challenger bank

Auto Added by WPeMatico

Auto Added by WPeMatico

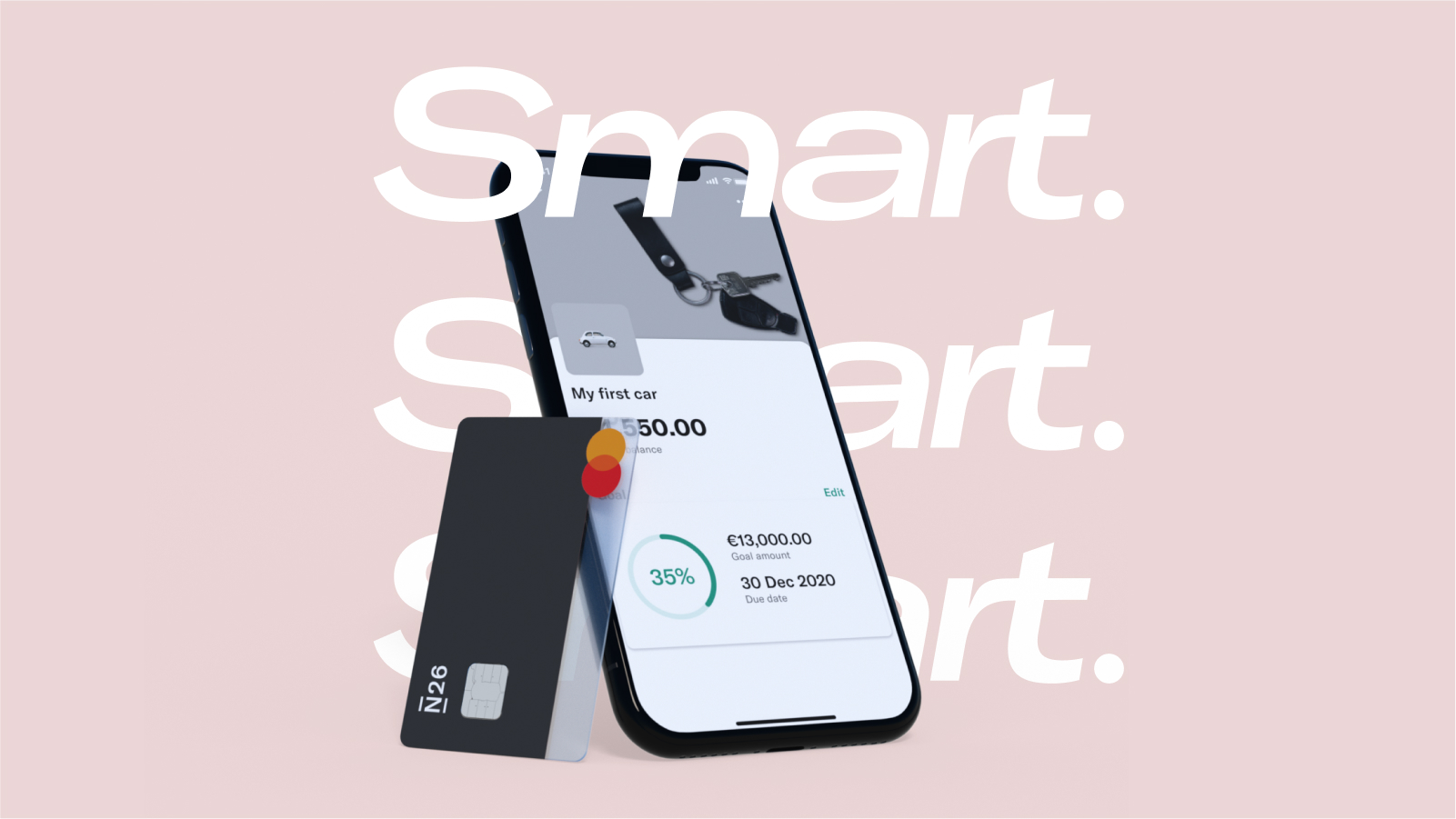

Challenger bank N26 is adding a third subscription product called N26 Smart. N26 Smart is designed to be a mid-tier subscription plan with advanced banking features but without a travel insurance package.

