brazil

Auto Added by WPeMatico

Auto Added by WPeMatico

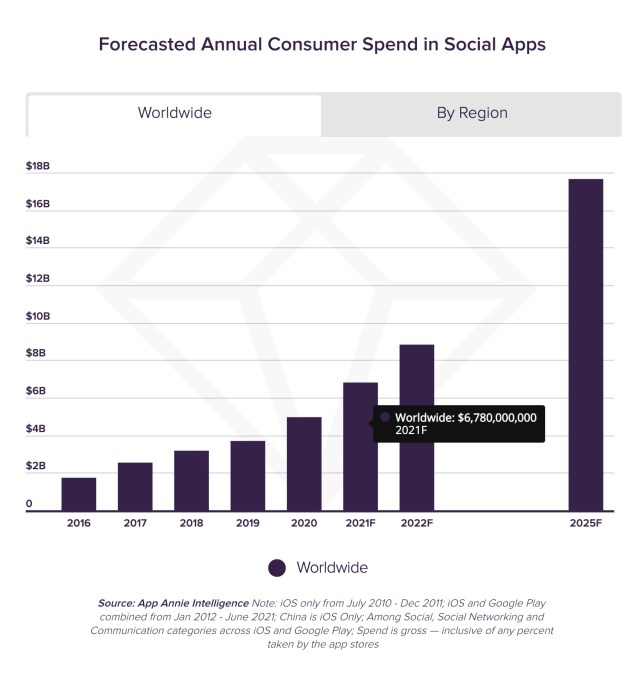

The livestreaming boom is driving a significant uptick in the creator economy, as a new forecast estimates consumers will spend $6.78 billion in social apps in 2021. That figure will grow to $17.2 billion annually by 2025, according to data from mobile data firm App Annie, which notes the upward trend represents a five-year compound annual growth rate (CAGR) of 29%. By that point, the lifetime total spend in social apps will reach $78 billion, the firm reports.

Image Credits: App Annie

Initially, much of the livestream economy was based on one-off purchases like sticker packs, but today, consumers are gifting content creators directly during their livestreams. Some of these donations can be incredibly high, at times. Twitch streamer ExoticChaotic was gifted $75,000 during a live session on Fortnite, which was one of the largest-ever donations on the game-streaming social network. Meanwhile, App Annie notes another platform, Bigo Live, is enabling broadcasters to earn up to $24,000 per month through their livestreams.

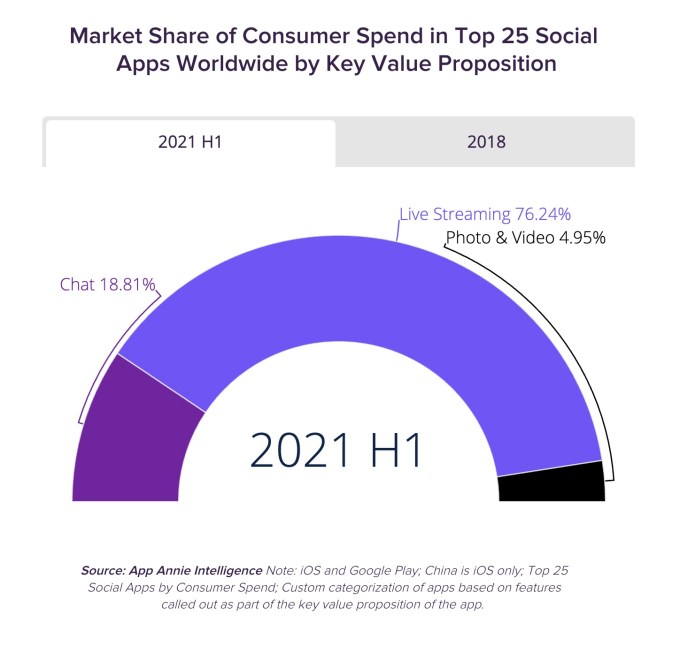

Apps that offer livestreaming as a prominent feature are also those that are driving the majority of today’s social app spending, the report says. In the first half of this year, $3 out every $4 spent in the top 25 social apps came from apps that offered livestreams, for example.

Image Credits: App Annie

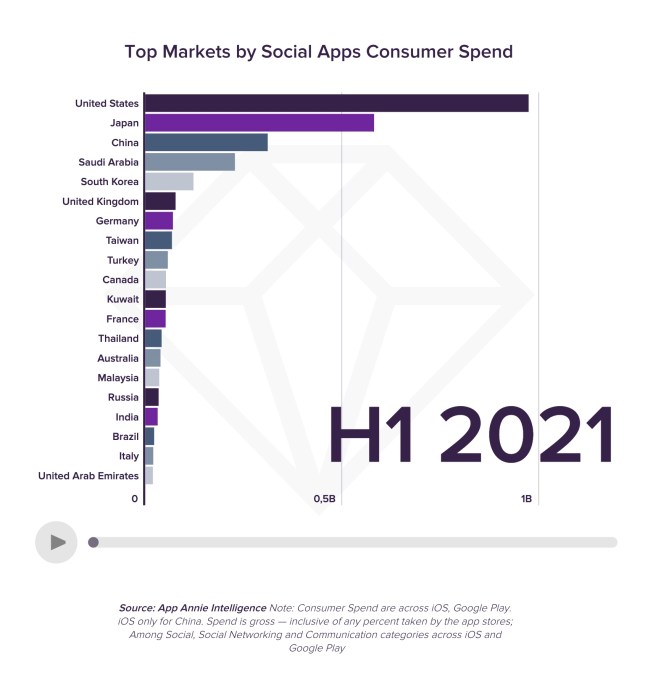

During the first half of 2021, the U.S. become the top market for consumer spending inside social apps, with 1.7x the spend of the next largest market, Japan, and representing 30% of the market by spend. China, Saudi Arabia and South Korea followed to round out the top 5.

