Walmart

Auto Added by WPeMatico

Auto Added by WPeMatico

Vijay Shekhar Sharma, founder and chief executive of India’s most valuable startup, Paytm, posed an existential question in a recent press conference.

“What do you think of the commercial model for digital mobile payments. How do we make money?” Sharma asked Nandan Nilekani, one of the key architects of the Universal Payments Infrastructure that created a digital payments revolution in the country.

It’s the multi-billion-dollar question that scores of local startups and international giants have been scrambling to answer as many of them aggressively shift their focus to serving merchants and building lending products and other financial services .

New Delhi’s abrupt move to invalidate much of the paper bills in the cash-dominated nation in late 2016 sent hundreds of millions of people to cash machines for months to follow.

For a handful of startups such as Paytm and MobiKwik, this cash crunch meant netting tens of millions of new users in a span of a few months.

India then moved to work with a coalition of banks to develop the payments infrastructure that, unlike Paytm and MobiKwik’s earlier system, did not act as an intermediary “mobile wallet” to serve as an intermediary between users and their banks, but facilitated direct transaction between two users’ bank accounts.

Silicon Valley companies quickly took notice. For years, Google and the likes have attempted to change the purchasing behavior of people in many Asian and African markets, where they have amassed hundreds of millions of users.

In Pakistan, for instance, most people still run errands to neighborhood stores when they want to top up credit to make phone calls and access the internet.

With China keeping its doors largely closed for foreign firms, India, where many American giants have already poured billions of dollars to find their next billion users, it was a no-brainer call.

“Unlike China, we have given equal opportunities to both small and large domestic and foreign companies,” said Dilip Asbe, chief executive of NPCI, the payments body behind UPI.

And thus began the race to participate in the grand Indian experiment. Investors have followed suit as well. Indian fintech startups raised $2.74 billion last year, compared to 3.66 billion that their counterparts in China secured, according to research firm CBInsights.

And that bet in a market with more than half a billion internet users has already started to pay off.

“If you look at UPI as a platform, we have never seen growth of this kind before,” Nikhil Kumar, who volunteered at a nonprofit organization to help develop the payments infrastructure, said in an interview.

In October, just three years after its inception, UPI had amassed 100 million users and processed over a billion transactions. It has sustained its growth since, clocking 1.25 billion transactions in March — despite one of the nation’s largest banks going through a meltdown last month.

“It all comes down to the problem it is solving. If you look at the western markets, digital payments have largely been focused on a person sending money to a merchant. UPI does that, but it also enables peer-to-peer payments and across a wide-range of apps. It’s interoperable,” said Kumar, who is now working at a startup called Setu to develop APIs to help small businesses easily accept digital payments.

Vice-president of Google’s Next Billion Users Caesar Sengupta speaks during the launch of the Google “Tez” mobile app for digital payments in New Delhi on September 18, 2017 (Photo: Getty Images via AFP PHOTO / SAJJAD HUSSAIN)

The Google Pay app has amassed over 67 million monthly active users. And the company has found the UPI pipeline so fascinating that it has recommended similar infrastructure to be built in the U.S.

In August, the Federal Reserve proposed to develop a new inter-bank 24×7 real-time gross settlement service that would support faster payments in the country. In November, Google recommended (PDF) that the U.S. Federal Reserve implement a real-time payments platform such as UPI.

“After just three years, the annual run rate of transactions flowing through UPI is about 19% of India’s Gross Domestic Product, including 800 million monthly transactions valued at approximately $19 billion,” wrote Mark Isakowitz, Google’s vice president of Government Affairs and Public Policy.

Paytm itself has amassed more than 150 million users who use it every year to make transactions. Overall, the platform has 300 million mobile wallet accounts and 55 million bank accounts, said Sharma.

But despite on-boarding more than a hundred million users on their platform, payment firms are struggling to cut their losses — let alone turn a profit.

At an event in Bangalore late last year, Sajith Sivanandan, managing director and business head of Google Pay and Next Billion User Initiatives, said current local rules have forced Google Pay to operate in India without a clear business model.

Mobile payment firms never levied any fee to users as a strategy to expand their reach in the country. A recent directive from the government has now put an end to the cut they were receiving to facilitate UPI transactions between users and merchants.

Google’s Sivanandan urged the local payment bodies to “find ways for payment players to make money” to ensure every stakeholder had incentives to operate.

Paytm, which has raised more than $3 billion to date, reported a loss of $549 million in the financial year ending in March 2019.

The firm, backed by SoftBank and Alibaba, has expanded to several new businesses in recent years, including Paytm Mall, an e-commerce venture, social commerce, financial services arm Paytm Money and a movies and ticketing category.

This year, Paytm has expanded to serve merchants, launching new gadgets such as a stand that displays QR check-out codes that comes with a calculator and a battery pack, a portable speaker that provides voice confirmations of transactions and a point-of-sale machine with built-in scanner and printer.

In an interview with TechCrunch, Sharma said these devices are already garnering impressive demand from merchants. The company is offering these gadgets to them as part of a subscription service that helps it establish a steady flow of revenue.

The firm’s Money arm, which offers lending, insurance and investing services, has amassed over 3 million users. The head of Paytm Money, Pravin Jadhav, resigned from the company this week, a person familiar with the matter said. A Paytm spokeswoman declined to comment. (Indian news outlet Entrackr first reported the development.)

