Advertising Tech

Auto Added by WPeMatico

Auto Added by WPeMatico

Instagram may finally let IGTV video makers earn money 18 months after launching the longer-form content hub. Instagram confirms to TechCrunch that it has internally prototyped an Instagram Partner Program that would let creators earn money by showing advertisements along with their videos. By giving creators a sustainable and hands-off way to generate earnings from IGTV, they might be inspired to bring more high-quality content to the destination.

The program could potentially work similarly to Facebook Watch, where video producers earn a 55 percent cut of revenue from “Ad Breaks” inserted into the middle of their content. There’s no word on what the revenue split would be for IGTV, but since Facebook tends to run all its ads across all its apps via the same buying interfaces, it might stick with the 55 percent approach that lets its say creators get the majority of cash earned.

Previously, Instagram only worked with a limited set of celebrities, paying “to offset small production costs” for IGTV content Bloomberg reported, but not offering a way to earn a profit. That left creators to look to sponsored content or product placement to generate cash, or to try to push their followers to platforms like YouTube where they could earn a reliable cut of ads.

A lack of monetization may have contributed to the absence of great content on IGTV. Many of the videos on the Popular page are low-grade rips of YouTube content or TV, or are clickbait teasers. That has led to mediocre view counts — only 7 million of Instagram’s billion-plus users downloading the standalone IGTV app — and Instagram dropping the homescreen button for opening IGTV.

That’s all disappointing considering TIkTok is blowing up on the back of more purposeful, storyboarded mobile video entertainment. Instagram has been looking at other ways to boost the quality of content users see, including today’s launch of unfollow suggestions.

But today, reverse engineering master and perennial TechCrunch tipster Jane Manchun Wong tipped us off to the IGTV monetization prototype she dug out of the code of Instagram’s Android app. She tells TechCrunch she first saw signs of the program a week and ago and was then able to generate screenshots of the unreleased feature. It shows an “Instagram Partner Program” with “Monetization Tools.” This seems to be different from the old “Partner Program” for business tool developers.

Users who are deemed “Eligible” according to criteria we don’t have info about could choose to “Monetize Your IGTV Videos.” The screen explains that, “You can earn money by runing short ads on your IGTV videos. When you monetize on IGTV, you agree to follow the Partner Program Monetization Policies.”

It’s not clear IGTV’s monetization policies would be different, but on Facebook they require that users:

Instagram confirmed to TechCrunch the authenticity of the prototype it’s been working on and provided the following statement (that it later tweeted): “We continue to explore ways to help creators monetize with IGTV. We don’t have more details to share now, but we will as they develop further.”

Given the company is confirming this as a prototype rather than a feature being beta tested, there are no public mentions. There’s no Instagram Help Center information published about it, and Instagram might not be testing the program externally yet. There’s still a chance Instagram could change directions and never launch the monetization program or alter it entirely before any eventual launch.

Update: Instagram CEO Adam Mosseri has commented on the new feature, replying to me here:

It’s no secret that we’ve been exploring this. We focused first on making sure the product had legs — else there would be little to monetize in the first place. IGTV is still in its early days, but it’s growing and so we’re exploring more ways to make it sustainable for creators.

— Adam Mosseri (@mosseri) February 7, 2020

Mosseri’s argument is that monetization hadn’t started sooner because Instagram wanted to ensure there was enough content to monetize. But Instagram had the money and scale to experiment much sooner, and it could have attracted that content to monetize by dangling payment.

IGTV has improved with time as more influencers and publishers get the hang of vertical mid-length video. However, there remains a fair amount of low-quality, unoriginal, overly captioned, meme-style videos promoted on its “Popular” page, at least for me.

Creator monetization has been a slow-going evolution on many of the major social networks. While YouTube was early to the space with ads, Twitter, Facebook and Snapchat are now testing an array of ways for influencers to earn money. Those include ad splits, subscriptions to exclusive content, tipping, connections to brands for sponsorship, merchandise sales and more.

Bloomberg’s Sarah Frier and Nico Grant reported this week that Instagram brought in $20 billion in revenue during 2019. It gets to keep that revenue since it currently doesn’t split any with creators. That contrasts with YouTube, which says it took in $15.1 billion in 2019 revenue this week in the first time it’s revealed the stat, though it has to pay out a substantial portion to creators. With Instagram now running ads in feed, Explore, and Stories, only IGTV and Direct remain as major surfaces lacking ads.

Social apps are wising up and realizing that if they want to keep their creators from straying to competitors and bringing fans with them, it needs to offer ways for people to turn their passion for creating content into a profession. IGTV spent a year and a half trying to get video makers to volunteer for free, and the result wasn’t entertaining. Now Instagram seems ready to share the proceeds if they can bring in viewers together.

