App Annie

Auto Added by WPeMatico

Auto Added by WPeMatico

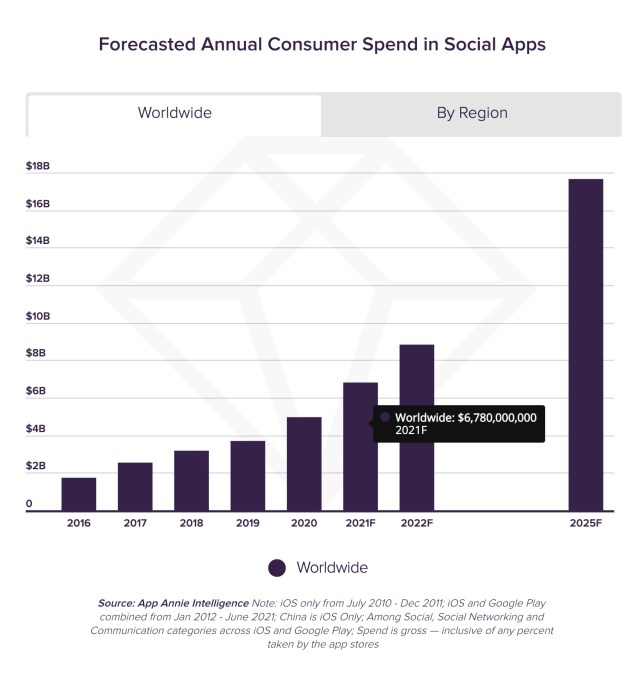

The livestreaming boom is driving a significant uptick in the creator economy, as a new forecast estimates consumers will spend $6.78 billion in social apps in 2021. That figure will grow to $17.2 billion annually by 2025, according to data from mobile data firm App Annie, which notes the upward trend represents a five-year compound annual growth rate (CAGR) of 29%. By that point, the lifetime total spend in social apps will reach $78 billion, the firm reports.

Image Credits: App Annie

Initially, much of the livestream economy was based on one-off purchases like sticker packs, but today, consumers are gifting content creators directly during their livestreams. Some of these donations can be incredibly high, at times. Twitch streamer ExoticChaotic was gifted $75,000 during a live session on Fortnite, which was one of the largest-ever donations on the game-streaming social network. Meanwhile, App Annie notes another platform, Bigo Live, is enabling broadcasters to earn up to $24,000 per month through their livestreams.

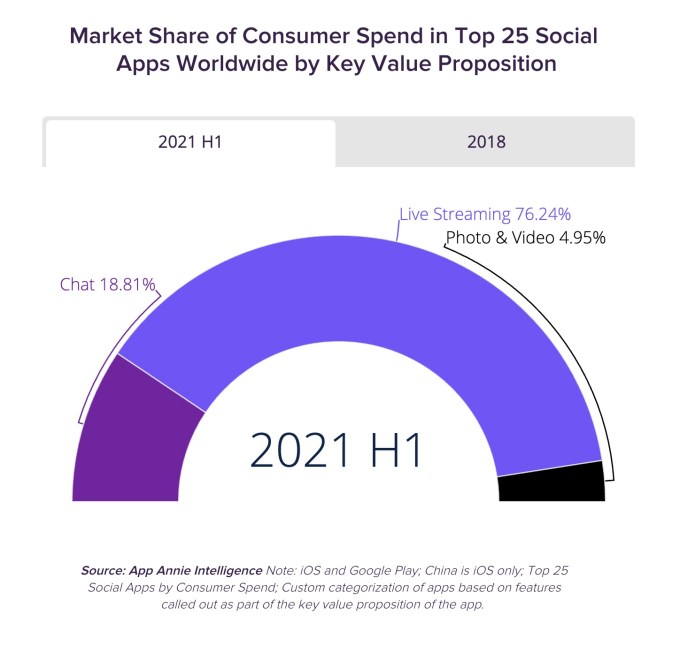

Apps that offer livestreaming as a prominent feature are also those that are driving the majority of today’s social app spending, the report says. In the first half of this year, $3 out every $4 spent in the top 25 social apps came from apps that offered livestreams, for example.

Image Credits: App Annie

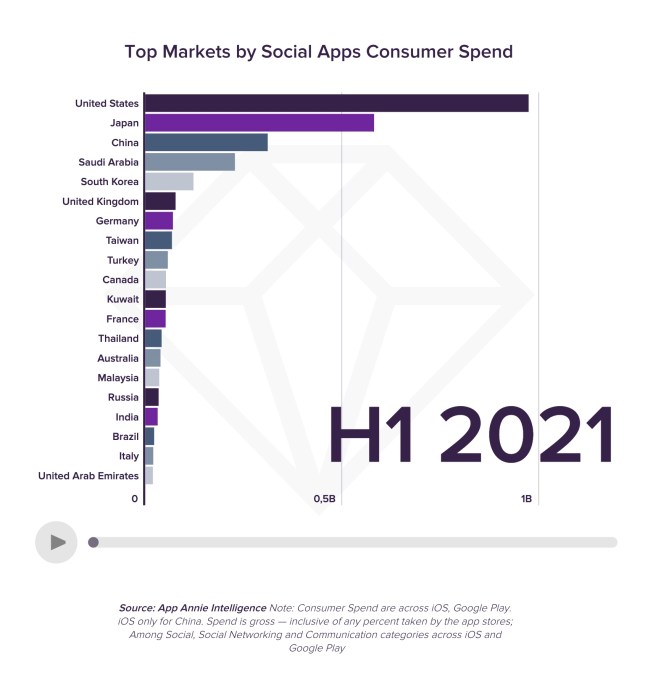

During the first half of 2021, the U.S. become the top market for consumer spending inside social apps, with 1.7x the spend of the next largest market, Japan, and representing 30% of the market by spend. China, Saudi Arabia and South Korea followed to round out the top 5.

Image Credits: App Annie

While both creators and the platforms are financially benefitting from the livestreaming economy, the platforms are benefitting in other ways beyond their commissions on in-app purchases. Livestreams are helping to drive demand for these social apps and they help to boost other key engagement metrics, like time spent in app.

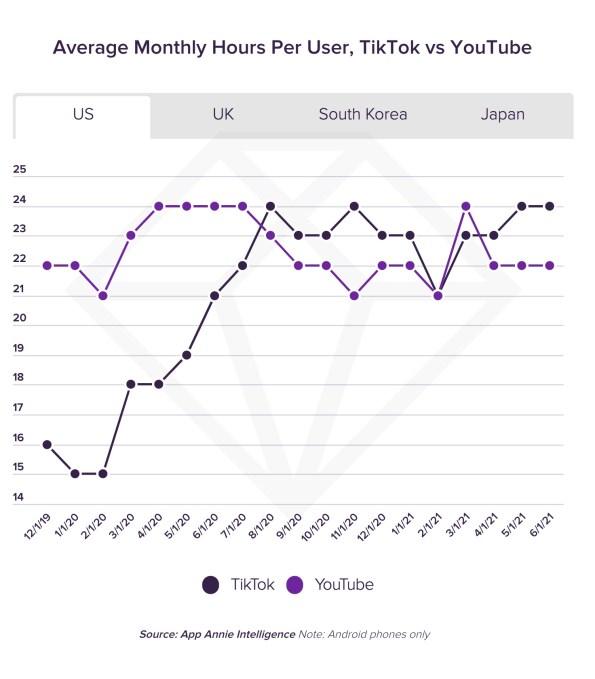

One top app that’s significantly gaining here is TikTok.

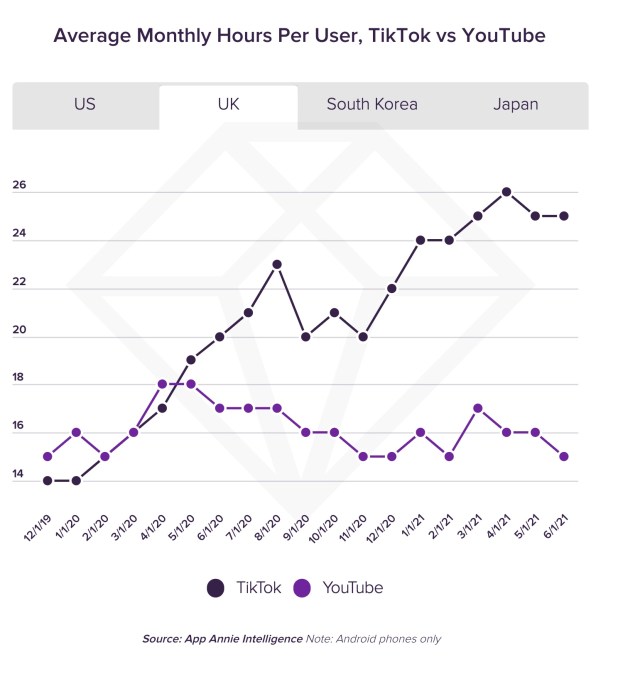

Last year, TikTok surpassed YouTube in the U.S. and the U.K. in terms of the average monthly time spent per user. It often continues to lead in the former market, and more decisively leads in the latter.

Image Credits: App Annie

Image Credits: App Annie

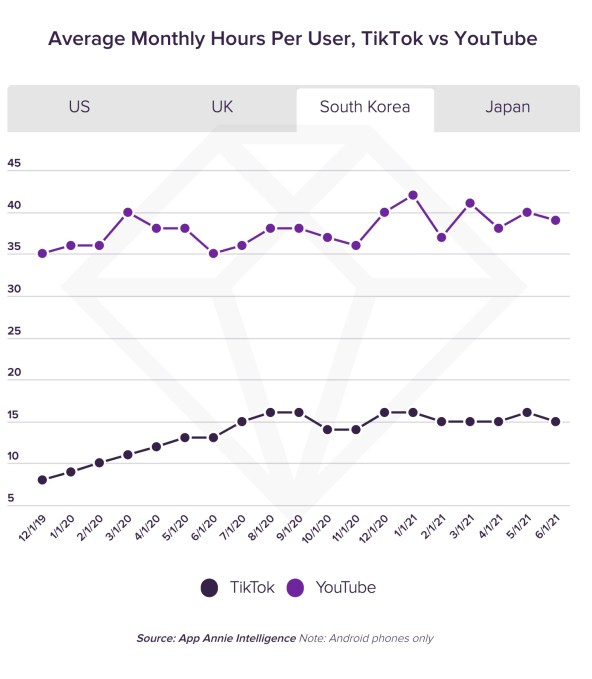

In other markets, like South Korea and Japan, TikTok is making strides, but YouTube still leads by a wide margin. (In South Korea, YouTube leads by 2.5x, in fact.)

Image Credits: App Annie

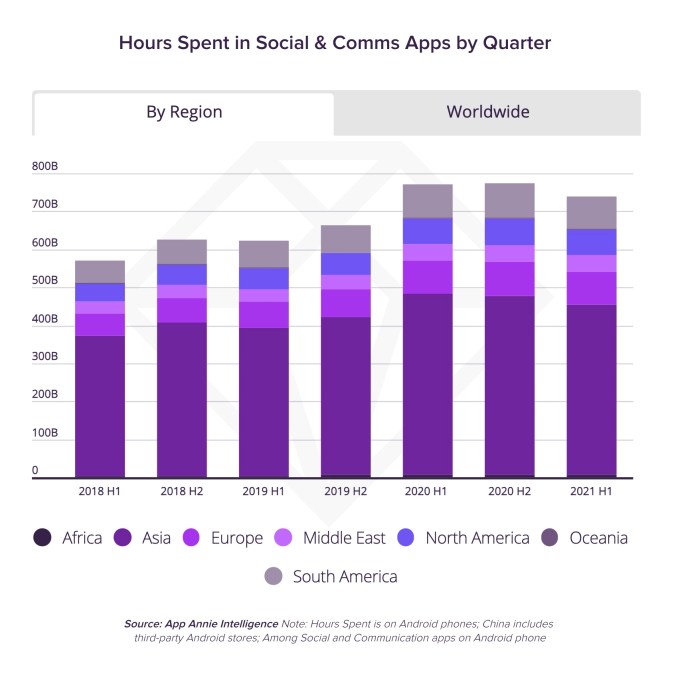

Beyond just TikTok, consumers spent 740 billion hours in social apps in the first half of the year, which is equal to 44% of the time spent on mobile globally. Time spent in these apps has continued to trend upwards over the years, with growth that’s up 30% in the first half of 2021 compared to the same period in 2018.

