Column

Auto Added by WPeMatico

Auto Added by WPeMatico

I’ve met hundreds of founders over the years, and most, particularly early-stage founders, share one common go-to-market gripe: Pricing.

For enterprise software, traditional pricing methods like per-seat models are often easier to figure out for products that are hyperspecific, especially those used by people in essentially the same way, such as Zoom or Slack. However, it’s a different ballgame for startups that offer services or products that are more complex.

Most startups struggle with a per-seat model because their products, unlike Zoom and Slack, are used in a litany of ways. Salesforce, for example, employs regular seat licenses and admin licenses — customers can opt for lower pricing for solutions that have low-usage parts — while other products are priced based on negotiation as part of annual renewals.

You may have a strong champion in a CIO you’re selling to or a very friendly person handling procurement, but it won’t matter if the pricing can’t be easily explained and understood. Complicated or unclear pricing adds more friction.

Early pricing discussions should center around the buyer’s perspective and the value the product creates for them. It’s important for founders to think about the output and the outcome, and a number they can reasonably defend to customers moving forward. Of course, self-evaluation is hard, especially when you’re asking someone else to pay you for something you’ve created.

This process will take time, so here are three tips to smoothen the ride.

Pricing is not a fixed exercise. The enterprise software business involves a lot of intangible aspects, and a software product’s perceived value, quality, and user experience can be highly variable.

The pricing journey is long and, despite what some founders might think, jumping headfirst into customer acquisition isn’t the first stop. Instead, step one is making sure you have a fully fledged product.

If you’re a late-seed or Series A company, you’re focused on landing those first 10-20 customers and racking up some wins to showcase in your investor and board deck. But when you grow your organization to the point where the CEO isn’t the only person selling, you’ll want to have your go-to-market position figured out.

Many startups fall into the trap of thinking: “We need to figure out what pricing looks like, so let’s ask 50 hypothetical customers how much they would pay for a solution like ours.” I don’t agree with this approach, because the product hasn’t been finalized yet. You haven’t figured out product-market fit or product messaging and you want to spend a lot of time and energy on pricing? Sure, revenue is important, but you should focus on finding the path to accruing revenue versus finding a strict pricing model.

Powered by WPeMatico

Funding for Black entrepreneurs in the U.S. hit nearly $1.8 billion in the first half of 2021 — a fourfold increase from the previous year. But most venture-backed startups are “still overwhelmingly white, male, Ivy-League-educated and based in Silicon Valley,” according to a study conducted by RateMyInvestor and Diversity VC.

With venture investors committing to funding Black and minority founders, alongside the growing availability of government-backed proposals, such as New Jersey allocating $10 million to a seed fund for Black and Latinx startups, can we expect to see fundamental change? Or will we have to repeat the same conversations about representation failings within VC funds?

Crunchbase examined the access to capital in the venture-backed startup ecosystem and proved that many industry leaders still worry that nothing will drastically shift. As a Black fintech founder, I believe that venture investors are making safe bets and investing in late-stage founders instead of early or even pre-seed stages.

But what about those minority founders who don’t have family, friends or connections to lean on for the first $250,000? Venture funding does remain elusive, but here are some tricks for startup founders to hack the system.

Getting your foot in the door with new venture capitalist partners is challenging, and it is often easy for minority founders to be naive at first. I thought that reading TechCrunch and analyzing other VC deals I saw in the news would help me land multiple responses and speak the language of those who managed to score million-dollar deals for their startups. However, I didn’t receive a single response while other founders received VC investment for basic ideas.

This is something I had to learn the hard way: What you hear in the media or read on a company blog post often simplifies the process, and sometimes fails to cover the trajectory that minority founders, in particular, must follow to secure funding.

I experienced hundreds of rejections before raising $2 million to start a mobile payment platform, Bleu, using beacon technology to drive simple and secure payments. It is a huge mountain to climb and a full-time job to continuously pitch your vision and yourself to reach the first meeting with a VC fund — and that’s still miles away from a funding discussion.

These discussions then bring further biases to the surface. If you sat in the conference rooms or on those Zoom calls and heard the types of deals proposed to minority founders, you’d see how offensive they can be. Often, these founders are offered all the money they have requested — but don’t be fooled. It is usually not given all at once due to what I consider to be a lack of trust. Essentially, interval funding equates to being babysat.

Therefore, as a minority founder, you have to realize that it will be a long ride, and you will face rejections because you are at a disadvantage before even opening your mouth to pitch your idea. It is all possible, but patience is key.

Once I figured out how complicated the funding process was, my coping mechanism was to figure out how to capitalize on the business ideas I already had in place in case I never received any VC funding.

Think: How could you make money without an institutional investor, friends, family or internal networks? You’ll be surprised by your entrepreneurial thirst for success when you’ve experienced 100 rejections. This is why minority businesses caught in these testing situations can quickly gain the upper hand, whether through ancillary and side businesses or crowdfunding over GoFundMe and Kickstarter.