In Europe, in addition to the free plan, N26 already provides two subscription tiers, called N26 You and N26 Metal. N26 You costs €9.90 per month and comes with higher limits, such as five free ATM withdrawals instead of three and free withdrawals in foreign currencies.

With an N26 You account you can create sub-accounts (N26 Spaces), share them with other N26 users or use them to save money. As an N26 You subscriber, you also get a travel insurance package with medical travel insurance, trip and flight insurance and more. You can also access some partner offers.

N26 Metal is the most expensive plan and costs €16.90 per month. In addition to everything in N26 You, you get car rental insurance when you’re abroad and phone insurance. As the name suggests, you also get a metal card.

The new N26 Smart subscription costs €4.90 and works well for people who don’t need travel insurance. With an N26 Smart subscription, you can create up to 10 sub-accounts. You get five free ATM withdrawals per month. You can also call N26 support directly in addition to in-app support chat.

N26 is launching a new round-up feature for N26 Smart users. It lets you round each purchase up to the nearest Euro and save it in a separate sub-account. N26 Smart accounts also have access to colorful debit cards — the same colors as N26 You.

This is just a first step, as N26 plans to revamp its subscription products altogether. In the near future, N26 You will become N26 International. There will be more features focused on borderless banking. N26 Metal will become N26 Unlimited.

As for the free N26 Standard account, the company wants to focus on digital cards. Some users are going to switch to the N26 Smart plan to keep some of the features that they’ve been using with a free account. That move should help the company’s bottom line.

Image Credits: N26

Powered by WPeMatico

Meet Bella, a new challenger bank launching on November 30th. The company is trying to differentiate itself with two distinctive features. First, you can interact with the app using keywords and text commands. Second, Bella is trying to build a community that helps each other to differentiate its product from soulless monolithic banking services.

