Column

Auto Added by WPeMatico

Auto Added by WPeMatico

I worked at Google for six years. Internally, you have no choice — you must use Kubernetes if you are deploying microservices and containers (it’s actually not called Kubernetes inside of Google; it’s called Borg). But what was once solely an internal project at Google has since been open-sourced and has become one of the most talked about technologies in software development and operations.

For good reason. One person with a laptop can now accomplish what used to take a large team of engineers. At times, Kubernetes can feel like a superpower, but with all of the benefits of scalability and agility comes immense complexity. The truth is, very few software developers truly understand how Kubernetes works under the hood.

I like to use the analogy of a watch. From the user’s perspective, it’s very straightforward until it breaks. To actually fix a broken watch requires expertise most people simply do not have — and I promise you, Kubernetes is much more complex than your watch.

How are most teams solving this problem? The truth is, many of them aren’t. They often adopt Kubernetes as part of their digital transformation only to find out it’s much more complex than they expected. Then they have to hire more engineers and experts to manage it, which in a way defeats its purpose.

Where you see containers, you see Kubernetes to help with orchestration. According to Datadog’s most recent report about container adoption, nearly 90% of all containers are orchestrated.

All of this means there is a great opportunity for DevOps startups to come in and address the different pain points within the Kubernetes ecosystem. This technology isn’t going anywhere, so any platform or tooling that helps make it more secure, simple to use and easy to troubleshoot will be well appreciated by the software development community.

In that sense, there’s never been a better time for VCs to invest in this ecosystem. It’s my belief that Kubernetes is becoming the new Linux: 96.4% of the top million web servers’ operating systems are Linux. Similarly, Kubernetes is trending to become the de facto operating system for modern, cloud-native applications. It is already the most popular open-source project within the Cloud Native Computing Foundation (CNCF), with 91% of respondents using it — a steady increase from 78% in 2019 and 58% in 2018.

While the technology is proven and adoption is skyrocketing, there are still some fundamental challenges that will undoubtedly be solved by third-party solutions. Let’s go deeper and look at five reasons why we’ll see a surge of startups in this space.

Docker revolutionized how developers build and ship applications. Container technology has made it easier to move applications and workloads between clouds. It also provides as much resource isolation as a traditional hypervisor, but with considerable opportunities to improve agility, efficiency and speed.

Powered by WPeMatico

With the fourth quarter now upon us, every industry faces a challenge in managing a holiday production calendar that will deliver the goods. The key for startups looking to defend the quarter from disruptions is to adopt a proactive, data-driven approach to inventory management.

Here are five methods we’ve been counseling clients to adopt:

Ultimately, AI will help startups understand how myriad disruptions affect their supply chain so they can better respond with a Plan B when the unthinkable happens.

Powered by WPeMatico

Sexual harassment is, unfortunately, always in the news. Of late, it’s revelations at gaming giants and governments. Yet despite how prevalent harassment is, companies often adopt an “it can’t happen here” stance — until it does, and then there are knee-jerk reactions and crisis communications.

A better approach: recognizing how pervasive it is and planning with that in mind.

When I first started Ethena, I explained the concept of innovative harassment prevention training to my father. Like any good parent, he thought my entrepreneurial genius was actually a terrible idea and advised me to stay put at my job. But when he finally accepted that I was going to start this company, he said, “Make sure you don’t have harassment at your company. That would be bad.”

He’s not wrong. My team provides a modern compliance training platform. Since our first product was harassment prevention training, it would be pretty bad if we were talking the talk without walking the walk.

Train your team members to better understand inclusion and recognize what harassment looks like so the bar is set higher than “let’s just not get sued.”

If I could prevent workplace harassment on optimism alone, I absolutely would. But I’ve seen the data on the prevalence of workplace harassment.

A 2018 Pew survey, for example, found that 59% of women and 27% of men reported experiencing sexual harassment. And the rise of remote work hasn’t changed things. In fact, there are some indications that harassment is on the rise thanks to “keyboard courage.”

Knowing that, I’ve come to terms with the fact that these are issues we’ll likely face, so I want us to be prepared. Today’s workplace demands that leaders acknowledge gray areas and engage with uncomfortable topics; it’s how companies grow in new and healthy directions. Here’s how we think about that growth.

As a Floridian, I grew up assuming hurricanes would hit my house. We always had some plywood and canned food because when you know something is going to happen, you plan for it.