Although generally considered non-essential, ancillary companies do provide a regular flow of income and services to assist your core business idea. Most importantly, a recurring revenue stream outside your core business demonstrates to investors that you can create valuable products and acquire loyal customers.

Make sure to find a niche market and carry out surveys with potential clients to find out what specific needs they have. Then, build a product with their feedback in mind and launch it to beta clients. When you publicly release the product, find resellers to keep internal headcount low and generate recurring revenue.

Don’t take ancillaries lightly, though; they are not just a side business. There can be payment issues if you get hooked on them for revenue, distractions from clients or partners wanting custom requests, and supply chain problems.

In my case, I built a point-of-sale (POS) software platform to sell to merchants, which gave me a different revenue stream that could integrate with Bleu’s payment technology. These ancillary businesses can help fund your core business until you manage to plan how to launch fully or source further funding.

In 2019, The New York Times published an article headlined “More Start-Ups Have an Unfamiliar Message for Venture Capitalists: Get Lost.” It highlights how more and more entrepreneurs shunned by the VC funding route are turning to alternatives and forming counter-movements. There are always alternatives to look at if the fundraising process is proving to be too arduous.

Accelerators allow ventures to define their products or services, quickly build networks and, most importantly, sit at tables they wouldn’t be able to on their own. Applying to accelerators as a minority founder was the real turning point for me because I met a crucial investor who allowed us to build credibility and open up to new networks, investors and clients.

I would suggest looking out for accelerators explicitly searching for minority founders by using platforms such as F6S. They match you with accelerators and early growth programs committed to innovation in various global industries, like financial technology. That’s how I found the VC FinTech Accelerator in 2016, where one-third of founders were from minority backgrounds.

Then, Bleu earned a spot in the 2020 class of the IBM Hyper Protect Accelerator dedicated to supporting innovative startups in fintech and health tech industries. These types of accelerators offer startups workshops, technical and business mentorship, and access to a network of partners, customers and stakeholders.

You can impress accelerators by creating a pitch deck and a company video less than two minutes long that shows your founder and the product, and engaging with the fintech community to spread the news.

The other alternative to accelerators is government funds, but they have had little success investing in startups for myriad reasons. It tends to be a more hands-off approach as government funds are not under significant pressure from limited partners (LPs, either institutional or individual investors) to perform.

What you need as a minority founder is an investor who is an active partner but, with government-backed funds, there is less demand to return the capital. We have to ask ourselves whether governments are really searching for the best minority-owned startups to help them get sufficient returns.

There are many unconscious social stigmas, stereotypes and unseen biases that exist in the U.S. And you’ll find those cultural dynamics are radically different in other countries that don’t have the same history of discrimination, especially when looking at a team or assessing founders.

I also noticed that, as well as reduced bias, investors out of Southeast Asia, Nordic countries and Australia seemed far more likely to take risks on new contactless payment technology as cash use decreased across their regions. Take Klarna and Afterpay as examples of fintech success stories.

First, I engaged in market research and pored over annual reports to decide whether I should look abroad for funding, instead of applying to funds closer to home. I looked at Nielsen reports, payment publications, PaymentSource and numerous government documents or white papers to figure out the cash usage globally.

My investigations revealed that fintech in Australia was far ahead of the curve, with four-fifths of the population using contactless payments. The financial services sector is also the largest contributor to the national economy, contributing around $140 billion to GDP a year. Therefore, I spoke to the Australian Department of Foreign Affairs and Trade in the U.S., and they recommended some regulatory payment groups.

I immediately flew to Australia to meet with the banking community, and I was able to find an Australian investor by word of mouth who was surrounded by the demand for mobile payment solutions.

In contrast, an investor in the U.S. still using cash and card had no interest in what I had to say. This highlights the importance of market research and seeking out investors rather than waiting for them to come to you. There is no science to it; leverage your network and reach out to people over LinkedIn, too.

VC funding needs to become more inclusive for women and minority groups by tackling the pipeline problem and addressing the level of diversity within VC funds. All of the networks that VCs reach out to first tend to come from university programs at Stanford, MIT and Harvard. These more privileged and wealthy students are able to easily leverage the traditional and outdated networks built to benefit them.

The number of venture dollars flowing to Black and Latinx founders is dismally low partly due to this knowledge gap; many female and minority founders don’t even know that VC funding is an option for them. Therefore, if you do receive seed funding, spread the news about it within your networks to help others.

Inclusion starts at the educational level but, when the percentage of Black and minority students at these elite colleges are still low, you can see why minority representation is needed in the VC ranks. Even if representation rises by a percent, that would be a significant change.

There are increasing numbers of VC funds announcing initiatives and interest in investing in minority businesses, and I would recommend looking at these in-depth. But what about the demographics of the VC firms? How many ethnicities are present in the executive ranks?

To change the venture-backed startup ecosystem, we need to start at the top and diversify those signing the checks. Looking toward the future, it is Black-led funds, like Sequoia, or others that focus on diversity, like Women’s Venture Fund, BackStage Capital and Elevate Capital Inclusive Fund, that are lighting the way to solutions that will reflect the diversity of the U.S.

