challenger bank

Auto Added by WPeMatico

Auto Added by WPeMatico

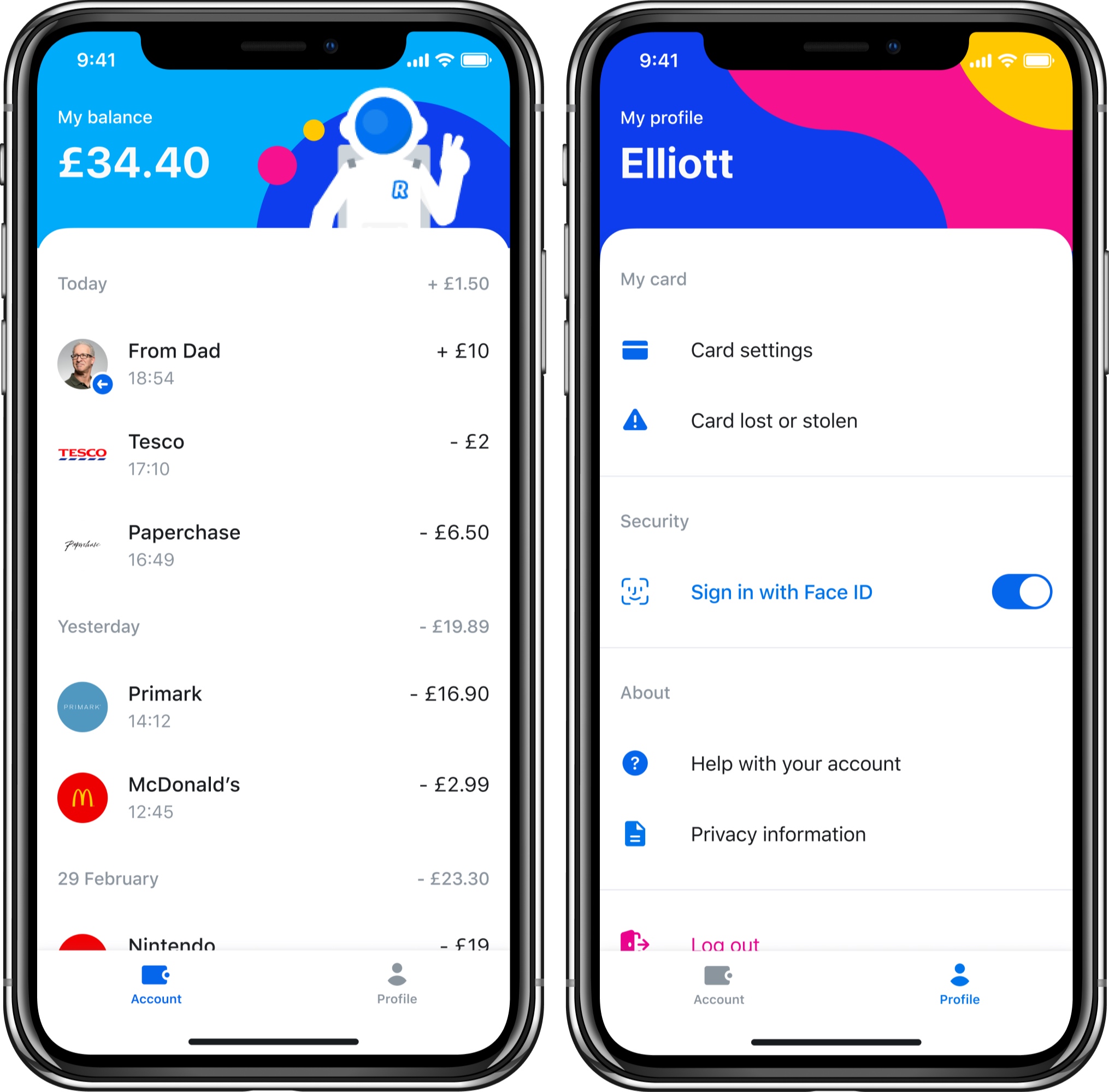

Revolut is introducing a new product specifically targeted toward kids aged 7-17 years old — Revolut Junior. Revolut Junior is a new app and service that integrates directly with the main Revolut app on the parent’s side.

Parents or legal gardians who are also Revolut users can create a Revolut Junior account for their kid. After that, your kid can download the Revolut Junior app and get a Revolut Junior card.