Unlike prepared Floridians, startups tend to adopt an ostrich approach when it comes to harassment. Instead of stocking the pantry, so to speak, companies wait until they’re already in a storm.

Early on, a startup is a small group of (usually homogeneous) friends, and it’s uncomfortable to acknowledge that bad things could happen. It’s much easier to hope that building a team of stellar humans is enough.

But, unfortunately, bad things do happen, because sometimes harassment is not as cut-and-dried as we are led to believe. Rather, harassment often grows from the complexities of human interactions — intent, perception, privilege and context, to name a few. It can start with a few small jokes, a colleague who gets drunkenly inappropriate every Friday, or a team that never seems to hire anyone outside of their social circle.

Then, things can escalate, and people start to realize that what they’re actually experiencing is a hostile work environment. Unfortunately, at that point, it’s really hard to right the ship because the company is suddenly 600 people and change gets harder as companies grow.

Knowing that problems are more likely as companies scale, it’s vital that teams prepare by learning how to identify warning signs early. At a bare minimum, train your team members to recognize what workplace harassment looks like and better understand inclusion so that the bar is set higher than “let’s just not get sued.”

Out of everyone at the company, managers really need to get the memo. As a company scales, senior leaders have a limited span of control, so frontline managers become the most crucial employees in either promoting or preventing inclusive workplaces. It just so happens that training is legally required in states like California and New York.

The traditional way that harassment is talked about is very binary. Either a workplace is perfectly inclusive or it’s a toxic cesspool. Obviously, it’s important to take these issues seriously, but the problem with treating every act as either fine or serious, capital-H harassment is that it gives employees a choice between bad and worse.

Let’s say Elena is on an engineering pod with Jonah, and Jonah occasionally does small things that cause her to feel less than included.

For example, they’re hiring for a new front-end engineer and Jonah always refers to this future hire as “he.” In the traditional, frowny-faced lawyer version of harassment, Elena has two options:

However, if training teaches Elena — and, ideally, everyone else on her team — to say something in the moment, Elena now has a tool she can actually use.

Next time Jonah says, “OK so when he joins … ” Elena can jump in with, “Unless you’re psychic, which seems unlikely given how poorly you did in Fantasy Football, please use ‘they’ to refer to our new hire, since we don’t know their gender.”

Did Elena need to insert the burn? Probably not, but humor can diffuse a tense situation so sure, why not? Regardless, once Elena says something, it’s on Jonah to accept her feedback and make a change; and, if team values are clear, hopefully Jonah’s colleagues will hold Jonah accountable, too.

This last lesson is only applicable after something at the company happens. Let’s say Jonah’s comments escalate, even after Elena gives feedback. Jonah consistently excludes Elena and other women from key meetings, talks over them, and when confronted, says, “Look, we all know they’re only here for diversity stats.”

If Jonah’s manager at this fictitious, problematic company does nothing, that’s the ballgame. There’s literally no amount of workshops, training, blog posts or all-hands meetings that can convince Elena that the company cares. Actions speak loudest.

The best possible version of dealing with an issue involves transparency so that people can learn from what happened and see that the company does care. Obviously, it’s hard when issues involve private information and protecting those who reported the issues, but to the extent possible, it’s crucial to have accountability.

Of course, my dad is right: Harassment at my company would be bad. But we’re preparing for it because scaling a company means rapidly increasing the number of human interactions.

Thankfully, building an inclusive company looks a lot like building a good company — preparation, feedback and accountability are managerial best practices that should be put in place early.