Today, the apps that enable livestreaming are outpacing those that focus on chat, photo or video. This is why companies like Instagram are now announcing dramatic shifts in focus, like how they’re “no longer a photo sharing app.” They know they need to more fully shift to video or they will be left behind.

The total time spent in the top five social apps that have an emphasis on livestreaming are now set to surpass half a trillion hours on Android phones alone this year, not including China. That’s a three-year CAGR of 25% versus just 15% for apps in the Chat and Photo & Video categories, App Annie noted.

Image Credits: App Annie

Thanks to growth in India, the Asia-Pacific region now accounts for 60% of the time spent in social apps. As India’s growth in this area increased over the past 3.5 years, it shrunk the gap between itself and China from 115% in 2018 to just 7% in the first half of this year.

Social app downloads are also continuing to grow, due to the growth in livestreaming.

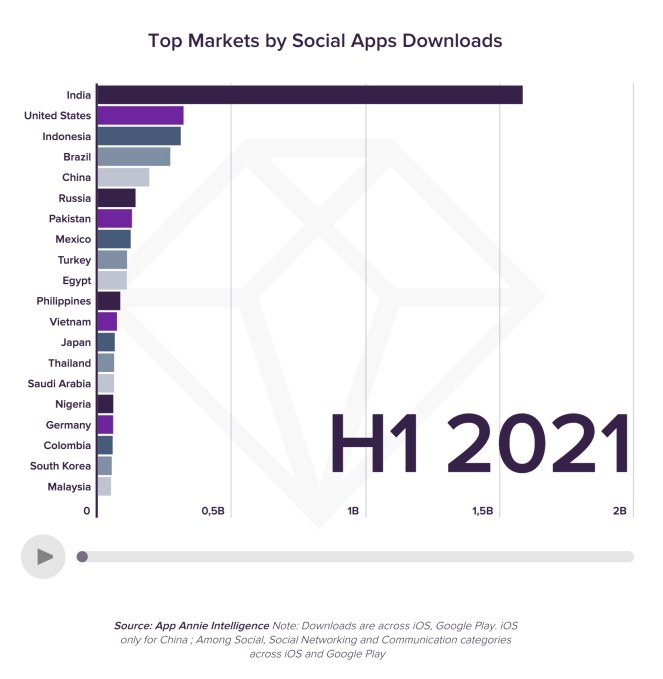

To date, consumers have downloaded social apps 74 billion times, and that demand remains strong, with 4.7 billion downloads in the first half of 2021 alone — up 50% year-over-year. In the first half of the year, Asia was the largest region region for social app downloads, accounting for 60% of the market.

This is largely due to India, the top market by a factor of 5x, which surpassed the U.S. back in 2018. India is followed by the U.S., Indonesia, Brazil and China, in terms of downloads.

Image Credits: App Annie

The shift toward livestreaming and video has also impacted what sort of apps consumers are interested in downloading, not just the number of downloads.

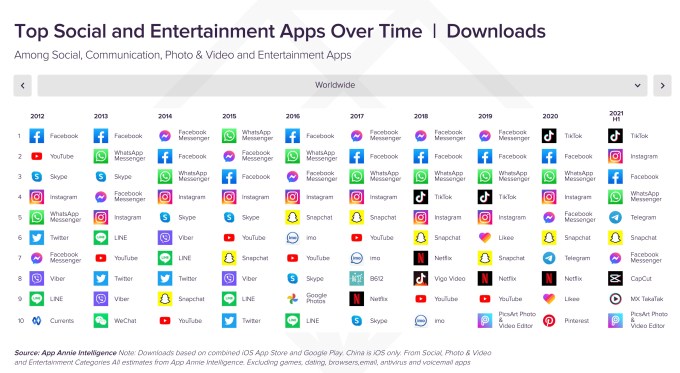

A chart that shows the top global apps from 2012 to the present highlights Facebook’s slipping grip. While its apps (Facebook, Messenger, Instagram and WhatsApp) have dominated the top spots over the years in various positions, TikTok popped into the number one position last year, and continues to maintain that ranking in 2021.

Further down the chart, other apps that aid in video editing have also overtaken others that had been more focused on photos or chat.

Image Credits: App Annie

Video apps like YouTube (#1), TikTok (#2) Tencent Video (#4), Bigo Live (#5), Twitch (#6), and others also now rank at the top of the global charts by consumer spending in the first half of 2021.

But YouTube (#1) still dominates in time spent compared with TikTok (#5), and others from Facebook — the company holds the next three spots for Facebook, WhatsApp and Instagram, respectively.

This could explain why TikTok is now exploring the idea of allowing users to upload even longer videos, by increasing the limit from 3 minutes to 5, for instance.

TikTok is testing a longer 5 minute video upload limit

pic.twitter.com/qiRbJmHkma

— Matt Navarra (@MattNavarra) August 25, 2021

In addition, because of livestreaming’s ability to drive growth in terms of time spent, it’s also likely the reason why TikTok has been heavily investing in new features for its TikTok LIVE platform, including things like events, support for co-hosts, Q&As and more, and why it made the “LIVE” button a more prominent feature in its app and user experience.

App Annie’s report also digs into the impact livestreaming has had on specific platforms, like Twitch and Bigo Live, the former which doubled its monthly active user base from the pre-pandemic era, and the latter which saw $314.2 million in consumer spend during H1 2021.

“The ability of social media users to communicate with each other using live video – or watch others’ live broadcasts – has not only maintained the growth of a social media app market, but contributed to its exponential growth in engagement metrics like time spent, that might otherwise have saturated some time ago,” wrote App Annie’s Head of Insights, Lexi Sydow, when announcing the new report.

The full report is available here.

Powered by WPeMatico

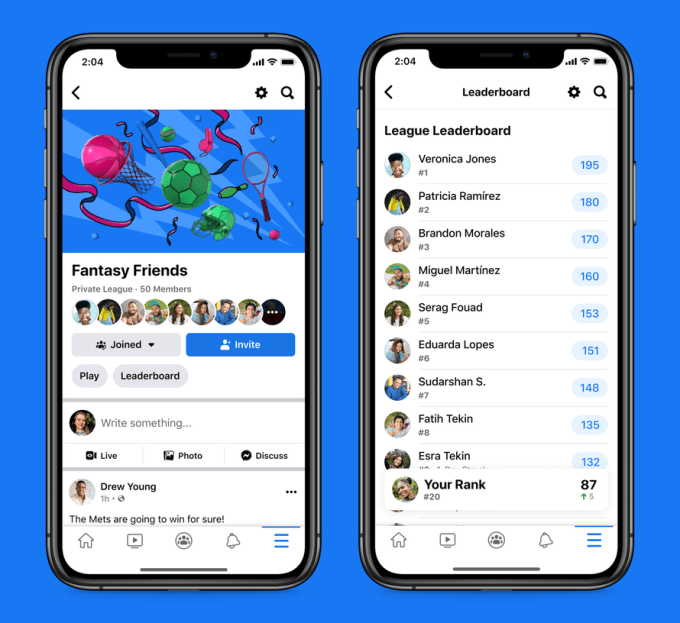

Facebook is getting into fantasy sports and other types of fantasy games. The company this morning announced the launch of Facebook Fantasy Games in the U.S. and Canada on the Facebook app for iOS and Android. Some games are described as “simpler” versions of the traditional fantasy sports games already on the market, while others allow users to make predictions associated with popular TV series, like “Survivor” or “The Bachelorette.”

The first game to launch is Pick & Play Sports, in partnership with Whistle Sports, where fans get points for correctly predicting the winner of a big game, the points scored by a top player or other events that unfold during the match. Players can also earn bonus points for building a streak of correct predictions over several days. This game is arriving today.

Image Credits: Facebook

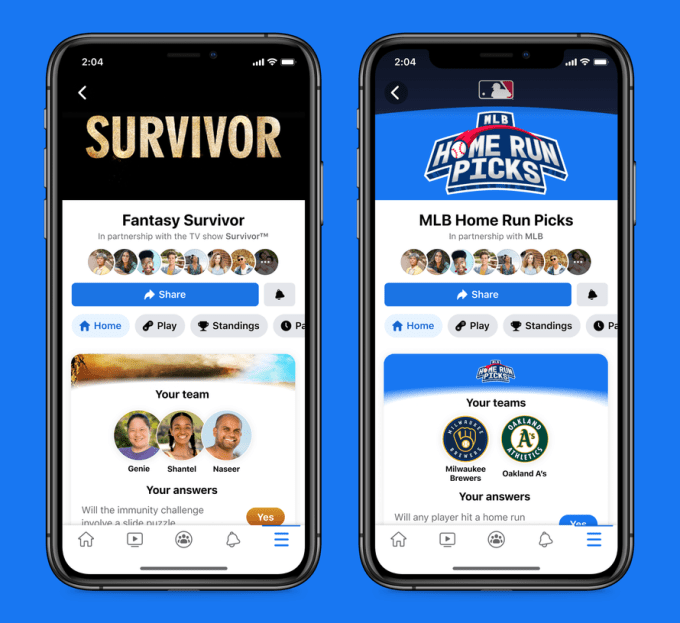

In the months ahead, it will be followed by other games in sports, TV and pop culture, including Fantasy Survivor, where players choose a set of castaways from the popular CBS TV show to join their fantasy team and Fantasy “The Bachelorette,” where fans will pick a group of men from the suitors vying for the Bachelorette’s heart and get points based on their actions and events that take place during the show. Other upcoming sports-focused games include MLB Home Run Picks, where players pick the team that they think will hit the most home runs, and LaLiga Winning Streak, where fans predict the team that will win that day.

In addition to top players being featured on leaderboards, games have a social component for those who want to play with friends.

Image Credits: Facebook

Players can create their own fantasy league with friends to compete with one another or against other fans, either publicly or privately. League members can compare scores with each other and will have a place where they can share picks, reactions and comments. This league area resembles a private group on Facebook, as it offers its own compose box for posting only to members, and its own dedicated feed. However, the page is designed to support groups with specific buttons to “play” or view the “leaderboard,” among others.

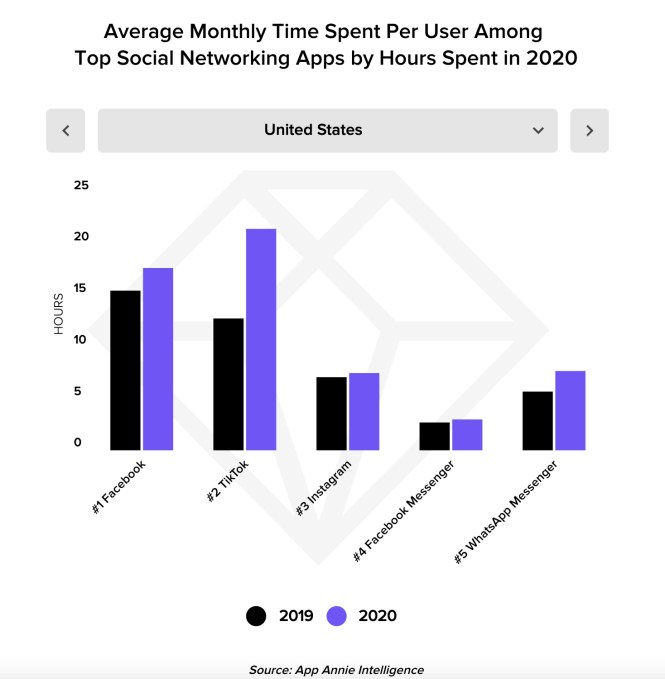

The addition of fantasy games could help Facebook increase the time users spent on its app at a time when the company is facing significant competition in social, namely from TikTok. According to App Annie, the average monthly time spent per user in TikTok grew faster than other top social apps in 2020, including by 70% in the U.S., surpassing Facebook.

Facebook had dabbled with the idea of becoming a second screen companion for live events in the past, but in a different way than fantasy sports and games. Instead, its R&D division tested Venue, which worked as a way for fans to comment on live events which were hosted in the app by well-known personalities.

The company has several other gaming investments, as well, including through its cloud gaming service on the desktop web and Android, its Games tab for streamers, and its VR company, Oculus.

The new league games will be available from the bookmark menu on the mobile app and in News Feed through notifications.