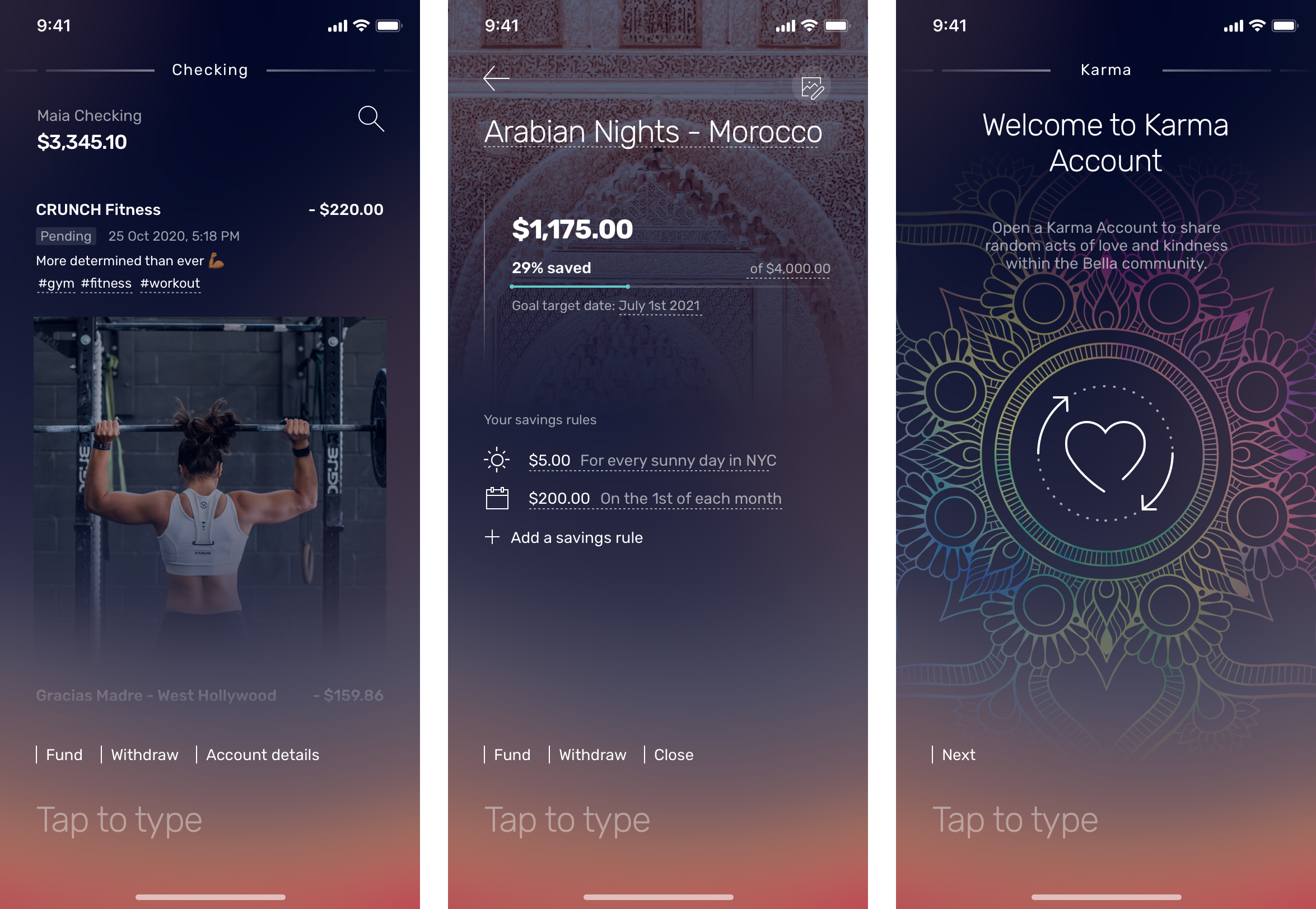

Let’s start with the basics. When you open a Bella account, you receive a rainbow debit card that works on the Visa network. You get a checking account as well as the ability to create savings accounts. Behind the scenes, Bella works with nbkc bank for the banking infrastructure. Accounts are FDIC insured up to $5 million.

Your card works with Apple Pay, Google Pay and Samsung Pay. There are no foreign transaction fees and Bella reimburses all ATM fees. There are no account minimums and service fees either.

Image Credits: Bella

But the app doesn’t look like your average banking app. There’s a text field at the bottom of the screen at all times. If you tap that field and enter a keyword, you can do all the interactions you’d expect to do. That feature is called Socratex.

This isn’t a chatbot, it’s more like a command line interface. For instance, if you type “Send”, it’ll suggest “Send money”. You can then enter an amount and hit next. After that, you can type the name of a contact, or add a contact, and then hit send.

You don’t have to find the right menu and hit the right button. The app tries to guide you so that you can construct a full sentence describing your intent. Bella uses LivePerson for that text-based interface. LivePerson is also Bella’s strategic backer.

Image Credits: Bella

And then, there is the Karma account. Over a hundred years ago in Naples, people started ordering two espressos and drinking just one. The second one would be a caffè sospeso. A poor person could ask for a caffè sospeso later that day and get a free coffee.

Bella is basically doing the same thing with its Karma account. Users can deposit up to $20 into a personal Karma account. Another user could use its Bella card and get a notification saying that their purchase is covered by someone else’s Karma account.

Similarly, Bella is introducing a randomized cashback program. The company randomly picks purchases and sends you back 5 to 200% in cashback.

When it comes to savings accounts, you can open as many savings accounts as you want and set some unconventional rules. For instance, you can set up a rule that puts some money aside when it’s sunny, when your sports team is winning, etc.

As you can see, Bella wants to introduce some randomized events so that you get surprised by your own bank account. The company wants to give back $1 million in cashback over the first four weeks on the market. Let’s see if that could turn the financial service into a viral experience.

Powered by WPeMatico

I’ve worked at TechCrunch for a little over a year, but this was one of the hardest weeks on the job so far.