Powered by WPeMatico

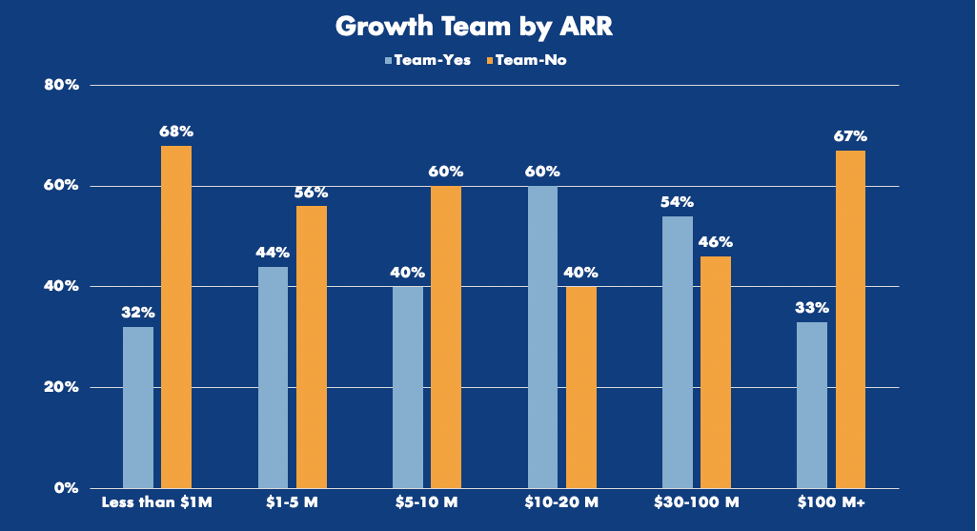

Everyone at an organization should own growth, right? Turns out when everyone owns something, no one does. As a result, growth teams can cause an enormous amount of friction in an organization when introduced.

Growth teams are twice as likely to appear among businesses growing their ARR by 100% or more annually. What’s more, they also seem to be more common after product-market fit has been achieved — usually after a company has reached about $5 million to $10 million in revenue.

Image Credits: OpenView Partners

I’m not here to sell you on why you need a growth team, but I will point out that product-led businesses with a growth team see dramatic results — double the median free-to-paid conversion rate.

Image Credits: OpenView Partners

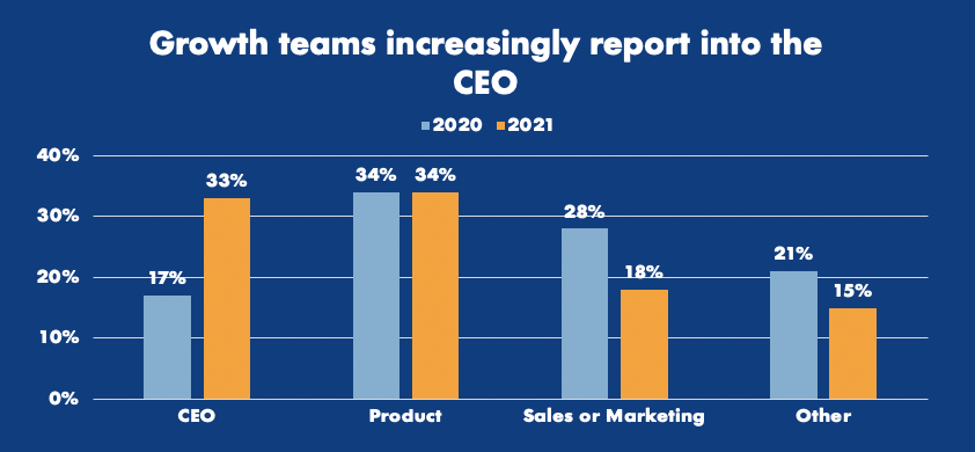

According to responses from product benchmarks surveys, growth teams have transitioned dramatically from reporting to marketing and sales to reporting directly to the CEO.

Some of the early writing on growth teams says that they can be structured individually as their own standalone team or as a SWAT model, where experts from various other departments in the organization converge on a regular cadence to solve for growth.

Image Credits: OpenView Partners

My experience, and the data I’ve collected from business-user focused software companies, has led me to the conclusion that growth teams in business software should not be structured as “SWAT” teams, with cross-functional leadership coming together to think critically about growth problems facing the business. I find that if problems don’t have a real owner, they’re not going to get solved. Growth issues are no different and are often deprioritized unless it’s someone’s job to think about them.

Becoming product-led isn’t something that happens overnight, and hiring someone will not be a silver bullet for your software.

I put early growth hires into a few simple buckets. You’ve got:

Product-minded growth experts: These folks are all about optimizing the user experience, reducing friction and expanding usage. They’re usually pretty analytical and might have product, data or MarketingOps backgrounds.

Powered by WPeMatico

Many VCs tout their mentorship and hands-on approach to founders, especially those who run early-stage startups. But in the recent era of lightning-fast rounds closing at sky-high valuations, the cap tables of early-stage startups are becoming increasingly crowded.

This isn’t to say that the value VCs bring has diminished. If anything, it’s quite the opposite — this new dynamic is forcing founders to be extremely selective about exactly who is sitting around their mentorship table. It’s simply not possible to have numerous deep and meaningful relationships to extract maximum value at the early stage from seasoned investors.