Powered by WPeMatico

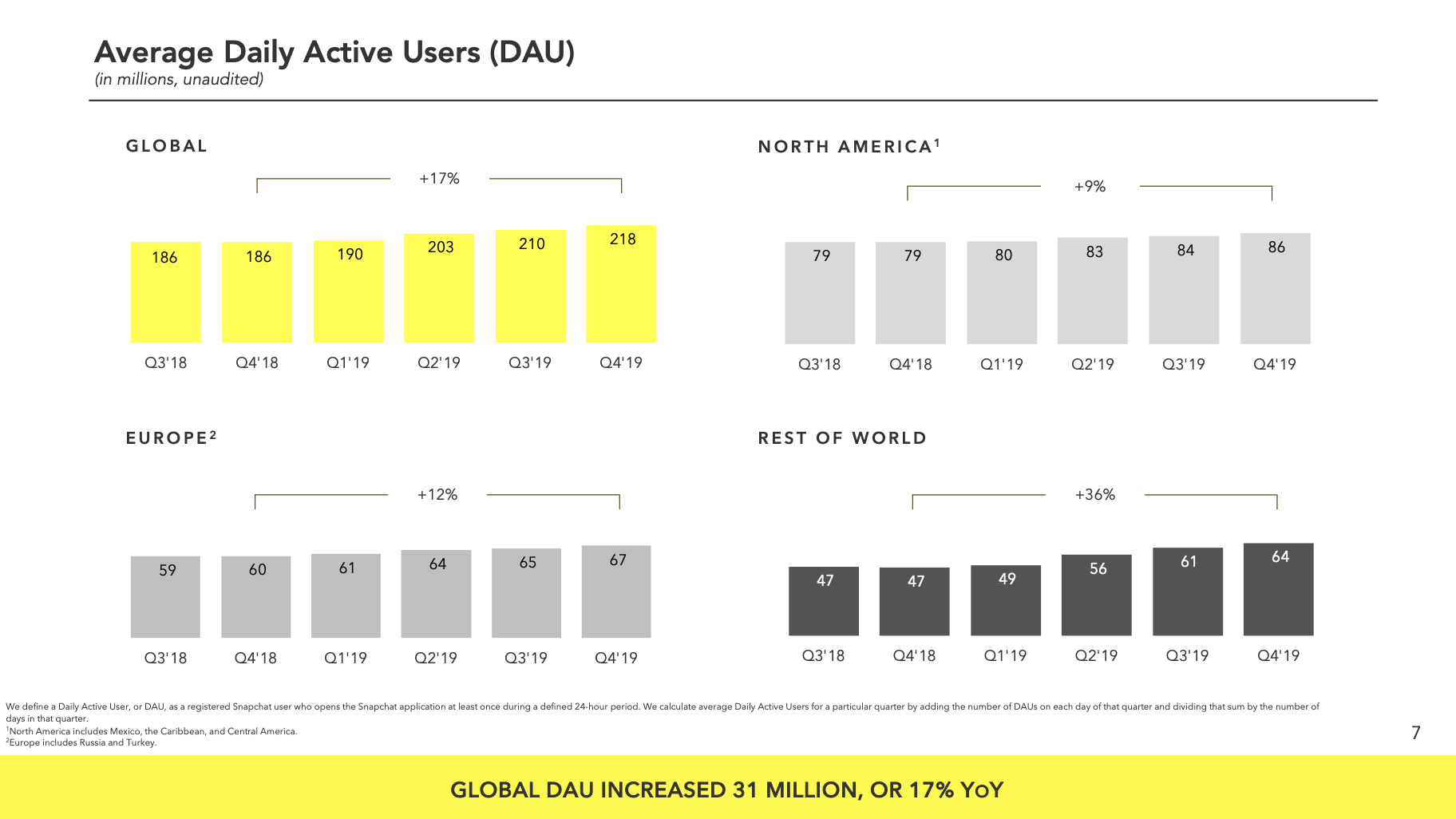

Snapchat still isn’t profitable nearly two years after its IPO. In Q4 2019, Snap lost $241 million on $560.8 million in revenue; that’s up 44% year-over-year and an EPS of $0.03. That comes from adding 8 million daily users to reach a total of 218 million up 3.8% this quarter from 210 million and 17% year-over-year.

The big problem was a one-time $100 million legal settlement that pushed it to lose $49 million more in Q4 2019 than Q4 2018. That comes from a shareholder lawsuit claiming Snap didn’t adequately disclose the impact of competition from Facebook on its business. The IPO was soured by weak user growth as people shifted from Snapchat Stories to Instagram Stories.

Snapchat had a mixed quarter compared to estimates, exceeding the EPS predictions but falling short on revenue. FactSet’s consensus predicted $563 million in revenue and a loss of $0.12 EPS. Estimize’s consensus came in at $568 million in revenue and an EPS gain of $0.02.

