Venmo

Auto Added by WPeMatico

Auto Added by WPeMatico

Welcome back to this week’s transcribed edition of Equity.

This week, TechCrunch’s Danny Crichton filled in for co-host Alex Wilhelm – who was out in preparation for his wedding this weekend – joining Kate to cover the big news of the week.

Kate and Danny dive straight into Slack’s IPO and the implications of its direct listing strategy, before shifting gears to discuss the launch of Facebook’s new ‘Libra’ cryptocurrency and the VCs backing the initiative.

The duo then took a look at Lime’s latest fundraising efforts and the potential headwinds facing scooter companies with an appetite for capital. Lastly, Kate and Danny talk about underappreciated tensions for founders, including getting pushed out of their own companies and handling their own salaries.

Crichton: Talking about founders and compensation, our correspondent, Ron Miller, talked to a bunch of VCs to ask how are founders paying themselves today? Obviously, the cost of living in the Bay Area, in New York and other startup hubs has increased dramatically. So VCs have had to become acutely aware of their founders’ financial means.

One of the things that really came out of this survey though, from my perspective, was just how high the numbers are. We surveyed small number. We put it out in the interviews. It came out to post-Series A people are starting to get paid around 200K. But the numbers, even a couple of years ago, I seem to recall was like $120 was the magic number around the Series A, $90K if you had a serious seed fund and like $60 to $80 if you are just getting started.

But the numbers that we saw out of this were significantly higher. I think that shows a lot about how the cost of living has just continued to creep up in San Francisco and in New York.

Clark: Yeah. I think the point is made in the story. If you live in San Francisco and you’re paying a mortgage and you have kids, of course, you need to make six figures really to get by, which is just an unfortunate reality. I can’t say I was surprised by how those salaries looked. Seeing $125K for a founder, if anything, I thought was maybe a little low.

But it reminded me of, nearly a year ago at this point, when I wrote something on how much VCs are paid. I had written it based off data that was provided to me from a consulting firm. People were just up in arms at what I had written because, and I understand looking back, I think it grouped VCs together as VCs who work at really big funds who are getting the 2% carry out of a multi-billion dollar fund and who are paid a lot more.

And there are of course VCs who run seed funds or any kind of fund. There are many different sizes of VC funds. Some VCs actually don’t have a salary at all and are up against the same challenges, if not even more difficult challenges, of a startup founder.

Want more Extra Crunch? Need to read this entire transcript? Then become a member. You can learn more and try it for free.

Kate Clark: Hello, and welcome back to Equity, TechCrunch’s venture capital-focused podcast. My co-host, Alex, is getting married this weekend so he’s not with us today, unfortunately. But we’ve got TechCrunch editor, Danny Crichton on the line. Danny, how are you?

Powered by WPeMatico

William Hockey, co-founder, chief technology officer and president of the fast-growing fintech business Plaid, will step down next week, TechCrunch has learned.

The former Bain associate (pictured above left) co-founded the startup in 2012 alongside chief executive officer Zach Perret. Today, the San Francisco-based company employs 300 with additional offices in Salt Lake City and New York.

Plaid has confirmed the news, stating that Hockey will remain on the company’s board of directors.

“This conclusion was neither a rash nor a recent decision,” Hockey writes in a blog post shared with TechCrunch. “Over the past couple of years, I have known that there would come a point at which I would choose to move to a purely strategic and advisorial role.”

Most companies should be constantly running running at least one exec search. Post-product/market fit, the limiting factor to scale generally derives from some version of not having enough great leaders.

— Zachary Perret (@zachperret) June 18, 2019

Plaid builds infrastructure that allows consumers to interact with their bank account on the web, powering a number of third-party applications, like Venmo, Robinhood, Coinbase, Acorns and LendingClub. It rose to prominence recently, closing a $250 million Series C investment at a $2.65 billion valuation late last year. The deal was led by famed venture capitalist and author of the Internet Trends report Mary Meeker, who’s joined the startup’s board of directors.

In total, Plaid has secured $310 million in venture capital funding from Andreessen Horowitz, Index Ventures, Norwest Venture Partners, Coatue Management, Goldman Sachs, NEA, Spark Capital and others.