Like many people, I’ve been distracted in recent days. As I write this, I have one eye on my keyboard and another on a TV that sporadically broadcasts election results from battleground states. Despite the background noise, I’m completely impressed with the TechCrunch staff; it takes a great deal of focus and energy to set aside the world’s top news story and concentrate on the work at hand.

Monday feels like a distant memory, so here’s an overview of top Extra Crunch stories from the last five days. These articles are only available to members, but you can use discount code ECFriday to save 20% off a one or two-year subscription. Details here.

Marketplaces created for B2B activity are surging in popularity. According to one report, transactions in these venues generated around $680 billion in 2018, but that figure is predicted to reach $3.6 trillion by 2024.

The COVID-19 pandemic is helping startups that innovate in areas like payments, financing, insurance and compliance.

Even so, according to Merritt Hummer, a partner at Bain Capital Ventures, “B2B marketplaces cannot simply remain stagnant, serving as simple transactional platforms.”

The startups that are first to market with innovative “adjacent services will emerge as winners in the next few years,” she advises.

For this morning’s edition of The Exchange, Alex Wilhelm interviewed three executives at cloud and SaaS companies to find out how well Q3 2020 has been treating them:

As one Twitter commenter noted, Alex doesn’t just talk to the best-known tech execs; he reaches out to a wide range of people, and it shows in the quality of his reporting.

New Regulation Crowdfunding guidelines the SEC released this week allow companies to directly raise up to $5 million each year from individual investors, an increase from the previous limit of $1.07 million.

“Life has gotten easier in other ways as well for founders pursuing this fundraising type and the platforms that seek to simplify it,” reports Lucas Matney, who interviewed Wefunder CEO Nicholas Tommarello.

Funding for seed-stage startups slumped 32% last quarter compared to 2019, so “the tide could be turning” for founders who were reluctant to raise from a giant pool of small dollars, Lucas found.

Reaching scale is paramount for software companies, so growth is a top priority.

In a guest post for Extra Crunch, Drift CEO David Cancel explains that too many SaaS and cloud companies waste time trying out a number of solutions before finding the right recipe.

“I can tell you that there absolutely is a repeatable process to building a successful SaaS business,” he says, “one that can reliably guide you to product-market fit and then help you quickly scale.”

Companies that hope to eliminate longstanding inequities in the workplace can’t just rely on doing what they think is right. Without a data-driven approach, subjective judgments and implicit bias tend to negate good intentions.

Many startups don’t hire full-time HR managers until they’ve reached scale, but this comprehensive post lays out several critical factors for creating — and maintaining — a fair pay model.

News broke this week that Airbnb plans to to raise approximately $3 billion in a public filing that would allow it to reach a valuation in the $30 billion range.

Our expert unicorn wrangler Alex Wilhelm says curious investors should ask themselves the following:

“People at the end of their career write memoirs,” Starling Bank founder Anne Boden told TechCrunch’s Steve O’Hear. “I’m at the beginning.”

In Boden’s new book, “Banking On It,” she shares the story of how (and why) she decided to found a challenger bank, eventually parting with colleagues who launched competitor Monzo.

“This is really putting down on paper where we are at the moment,” she said. “It’s been written over several years, and I’m hoping to use this to inspire a generation of entrepreneurs.”

Natasha Mascarenhas and Alex Wilhelm collaborated on Monday’s edition of The Exchange to report on how investors became less likely to fund female founders since the beginning of the COVID-19 pandemic.

Drawing on data from multiple sources, Alex and Natasha found that startups led by women and mixed-gender founding teams received 48% less VC funding in Q3 2020 than in Q2, even though overall funding bounced back.

“From fear in late Q1, to a middling Q2, to a boom in Q3,” they wrote. “It was an impressive comeback. For some.”

Natasha Mascarenhas has owned TechCrunch’s edtech beat since she came aboard at the start of 2020, just a few months before the pandemic led to widespread school closures.

She’s reported on countless funding rounds and interviewed founders and investors who are active in the space, but she recently spotted a new trend: “M&A activity is buzzier than usual.”

Alex Wilhelm shrugged off his Election Day distractions long enough to write a column that comprehensively examined fintech investment activity over the last quarter.