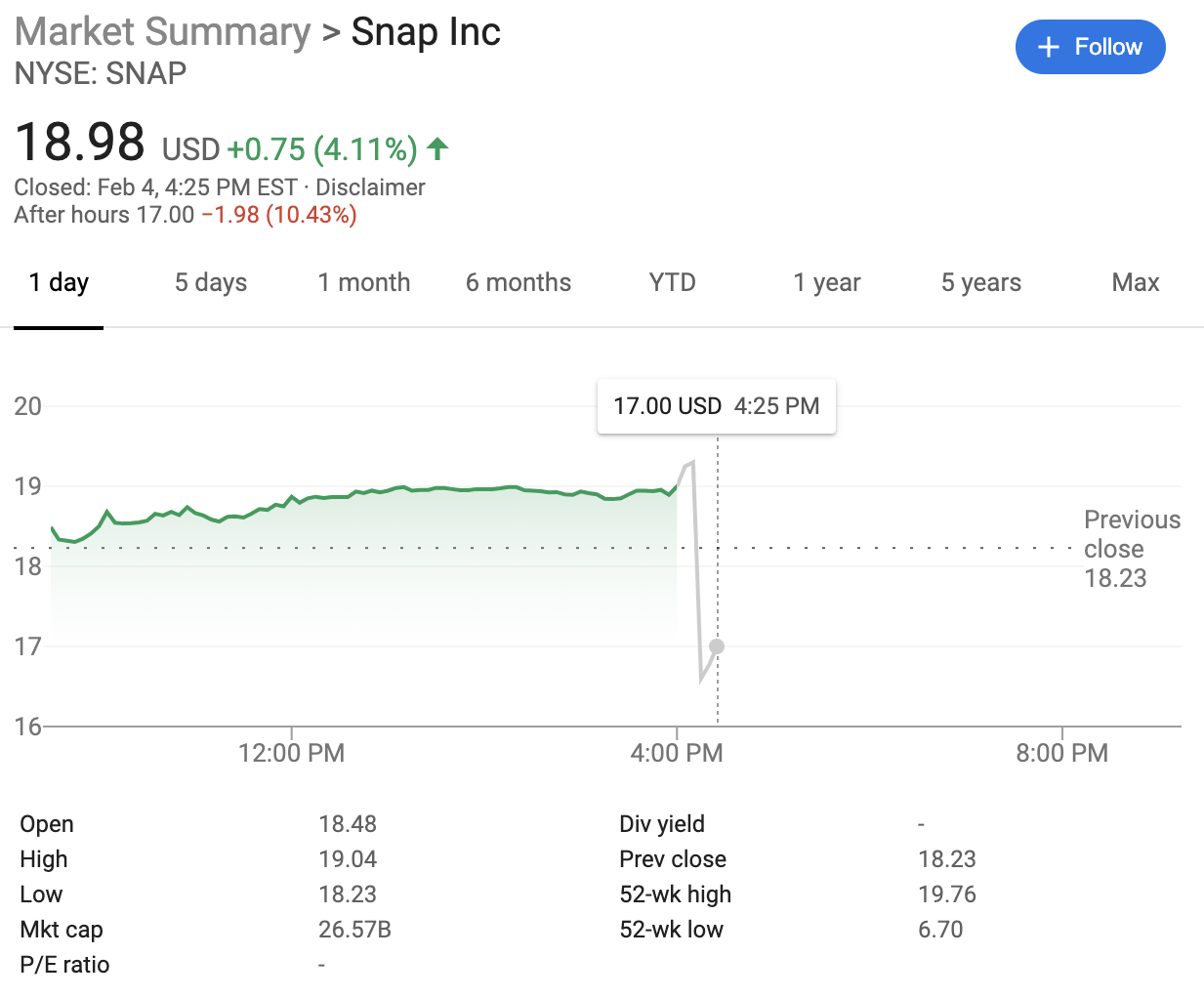

Snapchat shares plunged over 11% in after-hours trading following the announcement. Shares had closed up 4.17% at $18.99 today. That’s up from a low of $4.99 in December 2018 when its user count was shrinking under competition from Instagram Stories. It’s now hovering around its $17 IPO price, but it’s still under its post-IPO pop to $27.09.

Snap gave stronger than expected revenue guidance for Q1 2020 of $450 million to $470 million, and 224 million to 225 million users. The company’s CFO Derek Anderson says that “Q4 marked our first quarter of Adjusted EBITDA profitability at $42 million for the quarter, an improvement of $93 million over the prior year.” Still, he predicts an Adjusted EBITDA in Q1 of negative $90 million to negative $70 million. That’s manageable for Snap without raising more money, since it now has $2.1 billion in cash and marketable securities, down $148 million quarter-after-quarter.

“Throughout the course of 2019, we added 31 million daily active users, largely driven by investments in our core product and improvements to our Android application,” said Snapchat CEO Evan Spiegel . “We’ve recently completed our 2020 strategic planning process and have aligned our teams and resources around our goals of supporting real friendships on Snapchat, expanding our service to a broader global community, investing in our AR and content platforms, and scaling revenue while achieving profitability in order to self-fund our investments in the future.”

Some other highlights:

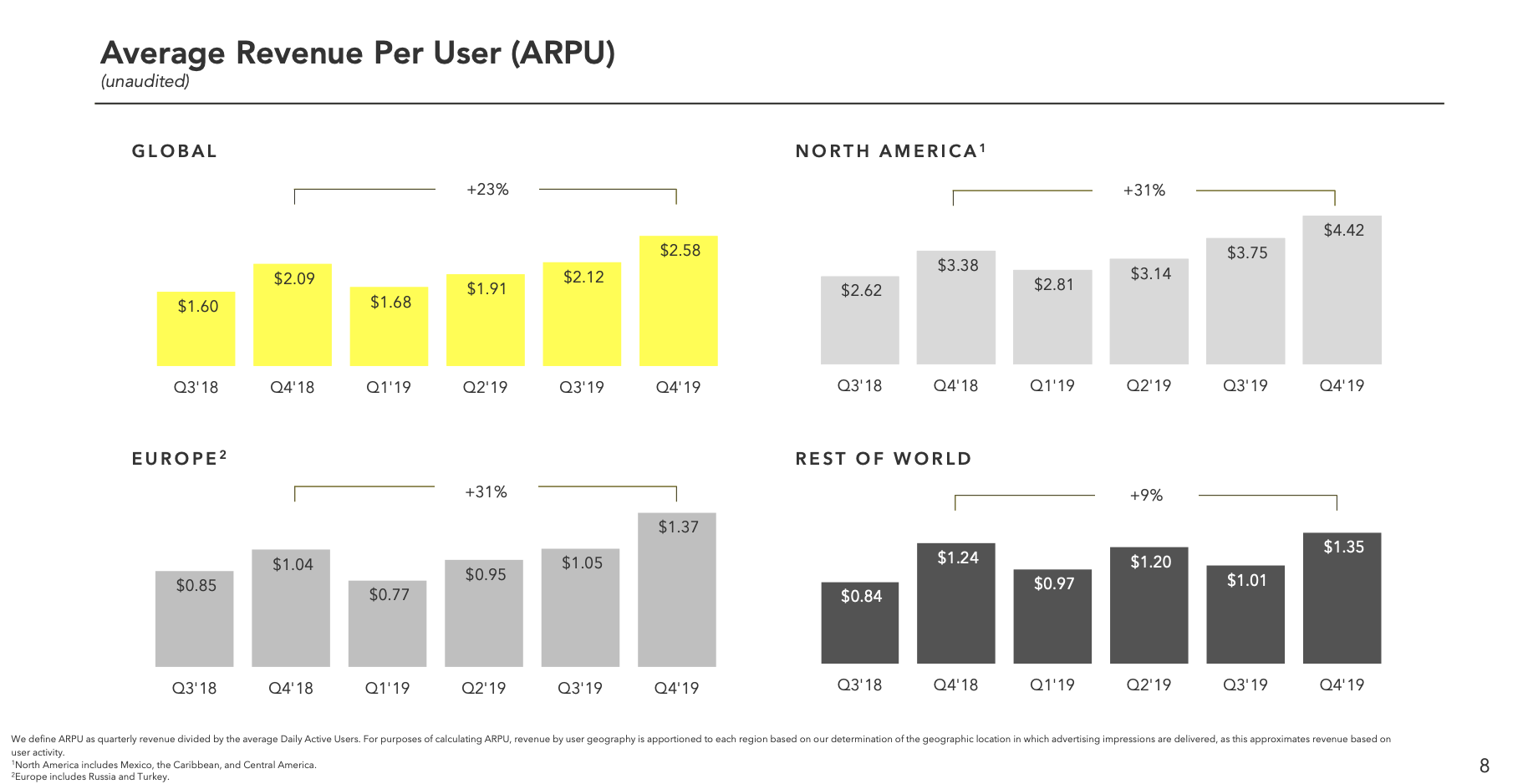

Snapchat’s user growth has been on a tear thanks to international penetration, especially in India, after it re-engineered its Android app for developing markets. It gained users in all markets. Crucially, it raised its average revenue per user 23% from $2.09 in Q4 2018 to $2.58, though only from $1.24 to $1.35 in the Rest of World region, where it’s growing user count the fastest. Snap will need to figure out how to squeeze more cash out of the international market to offset the costs of streaming tons of video to these users.