Plaid has integrated with 15,000 banks in the U.S. and Canada and says 25% of people living in those countries with bank accounts have linked with Plaid through at least one of the hundreds of apps that leverage Plaid’s application program interfaces (APIs) — an increase from 13% last year. Last month, the company launched its fintech platform in the U.K.

“As we’ve done in the U.S., Plaid will become the foundation for that growth by providing access to a financial network that allows developers to deliver the experience users expect from their financial apps,” the company wrote in a blog post.

TechCrunch participated in a panel discussion with Hockey and Brex CEO Henrique Dubugras last month, in which Hockey gave no indication of impending plans to leave the business. In fact, taking off just as Plaid amps up its global expansion efforts and accelerates growth is strange timing for a founder to depart.

Oftentimes, when a startup co-founder steps down from the C-suite, it’s to make room for a more experienced executive to lead the company through periods of fast growth. Recently, for example, Lime announced its co-founder Toby Sun would transition out of the CEO role to focus on company culture and R&D. Brad Bao, a Lime co-founder and longtime Tencent executive, assumed chief responsibilities.

Other times, it comes amid turmoil. Mike Cagney’s departure from SoFi, of course, is an example of this. One month after reports of a sexual harassment and wrongful termination lawsuit against the online lending business surfaced, SoFi announced Cagney would step down.

In Hockey’s case, the move was planned and calculated, he said. Plaid chief operating officer Eric Sager, who joined earlier this year, Perret and other executives will take over engineering and product reports, among Hockey’s other responsibilities.

“In tech, it has historically been taboo to talk about founders or executives transitioning to different roles inside companies,” Hockey writes. “Leadership transitions need to become a bedrock of any company that desires to endure across decades.”

Powered by WPeMatico

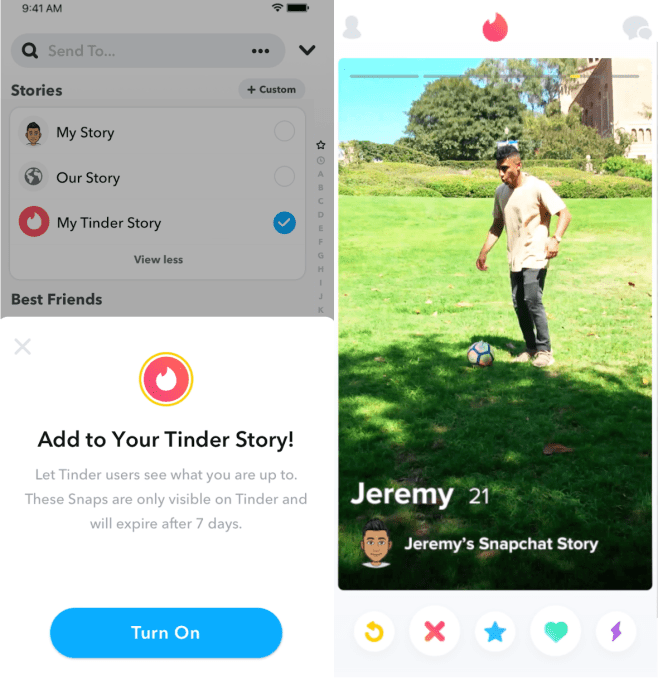

Snapchat has found an answer to the revenue problem stemming from its halted growth: it will show its ads in other apps with the launch of Snapchat Ad Kit and the Snapchat Audience Network. And rather than watching as other apps spin up their own knock-off versions of its camera and Stories, it will let apps like Tinder and Houseparty host Stories inside their own products that users can share to from the Snapchat camera with Stories Kit. They’ll both be launching later this year, and developers interested in monetization and engagement help can apply for access.

Snapchat debuted the big new additions to its Snap Kit at its first-ever press event in Los Angeles, the Snap Partner Summit, where it also announced a new augmented reality utility platform called Scan, and its new multiplayer games platform. More than 200 apps have already integrated the privacy-safe Snap Kit that lets users log in to other apps with Snapchat, bring their Bitmoji, view Our Stories content and share stickers back to Snapchat.

But later this year, developers will be able to earn money off of Snap Kit with Ad Kit. Developers will integrate Snapchat’s SDK, and then Snap’s advertisers will be able to extend their ad buys to reach both Snapchat users and non-users in other apps. Snapchat will split the ad revenue with developers, but refused to hint at what the divide will be, as it’s still gauging developer interest. The move is straight out of Facebook’s playbook, essentially copying the functionality and name of Facebook’s Audience Network.