In Q3 2020, “60% of all capital raised by financial technology startups came from just 25 rounds worth $100 million or more,” he reports.

Are these mega-rounds funding “the next crop of unicorns?” It’s too early to say, but it’s clear that pandemic-fueled uncertainty is driving consumers into the arms of companies like Robinhood, Chime, Lemonade and Root.

In 1,316 words, Alex captures the state of play in insurtech, banking, wealth management and payments investing: “Now, we just want to see some ******* IPOs.”

Five years ago, Terri Burns was a product manager at Twitter. Today, she’s the first Black woman — and the youngest person — to be promoted to partner at Google Ventures.

In a Q&A with Natasha Mascarenhas, Burns talked about her plans for the new role, as well as her investment thesis.

“I don’t know what it actually means to build a sustainable business and venture is a really great way to sort of learn that,” said Burns.

Are founders and investors really leaving Silicon Valley for greener pastures? Now that investors are limited to virtual interactions, are they being more hands-on with their portfolio companies?

In an Extra Crunch Live chat hosted by Darrell Etherington, GV General Partner MG Siegler talked about how the pandemic is — and is not — shaping the way he does business.

“I do feel like things are operating in a pretty streamlined manner, or as much as they can be at this point,” he said.

“But, you know, there’s always going to be some more wildcards — like we’re a week away, today, from the U.S. election.”

Thank you very much for reading Extra Crunch; I hope you have a great weekend.

Powered by WPeMatico

Lunar, the Nordic challenger bank that started out life as a personal finance manager app (PFM) but acquired a full banking license in 2019, has raised €40 million in Series C funding from existing investors.

The injection of capital follows a €20 million Series B disclosed in April this year and comes on the back of Lunar rolling out Pro paid-for subscriptions — similar to a number of other challenger banks in Europe — personal consumer loans, and the launch of business bank accounts in August.

The latter appears to have been an instant success, perhaps proof there is — like in the U.K. — pent up demand for more accessible banking for sole traders. Just months since launching in Denmark, Lunar Business claims to have signed up more than 50% of all newly founded sole trader businesses in the country.

I’m also told that Lunar has seen “best-in-class” user engagement with users spending €1,100 per month versus what the bank says is a €212 EU average for card transactions. Overall, the bank has 5,000 business users and 200,000 private users across Denmark, Sweden and Norway.

Meanwhile — and most noteworthy — after launching its first consumer lending products on its own balance sheet, Lunar has set its sights on the “buy now, pay later” market, therefore theoretically encroaching on $10.65 billion valued Klarna, and Affirm in the U.S., which just filed to go public. Other giants in the BNPL space also include PayPal.

Lunar founder and CEO Ken Villum Klausen says the “schizophrenic” Nordic banking market is the reason why the challenger is launching BNPL. “It’s the most profitable banking landscape in the world, but also the most defensive, with least competition from the outside,” he says. “This means that the traditional banking customer is buying all their financial products from their bank”.

It is within this context that Lunar’s BNPL products are built as “post-purchase,” where Lunar will prompt its users after they have bought something (not dissimilar to Curve’s planned credit offering). For example, if you were to buy a new television, the app will ask if you want to split the purchase into instalments. “This does not require merchant agreements etc, and will work on all transactions both retail and e-commerce,” explains Klausen.

“We do not view Klarna as a direct competitor as they are not in the Nordic clearing system,” he adds. “Hence, you cannot pay your bills, get your salary and use it for daily banking. Klarna is enormous in Sweden, but relatively small in Denmark, Norway and Finland”.

In total, Lunar has raised €104 million from investors including Seed Capital, Greyhound Capital, Socii Capital and Chr. Augustinus Fabrikker. The challenger has offices in Aarhus, Copenhagen, Stockholm and Oslo, with a headcount of more than 180 employees. It plans to launch its banking app in Finland in the first half of 2021.

Powered by WPeMatico

Fintech startup Revolut has rolled out a handful of additional features over the past few days. The financial app lets you track all your subscriptions that you pay with your Revolut account or your card. In the U.S., Revolut is adding a savings bonus based on your purchasing habits. Finally, business customers can now order metal cards.