Q4 saw Snapchat readying several new products that could help boost engagement and therefore ad views. Cameos, first reported by TechCrunch, lets users graft their face onto an actor in an animated GIF like a lightweight deepfake. Bitmoji TV, which won’t run ads initially but could drive attention to Snapchat Discover, offers zany four-minute cartoons that star your Bitmoji avatar. We could see a bump to engagement from these starting in Q1 2020.

To retain its augmented reality filter creators, Snapchat has pledged $750,000 in payouts in 2020. It also expanded the use of product catalog ads, and now lets advertisers buy longer skippable ads.

Outside of the legal settlement, Snapchat is inching closer to profitability, but still has a ways to go. It has managed to develop a strong synergy between its popular chat feature that’s tougher to monetize, and the Stories and Discover content where it can inject ads. The big question is whether Facebook Messenger, Instagram and WhatsApp will get more serious about ephemeral messaging that’s at the core of Snapchat. If it can hold onto the market and maintain its place as where teens talk, it could ride out its costs and build revenue until it’s sustainable for the long-term.

Powered by WPeMatico

Insticator, a startup helping publishers add to their content elements like polls, quizzes and suggested story widgets, has made its first acquisition — a commenting platform called Squawk-It.

Insticator CEO Zack Dugow said his platform benefits online publishers by keeping audiences engaged and bringing in new ad revenue (which is split between Insticator and the publisher). And he sees commenting as a natural next step toward his goal to become “the main monetization and community engagement solution for publishers.”

While “don’t read the comments” remains one of the most reliable pieces of advice you’ll get online, Dugow said Squawk-It (it was formerly known as Solid Opinion) stands out from other commenting platforms because of its reliance on “100 percent human moderation,” with moderators working in three shifts to monitor partner sites 24 hours each day.

“Anybody can game an algorithm,” he said.

And when I brought up the concern that so much of the discussion has moved out of the comments section and onto social media, Dugow responded that “merging social commenting” so that it feels like everything is part of the same conversation is “in our roadmap.”

Like other Insticator products, Squawk-It comments (which you can see below the article here) are monetized through advertising. But Dugow noted that the ads run above the comments, rather than interrupting or distracting from the comments themselves.

The financial terms of the acquisition were not disclosed. Dugow said the entire 13-person Squawk-It team (headquartered in New York but with an engineering team in Kiev) has joined Insticator, and that the product has already been rebranded as Insticator Comments.

Powered by WPeMatico

Facebook beat Wall Street estimates in Q4 but slowing profit growth beat up the share price. Facebook reached 2.5 billion monthly users, up 2%, from 2.45 billion in Q3 2019 when it grew 1.65%, and it now has 1.66 billion daily active users, up 2.4% from 1.62 billion last quarter when it grew 2%. Facebook brought in $21.08 billion in revenue, up 25% year-over-year, with $2.56 in earnings per share.

But net income was just $7.3 billion, up only 7% year-over-year compared to 61% growth over 2018. Meanwhile, operating margins fell from 45% over 2018 to 34% for 2019. Expenses grew to $12.2 billion for Q4 2019, up a whopping 34% from Q4 2018. For the year, Facebook’s $46 billion in expenses are up 51% vs 2018. One big source of those expenses? Headcount grew 26% year-over-year to 44,942, and Facebook now has over 1000 engineers working on privacy.

While Facebook’s user base keeps growing rather steadily, it’s having trouble squeezing more and more cash out of them with as much efficiency.

Facebook’s Q4 2019 earnings beat expectations compared to Zack’s consensus estimates of $20.87 billion in revenue and $2.51 earnings per share. Facebook shares fell over 7% in after-hours trading following the earnings announcement after closing up 2.5% at a peak $223.23 today. Still, Facebook remains near its previous share price high before this month.

Facebook CEO Mark Zuckerberg had previously warned that addressing hate speech, election interference, and other content moderation and safety issues would be costly. Still, expenses grew and profits shrunk faster than Wall Street seems to have expected. Facebook will have to hope its promise of using scalable AI to handle more of these jobs comes to fruition soon.

But some might see today as the proper reckoning for Facebook — penance for years of neglecting safety in favor of growth. Facebook’s CFO David Wehner confirms it has also just agreed to pay $550 million in a settlement over its violation of the Illinois Biometric Information Privacy Act. The class action suit stems from Facebook collecting users’ facial recognition data to power its Tag Suggestions feature that recommends friends tag you in photos in which you appear. The record-breaking settlement still falls far short of the $35 billion in potential penalties Facebook could have received.

Facebook’s executives are apparently bullish on its value despite the share price being at a peak, as today Facebook announced plans to grow its share-repurchase program by $10 billion, adding to its previous authorization of buying back up to $24 billion worth.

Facebook managed to add 1 million daily users in the U.S. & Canada region where it earns the most money after returning to growth there last quarter following a year of slow or no growth. Facebook’s stickiness, or daily to monthly active user ratio remained at 66% amidst competition from apps like TikTok and a resurgent Snapchat.

Facebook notes that there are now 2.26 billion users that open either Facebook, Messenger, Instagram, or WhatsApp each day, up from 2.2 billion last quarter. The family of apps sees 2.89 billion total monthly users, up 9% year-over-year.