There are still big questions about exactly how Snapchat will reach and track ad views of non-users, and how it will be able to provide brands with the analytics they need while maintaining user privacy. But simply by making Snapchat’s somewhat proprietary vertical video ad units reusable elsewhere, it could prove it has a scale to be worth advertisers’ time. The lack of scale has often scared buyers away from Snapchat. But Snap CEO Evan Spiegel says that “In the United States, Snapchat now reaches nearly 75 percent of all 13 to 34-year-olds, and we reach 90 percent of 13 to 24-year-olds. In fact, we reach more 13 to 24-year-olds than Facebook or Instagram in the United States, the U.K., France, Canada and Australia.”

To keep those users engaged even outside of Snapchat, it’s adding App Stories through Story Kit. Snapchat users will see an option to share to integrated apps after they create a photo or video. Those Stories will then appear in custom places in other apps. You’ll see Snaps injected alongside people’s photos when you’re browsing potential matches in Tinder. You can see what friends on group chat social network Houseparty are doing when they are not on the app. And you can see video recommendations from explorers on AdventureAide.

For now, Snapchat won’t run ads between Stories in other apps, but that’s always a possibility. We’ll have to see how long it takes Instagram and Facebook to try to copy Stories Kit and distribute their own versions to other apps.

Snap also has some other fun new integrations and big-name partnerships. Bitmoji Kit will bring your personalized avatar off your phone and onto Fitbit’s smart watches and Venmo transactions. Netflix will let you share preview images (but not trailers) from its shows to your Snapchat Story. A new publisher-sharing button for the web will let you share articles from The Washington Post and others to your Story.

By colonizing other apps with its experience, Snapchat decreases the need for them to copy it. Instead they get the original, and a lot less development work. And the platform makes your Snapchat account more valuable around the web. These integrations might not grow Snapchat too much, but it could help it keep its existing users happy and squeeze more cash out of them.

Powered by WPeMatico

I co-run an agency that teaches a hundred startups per year how to do growth marketing. This gives me a unique vantage point: I know which types of startups most often reach profitability.

That’s an important metric, because startups that don’t reach this milestone typically fail to raise additional funding — then die.

Here’s what we’ll learn:

Our sampling of startups isn’t as biased as startup valuation leaderboards, because we also see those that failed. That’s the key.

You can use our experience to de-risk your startup. That’s what this post explores: How to change your product roadmap to pursue a path more likely to reach profitability.

Here’s the data my agency is referencing for this post:

When we try to control for founder skill and funds raised, the types of startups that first reach profitability do so in this order:

On average, an e-commerce company is more likely to first reach profitability than an SMB SaaS company.

Before I explain why, let me explain how we’re differentiating startups: I use the word “type” instead of “business model” or “markets” because I’ve learned that business model and market are often not the best predictors of success. Instead, it’s your approach to customer acquisition. That’s what typically determines the likelihood of profitability.

Powered by WPeMatico

The only sure things in this life, according to Ben Franklin, are death and taxes. And a new startup called Visor has just raised $9 million in financing to make one of them as painless as possible.

Unlike Nectome, Visor won’t kill anyone, but it may ring the death knell for the high-end tax advisors that most Americans can’t even access to get help filing and paying their taxes. It’s like having a personalized accountant for the cost of a high-end do-it-yourself tax-prep service.

The $9 million Visor raised came from the venture capital firm Defy, with participation from Unusual Ventures, SVB Capital and existing investors like Obvious Ventures, Fika Ventures and Boxgroup, which had put a previous $6.5 million into the company.

The idea for the company had been percolating for co-founder and chief executive Gernot Zacke since he settled in the U.S.

Growing up in Sweden, Zacke was exposed to a much different process for paying taxes. “The experience of filing taxes in Sweden is that you receive a message from the government that stated how much you made and how much you were withholding. That’s it,” said Zacke. “Taxes should be as easy as ordering a cab.”

That’s the service that Visor aims to provide.

“If you think about the market there are two ways to get your taxes done. There’s the DIY space and then there are other online services but it requires the tax payer to fill out the forms and it leaves the tax payer with a little bit of anxiety,” said Zacke. “We’re delivering the CPA experience through the convenience of a web app and a mobile app.”