Flipkart’s PhonePe, another major player in India’s payments market, today serves more than 175 million users, and over 8 million merchants. Its app serves as a platform for other businesses to reach users, explained Rahul Chari, co-founder and CTO of the firm, in an interview with TechCrunch. The company is currently not taking a cut for the real estate on its app, he added.

But these startups’ expansion into new categories means that they now have to face off even more rivals, and spend more money to gain a foothold. In the social commerce category, for instance, Paytm is competing with Naspers-backed Meesho and a handful of new entrants; and heavily-backed OkCredit and KhataBook today lead the bookkeeping market.

BharatPe, which raised $75 million two months ago, is digitizing mom and pop stores and granting them working capital. And PineLabs, which has already become a unicorn, and MSwipe have flooded the market with their point-of-sale machines.

A vendor holds an Mswipe terminal, operated by M-Swipe Technologies Pvt Ltd., in an arranged photograph at a roadside stall in Bengaluru, India, on Saturday, Feb. 4, 2017. (Photographer: Dhiraj Singh/Bloomberg via Getty Images)

“They have no choice. Payment is the gateway to businesses such as e-commerce and lending that you can monetize. In Paytm’s case, their earlier bet was Paytm Mall,” said Jayanth Kolla, founder and chief analyst at research firm Convergence Catalyst.

But Paytm Mall has struggled to compete with giants Amazon India and Walmart’s Flipkart. Last year, Mall pivoted to offline-to-online and online-to-offline models, wherein orders placed by customers are serviced from local stores. The company also secured about $160 million from eBay last year.

An executive who previously worked at Paytm Mall said the venture has struggled to grow because its goal-post has constantly shifted over the years. It has recently started to focus on selling fastags, a system that allows vehicle owners to swiftly pay toll fees. At least two more executives at the firm are on their way out, a person familiar with the matter said.

Kolla said the current dynamics of India’s mobile payments market, where more than 100 firms are chasing the same set of audience, is reminiscent of the telecom market in the country from more than a decade ago.

“When there were just four to five players in the telecom market, the prospect of them becoming profitable was much higher. They were scaling like crazy. They grew with the lowest ARPU in the world (at about $2) and were still profitable.

“But the moment that number grew to more than a dozen overnight, and the new players started offering more affordable plans to subscribers, that’s when profitability started to become elusive,” he said.

To top that off, the arrival of Reliance Jio, a telecom operator run by India’s richest man, in 2016 in the country with the cheapest tariff plans in the world, upended the market once again, forcing several players to leave the market, or declare bankruptcies, or consolidate.

India’s mobile payments market is now heading to a similar path, said Kolla.

If there were not enough players fighting for a slice of India’s mobile payments market that Credit Suisse estimate could reach $1 trillion by 2023, WhatsApp, the most popular app in the country with more that 400 million users, is set to roll out its mobile payments service in the country in a couple of months.

At the aforementioned press conference, Nilekani advised Sharma and other players to focus on financial services such as lending.

Unfortunately, the coronavirus outbreak that promoted New Delhi to order a three-week lockdown last month is likely going to impact the ability of millions of people to use such services.

“India has more than 100 million microfinance accounts, serviced in cash every week by gig-economy workers, who hawk vegetables on street corners or embroider saris sold in malls, among other things. Three out of four workers make a living by working casually for others or at their family firms and farms. Prolonged shutdowns will impair their ability to repay loans of 2.1 trillion rupees ($28.5 billion), putting the world’s largest microfinance industry at risk,” wrote Bloomberg columnist Andy Mukherjee.

Powered by WPeMatico

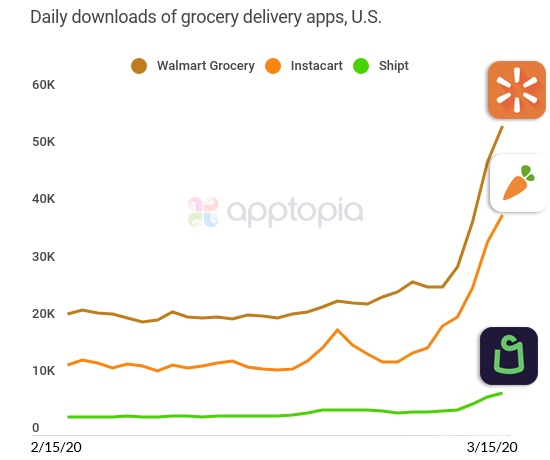

As the COVID-19 pandemic spreads across the U.S., grocery delivery apps have begun seeing record numbers of daily downloads, according to new data from app store intelligence firm Apptopia. On Sunday, online grocery apps, including Instacart, Walmart Grocery and Shipt, hit yet another new record for daily downloads for their respective apps, the firm says.

Comparing the average daily downloads in February to yesterday (Sunday, March 15), Instacart, Walmart Grocery and Shipt have seen their daily downloads surge by 218%, 160% and 124%, respectively.