Facebook released a new stat with this earnings report: Family Average Revenue Per Person. That’s essentially the company’s total revenue divided by total users on Facebook, Messenger, Instagram, and WhatsApp. Clearly, the company is trying to use Instagram’s growing ad revenue to make the rest of the company look stronger. This might help mask changes in the Facebook app’s own revenue as teens look to more youthful content feeds. Wehner confirmed the company will cease sharing Facebook-only stats in favor of Family Of Apps stats in late 2020.

Sadly Facebook’s isn’t calling this metric FARPP

Zuckerberg stressed Facebook’s need to stay focused on addressing social issues and consequences of the company’s growth during the earnings call. He said Facebook will continue to make its apps more private and secure.

As for product updates, Zuckerberg seized on opportunities in commerce. Facebook is building out WhatsApp Pay, and he says “I expect this to start rolling out in a number of countries and for us to make a lot of progress here in the next six months.” 140 million small businesses now use its tools. People bought almost $5 million in content on the Oculus Store on Christmas Day, which Zuckerberg called a milestone. He says Facebook’s Spark AR platform is most used of its kind by developers, with hundreds of millions of people experiencing face filters built with it.

Regarding plans to integrate the family’s chat interfaces, Zuckerberg says Messenger, Instagram, and WhatsApp will retain their brands. He also noted they’re already quite integrated on the backend…which could be an attempt to persuade regulators it might be difficult to break up the company.

For guidance, Wehner said “we expect our year-over-year total reported revenue growth rate in Q1 to decelerate by low-to-mid single digit percentage points as compared to our Q4 growth rate. “Factors driving this deceleration include the maturity of our business, as well as the increasing impact from global privacy regulation and other ad targeting related headwinds.”

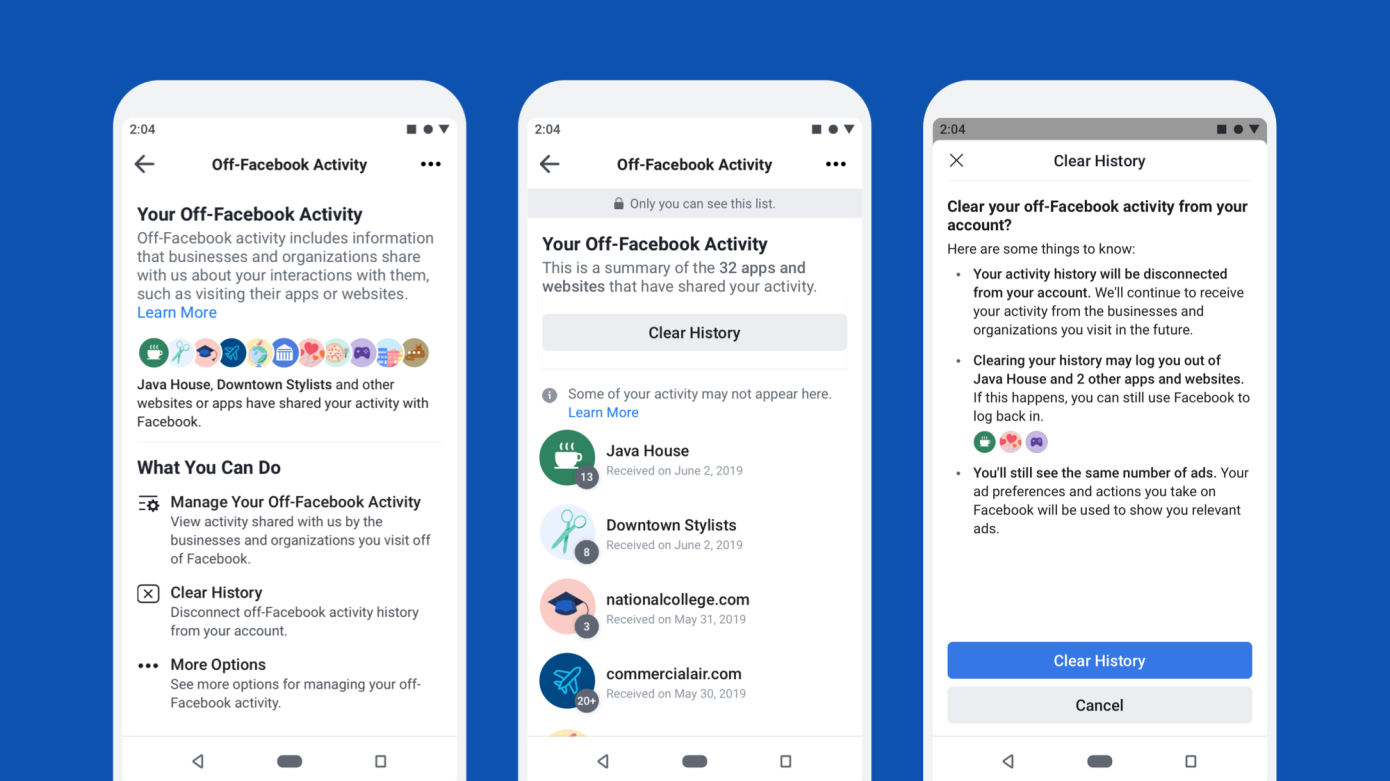

Wehner says to expect that the worst of these privacy headwinds are still to come due to regulatory initiatives like GDPR and CCPA, mobile operating systems and browser providers like Apple and Google limiting access to ad targeting singals, and Facebook’s own product changes like the new way to disconnect off-Facebook data from your acccount.

On Facebook’s perception issues, Zuckerberg said “We’re also focused on communicating more clearly what we stand for. One critique of our approach for much of the last decade was that, because we wanted to be liked, we didn’t always communicate our views as clearly because we were worried about offending people. So this led to some positive but shallow sentiments towards us and towards the company. And my goal for this next decade isn’t to be liked, but to be understood, because in order to be trusted, people need to know what you stand for.”

