App Annie

Auto Added by WPeMatico

Auto Added by WPeMatico

App Annie, a go-to source for mobile app market data and analytics, is expanding its platform with the acquisition of mobile analytics provider Libring. The deal will allow App Annie to present its mobile app market data side by side with advertising analytics data in order to paint a more complete picture of an app’s performance and revenue.

Already, App Annie customers leverage its platform to track key metrics related to their app’s growth and usage, like downloads, active users, retention numbers, demographics, rankings, reviews, competitive analysis and more. But the company said it heard from publishers and brands how it’s still difficult to analyze their user acquisition efforts, including their ad spend and related costs.

With the addition of Libring, App Annie is integrating adtech insights into its platform.

With the addition of Libring, App Annie is integrating adtech insights into its platform.

This includes the ability to combine the ad spend and monetization insights from more than 325 data sources, including Supply Side Platforms (SSPs), Demand Side Platforms (DSPs), app stores and analytics platforms.

This data is then presented in a single dashboard so it’s easier to understand critical metrics — like the customer acquisition cost, the lifetime value, the return on ad spend and the return on investment.

It’s ideal for larger organizations that have outgrown the spreadsheet, as it’s been sort of the App Annie of revenue aggregation, so to speak.

“The most successful companies find a way to capitalize on mobile, yet they have been struggling to maximize its value to their business,” explained App Annie CEO Ted Krantz, in a statement about the acquisition. “Today, this requires custom work to stitch together multiple point solutions, spreadsheets, business intelligence teams, agencies and consultants. We are committed to solving this by applying data science and machine learning to automate these composite metrics for brands and publishers,” he said.

The deal comes at a time when mobile ad spend is continuing to grow rapidly — it’s expected to double to $375 billion globally by 2022, the company noted. It’s now a massive part of the overall app industry, at triple the amount of consumer spending on the app stores.

As a result of the deal, Libring’s 30-plus employees are joining App Annie.

In the near-term, Libring’s current customers will continue to use its product as they do today.

But App Annie tells us there’s only some overlap between the two companies’ respective customer bases. For now, App Annie will work with its customers who want to purchase the new analytics service and find out what sort of enhancements they are looking for in an analytics solution. Libring’s customers can also purchase App Annie’s analytics, if they choose.

Later, App Annie will migrate the Libring backend to the same infrastructure provider the rest of App Annie uses, and will then integrate the front-end so customers can log in and visualize the new analytics and other market data together. More information about how this will all work will be shared when those tools are closer to being available, which is still several months from now.

Going forward, App Annie says its data science team will also offer predictive and prescriptive insights based on the new data.

According to Libring’s website, its customers included SEGA, Slickdeals, Reddit, Jam City, Wooga, EA, Zynga, Next Games, Meet Me, GameInsight, Deviant Art, Webedia, Ubisoft, theChive, saambaa, badoo, textnow and others.

App Annie declined to disclose the deal terms.

Related to the changes and expansion, App Annie also today introduced a new brand that features a gem logomark. The gem is meant to be a tribute to mobile gaming and the idea of “leveling up” while also a reflection of the value of actionable data, the company says.

![]()

The acquisition comes on the heels of several notable milestones for App Annie, including the launch of a product development testing ground, App Annie Labs; plus the addition of mobile web analytics in March — the same time when App Annie passed $100 million in annual recurring revenue.

The company is soliciting feedback about its plans for Libring and will post updates about the project on App Annie Labs, it says.

Powered by WPeMatico

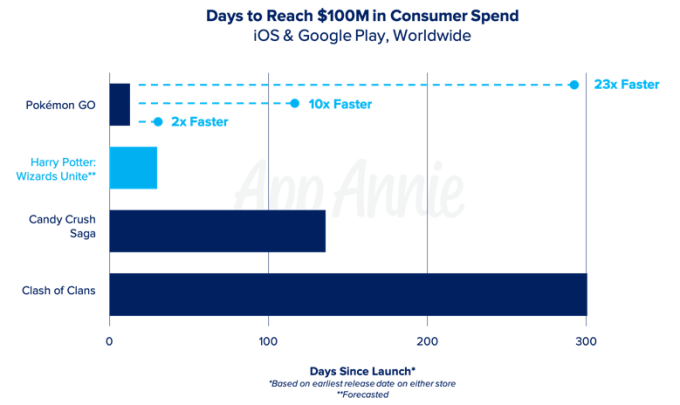

Harry Potter: Wizards Unite, the highly anticipated new mobile game from Pokémon GO makers Niantic and Warner Brothers’ games division, is off to a good start, but it’s not breaking Pokémon GO records. According to preliminary estimates from Sensor Tower, the new game has been installed some 400,000 times in its first 24 hours in its launch markets of the U.S. and U.K. — where the game arrived ahead of schedule on Thursday. Gross player spending in these markets hit around $300,000 across both iOS and Android during this time.

This is not the full picture, however.

The game was also available in Australia and New Zealand during a pre-launch beta trial of sorts, and is only now rolling out to worldwide users on a country-by-country basis. During its beta test period, Sensor Tower estimates the game grossed around $80,000.

But in the same number of days, Pokémon GO grossed $1.6 million in those two markets.

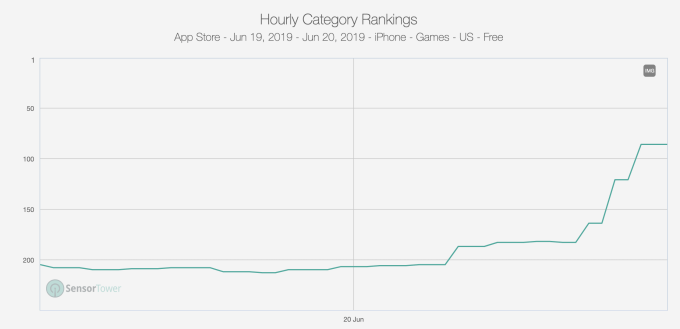

Following its U.S. launch, it took Harry Potter: Wizards Unite around 15 hours to reach the No.1 position on the iOS App Store. This ascension is also going a bit slower than Pokémon GO did when it arrived. That game was an immediate hit, debuting at No. 1 on its launch day of July 6, 2016. It was then installed 7.5 million times in the U.S. during its first 24 hours. And it didn’t reach the U.K. until seven days later.

In its first 24 hours, Pokémon GO became the No. 1 app by revenue in the U.S., as well. The new Harry Potter title is ranked No. 102 overall for iPhone revenue and No. 62 among top grossing games, Sensor Tower says. It’s also No. 48 for U.K. revenue. (It’s not yet ranked on Google Play.)

App Annie hasn’t yet put out numbers related to Harry Potter: Wizards Unite’s revenue, but the company tells us it hit No. 1 in the U.S. for downloads as of 12 AM on June 21, 2019. And for consumer spending, App Annie says the game broke into the top 100 grossing games by hitting No. 63 as of 7:00 AM June 21 on iPhone in the U.S.

The new game’s lesser demand compared with Pokémon GO could be attributed to a number of factors. Pokémon GO was hugely anticipated, had a massive fan base ready to download and was one of the first compelling use cases of AR in gaming.

Harry Potter’s fan base is active as well, but they’ve also had other games to play before now.

For example, Jam City has a Harry Potter: Hogwarts Mystery game that’s been getting a huge boost since yesterday’s news of the new Niantic title. That points to a case of mistaken identity or perhaps clever App Store SEO… or both.

It’s also worth noting the App Store itself has changed in the years since Pokémon GO’s launch.

In September 2017, Apple introduced its brand-new App Store that took the emphasis off its Top Charts as a means of discovery, and instead features apps in editorial “stories” on its Today tab. Within the dedicated apps and games section, the revamped App Store points users to editorial collections, with Top Charts only found upon scrolling down the page quite a bit.

We’ve heard from some developers that these changes reduced their downloads, as getting into the Top Charts doesn’t drive numbers like it used to. They said getting into the Today tab’s feature editorial doesn’t send as many installs, either. But this is all anecdotal — and of course, Apple doesn’t talk about numbers like this. Further investigation is needed.

