Walmart

Auto Added by WPeMatico

Auto Added by WPeMatico

Yesterday at TechCrunch’s Enterprise event in San Francisco, we sat down with three venture capitalists who spend a lot of their time thinking about enterprise startups. We wanted to ask what trends they are seeing, what concerns they might have about the state of the market and, of course, how startups might persuade them to write out a check.

We covered a lot of ground with the investors — Jason Green of Emergence Capital, Rebecca Lynn of Canvas Ventures and Maha Ibrahim of Canaan Partners — who told us, among other things, that startups shouldn’t expect a big M&A event right now, that there’s no first-mover advantage in the enterprise realm and why grit may be the quality that ends up keeping a startup afloat.

Jason Green: When we started Emergence 15 years ago, we saw maybe a few hundred startups a year, and we funded about five or six. Today, we see over 1,000 a year; we probably do deep diligence on 25.

Powered by WPeMatico

Flipkart, the largest e-commerce platform in India, said Tuesday it has concluded the roll-out of a range of features to its shopping app in what is its biggest update in recent years.

Chief among these new features is access to Flipkart in Hindi language. Prior to the revamp of the app, Flipkart was available only in English, a language spoken by 10% of India’s 1.3 billion population.

Flipkart says it is hoping that the new features, which includes a video streaming service, would help it reach the next 200 million users in India.

The major bet on Hindi, a language spoken by more than 500 million people in India, illustrates a growing push from local and international companies operating in the country as they adapt their services and business models to go beyond the urban cities.

And that’s where much of the opportunity, which countless startups and companies have trumpeted to investors to successfully raise hundreds of millions of dollars in debt and venture capital in recent years, lies in the nation.

Powered by WPeMatico

Walmart came out swinging earlier this week in a lawsuit that accused Tesla of breach of contract and gross negligence over problems with rooftop solar panel systems installed at the retail giant’s stores.

Now, just days later, the lawsuit has been placed on hold while the two companies try to reach an agreement that would keep the solar installations in place and put them back in service, according to a joint statement issued late Thursday night.

“Walmart and Tesla look forward to addressing all issues and re-energizing Tesla solar installations at Walmart stores, once all parties are certain that all concerns have been addressed,” the statement read. “Together, we look forward to pursuing our mutual goal of a sustainable energy future. Above all else, both companies want each and every system to operate reliably, efficiently, and safely.”

Walmart hasn’t dropped the lawsuit. The complaint is still on file with New York state court. But the two parties are going to try to reach an agreement that would avoid a lawsuit.

The lawsuit, which is aimed at Tesla’s energy unit that was formerly known as SolarCity, alleges that seven fires on Walmart rooftops were caused by the solar panel systems. Walmart asked Tesla to remove the solar panel systems on all 244 stores where they are currently installed and to pay for damages related to fires that the retailer alleges stem from the panels.

Now, a Walmart spokesperson said it is “actively working towards a resolution” with Tesla.

Neither Tesla or Walmart would explain the details of the negotiations.

The stakes are high for Tesla. Earlier this month, Tesla CEO Elon Musk announced a new rental offering for solar power in a bid to reboot the flagging renewable energy business.

Tesla’s share of the solar market has declined since its merger with SolarCity in 2016. In the second quarter Tesla deployed only 29 megawatts of new solar installations, while the number one and two providers of consumer solar, SunRun and Vivint Solar, installed 103 megawatts and 56 megawatts, respectively.

Tesla’s renewable energy business includes residential and commercial solar and energy storage products. The company also has a utility-scale energy product called Megapack. While Tesla still produces solar panels for residential use, much of its focus has been on developing its solar roof, which is comprised of tiles. It still operates a commercial business, which targets municipalities, schools, affordable housing, enterprise and agriculture and water districts as customers.

The company doesn’t provide a breakdown of its solar installations, making it difficult to determine if the commercial business is flat, falling or on the rise. Language in its latest 10-Q suggests Tesla is putting a renewed effort into its solar business.

Tesla said it’s working on revamping the customer service experience for solar products, according to the 10-Q. The company said while its retrofit solar system deployments have decreased it expects they “will stabilize and grow in the second half of the year.”

Powered by WPeMatico

India’s e-commerce giant Flipkart said on Tuesday that it is revamping its shopping app to add support for Hindi language, a video streaming service and an audio-visual assistant, the latest in a series of recent efforts to expand its reach in the country.

