Venmo

Auto Added by WPeMatico

Auto Added by WPeMatico

It’s pretty easy for individuals to send money back and forth, and there are lots of cash apps from which to choose. On the commercial side, however, one business trying to send $100,000 the same way is not as easy.

Paystand wants to change that. The Scotts Valley, California-based company is using cloud technology and the Ethereum blockchain as the engine for its Paystand Bank Network that enables business-to-business payments with zero fees.

The company raised $50 million Series C funding led by NewView Capital, with participation from SoftBank’s SB Opportunity Fund and King River Capital. This brings the company’s total funding to $85 million, Paystand co-founder and CEO Jeremy Almond told TechCrunch.

During the 2008 economic downturn, Almond’s family lost their home. He decided to go back to graduate school and did his thesis on how commercial banking could be better and how digital transformation would be the answer. Gleaning his company vision from the enterprise side, Almond said what Venmo does for consumers, Paystand does for commercial transactions between mid-market and enterprise customers.

“Revenue is the lifeblood of a business, and money has become software, yet everything is in the cloud except for revenue,” he added.

He estimates that almost half of enterprise payments still involve a paper check, while fintech bets heavily on cards that come with 2% to 3% transaction fees, which Almond said is untenable when a business is routinely sending $100,000 invoices. Paystand is charging a flat monthly rate rather than a fee per transaction.

Paystand’s platform. Image Credits: Paystand

On the consumer side, companies like Square and Stripe were among the first wave of companies predominantly focused on accounts payable and then building business process software on top of an existing infrastructure.

Paystand’s view of the world is that the accounts receivables side is harder and why there aren’t many competitors. This is why Paystand is surfing the next wave of fintech, driven by blockchain and decentralized finance, to transform the $125 trillion B2B payment industry by offering an autonomous, cashless and feeless payment network that will be an alternative to cards, Almond said.

Customers using Paystand over a three-year period are able to yield average benefits like 50% savings on the cost of receivables and $850,000 savings on transaction fees. The company is seeing a 200% increase in monthly network payment value and customers grew two-fold in the past year.

The company said it will use the new funding to continue to grow the business by investing in open infrastructure. Specifically, Almond would like to reboot digital finance, starting with B2B payments, and reimagine the entire CFO stack.

“I’ve wanted something like this to exist for 20 years,” Almond said. “Sometimes it is the unsexy areas that can have the biggest impacts.”

As part of the investment, Jazmin Medina, principal at NewView Capital, will join Paystand’s board. She told TechCrunch that while the venture firm is a generalist, it is rooted in fintech and fintech infrastructure.

She also agrees with Almond that the B2B payments space is lagging in terms of innovation and has “strong conviction” in what Almond is doing to help mid-market companies proactively manage their cash needs.

“There is a wide blue ocean of the payment industry, and all of these companies have to be entirely digital to stay competitive,” Medina added. “There is a glaring hole if your revenue is holding you back because you are not digital. That is why the time is now.”

Powered by WPeMatico

Lower, an Ohio-based home finance platform, announced today it has raised $100 million in a Series A funding round led by Accel.

This round is notable for a number of reasons. First off, it’s a large Series A even by today’s standards. The financing also marks the previously bootstrapped Lower’s first external round of funding in its seven-year history. Lower is also something that is kind of rare these days in the startup world: profitable. Silicon Valley-based Accel has a history of backing profitable, bootstrapped companies, having also led large Series A rounds for the likes of 1Password, Atlassian, Qualtrics, Webflow, Tenable and Galileo (which went on to be acquired by SoFi).

In fact, Galileo founder Clay Wilkes introduced the VC firm to Dan Snyder, Lower’s founder and CEO. The two companies have a few things in common besides being profitable: they were both bootstrapped for years before taking institutional capital and both have headquarters outside of Silicon Valley.

“We were immediately intrigued because Ohio-based Lower echoes both of these themes,” said Accel partner John Locke, who led the firm’s investment in Lower and is taking a seat on the company’s board as part of the investment. “Like Galileo, Lower will be one of the most successful bootstrapped fintech companies globally. The combination of a company built in a nontraditional region across the globe and a bootstrapped company reminds us of [other] companies we have partnered with for a large Series A.”