Founders should definitely pursue big rounds at sky-high valuations, but it’s important that they recognize how important it is to manage who they allow into their mentorship circles. Initially, founders should make sure their first layer consists of the real “doers” — usually angels and early venture investors who founders meet with weekly (or more frequently) to help solve some of the most granular problems.

Everything from hiring to operational hurdles all the way to deeper, more personal challenges like balancing family life with a rapidly growing startup.

This circle is where the real mentorship happens, where founders can be open and vulnerable. For obvious reasons, this circle has to be small, and usually consist of two to six people at most. Anything more simply becomes unwieldy and leaves founders spending more time managing these relationships than actually building their company.

How founders manage their VC circles can mean the difference in success or failure for a thousand different reasons.

The second layer should consist of the “quarterly crowd” of investors. These aren’t necessarily people who are uninterested or unwilling to participate in the nitty gritty of running the company, but this circle tends to consist of VCs who make dozens of investments per year. They, like their founders, aren’t capable of managing 50 relationships on a weekly basis, so their touch points on company issues tend to move slower or less frequently.

Powered by WPeMatico

In a company’s early days, the difference between C-level executives and the rest of the organization is simple — employees can walk away from a failure, but the leaders cannot. Under these conditions, certain kinds of people thrive in leadership roles and can take a company from ideation to production.

While there’s no magic formula for what works and what doesn’t, successful startups share common traits in terms of the way their foundational leadership teams are built.

We’ve all experienced what it looks like on the negative end of the spectrum — people making points simply to hear their own voice, leaders competing for credit and clashing agendas. When people would rather be heard than contribute, the output suffers. Members of a healthy leadership team are unafraid to let others have the limelight, because they trust the mission and the culture they’ve built together.

An honest self-assessment is necessary and this is something that only exceptional and selfless founders are capable of.

We are all imperfect human beings, founders included. There are always going to be moments that leaders can’t predict, and mistakes come with the territory. The right leadership team should be able to mitigate the unexpected, and sometimes make the future easier to predict. Putting the right people in the right roles early on can be the difference between success and failure — and that starts at the top.

Investors love founder-CEOs, and founders are often fantastic candidates for this role. But not everyone can do it well, and more importantly, not everyone wants to.

Startup founders should ask themselves a few questions before they lose sleep over the prospect of handing over the reigns:

An honest self-assessment is necessary and this is something that only exceptional and selfless founders are capable of. In many cases, founders decide they need outside help to fill the role. While a CEO may not be your first hire — or even one of the first five — the person you choose will ultimately occupy your organization’s most critical leadership role, so choose wisely.

What to look for: Ambitious vision grounded in execution reality. Your CEO should have hands-on experience that allows them to see around corners, predict pitfalls and identify opportunities.

What to watch out for: Leaders who lack respect for the founding vision or the ability to hire and balance an executive team quickly. A good CEO should be able to manage short-term cash flow and go-to-market needs without compromising the true north, while building a foundation and culture for the long term.

Powered by WPeMatico

I was four years old when my dad first showed me a computer. I immediately asked him if we could take it apart to see how it worked. I was hooked.

When I learned that Windows and Mac were based in the United States, I was 10. Since then, I’ve wanted to come here to launch my own tech business.

What I didn’t realize back then was that the first half of that dream — coming to the U.S. — would provide me with essential training for realizing the second half — launching a business.

As it turns out, the behaviors, attitude and mindset required to traverse the U.S. immigration system are many of the same ones required to navigate the uncertain waters of entrepreneurship.

The behaviors, attitude and mindset required to traverse the U.S. immigration system are many of the same ones required to navigate the uncertain waters of entrepreneurship.

In 2019, I launched Preflight, which makes smart and fast no-code test automation software for web applications. One big reason the business currently exists is that, in my journey to getting asylee status in the United States, I became really good at three things: accepting uncertainty, building resilience and maintaining a positive mental attitude.

I needed them all to get Preflight off the ground.

I had my first shot at making my longtime dream a reality when I was applying to college as an undergraduate. I figured if I could go to school in the United States, I could find a way to stay and start a business.

After doing some research, though, I realized that U.S. colleges were too expensive.

But I figured getting out of Turkey, my home country, would be a start. I looked around for affordable schools and saw that France had good options. So I went to France.