Image Credits: App Annie

While both creators and the platforms are financially benefitting from the livestreaming economy, the platforms are benefitting in other ways beyond their commissions on in-app purchases. Livestreams are helping to drive demand for these social apps and they help to boost other key engagement metrics, like time spent in app.

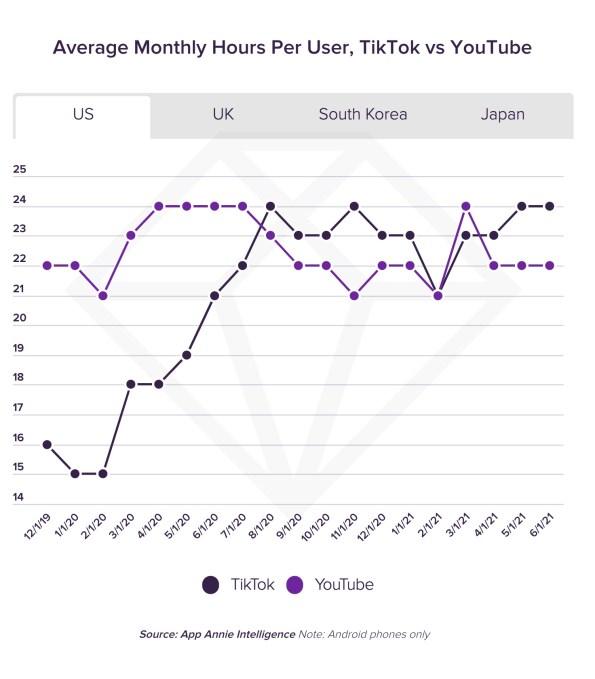

One top app that’s significantly gaining here is TikTok.

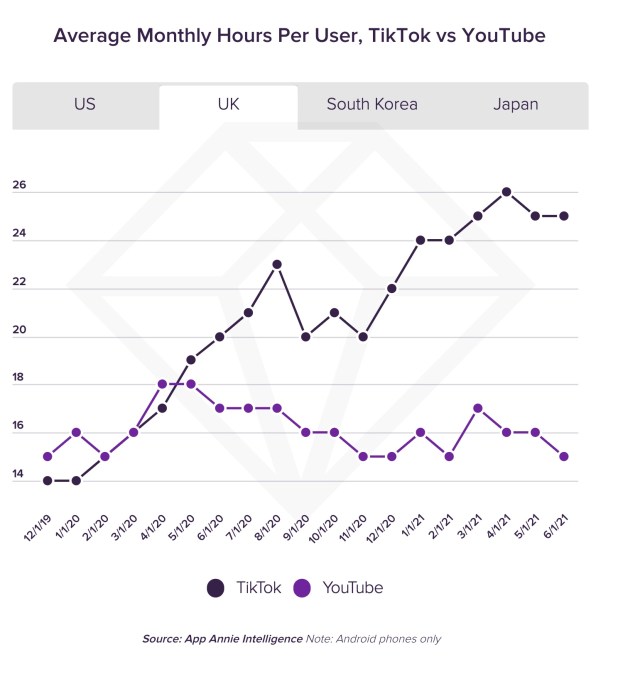

Last year, TikTok surpassed YouTube in the U.S. and the U.K. in terms of the average monthly time spent per user. It often continues to lead in the former market, and more decisively leads in the latter.

Image Credits: App Annie

Image Credits: App Annie

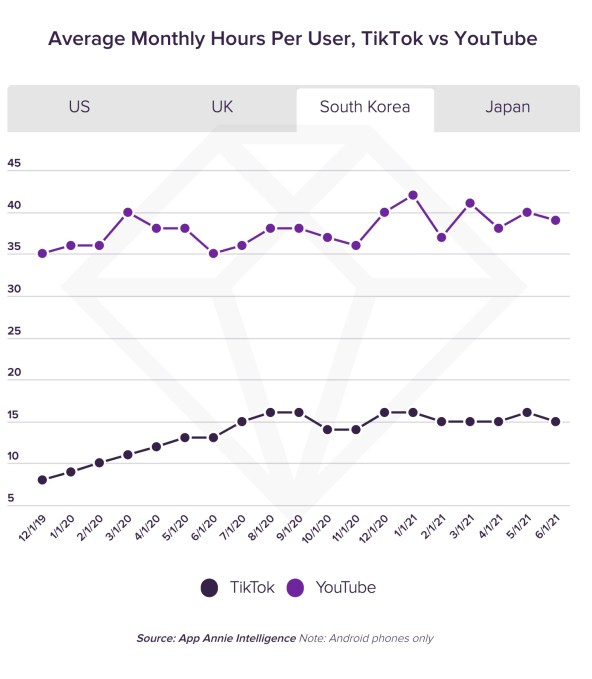

In other markets, like South Korea and Japan, TikTok is making strides, but YouTube still leads by a wide margin. (In South Korea, YouTube leads by 2.5x, in fact.)

