unicorn

Auto Added by WPeMatico

Auto Added by WPeMatico

Hundreds gathered this week at San Francisco’s Pier 48 to see the more than 200 companies in Y Combinator’s Winter 2019 cohort present their two-minute pitches. The audience of venture capitalists, who collectively manage hundreds of billions of dollars, noted their favorites. The very best investors, however, had already had their pick of the litter.

What many don’t realize about the Demo Day tradition is that pitching isn’t a requirement; in fact, some YC graduates skip out on their stage opportunity altogether. Why? Because they’ve already raised capital or are in the final stages of closing a deal.

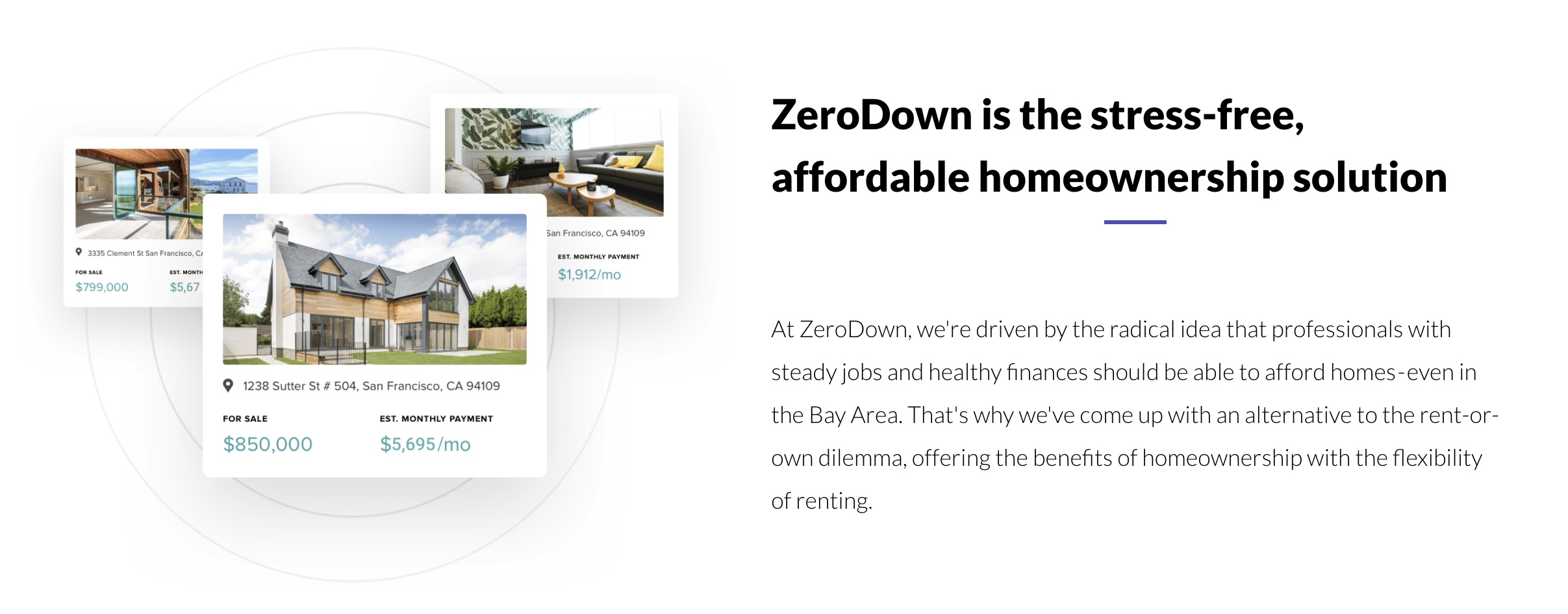

ZeroDown, Overview.AI and Catch are among the startups in YC’s W19 batch that forwent Demo Day this week, having already pocketed venture capital. ZeroDown, a financing solution for real estate purchases in the Bay Area, raised a round upwards of $10 million at a $75 million valuation, sources tell TechCrunch. ZeroDown hasn’t responded to requests for comment, nor has its rumored lead investor: Goodwater Capital.

Without requiring a down payment, ZeroDown purchases homes outright for customers and helps them work toward ownership with monthly payments determined by their income. The business was founded by Zenefits co-founder and former chief technology officer Laks Srini, former Zenefits chief operating officer Abhijeet Dwivedi and Hari Viswanathan, a former Zenefits staff engineer.

The founders’ experience building Zenefits, despite its shortcomings, helped ZeroDown garner significant buzz ahead of Demo Day. Sources tell TechCrunch the startup had actually raised a small seed round ahead of YC from former YC president Sam Altman, who recently stepped down from the role to focus on OpenAI, an AI research organization. Altman is said to have encouraged ZeroDown to complete the respected Silicon Valley accelerator program, which, if nothing else, grants its companies a priceless network with which no other incubator or accelerator can compete.