Powered by WPeMatico

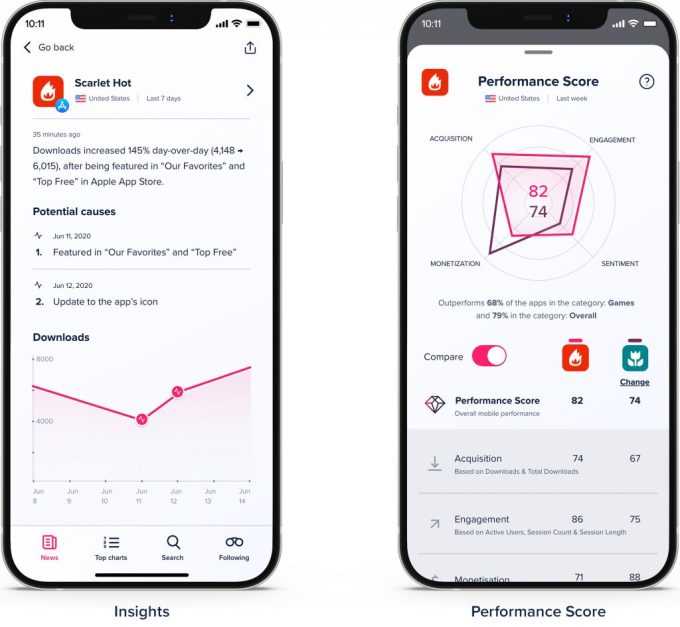

Mobile analytics and market data company App Annie launched a new app today that CEO Ted Krantz said is built not for the analyst who’s “immersed in the data,” but rather the executive who needs “a much more elevated, top-down view.”

The biggest new piece of the company’s Pulse app is something called the App Annie Performance Score, which Krantz compares to a FICO score for mobile apps. The idea is to take an app’s user acquisition, engagement, monetization and sentiment and boil them down into a single score that benchmarks how the app is performing relative to the competition.

Krantz said that eventually, the performance store could become more customizable for each customer, so that “you can tailor it to the metrics that matter to you.” The app also highlights any shifts in key app metrics and identifies potential causes, and it includes a newsfeed showing what’s happening to the apps and markets that a user follows.

Image Credits: App Annie

The goal, Krantz added, is to provide executives with a quick overview of the data they need without requiring them to dig through it or wait for a report — especially as “mobile is becoming such an imperative.” It’s the team’s “aspiration” to create an app that executives check every day, though he’s not necessarily expecting that to happen initially.

The Pulse app is based on App Annie’s market-level data, so Krantz said it shouldn’t be affected by Apple’s upcoming privacy changes. At the same time, he acknowledged that the company’s broader goals of bringing together first-party and third-party data are starting too look “a little tricky.”

App Annie Pulse is currently available on iOS, with the company planning to launch an Android version in the second quarter of this year. And while the full features of Pulse are only available to paying App Annie customers, Krantz said there are also plans for “revamping the free side of the equation and make that a little more meaty.”

Powered by WPeMatico

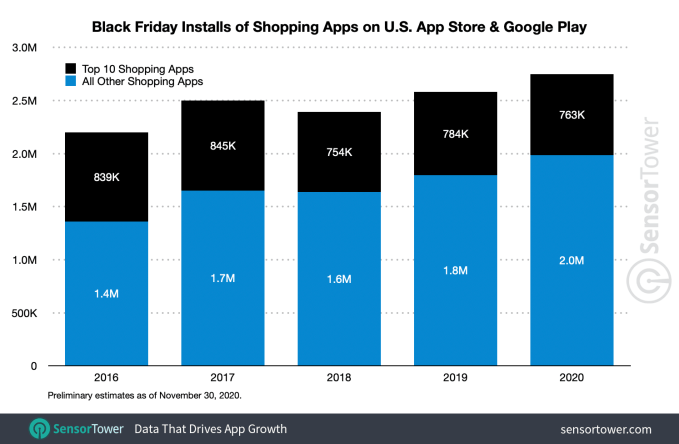

Many U.S. consumers spent this year’s Black Friday sales event shopping from home on mobile devices. That led to first-time installs of mobile shopping apps in the U.S. to break a new record for single-day installs on Black Friday 2020, according to a report from Sensor Tower. The firm estimates that U.S. consumers downloaded approximately 2.8 million shopping apps on November 27th — a figure that’s up by nearly 8% over last year.

However, this number doesn’t necessarily represent faster growth than in 2019, which also saw about an 8% year-over-year increase in Black Friday shopping app installs, the report noted. This could be because mobile shopping and the related app installs are now taking place throughout the month of November, though, as retailers adjusted to the pandemic and other online shopping trends by hosting earlier sales or even month-long sales events.

Image Credits: Sensor Tower

The data seems to indicate this is true. Between November 1 and November 29, U.S. consumers downloaded approximately 59.2 million shopping apps from across the App Store and Google Play — an increase of roughly 15% from the 51.7 million they downloaded in Novenber 2019. That’s a much higher figure than the 2% year-over-year growth seen during this same period in 2019.

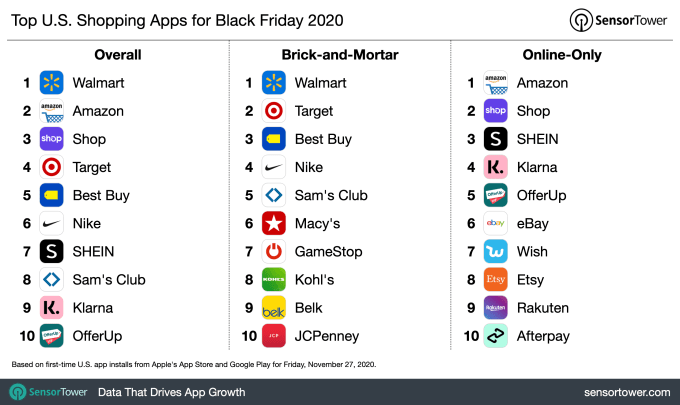

Another shift taking place in mobile shopping is the growing adoption of apps from brick-and-mortar retailers. During the first three quarters of 2020, apps from brick-and-mortar retailers grew installs 27%. This trend continued on Black Friday, when five out of the top 10 mobile shopping apps were those from brick-and-mortar retailers, led by Walmart.

Image Credits: Sensor Tower

Walmart saw the highest adoption this year, with around 131,000 Black Friday installs, followed by Amazon at 106,000, then Shopify’s Shop at 81,000. Combined, the top 10 apps saw 763,000 total new installs, or 27% of the first-time downloads in the Shopping category.

Because the firms are only looking at new app installs, they aren’t giving a full picture of the U.S. mobile shopping market, as many consumers already have these apps installed on their devices. And many more simply shop online via a desktop or laptop computer.

To give these figures some context, Shopify reported on Saturday it had seen record Black Friday sales of $2.4 billion, with 68% on mobile. And today, Amazon announced its small business sales alone topped $4.8 billion from Black Friday to Cyber Monday, a 60% year-over-year increase, but it didn’t break out the percentage that came from mobile.

Sensor Tower and rival app store analytics firm App Annie largely agreed on the top five shopping apps downloaded this Black Friday. They both saw Walmart again beating Amazon to become the most-downloaded U.S. shopping app on Black Friday — as it did in 2019. The two firms reported that Amazon remained No. 2 by downloads, followed by Shopify’s Shop app, then Target. However, Sensor Tower put Best Buy in fifth place, followed by Nike, while App Annie saw those positions swapped.

Image Credits: App Annie

The rest of Sensor Tower’s top 10 included SHEIN, Sam’s Club, Klarna, then Offer Up, while App Annie’s list was rounded out by SHEIN, Sam’s Club, Wish, then Offer Up.

The pandemic’s impact may not have been obvious given the growth in online shopping this year, but the recession it triggered has played a role in how U.S. consumers are paying for their purchases. “Buy Now, Pay Later” apps like Klarna were up this year, even breaking into the top 10 per Sensor Tower’s data. The firm also noted that many new shopping apps launched this year focused on discounts and deals, and retailers ran longer sales this year, as well.

Powered by WPeMatico

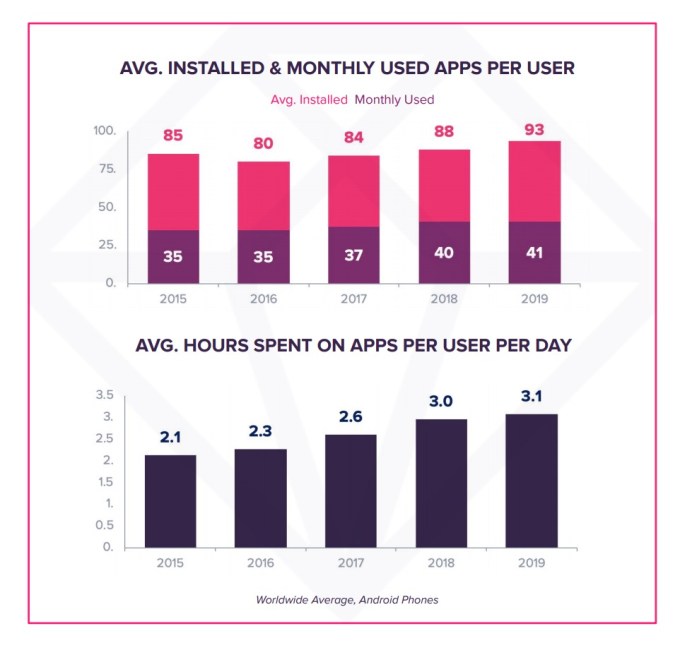

Mobile consumers are downloading and using more apps than ever before. According to recent data from App Annie, mobile users now have 93 apps on their phone as of the end of 2019, up from 85 apps at the end of 2015. They also now use around 41 apps per month, up from 35 in 2015. Related to this increase, users are now also spending more hours per day using apps. Worldwide, daily time spent in apps has grown to 3.1 hours per day in 2019, up from 2.1 hours per day in 2015, for instance.

But with that growth has also come increased diversity among the top apps, the report found. That means top apps now make up a smaller proportion of consumers’ total time spent in apps, compared with five years ago.

Image Credits: App Annie

It’s worth noting that this report was commissioned by Facebook, App Annie says, with a goal of offering a more detailed look at the evolving app ecosystem over the past five years. The report aims to determine how growth is playing out in terms of popular app categories, among the top publishers, and how quickly newly successful apps are achieving sizable growth.

Facebook, in the past, had generated this sort of market research data first-hand by way of its Onavo VPN application — now shuttered over privacy concerns — and other similar efforts.

Turning to App Annie’s data team is just a new way for the company to get at the same sort of data.

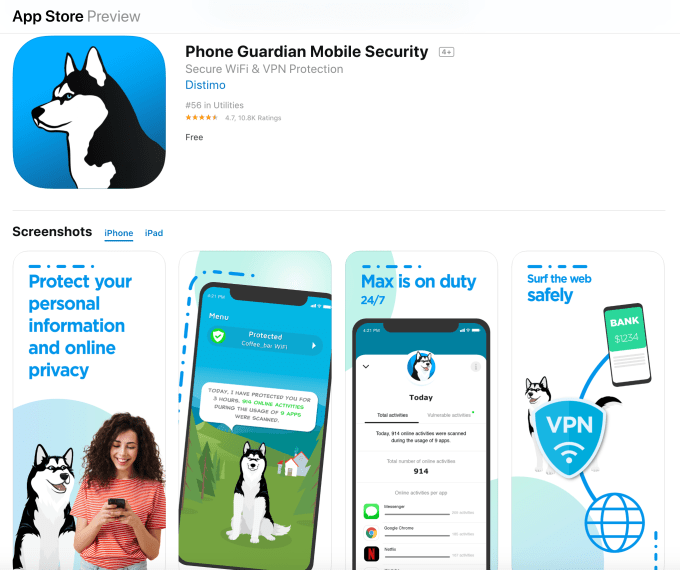

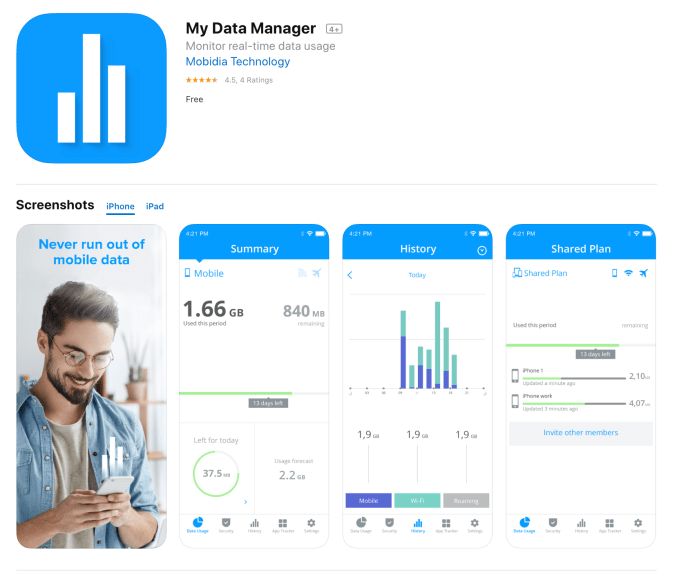

App Annie’s market analysis, in part, is similarly derived by way of third-party apps. The company acquired Distimo in 2014, and as of 2016 has run the VPN app Phone Guardian under the Distimo brand. It also acquired Mobidia in 2015 and has operated My Data Manager (now on the App Store under Distimo). Both apps disclose their relationship with App Annie and explain that the apps are used for market research purposes, with specific examples of the type of data collected.