Typically, these apps (except for Shipt) see tens of thousands to as many as 20,000+ downloads per day. But on Sunday, Instacart saw more than 38,500 downloads and Walmart Grocery saw nearly 54,000 downloads, the firm says. Shipt, though hitting record numbers, saw only 7,285 downloads on Sunday. To some extent, its lower figures could be due to Target’s move to integrate Shipt’s grocery delivery service, which it owns, into its main app.

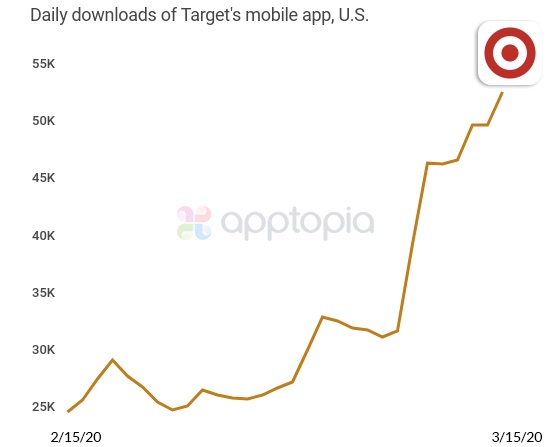

In fact, the Target app has also broken records for daily downloads, the report found. On Sunday, Target’s app saw more than 53,100 daily downloads; a month ago, it was seeing 25,000+.

Walmart very recently announced it would merge its grocery delivery service into its main app, as Target has done. But for now, consumers are still seeking and downloading its standalone grocery app at record levels.

These grocery delivery apps are in demand more than ever during this health crisis.

With government mandates to practice “social distancing,” U.S. consumers have been stocking up for long weeks to be spent at home. Stores were cleared of key supplies, like toilet paper, and several also saw long lines and crowds as panic-buying set in. Grocery delivery and pickup, meanwhile, presents an easier option — as well as one where you could limit your exposure to other people. With grocery pickup, consumers only have to interact with a single store employee from their curbside parking space. And with grocery delivery, most orders can simply be left on the doorstep with no person-to-person contact required.

Several grocery delivery services, including Instacart and others, promoted the fact they would add a “contactless” delivery option, which helps contribute to the huge sales boost. On Thursday, Instacart said its sales growth rates for the week was 10 times higher than the week before, and had increased by as much as 20 times in areas like California, New York, Washington and Oregon.

Apptopia’s report didn’t analyze the impact of the coronavirus outbreak on Amazon’s grocery delivery business, which includes Amazon Fresh and Whole Foods deliveries. This is more difficult to do because Amazon grocery orders aren’t placed inside a dedicated app, as with Instacart. However, Amazon confirmed a technical glitch on Sunday affected online orders through both its grocery delivery services, which the company attributed to the increase in online shopping.

“As COVID-19 has spread, we’ve seen a significant increase in people shopping online for groceries,” an Amazon spokeswoman explained, in a statement shared with Bloomberg. “This resulted in a systems impact affecting our ability to deliver Amazon Fresh and Whole Foods Market orders [on Sunday night]. We’re contacting customers, issuing concessions, and are working around the clock to quickly to resolve the issue,” they added.

Amazon Prime is also expected to experience delays and shortages as consumers stock up on non-grocery household items, the company says.

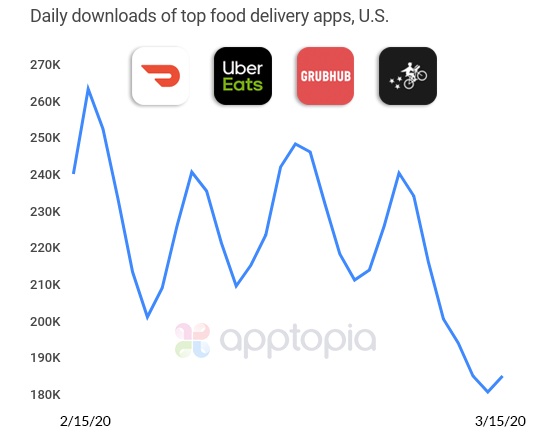

But even as grocery delivery booms, the market for food delivery apps has not seen the same results.

Despite promises for contactless delivery from several providers, including Uber Eats, food delivery apps are not experiencing a similar surge in daily downloads. According to Apptopia, the food delivery market earlier in March was starting to cool off. It later began to pick up but then cooled off again as consumers realized the expense of ordering food compared with home cooking, and because some consumers view restaurant delivery as not being as safe as cooking at home.

Powered by WPeMatico

Simsim, a social commerce startup in India, said on Friday it has raised $16 million in seven months of its existence as it attempts to replicate the offline retail experience in the digital world with help from influencers.

The Gurgaon-based startup said it raised $16 million across seed, Series A and Series B financing rounds from Accel Partners, Shunwei Capital and Good Capital. (The most recent round, Series B, was of $8 million in size.)

“Despite e-commerce players bandying out major discounts, most of the sales in India are still happening in brick-and-mortar stores. There is a simple reason for that: Trust,” explained Amit Bagaria, co-founder of Simsim, in an interview with TechCrunch.

The vast majority of Indians are still not comfortable with reading descriptions — and that too in English, he said.

Simsim is taking a different approach to tackle this opportunity. On its app, users watch short-videos produced in local languages by influencers who apply beauty products or try out dresses and explain the ins-and-outs of the products. Below the video, the items appear as they are being discussed and users can tap on them to proceed with the purchase.