In any event, the two app store intelligence firms — App Annie and Sensor Tower — both predict big numbers for the new Harry Potter title over time.

Sensor Tower estimates the game will pull in $400 million to $500 million in revenue in its first year. However, the firm notes that Harry Potter isn’t as popular in Asia — a market that delivers Pokémon GO over 40% of its revenue.

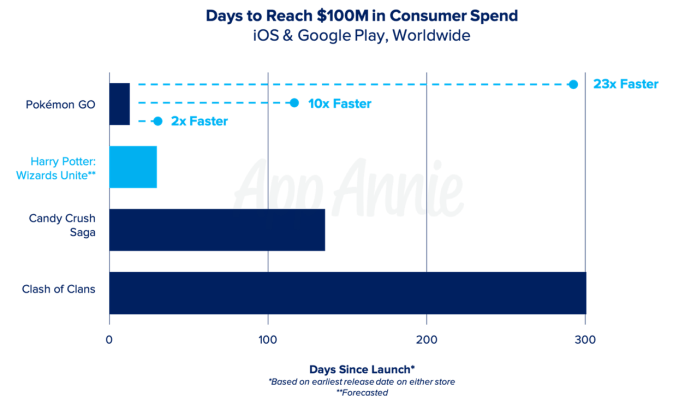

App Annie, meanwhile, predicts the game will hit $100 million in consumer spend in its first 30 days. (Pokémon GO hit this milestone in two weeks.)

“Pokémon GO shattered mobile gaming records, clearing $100 million in its first two weeks and becoming the fastest game to reach $1 billion in consumer spend,” noted App Annie. “While we don’t expect it to surpass Pokémon GO’s launch, Harry Potter: Wizards Unite is set to clear $100 million in its first 30 days — which is no small feat.”

Powered by WPeMatico

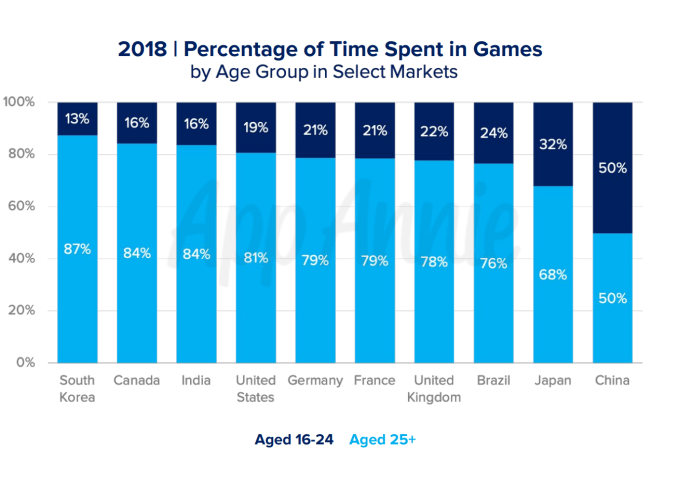

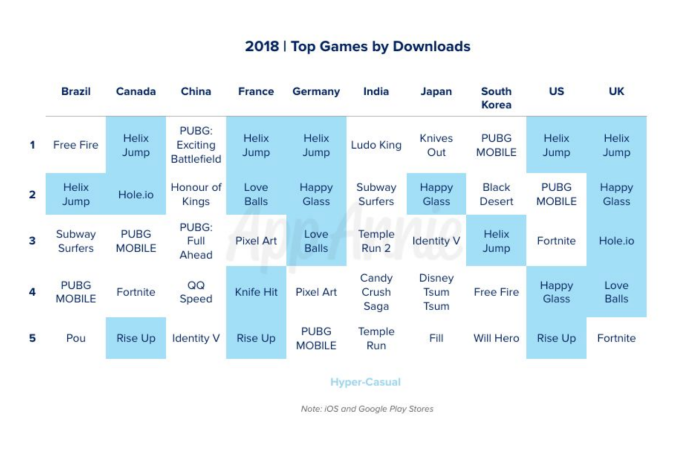

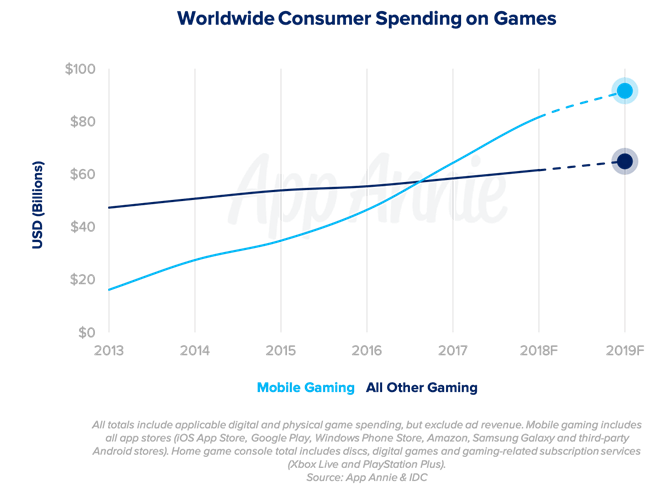

Mobile gaming continues to hold its own, accounting for 10% of the time users spend in apps — a percentage that has remained steady over the years, even though our time in apps overall has grown by 50% over the past two years. In addition, games are continuing to grow their share of consumer spend, notes App Annie in a new research report out this week, timed with E3.

Thanks to growth in hyper-casual and cross-platform gaming in particular, mobile games are on track to reach 60% market share in consumer spend in 2019.

The new report looks at how much time users spend gaming versus using other apps, monetization and regional highlights within the gaming market, among other things.

Despite accounting for a sizable portion of users’ time, games don’t lead the other categories, App Annie says.

Instead, social and communications apps account for half (50%) of the time users spent globally in apps in 2018, followed by video players and editors at 15%, then games at 10%.

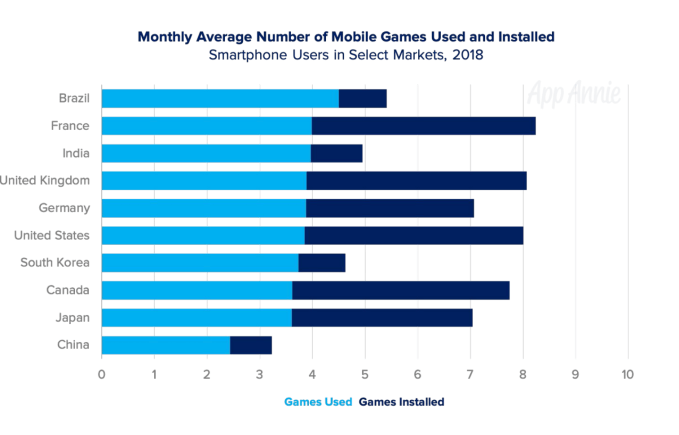

In the U.S., users generally have eight games installed per device; globally, we play an average of two to five games per month.

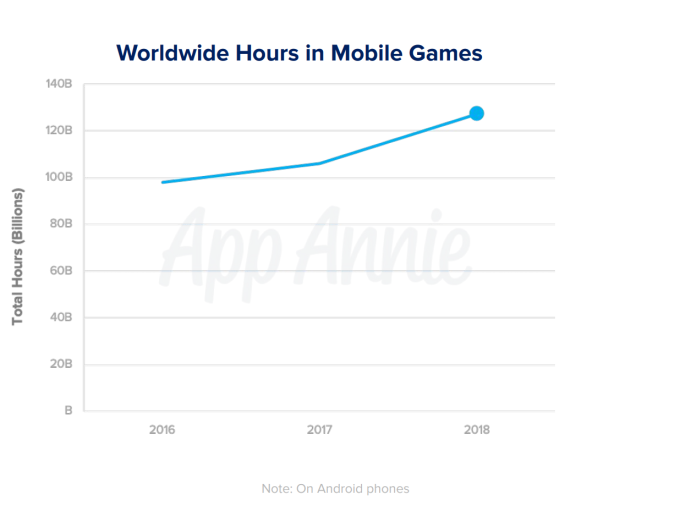

The number of total hours spent on games continues to grow roughly 10% year-over-year, as well, thanks to existing gamers increasing their time in games and from a broadening user base, including a large number of mobile app newcomers from emerging markets.

