challenger bank

Auto Added by WPeMatico

Auto Added by WPeMatico

Société Générale is acquiring French startup Shine. Terms of the deal are undisclosed. According to a source, Shine is getting acquired for around €100 million in an all-cash deal (around $112.6 million).

The startup had previously raised €10.8 million ($12.2 million) in total from Daphni, Kima Ventures, XAnge and various business angels.

If you’re not familiar with Shine, the startup has been building a challenger bank for freelancers and small companies in France. It lets you create a business account, get a debit card and take care of some of the most boring administrative tasks.

For instance, Shine helps you incorporate your company and also lets you create invoices directly from the app. You can send a link to your client, you get a notification when your client opens the invoice and they can view your Shine IBAN directly on the invoice.

And because the invoicing tool is integrated with your business bank account, your invoices are automatically marked as paid in the app.

When it comes to receipts, you can also open a card transaction and attach a receipt to that transaction. This way, all accounting information remains in the same app. If you’re working with an accountant, you can set up an automatic export of receipts, invoices and transactions once per month.

But the best feature of Shine is that it helps you stay on top of paperwork. You receive notifications to remind you that you should pay your taxes, you can see how much money will be left once you paid your taxes and more.

And it’s been working well with 70,000 freelancers and very small companies using Shine for their bank account. But Shine is built on top of Treezor, a banking-as-a-service company that provides financial services and debit cards to other fintech companies. At this scale, it would make sense for Shine to build its own infrastructure.

Shine has taken a different decision and is joining Société Générale, which also happens to be the company that acquired Treezor a few years ago.

Shine will operate independently from Société Générale and will still accept new customers — the two co-founders are staying at the helm of Shine. But the two companies have plans to cross-promote their respective offerings.

Société Générale could offer Shine to its business customers. And as freelancers start working with other people and turn their small independent business into a full-fledged company, Shine could also tell its customers to choose Société Générale for their business bank account.

Shine will also take advantage of Société Générale’s banking license and products. As a Shine customer, you could imagine getting a credit line from Société Générale. Having a banking giant behind you could greatly improve Shine’s offering. Now, let’s see if Société Générale manages to boost the potential of Shine.

Update: A spokesperson from Société Générale and a spokesperson from Shine have refuted the price of the acquisition. According to new information that I obtained from sources, the acquisition is happening over several tranches with the first payment currently happening. Combined, those tranches represent a total amount of around €100 million. In addition to that, founders will receive cash incentives if they can achieve certain goals over several years.

Image Credits: Shine

Powered by WPeMatico

Zopa, the 15-year-old peer-to-peer lending company, is announcing that it has been awarded its full U.K. bank licence, as it gears up to launch a fixed-term savings account, followed by a credit card.

Dubbed “Zopa Bank,” the new challenger bank will sit alongside its existing peer-to-peer lending business, under Zopa Group, creating what the veteran fintech previously described as the first hybrid peer-to-peer and digital bank offering.

Zopa had provisionally acquired a U.K. bank license in December 2018 “with restrictions,” the first major milestone in the licensing process. The full license, which required Zopa to raise a further £140 million late last year in a round led by IAG Capital in order to meet capital required to become a bank, means it can now launch more widely.

“The Zopa Fixed Term Savings Account offers a competitive rate over 1-5 years at a time when rates are at a historic low,” says the upstart bank. “The account can be opened in as little as 7 minutes online and is protected by the Financial Services Compensation Scheme (FSCS) up to £85,000.”

Next, Zopa says it plans to introduce a credit card in the coming months, which will include “innovative new features designed to put customers in control of their borrowing.”

“The card will address the needs of customers who have had to put up with poor service and unclear pricing from their existing card providers. These new products will sit alongside Zopa’s existing offering of personal and auto loans and investment products,” says Zopa Bank.

Whether or not a new challenger bank, even one with Zopa’s established brand, can cut through the noise this late in the race remains to be seen. The challenger bank space in the U.K. is crowded, to say the least, including burgeoning household names like Monzo and Starling, and to a lesser extent, Tandem, which on the surface looks to be Zopa’s most direct non-legacy competitor.