It’s up to the investor community at large to be intentional about building relationships with, and ultimately providing funding to, more women and minority-led startups.

Despite the barriers and hurdles minority founders face when searching for VC funding, more and more avenues for acquiring funding are appearing as the disparities are brought to the media’s attention.

As the outdated system adjusts, the key is to continue preparing yourself for rejections and searching for appropriate accelerators to build vital networks. Then, if you aren’t having any luck, consider what you could do with your business idea without the VC funding or turn to foreign markets, which may have a different setup and varied opportunities.

Powered by WPeMatico

With the rise of livestreaming, gaming has evolved from a toy-like consumer product to a legitimate platform and medium in its own right for entertainment and competition.

Twitch’s viewer base alone has grown from 250,000 average concurrent viewers to over 3 million since its acquisition by Amazon in 2014. Competitors like Facebook Gaming and YouTube Live are following similar trajectories.

The boom in viewership has fueled an ecosystem of supporting products as today’s professional streamers push technology to its limit to increase the production value of their content and automate repetitive aspects of the video production cycle.

The largest streamers hire teams of video editors and social media managers, but growing and part-time streamers struggle to do this themselves or come up with the money to outsource it.

The online streaming game is a grind, with full-time creators putting in eight- if not 12-hour performances on a daily basis. In a bid to capture valuable viewer attention, 24-hour marathon streams are not uncommon either.

However, these hours in front of the camera and keyboard are only half of the streaming grind. Maintaining a constant presence on social media and YouTube fuels the growth of the stream channel and attracts more viewers to catch a stream live, where they may purchase monthly subscriptions, donate and watch ads.

Distilling the most impactful five to 10 minutes of content out of eight or more hours of raw video becomes a non-trivial time commitment. At the top of the food chain, the largest streamers can hire teams of video editors and social media managers to tackle this part of the job, but growing and part-time streamers struggle to find the time to do this themselves or come up with the money to outsource it. There aren’t enough minutes in the day to carefully review all the footage on top of other life and work priorities.

An emerging solution is to use automated tools to identify key moments in a longer broadcast. Several startups compete to dominate this emerging niche. Differences in their approaches to solving this problem are what differentiate competing solutions from each other. Many of these approaches follow a classic computer science hardware-versus-software dichotomy.

Athenascope was one of the first companies to execute on this concept at scale. Backed by $2.5 million of venture capital funding and an impressive team of Silicon Valley Big Tech alumni, Athenascope developed a computer vision system to identify highlight clips within longer recordings.

In principle, it’s not so different from how self-driving cars operate, but instead of using cameras to read nearby road signs and traffic lights, the tool captures the gamer’s screen and recognizes indicators in the game’s user interface that communicate important events happening in-game: kills and deaths, goals and saves, wins and losses.

These are the same visual cues that traditionally inform the game’s player what is happening in the game. In modern game UIs, this information is high-contrast, clear and unobscured, and typically located in predictable, fixed locations on the screen at all times. This predictability and clarity lends itself extremely well to computer vision techniques such as optical character recognition (OCR) — reading text from an image.

The stakes here are lower than self-driving cars, too, since a false positive from this system produces nothing more than a less-exciting-than-average video clip — not a car crash.