“Videos help in educating users about the category. So many of them may not have used face masks, for instance. But it becomes easier when the community influencer is able to show them how to apply it,” said Rohan Malhotra, managing partner at Good Capital, in an interview with TechCrunch.

Influencers typically sell a range of items and users can follow them to browse through the past catalog and stay on top of future sales, said Bagaria, who previously worked at the e-commerce venture of financial services firm Paytm .

“This interactiveness is enabling Simsim to mimic the offline stores experience,” said Malhotra, who is one of the earliest investors in Meesho, also a social commerce startup that last year received backing from Facebook and Prosus Ventures.

“The beauty to me of social commerce is that you’re not changing consumer behavior. People are used to consuming on WhatsApp — and it’s working for Meesho. Over here, you are getting the touch and feel experience and are able to mentally picture the items much clearer,” he said.

Simsim handles the inventories, which it sources from manufacturers and brands, and it works with a number of logistics players to deliver the products.

“Several Indian cities and towns are some of the biggest production hubs of various high-quality items. But these people have not been able to efficiently sell online or grow their network in the offline world. On Simsim, they are able to work with influencers and market their products,” said Bagaria.

The platform today works with more than 1,200 influencers, who get a commission for each item they sell, said Bagaria, who plans to grow this figure to 100,000 in the coming years.

Even as Simsim, which has been open to users for six months, is still in its nascent stage, it is beginning to show some growth. It has amassed over a million users, most of whom live in small cities and towns, and it is selling thousands of items each day, said Bagaria.

He said the platform, which currently supports Hindi, Tamil, Bengali and English, will add more than a dozen additional languages by the end of the year. In about a month, Simsim also plans to start showing live videos, where influencers will be able to answer queries from users.

A handful of startups have emerged in India in recent years that are attempting to rethink the e-commerce market in the nation. Amazon and Walmart, both of which have poured billions of dollars in India, have taken a notice too. Both of them have added support for Hindi in the last two years and have made several more tweaks to their platforms to expand their reach.

Powered by WPeMatico

Alpha Foods, the vegetarian prepared food manufacturer, has raised $28 million in financing for its portfolio of vegetarian burritos, tamales, nuggets, pizzas, burgers, patties and sausages.

The Glendale, Calif.-based company was launched by Loren Wallis, the founder of the dairy substitute, Good Karma Foods, and Cole Orobetz, a former director with the agricultural debt lending firm Avrio Capital.

First launched in 2015, Alpha Foods previously raised $12 million in financing from investment firms like New Crop Capital and AccelFoods, whose other brands include Kite Hill, Good Catch, BRAMi and Evoke Healthy Foods.

As more Americans move to supplement their diets with plant-based products, companies like Alpha Foods have found willing investors for new food brands. The company’s new round was led by AccelFoods, with existing investors, including New Crop Capital, Green Monday Ventures and Blue Horizon, also participating.

Companies like Alpha compete with huge consumer packaged goods companies like Kellogg’s (through its Morningstar Farms line of vegetarian products) and Nestlé (through Sweet Earth Foods).

While the Morningstar Farms brand might seem a bit stale, the market has been reinvigorated through the marketing muscle and venture dollars supplied by companies like Beyond Meat and Impossible Foods, whose products have captured contracts from some of the world’s biggest fast food chains — including McDonald’s, KFC and Burger King.

Alpha Foods said it will use the latest money to launch new products, make new hires and expand its distribution channels nationally and internationally.

The company is already sold in well over 9,000 stores at chains including Wegmans, Walmart, Kroger and Publix.

“As more and more people actively seek out plant-based options, whether for their health or the environment, we are looking to expand our innovations within the category and bring easy to prepare products to a wider audience,” said Cole Orobetz, co-founder and president of Alpha Foods, in a statement.

The sale of pre-prepared plant-based meals reached $387 million in 2019, up 6% over the past year, according to data from the Good Food Institute.

“We are in the early days of plant-based consumption. As a portable, functional food business geared towards the newly emergent flexitarian consumer, the Alpha platform meets all of its customers’ snack and mealtime needs,” said AccelFoods Managing Partner Jordan Gaspar. “We couldn’t be prouder to lead this strong nexus of collaborative investors, who had the opportunity to organically build trust this past year allowing for an incredibly successful outcome in this financing.”