Powered by WPeMatico

Meet Vivid, a new challenger bank launching in Germany that promises low fees and an integrated cashback program. The two co-founders, Alexander Emeshev and Artem Yamanov, previously worked as executives for Russian bank Tinkoff Bank.

Vivid doesn’t try to reinvent the wheel and is building its product on top of well-established players. It relies on solarisBank for the banking infrastructure, a German company with a banking license that provides banking services as APIs to other fintech companies. As for debit cards, Vivid is working with Visa.

If you live in Germany and want to sign up to Vivid, you can expect a lot of features that you can find in other challenger banks, such as N26, but with a few additional features. Vivid users get a current account and a debit card. They can then manage their money from the mobile app.

The physical Vivid card doesn’t feature any identifiable details — there’s no card number, expiry date or CVV. Just like Apple’s credit card in the U.S., you have to check the mobile app to see those details. Every time you make a purchase, you receive a notification. You can lock and unlock your card from the app. The card works in Google Pay but not yet in Apple Pay.

In order to make money management easier, Vivid lets you create pockets. Those are sub-accounts presented in a grid view, like on Lydia or N26 Spaces. You can move money between pockets by swiping your finger from one pocket to another. Each pocket has its own IBAN.

You can associate your card with any pocket. Soon, you’ll also be able to share a pocket with another Vivid user. Like on Revolut, you can exchange money to another currency. The company adds a small markup fee but doesn’t share more details.

As for the cashback feature, the startup focuses on a handful of partnerships. You can earn 5% on purchases at REWE, Lieferando, BoFrost, Eismann, HelloFresh and Too Good To Go, and 10% on online subscriptions, such as Netflix, Prime Video, Disney+ and Nintendo Switch Online. While it’s generous, you’re limited to €20 maximum in cash back per month.

Interestingly, Vivid also wants to bring back Foursquare-style mayorship. If you often go to the same bar or café and you spend more than any other Vivid user over a two-week window, you become the mayor and receive 10% cashback.

Vivid has two plans — a free plan and a Vivid Prime subscription for €9.90 per month. Prime users receive a metal card, more cash back on everyday purchases and higher withdrawal limits.

The company plans to launch stock and ETF trading in the coming months. Vivid also plans to expand into other European countries this year.

Vivid is entering a crowded market, but already offers a solid product if everything works as expected. It’s going to be interesting to see how the product evolves and if they can attract a large user base.

Powered by WPeMatico

Fintech startup Revolut has expanded its open banking feature to Ireland. The feature first launched in the U.K. back in February. Once again, the startup is partnering with TrueLayer to let you add third-party bank accounts to your Revolut account.

The feature launch also marks the launch of TrueLayer in Ireland. For now, Revolut users can only link their Revolut account with AIB, Permanent TSB, Ulster Bank and Bank of Ireland. Revolut and TrueLayer will add support to other banks in the future. Revolut currently has 1 million customers in the Republic of Ireland.

The idea behind open banking is quite simple. Many online services rely on application programming interfaces (APIs) to talk to each other. You can connect with your Facebook account on many online services, you can interact with other services from Slack, etc.

Financial institutions have been lagging behind on this front, but it is changing thanks to new regulation and technical updates. With open banking, your bank account should work more like a traditional internet service.

When you connect your bank account with Revolut, you can view your balance and past transactions from a separate tab that lists all your linked accounts. Users can also take advantage of Revolut’s budgeting features with their bank accounts.

As TechCrunch’s Steve O’Hear noted when he first covered Revolut’s open banking feature, Revolut was originally authorized for Account Information Services (AIS) by the U.K. regulator, the Financial Conduct Authority. It lets you access and display information from other financial institutions.

But the startup now has permission to carry out Payment Initiation Services (PIS). It means that you’ll soon be able to initiate transfers from your bank account directly from Revolut. It should make it much easier to top up your Revolut balance, for instance.

While this feature might seem anecdotal, Revolut wants to build a comprehensive financial hub for all your financial needs — a sort of super app for everything related to money. With open banking, you theoretically no longer have to open your traditional banking app.

Image Credits: Revolut

Powered by WPeMatico

Monzo, the U.K. challenger bank with more than 4 million customers, has confirmed it has closed £60 million in top-up funding.