The business aside, Facebook had another tough quarter under the scrutiny of journalists and regulators. Democratic presidential candidates have railed against Zuckerberg’s decision to continuing allowing misinformation in political ads. The company dropped out of the top 10 places to work, and pledged $130 million to fund an Oversight Board for its content policies.

The CEO was grilled on Capitol Hill about Facebook’s cryptocurrency Libra that seems stuck in its tracks as major partners like Visa and Stripe dropped out. Facebook took heat for how its treats content moderators and how it tried to cut off competitors from its developer platform. The FTC continued its anti-trust investigation and weighed an injunction that would halt Facebook intermingling its messaging app infrastructure.

But those headwinds didn’t stop Facebook’s march forward. Its four main apps took the top four spots amongst the most downloaded apps of the 2010s. It moved deeper into hardware sales with its new Portal TV attachable camera. It acquired gaming companies like Playgiga and the studio behind VR hit Beat Saber, while signing exclusive game streaming deals with influencers like Disguised Toast. It launched Facebook News, Facebook Pay, its dating feature in the US, and it tested a meme-making app called Whale.

Facebook’s share price remains near an all-time high despite today’s tumble. While the world may be increasingly uncomfortable with Facebook’s access to private data, there’s no debate about how incredibly valuable that data is.

Powered by WPeMatico

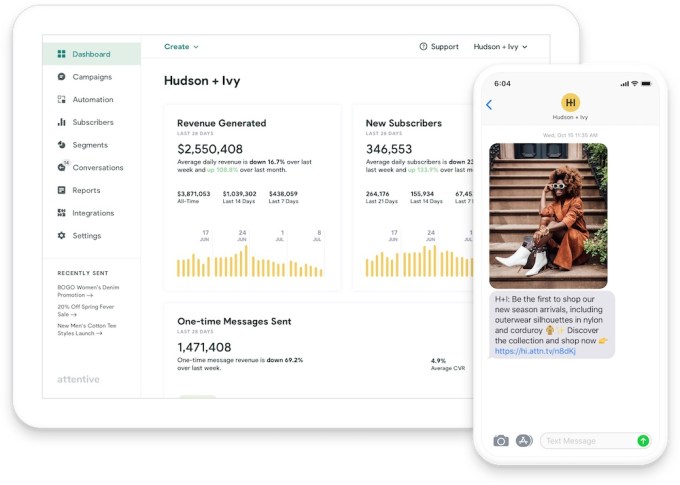

Less than six months after it announced $40 million in funding, Attentive has raised another $70 million — this time in Series C funding.

The new round was led by Sequoia and IVP, two firms that were part of the Series B. Previous investors Eniac Ventures and NextView Ventures also participated.

CEO Brian Long (who, along with his Attentive co-founder Andrew Jones, sold his previous startup TapCommerce to Twitter) told me that he wasn’t planning to raise money again so soon, but things were going even better than expected, with a client list that has grown to more than 750 businesses, including Coach, Urban Outfitters, CB2, PacSun, Party City and Jack in the Box.

Long noted that it’s always smarter to raise money when things are going swimmingly, rather than dealing with the “not-so-fun process” of trying to raise “when you really need it.”

He added, “When you see that you’re doing that well, you think, ‘Hey, we should hire a lot more people to support this growth.’ And then the other piece is just being able to move faster into new areas.”

Long attributed the success Attentive has had thus far to the growing importance of text messages as a channel for businesses to reach consumers, particularly as those consumers are less inclined to open marketing emails or download retailers’ mobile apps. And in contrast to broader messaging platforms, Long said Attentive is “focused on just doing this channel right.”

He said the platform is designed to solve the main problems faced by retailers trying to build a mobile messaging strategy — first, by helping them create a text subscriber list in a way that complies with regulations, then by offering “the ability to send messages that frankly aren’t going to piss people off.”

“We want the messages to be relevant for the consumer, we want to send them things that they care about,” Long said. “The package is on the way, real-time customer service, a product that you were looking at recently is on-sale … there’s a lot of data that you can put to work in order to do it at scale.”

Looking ahead, he hopes to expand beyond the United States and Canada, and to move into industries beyond e-commerce — for example, into more traditional retail, and also to start working with colleges that are looking to attract more applicants.

“Attentive’s growth is a clear indication that people want to interact with brands in new ways, and brands are embracing messaging as an effective way to reach consumers,” said Sequoia partner Pat Grady in a statement. “We are thrilled to double down on our partnership with Attentive so they can continue to deliver fantastic results for their customers and valuable experiences for consumers.”

Attentive has now raised a total of $124 million.

Powered by WPeMatico

Video advertising company Eyeview shut down in December, but its technology will live on thanks to an acquisition by Aki Technologies.

Aki CEO Scott Swanson told me that he’s anticipating serious growth in the demand for ad personalization, particularly as consumers see personalization everywhere else online.

Swanson argued that Eyeview’s technology stands out thanks to its focus on video, with “the ability to generate millions of permutations of a video creative and store them in the cloud.” It offers even more opportunities when combined with Aki’s existing platform, which delivers ads targeted for specific “mobile moments,” like whether the viewer is relaxing at home or out running errands.

Plus, the acquisition allows Aki to expand beyond mobile advertising to desktop and connected TV.

The financial terms of the deal were not disclosed, but Swanson said that in addition to acquiring the technology, he’s also working to bring on old Eyeview clients and hire Eyeview team members (he estimated that he’s hired nearly 15 so far and is aiming for around 20). At the same time, he acknowledged that there are challenges in resurrecting a business that had been shut down.

“The technology itself was decommissioned, it was taken down, it was backed up in the cloud,” Swanson said. “As the acquisition proceeds, we’ll literally be taking the code base and relaunching it in the cloud … Hiring the people was super important, and then because it’s not a traditional acquisition where we get customers and stuff, we have to go call up all the customers one-by-one, just as we have to hire people one-by-one.”

Eyeview had raised nearly $80 million in funding before running out of cash and laying off a team of around 100 employees. (Aki, meanwhile, has raised only a seed round of $3.75 million back in 2016; Swanson said the company has grown organically since then.) The news came only a few months after digital media veteran Rob Deichert took over as CEO.