There were other unnamed participants in the round, but Accel provided the “majority” of the investment, according to Lower.

Snyder co-founded Lower in 2014 with the goal of making the home-buying process simpler for consumers. The company launched with Homeside, its retail brand that Snyder describes as “a tech-leveraged retail mortgage bank” that works with realtors and builders, among others.

In 2018, the company launched the website for Lower, its direct-to-consumer digital lending brand with the mission of making its platform a one-stop shop where consumers can go online to save for a home, obtain or refinance a mortgage and get insurance through its marketplace. This year, it launched the Lower mobile app with a savings account.

Sitting (L to R): Co-founders Dan Snyder, Grayson Hanes

Standing (L to R): Co-founders Mike Baynes, Chris Miller

Not pictured: Robert Tyson; Image credit: Lower

Over the years, Lower has funded billions of dollars in loans and notched an impressive $300 million in revenue in 2020 after doubling revenue every year, according to Snyder.

“Our history is maybe a little atypical of fintech companies today,” he told TechCrunch. “We’ve had a view going back to the start of the company that we wanted to run it profitably. That’s been one of our pillars, so that’s what we’ve done. Also, we all grew up in the mortgage industry, so we saw firsthand the size of the market, but also how broken it was, so we wanted to change it.”

In launching the direct-to-consumer digital lending brand, the company was working to make the homebuying process more “digital, transparent and easier for consumers to access,” Snyder said.

At the same time, the company didn’t want to lose the human touch.

“We tried to design the app flow in a way where you can get as far along as you can in the application but if you want, at any point in time, to talk or chat with someone, we’re available,” Snyder added.

Image Credits: Lower

Lower’s typical customer is the millennial and now Gen Z who’s aspiring to own their first home, according to Snyder.

“They might be thinking, ‘OK, I might be living in an apartment now, but in the next few years I’m going to meet someone and/or have a child and I want to unlock the investment that is a home,’” he told TechCrunch. “And we’ll help them on that journey.”

Lower’s recently launched new app offers a deposit account it’s dubbed “HomeFund.” The interest-bearing, FDIC-insured deposit account offers a 0.75% Annual Percentage Yield and is designed to help consumers save for a home with a “dollar-for-dollar match in rewards” up to the first $1,000 saved, Snyder said.

Lower works with more than 35 major insurance carriers nationally, including Nationwide, Liberty Mutual and Allstate. It has more than 1,600 employees, about half of which are based in Lower’s home state. That’s up from about 650 employees in June of 2020.

Looking ahead, the company plans to add more services and has an “aggressive roadmap” for adding new features to its platform. Today, for example, Lower sells primarily to Fannie Mae and Freddie Mac. And while it services the majority of its loans, like many large lenders, it uses a subservicer. That will change, however, in early 2022, when Lower intends to launch its own native servicing platform.

And while the company intends to continue to run profitably, Snyder said he and his co-founders “think the time is now to gain share.”

“We want to become a global brand, raise money and gain market share,” he added. “We’re going to continue to double down on product and build out our capabilities. We are the best-kept secret in fintech and plan to change that with smart branding, advertising and sponsorships.”

And last but not least, Lower is eyeing the public markets as part of its longer-term roadmap.

“Ultimately, we know we can build a great public company,” Snyder told TechCrunch. “We’re of the scale to be a public company right now, but we’re going to keep our heads down and we’re going to keep building for the next few years and then I think we can be in a spot to be a strong public business.”

Accel’s Locke points out that in the U.S., mortgage and home finance are among the largest financial service markets, and they have primarily been handled by large banks.

“For most consumers, getting a mortgage through these banks continues to be an overly complex, slow-moving process,” Locke told TechCrunch. “We believe by providing consumers a great mobile experience, Lower will gain share from incumbent banks, in the same way that companies like Monzo have in banking or Venmo in payments or Trade Republic and Robinhood in stock trading.”

Powered by WPeMatico

This spring, Facebook confirmed it was testing Venmo-like QR codes for person-to-person payments inside its app in the U.S. Today, the company announced those codes are now launching publicly to all U.S. users, allowing anyone to send or request money through Facebook Pay — even if they’re not Facebook friends.

The QR codes work similarly to those found in other payment apps, like Venmo.