Overview .AI’s founders’ resumes are impressive, too. Russell Nibbelink and Christopher Van Dyke were previously engineers at Salesforce and Tesla, respectively. An industrial automation startup, Overview is developing a smart camera capable of learning a machine’s routine to detect deviations, crashes or anomalies. TechCrunch hasn’t been able to get in touch with Overview’s team or pinpoint the size of its seed round, though sources confirm it skipped Demo Day because of a deal.

Catch, for its part, closed a $5.1 million seed round co-led by Khosla Ventures, NYCA Partners and Steve Jang prior to Demo Day. Instead of pitching their health insurance platform at the big event, Catch published a blog post announcing its first feature, The Catch Health Explorer.

“This is only the first glimpse of what we’re building this year,” Catch wrote in the blog post. “In a few months, we’ll be bringing end-to-end health insurance enrollment for individual plans into Catch to provide the best health insurance enrollment experience in the country.”

TechCrunch has more details on the healthtech startup’s funding, which included participation from Kleiner Perkins, the Urban Innovation Fund and the Graduate Fund.

Four more startups, Truora, Middesk, Glide and FlockJay had deals in the final stages when they walked onto the Demo Day stage, deciding to make their pitches rather than skip the big finale. Sources tell TechCrunch that renowned venture capital firm Accel invested in both Truora and Middesk, among other YC W19 graduates. Truora offers fast, reliable and affordable background checks for the Latin America market, while Middesk does due diligence for businesses to help them conduct risk and compliance assessments on customers.

Finally, Glide, which allows users to quickly and easily create well-designed mobile apps from Google Sheets pages, landed support from First Round Capital, and FlockJay, the operator an online sales academy that teaches job seekers from underrepresented backgrounds the skills and training they need to pursue a career in tech sales, secured investment from Lightspeed Venture Partners, according to sources familiar with the deal.

Raising ahead of Demo Day isn’t a new phenomenon. Companies, thanks to the invaluable YC network, increase their chances at raising, as well as their valuation, the moment they enroll in the accelerator. They can begin chatting with VCs when they see fit, and they’re encouraged to mingle with YC alumni, a process that can result in pre-Demo Day acquisitions.

This year, Elph, a blockchain infrastructure startup, was bought by Brex, a buzzworthy fintech unicorn that itself graduated from YC only two years ago. The deal closed just one week before Demo Day. Brex’s head of engineering, Cosmin Nicolaescu, tells TechCrunch the Elph five-person team — including co-founders Ritik Malhotra and Tanooj Luthra, who previously founded the Box-acquired startup Steem — were being eyed by several larger companies as Brex negotiated the deal.

“For me, it was important to get them before batch day because that opens the floodgates,” Nicolaescu told TechCrunch. “The reason why I really liked them is they are very entrepreneurial, which aligns with what we want to do. Each of our products is really like its own business.”

Of course, Brex offers a credit card for startups and has no plans to dabble with blockchain or cryptocurrency. The Elph team, rather, will bring their infrastructure security know-how to Brex, helping the $1.1 billion company build its next product, a credit card for large enterprises. Brex declined to disclose the terms of its acquisition.

Y Combinator partners Michael Seibel and Dalton Caldwell, and moderator Josh Constine, speak onstage during TechCrunch Disrupt SF 2018. (Photo by Kimberly White/Getty Images)

Ultimately, it’s up to startups to determine the cost at which they’ll give up equity. YC companies raise capital under the SAFE model, or a simple agreement for future equity, a form of fundraising invented by YC. Basically, an investor makes a cash investment in a YC startup, then receives company stock at a later date, typically upon a Series A or post-seed deal. YC made the switch from investing in startups on a pre-money safe basis to a post-money safe in 2018 to make cap table math easier for founders.

Michael Seibel, the chief executive officer of YC, says the accelerator works with each startup to develop a personalized fundraising plan. The businesses that raise at valuations north of $10 million, he explained, do so because of high demand.

“Each company decides on the amount of money they want to raise, the valuation they want to raise at, and when they want to start fundraising,” Seibel told TechCrunch via email. “YC is only an advisor and does not dictate how our companies operate. The vast majority of companies complete fundraising in the 1 to 2 months after Demo Day. According to our data, there is little correlation between the companies who are most in demand on Demo Day and ones who go on to become extremely successful. Our advice to founders is not to over optimize the fundraising process.”

Though Seibel says the majority raise in the months following Demo Day, it seems the very best investors know to be proactive about reviewing and investing in the batch before the big event.