The new report’s findings may not be all good news for Facebook and other top app publishers. As the app economy evolved, users now have more places to spend time on mobile.

Image Credits: App Annie

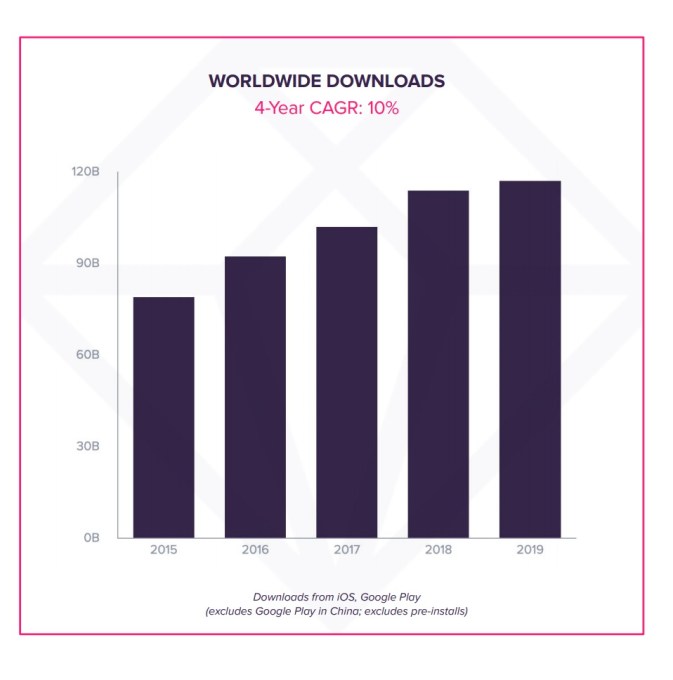

Over the past five years, worldwide downloads continued to grow to reach a record of 120 billion in 2019, with several key countries now driving growth, including India (10% year-over-year growth in 2019), Brazil (9%), Indonesia (8%) and Russia (7%).

Downloads in mature economies also hit record levels in 2019, including the U.S. (12.3 billion), Japan (2.5 billion), U.K. (2.1 billion), South Korea (2 billion), Germany (1.9 billion), and France (1.9 billion).

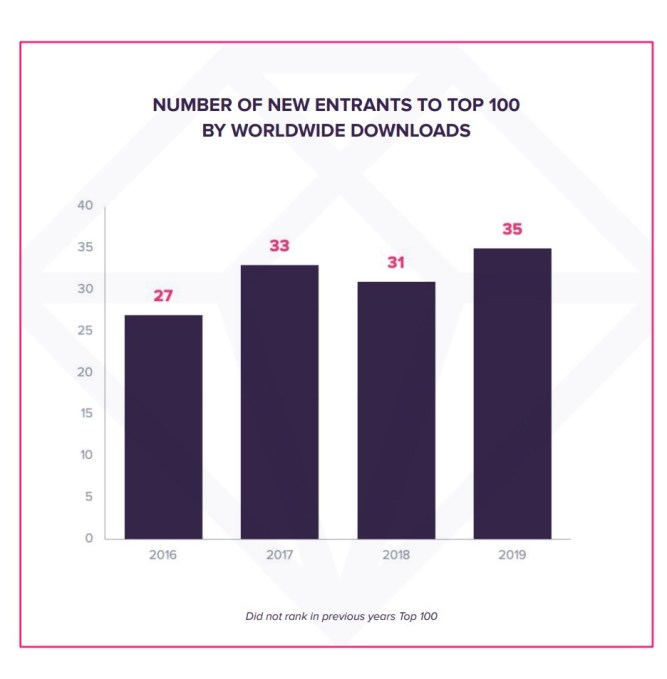

As users grew their time in app to 3.1 hours per day, they also began to use more of a variety of apps. According to the report, 35 of the top 100 apps were new entrants in 2019, up from 27 in 2016 across categories that included social, photography, video, communications, entertainment and more.

Image Credits: App Annie

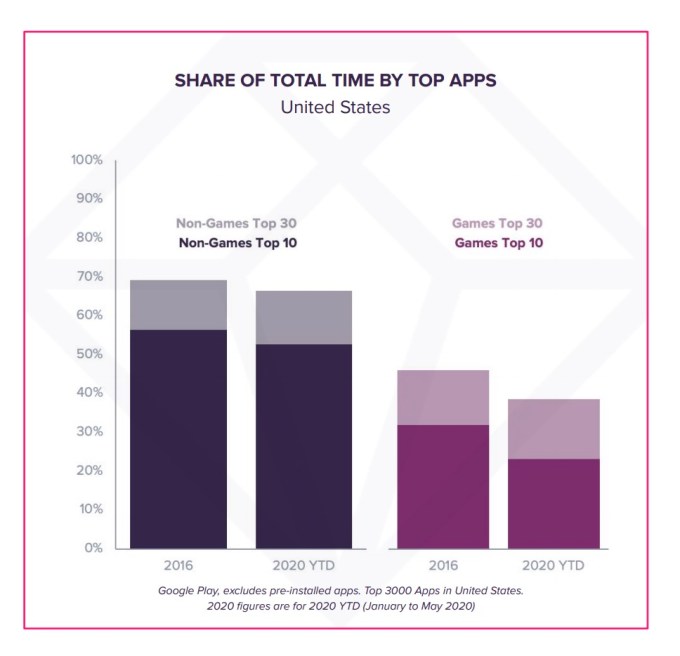

This is likely worrisome data for top app publishers, like Facebook, which has for years maintained a suite of top apps, including not only its flagship app, but also Instagram, Messenger and WhatsApp. As the competitive pressure increases, these top apps make up a smaller proportion of the time spent on mobile devices as users have grown more comfortable trying out newcomers — particularly across gaming, entertainment and video categories.

The top 30 non-game apps accounted for 69.4% of U.S. users’ total time spent in 2016 among non-games. That dropped to 65.5% in 2019, a nearly 4% decline. Among games, the share fell from 49% to 39%, a 10% drop. (This data was sourced from Google Play in the U.S.)

Image Credits: App Annie

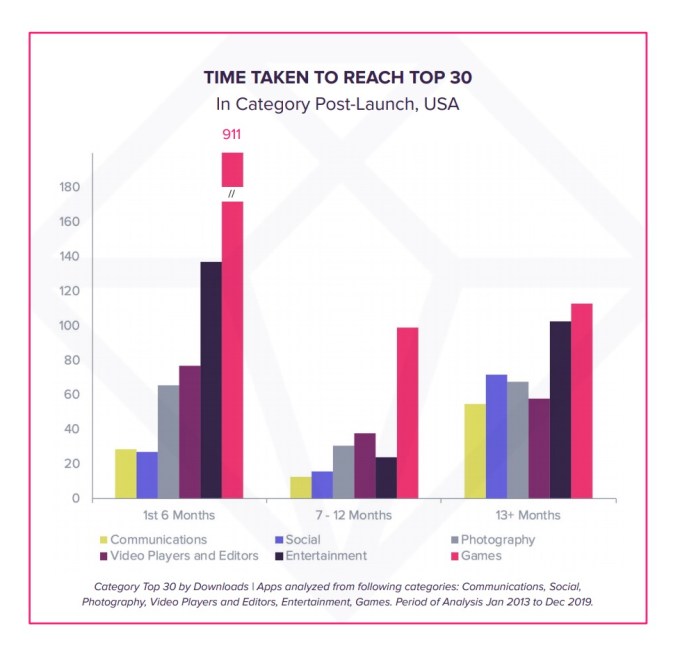

Not only are consumers more open to trying new apps, the report found that new apps can also quickly achieve app store success. In the U.S., for example, more than 60% of apps are able to reach their category’s Top 30 in their first six months.

This is aided by larger initial marketing pushes as well as improvements in terms of consumer’s devices themselves — like more storage and processing power, which encourages more downloads.

Image Credits: App Annie

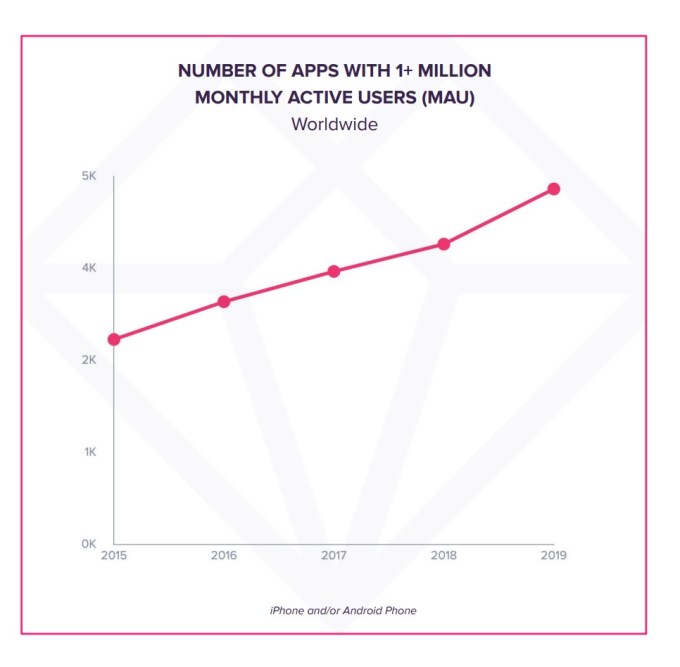

There are also more apps capable of achieving the once milestone metric of 1 million monthly active users (MAUs). In 2019, more than 4,600 apps saw 1 million MAUs, including those outside of social and communications like Netflix, Roku, Disney, CBS, Amazon, Alibaba, Walmart, Target, PayPal, Venmo, Chase, Capital One, Uber, DoorDash, McDonald’s and Starbucks.

Image Credits:App Annie

Image Credits: App Annie

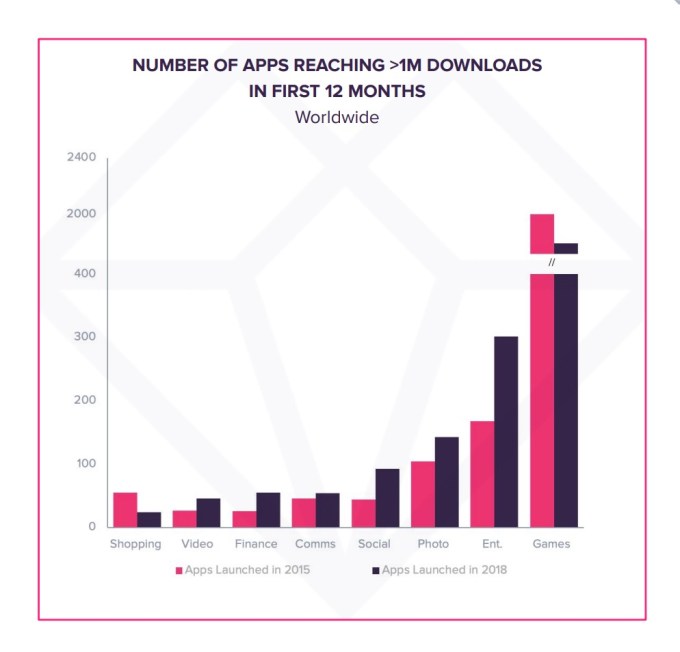

Apps are also achieving the 1 million downloads milestones more quickly, in data analyzed from 2015 to 2018. In the video, finance, communications, social, photo and entertainment categories, 67% of apps achieved the 1 million downloads milestone within their first 12 months, App Annie says.