The new app offers a limited set of features with an interface divided in two tabs — Account and Profile. Kids can see a list of transactions in real time in the Account tab. They can configure card settings in the Profile tab. And that’s about it.

On the other end, parents can control their kids’ spending from Revolut. They can transfer money to a Revolut Junior account instantly. Parents can also access balances and transactions as well as disable some card features, such as online payments. They can also choose to receive notifications when a child is using their card.

The reason why Revolut Junior can attract a ton of users is that Revolut itself already has over 10 million users. It’s going to be easier to convince existing Revolut customers to use Revolut Junior over a custom-made challenger bank for teens, such as Kard or Step. Arguably, the biggest competitor of challenger banks for teens is still cash.

As kids grow up, chances are they’ll switch to a full-fledged Revolut account if they’ve been using Revolut Junior for years. Revolut Junior represents a great acquisition funnel as well.

Revolut Junior is only available to Premium and Metal customers in the U.K. for now. The company will eventually roll it out to more users and more countries.

Revolut plans to add more features to Revolut Junior in the future. For instance, parents will be able to set a regular allowance and financial goals. Kids will get savings options, spending reports, spending limits and more.

Powered by WPeMatico

Fintech startup Revolut has introduced a new trading feature for premium users. Starting today, Premium and Metal users can access gold exposure from the app.

Revolut works with a gold services partner (London Bullion Market Association) so that money you spend on gold exposure is backed by real gold held by this partner. In other words, you’re not going to receive gold coins in the mail. You can just invest money based on the price of gold.

The startup has been building a financial hub and already lets you purchase cryptocurrencies and buy public shares. Gold is part of a new feature called Commodities.

There are multiple ways to invest in gold. You can purchase gold exposure directly at market price, set a limit price to auto-exchange gold when it reaches a certain price or get cashback in gold for Metal customers.

At any time, you can convert your gold investment back into fiat currencies or cryptocurrencies. If you spend money with your Revolut card and you only have gold, Revolut will use your gold exposure automatically. You can also transfer gold exposure to another Revolut user.

According to the company’s website, Revolut charges a 0.25% markup when you trade gold during the week and a 1% markup from Saturday at midnight to Monday at midnight U.K. time.

It’s worth noting that gold isn’t protected through the Financial Services Compensation Scheme in the U.K. “However, in the unlikely event of Revolut’s insolvency, all Precious Metals holdings will be sold and proceeds will be credited to your e-money account,” Revolut says. You’ll have to trust their word.

Powered by WPeMatico

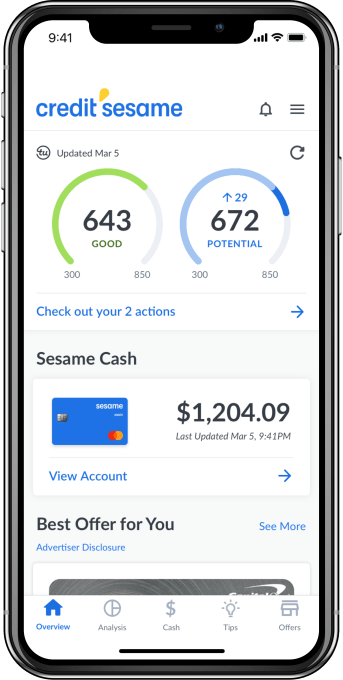

Credit Sesame is getting into digital banking. The credit and loans company, first launched at TechCrunch Disrupt in 2010, has since grown to 15 million registered users and, in 2016, achieved profitability. To date, its focus has been on helping consumers achieve financial health by taking steps to consolidate debt and raise their credit score. Now, it’s expanding to include digital banking, but with the goal of using its better understanding of its banking customers’ finances to better personalize its credit improvement recommendations.

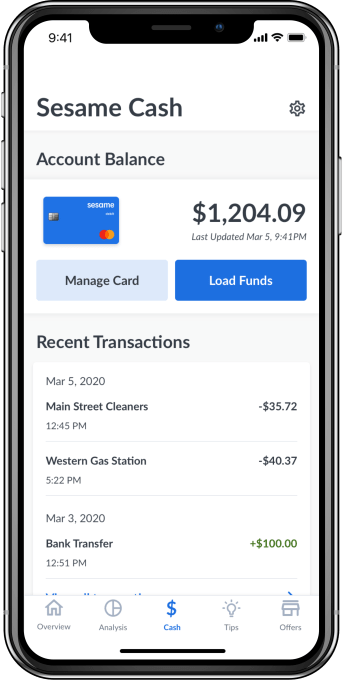

The new service, Sesame Cash, has many features found in other challenger banking apps, like a general lack of fees, real-time notifications, an early payday option, free access to a sizable ATM network, in-app debit card management and more. Specifically, Credit Sesame says it won’t charge monthly fees or overdraft fees, and it provides free access to more than 55,000 ATMs and a no-fee debit card from Mastercard.