This has also contributed to a widening age range for gamers.

Today, the majority of time spent in gaming is by those aged 25 and older. In many cases, these players may not even classify themselves as “gamers,” App Annie noted.

While games may not lead the categories in terms of time spent, they do account for a large number of mobile downloads and the majority of consumer spending on mobile.

One-third of all worldwide downloads are games across iOS, Google Play and third-party app stores.

Last year, 1.6+ million games launched on Google Play and 1.1+ million arrived on iOS.

On Android, 74 cents of every dollar is spent on games, with 95% of those purchases coming as in-app purchases, not paid downloads. App Annie didn’t have figures for iOS.

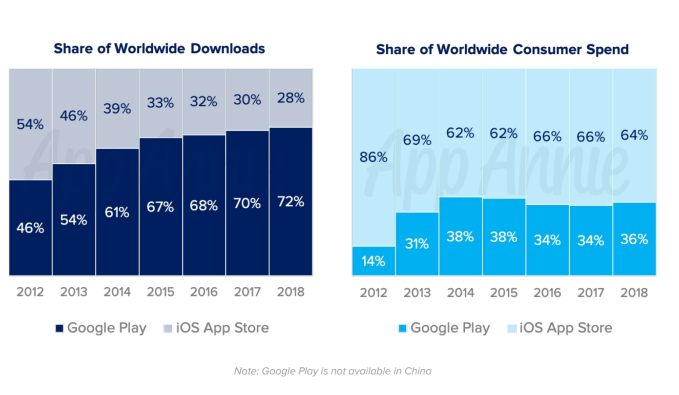

Google Play is known for having more downloads than iOS, but continues to trail on consumer spend. In 2018, Google Play grabbed a 72% share of worldwide downloads, compared with 28% on iOS. Meanwhile, Google Play only saw 36% of consumer spend versus 64% on iOS.

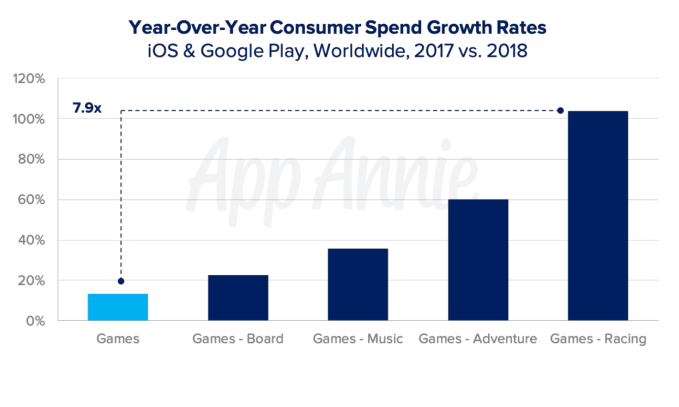

One particular type of gaming jumped out in the new report: racing games.

Consumer spend in this subcategory of gaming grew 7.9 times as fast as the overall mobile gaming market. Adventure games did well, too, growing roughly five times the rate of games in general. Music games and board games were also popular.

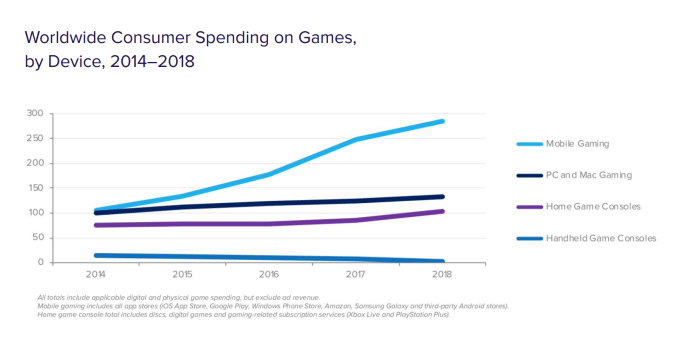

Of course, gaming expands beyond mobile. But it’s surprising to see how large a share of the broader market can be attributed to mobile gaming.

According to App Annie, mobile gaming is larger than all other channels, including home game consoles, handheld consoles and computers (Mac and PC). It’s also 20% larger than all these other categories combined — a shift from only a few years ago, attributed to the growth in the mobile consumer base, which allows mobile gaming to reach more people.

Cross-platform gaming is a key gaming trend today, thanks to titles like PUBG and Fortnite in particular, which were among the most downloaded games across several markets last year.

Meanwhile, hyper-casual games are appealing to those who don’t think of themselves as gamers, which has helped to broaden the market further.

App Annie is predicting the next big surge will come from AR gaming, with Harry Potter: Wizards Unite expected to bring Pokémon Go-like frenzy back to AR, bringing the new title $100 million in its first 30 days. The game is currently in beta testing in select markets, with plans for a 2019 release.

In terms of regions, China’s impact on gaming tends to be outsized, but its growth last year was limited due to the game license regulations. This forced publishers to look outside the country for growth — particularly in markets like North America and Japan, App Annie said.

Meanwhile, India, Brazil, Russia and Indonesia lead the emerging markets with regard to game

downloads, but established markets of the U.S. and China remain strong players in terms of sheer numbers.

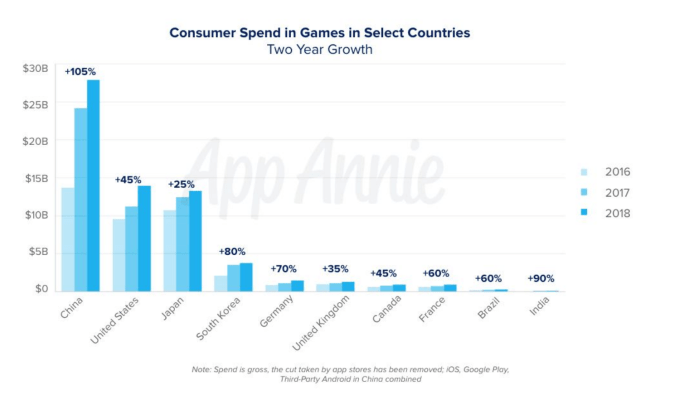

With the continued steady growth in consumer spend and the stable time spent in games, App Annie states the monetization potential for games is growing. In 2018, there were 1,900 games that made more than $5 million, up from 1,200 in 2016. In addition, consumer spend in many key markets is still growing too — like the 105% growth in two years in China, for example, and the 45% growth in the U.S.

The full report delves into other regions as well as game publishers’ user acquisition strategies. It’s available for download here.

Powered by WPeMatico

A slew of banks are coming together to back a new roll-up strategy for the Los Angeles-based mobile gaming studio Jam City and giving the company $145 million in new funding to carry that out.

There’s no word on whether the new money is in equity or debt, but what is certain is that JPMorgan Chase Bank, Bank of America Merrill Lynch and syndicate partners, including Silicon Valley Bank, SunTrust Bank and CIT Bank, are all involved in the deal.

“In a global mobile games market that is consolidating, Jam City could not be more proud to be working with JPMorgan, Bank of America Merrill Lynch, Silicon Valley Bank, SunTrust Bank and CIT Group to strategically support the financing of our acquisition and growth plans,” said Chris DeWolfe, co-founder and CEO of Jam City. “This $145 million in new financing empowers Jam City to further our position as a global industry consolidator. As we grow our global business, we are honored to be working alongside such prestigious advisers who share Jam City’s mission of delivering joy to people everywhere through unique and deeply engaging mobile games.”

The new money comes after a few years of speculation on whether Jam City would be the next big Los Angeles-based startup company to file for an initial public offering. It also follows a new agreement with Disney to develop mobile games based on intellectual property coming from all corners of the mouse house — a sweet cache of intellectual property ranging from Pixar, to Marvel, to traditional Disney characters.

Jam City is coming off a strong year of company growth. The Harry Potter: Hogwarts Mystery game, which launched last year, became the company’s fastest title to hit $100 million in revenue.

Add that to the company’s expansion into new markets with strategic acquisitions to fuel development and growth in Toronto and Bogota and it’s clear that the company is looking to make more moves in 2019.