The e-commerce firm, which sold a majority stake to Walmart for $16 billion last year and leads the local market, told TechCrunch that it has started to roll out the features on its shopping app and will push it to all its existing users within the next 20 days.

Only 10% of India’s 1.3 billion people speak English. Flipkart said it has been working to customize its entire platform for several months to add support for Hindi. More than 500 million people in India speak Hindi.

As part of the revamp, the company is also introducing an “audio visual guided navigation” feature, also built in Hindi, that is aimed at first-time internet users — and existing online users not comfortable with making transactions online — to make it easier for them to navigate the service and place orders.

Its rival Amazon India added support for Hindi last year, though the feature is limited to basic text translation.

As part of the accessibility push, Flipkart is also introducing an in-app video streaming feature dubbed “Flipkart Videos” that will syndicate movies, shows and other long-form and short-form content from a number of production houses and movie studios, the company said.

The inclusion of the video streaming feature comes as Indians’ appetite for consuming media content on the internet has ballooned in the recent years. Hotstar, a Disney-owned video streaming service, has amassed more than 300 million monthly active users in the country.

Flipkart said the video streaming feature will enable it to invite a new segment of users to its platform who are online but don’t currently shop on the internet. Even as more than 500 million users are connected to the web in India, only tens of millions of them currently shop there.

The streaming feature will be accessible to all users at no charge without any loyalty program, a company spokesperson said, refuting a recent media report that claimed otherwise.

“In the past 10 years our vision and ethos have been to solve for ‘Real India,’ create India specific tech solutions, here in India. What we are rolling out when it comes to addressing the needs of the next 200 million users in our country, is taking forward those founding principles of access and affordability,” said Kalyan Krishnamurthy, Group CEO of Flipkart, in a statement.

“We strongly believe that the next phase of our growth is rooted in loyalty, democratizing e-commerce and the country will continue seeing more innovations that stem from our deep understanding of Indian consumers, especially middle India.”

Flipkart said it is also attempting to make it easier for users to discover items on its app. So it is introducing a feed called “Flipkart Ideas” that will populate short-form videos, animated images, polls and quizzes.

For instance, a user may see a short-form video that shows a sportsperson wearing a pair of sneakers, a t-shirt, a pair of jeans and a cap. If they tap on the video, they will see the exact items the person in the video is wearing and other similar items. One more tap, and the user would be able to purchase any of those items.

The company said it is working with more than 400 influencers and 30 brands to create content that will appear on the feed.

All of these features, as well as a gaming section that Flipkart introduced last year, will now appear at the bottom of the screen for easier navigation, the company said. More than half a million users in India play mini-games on Flipkart everyday. The company said it will introduce more games to boost engagement levels and offer loyalty points as incentive to customers.

Powered by WPeMatico

The unchecked digital land grab for consumers’ personal data that has been going on for more than a decade is coming to an end, and the dominoes have begun to fall when it comes to the regulation of consumer privacy and data security.

We’re witnessing the beginning of a sweeping upheaval in how companies are allowed to obtain, process, manage, use and sell consumer data, and the implications for the digital ad competitive landscape are massive.

On the backdrop of evolving privacy expectations and requirements, we’re seeing the rise of a new class of digital advertising player: consumer-facing apps and commerce platforms. These commerce companies are emerging as the most likely beneficiaries of this new regulatory privacy landscape — and we’re not just talking about e-commerce giants like Amazon.

Traditional commerce companies like eBay, Target and Walmart have publicly spoken about advertising as a major focus area for growth, but even companies like Starbucks and Uber have an edge in consumer data consent and, thus, an edge over incumbent media players in the fight for ad revenues.

with a big hand making stop gesture (No!)")

Image via Getty Images / alashi

By now, most executives, investors and entrepreneurs are aware of the growing acronym soup of privacy regulation, the two most prominent ingredients being the GDPR (General Data Protection Regulation) and the CCPA (California Consumer Privacy Act).

Powered by WPeMatico

Away from the limelight of the press and the frenzy of fundraising, a tech startup in India has achieved a feat that few of its peers have managed: going public.

IndiaMART, the country’s largest online platform for selling products directly to businesses, raised nearly $70 million in a rare tech IPO for India this week.