Powered by WPeMatico

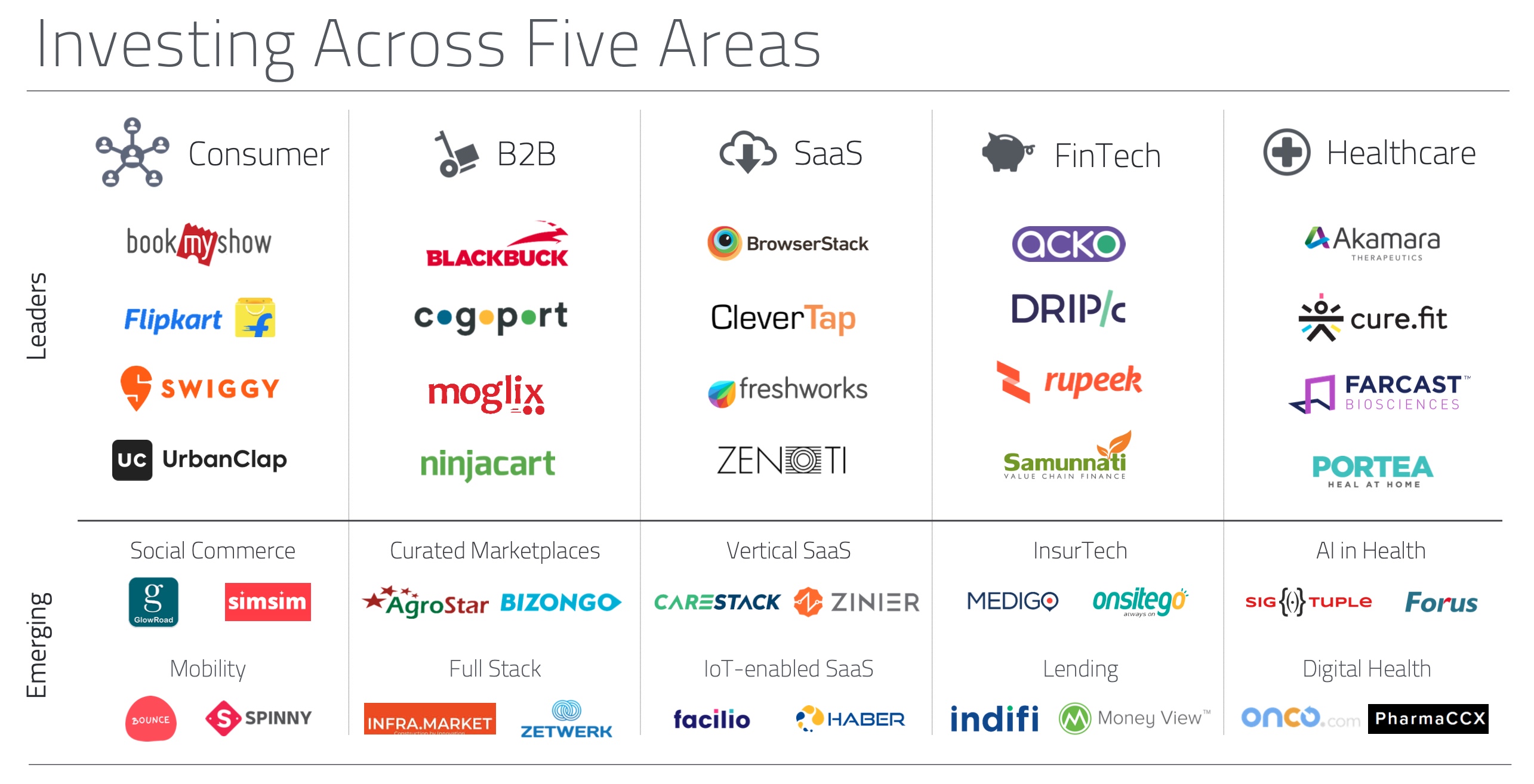

Accel, one of the world’s most influential venture capitalist firms, is getting more bullish on India.

The Silicon Valley-headquartered firm, which largely focuses on early-stage investments, said today it has closed $550 million for its sixth venture fund in India.

This is a significant amount of capital for Accel’s efforts in the country, where it began investing 15 years ago and has infused roughly $1 billion through all its previous funds.

Anand Daniel, a partner for Accel in India, told TechCrunch in an interview that the VC fund will continue to focus on identifying and investing in seed and early-stage startups.

But the fund realized it needed more money so it could actively participate in follow-on rounds (later-stage financing rounds) of its portfolio startups. The announcement today follows Accel’s similar recent push in Europe and Israel, where it closed a $575 million fund.

“We also selectively do growth investments for companies that are scaling well, such as Swiggy, UrbanClap, BlackStone and Bounce. We have continued to back them through Series B and Series C rounds,” he said.

At the risk of being accused of bias, I’ll say this: Accel India is a rare Indian fund that had credible exits and more promising exits in the pipeline. They’re also some of the nicest people to work with. https://t.co/aZGjDgSQKe

— JPK (@therealjpk) December 2, 2019

Like in many other markets, Accel’s track record in India is quite impressive. It participated in the seed financing round of e-commerce firm Flipkart, which was then valued at $4 million post-money. Walmart bought a majority stake in Flipkart last year for $16 billion. (This helped Accel net more than $1 billion in return from Flipkart.)

Accel, which has nine partners and more than 50 members in total in India, also invested in the seed round of SaaS giant Freshworks, which is now valued at more than $3 billion, food delivery startup Swiggy, also valued at north of $3 billion, and recently turned unicorn BlackBuck. Accel has been the first institutional investor for 85% of startups in its portfolio.

The VC firm says 44 of the 100-odd startups in its India portfolio today are valued at over $100 million each. In total, including Flipkart’s $21 billion market value, Accel’s portfolio firms have created $44 billion in market value.

Some of the investments Accel has made in India

“When we started our first fund in India in 2005, the world was a very different place. Just 1 in 50 Indians had access to the internet and mobile phone ownership was nascent. Yet we firmly believed that India was on the cusp of a big change,” the firm said in a statement.