The feature can be found under the “Facebook Pay” section in Messenger’s settings, accessed by tapping on your profile icon at the top left of the screen. Here, you’ll be presented with your personalized QR code which looks much like a regular QR code except that it features your profile icon in the middle.

Underneath, you’ll be shown your personal Facebook Pay UR which is in the format of “https://m.me/pay/UserName.” This can also be copied and sent to other users when you’re requesting a payment.

Facebook notes that the codes will work between any U.S. Messenger users, and won’t require a separate payment app or any sort of contact entry or upload process to get started.

Users who want to be able to send and receive money in Messenger have to be at least 18 years old, and will have to have a Visa or Mastercard debit card, a PayPal account or one of the supported prepaid cards or government-issued cards, in order to use the payments feature. They’ll also need to set their preferred currency to U.S. dollars in the app.

After setup is complete, you can choose which payment method you want as your default and optionally protect payments behind a PIN code of your choosing.

The QR code is also available from the Facebook Pay section of the main Facebook app, in a carousel at the top of the screen.

Facebook Pay first launched in November 2019, as a way to establish a payment system that extends across the company’s apps for not just person-to-person payments, but also other features, like donations, Stars and e-commerce, among other things. Though the QR codes take cues from Venmo and others, the service as it stands today is not necessarily a rival to payment apps because Facebook partners with PayPal as one of the supported payment methods.

However, although the payments experience is separate from Facebook’s cryptocurrency wallet, Novi, that’s something that could perhaps change in the future.

Image Credits: Facebook

The feature was introduced alongside a few other Messenger updates, including a new Quick Reply bar that makes it easier to respond to a photo or video without having to return to the main chat thread. Facebook also added new chat themes including one for Olivia Rodrigo fans, another for World Oceans Day, and one that promotes the new F9 movie.

Powered by WPeMatico

The COVID-19 pandemic has accelerated digital adoption in a way that no one could have ever anticipated, and as more people conduct more services online and via mobile devices, businesses have had to work even harder to validate users and security. One company working to serve that need, Socure — which uses AI and machine learning to verify identities — announced Tuesday that it has raised $100 million in a Series D funding round at a $1.3 billion valuation.

Given how much of our lives have shifted online, it’s no surprise that the U.S. digital identity market is projected to increase to over $30 billion by 2023 from just under $15 billion in 2019, according to One World Identity. This has led to skyrocketing demand for the services provided by identity verification companies.

The founding team set out on a mission to be able to verify 100% of “good IDs” in real-time while “completely eliminating” identity fraud across the internet.

Historically, Socure has been focused on the financial services industry, but it plans to use its new capital to further expand into “every consumer-facing vertical” including online gaming, healthcare, telco, e-commerce and on-demand services.

The startup’s predictive analytics platform applies artificial intelligence and machine-learning techniques with online/offline data intelligence (from email, phone, address, IP, device, velocity and the broader internet) to verify that people are, in fact, who they say they are when applying for various accounts.

Today, Socure has more than 350 customers including three top five banks, six top 10 card issuers, a “top” credit bureau and over 75 fintechs such as Varo Money, Public, Chime and Stash.

In 2020, Socure grew its customer base by over 85% year over year and expanded its workforce by over 50% to about 240 people today.

Accel led Socure’s latest financing, which included participation from existing backers Commerce Ventures, Scale Venture Partners, Flint Capital, Citi Ventures, Wells Fargo Strategic Capital, Synchrony, Sorenson, Two Sigma Ventures and others.

The round comes less than six months after the company raised $35 million in a round led by Sorenson Ventures, and brings the New York-based company’s total raised to $196 million since its 2012 inception.

Socure founder and CEO Johnny Ayers says his company’s identity management products can help B2C enterprises achieve know-your-customer (KYC) auto-approval rates of up to 97%. This means that financial institutions can more easily capture fraud, for example, via Socure’s single API. The company also claims that by more easily verifying thin-file (those without much credit history) and young consumers, it can help reduce the underbanked population.

The pandemic and resulting shutdowns resulted in a massive demand for trusted digital identity, Ayers believes.

“This growth tracks with a larger trend marked by the broad migration of businesses to accept applications and onboard new customers online, with many companies accelerating their transformation from digital-first to digital-only,” he told TechCrunch.