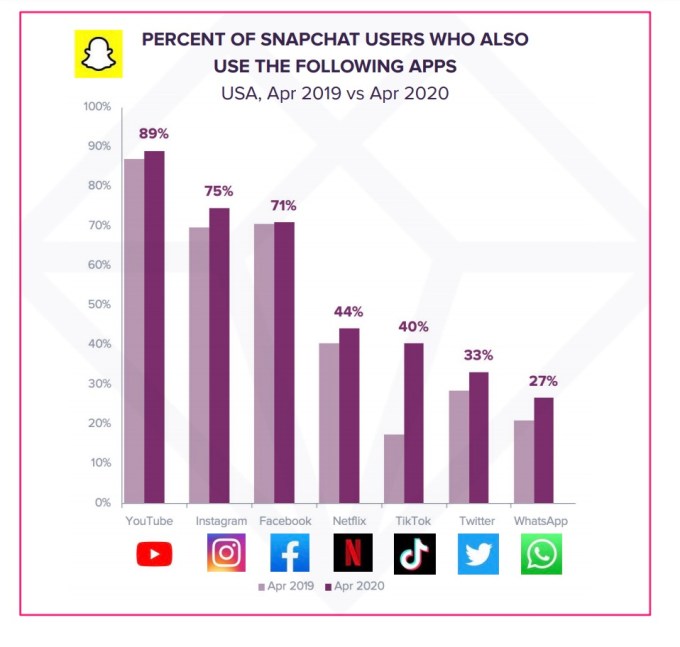

Because of the increases, there’s now a lot of overlap in between top apps. Today, mobile consumers will often choose and use multiple apps within and across categories to address similar needs, including on social, the report found.

For example, 89% of Snapchat’s users also used YouTube in April 2020 in the U.S., and 75% also used Instagram.

Image Credits: App Annie

TikTok saw the greatest year-over-year increase in cross-app usage of Snapchat, rising from 17% in April 2019 to April 2020 — an indication of how much it has captured the youth demographic.

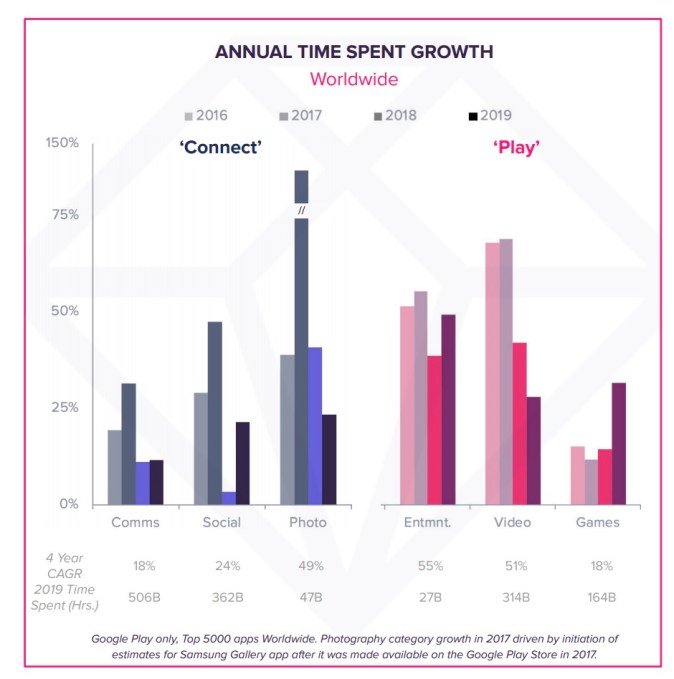

Meanwhile, video apps and gaming are taking up more of users’ time spent in apps. This broad category of “play”-focused apps accounted for 22% of the growth in time spent in apps in 2019.

Image Credits: App Annie

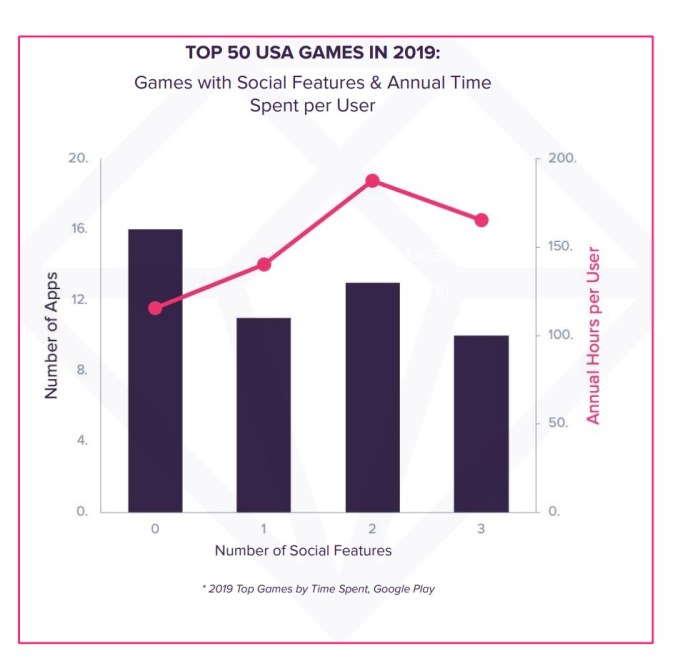

Plus, top gaming apps are also implementing social features, including Top 50 games like Fortnite, Clash of Clans, Call of Duty: Mobile, Township, Star Wars: Galaxy of Heroes, New Yahtzee with Buddies, Golf Clash and Slotomania, for example.

More than two-thirds of the Top 50 games have added at least one social feature, whether that’s inviting friend to play, social assists for progressing, guilds or clans or in-app chat. This, in turn, has led to players spending more time in games as they can connect with friends there.

Image Credits: App Annie

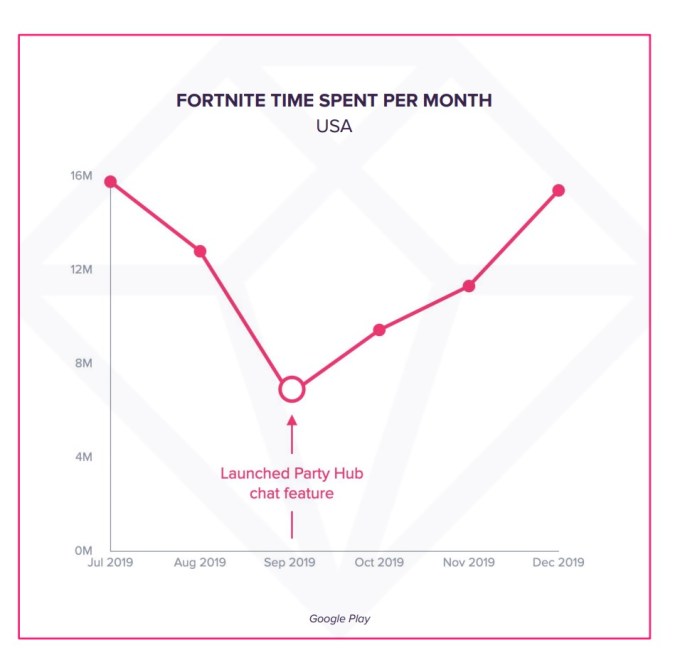

Fortnite, as one key example of this trend, rolled out Party Hub based on its acquired Houseparty technology, in September 2019. In the three months after the rollout, time spent in Fortnite grew 130%.

Image Credits: App Annie

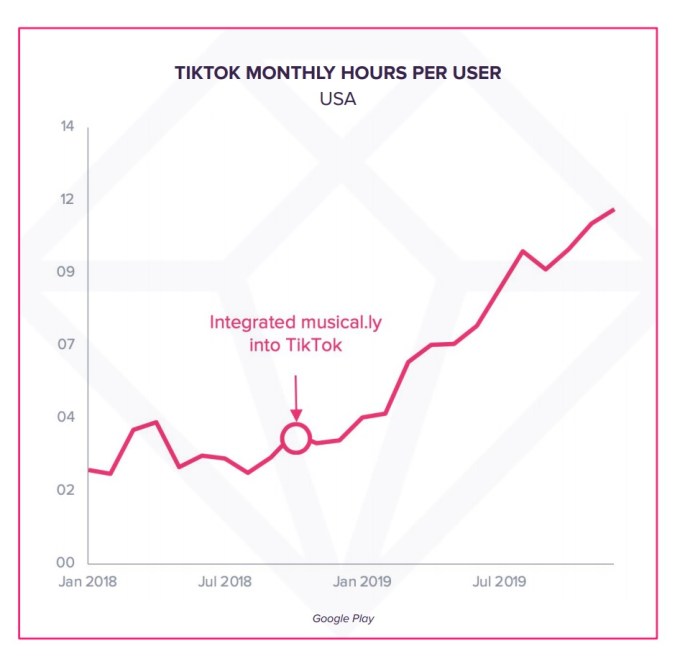

Outside of games, TikTok has risen by blending elements of top categories like social, video and entertainment. After merging with Musical.ly, it has rapidly rolled out more video editing features and increased ad spend aggressively to grow its user base and drive engagement. By December 2019, U.S. users were spending 16 hours, 20 minutes in the app per month, on average, up from 5 hours, 4 minutes in August 2018.

Image Credits: App Annie (note above chart only showcases Google Play data)

The full report also delves into country-by-country breakdowns but, overall, found that most countries saw record downloads in 2019 and similar trends in terms of app usage frequency increases and time spent.

One notable point of comparison is that U.S. users have more apps installed than in other markets (97 versus 93), but tend to use fewer apps compared with worldwide trends (36 versus 41). They also spend slightly fewer hours per day in apps, on average, than the worldwide average at 2.7 hours versus 3.1 hours.

“This report shows that the app industry is more competitive today than ever. New companies are succeeding with innovative apps that meet needs people might not even know they have,” said Ime Archibong, head of Facebook’s New Product Experimentation team, an internal team at Facebook looking to find new models for social apps. “All of this choice and competition fuels innovation, and that’s the heart of our work at Facebook,” he added.

App Annie’s report is available upon request here.

Powered by WPeMatico

The underpinnings of how app store analytics platforms operate were exposed this week by BuzzFeed, which uncovered the network of mobile apps used by popular analytics firm Sensor Tower to amass app data. The company had operated at least 20 apps, including VPNs and ad blockers, whose main purpose was to collect app usage data from end users in order to make estimations about app trends and revenues. Unfortunately, these sorts of data collection apps are not new — nor unique to Sensor Tower’s operation.

Sensor Tower was found to operate apps such as Luna VPN, for example, as well as Free and Unlimited VPN, Mobile Data and Adblock Focus, among others. After BuzzFeed reached out, Apple removed Adblock Focus and Google removed Mobile Data. Others are still being investigated, the report said.

Apps’ collection of usage data has been an ongoing issue across the app stores.

Facebook and Google have both operated such apps, not always transparently, and Sensor Tower’s key rival App Annie continues to do the same today.

For Facebook, its 2013 acquisition of VPN app maker Onavo for years served as a competitive advantage. The traffic through the app gave Facebook insight into which other social applications were growing in popularity — so Facebook could either clone their features or acquire them outright. When Apple finally booted Onavo from the App Store half a decade later, Facebook simply brought back the same code in a new wrapper — then called the Facebook Research app. This time, it was a bit more transparent about its data collection, as the Research app was actually paying for the data.

But Apple kicked out that app, too. So Facebook last year launched Study and Viewpoints to further its market research and data collection efforts. These apps are still live today.

Google was also caught doing something similar by way of its Screenwise Meter app, which invited users 18 and up (or 13 if part of a family group) to download the app and participate in the panel. The app’s users allowed Google to collect their app and web usage in exchange for gift cards. But like Facebook, Google’s app used Apple’s Enterprise Certificate program to work — a violation of Apple policy that saw the app removed, again following media coverage. Screenwise Meter returned to the App Store last year and continues to track app usage, among other things, with panelists’ consent.

App Annie

App Annie, a firm that directly competes with Sensor Tower, has acquired mobile data companies and now operates its own set of apps to track app usage under those brands.

In 2014, App Annie bought Distimo, and as of 2016 has run Phone Guardian, a “secure Wi-Fi and VPN” app, under the Distimo brand.