“Today, the opportunity ahead is significantly bigger than when we started in 2005: India can now digitally identify 1.3 billion people, has 600 million internet users and 150 million online transacting customers with a national payments platform that processes $20 billion a month.”

Daniel said moving forward Accel will continue to focus on consumer, business-to-business, fintech, healthcare and global SaaS categories. “We have nine partners with their own areas of interest. They invest from their own conviction and finance seed rounds. If we see a particular sector evolving, then we do a deeper thesis work,” he said.

“We then develop deeper confidence for the space. For example, back in the day we invested in mobility startup TaxiForSure, long before Uber had arrived in India. That helped us understand mobility well. We have used those learnings to invest in several more mobility startups.”

Accel’s growing interest in India comes at a time when several other giants, including SoftBank and Prosus Ventures, have also become more active in the nation — though they tend to finance later-stage rounds.

For Indian startups that are already having their best year, this can only be good news.

Powered by WPeMatico

E-commerce now accounts for 14% of all retail sales, and its growth has led to a rise in the fortunes of startups that build tools to enable businesses to sell online. In the latest development, a company called VTEX — which originally got its start in Latin America helping companies like Walmart expand their business to new markets with an end-to-end e-commerce service covering things like order and inventory management, front-end customer experience and customer service — has raised $140 million in funding, money it will be using to continue taking its business deeper into more international markets.

The investment is being led by SoftBank, specifically via its Latin American fund, with participation also from Gávea Investimentos and Constellation Asset Management. Previous investors include Riverwood and Naspers; Riverwood continues to be a backer, the company said.

Mariano Gomide, the CEO who co-founded VTEX with Geraldo Thomaz, said the valuation is not being disclosed, but he confirmed that the founders and founding team continue to hold more than 50% of the company. In addition to Walmart, VTEX customers include Levi’s, Sony, L’Oréal and Motorola . Annually, it processes some $2.4 billion in gross merchandise value across some 2,500 stores, growing 43% per year in the last five years.

VTEX is in that category of tech businesses that has been around for some time — it was founded in 1999 — but has largely been able to operate and grow off its own balance sheet. Before now, it had raised less than $13 million, according to PitchBook data.

This is one of the big rounds to come out of the relatively new SoftBank Innovation Fund, an effort dedicated to investing in tech companies focused on Latin America. The fund was announced earlier this year at $2 billion and has since expanded to $5 billion. Other Latin American companies that SoftBank has backed include online delivery business Rappi, lending platform Creditas and property tech startup QuintoAndar.

The common theme among many SoftBank investments is a focus on e-commerce in its many forms (whether that’s transactions for loans or to get a pizza delivered), and VTEX is positioned as a platform player that enables a lot of that to happen in the wider marketplace, providing not just the tools to build a front end, but to manage the inventory, ordering and customer relations at the back end.

“VTEX has three attributes that we believe will fuel the company’s success: a strong team culture, a best-in-class product and entrepreneurs with profitability mindset,” said Paulo Passoni, managing investment partner at SoftBank’s Latin America fund, in a statement. “Brands and retailers want reliability and the ability to test their own innovations. VTEX offers both, filling a gap in the market. With VTEX, companies get access to a proven, cloud-native platform with the flexibility to test add-ons in the same data layer.”

Although VTEX has been expanding into markets like the U.S. (where it acquired UniteU earlier this year), the company still makes some 80% of its revenues annually in Latin America, Gomide said in an interview.

There, it has been a key partner to retailers and brands interested in expanding into the region, providing integrations to localise storefronts, a platform to help brands manage customer and marketplace relations, and analytics, competing against the likes of SAP, Oracle, Adobe and Salesforce (but not, he said in answer to my question, Commercetools, which builds Shopify -style API tools for mid and large-sized enterprises and itself raised $145 million last month).

E-commerce, as we’ve pointed out, is a business of economies of scale. Case in point: While VTEX processes some $2.5 billion in transactions annually, it makes a relatively small return on that — $69 million, to be exact. This, plus the benefit of analytics on a wider set of big data (another economy of scale play), are two of the big reasons VTEX is now doubling down on growth in newer markets like Europe and North America. The company now has 122 integrations with localised payment methods.

“At the end of the day, e-commerce software is a combination of knowledge. If you don’t have access to thousands of global cases you can’t imbue the software with knowledge,” Gomide said. “Companies that have been focused on one specific region are now realising that trade is a global thing. China has proven that, so a lot of companies are now coming to us because their existing providers of e-commerce tools can’t ‘do international.’ ” There are very few companies that can serve that global approach and that is why we are betting on being a global commerce platform, not just one focused on Latin America.”

Powered by WPeMatico

Walmart has dropped a lawsuit that accused Tesla of breach of contract and gross negligence after rooftop solar panel systems on seven of the retailer’s stores allegedly caught fire.

A settlement has been reached and stipulation of dismissal has been filed with the court, a Walmart spokesperson said in an email. It is unclear what the settlement entails. TechCrunch has requested more information and will update the article if new details emerge.

The two companies issued a joint release Tuesday announcing that the issues raised by Walmart have been resolved.

“Safety is a top priority for each company and with the concerns being addressed, we both look forward to a safe re-energization of our sustainable energy systems,” the emailed statement reads.