Overall fraud attempts among Socure’s existing customer base nearly doubled in the second quarter of 2020 — with certain segments seeing rises as high as 150%, according to Ayers.

“These instances did not involve actual fraud but instead were flagged by Socure as suspicious and blocked prior to inflicting damage,” he said.

Looking ahead, the company plans to use its new capital to also enhance its product offering as it continues to develop patents.

Accel partner Amit Jhawar will join Socure’s board as part of the funding round.

In a blog post, Jhawar described Socure as “a purpose-built solution designed to handle the wave of new online users because its machine learning models have learned from every identity it has already seen.”

As former COO at Braintree and general manager at Venmo, Jhawar knows a thing or two about the importance of identity verification, especially in the financial services space.

He wrote: “I knew immediately that the Socure solution would be a game-changer because the solution can be used in every step of the customer lifecycle, from account creation to login to transaction.”

Socure also has hinted that it has an IPO in its future.

In a written statement, Ayers said: “We are incredibly grateful for the chance to innovate and partner to solve this problem with some of the greatest companies in the world and are energized for the opportunities that lay ahead for Socure, especially as we make our march to a potential IPO.”

Via email, he told TechCrunch that the company will “potentially” look at public markets in 2022 or 2023, when it feels “the time is right for the business.”

The story was updated post-publication with live comments from Socure

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion. Use code “TCARTICLE at checkout to get 20% off tickets right here.

Powered by WPeMatico

JoomPay, a startup with a similar product to PayPal-owned Venmo in the U.S., is set to launch in Europe shortly after being granted a Luxembourg Electronic Money Institution (EMI) license. The app allows people to send and receive money with anyone, instantly and for free. “Venmo me” has become a common phrase in the U.S., where people use it to split bills in restaurants or similar instances. Venmo is in common use in the U.S., but it’s not available in Europe, although dozens of other innovative mobile peer to peer transfer options exist, such as Revolut, N26, Monese and Monzo. The waitlist for the app’s beta is open now (iOS, Android).

Europe leads the world’s instant payments industry, with $18 trillion in worldwide volume predicted by 2025, up from $3 trillion in 2020 — a growth of more than 500%. Western Europe — and COVID-19 — is now driving that innovation and will account for 38% of instant payment transaction value by 2025. While Europe lacks simple peer-to-peer payments solutions such as Venmo or Square Cash App in the U.S., challenger banks have stepped up to provide similar kinds of services. JoomPay’s opportunity lies in being able to be a middle-man between these various banking systems.

Shopping app Joom, which has been downloaded 150 million times in Europe, has spun-off JoomPay to solve this problem. The app allows users to send and receive money from any person, regardless of whether they use JoomPay or not — and you only need to know their email or the phone number. JoomPay connects to any existing debit/credit card or a bank account. It also provides its users with a European IBAN and an optional free JoomPay card with cashback and bonuses.

Yuri Alekseev, CEO and co-founder of JoomPay, said: “Since COVID-19 started, we’ve seen a significant decline in cash usage. People can’t meet as easily as before but still need to send money, and we offer a viable alternative.”

JoomPay may have an uphill struggle. Its main competitors in Europe are the huge TransferWise, Paysend and, of course, PayPal itself.

Powered by WPeMatico

PayPal this week laid out its vision for the future of its digital wallet platform and its PayPal and Venmo apps. During its third-quarter earnings call on Monday, the company said it plans to roll out substantial changes to its mobile apps over the next year to integrate a range of new features, including enhanced direct deposit, check cashing, budgeting tools, bill pay, crypto support, subscription management, buy now/pay later functionality and all of Honey’s shopping tools.

While PayPal had spoken in the past about bringing Honey’s capabilities into PayPal, CEO Dan Schulman detailed the integrations PayPal has in store for the deal-finding platform it bought last year for $4 billion, as well as a timetable for both this and the other app updates it has in store.

The Honey acquisition had brought 17 million monthly active users to PayPal. These users turned to Honey’s browser extension and mobile app to find the best savings on items they want to buy, track prices and more.

But today, the Honey experience still remains separate from PayPal itself. That’s something the company wants to change next year.