On average, Americans spend about 13 hours each year dealing with taxes, and the average American doesn’t have the benefits of a professional advisor who can help optimize the process. That’s what Visor wants to provide.

“You provide the same amount of information you provide to a CPA or TurboTax… we make sure that that information is filed securely on AWS and shared between the docs and the backend,” said Zacke.

The target customers for Zacke’s services are folks who have had a change to their tax situation — whether moving, buying a home or any other life event; or folks who have had a CPA and don’t want to pay the higher fees, he said.

Visor currently has an operations team of around 34 people split between San Francisco and Atlanta.

For Zacke, the pain point he’s solving with the Visor service is very real. A former employee of the European investment firm Atomico, Zacke bounced between the U.S. and Europe — eventually running U.S. investments for the firm before leaving to launch Visor.

Other co-founders and senior executives hail from the tax advisory world, and from employee benefits outsourcing services company Zenefits, along with former Venmo and Square developers.

“Taxpayers spend $20 billion a year to get their taxes prepared and are stuck between spending hours filling out DIY tax software and hiring an expensive CPA,” said Zacke, in a statement. “

Powered by WPeMatico

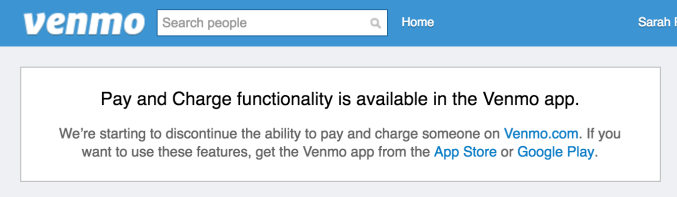

PayPal-owned, peer-to-peer payments app Venmo is ending web support for its service, the company announced in an email to users. The changes, which are beginning to roll out now, will see the Venmo .com website phasing out support for making payments and charging users. In time, users will see even less functionality on the website, the company says.

The message to users was quietly shared in the body of Venmo’s monthly transaction history email. It reads as follows:

NOTICE: Venmo has decided to phase out some of the functionality on the Venmo.com website over the coming months. We are beginning to discontinue the ability to pay and charge someone on the Venmo.com website, and over time, you may see less functionality on the website – this is just the start. We therefore have updated our user agreement to reflect that the use of Venmo on the Venmo.com website may be limited.

The decision represents a notable shift in product direction for Venmo. Though best known as a mobile payments app, the service has also been available online, similar to PayPal, for many years.

The Venmo website today allows users to sign in and view their various transaction feeds, including public transactions, those from friends, and personal transactions. You can also charge friends and submit payments from the website, send payment reminders, like and comment on transactions, add friends, edit your profile, and more.

Some users may already be impacted by the changes, and will now see a message alerting them to the fact that charging friends and making payments can only be done in the Venmo app from the App Store or Google Play.

It’s not entirely surprising to see Venmo drop web support. As a PayPal-owned property after its acquisition by Braintree which later brought it to PayPal, there’s always been a lot of overlap between Venmo and its parent company, in terms of peer-to-peer payments.

Venmo had grown in popularity for its simple, social network-inspired design and its less burdensome fee structure among a younger crowd. This made it an appealing way for PayPal to gain market share with a different demographic.

It’s also cheaper, which people like. PayPal doesn’t charge for money transfers from a bank account or PayPal balance, but does charge 2.9 percent plus a $0.30 fixed fee on payments from a credit or debit card in the U.S. Venmo, meanwhile, charges a fee of 3 percent for credit card payments, but makes debit card payments free. That’s appealing to millennials in particular, many of whom have ditched credit cards entirely, and are careful about their spending.

Plus, as a mobile-first application, Venmo was offering a more modern solution for mobile payments, at a time when PayPal’s app was looking a bit long in the tooth. (PayPal has since redesigned its mobile app experience to catch up.)

Another factor in Venmo’s decision could be that, more recently, it began facing competition from newcomer Zelle, the bank-backed mobile payments here in the U.S. which is forecast to outpace Venmo on users sometime this year, with 27.4 million users to Venmo’s 22.9 million. In light of that threat, Venmo may have wanted to consolidate its resources on its primary product – the mobile app.