Let’s start with subscription tracking. For customers in Europe, Revolut is trying to make it easier to stay on top of your various subscriptions. Direct debit or card transactions are automatically marked as recurring. You can also manually mark transactions as subscriptions in case they aren’t automatically marked.

After that, you can see all your recurring payments from the app and check how much you’re spending with each merchant. If you spot a subscription that you completely forgot, you can block it — future payments will be declined.

And if you don’t have a lot of money on your account, you receive a notification warning you that a subscription payment is coming up. Subscriptions can be accessed from the Payments tab under Scheduled.

If you have multiple bank accounts, some users might switch their payment information to their Revolut card just to keep all their subscriptions in Revolut. It could boost usage.

In some markets, Revolut offers savings vaults. As the name suggests, those sub-accounts let you put some money aside and earn interest. You can round up card transactions and save spare change in a vault, you can set up weekly or monthly transactions or you can transfer money manually whenever you want.

In the U.S., customers earn 0.25% annualized percentage yield (APY) with their savings vaults. If you pay for a premium subscription, you get 0.5% APY with a Revolut Premium or Revolut Metal plan.

During the COVID-19 pandemic, you get a generous bonus on top of your normal interest rate: Revolut calculates how much you spent with your Revolut debit card the previous month; that amount is eligible for a 4.5% APY bonus.

For instance, if you spent $400 with your card last month and you have $500 in your savings vault, you’ll receive the 4.5% bonus on $400. You’ll also earn 0.25% to 0.5% on the entire savings vault.

If your savings vault balance is lower than how much you spent with your card last month, your entire vault is eligible for the bonus. Interest is calculated daily using an annualized rate and paid out the first business day of the following month.

Once again, the new feature should boost engagement in the U.S. for both card transactions and savings vaults. Revolut has 13 million customers in total, including 150,000 in the U.S.

People care about metal cards. That’s why many fintech startups now offer expensive monthly plans with metal cards — N26, Bunq, Curve and Revolut.

But Revolut Business customers have been limited to plastic cards (or virtual cards). If you use Revolut Business for your company, you can now order metal cards depending on your plan.

Revolut Business customers with a free account or a freelancer account can’t order metal cards. Customers on the Grow, Scale or Enterprise plans receive one, two or five metal cards respectively.

And if you want to order more metal cards, it costs £49 per card. You can choose a card among five different colors — black, gold, rose gold, space grey and silver.

Other than a new look, metal cards don’t differ from standard cards. It’s a small perk that you get with a paid plan. Revolut has managed to attract 500,000 customers for its Revolut Business product.

Powered by WPeMatico

Fintech startup N26 is announcing some changes in the leadership team with two new C-Level hires. First, Adrienne Gormley, pictured above, is joining the company as chief operating officer, replacing Martin Schilling who left the company in March 2020. Second, Diana Styles, pictured below, will become N26’s chief people officer.

Gormley has spent the last six years working for Dropbox in Dublin. She was the VP of Global Customer Experience as well as the head of EMEA for Dropbox. Previously, she’s worked at Google and Transware.

At N26, she will be in charge of a large chunk of the company, from customer service, to business operations, service experience and workplace division.

Styles has many years of human resources experience. She was the senior vice president of Human Resources, Global Sales and Brands at Adidas. Similarly, as chief people officer, she will oversee important aspects of the company, such as employee retention, leadership development, talent acquisition and more.

Both will be based in Berlin and report to the company’s co-founder and chief financial officer Maximilian Tayenthal. N26 has grown quite a lot over the past few years as there are now 1,500 employees working for the company.

Image Credits: N26

Powered by WPeMatico

Meet Fondeadora, a fintech startup based in Mexico City that wants to build a full-stack neobank. The company just raised a $14 million Series A round led by Gradient Ventures, Google’s AI-focused venture fund. Founded in 2018, the company already manages 150,000 accounts and is adding $20 million in deposits every month.