Jam City already holds intellectual property for a new game built on Disney’s “Frozen 2,” the company’s newly acquired Fox Studio assets like “Family Guy” and the Harry Potter property. Add that to its own Cookie Jam and Panda Pop properties and it seems like the company is ready to make moves.

Meanwhile, games are quickly becoming the go-to revenue driver for the entertainment industry. According to data collected by Newzoo, mobile games revenue reached a record $63.2 billion worldwide in 2018, representing roughly 47 percent of the total revenue for the gaming industry in the year. That number could reach $81.3 billion by 2020, the Newzoo data suggests.

Roughly half of the U.S. plays mobile games, and they’re spending significant dollars on those games in app stores. App Annie suggests that roughly 75 percent of the money spent in app stores over the past decade has been spent on mobile games. And consumers are expected to spend roughly $129 billion in app stores over the next year. The data and analytics firm suggests that mobile gaming will capture some 60 percent of the overall gaming market in 2019, as well.

All of that bodes well for the industry as a whole, and points to why Jam City is looking to consolidate. And the company isn’t the only mobile games studio making moves.

The publicly traded games studio Zynga, which rose to fame initially on the back of Facebook’s gaming platform, recently expanded its European footprint with the late-December acquisition of the Helsinki-based gaming studio Small Giant Games.

Powered by WPeMatico

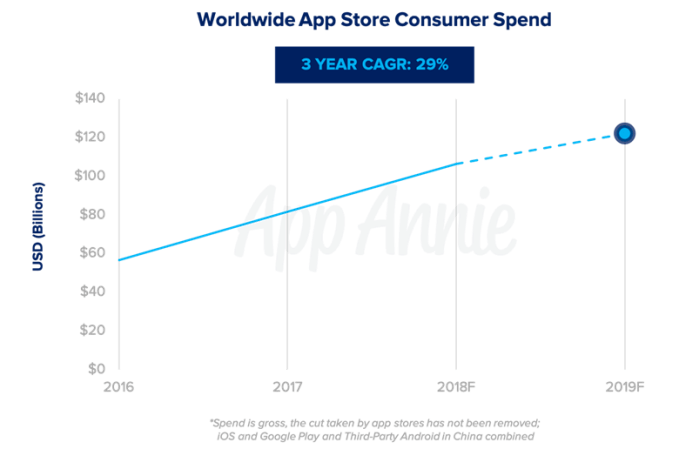

Mobile intelligence and data firm App Annie is today releasing its 2019 predictions for the worldwide app economy, including its forecast around consumer spending, gaming, the subscription market and other highlights. Most notably, it expects the worldwide gross consumer spend in apps — meaning before the app stores take their own cut — to surpass $122 billion next year, which is double the size of the global box office market, for comparison’s sake.

According to the new forecast, the worldwide app store consumer spend will grow five times as fast as the overall global economy next year.

But the forecast also notes that “consumer spend” — which refers to the money consumers spend on apps and through in-app purchases — is only one metric to track the apps stores’ growth and revenue potential.

Mobile spending is also expected to continue growing for both in-app advertising and commerce — that is, the transactions that take place outside of the app stores in apps like Uber, Amazon and Starbucks, for example.

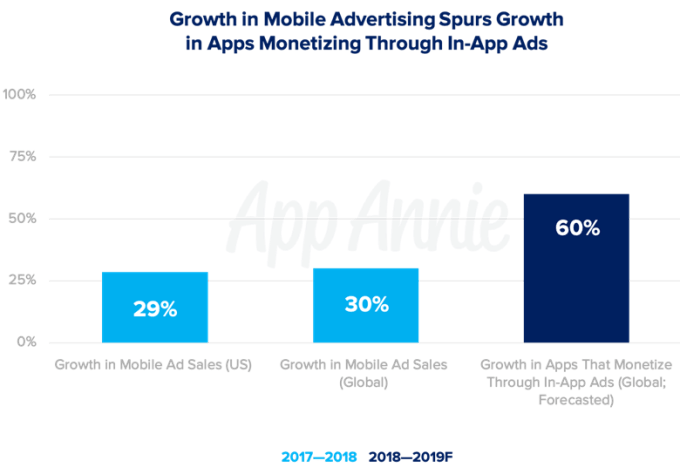

Specifically, mobile will account for 62 percent of global digital ad spend in 2019, representing $155 billion, up from 50 percent in 2017. In addition, 60 percent more mobile apps will monetize through in-app ads in 2019.

As in previous years, mobile gaming is contributing to the bulk of the growth in consumer spending, the report says.

Mobile gaming, which continues to be the fastest growing form of gaming, matured further this year with apps like Fortnite and PUBG, says App Annie . These games “drove multiplayer game mechanics that put them on par with real-time strategy and shooter games on PC/Mac and Consoles in a way that hadn’t been done before,” the firm said.

They also helped push forward a trend toward cross-platform gaming, and App Annie expects that to continue in 2019 with more games becoming less siloed.

However, the gaming market won’t just be growing because of experiences like PUBG and Fortnite. “Hyper-casual” games — that is, those with very simple gameplay — will also drive download growth in 2019.

Over the course of the next year, consumer spend in mobile gaming will reach 60 percent market share across all major platforms, including PC, Mac, console, handheld and mobile.

China will remain a major contributor to overall app store consumer spend, including mobile gaming, but there may be a slight deceleration of their impact next year due to the game licensing freeze. In August, Bloomberg reported China’s regulators froze approval of game licenses amid a government shake-up. The freeze impacted the entire sector, from large players like internet giant Tencent to smaller developers.

If the freeze continues in 2019, App Annie believes Chinese firms will push toward international expansion and M&A activity could result.

App Annie is also predicting one breakout gaming hit for 2019: Niantic’s Harry Potter: Wizards Unite, which it believes will exceed $100 million in consumer spend in its first 30 days. Niantic’s Pokémon GO, by comparison, cleared $100 million in its first two weeks and became the fastest game to reach $1 billion in consumer spend.

But App Annie isn’t going so far as to predict Harry Potter will do better than Pokémon GO, which tapped into consumer nostalgia and was a first-to-market mainstream AR gaming title.

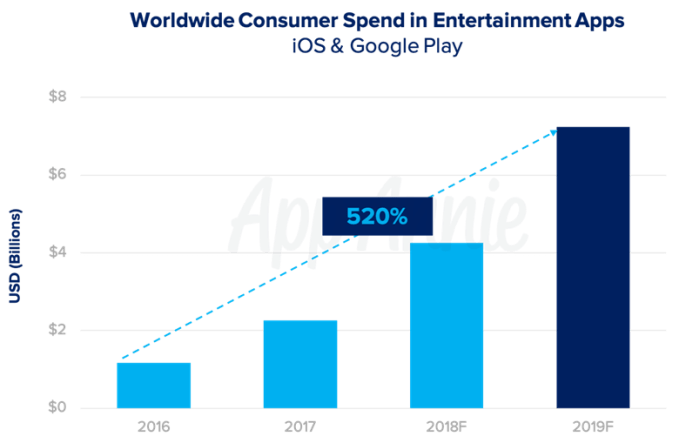

Another significant trend ahead for the new year is the growth in video streaming apps, fueled by in-app subscriptions.

Today, the average person consumers more than 7.5 hours of media per day, including watching, listening, reading or posting. Next year, 10 minutes of every hour will be spent consuming media across TV and internet will come from streaming video on mobile, the forecast says.

The total time in video streaming apps will increase 110 percent from 2016 to 2019, with consumer spend in entertainment apps up by 520 percent over that same period. Most of those revenues will come from the growth in in-app subscriptions.

Much of the time consumers spend streaming will come from short-form video apps like YouTube, TikTok and social apps like Instagram and Snapchat.

YouTube alone accounts for 4 out of every 5 minutes spent in the top 10 video streaming apps, today. But 2019 will see many changes, including the launch of Disney’s streaming service, Disney+, for example.

App Annie’s full report, which details ad creatives and strategies as well, is available on its blog.