Unfortunately, even after three attempts, I wasn’t able to get a student visa. So I headed back to Turkey and went to college there. After graduation, I knew I had a second shot at the U.S.: a master’s degree. I applied to computer science programs and got accepted — a huge win!

I first arrived in Georgia, where I got my TOEFL certification, then enrolled at Tennessee State University, where I got a teaching assistantship.

Keep in mind, to do all this, I had to have the right visas. I needed a student visa for my master’s degree, but if I wanted to work after graduation, I’d need a work visa.

The thing is, though, I didn’t want to work at a “job.” I wanted to start my own business, which requires a different type of visa altogether.

Oh, and there was another factor at play: I was enrolled at Tennessee State from 2014 to 2016, during the lead-up to the election of Donald Trump. So in addition to trying to figure out which visa I could reasonably get, I had to deal with the fact that the rules for visas could all change in the coming months.

These experiences are similar to what many founders deal with every day in the process of launching and running a business.

We don’t know if our products will work or if they’ll find a market. We don’t know how changing regulations might affect what we’re doing. We have no idea when something like a pandemic will pull the rug out from everything we’ve built.

But we keep going anyway. In my experience, the most successful founders are the ones who don’t wait for all the pieces to fall into place — they know that will never happen. They’re the ones who do the best they can with what they have. They trust that they’ll be able to adapt and adjust when things inevitably change.

Which brings me to my next lesson.

Hearing “no” isn’t fun, especially when that “no” is about something you’ve wanted for more than a decade.

I experienced a lot of “no”s in my immigration journey, as one visa attempt after another failed. If I’d let any one of those failures stop me, I wouldn’t be where I am today — working at my own startup in the U.S.

The lesson I learned was to hear “no” as “not yet.” It’s been invaluable to me in my journey to becoming a founder.

For example: In 2014, while I was in graduate school, I learned about Y Combinator and decided that I wanted to be a part of it. Throughout grad school, I applied and got rejected three times.

The clock was ticking on my student visa, so I decided to shift my tactics. I applied to jobs at companies that were Y Combinator graduates to see what I could learn.

In 2016, I got hired at ShipBob, a Chicago-based company that was in Y Combinator’s Summer 2014 batch. I joined the team as its first full-time developer and the first one based in the States. From there, things changed dramatically.

For starters, I learned a lot. In my time with ShipBob — just two and a half years — we grew from 10 people to more than 400. I built two apps and applied to Y Combinator twice more and got rejected both times.

But in my work growing and leading a team of developers, I saw a need for a product that didn’t yet exist: a smart, fast, no-code test automation tool.

My team was spending way too much time building tests for ShipBob’s latest updates to make sure existing functionalities worked when we deployed. But when the code changed too quickly, our tests were outdated. It was incredibly frustrating.

Then we hired two quality assurance engineers and it took them four months to get 10% automated test coverage.

These problems led me to an aha moment: I could build a company to address this. A tool that is fast in test creation and can adapt to the UI changes.

That company is Preflight, and it’s the one that finally got me admitted to Y Combinator in the Winter 2019 batch. I was ecstatic when I heard that we’d been accepted. But then I realized that I couldn’t actually work on Preflight full time with my current visa status — at least, if I wanted to one day make a salary, I couldn’t.

And that brings me to my next point.

My professional life wasn’t the only thing that changed dramatically while I was at ShipBob. My immigration status also evolved.

ShipBob applied for and got me an H-1B visa, which made me eligible to work in the U.S.

But when I got accepted to Y Combinator on my sixth application, I knew I needed an alternative: If I left ShipBob to run Preflight, I would lose my H-1B and my ability to work in the U.S.

This kind of conundrum is all too familiar to most startup founders: There’s no new opportunity without a new challenge to accompany it.

So I did what any founder would do: I focused on the positive (I’d gotten into YC!) and dedicated myself to figuring out a different way to stay in the country.

First, I tried to apply for the EB-1 visa, but the required documentation was too burdensome. I don’t think any founder could prepare for that application without several months of preparation.

Then I tried the O-1. No luck.

So I asked ShipBob if I could take an unpaid sabbatical, which would let me keep my H-1B status while I attended Y Combinator and worked on Preflight. They agreed. My brothers, who had both moved to Chicago and started working at ShipBob (you’re welcome, guys!) agreed to support me (thanks, guys!).