According to Schulman, the company’s apps will be updated to include Honey’s shopping tools, like its Wish List feature that allows you to track items you want to buy, price monitoring tools that alert you to savings and price drops, plus its deals, coupons and rewards. These tools will become part of PayPal’s checkout solution itself.

That means the company will be able to track the customer from the initial deal-hunting phase where they’re indicating their interest in a certain product, target them with savings and offers, then guide them through its checkout experience all in one place.

PayPal will also provide “anonymous demand data” to merchants based on consumer engagement with Honey’s tools to help them drive sales, the company said.

What’s more, PayPal put timeline on the Honey integrations and the other updates it plans to roll out over the course of the next year.

Bill Pay will start to roll out this month, PayPal said, with a large redesign of the digital wallet experience expected for the first half of 2021. Much of the new functionality will be arriving in the second quarter and the second half of the year, with a goal of having the majority of the changes rolled out by the end of next year.

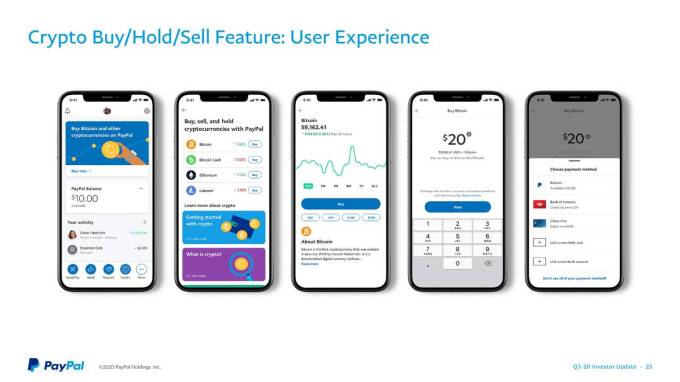

This also includes PayPal’s plans for cryptocurrencies, announced at the end of October. The company aims to support Bitcoin, Ethereum, Bitcoin Cash and Litecoin at first, initially in the U.S.

Speaking to investors during the earnings call, Schulman also noted when PayPal plans to bring crypto to more users and geographies. He said the ability to buy, sell and hold cryptocurrencies will first arrive in the U.S., then will roll out to international markets and the Venmo app in the first half of next year. (Currently, PayPal is offering U.S. users to join a waitlist for the new crypto features in-app).

Image Credits: PayPal

This change will allow PayPal’s users to shop using cryptocurrencies across the company’s 28 million merchants without requiring additional integrations on merchants’ part. The company explained this is due to how it will handle the settlement process, where users will be able to instantaneously transfer crypto into fiat currency at a set rate when checking out with PayPal merchants.

“This solution will not involve any additional integrations, volatility risk or incremental transaction fees for either consumers or merchants, and will fundamentally bolster the utility of cryptocurrencies,” said Schulman. “This is just the beginning of the opportunities we see as we work hand in hand with regulators to accept new forms of digital currencies,” he added.

PayPal also recently joined the “buy now, pay later” race with its new “Pay in 4” installment program that lets consumers split purchases into four payments. This debuted in France ahead of its late August U.S. launch and has since rolled out to the U.K. (as Pay in 3). This too, will become more integrated into the company’s apps in the months ahead.

Venmo — which the company expects to reach $900 million in revenues next year — will see the expansion of business profiles, and will gain crypto capabilities, more basic financial tools and shopping tools, as well as a revamp of the “Pay with Venmo” checkout experience.

Schulman referred to the company’s plans to overhaul its Venmo and PayPal apps as a “fundamental transformation,” due to how much new functionality they will include as the changes roll out over the next year as well as the new user experience — basically, a redesign — that will allow people to move easily from one experience to the next instead of having to change apps or use a desktop browser, for example.

PayPal’s earnings hadn’t excited Wall Street investors this week, sending the stock down on its lack of 2021 guidance. But the year ahead for PayPal’s digital wallet apps looks to be an interesting one.

Powered by WPeMatico

It’s only been a few months since Lili announced its $10 million seed round, and it’s already raised more funding — namely, a $15 million Series A.

The startup, founded by CEO Lilac Bar David and CTO Liran Zelkha, is creating a bank account and associated products designed for freelancers, with features like early access to direct deposit payments and the ability to set aside a percentage of income for taxes.