The milestone for the 23-year-old firm is so uncommon for India’s otherwise burgeoning startup ecosystem that, beyond being over-subscribed 36 times, pent up demand for IndiaMART’s stock saw its share price pop 40% on its first day of trading on National Stock Exchange on Thursday — a momentum that it sustained on Friday.

The stock ended Friday at Rs 1326 ($19.3), compared to its issue price of Rs 973 ($14.2).

IndiaMART is the first business-to-business e-commerce firm to go public in India. Its IPO also marks the first listing for a firm following the May reelection of Narendra Modi as the nation’s Prime Minister and the months-long drought that led to it.

Accounting firm EY said it expects more companies from India to follow suit and file for IPO in the coming months.

“Now that national elections are over and favorable results secured, IPO activity is expected to gain momentum in H2 2019 (second half of the year). Companies that had filed their offer documents with the Indian stock markets regulator during H2 2018 and Q1 2019 may finally come to market in the months ahead,” it said in a statement (PDF).

The fireworks of the IPO are just as impressive as IndiaMART’s journey.

The startup was founded in 1996 and for the first 13 years, it focused on exports to customers abroad, but it has since modernized its business following the wave of the internet.

“The thesis was, in 1996, there were no computers or internet in India. The information about India’s market to the West was very limited,” Dinesh Agarwal, co-founder and CEO of IndiaMART, told TechCrunch in an interview.

Until 2008, IndiaMART was fully bootstrapped and profitable with $10 million in revenue, Agarwal said. But things started to dramatically change in that year.

“The Indian rupee became very strong against the dollar, which dwindled the exports business. This is also when the stock market was collapsing in the West, which further hurt the exports demand,” he explained.

Dinesh Agarwal, founder and CEO of IndiaMart.com, poses for a profile shot on July 29, 2015 in Noida, India.

By this time, millions of people in India were on the internet and, with tens of millions of people owning a feature phone, the conditions of the market had begun to shift towards digital.

“This is when we decided to pursue a completely different path. We started to focus on the domestic market,” Agarwal said.

Over the last 10 years, IndiaMART has become the largest e-commerce platform for businesses with about 60% market share, according to research firm KPMG. It handles 97,000 product categories — ranging from machine parts, medical equipment and textile products to cranes — and has amassed 83 million buyers and 5.5 million suppliers from thousands of towns and cities of India.

According to the most recent data published by the Indian government, there are about 50 to 60 million small and medium-sized businesses in India, but only around 10 million of them have any presence on the web. Some 97% of the top 50 companies listed on National Stock Exchange use IndiaMART’s services, Agarwal said.

That’s not to say that the transition to the current day was a straightforward process for the company. IndiaMART tried to capitalize on its early mover advantage with a stream of new services which ultimately didn’t reap the desired rewards.

In 2002, it launched a travel portal for businesses. A year later, it launched a business verification service. It also unveiled a payments platform called ABCPayments. None of these services worked and the firm quickly moved on.

Part of IndiaMART’s success story is its firm leadership and how cautiously it has raised and spent its money, Rajesh Sawhney, a serial angel investor who sits on IndiaMART’s board, told TechCrunch in an interview.

IndiaMART, which employs about 4,000 people, is operationally profitable as of the financial year that ended in March this year. It clocked some $82 million in revenue in the year. It has raised about $32 million to date from Intel Capital, Amadeus Capital Partners and Quona Capital. (Notably, Agarwal said that he rejected offers from VCs for a very long time.)

The firm makes most of its revenue from subscriptions it sells to sellers. A subscription gives a seller a range of benefits including getting featured on storefronts.

4/4. So many Indian small businesses have so much to thank @DineshAgarwal for. And after the iconic IPO, so many Indian entreprenuers will have so much to thank him for – forever unlocking the Indian public markets to current & future generation of Indian internet companies

— Kunal Bahl (@1kunalbahl) July 4, 2019

There are only a handful of internet companies in India that have gone public in the last decade. Online travel service MakeMyTrip went public in 2010. Software firm Intellect Design Arena and e-commerce store Koovs listed in 2014, then travel portal Yatra and e-commerce firm Infibeam followed two years later.