Mexico represents a massive opportunity for a challenger bank as many people still rely on cash for most of their transactions. Given that all countries are progressively switching to card and digital payments, it seems like the right time to launch Fondeadora .

Y Combinator, Scott Belsky, Sound Ventures, Fintech Collective and Ignia are also participating in the funding round.

“We launched the first crowdfunding platform in Mexico about 10 years ago,” co-founder and co-CEO Norman Müller told me. “About 50% of card transactions failed in the system.”

That platform was also called Fondeadora. After a deal with Kickstarter, Müller and Fondeadora co-founder René Serrano went back to the drawing board and thought about the problems they had while operating the crowdfunding platform. It became Fondeadora as we know it today, a challenger bank that wants to improve the banking experience in Mexico.

The team traveled across Mexico to find a bank charter that they could use. “We acquired the charter, it was owned by a group of tomato farmers in Mexico. Twenty years ago, the government gave about 10 charters to create financial inclusion,” Müller told me.

The company launched its banking service after that. You can open an account without visiting a branch. You then receive a Mastercard debit card. You can choose to receive notifications after each purchase, lock and unlock your card, send instant transfers to other users and more. There are no monthly subscription fee and no foreign transaction fee.

Up next, Fondeadora wants to democratize savings accounts. “Cash has a great UX and UI. You can touch it, you can store it in your drawer. But as a medium to generate income, it’s terrible,” Müller told me.

In the coming months, you’ll earn interest on your deposits in your Fondeadora account. “We’re investing in government bonds, it’s a very secure type of instruments. In Mexico, you can get 5% or 6% interest rate,” Müller said. The startup could allocate a small portion of deposits to medium-risk investments as well.

Image credits: Fondeadora

Powered by WPeMatico

Venture capitalists and other investors have poured capital into fintech startups around the world in recent years, including a record number of rounds worth $100 million or more in the second quarter of 2020. In Q2 2020 venture-backed fintech startups raised 28 nine-figure rounds, underscoring the scale of the bet investors are making on fintech’s long-term success.

The Exchange explores startups, markets and money. You can read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Inside that fintech wave are various hubs of activity, including payments tech, investing and banking. That last category has helped give rise to so-called neobanks, startup banking entities that offer mobile-first, consumer-friendly banking tools and services. Given the old-fashioned nature of banking in many countries (and how far out of reach banking remains for many) neobanks have seen strong uptake by users in recent years.

And the startup cohort has raised oceans of capital to help fuel its growth. In America, Chime was most recently valued at $5.8 billion after raising hundreds of millions in late 2019. More recently, neobank Revolut added $80 million to its Q1 2020 round worth $500 million. Revolut is also worth north of $5 billion. Monzo is well-funded (albeit at a recent valuation reduction), Latin America-focused NuBank is worth $10 billion, according to Crunchbase, Starling recently raised another £40 million, while Germany’s N26 is worth over $3 billion after its most recent nine-figure round.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

From the fundraising perspective, then, neobanks are killing the game. And thanks to recent tailwinds from the COVID-19 pandemic that have bolstered interest in savings-related products, many of the same entities could be enjoying a strong year thus far. But recent self-reporting of some neobank’s 2019-era results details ample red ink — perhaps more than we might have anticipated.

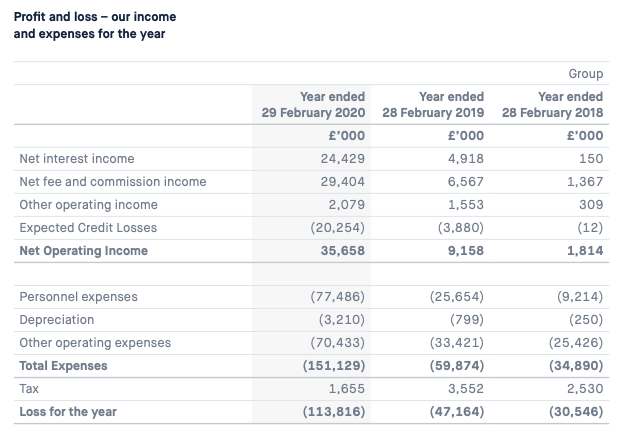

Of course, startups don’t raise money for fun; they raise it to invest it in their operations and drive scale. So, we knew that these megafundraisers were losing money on purpose. All the same, let’s peek at the economics of several neobanks, as their now dated and thus not at all current results can provide useful context on two points: Why investors are excited to put their capital to work in neobanks, and why neobanks always seem to have another check to announce.