Image Credits: App Annie

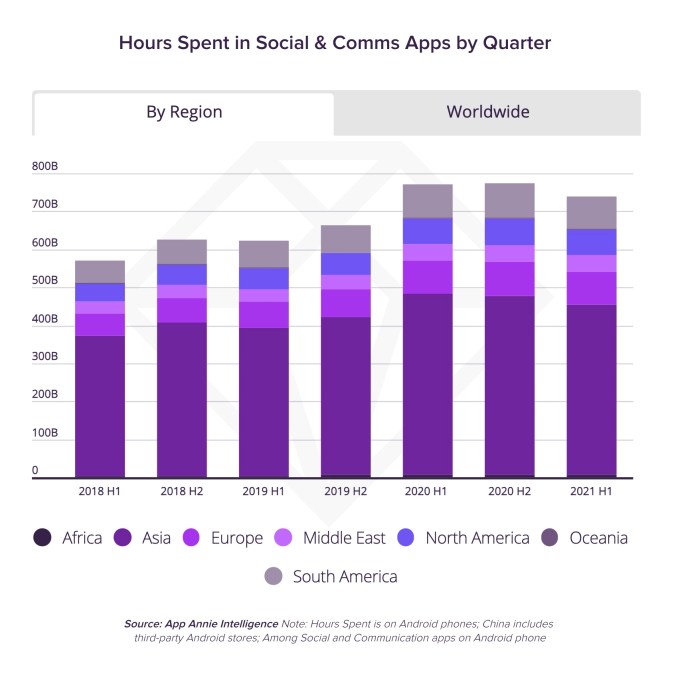

Beyond just TikTok, consumers spent 740 billion hours in social apps in the first half of the year, which is equal to 44% of the time spent on mobile globally. Time spent in these apps has continued to trend upwards over the years, with growth that’s up 30% in the first half of 2021 compared to the same period in 2018.

Today, the apps that enable livestreaming are outpacing those that focus on chat, photo or video. This is why companies like Instagram are now announcing dramatic shifts in focus, like how they’re “no longer a photo sharing app.” They know they need to more fully shift to video or they will be left behind.

The total time spent in the top five social apps that have an emphasis on livestreaming are now set to surpass half a trillion hours on Android phones alone this year, not including China. That’s a three-year CAGR of 25% versus just 15% for apps in the Chat and Photo & Video categories, App Annie noted.

Image Credits: App Annie

Thanks to growth in India, the Asia-Pacific region now accounts for 60% of the time spent in social apps. As India’s growth in this area increased over the past 3.5 years, it shrunk the gap between itself and China from 115% in 2018 to just 7% in the first half of this year.

Social app downloads are also continuing to grow, due to the growth in livestreaming.

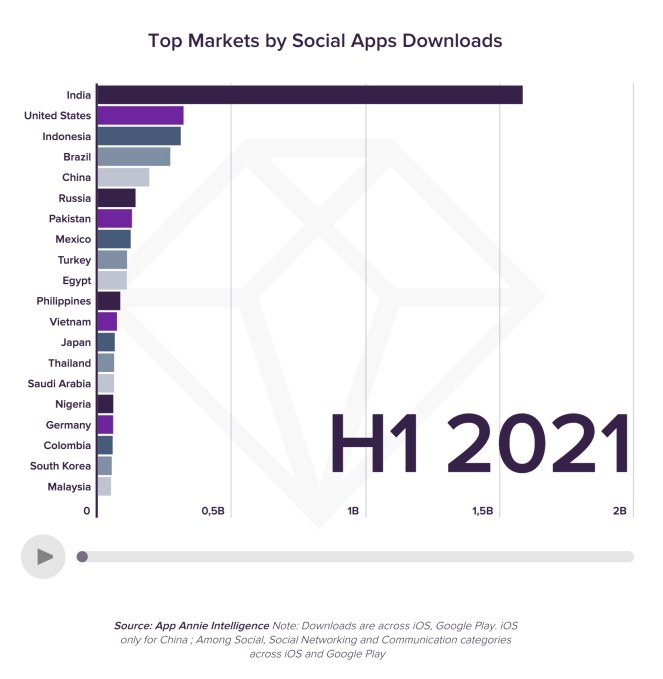

To date, consumers have downloaded social apps 74 billion times, and that demand remains strong, with 4.7 billion downloads in the first half of 2021 alone — up 50% year-over-year. In the first half of the year, Asia was the largest region region for social app downloads, accounting for 60% of the market.

This is largely due to India, the top market by a factor of 5x, which surpassed the U.S. back in 2018. India is followed by the U.S., Indonesia, Brazil and China, in terms of downloads.

Image Credits: App Annie

The shift toward livestreaming and video has also impacted what sort of apps consumers are interested in downloading, not just the number of downloads.

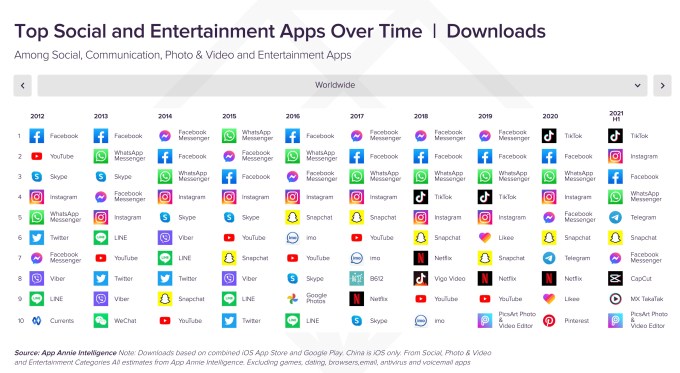

A chart that shows the top global apps from 2012 to the present highlights Facebook’s slipping grip. While its apps (Facebook, Messenger, Instagram and WhatsApp) have dominated the top spots over the years in various positions, TikTok popped into the number one position last year, and continues to maintain that ranking in 2021.

Further down the chart, other apps that aid in video editing have also overtaken others that had been more focused on photos or chat.

Image Credits: App Annie

Video apps like YouTube (#1), TikTok (#2) Tencent Video (#4), Bigo Live (#5), Twitch (#6), and others also now rank at the top of the global charts by consumer spending in the first half of 2021.

But YouTube (#1) still dominates in time spent compared with TikTok (#5), and others from Facebook — the company holds the next three spots for Facebook, WhatsApp and Instagram, respectively.

This could explain why TikTok is now exploring the idea of allowing users to upload even longer videos, by increasing the limit from 3 minutes to 5, for instance.