However, the banking app also serves a secondary purpose beyond its plan to take on traditional banks. Because the company has insights into users’ finances and repayment abilities, it will be able to offer personalized recommendations, including those for relevant credit products from its hundreds of financial institution partners.

However, the banking app also serves a secondary purpose beyond its plan to take on traditional banks. Because the company has insights into users’ finances and repayment abilities, it will be able to offer personalized recommendations, including those for relevant credit products from its hundreds of financial institution partners.

Other features also differentiate Sesame Cash from rival challenger banks, including built-in access to view your daily credit score and a system that rewards consumers with cash incentives — up to $100 per month — for credit score improvements. The banking app includes $1 million in credit and identity theft protection, as well.

In the months following its launch, the company is planning to introduce a smart bill pay service that manages cash to improve credit and lower interest rates on credit balances, plus an auto-savings feature that works by rounding up transactions, a rewards program for everyday purchases and other smart budgeting tools.

“Through the use of advanced machine learning and AI, we’ve helped millions of consumers improve and manage their credit. However, we identified the disconnect between consumers’ cash and credit—how much cash you have, and how and when you use your cash has an impact on your credit health,” said Adrian Nazari, Credit Sesame Founder and CEO, in a statement. “With Sesame Cash, we are now bridging that gap and unlocking a whole new set of benefits and capabilities in a new product category. This underscores our mission and commitment to innovation and financial inclusion, and the importance we place in working with partners who share the same ethos,” he added.

Credit Sesame today caters to consumers interested in bettering their credit. The company says 61% of its members see credit score improvements within their first six months, and 50% see scores improve by more than 10 points during that time. Indeed, 20% see their score improve by more than 50 points during the first six months.

But one challenge Credit Sesame faces is that after consumers reach their goals, credit-wise, they may become less engaged with the Credit Sesame platform. The new banking app changes that, by allowing the company to maintain a relationship with customers over time.

But one challenge Credit Sesame faces is that after consumers reach their goals, credit-wise, they may become less engaged with the Credit Sesame platform. The new banking app changes that, by allowing the company to maintain a relationship with customers over time.

Credit Sesame is a smaller version of Credit Karma, which was recently acquired by Intuit for $7 billion. Since then, it has been rumored to be another potential acquisition target for Intuit, if it didn’t proceed to go public. The banking service would make Credit Sesame more attractive to a potential acquirer, if that’s the case, as it would offer something Credit Karma did not.

The company says Sesame Cash bank accounts are held with Community Federal Savings Bank, Member FDIC.

The banking service will initially be made available to existing customers, before becoming available to the general public. The Credit Sesame mobile app is a free download for iPhone and Android.

Powered by WPeMatico

German fintech startup N26 is shutting down its operations in the U.K. Customers who opened a bank account in the U.K. will have to transfer their deposits, spend everything with their card or withdraw money at an ATM, as all accounts will be automatically closed on April 15, 2020.

Many European fintech companies take advantage of a European process called passporting. It lets you apply for a license to operate as a bank or a financial service in an EU member state and then expand to all EU member states.

As you may have guessed, N26 has to exit from the U.K. banking market because it currently has a European banking license through the central bank of Germany. Passporting is going to change following Brexit.

In particular, European companies that operate in the U.K. using inward passporting have to follow a new application process in order to continue operating in the U.K.

“The timings and framework outlined in the EU Withdrawal Agreement mean that the company will in due course be unable to operate in the UK with its European banking licence,” N26 writes in a statement. N26 users in other markets won’t be affected by this change.

N26 also faces a ton of competition in the U.K. from Monzo, Starling and in some ways Revolut. It’s also possible that N26 didn’t want to invest a lot of time and money in order to set up a proper subsidiary company in the U.K. with its own banking license.

You can no longer sign up in the U.K. If you’re an existing customer, everything will work normally until April 15. You should empty your bank account, move your recurring payments to another bank, identify all your subscriptions, direct debits and deposits and move them to another bank.