Backing the round are existing investors Y Combinator, General Catalyst, Accel, Stripe, Goodwater, Orange, Thrive and Passion Capital, along with new investors Reference Capital and Vanderbilt University.

One of fintech’s worst-kept secrets, the down round sees the bank take a 40% hit in its paper pre-money valuation compared to its previous round, now priced at £1.24 billion.

That’s likely a reflection of the current funding climate amidst the coronavirus crisis, with Monzo having to raise a bridge round at quite possibly the worst time.

I also understand from sources that a number of Monzo’s later-stage investors played hardball, in a bid to force down the challenger bank’s ticket price, perhaps after investing at the height of the funding market pre-COVID-19. What is also interesting about the new round is that the share price is the same as the bank’s last equity crowdfund, meaning that the most recent armchair investors haven’t seen a paper loss.

Monzo is also disclosing that its business banking product has now reached 25,000 signups. Launched officially in March, the business bank account is aimed at sold traders and SMEs, with both free and premium paid-for versions available, offering various feature sets.

Meanwhile, it has been a turbulent time for Monzo, as it, along with many other fintech companies, tries to insulate itself from the coronavirus crisis and resulting economic downturn.

Planned layoffs in the U.K. were communicated internally earlier this month — up to 120, but now thought to be around 80. It followed earlier U.S. layoffs and the shuttering of its Las Vegas-based customer support office, and almost 300 U.K. staff being furloughed.

Like other banks and fintechs, the coronavirus crisis has resulted in Monzo seeing customer card spend reduce at home and (of course) abroad, meaning it is generating significantly less revenue from interchange fees. The bank has also postponed the launch of premium paid-for consumer accounts, one of only a handful of known planned revenue streams, alongside lending, of course, and the more recent business banking.

Separately, in May, Monzo co-founder Tom Blomfield announced internally that he was stepping down as CEO of the U.K. challenger bank to take up the newly created role of president. His replacement is current U.S. CEO TS Anil, who now also holds the title of “Monzo UK Bank CEO,” subject to regulatory approval.