TikTok is testing a longer 5 minute video upload limit

pic.twitter.com/qiRbJmHkma

— Matt Navarra (@MattNavarra) August 25, 2021

In addition, because of livestreaming’s ability to drive growth in terms of time spent, it’s also likely the reason why TikTok has been heavily investing in new features for its TikTok LIVE platform, including things like events, support for co-hosts, Q&As and more, and why it made the “LIVE” button a more prominent feature in its app and user experience.

App Annie’s report also digs into the impact livestreaming has had on specific platforms, like Twitch and Bigo Live, the former which doubled its monthly active user base from the pre-pandemic era, and the latter which saw $314.2 million in consumer spend during H1 2021.

“The ability of social media users to communicate with each other using live video – or watch others’ live broadcasts – has not only maintained the growth of a social media app market, but contributed to its exponential growth in engagement metrics like time spent, that might otherwise have saturated some time ago,” wrote App Annie’s Head of Insights, Lexi Sydow, when announcing the new report.

The full report is available here.

Powered by WPeMatico

Factorial, a startup out of Barcelona that has built a platform that lets SMBs run human resources functions with the same kind of tools that typically are used by much bigger companies, is today announcing some funding to bulk up its own position: the company has raised $80 million, funding that it will be using to expand its operations geographically — specifically deeper into Latin American markets — and to continue to augment its product with more features.

CEO Jordi Romero, who co-founded the startup with Pau Ramon and Bernat Farrero — said in an interview that Factorial has seen a huge boom of growth in the last 18 months and counts more than anything 75,000 customers across 65 countries, with the average size of each customer in the range of 100 employees, although they can be significantly (single-digit) smaller or potentially up to 1,000 (the “M” of SMB, or SME as it’s often called in Europe).

“We have a generous definition of SME,” Romero said of how the company first started with a target of 10-15 employees but is now working in the size bracket that it is. “But that is the limit. This is the segment that needs the most help. We see other competitors of ours are trying to move into SME and they are screwing up their product by making it too complex. SMEs want solutions that have as much data as possible in one single place. That is unique to the SME.” Customers can include smaller franchises of much larger organizations, too: KFC, Booking.com, and Whisbi are among those that fall into this category for Factorial.

Factorial offers a one-stop shop to manage hiring, onboarding, payroll management, time off, performance management, internal communications and more. Other services such as the actual process of payroll or sourcing candidates, it partners and integrates closely with more localized third parties.

The Series B is being led by Tiger Global, and past investors CRV, Creandum, Point Nine and K Fund also participating, at a valuation we understand from sources close to the deal to be around $530 million post-money. Factorial has raised $100 million to date, including a $16 million Series A round in early 2020, just ahead of the Covid-19 pandemic really taking hold of the world.

That timing turned out to be significant: Factorial, as you might expect of an HR startup, was shaped by Covid-19 in a pretty powerful way.

The pandemic, as we have seen, massively changed how — and where — many of us work. In the world of desk jobs, offices largely disappeared overnight, with people shifting to working at home in compliance with shelter-in-place orders to curb the spread of the virus, and then in many cases staying there even after those were lifted as companies grappled both with balancing the best (and least infectious) way forward and their own employees’ demands for safety and productivity. Front-line workers, meanwhile, faced a completely new set of challenges in doing their jobs, whether it was to minimize exposure to the coronavirus, or dealing with giant volumes of demand for their services. Across both, organizations were facing economics-based contractions, furloughs, and in other cases, hiring pushes, despite being office-less to carry all that out.

All of this had an impact on HR. People who needed to manage others, and those working for organizations, suddenly needed — and were willing to pay for — new kinds of tools to carry out their roles.

But it wasn’t always like this. In the early days, Romero said the company had to quickly adjust to what the market was doing.

“We target HR leaders and they are currently very distracted with furloughs and layoffs right now, so we turned around and focused on how we could provide the best value to them,” Romero said to me during the Series A back in early 2020. Then, Factorial made its product free to use and found new interest from businesses that had never used cloud-based services before but needed to get something quickly up and running to use while working from home (and that cloud migration turned out to be a much bigger trend played out across a number of sectors). Those turning to Factorial had previously kept all their records in local files or at best a “Dropbox folder, but nothing else,” Romero said.

It also provided tools specifically to address the most pressing needs HR people had at the time, such as guidance on how to implement furloughs and layoffs, best practices for communication policies and more. “We had to get creative,” Romero said.

But it wasn’t all simple. “We did suffer at the beginning,” Romero now says. “People were doing furloughs and [frankly] less attention was being paid to software purchasing. People were just surviving. Then gradually, people realized they needed to improve their systems in the cloud, to manage remote people better, and so on.” So after a couple of very slow months, things started to take off, he said.

Factorial’s rise is part of a much, longer-term bigger trend in which the enterprise technology world has at long last started to turn its attention to how to take the tools that originally were built for larger organizations, and right size them for smaller customers.

The metrics are completely different: large enterprises are harder to win as customers, but represent a giant payoff when they do sign up; smaller enterprises represent genuine scale since there are so many of them globally — 400 million, accounting for 95% of all firms worldwide. But so are the product demands, as Romero pointed out previously: SMBs also want powerful tools, but they need to work in a more efficient, and out-of-the-box way.

Factorial is not the only HR startup that has been honing in on this, of course. Among the wider field are PeopleHR, Workday, Infor, ADP, Zenefits, Gusto, IBM, Oracle, SAP and Rippling; and a very close competitor out of Europe, Germany’s Personio, raised $125 million on a $1.7 billion valuation earlier this year, speaking not just to the opportunity but the success it is seeing in it.

But the major fragmentation in the market, the fact that there are so many potential customers, and Factorial’s own rapid traction are three reasons why investors approached the startup, which was not proactively seeking funding when it decided to go ahead with this Series B.

“The HR software market opportunity is very large in Europe, and Factorial is incredibly well positioned to capitalize on it,” said John Curtius, Partner at Tiger Global, in a statement. “Our diligence found a product that delighted customers and a world-class team well-positioned to achieve Factorial’s potential.”