On April 15, you won’t be able to access your account. Your card will be deactivated. Direct debits and deposits will bounce as well. If you have a premium subscription, N26 is going to stop charging you for your N26 You or N26 Metal subscription from March 14.

Powered by WPeMatico

Over the past year, startup banks have proven that they have a shot at disrupting retail banking. These challengers have amassed a war chest of funding, announced some ambitious international expansion plans and attracted millions of customers.

And yet, building a bank has proven to be even harder than building a startup in general. Retail banks aren’t willing to sit back and watch startups eat their lunch. Here’s a look back at the biggest moves of the year from challenger banks, some trends you should keep an eye on and the upcoming challenges for those startups.

Due to the regulatory framework and the size of the market, it is much easier to launch a challenger bank in Europe compared to anywhere else in the world. That’s why challenger banks have been thriving in Europe.

When a company gets a full banking license from the central bank of a EU country, the startup can passport its license across all EU countries and operate across the continent.

N26 raised a ton of money in 2019: last January, the Berlin-based startup announced a $300 million funding round, raising another $170 million in July. The company is now valued at $3.5 billion.

With more than 3.5 million customers in Europe, N26 announced some ambitious expansion plans. N26 is now live in the U.S. and is already planning a launch in Brazil.

Revolut has also been aggressively expanding in order to beat its competitors to new markets. In addition to its home market in the U.K., Revolut is available across Europe. In 2019, the company expanded to Singapore and Australia and currently has at least 8 million users.

While Revolut announced that it should launch in the U.S. and Canada by the end of last year, the clock ran out on that prediction. The startup has been very transparent about its expansion plans, even though it sometimes means that you have to wait months or even years before a full rollout.

For instance, Revolut announced in September 2018 that it would launch in New Zealand, Hong Kong and Japan “in the coming months.” It later became “early 2019,” then “2019.” India, Brazil, South Africa, Mexico and the UAE have also all been mentioned at some point. In other words: launching a banking product in a new country is hard.

The U.S. is a tedious market as you have to get a license in all 50 states to operate across the country

Monzo has been doing well at home in the U.K. It has attracted 3 million customers and raised £113 million (~$144m) in funding last year from Y Combinator’s Continuity fund. It is expanding to the U.S., but the rollout has been slow.

Nubank is another well-funded challenger bank. Backed by Tencent, the startup has raised a $400 million Series F round from TCV. According to the WSJ, the startup has a valuation above $10 billion.

Originally from Brazil, Nubank expanded to Mexico and has plans to expand to Argentina.

Chime is increasingly looking like the bigger player in the U.S., recently raising a $500 million funding round and reached a valuation of $5.8 billion. It only operates in the U.S.

Starling Bank and Atom Bank only operate in the U.K. Bunq is based in Amsterdam with a product tailor-made for the Netherlands, but it accepts customers across Europe.

This isn’t meant to be an exhaustive list as it’s becoming increasingly hard to cover all challenger banks.

There are a few basic features that separate challenger banks from legacy retail banks. Signing up is extremely simple and only requires a mobile app. The mobile app itself is usually much more polished than traditional banking apps.

Users receive a Mastercard or Visa debit card that communicates with the company’s server for each transaction. This way, users can receive instant notifications, block and unblock their cards and turn off some features, such as foreign payments, ATM withdrawals and online transactions.

Challenger banks usually customers promise no markup fees on transactions in foreign currencies, but there are sometimes some limits on this feature.

So how do these companies make money? When you pay with your card, banks generate a tiny, tiny interchange fee of money on each transaction. It’s really small, but it could become serious revenue at scale with tens of millions or hundreds of millions of users.

Challenger banks also offer other financial services like insurance products, foreign exchange or consumer credit. Some challenger banks develop those features in house, but many of those features are actually managed by external fintech partners. Challenger banks generate a commission on those products.

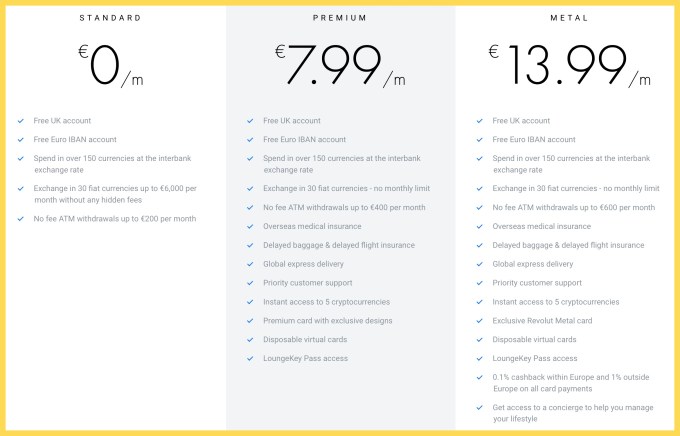

But the most promising product is premium subscriptions. While challenger banks started with free accounts and low, transparent fees, they have been selling premium subscriptions for a fixed monthly fee.