The resolution comes just three months after Walmart filed the lawsuit in New York state court. The lawsuit was aimed at Tesla Energy Operations, a division within the clean energy and electric vehicle automaker that was formerly known as SolarCity.

Days after the lawsuit was filed, the two companies announced efforts were underway to try to reach an agreement that would keep the solar installations in place and put them back in service, according to a joint statement issued at the time.

While the announcement signaled progress, the specter of a lawsuit still loomed. Until now.

Walmart said it sued Tesla after years of gross negligence and failure to live up to industry standards by Tesla, according to court documents. Walmart asked Tesla to remove solar panels from all 240 locations where they have been installed, as well as pay for damages related to fires that the retailer alleges stem from the panels. The lawsuit points to several fires on the retailer’s rooftops that allegedly stem from Tesla solar panels.

Powered by WPeMatico

Walmart announced today an expansion of its existing relationship with financial services provider Green Dot, which will continue to serve as the issuing bank and program manager for the Walmart MoneyCard program for another seven years. The two companies also agreed to partner on the creation of a new accelerator that focuses on the intersection of retail and consumer financial services.

The accelerator, called Tailfin Labs, will help startups develop solutions that integrate omni-channel shopping and financial tech, which can be aimed either at consumers or businesses. These may involve products built on top of Green Dot’s “Banking-as-a-Service” (BaaS) platform.

“Green Dot is extremely proud and honored to both extend our MoneyCard partnership for many years and to additionally enter into an entirely new equity partnership with Walmart in the creation of a fintech accelerator,” said Steve Streit, founder and CEO, Green Dot, in a statement. “We believe the combination of Walmart’s unmatched retail ecosystem with Green Dot’s innovative and highly flexible BaaS platform, which enables the world’s largest technology and consumer brands to address their consumers with bespoke financial products and services, has the opportunity to create and bring to market many new and exciting innovations over the years to come.”

Walmart partnered with Green Dot in 2006 to create the Walmart MoneyCard, which offers FDIC-insured accounts and cash-back rewards on Walmart purchases, alongside other features, like early direct deposit, online bill pay, prize savings entries and more — as well as the usual set of features you’d have in a personal checking account, but without the fees. It’s now the largest retailer exclusive prepaid account program in the U.S.

Walmart partnered with Green Dot in 2006 to create the Walmart MoneyCard, which offers FDIC-insured accounts and cash-back rewards on Walmart purchases, alongside other features, like early direct deposit, online bill pay, prize savings entries and more — as well as the usual set of features you’d have in a personal checking account, but without the fees. It’s now the largest retailer exclusive prepaid account program in the U.S.

In many ways, it was also a precursor to the sort of mobile banking startups seen today, which directly target consumers with similar products.

This is a busy space these days, as more companies go after the growing market of millennials (and even their younger Gen Z counterparts) who don’t want a traditional bank. Instead, they want banking services in a modern, easy-to-use mobile interface, where innovative features help them to better save and manage their money.

Just last week, for example, mobile banking app Current snagged $20 million more in funding for its service, now used by half a million users. Others in the space include Step, Cleo, N26, Chime, Simple and Stash, to name a few.

The new accelerator is seemingly poised to capitalize on this trend, while also giving Walmart and Green Dot a new foothold in the market.

“Over the years, Walmart has brought to market many innovative industry-defining financial services offerings to serve our customers – including several introduced through the Walmart MoneyCard program managed by Green Dot,” noted Daniel Eckert, senior vice president, Walmart Services and Digital Acceleration, in an announcement. “With this expanded relationship, and by leveraging Walmart’s footprint and existing offerings with Green Dot’s cutting-edge capabilities, we’ll be uniquely positioned to offer an unmatched set of customer experiences that sit at the nexus of omni-channel retail and tech-enabled financial services,” he said.

The new agreement between Green Dot and Walmart begins January 1, 2020 and will replace the agreement that would have otherwise expired in May 2020.

Powered by WPeMatico

Uber will acquire Cornershop, a grocery delivery startup that began life serving the Latin American market and recently shifted to offer service in Toronto, its first North American city. Uber announced on Friday that it expects its acquisition of a majority ownership stake in Cornershop in early 2020, once it receives all the necessary regulatory sign-offs.

Cornershop was founded in 2015 by Oskar Hjertonsson, Daniel Undurraga and Juan Pablo Cuevas; it’s headquartered in Chile. The company will continue to operate under that leadership in its current form for now, Uber says, and will report to a board that counts Uber leadership in the majority of its overall makeup.

Over the course of four rounds of funding, Cornershop raised $31.7 million from investors including Accel, Jackson Square Ventures and others. The on-demand grocery company was supposed to be acquired by Walmart in a deal valued at $225 million announced in September, but that deal ultimately fell apart in June when Mexican anti-trust regulators blocked it from going through.

Meanwhile, Walmart has continued to work with Cornershop, expanding its service offerings in Toronto with the startup as recently as yesterday. Uber has previously experimented with grocery delivery, including in partnership with Walmart, and Uber CEO Dara Khosrowshahi has said that grocery delivery is a natural place for the company to expand its business, given the success of Uber Eats. It’ll face competition from entrenched players, including Instacart and Postmates, but Uber Eats also faced competition from much more established players at its genesis, too.