“It is now clear that labor markets around the world have shifted over the past 18 months,” added Reid Christian, general partner at CRV, which led its previous round, which had been CRV’s first investment in Spain. “This has strained employers who need to manage their HR processes and properly serve their employees. Factorial was always architected to support employers across geographies with their HR and payroll needs, and this has only accelerated the demand for their platform. We are excited to continue to support the company through this funding round and the next phase of growth for the business.”

Notably, Romero told me that the fundraising process really evolved between the two rounds, with the first needing him flying around the world to meet people, and the second happening over video links, while he was recovering himself from Covid-19. Given that it was not too long ago that the most ambitious startups in Europe were encouraged to relocate to the U.S. if they wanted to succeed, it seems that it’s not just the world of HR that is rapidly shifting in line with new global conditions.

Powered by WPeMatico

There has been significant hype around Latin America’s startup success. For good reason, too: Startups have raised $9.3 billion in just the first half of 2021, almost double the amount in all of 2020, and mega-rounds are a growing trend.

But while the industry hails the rise of the region’s ecosystem and its growing fleet of unicorns, Latin America’s startup story has a far longer past. And it’s one we should keep in mind as entrepreneurs and investors around the world forge the region’s future.

People often ask me: How are consumers different in Brazil? How does the Peruvian market behave compared to the United States? These questions don’t really see each country for its inherent value, but instead gear people up to expect the unexpected from a historically economically disadvantaged region.

In fact, the evolution of business shares far more similarities across countries than we might expect. Latin America’s market has evolved over a very long time — as long as Silicon Valley and any other hub. This region has a global outlook, spectacular universities, a diverse population and an army of entrepreneurs.

It’s important for investors outside of Latin America to get involved in fundraising at earlier stages, when founders need extra support from everyone around.

That’s why the unicorns and megadeals should come as no surprise: They’re the natural evolution of the ecosystem, of more capital generating more success after years of hard work.

As Latin America has grown, competition has grown even more intense in the United States. VCs have more money than ever, and it’s getting increasingly expensive to invest in North America. So they’re looking to diversify their investments with high-potential opportunities abroad. Big funds are now dedicating resources to exclusively targeting Latin America, from SoftBank creating a region-specific fund, to Sequoia saying it will pay more attention to the region.

These incoming investors must bring more than money to ensure that entrepreneurship continues to grow in a healthy manner, rather than set it off balance. Investors should bring a local strategy that makes them an asset to Latin America’s startup ecosystem.

Most Latin American companies reaching unicorn status and going public now were started around 2012. This is not very different from the timeline of businesses in other markets such as the United States. For instance, e-commerce giant MercadoLibre launched in Argentina around the time eBay was emerging.

What this tells us is that foreign investors would do well to keep a sharp eye on emerging opportunities beyond heavily covered markets like Brazil and Mexico. There is a huge opportunity to do what local investors did in Brazil and Mexico years ago, and play a significant role in the next chapter of countries with blossoming markets like Colombia, Peru or Uruguay.

The amount of VC capital being funneled into Latin American startups has surged since 2017, with angel investment close behind. However, much of this investment comes from local and regional investors. Every top university in Brazil has a pool of angels. Investors in the Andean region cover Peru, Chile and Colombia. If today’s ecosystem is flourishing, it’s largely because native investors are lighting the spark.

Meanwhile, U.S. investor presence at the early stages is still low and risk averse. It’s much harder for a pre-seed or seed startup to get foreign investor interest than when they’ve already reached Series A or B. Investors also tend to come in on an ad hoc basis or as outliers brought about by a mutual contact. Foreign investors are the exception, not the rule.

It’s important for investors outside of Latin America to get involved in fundraising at earlier stages, when founders need extra support from everyone around. Investors should be pursuing a long-term strategy that will bring more consistency to the local ecosystem as a whole.

Your contribution as an investor is largely about the resources you can offer. That’s especially challenging for a foreigner who has less of an understanding of the local industry and lacks a network and people on the ground.

While investors may say their your regular value offering is enough — network and U.S. customers — in truth, this won’t necessarily be of much use. Your hiring network might not be ideal for a Latin American company, and your thorough understanding of the U.S. market might not reflect developments in Latin America.

Remember that the region has a plethora of VC organizations who have worked with local startups over the course of a decade. Latin America is a very welcoming and open market, and local investors and accelerators will happily work with foreign investors, including in deal-sharing opportunities.

It’s crucial to create incentives within the ecosystem, which — like in the United States — largely means matching founders with unique opportunities. In North America, this often happens organically, because people are on the ground and actively engaged with what’s happening in the region, from networking events, to awards, and grants and partnership opportunities.

To create this in Latin America, foreign investors need to dedicate a team and money to their regional commitments. They will have to understand the local industry and be available to mentor founders with diverse perspectives.

In my experience helping EA, Pinterest and Facebook land in Latin America, we always had someone on the ground or working remotely but fully dedicated to the region. We had people focused on localizing the product, and we had research teams studying similarities and differences in user behavior. That’s how corporations land their products; it’s how VCs should land their money.

The idea is for foreign investors to strike a balance locally while creating disruptions when it helps startups look outward rather than attempting to overhaul steady, positive internal growth. That can mean encouraging companies to incorporate in the United States to make it easier for investors from anywhere to invest or preparing the company to go global. Local investors can help investors new to the region understand the balance of things that should or shouldn’t be disrupted.

Don’t be surprised when Latin America’s apparent “boom” starts happening in other emerging markets like Africa and Asia. This isn’t about a secret hack coming in from the outside. It’s just about creating the right environment for local talent to flourish and ensuring it maintains healthy growth.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Natasha and Alex and Grace and Chris were joined by none other than TechCrunch’s own Mary Ann Azevedo, in her first-ever appearance on the show. She’s pretty much the best person and we’re stoked to have her on the pod.