Finally, I had a solution that worked — but only for the time being. If Preflight was successful, I’d have to find a different way to stay in the country.

Transferring my H-1B to Preflight wouldn’t work, in part because it would require me to yield 70% to 80% ownership to my co-founder and agree that he could fire me at any time.

But there was another option I’d been reluctant to lean on: asylee status. In 2016, there was an attempted coup in Turkey (that’s the official story, anyway). I won’t get into the political details, but my family and I were supporters of the movement blamed for the attempt. As a result, we were at risk of imprisonment if we stayed in Turkey — and eligible for asylum status in the U.S.

I applied, but hoped that I’d land a work visa in the meantime, partly because asylum status can take years to get approved and partly because there was no telling whether the current administration would change the rules to make me ineligible before my status came through.

When I got accepted to Y Combinator, my asylum status was pending. When my initial sabbatical from ShipBob ran out, it was still pending. I asked for an extension and got it (thanks, ShipBob!). A few months later, I figured I could not get the visa sorted. I wanted to focus on my business and use asylum-pending status, which would give me work authorization for two years. I was therefore able to work on and take a salary from Preflight.

My asylum was granted early this year, four years after applying. Getting asylee status was a big win because it meant I could realize my dream of running a business in the U.S. So I was, in some ways, at the resolution of my immigration journey — but I was just at the beginning of my journey as a founder.

Right away, I had my first experience applying all the lessons I’d learned in the last six years: We wanted to raise our first funding round. That funding would let me start taking a salary.

All told, we approached more than 100 VCs before we got a yes. But we did get that yes, and we raised a seed round of $1.2 million in September 2019.

It was a big win for Preflight, but it didn’t have the transformational power for the company I’d hoped for. That’s because, after closing our round, we didn’t focus on sales and marketing to the extent that we should have.

After several months of frustrating results, I consulted with my advisers about how to proceed. They offered me insight that seemed obvious once I had it — but that I may not have gotten on my own — which was discussing everything that’s happening internally with the investors. And the outcome was me being the CEO.

In the month and a half after I adjusted course based on my vision, I grew Preflight’s revenue 600% in just about two months.

The whole startup ethos of disrupting what’s not working to improve people’s lives is based on the premise that the world is constantly changing. The global disruption caused by COVID-19 underscored that in a major way.

Founders who accept that change is inevitable and who embrace uncertainty, develop resilience for when things go wrong, and maintain a positive mental attitude about the ups and (especially) the downs of running a startup will be the ones who succeed for the long haul.

I’ve known since I was 10 that I wanted to run a company in the United States. Given the choice, I would have opted for a much smoother road to entrepreneurship. But what I’ve discovered is that the difficult immigration path I had to follow provided exactly the training I needed to succeed in the challenging role of a founder.

Powered by WPeMatico

The startup world can be a rollercoaster. While investment continues to pour in — with both founders and investors looking for the next unicorn — the reality is that 90% of startups fail, with over half of those going under in the first three years.

I’ve founded two companies that I grew and sold (Mezi and Dhingana). I encountered many of the issues that new founders face, learned on the job, and thankfully persevered. Using the knowledge that I acquired in my previous companies, I’ve founded a third — Zeni — to try and help founders make more informed, sustainable financial decisions.

For many founders, a transformative idea and initial outside investment doesn’t translate into understanding the underlying financial complexities of running a business.

Whether you’re just wrapping your seed round, or on to Series B, avoiding these common issues is the best way to ensure that you’re set on solid ground and free to focus on your vision.

Startups go under for a variety of reasons. Some fail to achieve product-market fit in a scalable way. Many others simply run out of money. While the above two reasons are often cited as the two primary reasons for startup failure, they’re also related. If you don’t solve a market problem and don’t generate customers, you’re eventually going to run out of money.

Unfortunately, many of the startups that fail shouldn’t. They’re led by bright entrepreneurs with a great idea. But for many founders, a transformative idea and initial outside investment doesn’t translate into understanding the underlying financial complexities of running a business.

When you break down the various complexities founders face in understanding business finances, there are three primary hurdles they face:

All of the above issues put increased workload and strain on founders, which can lead to burnout. Owners, on average, spend around 40% of their working hours on tasks like hiring, HR and payroll. While hiring is integral to a founders’ day-to-day role, other administrative tasks related to finance, HR and payroll distract founders from focusing on their overall vision and goals.