India has consistently attracted billions of dollars in funding in recent years and produced many unicorns. Those include Flipkart, which was acquired by Walmart last year for $16 billion, Paytm, which has raised more than $2 billion to date, Swiggy, which has bagged $1.5 billion to date, Zomato, which has raised $750 million, and relatively new entrant Byju’s — but few of them are nearing profitability and most likely do not see an IPO in their immediate future.

In that context, IndiaMART may set a benchmark for others to follow.

“The fact that we have a homegrown digital commerce business, serving both the urban and smaller cities, and having struggled and been around for so long building a very difficult business and finally going public in the local exchange is a phenomenal story,” Ganesh Rengaswamy, a partner at Quona Capital, told TechCrunch in an interview. “It keeps the story of India tech, to the Western world, going.”

Congratulations @DineshAgarwal for an iconic IPO! @IndiaMART has set an example and hope for all Indian Internet companies looking to go public. Cheers! https://t.co/yJumFjfitS

— Vani Kola (@VaniKola) July 4, 2019

Generally, it is agreed that there are too few IPOs in India and the industry can benefit from momentum and encouragement of high profile and successful public listings.

“There is a firm consensus that in India, markets will prefer only the IPOs of companies that are profitable. And investors in India might not value those companies. Both of these issues are being addressed by IndiaMART,” said Sawhney.

“We need 30 to 40 more IPOs. This will also mean that the stock market here has matured and understands the tech stocks and how it is different from other consumer stocks they usually handle. More tech companies going public would also pave the way for many to explore stock exchanges outside of India.

“Indian market is ready for more tech stocks. We just need to get more companies to go out there,” Sawhney added, although he did predict that it will take a few years before the vast majority of leading startups are ready for the public market.

The Indian government, for its part, this week announced a number of incentives to uplift the “entrepreneurial spirit” in the nation.

Finance minister Nirmala Sitharaman said the government would ease foreign direct investment rules for certain sectors — including e-commerce, food delivery, grocery — and improve the digital payments ecosystem. Sitharaman, who is the first woman to hold this position in India, said the government would also launch a TV program to help startups connect with venture capitalists.

IndiaMART has managed to build a sticky business that compels more than 55% of its customers to come back to the platform and make another transaction within 90 days, Agarwal — its CEO — said. With some 3,500 of its 4,000 employees classified as sales executives, the company is aggressive in its pursuit of new customers. Moving forward, that will remain one of its biggest focuses, according to Agarwal.

“Most of our time still goes into educating MSMEs on how to use the internet. That was a challenge 20 years ago and it remains a challenge today,” he told TechCrunch.

In recent years, IndiaMART has begun to expand its suite of offerings to its business customers in a bid to increase the value they get from its platform and thus increase their reliance on its service.

IndiaMART has built a customer relationship management (CRM) tool so that customers need not rely on spreadsheets or other third-party services.

“We will continue to explore more SaaS offerings and look into solving problems in accounting, invoice management and other areas,” said Agarwal.

The firm also recently started to offer payment facilitation between buyers and sellers through a PayPal -like escrow system.

“This will bridge the trust gap between the entities and improve an MSME’s ability to accept all kinds of payment options including the new age offerings.”

There’s an elephant in the room, however.

A bigger challenge that looms for IndiaMART is the growing interest of Amazon and Walmart in the business-to-business space. Several startups including Udaan — which has raised north of $280 million from DST Global and Lightspeed Venture Partners — have risen up in recent years and are increasingly expanding their operations. Agarwal did not seem much worried, however, telling TechCrunch that he believes that his prime competition is more focused on B2C and serving niche audiences. Besides he has $100 million in the bank himself.

Indeed, as Quona Capital’s Rengaswamy astutely noted, competition is not new for IndiaMART — the company has survived and thrived more than two decades of it.

“Alibaba came and gave up,” he noted.

An important — and unanswered question — that follows the successful IPO is how IndiaMART’s stock will fare over the coming months. A glance to the U.S. — where hyped companies like Uber, Lyft and others have seen prices taper off — shows clearly that early demand and sustained stock performance are not one and the same.

Nobody knows at this point, and the added complexity at play is that the concept of a tech IPO is so uncommon in India that there is no definitive answer to it… yet. But IndiaMART’s biggest achievement may be that it sets the pathway that many others will follow.

Powered by WPeMatico

IBM announced its latest blockchain initiative today. This one is in partnership with KPMG, Merk and Walmart to build a drug supply chain blockchain pilot.