The account (and associated Visa debit card) is free of overdraft fees or minimum balance requirements; Bar David said the company only makes money from card processing fees.

She also said that the platform has seen rapid growth this year, with transactions up 700% since the beginning of the pandemic and nearly 100,000 accounts opened since the launch in 2019.

Bar David suggested that the economic turmoil caused by COVID-19 has prompted (or forced) more skilled workers — such as programmers and digital marketers — to turn to freelancing. Meanwhile, she’s also seen “a big shift from part-time freelance to full-time freelance.”

Lili CEO Lilac Bar David

Bar David predicted that the recent growth of the freelance economy won’t simply disappear once the pandemic is over, because workers are discovering the benefits of freelancing.

“If you have a 9-to-5 job, you’re dependent on one employer,” she said. “If something happens you’re out of a job … If you’ve got a diversified customer base, you’re not dependent on just one source of income.”

In recent months, Lili has added new features like automatically generated quarterly income and expense reports, a digital debit card (which customers can use before the physical card arrives in the mail) and the ability to send and receive money via Google Pay (Lili already supported Cash App and Venmo) .

Bar David said the startup decided to raise more funding to expand its engineering team and further accelerate its growth. Apparently she was preparing for a traditional Series A fundraising process (albeit one that was conducted in the middle of a pandemic), but “our current investors were so tremendously impressed by the product-market fit and the growth” that they were willing to fund almost all of the new round.

So the Series A was led by previous investor Group 11, with participation from Foundation Capital, AltaIR Capital, Primary Venture Partners and Torch Capital — along with new backer Zeev Ventures.

“As the global workforce evolves at a rapid pace, we are excited to lead another round of funding to help Lili capitalize on unprecedented demand and offer an entirely new solution to help freelancers seamlessly save time and money,” said Group 11’s Dovi Frances in a statement.

Powered by WPeMatico

Years from now, people will look back on the COVID-19 pandemic as a watershed moment for society and the global economy.

Wearing a mask might be as common as owning a phone; telework, telemedicine and online education will be more of a norm than a backup plan; and for the global economy, the cloud will have transformed the underlying infrastructure of businesses and entire industries.

COVID-19 is a turning point for the cloud and cloud company founders. For its computing power and as a delivery model of software, the cloud has been embraced as a solution to many challenges that businesses face during today’s economic downturn and recovery. Not only is the cloud industry more resilient than other industries, but the cloud model offers businesses a promising future in the age of social distancing and beyond.

We believe that once founders find shelter in the cloud, they’ll never go back.

Over the past decade, there’s been a massive market shift from on-premises to cloud, as 94% of enterprises use at least one cloud service today. 2020 was already a milestone year for the cloud industry, as aggregate SaaS and IaaS run-rate revenue each crossed $100 billion, and the BVP Nasdaq Emerging Cloud Index (^EMCLOUD) market cap crossed $1 trillion in early February. Yet in a matter of days, as the COVID-19 pandemic spread, fear tore through financial markets.

In early March, public markets experienced the steepest crash in history with volatility we haven’t seen since the Great Recession. The cloud index market cap dropped to ~$750 million and cloud multiples returned close to their historical averages of ~7x while the VIX volatility index spiked to the mid-80s. Both at global highs in February 2020, the ^EMCLOUD and the S&P 500 traded off by roughly 35% by mid-March. Over the next two months, though, the ^EMCLOUD recouped those losses, charging to a new all-time high on May 7.

The cloud index has continued its rise since then, and as of the close on May 11 has a market cap above $1.2 trillion and has returned to the lofty 12x forward run rate revenue multiples from 2019. Similar to Adobe in 2012, we expect many enterprises to transition over to the cloud model, and the index will continue to expand. As we predicted in this year’s State of the Cloud 2020, by 2025 we expect the cloud to penetrate 50% of enterprise software.

Powered by WPeMatico

Allowance is going digital. Venmo has been spotted prototyping a new feature that would allow adult users to create for their teenage children a debit card connected to their account. That could potentially let parents set spending notifications and limits while giving kids more flexibility in urgent situations than a few dollars stuffed in a pocket.

Delving into children’s banking could establish a new reason for adults to sign up for Venmo, get them saving more in Venmo debit accounts where the company can earn interest on the cash and drive purchase frequency that racks up interchange fees for Venmo’s owner PayPal .