“While it was disappointing to have to shut down the Eyeview business, I’m very happy that the technology assets have found a home with Aki,” Deichert told me via email. “Their business is a logical fit for the technology.”

And despite Eyeview’s misfortunes, Swanson said he’s confident that the company still works as a standalone business: “Look, these guys have been running a business that was full of really happy customers who were seeing good results and seem to have been disappointed when they shut down.”

The bigger issue, he suggested, is the adtech industry as a whole, with advertisers feeling fatigued “with having too many options,” along with a lack of “appetite on the large exit side.”

“The broader trend here is for companies that operate profitably and can support themselves effectively to become a little bit more tech-enabled managed services business,” Swanson said.

Powered by WPeMatico

AppsFlyer has raised a massive Series D of $210 million, led by General Atlantic.

Founded in 2011, the company is best known for mobile ad attribution — allowing advertisers to see which campaigns are driving results. At the same time, AppsFlyer has expanded into other areas, like fraud prevention.

And in the funding announcement, General Atlantic Manager Director Alex Crisses suggested that there’s a broader opportunity here.

“Attribution is becoming the core of the marketing tech stack, and AppsFlyer has established itself as a leader in this fast-growing category,” Crisses said. “AppsFlyer’s commitment to being independent, unbiased, and representing the marketer’s interests has garnered the trust of many of the world’s leading brands, and we see significant potential to capture additional opportunity in the market.”

Crisses and General Atlantic’s co-president and global head of technology, Anton Levy, are both joining AppsFlyer’s board of directors. Previous investors Qumra Capital, Goldman Sachs Growth, DTCP (Deutsche Telekom Capital Partners), Pitango Venture Capital and Magma Venture Partners also participated in the round, which brings the company’s total funding to $294 million.

AppsFlyer said it works with more than 12,000 customers, including eBay, HBO, Tencent, NBC Universal, Minecraft, US Bank, Macy’s and Nike. It also says it saw more than $150 million in annual recurring revenue in 2019, up 5x from its Series C in 2017.

Co-founder and CEO Oren Kaniel said that as attribution becomes more important, marketers need a partner they can trust. And with AppsFlyer driving $28 billion in ad spend last year, he argued, “There’s a lot of trust there.”

Kaniel added, “It doesn’t really matter how sophisticated your marketing stack is, or whether you have AI or machine learning — if the data feed is wrong … everything else will be wrong. I think companies realize how sensitive and critical this data platform is for them. I think that in the past couple of years, they’re investing more in selecting the right platform.”

In order to ensure that trust, he said that AppsFlyer has avoided any conflicts of interest in its business model — a position that extends to fundraising, where Kaniel made sure not to raise money from any of the big players in digital advertising.

And moving forward, he said, “We will never go into media business, never go into media services. We want to maintain our independence, we want to maintain our previous unbiased positions.”

Kaniel also argued that while he doesn’t see regulations like Europe GDPR and California’s CCPA hindering ad attribution directly, the regulatory environment has justified AppsFlyer’s investment in privacy and security.

“Even more than just being in compliance, [with AppsFlyer], marketers all of a sudden have full control of their data,” he said. “Let’s say on the web, probably your website is sending data and information to partners who don’t need to have access to this information. The reason is, there’s no logic, there’s a lot of pixels going everywhere, the publishers don’t have control. If you use our platform, you have full control, you can configure the exact data points that you’d like to share.”

Powered by WPeMatico

ActionIQ co-founder and CEO Tasso Argyros knows there are plenty of companies promising to help businesses use their customer data to deliver personalized experiences — as he put it, “The space has gotten very, very hot over the last couple of years.”

But in the face of growing competition, ActionIQ (founded in 2014 and headquartered in New York) has attracted some impressive customers, like The New York Times, Conde Nast, American Eagle Outfitters, Vera Bradley and Pandora Media, as well as high-profile investors like Sequoia Capital and Andreessen Horowitz.

Today, it’s announcing that it has raised $32 million in Series C funding.

“At this point, we believe we are four to five years ahead of the market,” Argyros told me. “[Customer data platforms are] very hot, you see people really jumping into it, but nobody really has a product.”

He attributed the rise of these platforms to the growth in customer acquisition costs: “Everybody’s switched their focus from ‘How do we acquire more customers?’ to ‘How do you grow lifetime value?’ ”

The key, Argyros said, is “delivering personalized experiences at scale.” So if you’re a business trying to understand which customers need to be convinced to stick around, which customers are ready to upgrade to a paid subscription and so on, you need a platform like ActionIQ: “What’s common about all these questions is that they’re all data questions.”

He described ActionIQ’s approach as “product-first,” creating self-serve tools for enterprises rather than relying on consulting or IT services, and he said the product is designed to “drive intelligent actions activated through any channel.”

Argyros contrasted this approach with the large marketing clouds, where he said that stitching together products from various acquisitions has led to “a huge data gap between what marketing clouds promise and what they can actually deliver.” And he said other customer data platforms are limited to bringing the data together — but “just putting customer data in one place, that doesn’t mean business can use the customer data to drive value.”

March Capital Partners led the round, with participation from Cisco Ventures, as well as previous investors Sequoia, Andreessen and FirstMark Capital. Meredith Finn, a partner at March, is joining ActionIQ’s board of directors.

“From my professional experience at Salesforce and Twitter, when it comes to building a relationship with your customers, data is everything,” Finn said in a statement. “ActionIQ took a data-first approach from day one in contrast to many vendors that are now scrambling to address their data gaps by duct-taping data infrastructure to their existing point solutions. … The potential of such a platform is limitless, and spans well beyond traditional marketing channels to other areas of customer interactions including web and mobile app experiences, customer support and sales.”

ActionIQ has now raised a total of $75 million in funding. And while the Series C isn’t significantly larger that the $30 million that ActionIQ raised in 2017, Argyros said the company didn’t need to raise a huge round this time around, because it’s already built out the core product.