These four companies are coming together to help come up with a solution to track certain drugs as they move through a supply chain. IBM is acting as the technology partner, KPMG brings a deep understanding of the compliance issues, Merk is of course a drug company and Walmart would be a drug distributor through its pharmacies and care clinics.

The idea is to give each drug package a unique identifier that you can track through the supply chain from manufacturer to pharmacy to consumer. Seems simple enough, but the fact is that companies are loathe to share any data with one another. The blockchain would provide an irrefutable record of each transaction as the drug moved along the supply chain, giving authorities and participants an easy audit trail.

The pilot is part of a set of programs being conducted by various stakeholders at the request of the FDA. The end goal is to find solutions to help comply with the U.S. Drug Supply Chain Security Act. According to the FDA Pilot Program website, “FDA’s DSCSA Pilot Project Program is intended to assist drug supply chain stakeholders, including FDA, in developing the electronic, interoperable system that will identify and trace certain prescription drugs as they are distributed within the United States.”

IBM hopes that this blockchain pilot will show it can build a blockchain platform or network on top of which other companies can build applications. “The network in this case, would have the ability to exchange information about these pharmaceutical shipments in a way that ensures privacy, but that is validated,” Mark Treshock, global blockchain solutions leader for healthcare and life sciences at IBM told TechCrunch.

He believes that this would help bring companies on board that might be concerned about the privacy of their information in a public system like this, something that drug companies in particular worry about. Trying to build an interoperable system is a challenge, but Treshock sees the blockchain as a tidy solution for this issue.

Some people have said that blockchain is a solution looking for a problem, but IBM has been looking at it more practically, with several real-world projects in production, including one to track leafy greens from field to store with Walmart and a shipping supply chain with Maersk to track shipping containers as they move throughout the world.

Treshock believes the Walmart food blockchain is particularly applicable here and could be used as a template of sorts to build the drug supply blockchain. “It’s very similar, tracking food to tracking drugs, and we are leveraging or adopting the assets that we built for food trust to this problem. We’re taking that platform and adapting it to track pharmaceuticals,” he explained.

Powered by WPeMatico

Away from the limelight of urban cities, where an increasingly growing number of firms are fighting for a piece of India’s digital payments market, a South Korean startup’s app is quietly helping millions of Indians pay digitally and enjoy many financial services for the first time.

The app, called True Balance, began its life as a tool to help users easily find their mobile balance, or topping up pre-pay mobile credit. But in its four-year journey, its ambition has significantly grown beyond that. Today, it serves as a digital wallet app that helps users pay their mobile and electricity bills, and it also lets users pay later.

One thing that has not changed for the parent company of True Balance, BalanceHero, which employs less than 200 people, is its consumer focus. It is strictly catering to people in tier-two and tier-three markets — often dubbed as India 2 and India 3 — who have relatively limited access to the internet, and lower financial power. And it remains operational just in India.

Even as India is already the second largest internet market with more than 500 million users, more than half of its population remains offline. In recent years, the nation has become a battleground for Silicon Valley giants and Chinese firms that are increasingly trying to win existing users and bring the rest of the population online.

And like many other companies, BalanceHero’s bet on India is beginning to pay off. The startup told TechCrunch today that it has clocked $100 million in GMV sales and has amassed about 60 million registered users. Yongsung Yoo, a spokesperson for the startup, added that BalanceHero, which has raised $42 million to date, is also nearing profitability.

The South Korean firm’s playbook is different from many other players that are racing to claim a slice of India’s burgeoning digital payments market. True Balance competes with the likes of Paytm, MobiKwik, Google, Amazon and Walmart-owned Flipkart, though its competitors are still largely catering to the urban parts of India.

In the last two years, many firms have begun to explore smaller cities and towns, but their services are still too out-of-the-world for local residents. Raising awareness about digital services is a big challenge in such markets, Yoo said, so the startup is relying on existing users to help others make their first transactions and in paying bills.

Yoo said the startup rewards these “digital agents” with cash back and other benefits. For these digital agents, many of whom do not have a day job, True Balance has emerged as a side project to make extra money.

Later this year, Yoo said the startup, which recently also added support for UPI in its service, will open an e-commerce store on its app and also offer insurance to users. To accelerate its growth and expansion, True Balance is in the final stages of raising between $50 million to $70 million in a new round that it expects to close in July this year, Yoo said.