Challenger banks have become a software-as-a-service industry with a freemium component

For example, Revolut offers premium accounts for €7.99 per month with higher limits, some insurance benefits that you’d expect from a premium card and access to advanced features, such as cryptocurrencies and disposable virtual cards. There’s a super premium product for €13.99 called Metal with a metal card design, cashback on card payments and access to a concierge feature.

This seems a bit counterintuitive, but premium subscriptions have been performing well, according to discussions with people working in the industry. You pay a lot in subscription fees in order to avoid small transactional fees. (And you also get a cool card.)

Challenger banks have become a software-as-a-service industry with a freemium component. It leads to a premium positioning and high expectations from customers.

Revolut’s fees top out at €13.99/month.

Powered by WPeMatico

Meet Pixpay, a French startup that wants to replace cash when you’re handing out pocket money to your kids. Anybody who is older than 10 years old can create a Pixpay account, get a debit card and manage pocket money.

Challenger banks are nothing new, but they’re still mostly targeted towards adults. If you want to create an N26 or Revolut account, you need to be at least 18 years old. You can create a Lydia account if you’re at least 14 years old with parental consent.

Pixpay, like Kard, wants to fill that gap and offer modern payment methods to teens so that you can ditch cash altogether. Parents and kids both download the Pixpay app to interact with the service.

A few days after creating an account, your child receives a Mastercard. It offers the same features that you’d expect from a challenger bank — you can customize the PIN code, lock it and unlock it, receive a notification with each transaction and restrict some features, such as limits, ATM withdrawals, online payments and payments abroad. Pixpay also lets you generate virtual cards for online payments.

In addition to some spending analytics, users can create projects and set money aside to buy an expensive thing after months of savings. Parents can also define an interest rate on a vault account to teach children how to save money. In the future, Pixpay wants to let teens collect money after a babysitting job for instance.

As for parents, they can send money instantly from the Pixpay app. You can top up your Pixpay account with your favorite debit card and send money on a regular basis (€4 per week for instance) or for one-off payment (here’s €15 for your movie ticket and fast food).

Parents can see an overview of multiple accounts in case you have multiple children using Pixpay. Eventually, the startup wants to let multiple parents manage the account of their child, which could be useful for separated couples.

Pixpay costs €2.99 per month per card. Payments and ATM withdrawals in the Eurozone are free. Transactions in foreign currencies cost 2% in foreign exchange and ATM withdrawals outside of the Eurozone cost €2.

The startup has raised $3.4 million (€3.1 million) from Global Founders Capital. The company partners with Treezor, a banking-as-a-service platform that lets you generate cards and e-wallet accounts using an API.

Powered by WPeMatico

Fintech startup Bunq is launching a metal card called the Green Card. While some banks offer a cashback program with premium cards, Bunq is offering a special kind of “cashback”. For every €100 spent, Bunq plants a tree. The company has partnered with Eden Reforestation Projects to finance reforestation around the globe.

Manufacturing a metal card isn’t particularly environmentally friendly. That’s why the Green Card expires after six years instead of four years. It is also made of recyclable material (even though I’m not sure it’s that easy to recycle a metal card with a chip, a magnetic stripe and an NFC antenna after it expires).

Other than that, the Green Card works more or less like the Travel Card. While Bunq offers traditional bank accounts, you can order a Travel Card or a Green Card and keep your existing bank account.

The Green Card is a Mastercard without any foreign exchange fee. The company uses the standard Mastercard exchange rate but doesn’t add any markup fee.

While the Green Card is a credit card, it doesn’t work like normal credit cards. You don’t get a direct debit on your bank account once a month to cover your credit line. Instead, you have to open the Bunq app and top up your Bunq account — topping up your account with another card may incur some fees, more details here. If you don’t have enough money on your account, the transaction gets rejected like a debit card.

The Travel Card costs €9.99 to order the card. There’s no monthly fee after that. The Green Card costs €99 per year. Bunq charges €0.99 per ATM withdrawal but you get 10 free withdrawals with the Green Card.