The app discloses its relationship with App Annie in its App Store description, but remains vague about its true purpose:

“Trusted by more than 1 million users, App Annie is the leading global provider of mobile performance estimates. In short, we help app developers build better apps. We build our mobile performance estimates by learning how people use their devices. We do this with the help of this app.”

In 2015, App Annie acquired Mobidia. Since 2017, it has operated real-time data usage monitor My Data Manager under that brand, as well. The App Store description only offers the same vague disclosure, which means users aren’t likely aware of what they’re agreeing to.

Disclosure?

The problem with apps like App Annie’s and Sensor Tower’s is that they’re marketed as offering a particular function, when their real purpose for existing is entirely another.

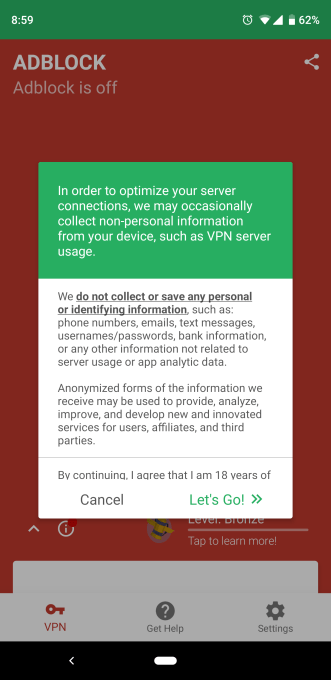

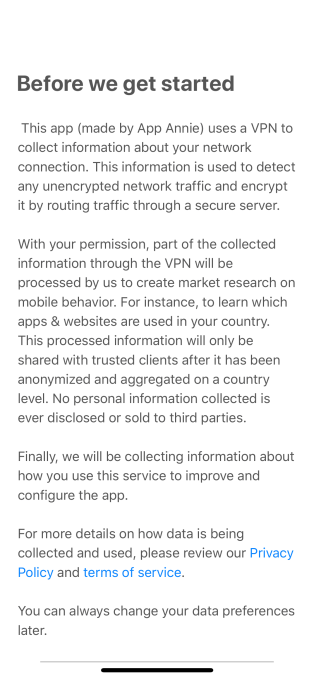

The app companies’ defense is that they do disclose and require consent during onboarding. For example, Sensor Tower apps explicitly tell users what is collected and what is not:

App Annie’s app offers a similar disclosure, and takes the extra step of identifying the parent company by name:

App Annie also says its apps can continue to be used even if data sharing is turned off.

Despite these opt-ins, end users may still not understand that their VPN app is actually tied to a much larger data collection operation, however anonymized that data may be. After all, App Annie and Sensor Tower aren’t household names (unless you’re an app publisher or marketer.)

Apple and Google’s responsibility

Apple and Google, let’s be fair, are also culpable here.

Of course, Google is more pro-data collection because of the nature of its own business as an advertising-powered company. (It even tracks users in the real world via the Google Maps app.)

Apple, meanwhile, markets itself as a privacy-focused company, so is deserving of increased scrutiny.

It seems unfathomable that, following the Onavo scandal, Apple wouldn’t have taken a closer look into the VPN app category to ensure its apps were compliant with its rules and transparent about the nature of their businesses. In particular, it seems Apple would have paid close attention to apps operated by companies in the app store intelligence business, like App Annie and its subsidiaries.

Apple is surely aware of how these companies acquire data — it’s common industry knowledge. Plus, App Annie’s acquisitions were publicly disclosed.

oh wait! pic.twitter.com/ktVc6E9t1f

— Will Strafach (@chronic) March 10, 2020

But Apple is conflicted. It wants to protect app usage and user data (and be known for protecting such data) by not providing any broader app store metrics of its own. However, it also knows that app publishers need such data to operate competitively on the App Store. So instead of being proactive about sweeping the App Store for data collection utilities, it remains reactive by pulling select apps when the media puts them on blast, as BuzzFeed’s report has since done. That allows Apple to maintain a veil of innocence.

But pulling user data directly covertly is only one way to operate. As Facebook and Google have since realized, it’s easier to run these sorts of operations on the App Store if the apps just say, basically, “this is a data collection app,” and/or offer payment for participation — as do many marketing research panels. This is a more transparent relationship from a consumer’s perspective too, as they know they’re agreeing to sell their data.

Meanwhile, Sensor Tower and App Annie competitor Apptopia says it tested then scrapped its own ad blocker app around six years ago, but claims it never collected data with it. It now favors getting its data directly from its app developer customers.

“We can confidently state that 100% of the proprietary data we collect is from shared App Analytics Accounts where app developers proactively and explicitly share their data with us, and give us the right to use it for modeling,” stated Apptopia co-founder and COO, Jonathan Kay. “We do not collect any data from mobile panels, third-party apps or even at the user/device level.”

This system (which is used by the others as well) isn’t necessarily a solution for end users concerned about data collection, as it further obscures the collection and sharing process. Generally, consumers don’t know which app developers are sharing this data, what data is being shared, or how it’s being utilized. App data of this nature isn’t on the user level (meaning it’s not personal data), but it’s still about reporting back to the developer things like installs, daily and monthly users, and revenue, among other things. (Fortunately, Apple allows users to disable the sharing of some diagnostic and usage data from within iOS Settings.)

Data collection done by app analytics firms is only one of many, many ways that apps leak data, however.

In fact, many apps collect personal data — including data that’s far more sensitive than anonymized app usage trends — by way of their included SDKs (software development kits). These tools allow apps to share data with numerous technology companies, including ad networks, data brokers and aggregators, both large and small. It’s not illegal, and mainstream users probably don’t know about this either.

Instead, user awareness seems to crop up through conspiracy theories, like “Facebook is listening through the microphone,” without realizing that Facebook collects so much data it doesn’t really need to do so. (Well, except when it does).

In the wake of BuzzFeed’s reporting, Sensor Tower says it’s “taking immediate steps to make Sensor Tower’s connection to our apps perfectly clear, and adding even more visibility around the data their users share with us.”

Google isn’t providing an official comment. Apple didn’t respond to requests for comment.

Sensor Tower’s full statement is below:

Our business model is predicated on high-level, macro app trends. As such, we do not collect or store any personally identifiable information (PII) about users on our servers or elsewhere. In fact, based on the way our apps are designed, such data is separated before we could possibly view or interact with it, and all we see are ad creatives being served to users. What we do store is extremely high level, aggregated advertising data that may demonstrate trends that we share with customers.

Our privacy policy follows best practices and makes our data use clear. We want to reiterate that our apps do not collect any PII, and therefore it cannot be shared with any other entity, Sensor Tower or otherwise. We’ve made this very clear in our privacy policy, which users actively opt into during the apps’ onboarding processes after being shown an unambiguous disclaimer detailing what data is shared with us. As a routine matter, and as our business evolves, we’ll always take a privacy-centric approach to new features to help ensure that any PII remains uncollected and is fully safeguarded.

Based on the feedback we’ve received, we’re taking immediate steps to make Sensor Tower’s connection to our apps perfectly clear, and adding even more visibility around the data their users share with us.

App Annie shared the below statement, referencing the root certificate installations mentioned in the BuzzFeed article. (On iOS devices, VPN certificates don’t get full root access, however):

App Annie does not use root certificates at any point in its data collection process.

App Annie discloses that when users opt into data collection (and data sharing is not mandatory to use our apps), data will be shared with App Annie for the purposes of creating market research. We only collect data after users expressly consent to this collection within our apps. We are very transparent, both on the app stores and in the apps themselves and clearly connect App Annie to our mobile apps.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

Earlier this week, the popular free stock trading service Robinhood suffered downtime over a two-day period. The company, a well-funded unicorn taking on incumbents in its industry, failed to operate properly when the public markets were surging on Monday (bad) and falling on Tuesday (very bad).

Complaints flooded investing forums and social media. Images of Robinhood account screens featuring huge losses from the periods of downtime (or missed upside) weren’t hard to find. For Robinhood, it wasn’t its first misstep, but it was perhaps its worst. Mishandling the rollout of a high-yield savings function? Embarrassing, but hardly a serious wound. Some options oddness? Eh, not the worst.

Going down during surging volatility? Much worse. The company is already in the market with apologies and some give-aways to try to stem the negative news cycle. But what’s notable so far is that, while you might expect to see rival apps and services to Robinhood boom in the wake of its downtime, it instead appears that only select competitors to the popular company are seeing a jump in downloads this week. And given the insane market movements, it’s hard to pin some of their gains on Robinhood instead of, say, what stocks are themselves doing.

I’d expected by today to have some data in hand that painted a starker picture for Robinhood, given that the company’s recent missteps triggered a lot of negative press and user reaction. Let’s peek at what numbers can tell us, and try to figure out if there’s a lesson for consumer fintech and finservies companies while we’re at it.

Powered by WPeMatico

Consumers downloaded a record 204 billion apps in 2019, up 6% from 2018 and up 45% since 2016, and spent $120 billion on apps, subscriptions and other in-app spending in the past year. The average mobile user, meanwhile, is spending 3.7 hours per day using apps. This data and more comes from App Annie’s annual report, “State of Mobile,” which highlights the biggest app trends for the past year, and sets forecasts for the years ahead.

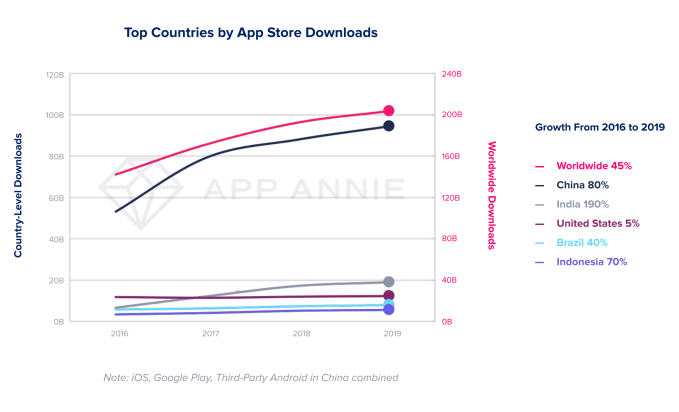

According to App Annie, the record growth in mobile downloads in 2019 can be attributed to the growth taking place in emerging markets like India, Brazil and Indonesia, which have seen downloads soar 190%, 40% and 70%, respectively, since 2016. Meanwhile, download growth in the U.S. has slowed to just 5% during that same time, while China saw 80% growth.

That doesn’t mean users in mature markets aren’t downloading apps, only that the growth in year-over-year download numbers is starting to level off. Still, these more mature markets continue to see large numbers of installs, with more than 12.3 billion downloads in the U.S. in 2019, 2.5 billion in Japan and 2 billion in South Korea.

The record numbers are notable also, given that App Annie’s analysis excludes re-installs and app updates.

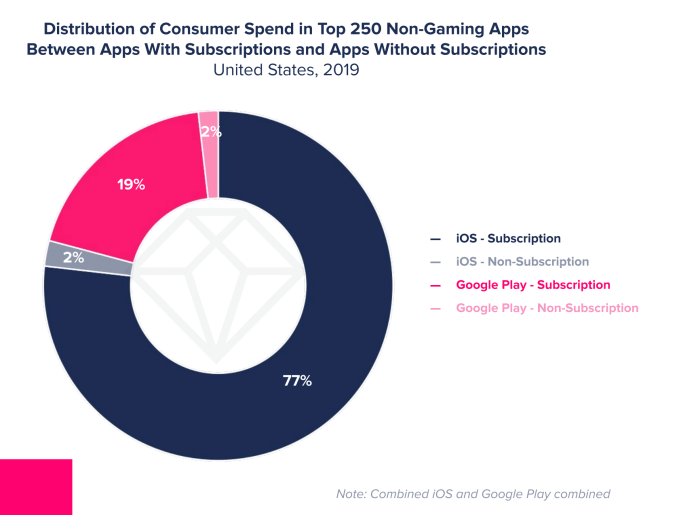

App store consumer spending was on the rise in 2019, as well, with $120 billion spent on apps — a figure that’s up 2.1x from 2016. Games continue to account for the majority (72%) of that spending, but the shift toward subscriptions has played a role, too. Last year, subscriptions in non-gaming apps accounted for 28% of consumer spending, up from 18% in 2016.