Powered by WPeMatico

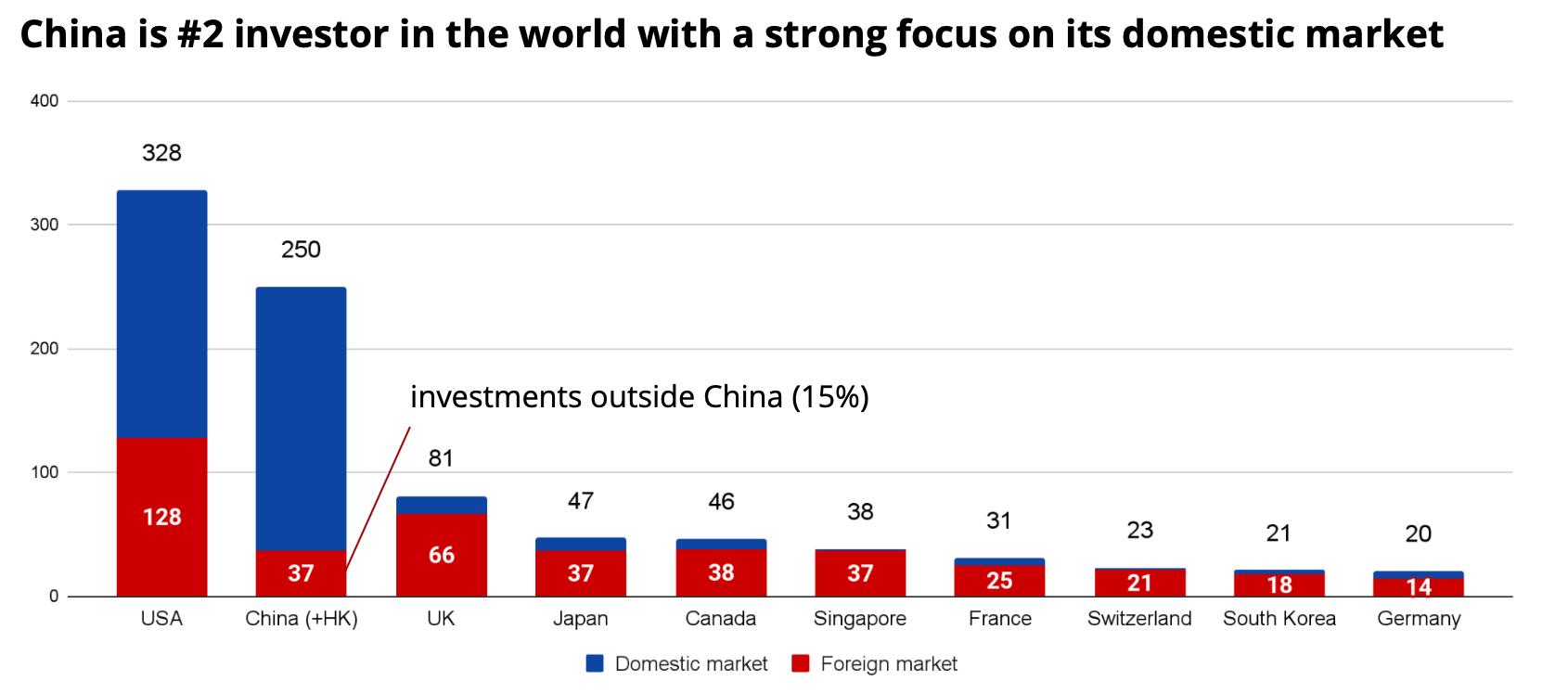

China is becoming a superpower in the tech industry. According to Straits Times, China is the only place in the world where it takes less than six years for a startup to become a unicorn — it takes seven years in the U.S., eight years in the U.K. and 11 years in Germany. Despite geopolitical tensions and recent amendments in CFIUS, it is hard to ignore China.

When I joined Runa Capital almost a year ago, my task was to help our portfolio companies enter the Chinese market, find the right partners and raise funding from Chinese investors. And almost on every call with our startups, colleagues from Runa or other global VCs, I heard: Is it a good idea to raise from a Chinese VC? Is it OK to co-invest with Chinese investors? I was surprised to learn that there is little research answering such questions, as there is a lack of adequate information in English about Chinese investments.

Access to the Chinese market seems to be an obvious reason to invite Chinese funds aboard, but only about 20% of Western startups with Chinese capital have operations in China.

So as a Mandarin-speaking specialist, I decided to fill this gap by conducting a study based on Chinese VC database ITjuzi (the Chinese version of Crunchbase) with the help of our powerful data science resources developed by Danil Okhlopkov.

Below, I will try to answer the following questions using statistics and a case-based approach:

After studying data from ITjuzi, we estimated that Chinese funds invested around $250 billion in 2020 (three times higher than the figure reported in Crunchbase). This figure puts Chinese VC investments only 30% lower than investments by U.S. funds, but three times that of U.K. funds and 12.5 times more than German funds.

Fig. 1 — Comparison of investment from different countries in 2020, $bn. Source: Crunchbase, ITjuzi. Image Credits: Denis Kalinin