And it was good that Mary Ann was on the show this week as she wrote about half the dang site. Which meant that we got to include all sorts of her work in the rundown. Here’s the agenda:

Powered by WPeMatico

If you’re a founder who finds yourself in a meeting with a VC, try to remember two things:

Even so, many entrepreneurs squander this opportunity, often because they direct questions or fail to understand their BATNA (best alternative to a negotiated agreement).

“As the venture landscape becomes more a meritocratic environment where resumes and institutional affiliations matter less, these strategies can make the difference between a successful fundraise and a fruitless meeting,” says Agya Ventures co-founder Kunal Lunawat.

Whether you’re already in the fundraising process or plan to be in the future, be sure to read “A crash course on corporate development” that Venrock VP Todd Graham shared with us this week.

“If you’re going to get acquired, chances are you’re going to spend a lot of time with corporate development teams,” says Graham. “With a hot stock market, mountains of cash and cheap debt floating around, the environment for acquisitions is extremely rich.”

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

On Wednesday, August 24 at 3 p.m. PDT/6 p.m. EDT/11 p.m GMT, Managing Editor Danny Crichton will host a conversation on Twitter Spaces with Eric Dean Wilson, author of “After Cooling: On Freon, Global Warming, and the Terrible Cost of Comfort.”

Wilson’s book explores the history of freon, a common refrigerant that was later banned due to its devastating impact on the ozone layer. After their discussion, they’ll take questions from the audience.

Thanks very much for reading Extra Crunch this week! I hope you have an excellent weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Carol Yepes (opens in a new window) / Getty Images

Apple iPhone, Apple Mail and Apple iPad account for nearly half of all email opens, but the privacy features included with iOS 15 will allow consumers to block marketers from seeing their physical location, IP address and tracking data like invisible pixels.

Email marketers rely heavily on these and other metrics, which means they should prepare now for the changes to come, advises Litmus CMO Melissa Sargeant.

In a detailed post, she shares several action items that will help marketing teams leverage their email analytics so they can “continue delivering personalized experiences consumers crave.”

Image Credits: Cimmerian (opens in a new window) / Getty Images

Venrock Vice President Todd Graham has some frank advice for founders at venture-backed startups: “It would be wise to generate a return at some point.”

With that in mind, he authored a primer on corporate development that lays out the three most common categories of acquisitions, tips for dealing with bankers, and explains why striking a partnership with a big company isn’t always the best way forward.

Regardless of the path you choose, “you need to take the meeting,” advises Graham.

“In the worst-case scenario, you’ll get a few new LinkedIn connections and you’re now a known quantity. The best-case scenario will be a second meeting.”

Image Credits: Nigel Sussman (opens in a new window)

The pandemic failed to slow the momentum of venture capitalists pouring money into startups, but Chicago stands out as an “outlying benefactor of accelerating venture capital activity and the rise of remote investing,” Alex Wilhelm and Anna Heim write for The Exchange.

When the world shut down and it didn’t matter if you were in NYC or SF (because everyone was on Zoom), the Windy City was ready to present itself as the venture champion of the Midwest.

Image Credits: Priscila Zambotto (opens in a new window) / Getty Images

The Brazilian Central Bank made a major reform to the way payments are processed that may throw the doors open for e-commerce in South America’s largest market.

Historically, merchants who accepted credit card payments had two options: Receive the full payment distributed over two to 12 installments, or offer a deep discount to receive a smaller sum up front.

But in June 2021, the BCB created new “registration entities” that permit “any interested receivables buyer/acquirer to make an offer for those receivables, forcing buyers to become more competitive in their discount offers,” says Leonardo Lanna, head of payment products at Monkey Exchange.

The new framework benefits consumers and sellers, but for the region’s startups, “it opens the door to a plethora of opportunities and new business models, from payments to credit.”

Image Credits: Nigel Sussman (opens in a new window)

An inflow of VC dollars, notable acquisitions and rising unicorn counts are all features of the Brazilian tech startup market, Anna Heim and Alex Wilhelm note in The Exchange.

“The IPO market in Brazil is changing,” they write. “TechCrunch noted last year that in the decade leading up to 2020, just two of the 56 IPOs in Brazil were technology companies. More recently, the number of technology companies listed in the country has swelled to at least 16, up from just four in 2019.”

Image Credits: Andriy Onufriyenko / Getty Images

“For good reason, security certifications like the SOC 3 really put you through the wringer,” Waydev CEO Alex Cercei writes in a guest column.

Waydev, a Git analytics tool that helps engineering leaders measure team performance automatically, just attained the SOC 3 certification.

“We learned so much from the process, we felt it was right to share our experience with others that might be daunted by the prospect,” Cercei writes.

“So here’s our advice on how teams can smoothly reach an SOC 3 while simultaneously balancing workloads and minimizing disruption to users.”

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

I’m on an H-1B living and working in the U.S. I want to apply for a green card on my own. I’m concerned about only relying on my current employer and I want to be able to easily change jobs or create a startup. I’ve been looking at the EB-1A and EB-2 NIW.

I’m not sure if I would qualify for an EB-1A, but since I was born in India, I face a much longer wait for an EB-2 NIW.

Any tips on how to proceed?

— Inventive from India

Image Credits: Cordelia Molloy Science Photo Library (opens in a new window) / Getty Images

Most startups could use an advisory board, but in health tech, it’s a core requirement.

Founders seeking to innovate in this area have a unique need for mentors who have experience navigating regulations, raising capital and managing R&D, to name just a few areas.

Based on his own experience, Patrick Frank, co-founder and COO of PatientPartner, shared some very specific ideas about who to recruit, where to find them and how to fit them into your cap table.

“You want to leverage these individuals so you are able to focus on the full view of the company to ensure it is something that both the market and investors want at scale,” says Frank.