The deal is still subject to regulatory approval, as mentioned, and that’s exactly where the planned Walmart acquisition stumbled, so it’s worth keeping a close eye on this one. Still, Uber’s not making any secret of its intentions with the grocery category, so that looks likely to take shape one way or another.

Powered by WPeMatico

Hello and welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week, I wrote about Stripe’s grand plans. Before that, I noted Peloton’s secret weapons.

Remember, you can send me tips, suggestions and feedback to kate.clark@techcrunch.com or on Twitter @KateClarkTweets. If you don’t subscribe to Startups Weekly yet, you can do that here.

The best companies are built by people who have personally experienced the problem they’re attempting to solve. Lauren Jonas, the founder and chief executive officer of Part & Parcel, is intimately familiar with the struggles faced by the women she’s building for.

San Francisco-based Part & Parcel is a plus-sized clothing and shoe startup providing dimensional sizing to women across the U.S. The company operates a bit differently than your standard direct-to-consumer business by seeking to include the women who wear and evangelize the Part & Parcel designs by giving them a cut of their sales.

Here’s how it works: Ambassadors sign up to receive signature styles from Part & Parcel, which they then share and sell to women in their network. Ultimately, the sellers are eligible to receive up to 30% of the profit per sale. The out-of-the-box model, which might remind you somewhat of Mary Kay or Tupperware’s business strategy, is meant to encourage a sense of community and usher in a new era in which plus-sized women can facilitate other plus-sized women’s access to great clothes.

“I bought a brown men’s polyester suit and wore it to an interview,” Jonas, an early employee at Poshmark and the long-time author of the popular blog, ‘The Pear Shape,’ tells TechCrunch. “I was that kid wearing a men’s suit.”

Clothing tailored to plus-sized women has long been missing from the retail market. Increasingly, however, new brands are building thriving businesses by catering precisely to the historically forgotten demographic. Dia&Co., for example, raised another $70 million in venture capital funding last fall from Sequoia and USV. And Walmart recently acquired another brand in the space, ELOQUII, for an undisclosed amount. Part & Parcel, for its part, has raised $4 million in seed funding in a round led by Lightspeed Venture Partners’ Jeremy Liew.

The startup launched earlier this year in Anchorage, “a clothing desert,” and has since grown its network to include women in several other underserved markets. Given her own history struggling to find a fitted woman’s suit, Jonas launched her line with structured pieces, including suits and blouses — though the startup’s biggest success yet, she says, has been its boots, which come in three different calf width options.

“Seventy percent of women in this country are plus-sized,” Jonas said. “I’m bringing plus out of the dark corner of the department store.”

Image: Bryce Durbin / TechCrunch

TechCrunch’s Megan Rose Dickey published a highly anticipated deep dive on the state of sex tech this week. The piece provides new data on funding in sex tech and wellness companies, analysis on sex tech startup’s battle for public advertising and responses from industry leaders on how we can destigmatize sex with technology. Here’s a short passage from the story:

Cindy Gallop sees a market opportunity in every type of business obstacle she encounters. That’s why All The Sky will also seek to invest in startups that tackle the infrastructural tools needed to fuel sextech, like payments, hosting providers and e-commerce sites.

“I want to fund the sextech ecosystem to maintain and sustain a portfolio for All the Skies, to create a bloody huge sextech ecosystem and three, to monopolistically build out the ecosystem to be a multi-trillion-dollar market,” Gallop says.

I swung by Contrary Capital‘s Demo Day this week, in which a number of startups gave a 4- to 5-minute pitch. Next on my list is Alchemist‘s Demo Day in Menlo Park. The accelerator welcomes enterprise startups for a six-month program focused on early customer adoption, company development and mentorship.

Also on my radar is Females To The Front. The event began this week in Palm Springs and if I were based in SoCal, I would have swung by. Led by Amy Margolis, the event is said to be the largest gathering of female cannabis founders and funders to date. Here’s how the group describes the event: “Females to the Front Retreat will mix immersive and hands-on workshops, pitch training, investment deck preparation and business skill set education with investor meetings and plenty of shared meals, pool time, yoga, connections, rest and rejuvenation. Every workshop is built to directly engage attendees instead of powerpoint and panels. Be prepared to return home inspired, engaged and with so many more tools in your toolbox.”

For the record, I don’t advertise events in my newsletter just wanted to give props to this one because it’s a great development for the cannabis tech ecosystem.

We are just weeks away from our flagship conference, TechCrunch Disrupt San Francisco. We have dozens of amazing speakers lined up. In addition to taking in the great line-up of speakers, ticket holders can roam around Startup Alley to catch the more than 1,000 companies showcasing their products and technologies. And, of course, you’ll get the opportunity to watch the Startup Battlefield competition live. Past competitors include Dropbox, Cloudflare and Mint… You never know which future unicorn will compete next.

You can take a look at the full agenda here. And if you still need convincing, here’s five reasons to attend this year’s conference from our COO himself.

This week, the lovely Alex Wilhelm, editor-in-chief of Crunchbase News, and I gathered to discuss a number of topics including WeWork’s IPO and Uber’s attempts to bypass a new law meant to protect gig workers. Listen here.

Powered by WPeMatico