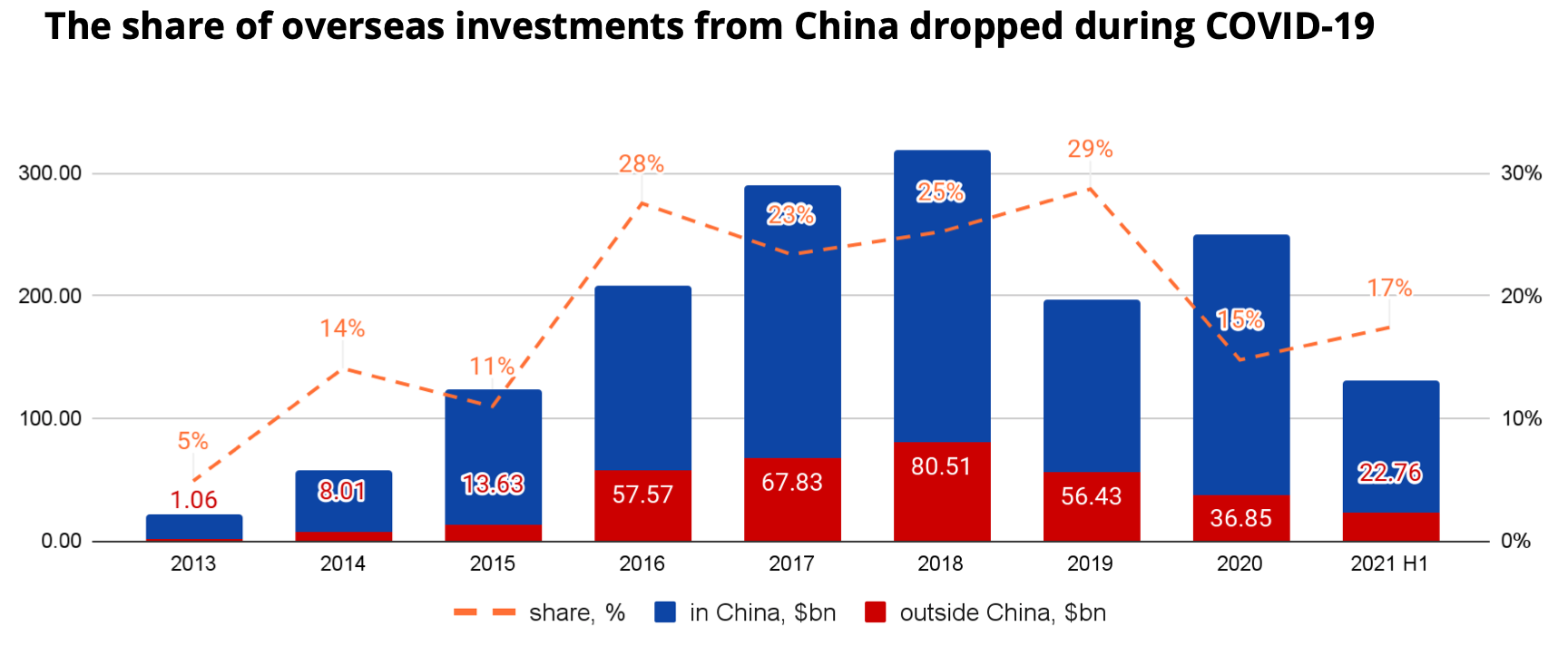

However, only 15% of investments in 2020 and 17% of investments in the first half of 2021 were in companies outside China, significantly lower than in 2019. This appears to be because during COVID, China’s economy recovered much faster than other countries’, so many Chinese investors preferred to redirect their capital flows to the domestic market.

On the other hand, there is great potential for overseas investments to rebound as soon as the borders reopen and the global economy starts to recover.

Fig. 2 — Dynamics of Chinese investments. $bn. Source: Crunchbase, ITjuzi. Image Credits: Denis Kalinin

We can also see that Chinese investors are eyeing European startups favorably, which is related to U.S.-China geopolitical tensions as well as the fact that the European VC market is becoming mature.

Powered by WPeMatico

Both as a term and as a financial product, “buy now, pay later” has become mainstream in the past few years. BNPL has evolved to assume various forms today, from small-ticket offerings by fintechs on consumer checkout platforms and marketplaces, to closed-loop products offered on marketplaces such as Amazon Pay Later (which they are now extending for outside use as well). You can also see some variants offered by companies that want to expand the scope of consumption and consumer credit.

Globally, BNPL has seen the most growth in the consumer segment and has driven retail consumption and lending over the past few years. Consumer BNPL offerings are a good alternative to credit cards, especially for people who do not have a credit history and can’t get credit from banks. That said, a specific vertical of BNPL products is gaining traction — one targeted toward small and medium enterprises (SMEs). This new vertical is known as “SME BNPL.”

BNPL can be particularly useful when flow-based underwriting or transaction-based underwriting is used to offer credit to small businesses.

E-commerce has seen tremendous growth in India over the past decade. Skyrocketing smartphone and internet penetration led to rapid growth in e-commerce across large cities and smaller towns alike. Consumer credit has also taken off in parallel as credit cards and digital lending spurred credit-based consumption across offline and online stores.

However, the large B2B supply chain enabling the burgeoning retail market was plagued by bottlenecks and inefficiencies because it involved a plethora of intermediaries and streamlining became a big problem. A number of tech players responded by organizing the previously disorganized B2B commerce market at various touch points, inserting convenience, pricing and easier product access through tech-enabled logistics and a modern supply chain.

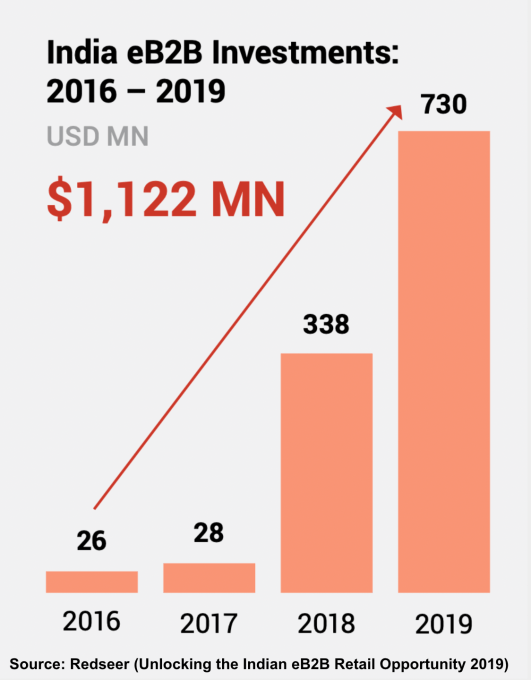

Image Credits: Redseer

India’s B2B e-commerce space has developed rapidly since 2020. Small businesses have moved from using paper to smartphone apps for running a significant part of their day-to-day business, leading to widespread disruption in how businesses transact today. The COVID-19 pandemic also forced small businesses, which were earlier using physical means to procure goods and services, to try new and online models to conduct their affairs.