Powered by WPeMatico

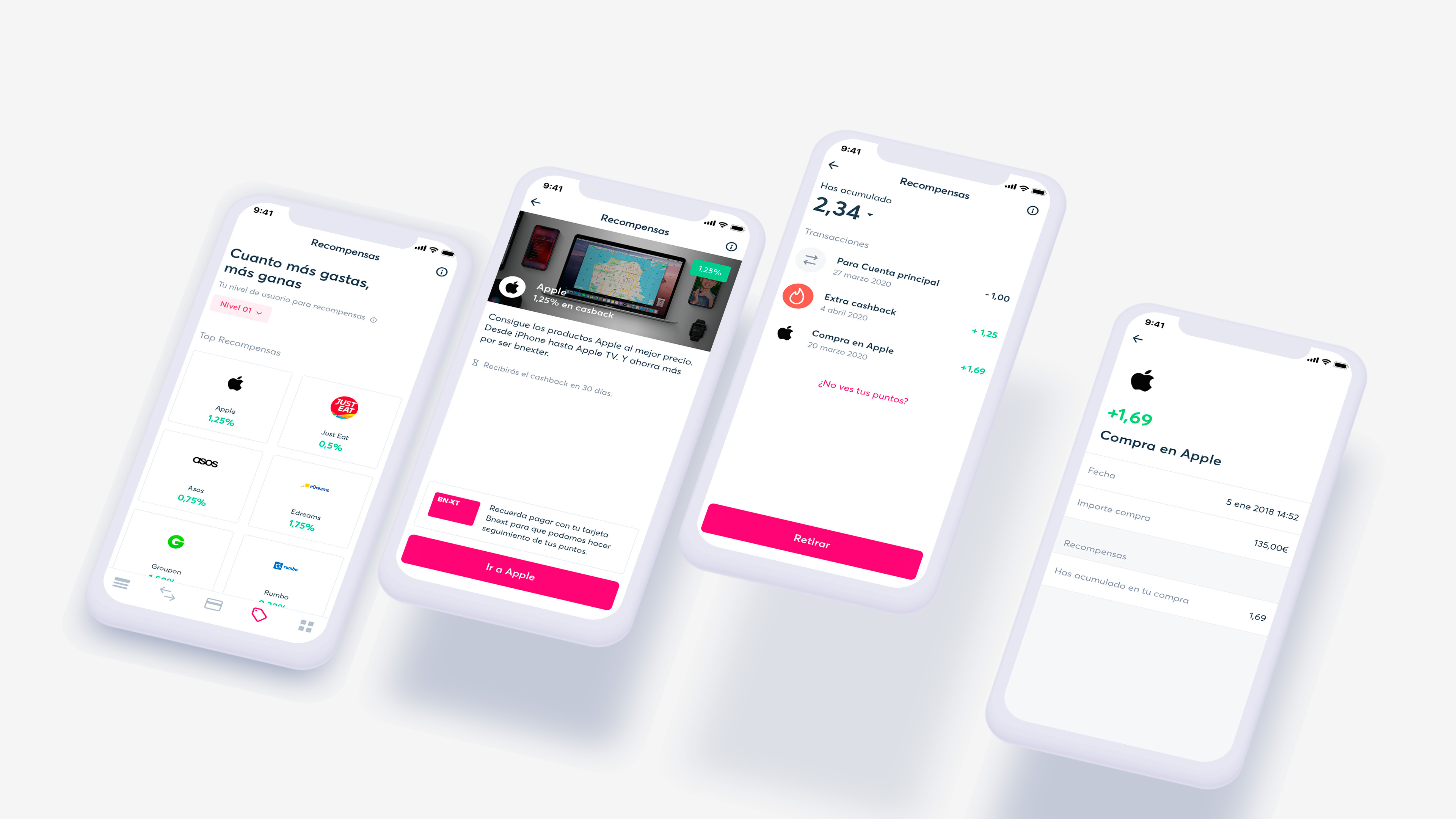

Spanish startup Bnext is revamping its cashback program so that you can buy from partner stores directly from the Bnext app and get some money back. The company has partnered with Button and the feature is available as an open beta.

Traditional cashback portals are a bit clunky. When you find an offer that gives you 2% of your money back, you click on the offer, get redirected to the partner site and hope that your purchase will be registered. A bit later, you get some money back on the cashback website, which you need to cash out to your bank account.

If you’re using Bnext as your bank account, you’ll be able to access rewards directly from your banking app. In addition to that, you don’t get redirected to another site as you purchase goods directly from the Bnext app.

There are multiple levels. If you’re making your first purchase through the feature, you get 1% in savings on average. If you’ve made more than three purchases over the past 30 days, you get 3% in savings on average. In order to reach level 3, you need a premium Bnext subscription. With that level, you get 5% in savings on average.

Partners include AliExpress, Booking.com, eDreams, Europcar, Nike, Just Eat and more. Eventually, the startup wants to let you earn rewards from in-store purchases as well. Bnext is creating a new revenue stream with this feature as the startup will keep a share of the revenue from each transaction.

Bnext provides current accounts and payment cards. You can receive notifications for each transaction with your card, and temporarily lock and unlock your card. You don’t pay any foreign transaction fee as long as you spend less than €2,000 per month with a standard account.

The company has also put together a marketplace of fintech products. You can earn interest by lending money to small companies on October, get a loan, an insurance product and more.

Earlier this year, the startup expanded to Mexico. The company plans to roll out rewards in Mexico soon. Bnext has managed to attract a bit less than 400,000 users.

Powered by WPeMatico

Challenger bank Bunq is adding a new feature that lets you donate to charities directly from the app. In addition to that, Bunq is also in the process of redesigning its app. The company is launching a public beta test to get feedback from its users.

Other fintech startups, such as Revolut and Lydia, have launched donation features in the past. But in those cases, startups have selected a handful of charities.

Bunq has chosen a different approach, as you can create your own donation campaigns in the app. As long your local charity has an IBAN number, you can add it to Bunq’s donation feature. You can even add a local business in case you want to help them stay in business.

You can then invite other people to donate to your charities. You can also track the total amount of your donations, as well as the total donations from the entire Bunq user base.