Subscriptions are now the primary way many non-gaming apps generate revenue. For example, 97% of consumer spending in the top 250 U.S. iOS apps was driven by subscriptions, and 94% of the apps used subscriptions. On Google Play, 91% of the consumer spending was subscription-based, while 79% of the top 250 apps used subscriptions.

In particular, dating apps like Tinder and video apps like Netflix and Tencent Video topped 2019’s consumer spend charts, thanks to subscription revenue.

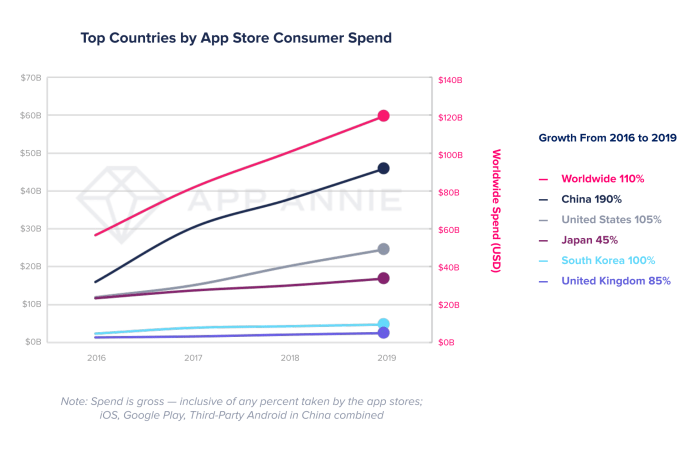

Mature markets, including the U.S., Japan, South Korea and the U.K. are helping to fuel consumer spending across both games and subscriptions, App Annie found. But China remains the largest market by far, accounting for 40% of global spend.

App Annie also forecast that the mobile industry will contribute $4.8 trillion to the global GDP by 2023.

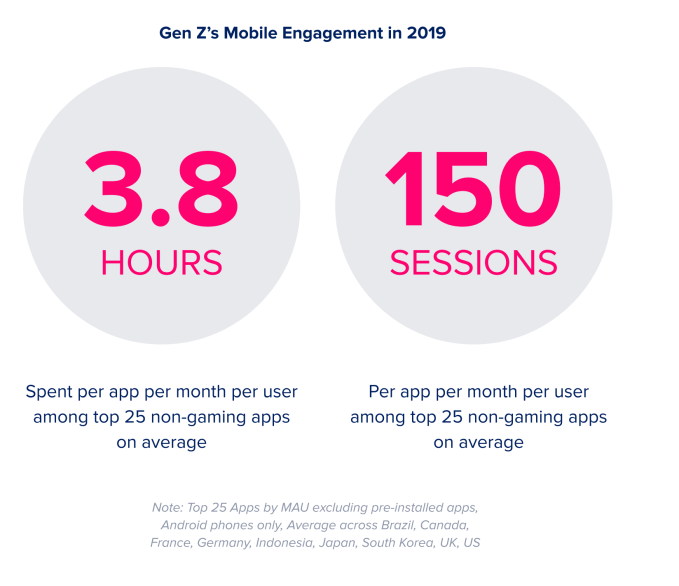

The report additionally identified several mobile trends from 2019, including the mobile app connection to the Internet of Things and smart home devices (106 million downloads for the top 20 IoT apps last year); the huge mobile engagement by Gen Z (3.8 hours per app per month, among the top 25 non-game apps, on avgerage); and mobile ad spend’s growth ($190 billion in 2019 to $240 bilion in 2020).

Ad spending combined with consumer spending is expected to reach $380 billion worldwide by 2020, App Annie forecast.

Gaming was given a big breakout section, given its contribution to consumer spending.

Consumer spending in mobile gaming was 2.4x that of Mac/PC gaming, and 2.9x more than game consoles. In 2019, mobile gaming saw 25% more spending than all other gaming, and is on track to surpass $100 billion across all app stores by next year.

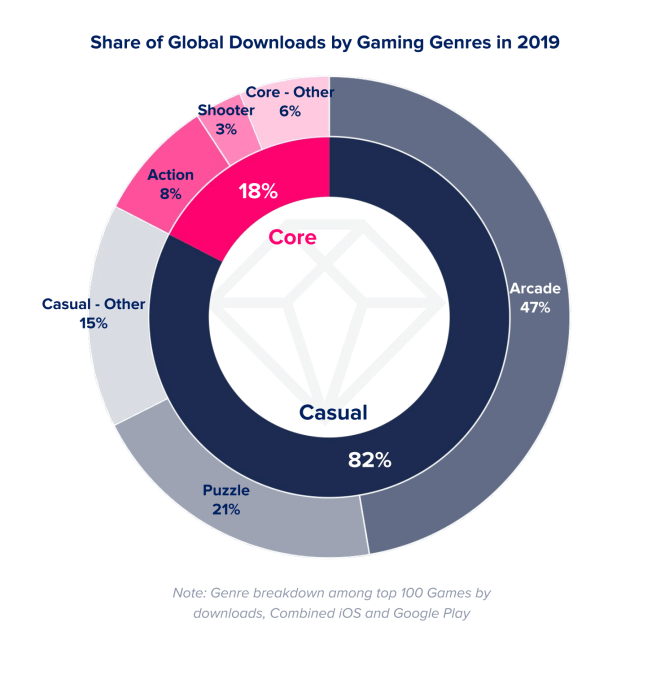

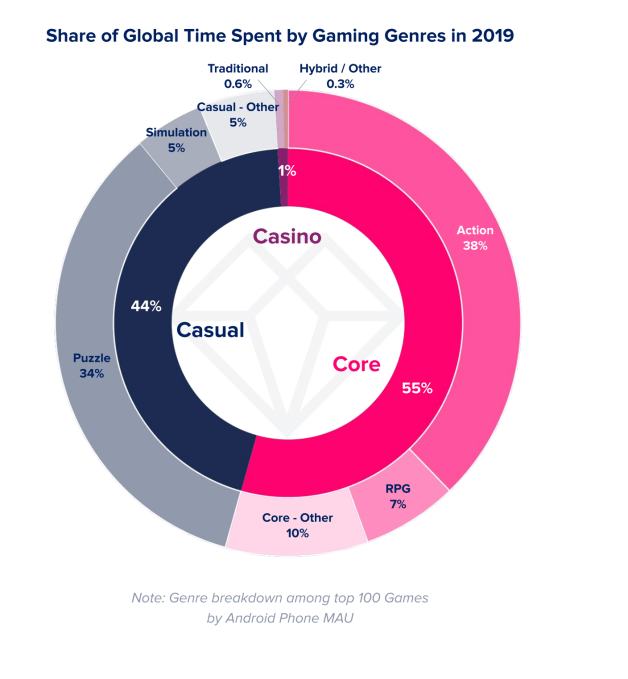

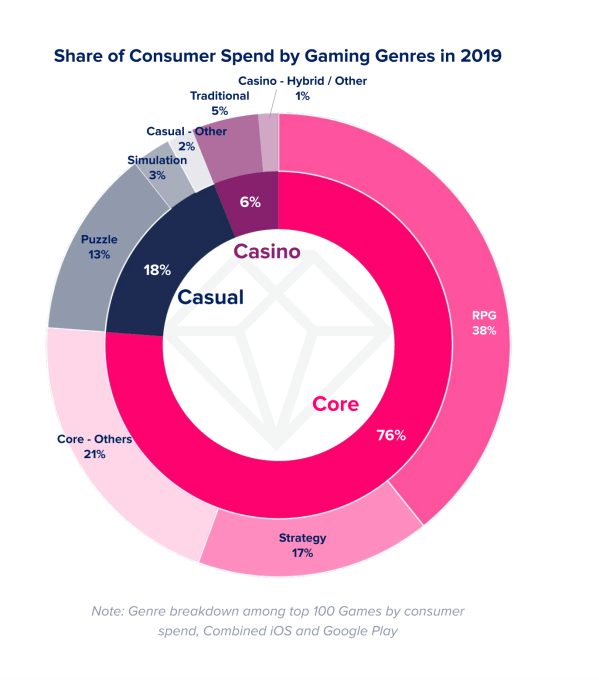

Casual gaming (led by Puzzle and Arcade) was the most downloaded type of games in 2019. Meanwhile, core games (e.g. Action, RPG, etc.) — which were only 18% of downloads — accounted for 55% of time spent in top games. PUBG Mobile was the No. 1 core game (action) on Android in 2019, in terms of time spent, while Anipop (puzzle) was the top casual game.

Core games also accounted for the majority (76%) of game spending, followed by casual (18%), then casino (6%).

In 2019, 17% more games surpassed $5 million in consumer spending versus 2017. And the number of games to top $100 million grew 59% compared to two years prior. Despite the sizable growth in revenues, App Annie also pointed to new models in mobile gaming, like Apple Arcade, which is giving other types of games a chance to thrive. Unfortunately, no third-party firm is able to track Arcade revenues, which will become a glaring blind spot for App Annie in the years ahead.

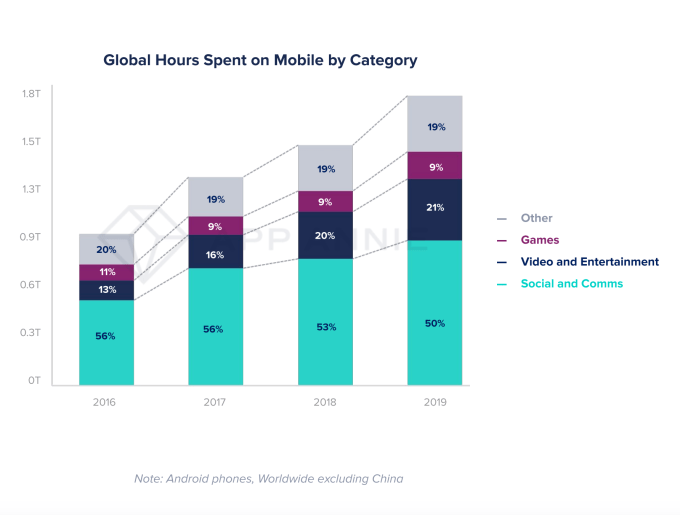

App Annie also examined other sizable segments of the mobile market for trends, including fintech, retail, streaming and social. Some of the more significant findings included: the fintech app user base growth topping that of traditional banking apps; shopping app downloads saw 20% year-over-year growth to reach 5.4 billion downloads; streaming growth that included 50% sessions in 2019 compared to 2017; and 50% of time spent on mobile was spent in social networking and communication apps.

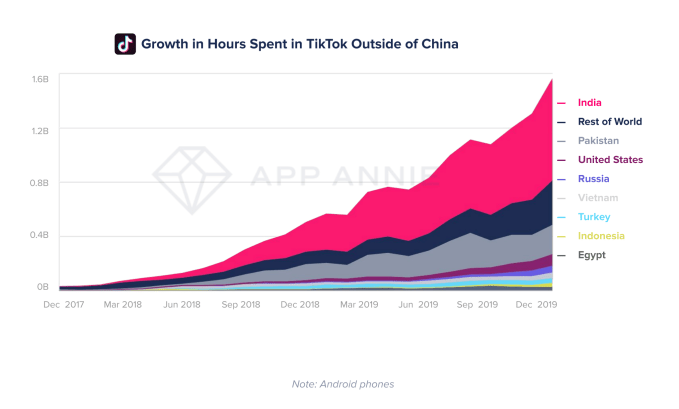

TikTok was given special attention, given its rapid growth last year. Time spent in the short-form video app grew 210% year-over-year in 2019 globally. Even though eight out of every 10 minutes spent in TikTok were by users in China, the app’s usage skyrocketed in other markets as well, App Annie said.

TikTok was given special attention, given its rapid growth last year. Time spent in the short-form video app grew 210% year-over-year in 2019 globally. Even though eight out of every 10 minutes spent in TikTok were by users in China, the app’s usage skyrocketed in other markets as well, App Annie said.

Industries App Annie identified as being transformed by mobile in 2019 included ridesharing, fast food/food delivery, dating, sports streaming, plus health and fitness. The full report offers a few more details and mobile trends for each of these.