Image Credits: Redseer

Moreover, the Indian government’s widespread promotion of an instant payments system in the form of the Unified Payments Interface (UPI) has changed how people send money to each other or pay merchants for their goods and services. The next step for solving the digital B2B puzzle is to embed credit inside every transaction and invoice.

Image Credits: Redseer

If we compare online B2B transactions to the offline world, there is only one missing link: The terms offered to small businesses by their supplier/distributor or vendor. Businesses, unlike consumers, must buy goods and services to eventually trade them, or add value and sell to consumers or others down the value chain. This process is not immediate and has a certain time cycle attached.

The longer sales cycle means many small businesses require credit payment terms when buying inventory. As B2B commerce scales and grows through digital means, a BNPL product that caters to the needs of SMEs can support their growth and alleviate the burden on their cash flows.

An SME BNPL product is a purchase financing product for small businesses transacting with suppliers, distributors, aggregator platforms or B2B marketplaces.

Powered by WPeMatico

As a parent of teenagers, I’m used to having tough, sometimes even awkward, conversations about topics that are complex but important. Most parents will likely agree with me when I say those types of conversations never get easier, but over time, you tend to develop a roadmap of how to approach the subject, how to make sure you’re being clear and how to answer hard questions.

And like many parents, I quickly learned that my children have just as much to teach me as I can teach them. I’ve learned that tough conversations build trust.

I’ve applied this lesson about trust-building conversations to an extremely important aspect of my role as the chief legal officer at Foursquare: Conducting “The Privacy Talk.”

The discussion should convey an understanding of how the legislative and regulatory environment are going to affect product offerings, including what’s being done to get ahead of that change.

It’s the conversation that goes beyond the written, publicly posted privacy policy and dives deep into a customer, vendor, supplier or partner’s approach to ethics. This conversation seeks to convey and align the expectations that two companies must have at the beginning of a new engagement.

RFIs may ask a lot of questions about privacy compliance, information security and data ethics. But it’s no match for asking your prospective partner to hop on a Zoom to walk you through their broader approach. Unless you hear it firsthand, it can be hard to discern whether a partner is thinking strategically about privacy, if they are truly committed to data ethics and how compliance is woven into their organization’s culture.

Powered by WPeMatico

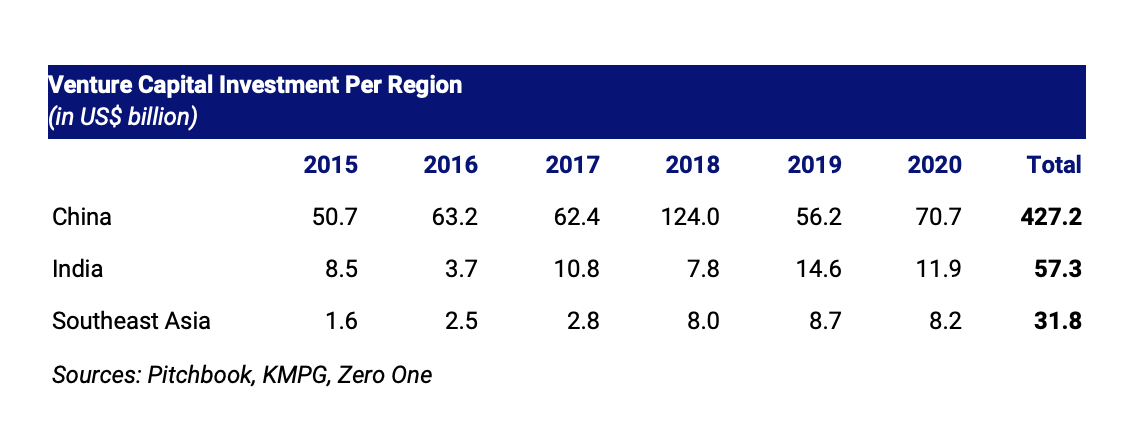

Southeast Asian tech companies are drawing the attention of investors around the world. In 2020, startups in the region raised over $8.2 billion, about four times more than they did in 2015. This trend continued in 2021, with regional M&A hitting a record high of $124.8 billion in the first half of 2021, up 83% from a year earlier.

This begs the question: Who exactly is investing in Southeast Asia?

Let’s explore the three key types of investors pouring money into and driving the growth of Southeast Asia’s tech ecosystem.

Over 229 family offices have been registered in Singapore since 2020, with total assets under management of an estimated $20 billion.

Southeast Asia has become an attractive market for U.S. and Chinese tech firms. Internet penetration here stands at 70%, higher than the global average, and digital adoption in the region remains nascent — it wasn’t until the pandemic that adoption of digital services such as e-wallets and online shopping took off.