Not everyone is happy about Venmo’s changes, of course. After all, even if the Venmo website wasn’t heavily used, it was used by some who will certainly miss it.

@venmo i only use the website to send/receive payments so in guess you’re cancelled!

— respectfully yours (@biking_away_) June 15, 2018

@venmo This makes me really #sad….”Venmo has decided to phase out some of the functionality on the https://t.co/Dw7W551BsL website over the coming months.” #CanWeGoBackToHowItWas

— V Lav (@Druzy920) June 14, 2018

@venmo Why are you breaking your website?

— Lozaning (@lozaning) June 14, 2018

@VenmoSupport @venmo Just got an email saying you’re phasing out website functions. What’s the justification? Pay and charge by web is incredibly useful.

— Woode (@Woode2380) June 14, 2018

Venmo email: “We are beginning to discontinue the ability to pay and charge someone on the https://t.co/iAFTbn3EY0 website, and over time, you may see less functionality on the website – this is just the start.”

Is this a threat?

— Noah Mittman (@noahmittman) June 14, 2018

Reached for comment, Venmo explained the decision to phase out the website functionality stems from how it sees its product being used.

A Venmo spokesperson told TechCrunch:

Venmo continuously evaluates our products and services to ensure we are delivering our users the best experience. We have decided to begin to discontinue the ability to pay and charge someone on the Venmo.com website. Most of our users pay and request money using the Venmo app, so we’re focusing our efforts there. Users can continue to use the mobile app for their pay and charge transactions and can still use the website for cashing out Venmo balances, settings and statements.

The company declined to clarify what other functionality may be removed from the website over time, but noted that using Venmo to pay authorized merchants is unaffected.

Powered by WPeMatico

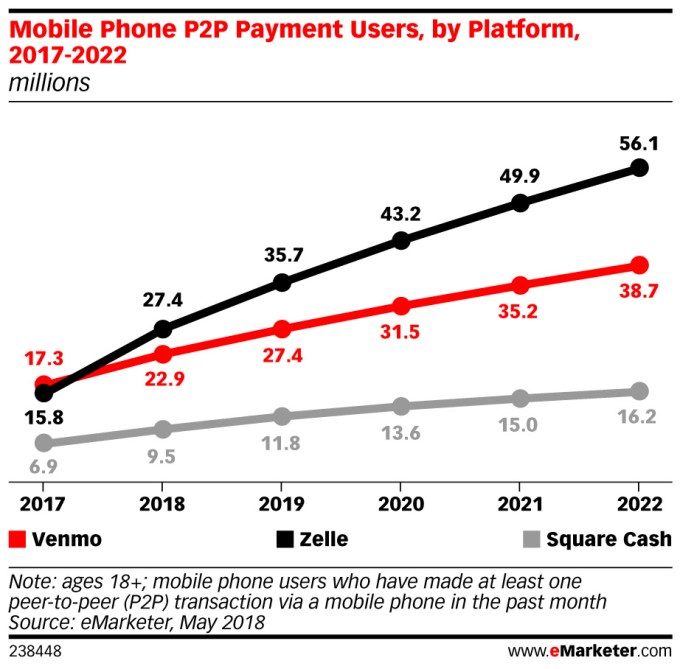

Despite some concerns over its adoption by scammers, new payment service Zelle is shaping up to overtake rival Venmo this year, according to a new forecast from eMarketer. The firm expects Zelle to grow more than 73 percent in 2018, to reach 27.4 million users in the U.S., ahead of Venmo’s 22.9 million. Square Cash will trail with 9.5 million users.

This growth isn’t necessarily chalked up to user preference, but rather, ubiquity.

Zelle is backed by a network of over 30 U.S. banks, as their means of winning over users from other payment apps including Venmo, PayPal, and Square Cash. The banks had wanted to develop their own alternative these apps for several years, but only recently had those efforts gained momentum. The Zelle website now claims participation from over 100 financial institutions, as well as processor partners CO-OP Financial Services, FIS, Fiserv and Jack Henry, and network partners VISA and MasterCard.

The participating banks are now integrating Zelle into their own websites and mobile apps – meaning, users are finding Zelle as they use their existing banking applications. They’re not seeking it out directly, in many cases.

“One of the main hurdles new apps face is building trust and a sizable audience,” explained eMarketer forecasting analyst Cindy Liu. “But Zelle has leapfrogged the early stages of adoption by having the benefit of being embedded into the already existing apps of participating banks,” she said.