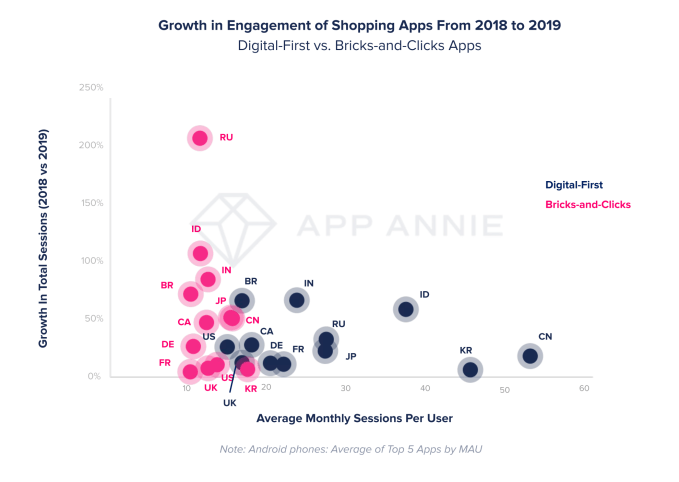

One bigger highlight was that digital-first shopping apps still had 3.2x more average monthly sessions per user compared with apps from traditional brick-and-mortar retailers (dubbed “bricks-and-clicks” apps in the report).

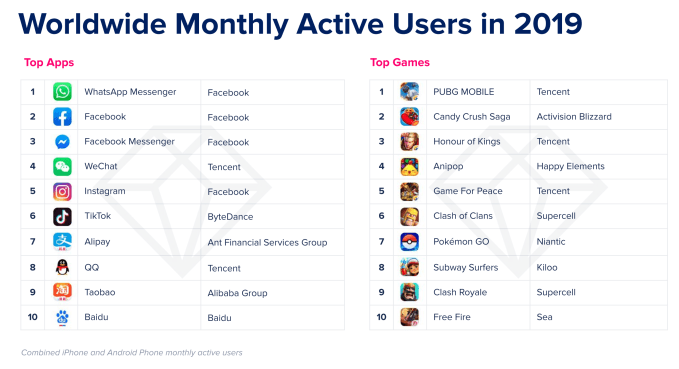

App Annie also compiled its own list of the top apps of 2019 by active users, downloads and revenue. Facebook apps still led by engagement, with WhatsApp, Facebook and Messenger in the top three spots and Instagram as No. 5. And they maintained similar positions by downloads, only swapping places with one another.

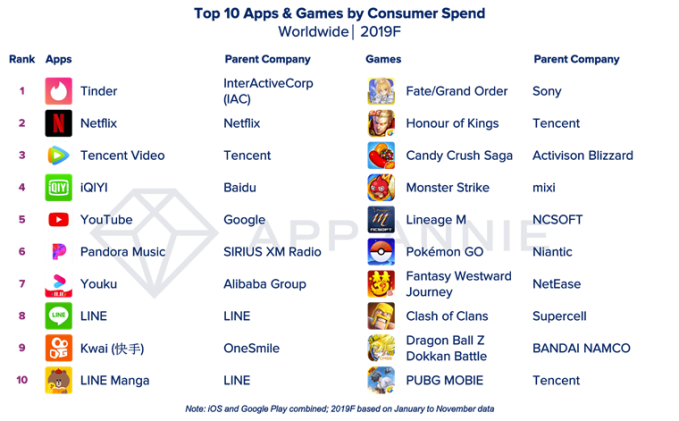

Consumer spending was a different story, with Tinder generating the most revenue in 2019, followed by entertainment and streaming apps like Netflix, Tencent Video, iQIYI, YouTube and others.

Powered by WPeMatico

Mobile consumers worldwide will have downloaded a record 120 billion apps from Apple’s App Store and Google Play by the end of 2019, according to App Annie’s year-end report on app trends. This represents a 5% increase from 2018 — a notable achievement given that the number doesn’t include re-installations or app updates. Consumer spending on apps, meanwhile, approached $90 billion in 2019 across both app stores, up 15% from last year. The new report also examined the year’s biggest apps, including the most downloaded apps and games, as well as the most profitable.

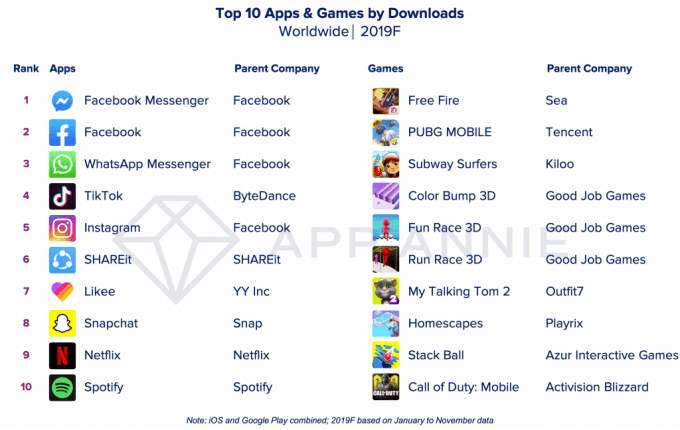

Worldwide, the most downloaded non-game apps remained relatively consistent in 2019, with only one new entry on the list of the most downloaded apps — a short-form video creation and sharing app called Likee, which is benefiting from the overall popularity of short-form video. Elsewhere on the chart, TikTok came in at No. 4, beating out Facebook-owned Instagram, plus Snapchat, Netflix and Spotify.

However, Facebook still owned the top of the charts. Its Messenger app was the most downloaded non-game app of 2019, followed by Facebook’s main app, then WhatsApp.

The top 10 games chart showed more volatility in 2019, as seven out of the top 10 games were new to the chart this year. This included the hyper-casual title Fun Race 3D, as well as the anticipated Call of Duty: Mobile, representing the battle royale genre.

While mobile gaming drives the majority of consumer spending on apps, the subscription economy in 2019 played a big role in increasing app revenues, as well.

Specifically, the non-game apps driving revenue growth this year included those in the Photo & Video and Entertainment categories — a trend App Annie predicts will continue in 2020, as new video services, like Disney+, continue to rise. 2020 will additionally see the launch of several other video services, including HBO Max, NBCU’s Peacock and Jeffrey Katzenberg’s Quibi, which could aid in those increases.

Already, many of the top apps are subscription-based, App Annie had previously noted. During the 12 months ending in September 2019, more than 95% of the top 100 non-gaming apps by consumer spend were offering subscriptions through in-app purchases. Publishers’ growing use of subscription services will continue in 2020 to drive consumer spending even higher, the firm says.

This year, Tinder switched places with Netflix for the No. 1 spot on this chart — last year, it was the other way around. HBO NOW, which saw a surge in spending thanks to “Game of Thrones,” also fell out of the top chart this year, allowing LINE Manga to take its spot. Tencent Video and iQIYI have the same positions as 2018, while YouTube grew from No. 7 to No. 5, and Pandora slipped from No. 5 to No. 6 compared with last year.

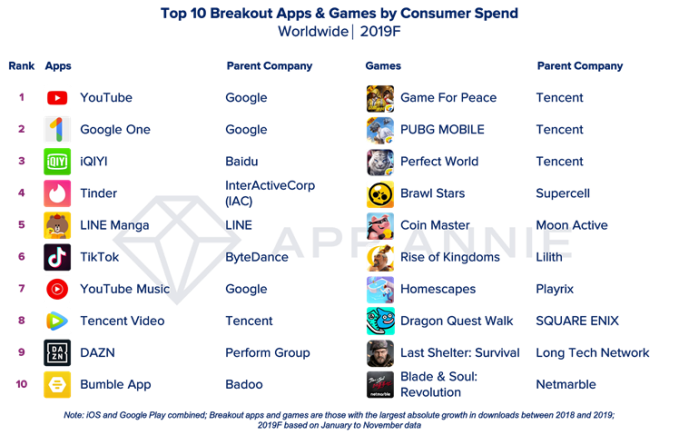

App Annie also took a look at a new category of apps that it’s calling the “breakout” apps of the year. These are those that saw the largest absolute growth in downloads or consumer spending between 2018 and 2019. On this list, the No. 7 most-downloaded app of the year, Likee, from YY Inc., becomes the No. 1 “breakout” app of the year, followed by YY Inc.’s Noizz and Helo. Meanwhile, Indian users drove the adoption of social gaming app Hago at No. 4, which is also popular with Gen Z users in Indonesia.

Breakout apps by consumer spending included YouTube, iQIYI, DAZN and Tencent Video — similar to the top 10 list.

On the gaming side, hyper-casual titles were successful, claiming seven out of 10 slots on the breakout games of the year chart. Hot releases like Mario Kart Tour and Call of Duty: Mobile also appeared. But by consumer spending, core games like No. 1 Game for Peace and No. 2 PUBG Mobile, both published by Tencent, made up the top spots.

Powered by WPeMatico

Global app revenue continues to climb, thanks to the growth in mobile gaming and the subscription economy. In the third quarter of 2019, consumer revenue grew 22.9% year-over-year from $17.9 billion to reach an estimated $21.9 billion across both the App Store and Google Play worldwide, according to new data from Sensor Tower.

Notably, the App Store continues to account for the large majority of this revenue, the report found, making up 65% of total spending compared with just 35% on Google Play.

App Store users spent $14.2 billion, up 22.3% from the $11.6 billion they spent in Q3 2018. Google Play generated $7.7 billion in revenue, up 24% from the $6.2 billion spent in the year-ago quarter.

Sensor Tower’s revenue estimates are a bit lower than those provided by App Annie’s recent report, which said the quarter saw $23 billion in consumer spending, not ~$22 billion.

App Annie also estimated nearly 31 billion downloads in Q3, while Sensor Tower claimed 29.6 billion.

In both cases, Google Play is still said to be the main source for downloads, with nearly three times more first-time installs than the App Store. In Q3, the total number of downloads was up 9.7% year-over-year to 29.6 billion, said Sensor Tower, with Google Play accounting for 21.6 billion of those.

Despite the overall growth, one big app market — China — saw a slight decline, Sensor Tower found. Its installs dropped 6% year-over-year to 2.2 billion in the quarter. But its revenue grew by 26.9% to $4.1 billion, up from $3.2 billion the year prior. This could be attributed to the nine-month game license freeze in China which, though now lifted, had slowed momentum.

Sensor Tower’s charts don’t include third-party app stores, so it’s not a full picture of the Chinese app market, it’s worth noting.

The top money-making (non-game) app in the quarter was again Tinder, which generated $233 million in consumer spending, up 7% over the prior quarter. Netflix was No. 2 and YouTube clocked in at No. 3, at $164 million in Q3.

App Annie has a slightly different ranking. It has Tinder and Netflix leading the top-grossing charts, but puts IQIYI ahead of YouTube. This could be because App Annie has a bigger window into the Chinese app market.

In terms of downloads, TikTok is continuing to disrupt Facebook-owned apps’ dominance over the top of the charts. In Sensor Tower’s rankings, WhatsApp was No. 1 and Messenger was No. 3, but Facebook and Instagram dropped to No. 4 and No. 5, respectively. And TikTok reached No. 2.

This isn’t the first time TikTok has passed Facebook, Sensor Tower said — it did so back in Q4 2018 and in Q1 2019, before dropping to No. 4 again last quarter. But with 177 million downloads in Q3, it’s inching its way up to the top.

App Annie, on the other hand, sees TikTok having just a bit more of climb, sticking it at No. 3 in the quarter, behind Messenger and Facebook. It also called out some Q3 break-out hits, like the return of FaceApp’s popularity (No. 9 in downloads) and the growing subscription revenue of Google One (No. 7 in non-game revenue). Sensor Tower put FaceApp at No. 6 instead, but agreed on Google One.

Mobile gaming continues to generate most of the cash, and did so again in Q3 with $16.3 billion in mobile game gross revenue — or 74% of the total in-app spending, the new report said. The App Store accounted for $9.8 billion of that figure, with Google Play users spending $6.5 billion.

Game downloads across both Google Play and the App Store increased by 17.6% in Q3 from 9.5 billion last year to 11.1 billion.

The top three games in the quarter by downloads were Fun Race 3D (123 million downloads), PUBG Mobile (94 million) and newcomer Mario Kart Tour, which hit 86 million downloads despite only launching in late September.

PUBG Mobile was the top-grossing game with $496 million in revenue, up 652% over last year. The No. 2 title, Tencent’s Honor of Kings, and No. 3 Aniplex’s Fate/Grand Order generated $377 million and $354 million, respectively.

Image credits: Sensor Tower

Correction: App Annie estimated nearly 31 billion downloads in Q3, not 23 billion as first written. We corrected this. Apologies for the error.

Powered by WPeMatico