China’s tech giants Tencent and Alibaba were among the first to support early e-commerce growth in Southeast Asia with investments in Sea Limited and Lazada, and have since expanded their footprint into other internet verticals. Alibaba has backed Akulaku, M-Pay (eMonkey), DANA, Wave Money and Mynt (GCash), while Tencent has invested in Voyager Innovations (PayMaya), SHAREit, iflix, Ookbee and Sanook.

U.S. tech firms have also recently entered the scene. In June 2020, Gojek closed a $3 billion Series F round from Google, Facebook, Tencent and Visa. Google, together with Singapore’s Temasek Holdings, invested some $350 million in Tokopedia in October. Meanwhile, Microsoft invested an undisclosed amount in Grab in 2018 and has invested $100 million in Indonesian e-commerce firm Bukalapak.

In Q1 2021, Southeast Asian startups raised $6 billion, according to DealStreetAsia, positioning 2021 as another record year for VC investment in the region.

The region is also rising in prominence as a destination for investment capital relative to the rest of Asia. Regional VC investment grew 5.2 times to $8.2 billion in 2020 from $1.6 billion in 2015, as we can see in the table below.

Image Credits: Jungle VC

Southeast Asia also has many opportunities for VC investment relative to its market size. From 2015 to 2020, China saw VC investment of nearly $300 per person; for Southeast Asia — despite a recent investment boom — this metric sits at just $47.50 per person, or just a sixth of that in China. This implies a substantial opportunity for investments to develop the region’s digital economy.

The region’s rising population and growth prospects are higher due to China’s population growth challenges, alongside the latter’s higher digital economy market saturation and maturity.

Powered by WPeMatico

The quest to make fusion power a reality recently took a massive step forward. The National Ignition Facility (NIF) at Lawrence Livermore National Laboratory announced the results of an experiment with an unprecedented high fusion yield. A single laser shot initiated reactions that released 1.3 megajoules of fusion yield energy with signatures of propagating nuclear burn.

Reaching this milestone indicates just how close fusion actually is to achieving power production. The latest results demonstrate the rapid pace of progress — especially as lasers are evolving at breathtaking speed.

Indeed, the laser is one of the most impactful technological inventions since the end of World War II. Finding widespread use in an incredibly diverse range of applications — including machining, precision surgery and consumer electronics — lasers are an essential part of everyday life. Few know, however, that lasers are also heralding an exciting and entirely new chapter in physics: enabling controlled nuclear fusion with positive energy gain.

After six decades of innovation, lasers are now assisting us in the urgent process of developing clean, dense and efficient fuels, which, in turn, are needed to help solve the world’s energy crisis through large-scale decarbonized energy production. The peak power attainable in a laser pulse has increased every decade by a factor of 1,000.

Physicists recently conducted a fusion experiment that produced 1,500 terawatts of power. For a short period of time, this generated four to five times more energy than what the whole world consumes at a given moment. In other words, we are already able to produce vast amounts of power. Now we also need to produce vast amounts of energy so as to offset the energy expended to drive the igniting lasers.

Beyond lasers, there are also considerable advances on the target side. The recent use of nanostructure targets allows for more efficient absorption of laser energies and ignition of the fuel. This has only been possible for a few years, but here, too, technological innovation is on a steep incline with tremendous advancement from year to year.

In the face of such progress, you may wonder what is still holding us back from making commercial fusion a reality.

There remain two significant challenges: First, we need to bring the pieces together and create an integrated process that satisfies all the physical and technoeconomic requirements. Second, we require sustainable levels of investment from private and public sources to do so. Generally speaking, the field of fusion is woefully underfunded. This is shocking given the potential of fusion, especially in comparison to other energy technologies.

Investments in clean energy amounted to more than $500 billion in 2020. The funds that go into fusion research and development are only a fraction of that. There are countless brilliant scientists working in the sector already, as well as eager students wishing to enter the field. And, of course, we have excellent government research labs. Collectively, researchers and students believe in the power and potential of controlled nuclear fusion. We should ensure financial support for their work to make this vision a reality.

What we need now is an expansion of public and private investment that does justice to the opportunity at hand. Such investments may have a longer time horizon, but their eventual impact is without parallel. I believe that net-energy gain is within reach in the next decade; commercialization, based on early prototypes, will follow in very short order.

But such timelines are heavily dependent on funding and the availability of resources. Considerable investment is being allocated to alternative energy sources — wind, solar, etc. — but fusion must have a place in the global energy equation. This is especially true as we approach the critical breakthrough moment.

If laser-driven nuclear fusion is perfected and commercialized, it has the potential to become the energy source of choice, displacing the many existing, less ideal energy sources. This is because fusion, if done correctly, offers energy that is in equal parts clean, safe and affordable. I am convinced that fusion power plants will eventually replace most conventional power plants and related large-scale energy infrastructure that are still so dominant today. There will be no need for coal or gas.