Powered by WPeMatico

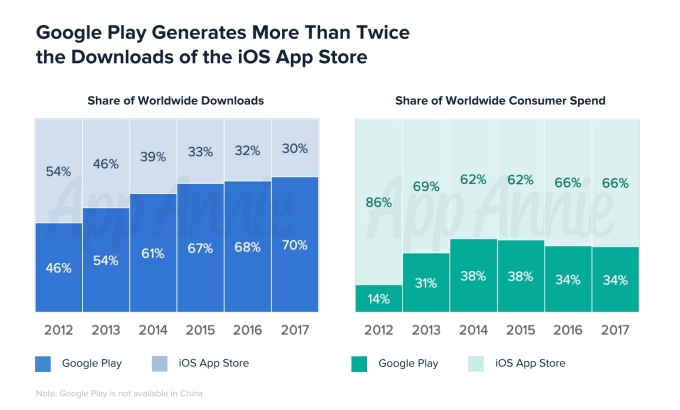

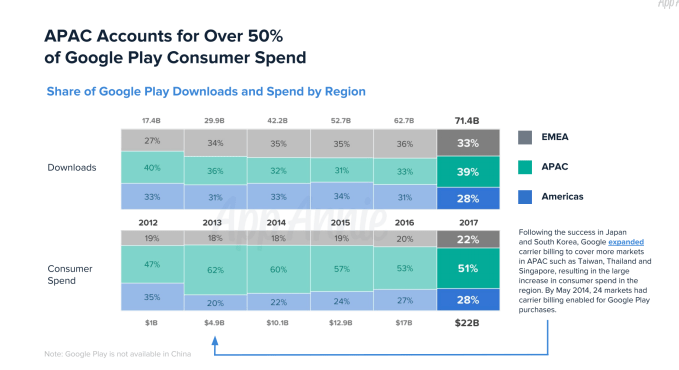

Google Play has generated more than twice the downloads of the iOS App Store, reaching a 70 percent share of worldwide downloads in 2017, according to a new report from App Annie, released in conjunction with the 10th anniversary of the Android Market, now called Google Play. The report also examined the state of Google Play’s marketplace and the habits of Android users.

It found that, despite the large share of downloads, Google Play only accounted for 34 percent of worldwide consumer spend on apps, compared with 66 percent on the iOS App Store in 2017 — a figure that’s stayed relatively consistent for years.

Those numbers are consistent with the narrative that’s been told about the two app marketplaces for some time, as well. That is, Google has the sheer download numbers, thanks to the wide distribution of its devices — including its reach into emerging markets, thanks to low-cost smartphones. But Apple’s ecosystem is the one making more money from apps.

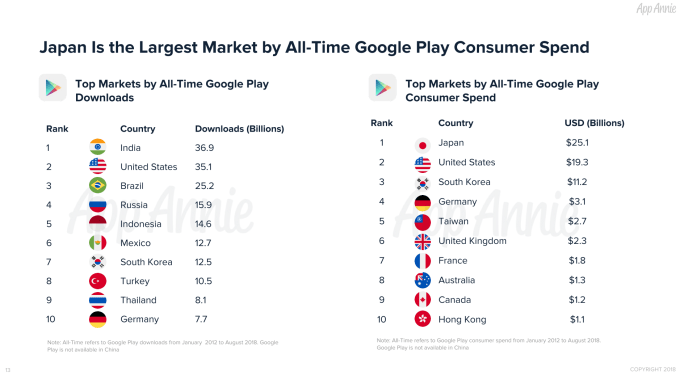

App Annie also found that the APAC (Asia-Pacific) region accounts for more than half of Google Play consumer spending. Japan was the largest market of all-time on this front, topping the charts with $25.1 billion dollars spent on apps and in-app purchases. It was followed by the U.S. ($19.3 billion) and South Korea ($11.2 billion).

The firm attributed some of Google Play’s success in Japan to carrier billing. This has allowed consumer spending to increase in markets like South Korea, Taiwan, Thailand and Singapore, as well, it said.

As to what consumers are spending their money on? Games, of course.

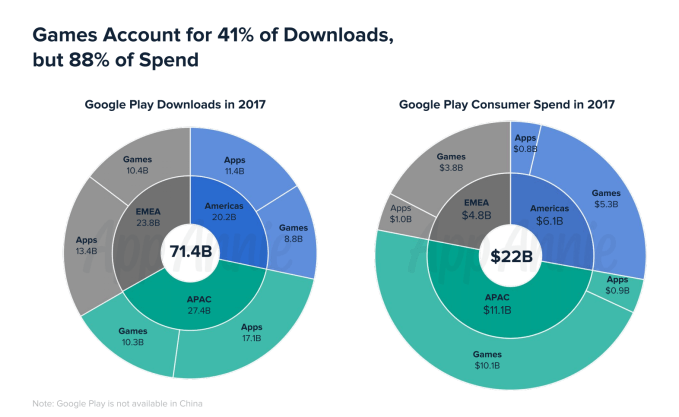

The report found that games accounted for 41 percent of downloads, but 88 percent of spend.

Outside of games, in-app subscriptions have contributed to revenue growth.

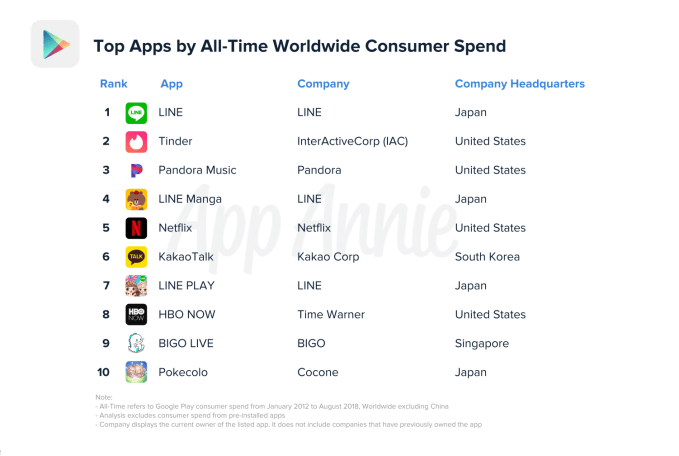

Non-game apps reached $2.7 billion in consumer spend last year, with 4 out of the top 5 apps offering a subscription model. The No. 1 app, LINE, was the exception. It was followed by subscription apps Tinder, Pandora, Netflix and HBO NOW.

In addition, App Annie examined the app usage patterns of Android users, and found they tend to have a lot of apps installed. In several markets, including the U.S. and Japan, Android users had more than 60 apps installed on their phones, and they used more than 30 apps every month.

Australia, the U.S. and South Korea led the way here, with users’ phones holding 100 or more apps.

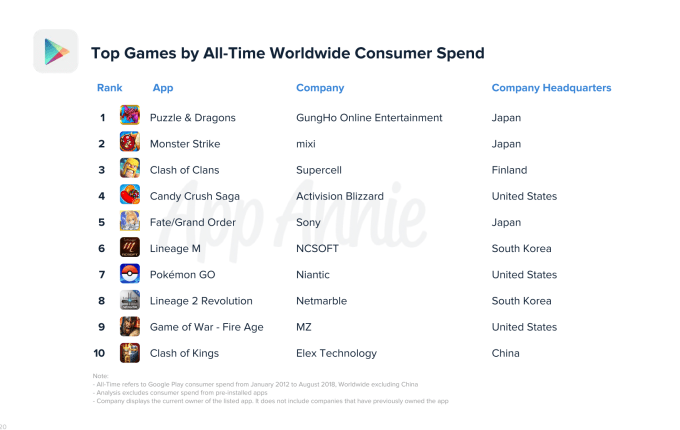

The report also looked at the most popular games and apps of all time by both downloads and consumer spend. There weren’t many surprises on these lists, with apps like those made by Facebook dominating the top apps by downloads list, and subscription services dominating top apps by spend.