The good news is that by being aware of the above issues, you can solve them and eliminate the consequences of burnout, distraction and, ultimately, failure. Let’s talk about how.

The financial decision-making and tasks of most startups start and stop with the founder. This means that bookkeeping, bill paying, invoicing, financial projections, employee payments and taxes all run into a bottleneck. Even worse, each of these functions requires another employee, vendor or third-party expert — finance firms, admins, CFOs, CPA firms — each using its own software and applications to accomplish their goals.

Each of these parties is reporting back up to the founder, who is then in charge of making sense of it all and disseminating the information to the entities that need it. This means that not only is everything slower, but often things fall through the cracks, as communication can become a serious issue.

Worse still, this creates cash flow problems, as bills go unpaid, invoices go unsent, and important financial documents are delayed. I’ve seen revenue go unreported and invoices unsent and uncollectable due to the fragmentation-bottleneck system most founders experience.

Powered by WPeMatico

Though 2021 is far from over, it’s already witnessed a record level of venture capital activity in the technology sector. With larger round sizes announced daily, founders may have their pick of term sheets — but they need to think critically and strategically about which firms to add to their cap table.

So far this year, we’ve seen $292.4 billion in venture financing across the globe, of which $138.9 billion was raised in the United States. Specific to tech companies, the capital is only accelerating: In Q2, founders raised 157% more capital compared to the same period last year, according to the latest data from CB Insights.

It’s not just that more companies are raising money — they are doing so at a higher valuation. Median seed and Series A stage valuations today stand at $12 million and $42 million, respectively, up 20% to 30% from 2020. This can be partly attributed to growing exits/M&A activity in the technology sector, a record number of IPOs and a general bullishness around technology, as well as low interest rates and liquidity in the market.

Good VCs who are aligned with a startup’s vision create more value than the dollars they bring to the table.

At a time when we are witnessing record VC activity, founders would be well served to go back to the basics and focus on the principles of fundraising when determining who sits on their cap table. Here are a few pointers for founders in that direction:

Good VCs who are aligned with a startup’s vision create more value than the dollars they bring to the table. Typically, such value is created across a few distinct functions — product, sales, domain expertise, business development and recruiting, to name a few — based on the background of the partners of the fund and the composition of their limited partners (investors in the venture fund).

Further, the right VC can serve as an authentic, objective sounding board for CEOs, which can be an asset to have as a startup navigates uncertainty and the typical challenges that come with scaling a young company. As founders assess multiple term sheets, it’s worth thinking through whether they should optimize for VCs who offer the highest valuation, or for ones who bring the most value to the table.

Running an efficient fundraising process, in part, entails holding VCs accountable to their own diligence requests. While it is unfortunately common for VCs to request a lot of data upfront, startups should share information after assessing intent and appetite on the investors’ part.

For every additional data request, founders are well within their rights (and should) check with their potential investors on where the process stands and get indicative timelines for moving forward with next steps. Mark Suster said it best: “Data rooms are where fundraising processes go to die.”