“A lot of dollars were invested heavily in the product way before the demand was there,” he said. “The Series B was pretty significant because there was so much upfront product investment. … Most of these funds are going towards expanding the business in sales and marketing.”

Powered by WPeMatico

Do you remember as a kid going to the grocery store with your parents and being just totally overwhelmed by the bright, loud packaging of products on shelf after shelf, aisle after aisle?

I certainly do. Each product had a brand — you’d recognize the Kix by its bright red box and Tide by its loud orange bottle. Every package screamed its brand name at you.

Branded packaging as we know it hasn’t been around that long. While people have been packaging goods for millennia, trademarked printed boxes, tins and shrink-wrapped containers were only invented in the late 1800s — less than 150 years ago, beginning with Uneeda Biscuits around 1896.

When branded packaging was invented, and up until very recently, its purpose and value to nearly every industry made a ton of good sense. The average consumer would shop in a catalog, browsing ads and offerings, or in a store, perusing shelves of products. The more a product stood out and set itself apart, the more memorable it would be and the more likely it would be purchased. Good packaging made products easy to recommend and spread by sharing visually.

And then, the internet came along.

Our team recently launched our new studio product, Regular, a service directed at small businesses hitting their growth inflection point. As we began to design our own website and work on branding, we did a lot of research into branding trends for consumer packaged goods, and what we uncovered was surprising.

We found was that there is a surprising movement towards “unbranding” — specifically choosing not to create a strong association between a product and its maker. Instead of bright packaging, large logos and stamped products, many companies are now going the other direction by operating without logos and offering minimal (or no) packaging.

Pens from MUJI (Photo: Michael/Flickr)

One of the earliest companies to adopt this mindset was Japanese home goods store MUJI, whose name literally means “No Brand” (it doesn’t get more literal than that). Most of its products come unpackaged with just a small price tag, or in minimal packaging with a single informational label (e.g., “lotion,” “body soap”) to identify its contents.

But MUJI has been since the 1980s, so why are we talking about this now?

Powered by WPeMatico

In a world where ad rates are declining for traditional broadcast media, the corporations responsible for making the fictions that millions devour daily need to find a new business model.

Subscription services are on the rise — with every major broadcaster launching an on-demand service — and so are ad-supported video streaming services to replace the traditional networks.

But there’s another Holy Grail of the advertising industry, long thought to be too technologically difficult to achieve, that may finally be within reach. It’s the on-demand product placement of branded goods in a video, and it’s the technology that Ryff has been developing since it was founded in early 2018.

Product placement is an increasingly big business in the U.S., raking in some $11.44 billion in 2019, according to data collected by Statista. That figure is up from $4.75 billion in 2012. The same report indicated that roughly 49% of Americans took action after seeing product placement in media.

The effectiveness of product placement has even been proven by researchers from Indiana University and Emory University. They found that “prominent product placement embedded in television programming does have a net positive impact on online conversations and web traffic for the brand.”

And while streaming services enjoy the dollars their subscribers are throwing at them, they’re also looking at ways to diversify their revenue streams. Netflix and Hulu are both expanding their product marketing divisions and analysts like those from Forrester Research predict that product placement will be a huge moneymaker for the company as traditional ad rates decline.

There are companies that handle product placement already. Startups like Branded Entertainment Network, which works with brands and producers to place real brands into contextually relevant scenes in movies and television, and Mirriad, which adds branded billboards to scenes, are working to bring more money to platforms and producers.

Ryff takes the technology to the next level, using computer vision, machine learning and rendering technologies to identify objects in a scene and replace them with branded products that can be tailored based on customer data.

“The infusion of SVOD/streaming platforms into the market, combined with platforms like Netflix that are unsuccessfully trying to grow their subscriber base will force those same platforms to explore and embrace alternative revenue streams,” said Marlon Nichols, managing general partner at MaC Venture Capital, and a new director on the Ryff board. “In addition, consumers on paid platforms do not want their content consumption interrupted by ads. As such, product placement will be an important growth channel and Ryff’s new marketplace and unique technology set it up to be the unequivocal growth market leader.”

To continue its technology development and ramp up sales and marketing, the company has raised $5 million in financing. According to Crunchbase, Ryff had previously raised $3.6 million from investors, including a subsidiary of the Mahindra Group and undisclosed investors. The new financing came from Valor Siren Ventures, MaC Venture Capital, Moneta Ventures and Vulcan Capital.

“Ryff’s offering is well-timed with the rapidly increasing demand for solutions that extend the reach of a brand’s content and drive business results,” said Uday Ghare, vice president for media and entertainment at Tech Mahindra, in a statement at the time of the company’s investment. “We believe the market will continue to see a shift of brand dollars to both content marketing and programmatic advertising as brands increase their reliance on content-centric programs and look to scale those efforts.”

Ryff’s ads can be tailored to the viewer’s taste, the platform on which video is being distributed, the geography of the broadcast, the date and time of the broadcast and a broader demographic profile, according to the company. Basically it’s like AdWords for videos.

In a blog post writing about the rationale behind his investment firm’s capital commitment to the company, Marlon Nichols of MaC Ventures wrote:

Imagine a future where an IP owner can maximize the value of its content by putting it on the Ryff marketplace, where that content will be mapped for dozens if not hundreds of product placement opportunities and be layered with restrictions that comply with creative needs. Those opportunities will be ranked and priced by their effectiveness to drive marketing goals for brands. Brands can bid on in-video placement opportunities that fit their marketing strategies and budgets. 3D brand assets can be uploaded and inserted dynamically into content right before the moment of video delivery.

Ryff’s first disclosed partnership is with the “reality” television producer Endemol Shine.

“Ryff successfully takes the concept of product placement, the only advertising format that can’t be skipped by the viewer, and delivers a scalable and adaptable advertising solution that can be applied to any content, at any time and in any market,” said Roy Taylor, founder and CEO of Ryff, in a statement. “The result benefits all — content free from annoying distractions, audience-specific brand placement and delivering a new means towards monetizing video assets.”

Powered by WPeMatico