Image Credits: Nigel Sussman (opens in a new window)

There’s no shortage of tech news to analyze, Alex Wilhelm notes, but this week, he took a fresh look at crypto.

How come?

“Because there are some rather bullish trends that indicate the world of blockchain is maturing and creating a raft of winning players,” he writes.

Image Credits: kentoh (opens in a new window) / Getty Images (Image has been modified)

In one recent survey, 58% of workers said they plan to quit if they’re not allowed to work remotely.

Startups that don’t offer employees work-from-home flexibility are at a competitive disadvantage, but figuring out how to pay hybrid workers raises a complex set of questions:

Powered by WPeMatico

Less than three months after announcing a $300 million Series E, Brazilian proptech QuintoAndar has raised an additional $120 million.

New investors Greenoaks Capital and China’s Tencent co-led the round, which included participation from some existing backers as well. São Paulo-based QuintoAndar is now valued at $5.1 billion, up from $4 billion at the time of its last raise in late May. With the extension, the startup has now raised more than $700 million since its 2013 inception. Ribbit Capital led the first tranche of its Series E.

QuintoAndar describes itself as an “end-to-end solution for long-term rentals” that, among other things, connects potential tenants to landlords and vice versa. Last year, it also expanded into connecting home buyers to sellers. Its long-term plan is to evolve into a one-stop real estate shop that also offers mortgage, title insurance and escrow services.

To that end, earlier this month, the startup acquired Atta Franchising, a 7-year-old São Paulo-based independent real estate mortgage broker. Specifically, acquiring Atta is designed to speed up its ability to offer mortgage services to its users. QuintoAndar also plans to explore the possibility of offering a product to perform standalone transactions outside of its marketplace in partnership with other brokers, according to CEO and co-founder Gabriel Braga.

This year, QuintoAndar expanded operations into 14 new cities in Brazil. Eventually, QuintoAndar plans to enter the Mexican market as its first expansion outside of its home country, but it has not yet set a date for that step. Today, the company has more than 120,000 rentals under management and about 10,000 new rentals per month. Its rental platform is live in 40 cities across Brazil, while its home-buying marketplace is live in four (São Paulo, Rio de Janeiro, Belo Horizonte and Porto Alegre) and seeing more than 10,000 sales in annualized terms.

QuintoAndar, he said, is open to acquiring more companies that it believes can either help it accelerate in a particular way or add something it had not yet thought about.

“We’re receptive to the idea but our core strategy is to focus on organic growth and our own innovation and accelerate that,” Braga said.

The Series E was oversubscribed with investors who got in and “some who could not join,” according to Braga.

Greenoaks and Tencent, he said, couldn’t participate because of “timing issues.”

“We kept talking and they came back to us after the round, and wanted to be involved so we found a way to have them on board,” Braga said. “We did not need the money. But we have been constantly overachieving on the forecast that we shared with our investors. And that’s part of the reason why we had this extension.”

Greenoaks’ long-term time horizon was appealing because the firm’s investment was designed to be “perpetual capital with no predefined time frame,” Braga said.

“We’re doing our best to build an enduring company that will be around for many, many years, so it’s good to have investors who share that vision and are technically aligned,” he added.

Greenoaks partner Neil Shah said his firm believes that what QuintoAndar is building will “fundamentally reshape real estate transactions, enhancing transparency, expanding options for Brazilians seeking housing, dramatically simplifying the experience for landlords and driving increased investment into real estate across the country.” He also believes there is big potential for the company to take its offering to other parts of Latin America.

“We look forward to being partners for decades to come,” he added.

Tencent’s experience in China is something QuintoAndar also finds valuable.

“We believe we can learn a lot from them and other Chinese companies doing interesting stuff there,” Braga said.

QuintoAndar isn’t the only Brazilian proptech firm raising big money: In March, São Paulo digital real estate platform Loft announced it had closed on $425 million in Series D funding led by New York-based D1 Capital Partners. Then, about one month later, it revealed a $100 million extension that valued the company at $2.9 billion.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Danny was back, joining Natasha and Alex and Grace and Chris to chat through the week’s coming and goings. But, before we get to the official news, here’s some personal news: Danny is stepping back from his role as co-host of the Friday show! Yes, Mr. Crichton will still take part in our mid-week, deep-dive episodes, but this is the conclusion of his run as part of the news roundup. We will miss him, glad that his transitions and wit will continue to be part of the Equity universe.

Who will take the third chair? Well, stay tuned. We have some neat things planned.

Now, the rundown:

Powered by WPeMatico

The gamification of payments is not a new concept.

A number of companies are attempting to combine gamification and payments in creative ways. And today, one such company, Play2Pay, has raised $13 million in a Series A round of funding.

The Miami-based startup has a straightforward mission. It wants to give consumers a way to reduce their bills — it claims by an average of 30%! — by playing games, watching videos and completing daily challenges, offers and surveys.

Play2Pay was bootstrapped for the first five years of its life, raising its first external capital in June of 2020 — a $7.5 million seed round from individual angel investors. Telesoft Partners led its Series A round, which included participation from Harbor Spring Capital and individual investors including former AT&T vice chairman Ralph de la Vega, former Reuters CEO Tom Glocer, Madison Dearborn Partners co-founder and senior advisor Jim Perry and Virtusa founder and former CEO, Kris Canekeratne.

The alternative payment platform says it brokers a “value exchange” between brands and consumers, converting attention and engagement into a currency, which can be redeemed for bill payment. Meanwhile, brands get a new way to promote their products and services.

Play2Pay founder and CEO Brian Boroff started the company in 2015 based on a vision that prepaid mobile phone users should have an alternative way to pay for their mobile phone service and that wireless carriers would adopt an ad-funded commercial model.

Today, the company claims to be positioned to be the world’s first “ad supported payment rail” directly integrated into payments platforms of major service providers and financial institutions. It also claims to be the only company that converts user engagement directly into bill payment.