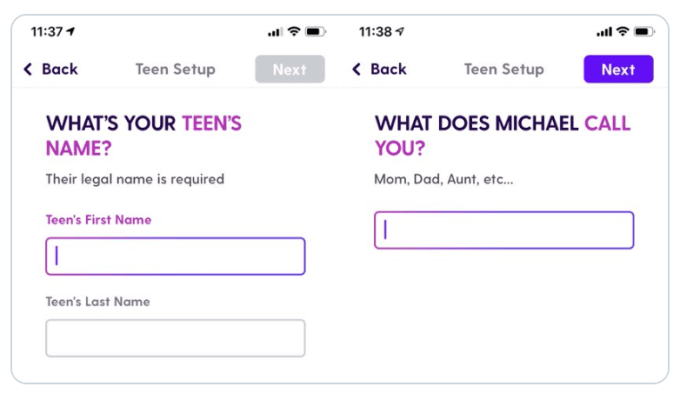

But Venmo is arriving late to the teen debit card market. Startups like Greenlight and Step let parents manage teen spending on dedicated debit cards. More companies like Kard and neo banking giant Revolut have announced plans to launch their own versions. And Venmo’s prototype uses very similar terminology to that of Current, a frontrunner in the children’s banking space with over 500,000 accounts that raised a $20 million Series B late last year.

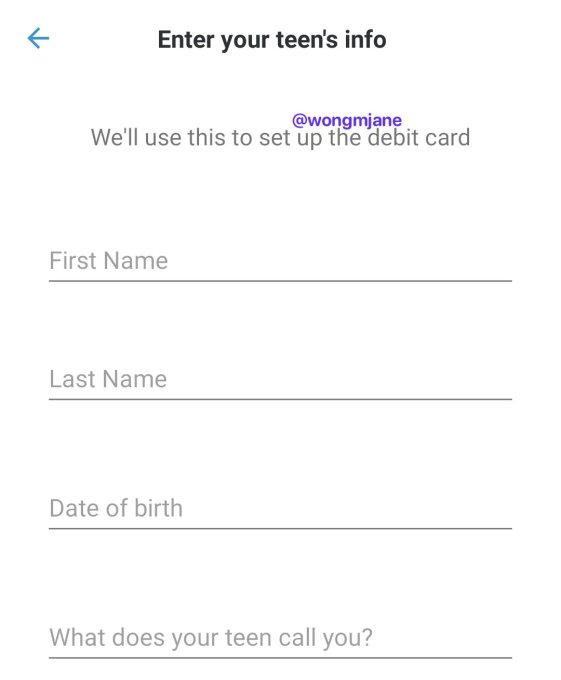

The first signs of Venmo’s debit card were spotted by reverse engineering specialist Jane Manchun Wong, who has provided slews of accurate tips to TechCrunch in the past. Hidden in Venmo’s Android app is code revealing a “delegate card” feature, designed to let users create a debit card that’s connected to their account but has limited privileges.

A screenshot generated from hidden code in Venmo’s app, via Jane Manchun Wong

A set-up screen Wong was able to generate from the code shows the option to “Enter your teen’s info,” because “We’ll use this to set up the debit card.” It asks parents to enter their child’s name, birth date and “What does your teen call you?” That’s almost identical to the “What does [your child’s name] call you?” set-up screen for Current’s teen debit card.

When TechCrunch asked about the teen debit feature and when it might launch, a Venmo spokesperson gave a cagey response that implies it’s indeed internally testing the option, writing “Venmo is constantly working to identify ways to refine and enhance the user experience. We frequently test product offerings to understand the value it could have for our users, and I don’t have anything further to share right now.”

Typically, the tech company product development flow sees them come up with ideas, mock them up, prototype them in their real apps as internal-only features, test them externally with small percentages of real users, then launch them officially if feedback and data is positive throughout. It’s unclear when Venmo might launch teen debit cards, though the product could always be scrapped. It’d need to move fast to beat Revolut and Kard to market.