Powered by WPeMatico

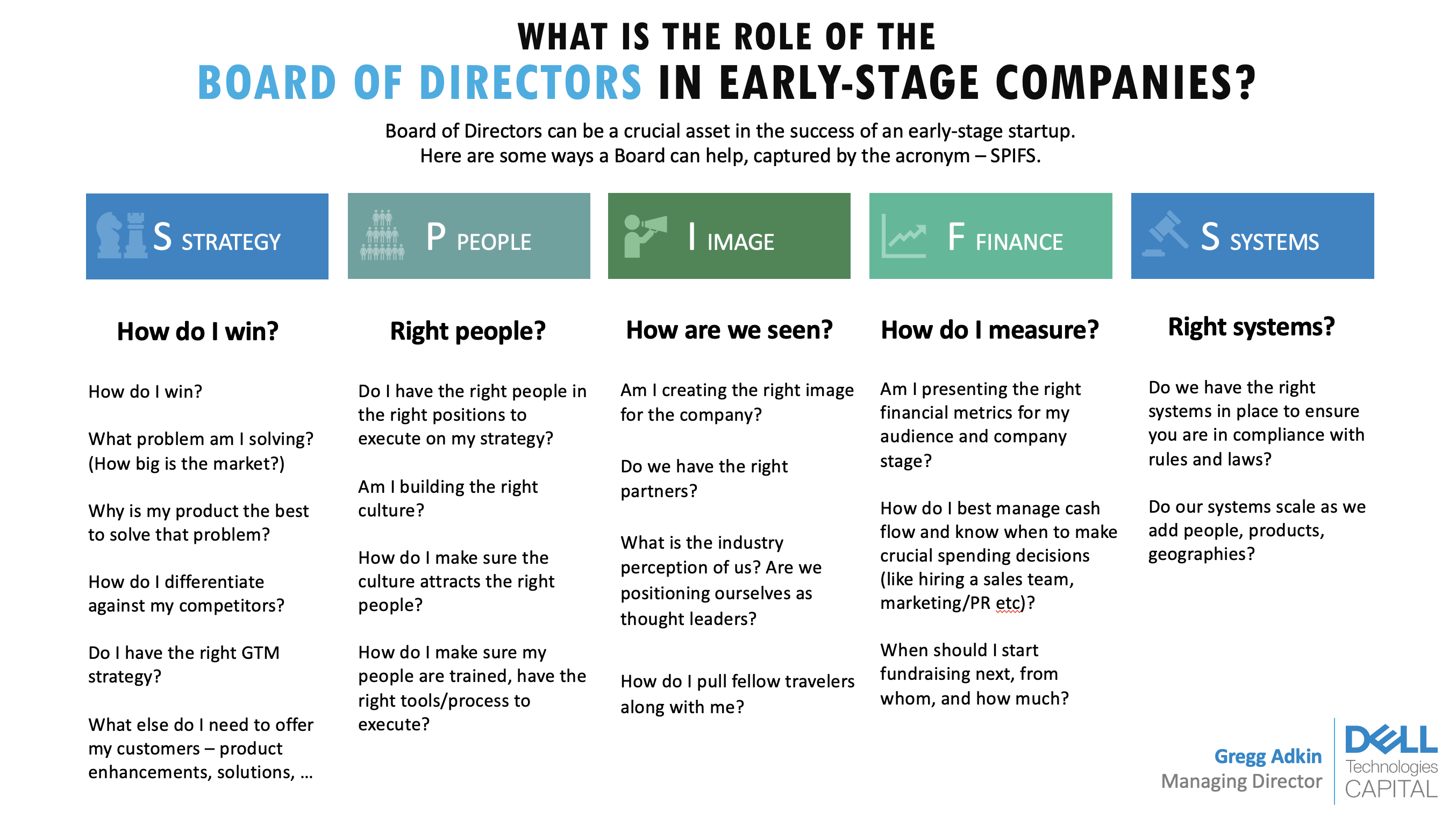

What’s the board’s role in an early-stage startup?

Startup founders frequently ask me about the role of a board of directors. A board can be a crucial asset in an early-stage startup.

Here’s a framework for how it can help drive success at your company: Strategy, People, Image, Finance and Systems for compliance, or “SPIFS.”

The board of directors helps with governance of the company. U.S. law requires that any company have one, though does not require how big it should be. By generic definition, the board of directors consists of elected individuals that represent shareholders. It is the governing body that provides company oversight and helps set business policy and strategy.

On a more practical level and in a startup environment, the board can aid in creating a successful business strategy, putting together the right management team, developing branding, building good financial habits, and avoiding legal and compliance issues. The needs and composition of the board will change depending on the startup’s stage, management and financing history (e.g., if there are preferred shareholders, investors that require a board seat and more).

Investors often ask founders about their board: It says a lot about their character, their judgment and their willingness to be challenged.

Investors often ask founders about their board for two reasons. First, it says a lot about their character, their judgment and their willingness to be challenged. The founder can typically choose who is on their board (through careful selection of investors and advisers) and negotiate a board structure they prefer.

Typically, a healthy board will have a good balance between common shareholders, preferred shareholders and independents. It also helps investors and analysts understand who will ask critical questions and give important advice to the company’s executive management, especially when the going gets tough (it inevitably does!).

After 20 years as a venture capitalist and board member, I boiled down the value of a board into five main pieces under the acronym SPIFS: Strategy, People, Image, Finance and Systems for compliance.

Image Credits: Dell Technologies Capital

Setting business strategy is one of the main ways that the board helps founders, especially if it’s their first time running a business. It is a valuable sounding board for validating that you have taken a sober account of the market and have the right plan to develop your product and acquire customers.

The board should ask these questions when guiding founders through setting strategy:

Powered by WPeMatico