Image Credits: Play2Pay

The “opt-in” offering is currently available to more than 100 million mobile subscribers across the United States, United Kingdom, Mexico, Brazil and Indonesia through partnerships with telecom companies such as AT&T Mexico, Cricket in the U.S., TIM in Brazil, lndosat Ooredoo in Indonesia and U.K.-based Lycamobile.

The rewarding approach seems to be resonating with users. From June 2020 to June 2021, the startup saw its ARR (annual recurring revenue) spike by nearly 300%, according to Boroff, a telecom veteran.

Among the users engaged on the platform, about 25% generated revenue daily, he said. And service providers realized up to 17% revenue expansion as a result of subscriber engagement on the Play2Pay platform, according to Boroff.

“Our distribution model is B2B2C, with Tier-1 service providers worldwide directly integrating our bill payment capability. We’re growing our audience through promotion of the service to their customer base,” he told TechCrunch.

End users, he added, can share their targeting preferences in exchange for value, giving mobile app developers and brands more information when promoting their own products and services to Play2Pay’s audience.

The platform is free for service providers and merchants, meaning the payment does not have costs or fees from interchange, acquirers, chargebacks or gateways.

Instead, Play2Pay generates revenue from mobile app developers and brands. Those developers and brands pay to access Play2Pay’s mobile audience in order to promote their products and services. For example, a mobile gaming company might pay Play2Pay $100 for every user that downloads their app from the Play2Pay app and plays the game for a period of time (such as two hours). Through its technology and partner network, Play2Pay has attribution tracking to ensure that the end user and mobile gaming company both know how much progress has been made toward completing that goal. Other formats include watching videos, completing surveys and more conventional native advertising in some areas.

Powered by WPeMatico

Brazil is a country riven with economic contradictions. It has one of the largest and most profitable banking industries in Latin America, and is among the world’s most developed financial markets. Financial transactions that would take days to process in the United States through ACH happen instantaneously in Brazil. This sophistication, however, masks a backward state of affairs plagued by appalling customer service, exorbitant fees and lack of banking access for many.

The country’s financial system is volatile and often leaves its citizens with few or no alternatives. According to an HBS case study, “in December 2018 the interest rate in Brazil for corporate loans was 52.3%, for consumer loans it was 120.0% and for credit card indebtedness it was 272.42%.” Those rates are many multiples higher compared to figures in neighboring countries.

Brazil’s banking system is a massive market, and one ill-served by incumbents. If someone could thread the needle of product development, strategy and political horse trading required to build a bank in a country where it is nearly impossible for foreigners to own or invest in a bank, it would be one of the great startup and economic success stories of this century.

Nubank is on its way to realizing that objective. Its story is one of unmitigated success, even by the standards of our EC-1 series on high-flying companies and their hard-learned lessons. Just last week, this Brazilian credit card and banking fintech raised a $750 million round led by Berkshire Hathaway at a $30 billion valuation, becoming one of the most valuable startups in the world. It has 40 million users across Brazil, as well as Mexico and Colombia.

Yet, it’s a startup with a CEO and co-founder who isn’t Brazilian, didn’t speak the local language of Portuguese, hadn’t started a company before, and didn’t really know a lot about banking to begin with. This is a story of how raw execution, a “faster, faster” mentality and a fanaticism for making customer experience as enjoyable as a trip to Disney World can completely change the history of an industry — and country — forever.

Our lead writer for this EC-1 is Marcella McCarthy. McCarthy, who spent significant time in Brazil growing up and is trilingual in English, Spanish and Portuguese, has been covering the LatAm and Miami ecosystems for TechCrunch with an eye to the disruption underway in these interconnected regions. The lead editor for this package was Danny Crichton, the assistant editor was Ram Iyer, the copy editor was Richard Dal Porto, and illustrations were drawn by Nigel Sussman.

Nubank had no say in the content of this analysis and did not get advance access to it. McCarthy has no financial ties to Nubank or other conflicts of interest to disclose.

The Nubank EC-1 comprises four main articles numbering 9,200 words and a reading time of 37 minutes. Here’s what’s in the bank:

We’re always iterating on the EC-1 format. If you have questions, comments or ideas, please send an email to TechCrunch Managing Editor Danny Crichton at danny@techcrunch.com.

Powered by WPeMatico

For most startups, the hardest early challenge is identifying a market and a product to serve it. That wasn’t the case for Nubank CEO David Velez, who understood the massive potential for success if he could break into Latin America’s most valuable economy with even a moderately modern banking offering.

Instead, the challenge was how to rebuild the concept of a bank in a country where banking is widely hated, all while the incumbents heavily entrenched with the state worked to block every move.

Nubank knew its market and geography, and through tenacious fundraising, inventive marketing and product development, and a series of contrarian hires, Velez and his team stripped bare the morass of Brazilian banking to build one of the world’s great fintech companies.

The challenge was how to rebuild the concept of a bank in a country where banking is widely hated, all while the incumbents heavily entrenched with the state worked to block every move.

In the first part of this EC-1, I’ll look at how Velez brought his skills and experience to bear on this market, how Nubank was founded in 2013, and how the team brought a Californian rather than Brazilian vibe to their first office on — no joke — California Street, in a neighborhood called Brooklin in the city of São Paulo.

The idea of being his own boss was ingrained in Velez from his earliest days in Colombia, where he grew up in an entrepreneurial family, with a father who owned a button factory. “I heard from my dad over and over again that you need to start your own company,” Velez said.

But years would pass and Velez still had no idea what he wanted to do. To “kill time,” and also to surround himself with entrepreneurial energy, Velez attended Stanford University — partially financed by the sale of some livestock — and then worked as an analyst at Goldman Sachs and Morgan Stanley before switching to venture capital at General Atlantic and Sequoia.

Powered by WPeMatico