2 NIW. And that means an EB-1A is typically quicker to get, which is particularly the case now: According to the August 2021 Visa Bulletin, there is no wait for an EB-1A green card regardless of country of birth, while only individuals who were born in India and have a priority date of June 1, 2011 or earlier can proceed with their EB-2 NIW petition.

Please remember that the Visa Bulletin fluctuates and changes every month. Also, the EB-1A is currently eligible for premium processing on the I-140. Although there is talk to add this option to the EB-2 NIW one day, premium processing is not available for EB-2 NIW I-140s yet.

Powered by WPeMatico

The pandemic has been extremely painful for many. But as lockdowns lifted and people began resuming their outdoor hobbies, mobile-first businesses have seen growth accelerate as consumers turned to digital tools to improve their time outdoors.

The Dyrt, for example, is the top camping app on the Apple and Google Play App Stores. The app sits at the confluence of two trends: An increased interest in outdoor recreation and travel, and an explosion in consumer subscription software (CSS).

The Dyrt launched its premium offering in 2019, The Dyrt PRO, in time to take advantage of the rising number of Americans making the great outdoors part of their lifestyle. A year later, it had a new subscriber every two minutes paying for features like offline maps and detailed camping information.

CSS businesses at the forefront of outdoor activities have closed major deals in recent years such as hunting app OnX (Summit Partners), hiking app Alltrails (Spectrum Equity), Surfline (The Chernin Group) and mountain bike leader Pinkbike (Outside Media). Companies like Netflix and Spotify have trained consumers to pay monthly or annual fees for software that enhances their lives, creating a business model investors view as reliable and poised for growth.

I think of different outdoor activities almost like individual genres on Netflix. Dominating camping or surfing might be like capturing the streaming market for comedy or horror.

Fitness and the outdoor passion space is one of the most exciting CSS categories in a growing landscape that includes everything from family planning/management services to entertainment and education. I believe CSS is still in the early stages of its growth — perhaps where B2B SaaS was a decade ago.

So what sets apart the great CSS businesses from the good ones?

The beauty of the CSS model is the complete alignment between the business and its customers. CSS companies don’t have to please advertisers, and they can design purely for their users.

This dynamic is particularly powerful for CSS companies in the outdoors space, which make your favorite outdoor activity better with performance analytics and enhanced information such as maps, reviews, air quality reports and fire warnings. Consumers are happy to spend money on the activities and hobbies they enjoy, and CSS companies are able to make pleasing those consumers their top priority.

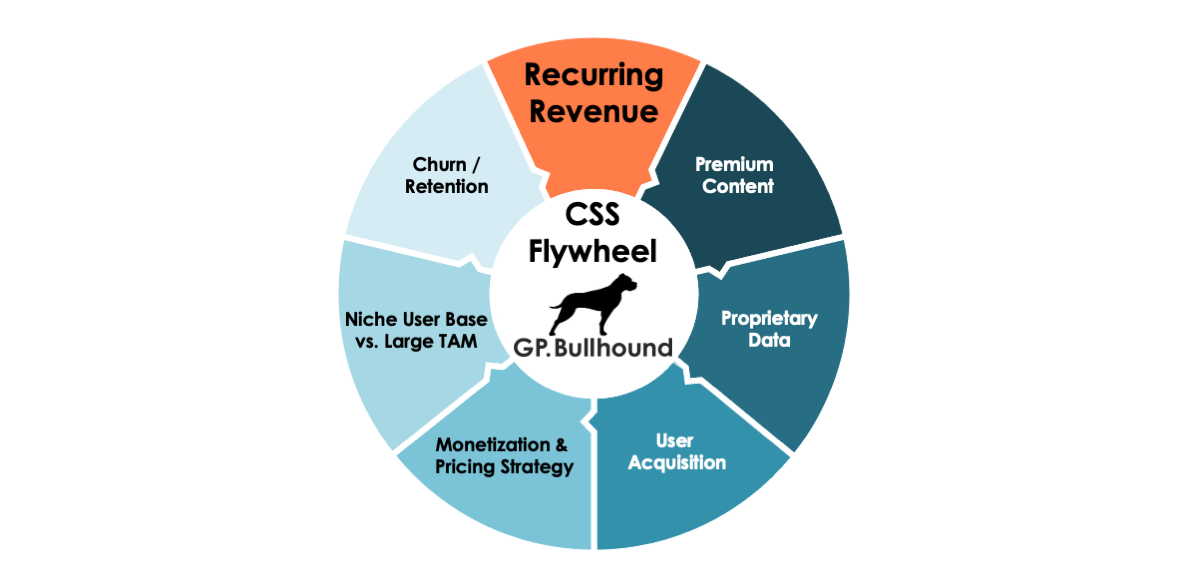

The result is what I call the CSS flywheel, in which a quality CSS product attracts and retains loyal users. Those users contribute their data through posts, photos and reviews, which creates a better product that further attracts new users, and so on.

The CSS flywheel shows the cycle that results when a quality CSS product attracts and retains loyal users. Image Credits: GP Bullhound

When companies get this flywheel right, it’s incredibly appealing to investors, because of the advantages of scale in CSS. Each niche will probably be dominated by one or two players, and a given niche can have tens of millions of consumers.

Powered by WPeMatico