Current’s teen debit card

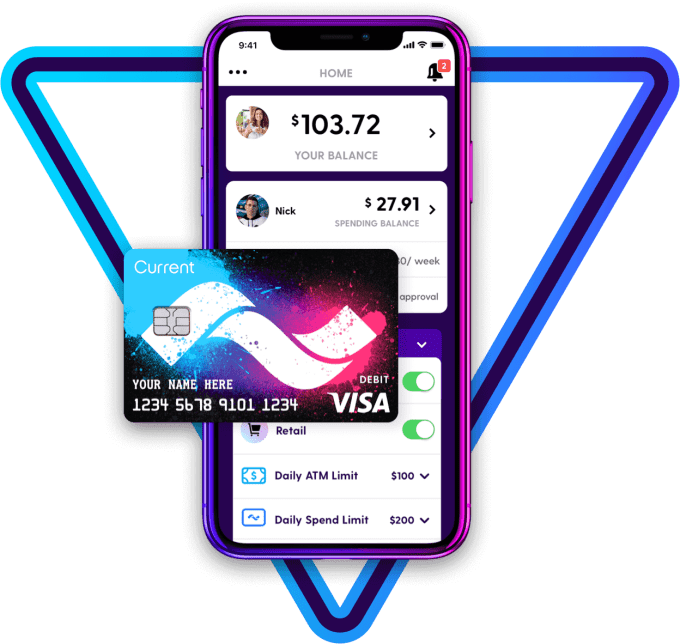

The launch would build upon the June 2018 launch of Venmo’s branded Mastercard debit card that’s monetized through interchange fees and interest on savings. It offers payment receipts with options to split charges with friends within Venmo, free withdrawls at MoneyPass ATMs, rewards and in-app features for reseting your PIN or disabling a stolen card. Venmo also plans to launch a credit card issued by Synchrony this year.

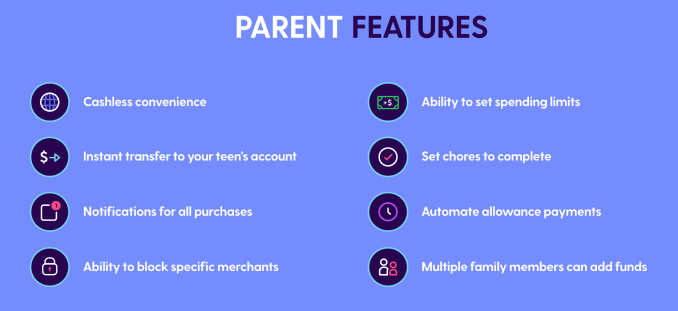

Venmo might look to equip its teen debit card with popular features from competitors, like automatic weekly allowance deposits, notifications of all purchases or the ability to block spending at certain merchants. It’s unclear if it will charge a fee like the $36 per year subscription for Current.

Current offers these features for parents who set up a teen debit card

Tech startups are increasingly pushing to offer a broad range of financial services where margins are high. It’s an easy way to earn cheap money at a time when unit economics are coming under scrutiny in the wake of the WeWork implosion. Investors are pinning their hopes on efficient financial services too, pouring $34 billion into fintech startups during 2019.

Venmo’s already become a popular way for younger people to split the bill for Uber rides or dinner. Bringing social banking to a teen demographic probably should have been its plan all along.

Powered by WPeMatico

Sam Lessin, a former product management executive at Facebook and old friend to Mark Zuckerberg, incorporated his latest startup under the name “Fin Exploration Company.”

Why? Well, because he wanted to explore. The company — co-founded alongside Andrew Kortina, best known for launching the successful payments app Venmo — was conceived as a consumer voice assistant in 2015 after the two entrepreneurs realized the impact 24/7 access to a virtual assistant would have on their digital to-do lists.

The thing is, developing an AI assistant capable of booking flights, arranging trips, teaching users how to play poker, identifying places to purchase specific items for a birthday party and answering wide-ranging zany questions like “can you look up a place where I can milk a goat?” requires a whole lot more human power than one might think. Capital-intensive and hard-to-scale, an app for “instantly offloading” chores wasn’t the best business. Neither Lessin nor Kortina will admit to failure, but Fin‘s excursion into B2B enterprise software eight months ago suggests the assistant technology wasn’t a billion-dollar idea.

Staying true to its name, the Fin Exploration Company is exploring again.

Powered by WPeMatico