To prevent my receiving unhappy emails from irked fans of these companies, please bear in mind that we’re looking several quarters back when observing the following results.

It would be lovely to have more recent data, but with European neobanks reporting their — roughly — 2019 results in recent weeks, this is what we have. We are going to parse the numbers, but we will not conflate past performance with current results. We do not know much about 2020 neobank financial performance.

Anyhoo, to the numbers. You can read the full documents from Monzo here, Starling here (or here, if that link is struggling) and Revolut here.

Let’s start with Monzo, which has a clear set of figures for us to peek at:

Image Credits: Monzo

Powered by WPeMatico

Point, a new challenger bank in the U.S., is launching publicly today with an invite system. While Point is technically providing a bank account, the company focuses on rewards associated with a debit card.

“I started Point as a solution about everything that is frustrating and complicated about credit cards. The incentives between credit card companies and cardholders are misaligned,” Point co-founder and CEO Patrick Mrozowski told me.

When Mrozowski first got a credit card, he was spending a ton of money to reach a certain level of spending and unlock the sign-up bonus. At the end of the month, he ended up with credit card debt for no valid reason.

“What would American Express look like today?” he says to sum up Point’s vision. It comes down to two important principles — being in charge of your budget so that you don’t end up with debt and unlocking rewards from brands that you actually interact with.

Many challenger banks want to provide a simple banking experience for the underbanked. Point doesn’t have the same positioning. Creating a Point account is more like joining a membership program.

When you sign up, you get a debit card with some level of insurance as it’s a Mastercard World Debit card. You can expect some trip cancellation insurance, rental car insurance, purchase insurance, etc.

As the name of the startup suggests, you earn points with each purchase. You get 5x points on subscriptions, such as Spotify and Netflix, 3x points on food, grocery deliveries and ride sharing, and 1x points on everything else. Points can be redeemed for dollars — each point is worth $0.01. In addition to that, Point is going to create a feed of offers with discounts, content, events and more.

Due to its premium positioning, Point isn’t free. You have to pay $6.99 per month or $60 per year to join Point. Point doesn’t charge any foreign transaction fees.

You can connect your Point account with another bank account using Plaid. It lets you top up your account using ACH transfers. Behind the scenes, Point works with Radius Bank for the banking infrastructure, an FDIC-insured bank.

The company announced earlier this month that it has raised a $10.5 million Series A led by Valar Ventures with Y Combinator, Kindred Ventures, Finventure Studio and business angels also participating.

Image Credits: Point

Powered by WPeMatico

Fintech startup Revolut just announced that it has raised $80 million as part of its Series D round that it announced in February. The new influx of funding comes from TSG Consumer Partners.

In February, Revolut raised a $500 million led by TCV at a $5.5 billion valuation. Today’s new funding extends that funding round to $580 million — the company says the valuation remains the same.

If you’re not familiar with Revolut, the company is building a financial service to replace traditional bank accounts. You can open an account from an app in just a few minutes. You can then receive, send and spend money from the app or use a debit card. Revolut also lets you exchange currencies.

The startup expanded beyond that simple feature set and now wants to become a financial hub, a super app for all things related to money. For instance, you can insure your phone, get a travel medical insurance package, buy cryptocurrencies, buy shares, donate to charities and save money from Revolut.

The company says it’ll use the investment to add new features in the U.S. and roll out banking operations across Europe — you can expect local banking details in multiple European countries. Eventually, Revolut also plans to offer credit products across Europe.

In addition to that, Revolut is working on a subscription management tool. It lets you see all your active subscriptions, cancel them from Revolut and receive alerts when a free trial ends.

There are now 12 million registered users on Revolut.

Powered by WPeMatico