Earlier this year, Zelle said it was signing up users at a rate of 100,000 consumers per day, and claimed it had processed 247 million payments totaling $75 billion in 2017. That’s a sizable chunk of the peer-to-peer payments market.

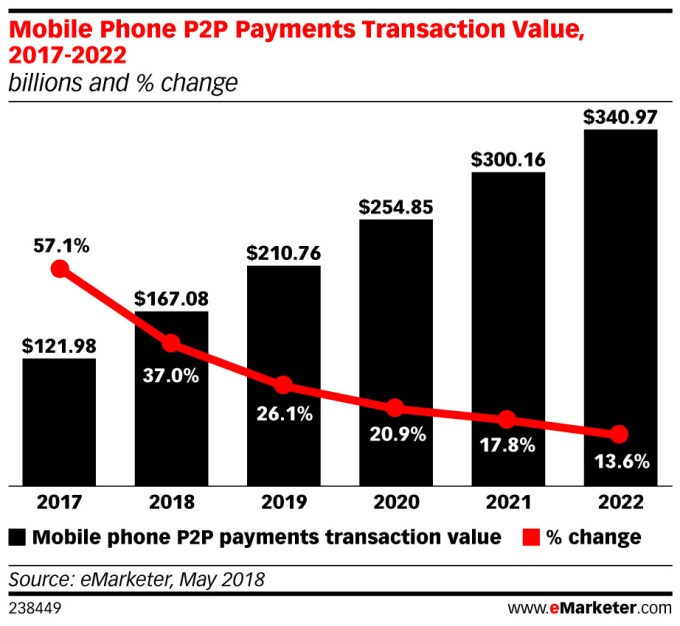

Emarketer’s forecast estimates the total number of U.S. p2p mobile payment users will grow 30 percent in 2018 to reach 82.5 million people, or 40.5 percent of U.S. smartphone users. It also expects the total transaction volume of p2p mobile payments to grow 37 percent this year to reach $167.08 billion. By 2021, that figure will reach over $300 billion.

That leaves room for all services to carve out their piece of the market, even if Zelle ends up in the lead.

Powered by WPeMatico

A peer-to-peer payment app that works similarly to Venmo from startup Lydia in France now works with Apple Pay (a feature originally announced in July), making it possible to spend your balance from the app wherever MasterCard and Apple Pay are accepted. It’s a neat use of Apple Pay to make it possible to do mobile payments without requiring that a user have a credit card – and it… Read More

A peer-to-peer payment app that works similarly to Venmo from startup Lydia in France now works with Apple Pay (a feature originally announced in July), making it possible to spend your balance from the app wherever MasterCard and Apple Pay are accepted. It’s a neat use of Apple Pay to make it possible to do mobile payments without requiring that a user have a credit card – and it… Read More

Powered by WPeMatico

Zelle, the PayPal rival backed by more than 30 U.S. banks, is preparing to launch its standalone mobile app on Tuesday, September 12th. The move is meant to give the U.S. banking industry a foothold in the person-to-person payments business, where they’re losing ground to services like PayPal, Venmo, Square Cash and, very soon, Apple’s iMessage, powered by Apple Pay. Read More

Zelle, the PayPal rival backed by more than 30 U.S. banks, is preparing to launch its standalone mobile app on Tuesday, September 12th. The move is meant to give the U.S. banking industry a foothold in the person-to-person payments business, where they’re losing ground to services like PayPal, Venmo, Square Cash and, very soon, Apple’s iMessage, powered by Apple Pay. Read More

Powered by WPeMatico

Here’s a sentence you might not have expected to read: a service built around crowdfunding is building in a one-to-one payments option in what might be one of the most increasingly crowded spaces in the U.S. That’s what Tilt, an app geared toward crowdfunding events like parties or travel plans, is hoping will make its service even more sticky and a one-stop destination for… Read More

Here’s a sentence you might not have expected to read: a service built around crowdfunding is building in a one-to-one payments option in what might be one of the most increasingly crowded spaces in the U.S. That’s what Tilt, an app geared toward crowdfunding events like parties or travel plans, is hoping will make its service even more sticky and a one-stop destination for… Read More

Powered by WPeMatico