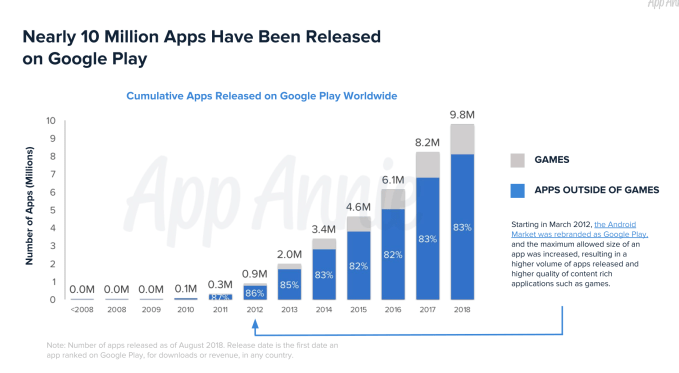

App Annie also noted Google Play has seen the release of nearly 10 million apps since its launch in 2008. Not all these remain, of course — by today’s count, there are just over 2.8 million apps live on Google Play.

The full report is available here.

Powered by WPeMatico

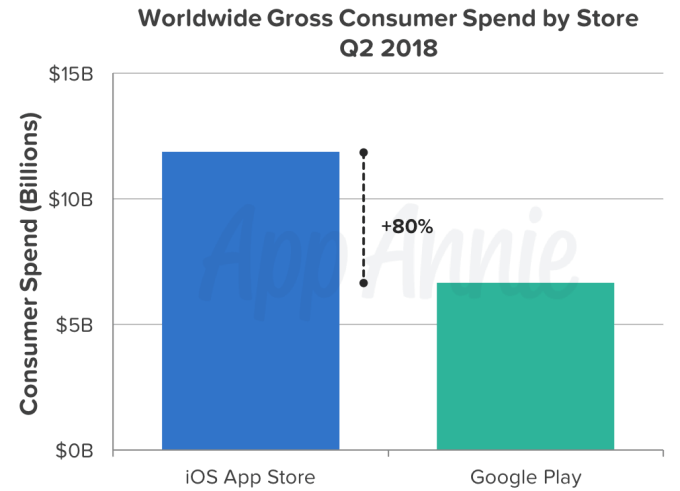

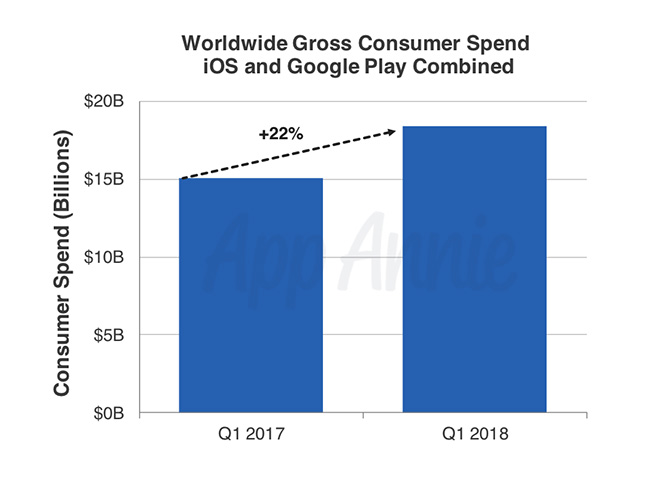

The second quarter of 2018 was another record-breaker for mobile app downloads and revenue. According to a new report this week from App Annie, there were over 28.4 billion app downloads worldwide across both iOS and Google Play in the quarter, up 15 percent year-over-year. That number is even more remarkable because it doesn’t include reinstalls or updates – only new app downloads. In addition, consumer spending in apps was up 20 percent year-over-year to reach $18.5 billion across iOS and Google Play combined.

This is the most money spent in apps compared with any other quarter before, the report notes, topping the prior quarter’s record-breaking $18.4 billion in app revenue, and 27.5 billion downloads.

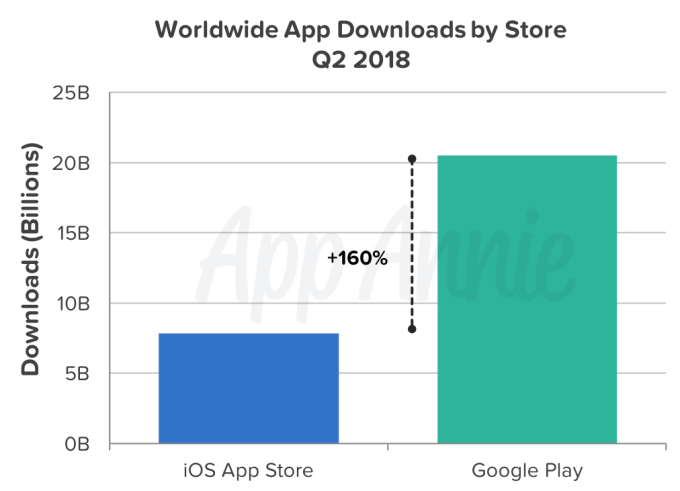

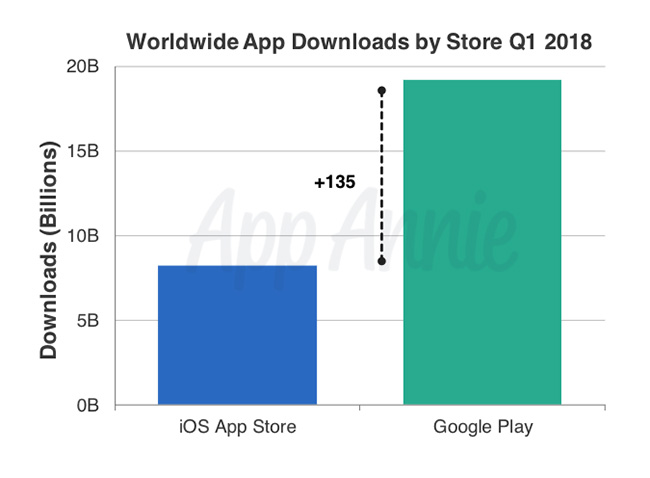

Much of the download activity in Q2 came from Google Play.

On its app marketplace alone, global downloads topped 20 billion, up 20 percent year-over-year and widening the gap between itself and iOS by 25 percent points to 160 percent. (See below).

This massive download growth is attributable largely to India, says App Annie .

The country was the biggest driver of download growth year-over-year in both absolute values and growth in market share. Indonesia also played a big role in Google Play downloads.

Meanwhile, the U.S., Russia and Saudi Arabia saw the largest growth in iOS downloads.

In particular, Google Play app downloads included growth in categories like games, video players and editors, and – not surprisingly, given the World Cup – sports applications. And on iOS, Sports apps were also the largest driver of global iOS downloads, followed by Finance and Travel apps.

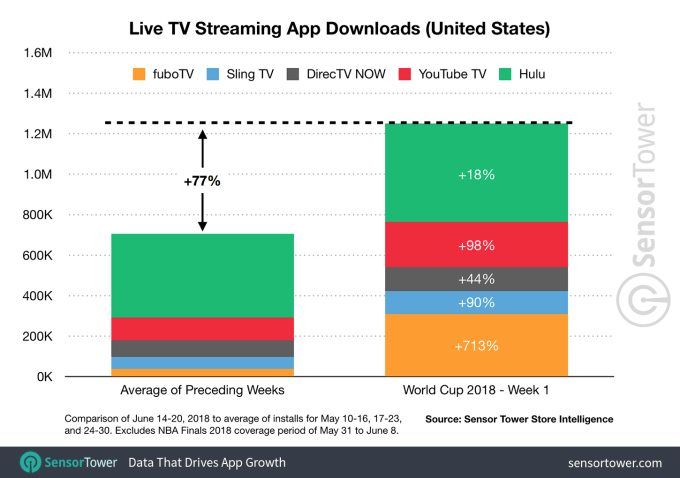

The impact on the 2018 FIFA World Cup on sports app downloads was also highlighted last month by Sensor Tower, whose own analysis found that new installs of the five leading live TV on demand apps offering channels with the World Cup grew 77 percent during the first week of World Cup coverage, compared with the three preceding weeks (excluding the NBA Finals period).

Sports streaming service fuboTV saw the largest impact, growing at a whopping 713 percent and adding 309K new users in the U.S., while Hulu saw the smallest impact at 18 percent growth.

Single network apps grew, too, this earlier report said. FOX Sports downloads increased by 95x for the same period, while Telemundo Deportes En Vivo grew 444x, for example.