The company is selling a limited edition today with “Founders Edition” engraved in the top right corner but the first batch is nearly sold out:

Powered by WPeMatico

Fintech startup Revolut is adding a key feature for users who want to replace their traditional bank account altogether. You can now pay with GBP direct debits. Revolut already added EUR direct debits last year.

While most people use cards to pay for goods and services in the U.K., some businesses require you to pay with direct debit. It can be a utility bill, a gym membership or a phone contract for instance.

Compared to card transactions, direct debits pull money directly from your account and transfer it to the recipient’s account. It doesn’t go through Mastercard or Visa. Some businesses love direct debits because it’s usually cheaper than card processing fees. Direct debits also don’t have an expiry date, unlike cards.

Customers from the European Economic Area can now share their GBP account details for direct debits in the U.K. Direct debits are protected against some fraud and payment errors by the U.K. Direct Debit Guarantee.

Revolut has partnered with Modulr for this feature as it uses Modulr’s API. Business customers will also be able to take advantage of direct debits. You can now pay suppliers with your account details, which could be convenient for large sums of money for instance.

Powered by WPeMatico

London-based fintech startup Revolut has two pieces of news to announce this week. First, Revolut is expanding to Singapore after a long beta period. The company already has 30,000 customers there and anyone can open an account now.

Singapore residents will be able to take advantage of all of Revolut’s core features. You can open an account from your phone, get a card and start spending anywhere in the world.

Revolut supports Singapore dollar as well as 13 other currencies. You can top up your account, and send and receive money from the app.

With a free account you can convert money in the app without any markup fee on weekdays up to S$9000 per month. You can also withdraw money anywhere in the world without any fee, up to S$9000 per month.

Premium accounts cost S$9.99 per month and Metal accounts cost S$19.99 per month in Singapore. You get higher limits and a few additional features with Metal.

Revolut is currently available in the U.K., Europe and Australia. There are 7 million Revolut customers in total. The company is still working on its launch in the U.S. and Canada for later this year.

The other piece of news is that Revolut has signed a global partnership with Mastercard. Revolut has already been working with Mastercard to issue cards, so this is an expansion of the current deal.

Revolut can now issue cards that work on the Mastercard network in any market where Mastercard is accepted, which represents around 210 countries. It doesn’t mean that Revolut will launch in 210 countries. But the startup says that the first Revolut cards in the U.S. will work on Mastercard.

It also doesn’t mean that Revolut will work exclusively with Mastercard. The company also works with Visa and recently announced a partnership deal. But at least 50% of all existing and future Revolut cards in Europe will be Mastercard branded.

It shouldn’t matter much to end customers, as I have yet to see a place that accepts Mastercard but not Visa, or Visa but not Mastercard. But Revolut is clearly using market competition to its advantage.

Powered by WPeMatico

European challenger bank Bunq is announcing a handful of updates today. You now get a better overview of your account with more insights on how you spend money. If you’re going on vacation with someone else, you can now choose to automatically add transactions to a Slice Group. There are also improvements to VAT management for business users.

Slice Groups are shared accounts for owners of the Bunq Travel Card. You can create a group with multiple Bunq users and then add expenses to the group. You can’t add money to a Slice Group directly. It is essentially a group accounting feature that lets you keep track of who paid for what, who has a positive balance and who has a negative balance.

While you could easily add Bunq transactions to a group, you still had to manually add them every time there are some new transactions. You can now turn on AutoSlice, a feature that lets you temporarily add all card transactions to a Slice Group.

In other news, Bunq wants to give you more information about your spending habits. It starts with a new feature called Bunq Insights. As the name suggests, your payments are now automatically categorized so that you can see a breakdown of what you do with your money.

When you travel, Bunq now gives you information about your travel destination, such as the exchange rate as well as tips and tricks for that country. Bunq users can add recommendations for other Bunq users.

And if you’re always wondering if you’re spending too much money after getting paid, Bunq now tries to predict how much money you’ll have left at the end of the month. The company analyzes your past transactions to predict how much you’re going to spend over the coming weeks.

Finally, Bunq is updating AutoVAT for business users who have to deal with VAT in Europe. In addition to setting aside VAT you’ll have to pay back, the app now counts how much VAT you’ve paid so far so that you know how much you can reclaim. By combining these two figures, you get the exact VAT amount for your taxes.

Powered by WPeMatico