Powered by WPeMatico

Amazon and Walmart’s problems in India look set to continue after Narendra Modi, the biggest force to embrace the country’s politics in decades, led his Hindu nationalist Bharatiya Janata Party to a historic landslide re-election on Thursday, reaffirming his popularity in the eyes of the world’s largest democracy.

The re-election, which gives Modi’s government another five years in power, will in many ways chart the path of India’s burgeoning startup ecosystem, as well as the local play of Silicon Valley companies that have grown increasingly wary of recent policy changes.

At stake is also the future of India’s internet, the second largest in the world. With more than 550 million internet users, the nation has emerged as one of the last great growth markets for Silicon Valley companies. Google, Facebook, and Amazon count India as one of their largest and fastest growing markets. And until late 2016, they enjoyed great dynamics with the Indian government.

But in recent years, New Delhi has ordered more internet shutdowns than ever before and puzzled many over crackdowns on sometimes legitimate websites. To top that, the government recently proposed a law that would require any intermediary — telecom operators, messaging apps, and social media services among others — with more than 5 million users to introduce a number of changes to how they operate in the nation. More on this shortly.

Powered by WPeMatico

More than five years ago, Sequoia partner Alfred Lin called Tony Xu, the founder of a small on-demand delivery startup called DoorDash, to say he was passing on the company’s seed round.

This was, of course, before venture capital funding in food delivery startups had taken off. DoorDash, launched out of Xu’s Stanford graduate school dorm room, wasn’t worth Sequoia’s capital — yet.

Today, venture capitalists are valuing the San Francisco-based company at a whopping $12.6 billion with a $600 million Series G. New investors Darsana Capital Partners and Sands Capital participated in the deal, which nearly doubles DoorDash’s previous valuation, alongside existing backers Coatue Management, Dragoneer, DST Global, Sequoia Capital, the SoftBank Vision Fund and Temasek Capital Management.

As for Sequoia’s Alfred Lin, he realized his mistake years ago and jumped in on DoorDash’s 2014 Series A, and has participated in every subsequent round since. DoorDash, a graduate of Y Combinator’s Summer 2013 cohort, is also backed by Kleiner Perkins, CRV and Khosla Ventures, among others. In total, the company has raised $2.5 billion in VC funding, making it one of the most well-capitalized private companies in the U.S.

SoftBank, via its prolific dealmaker Jeffrey Housenbold, was responsible for making DoorDash a unicorn in early 2018. The nearly $100 billion Vision Fund led DoorDash’s $535 million Series D, valuing the business at $1.4 billion. Just three months ago, the SoftBank Vision Fund, DST Global, Coatue Management, GIC, Sequoia and Y Combinator put an additional $400 million in the fast-growing business.