App Annie added that the top 3 sports apps in Android in the U.S. during the first three weeks of the tournament were Telemundo Deportes (#1), FOX Sports GO (#2), and FOX Sports (#3), in terms of average megabytes per user – an indication of users’ live-streaming activity. The apps were also new entrants to the top 10 list of apps by total time spent, compared with the three weeks directly prior.

In the U.K., over 6 million hours were spent in the top 10 sports apps on Android during the first 3 weeks of the World Cup, up 65 percent from the 3 weeks prior.

The World Cup also had an impact on consumer spending in apps in the quarter.

Sports apps on iOS were the third largest contributors to absolute growth in consumer spend and in market share in Q2, while Entertainment and Productivity apps were numbers one and two, respectively. In-app subscriptions for both Sports and Entertainment apps drove the consumer spending increases.

On Google Play, Games, Social, and Music & Audio apps saw the largest download growth, quarter-over-quarter.

However, despite the downloads and consumer spending in sports and TV apps, the charts of the top 10 apps by worldwide downloads and consumer spending look a lot like they usually do – with Facebook apps dominating the top 10 by downloads (Messenger, Facebook, WhatsApp and Instagram were the top 4).

And the top 10 apps by spending were still largely those subscription-based entertainment services like Netflix, Tencent Video, iQIYI, Pandora, Youku, and YouTube.

Powered by WPeMatico

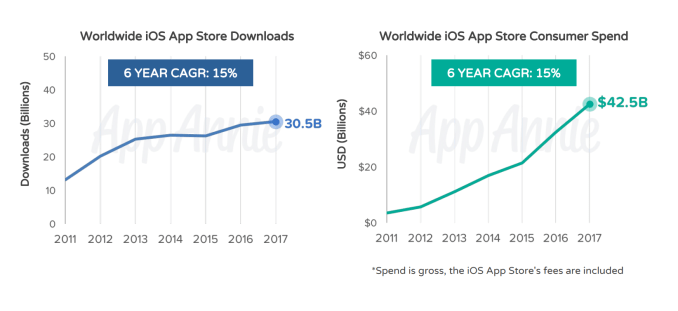

The App Store has seen over 170 billion downloads over the past decade, totaling over $130 billion in consumer spend. This data was shared this morning by app intelligence firm App Annie, which is marking the App Store’s 10th Anniversary with a look back on the store’s growth and the larger trends it’s seen. These figures aren’t the full picture, however – the App Store launched on July 10, 2008 with just 500 applications, but App Annie arrived in 2010. The historical data for this report, therefore, goes from July 2010 through December 2017.

That means the true numbers are even higher that what App Annie can confirm.

The report paints a picture of the continued growth of the App Store over the years, noting that iOS App Store revenue growth outpaces downloads, and that nearly doubled between 2015 to 2017.

iOS device owners apparently love to spend on apps, too.

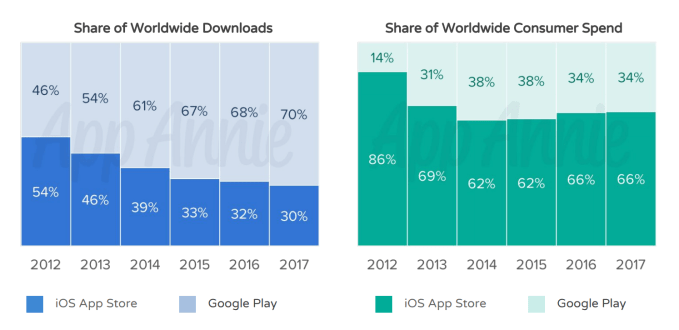

The iOS App Store only has a 30 percent share of worldwide downloads, but accounts for 66 percent of consumer spend, the report says.

But this isn’t a complete picture of the iOS vs. Android battle, as Google Play isn’t available in China. App Annie’s data is incomplete on this front as it’s not accounting for the third-party Android app stores in China.

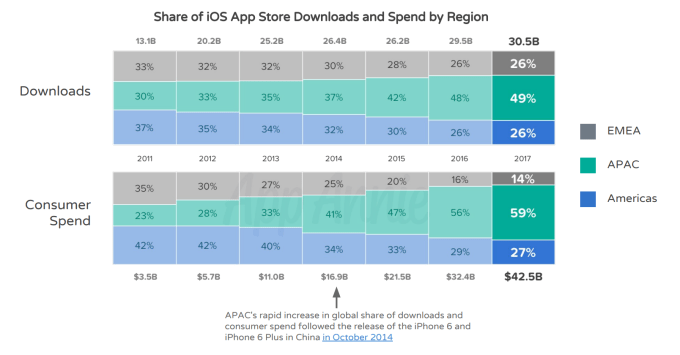

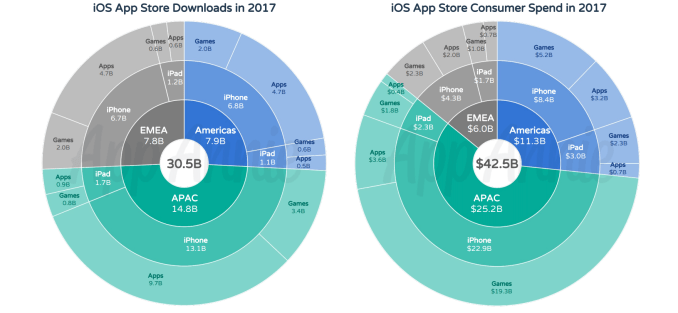

China today plays an outsized role, as App Annie has repeatedly reported, in terms of App Store revenue, even without Google Play. In fact, the APAC region accounts for nearly 60 percent of consumer spend – a trend that began in earnest with the October 2014 release of the iPhone 6 and 6 Plus in China.

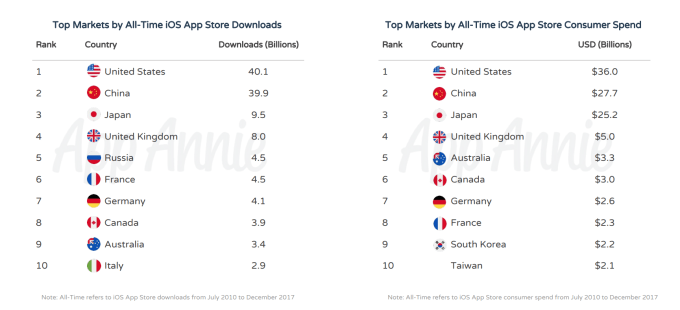

But when you look back at the App Store trends to date (or, as of July 2010 – which is as far back as App Annie’s data goes), it’s the U.S. that leads by a slim margin. China has quickly caught up but the U.S. is still the top country for all-time downloads, with 40.1 billion to China’s 39.9 billion; and it has generated $36 billion in consumer spend to China’s $27.7 billion.

iPhone users are heavy app users, too, the report notes.

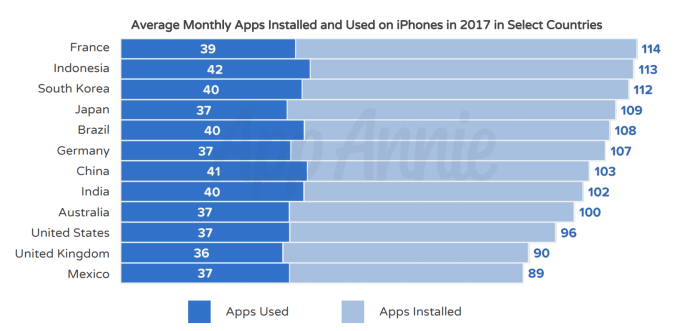

In several markets, users have 100 or more apps installed, including Australia, India, China, Germany, Brazil, Japan, South Korea, Indonesia, and France. The U.S., U.K., and Mexico come close, with 96, 90, and 89 average monthly apps installed in 2017, respectively.

Of course the numbers of apps used monthly are much smaller, but still range in the high 30’s to low 40’s, App Annie claims.

The report additionally examines the impact of games, which accounted for only 31 percent of downloads in 2017, but generated 75 percent of the revenue. The APAC regions plays a large role here as well, with 3.4 billion game downloads last year, and $19.3 billion in consumer spend.