The company has also been working on the third major version of the app. In order to test it before the public release, Bunq is launching a public beta program. The first build will roll out in the coming weeks.

In order to simplify navigation, Bunq has tried to remove clutter by focusing on one main button on each page. The app will be divided in four main tabs.

The first tab, called “Me,” will feature all your personal information — personal bank accounts, savings goals, etc. On the second tab, called “Us,” you can see information about Bunq, such as total investments and total donations. The third tab features your profile information.

Finally, the fourth tab is a dedicated camera button. It lets you scan invoices and receipts, which could be particularly useful for business customers. I’m not sure a lot of people use that feature, but things could still change before the final release.

Powered by WPeMatico

Consumer fintech startups were massively successful in 2019, attracting millions of new users and disrupting traditional retail banks and financial services with mobile-first, consumer-oriented products. Despite the economic downturn in public markets and the massive wave of cuts at public and private companies in recent weeks, fintech startups have been raising a ton of money.

It feels like they’re all building a war chest to survive the economic winter as traditional banks continue to iterate so they can catch up and offer more user-friendly services. This is not the time to raise fees, slow down on product development or plans to acquire new users.

Back in January, I looked at challenger banks and their growth trajectories, but since then, they have managed to attract even more customers. According to the most recent figures:

And that’s without mentioning Starling Bank, Atom Bank, Bunq, Bnext, Paysend, etc. At some point, there will be as many challenger banks as non-challenger banks — perhaps we shouldn’t call them challenger banks anymore.

Beyond these startups, trading app Robinhood recently reached 13 million users, international payments startup TransferWise has 7 million customers and cryptocurrency exchange Coinbase has 30 million users.

Powered by WPeMatico

Stripe and Shopify have transformed the face of commerce for small business users, yet when it comes to putting that cash somewhere, SMBs have found that the banking options aren’t quite as transformative.

Wise is a new challenger bank built specifically for small businesses. The startup is aiming to insert itself as an essential service in the small business repertoire by bundling banking with payment services powered by Stripe. Customers can receive payments, manage their cash and pay employees all via Wise’s app.

CEO Arjun Thyagarajan tells TechCrunch that his company has closed a $5.7 million seed round led by Base10 Partners . Abstract Ventures, Backend Capital, The Fund and Two Culture Capital also participated in the round.

While the advent of challenger banks has helped drive plenty of innovation on the consumer banking side, says Rexhi Dollaku, a principal at Base10 who led the Wise deal, “very little of that innovation has happened in the business banking context.”

Thyagarajan and his investors hope that the startup can keep churn low by embedding a wider scope of financial services products inside its core product, expanding beyond the traditional scope of banking features by offering functionality to power things like payroll and accounting.

Rather than plunging into direct customer sales, Wise is partnering with behemoth platforms like Shopify to onboard small businesses where they already are. “If you look at other [banking] options out there, they’re going direct to the customer; what we’ve learned is that it is better to partner,” Thyagarajan says. “They’re signing up inside these ecosystems so we want to partner with these ecosystems.”

The small team has already built up a customer base of 1,000 businesses. The average Wise customer has between 2-10 employees and is pulling in somewhere between $500,000 and $5 million in ARR, the company tells us. Bank accounts on Wise’s platform are FDIC-insured up to $250,000 through the startup’s partnership with banking partner BBVA USA.

While Thyagarajan says they’ve seen online spend increasing, the COVID-19 pandemic has impacted plenty of Wise’s potential customers, and has pushed the company to stay flexible in the businesses they cater to. “I think a lot of industries are going to get accelerated and fast-forwarded,” he says. “The customers we want to cater to are rapidly modernizing.”

Alongside the funding announcement, the startup shared that Raghav Lal, a former general manager of Small Business at Visa, will be joining the startup as its president.