The ongoing optimization of the fusion process, which results in higher yields and lower costs, promises energy production at much below the current price point. At the limit, this corresponds to a source of unlimited energy. If you have unlimited energy, then you also have unlimited possibilities. What can you do with it? I foresee reversing climate change by taking out the carbon dioxide we have put into the atmosphere over the last 150 years.

With a future empowered by fusion technology, you would also be able to use energy to desalinate water, creating unlimited water resources that would have an enormous impact in arid and desert regions. All in all, fusion enables better societies, keeping them sustainable and clean rather than dependent on destructive, dirty energy sources and related infrastructures.

Through years of dedicated research at the SLAC National Accelerator Laboratory, the Lawrence Livermore National Laboratory and the National Ignition Facility, I was privileged to witness and lead the first inertial confinement fusion experiments. I saw the seed of something remarkable being planted and taking root. I have never been more excited than I am now to see the fruits of laser technology harvested for the empowerment and advancement of humankind.

My fellow scientists and students are committed to moving fusion from the realm of tangibility into that of reality, but this will require a level of trust and help. A small investment today will have a big impact toward providing a much needed, more welcome energy alternative in the global arena.

I am betting on the side of optimism and science, and I hope that others will have the courage to do so, too.

Powered by WPeMatico

Many efforts are underway to reduce the environmental impact of cars, but what about the tires those cars ride on? Continental thinks it might help. Roadshow reports the company has introduced the Conti GreenConcept (yes, a concept tire) where more than half of the materials are “traceable, renewable and recycled.” You can even renew the natural rubber tread with little trouble — not a completely new idea, but refreshable treads have generally been reserved for large commercial trucks. Three renewals would be enough to ensure the material used for casing is cut in half relative to the total mileage.

About 35 percent of the materials are renewables, including dandelion rubber, silicate made from rice husk ash and a string of vegetable oils and resins. Another 17 percent is polyester yarn made from recycled PET bottles, reclaimed steel and recovered carbon black.

The design should improve the efficiency of the cars themselves, Continental added. New casing, sidewall and tread patterns make the GreenConcept about 40 percent lighter than a conventional tire at about 16.5lbs, That, in turn, leads to 25 percent lower rolling resistance than the highest-rated tires in the EU. Continental estimates you’d get six percent more range from an electric vehicle.

While you might not outfit your car with these exact tires any time soon, this is more than just a thought exercise. Continental plans to gradually deploy its recycling technology starting in 2022, including the production of tires using recycled bottles.

Efforts like the Conti GreenConcept are partly meant to burnish Continental’s public image. It wants to be the most environmentally responsible tire company by 2030, and become completely carbon-neutral by 2050 “at the latest.” However, it also hints at a more holistic approach to eco-friendly cars where many components, not just the powertrain, are kinder to the planet.

Editor’s note: This post originally appeared on Engadget.

Powered by WPeMatico

We have been raised to believe in recycling, but it has mostly been a sham — only 9% of all plastic waste produced in 2018 was recycled. The beauty industry produces over 120 billion units of packaging every year, little of which is recycled. Globally, an estimated 92 million tons of textile waste ends up in landfills.

Reducing waste is key to meeting environmental milestones, and some retail firms have narrowed in on a unique approach to minimize what their customers throw away: personalization. Accurate personalization can guide consumers to the right products, reducing waste while increasing conversion and loyalty.

Reducing waste is key to meeting environmental milestones, and some retail firms have narrowed in on a unique approach to minimize what their customers throw away: personalization.

For big brands and retailers, personalization is expected to be the top category for tech investment this year. Moreover, personalization holds high appeal, with 80% of survey respondents indicating they are more likely to do business with a company if it offers personalized experiences and 90% indicating that they find personalization appealing, according to a survey by Epsilon.

Startups that deliver sustainable personalization solutions that also improve business for retailers and brands fall into three categories:

Faces are easy to map, since it’s not difficult to virtually place a lipstick color on a face, but using AR and AI to recommend skin-tone-matching makeup products has been challenging for many AR virtual try-on companies. “I’ve been searching for an intuitive foundation-shade-finder tool since launching Cult Beauty in 2008, and nothing has lived up to the experience of having a professional match you in daylight until I discovered MIME,” says Alexia Inge, founder of Cult Beauty. “There are so many variables like light, skin tones, prevalent undertones, device, screen, OS, formula density, formula oxidation, as well as preferences for coverage levels, finish, brand and skin type,” she says.

MIME founder and CEO Christopher Merkle said, “Virtual try-on has exploded in the past few years, but for color cosmetics, the technology doesn’t help solve the primary customer pain point: shade matching. From day one, I decided to focus our company’s R&D efforts exclusively on color accuracy. I want to make sure that when the consumer receives their foundation or concealer in the mail, it’s the perfect shade once applied to their skin.”

MIME’s Shade Finder AI allows consumers to take a photo of themselves, answer a few questions, then get matched with a makeup color that pairs with their skin tone. MIME helps retailers and brands increase their online and in-store purchase conversion by up to five times. More than 22% of beauty returns are due to poor customer color purchases, but Merkle says MIME can get returns as low as 0.1%.

Powered by WPeMatico

{kind=link}