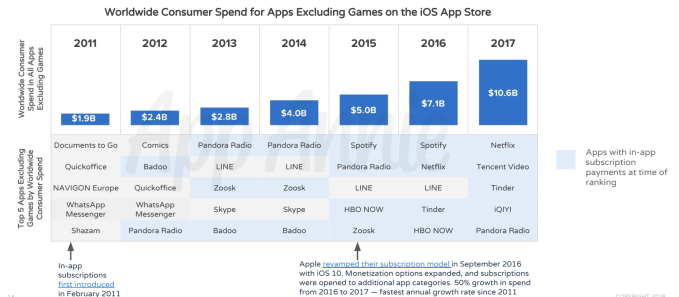

Subscriptions, meanwhile, are a newer trend, but one that’s already boosting App Store revenues considerably, accounting for $10.6 billion in consumer spend in 2017. This is driven mainly by media streaming apps like Netflix, Pandora, and Tencent Video, for example, but Tinder makes a notable showing as one of the top five worldwide apps by revenue.

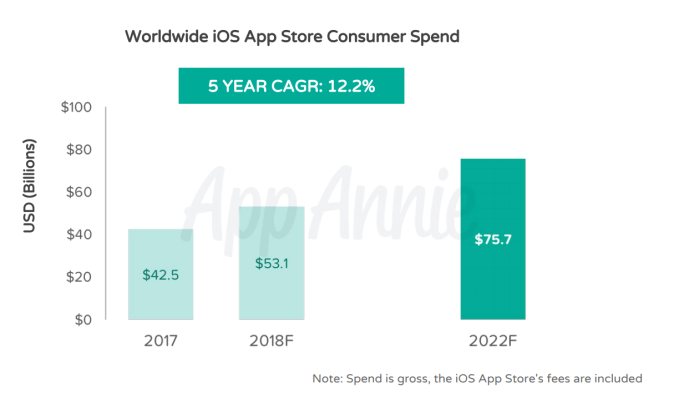

Thanks to subscriptions and other trends, App Annie predicts the worldwide iOS App Store revenue will grow 80 percent from 2017 to $75.7 billion by 2022.

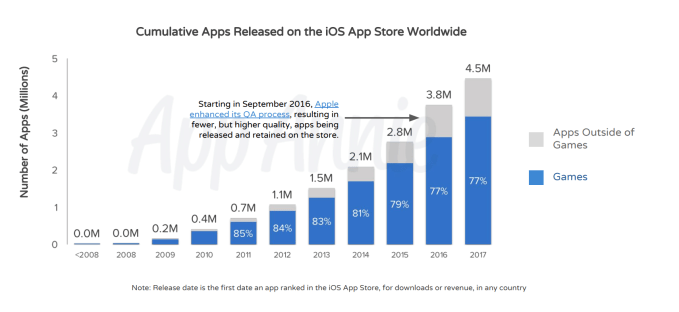

And while the App Store today has over 2 million apps, it has seen over 4.5 million apps released on its store to date. Many of these have been removed by Apple or the developers, which is why the number of live apps is so much lower.

The full report with the charts included is here.

Powered by WPeMatico

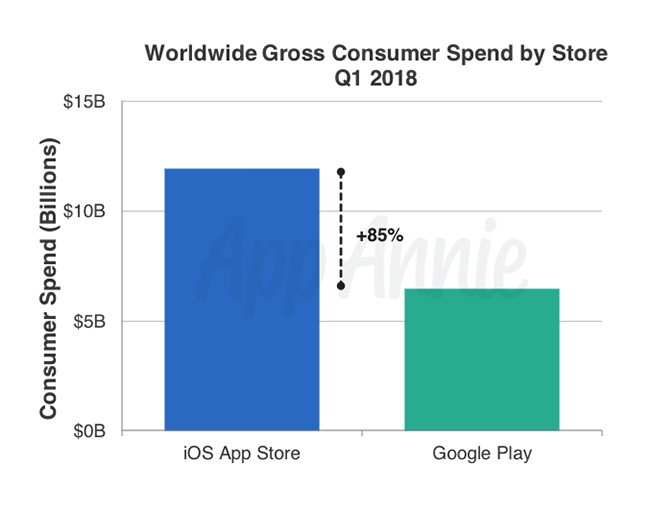

Global app downloads and consumer spending in apps had yet another record quarter, according to a new report from App Annie, out on Monday. In the first quarter of 2018, iOS and Google Play downloads grew more than 10 percent year-over-year to reach 27.5 billion – the highest figure to date. In addition, consumer spending on iOS and Google Play grew 22 percent year-over-year to reach $18.4 billion – also a record number.

The download figure is especially notable because App Annie is not counting app updates or re-installs. That means someone re-downloading an app on a new phone – like one received as a gift over the holidays – wouldn’t have been counted here. Only new app installs were counted.

Plus, the report points out that the total dollar amount to the app economy is much higher than the $18.4 billion reported for Q1, as App Annie only takes into account paid apps, in-app purchases, and subscriptions. It’s not measuring things like in-app advertising, the commerce taking place in apps (e.g. shopping and ride-sharing), or the money being made on the third-party Android app stores around the world.

This is not the first time App Annie has reported record numbers for downloads and consumer spending. The app marketplaces have continued to see steady growth, even as reports of app saturation in the U.S. circulate.

In Q4 2017 – the busy holiday quarter – the app stores had also broken these same records around downloads and revenues. Specifically, Google Play saw its highest downloads to date in the fourth quarter. The app stores had a record-breaking Q3 2017, too – something App Annie attributed then to the growth of the app market in China, India, and other Southeast Asian nations.

This time, App Annie pointed to India, Indonesia and Brazil’s impact on the year-over-year growth in Google Play downloads, and the U.S., Russia and Turkey’s impact on the growth of iOS downloads.

Also notable is that Google Play achieved another record of its own in Q1 2018, with record growth in consumer spend thanks to the U.S, followed by Japan and the Philippines. The Play Store grew 25 percent year-over-year, versus iOS’s 20 percent growth. Despite this, iOS continued to have a large lead in terms of total dollars spent.

Music & Audio along with Entertainment apps had a big impact on Google Play spending, the report noted, both on a quarter-over-quarter and year-over-year basis. This is attributed to the rise in music and video subscription services delivered via apps. App Annie isn’t the only one to spot this trend – app store intelligence firm Sensor Tower had previously found that top subscription video on demand apps grew by 77 percent in 2017, reaching $781 million in revenues across iOS and Google Play. And Netflix became 2017’s top non-game app by revenue.

App Annie said also that iOS spending in Q1 2018 benefitted from subscriptions to health and fitness apps, driven by New Year’s Resolutions and people’s embrace of the subscription model. The U.S., followed by the U.K. then Germany saw the largest market share growth quarter-over-quarter and year-over-year.

Combined, Google Play and the iOS App Store offered 6.2 million apps by the end of Q1 2018, with games driving downloads across both stores during the quarter. PUBG Mobile and Fortnite were especially big, App Annie noted.

Shopping apps also saw large year-over-year growth in market share, the report found.

More broadly, the new report is yet another example of how big a role emerging markets are having on app downloads and the app economy. This trend, while still remarkable, is not all that new. In 2016, China overtook the U.S. in App Store revenue, and App Annie has continued to note China, India and other emerging markets as key drivers of growth in its quarterly and annual reports.

Powered by WPeMatico

![]() Smartphone adoption in emerging markets just delivered the highest number of app downloads Google Play has ever seen in a quarter. According to today’s report from App Annie, Google Play app downloads topped 19 billion in Q4 2017, a new record. That also makes Google Play’s download lead over iOS its largest ever, at 145 percent. Specifically, the downloads were driven by… Read More

Smartphone adoption in emerging markets just delivered the highest number of app downloads Google Play has ever seen in a quarter. According to today’s report from App Annie, Google Play app downloads topped 19 billion in Q4 2017, a new record. That also makes Google Play’s download lead over iOS its largest ever, at 145 percent. Specifically, the downloads were driven by… Read More

Powered by WPeMatico