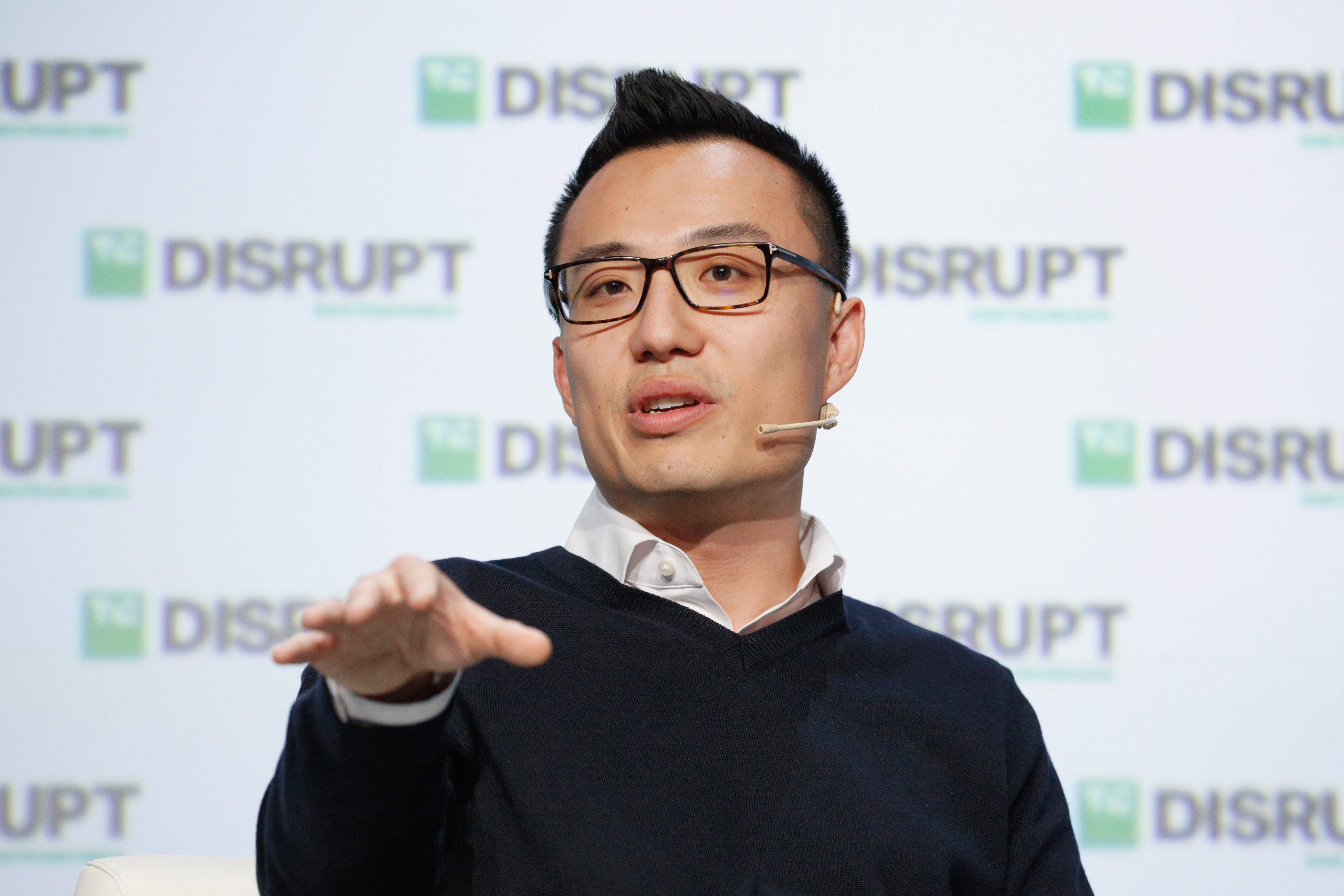

SAN FRANCISCO, CA – SEPTEMBER 05: DoorDash CEO Tony Xu speaks onstage during Day 1 of TechCrunch Disrupt SF 2018 at Moscone Center on September 5, 2018 in San Francisco, California. (Photo by Kimberly White/Getty Images for TechCrunch)

Xu told TechCrunch the company’s Series F was “a reflection of superior performance over the past year.” DoorDash was currently seeing 325% growth year-over-year, he said, pointing to recent data from Second Measure showing the service had overtaken Uber Eats in the U.S., coming in second only to GrubHub.

“I think the numbers speak for themselves,” Xu said at the time. “If you just run the math on DoorDash’s course and speed, we’re on track to be number one.”

At a venture capital-focused summit hosted in April, Xu added that DoorDash was the largest delivery platform in America by “pretty wide margins,” explaining that it was, in fact, growing 4x faster than its next closest peer. In this morning’s announcement, the company added that it’s grown 60% since its late February Series F, with its annualized total sales hitting $7.5 billion in March, an increase of 280% year-over-year.

Still, one wonders what kind of growth metrics DoorDash might be sharing to attract that kind of valuation multiple. The company has yet to disclose revenues and is not yet profitable, but has seen its price tag grow astronomically in just two years. Since March 2018, DoorDash’s valuation has skyrocketed from $1.4 billion to $4 billion with a $250 million Series E to $7.1 billion with a $350 million Series F and, finally, to nearly $13 billion with its Series G.

The $12.6 billion valuation makes DoorDash one of the 10 most valuable venture-backed companies in the U.S., surpassing Coinbase, Instacart and even Slack, according to PitchBook.

DoorDash is currently active in more than 4,000 cities in the U.S. and Canada, with hundreds of partners, including both restaurants and supermarkets (Walmart is using DoorDash for grocery deliveries). The company also operates DoorDash Drive, which allows businesses to use the DoorDash network to make their own deliveries.

Powered by WPeMatico