Powered by WPeMatico

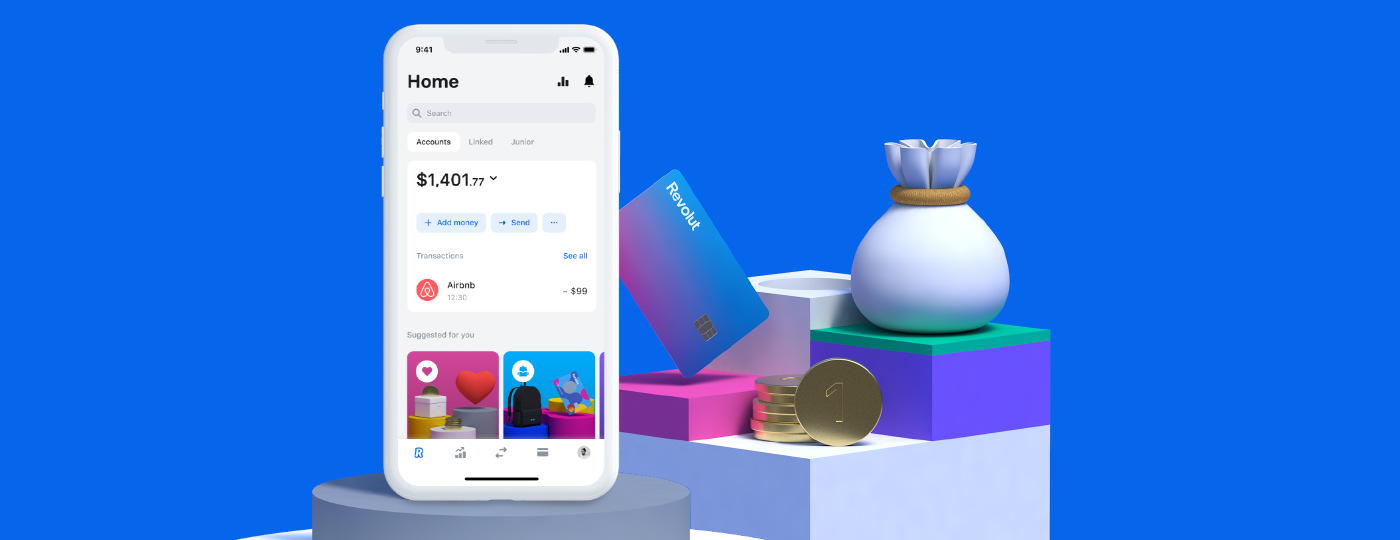

European fintech startup Revolut is launching its app and service in the U.S. Starting today, anybody can sign up and get a Revolut debit card. In the U.S., Revolut has partnered with Metropolitan Commercial Bank for the banking infrastructure — deposits are FDIC insured up to $250,000.

In just a few years, Revolut has managed to attract over 10 million customers by building a financial hub that lets you spend, send, receive and manage money from a single app. The company recently raised a $500 million funding round, valuing the company at $5.5 billion.

But the U.S. has been watching from the sidelines. Tens of thousands of customers have signed up to the waiting list and they’ll now be able to access all of Revolut’s core features.

Like competing challenger banks, such as Chime and N26, Revolut lets you open an account from your phone. After downloading the app, you enter personal details and send a few official documents to comply with know-your-customer regulation.

After that, you get U.S. account details and you can instantly top up your account with a bank transfer or a card transfer. A few days later, you also receive a physical debit card. You can also generate a virtual debit card from the app.

Revolut lets you control your debit card from the app directly. You can receive notifications every time you make a transaction. You can freeze and unfreeze your card, set some limits and restrict some feature, such as online payments or ATM withdrawals.

One of Revolut’s key features is that you can convert from one currency to another based on interbank rate with a low fee — sometimes without any markup for popular currencies and small transactions (more details on foreign exchange fees here). You can hold foreign currencies in your Revolut account or send money to another Revolut user or a bank account in another country.

In the U.S., Revolut offers the ability to receive your salary two days in advance if you share your Revolut banking details with your employer.

Revolut offers a ton of additional features in Europe, but the company is starting with this basic feature set in the U.S. You can expect more features in the future, such as the ability to purchase cryptocurrencies and invest on the stock market.

In Europe, Revolut also offers insurance products through premium monthly subscriptions, mobile phone insurance, savings accounts, credit, rewards and more. Many of those features require partnerships with third-party companies. But it gives you an idea of Revolut’s roadmap in the U.S.

Powered by WPeMatico