Khosla Ventures, like other top VC firms, meets with YC companies as early as possible, partner Kristina Simmons tells TechCrunch, even scheduling interviews with companies in the period between when a startup is accepted to YC to before they actually begin the program. Another Khosla partner, Evan Moore, echoed Seibel’s statement, claiming there isn’t a correlation between the future unicorns and those that raise capital ahead of Demo Day. Moore is a co-founder of DoorDash, a YC graduate now worth $7.1 billion. DoorDash closed its first round of capital in the weeks following Demo Day.

“I think a lot of the activity before demo day is driven by investor FOMO,” Moore wrote in an email to TechCrunch. “I’ve had investors ask me how to get into a company without even knowing what the company does! I mostly see this as a side effect of a good thing: YC has helped tip the scale toward founders by creating an environment where investors compete. This dynamic isn’t what many investors are used to, so every batch some complain about valuations and how easy the founders have it, but making it easier for ambitious entrepreneurs to get funding and pursue their vision is a good thing for the economy.”

This year, given the number of recent changes at YC — namely the size of its latest batch — there was added pressure on the accelerator to showcase its best group yet. And while some did tell TechCrunch they were especially impressed with the lineup, others indeed expressed frustration with valuations.

Many YC startups are fundraising at valuations at or higher than $10 million. For context, that’s actually perfectly in line with the median seed-stage valuation in 2018. According to PitchBook, U.S. startups raised seed rounds at a median post-valuation of $10 million last year; so far this year, companies are raising seed rounds at a slightly higher post-valuation of $11 million. With that said, many of the startups in YC’s cohorts are not as mature as the average seed-stage company. Per PitchBook, a company can be several years of age before it secures its seed round.

I did not talk to a single company in this batch raising under $10M post (admittedly I only was able to speak with a fraction of the 205).

— Peter Rojas (@peterrojas) March 20, 2019

Nonetheless, pricey deals can come as a disappointment to the seed investors who find themselves at YC every year but because their reputations aren’t as lofty as say, Accel, aren’t able to book pre-Demo Day meetings with YC’s top of class.

The question is who is Y Combinator serving? And the answer is founders, not investors. YC is under no obligation to serve up deals of a certain valuation nor is it responsible for which investors gain access to its best companies at what time. After all, startups are raking in larger and larger rounds, earlier in their lifespans; shouldn’t YC, a microcosm for the Silicon Valley startup ecosystem, advise their startups to charge the best investors the going rate?

Powered by WPeMatico

I spent the week at SXSW, Austin’s really, really huge technology, music, comedy and film festival. It’s my first year making the trek down here for the event, which I did to interview sextech entrepreneur Lora DiCarlo founder Lora Haddock, whose robotics innovation reward was infamously revoked at this year’s CES.

“I brush my teeth and I masturbate. It’s all normal,” she said, addressing the stigma surrounding female-focused pleasure tech. Haddock, during our chat, also announced the first-ever government grant for a sextech startup, a $99,637 funding for Lora DiCarlo from the state of Oregon. Lora DiCarlo plans to release its first product, the Osé, this fall.

Here’s what happened while I was wondering confused around Austin.

Uber dominated the news cycle this week; here’s the TL;DR. The ride-hailing company is probably, most likely going to unveil its S-1 next month and it’s tying up some loose ends ahead of its big IPO. Uber wants to raise roughly $1 billion at a valuation of between $5 billion and $10 billion for its autonomous vehicles unit — yes, the same one that was burning through $20 million per month. Waymo, similarly, is looking to raise outside capital for the first time for its AV efforts.

Top TPG dealmaker caught in college admissions scandal

Bill McGlashan, who built his career as a top investor at the private equity firm TPG, was fired (or maybe quit?) says the firm after he was caught up in what the Justice Department said is the largest college admissions scandal it has ever prosecuted. Even worse, McGlashan lead TPG’s social impact strategy under the Rise Fund brand, making the charges particularly damning.

HotelTonight and Slack stakeholder Accel raised $2.525 billion, sources confirm to TechCrunch; $525 million for its fourteenth early-stage fund, $1.5 billion for its fifth growth fund and $500 million for its second Leaders Fund, or a dedicated pool of capital meant to help the firm strengthen its positions on particularly competitive bets. Plus, 137 Ventures announced its fourth fund with $210 million in committed capital. The firm provides liquidity to founders and early employees of “sustainable, fast-growing, private companies.” In essence, 137 Ventures buys shares directly from employees at unicorn tech companies, like Palantir, Flexport and Airbnb.

Last week, we reported Y Combinator president Sam Altman would be stepping down to focus on OpenAI. TechCrunch’s Connie Loizos questions whether he had a positive or negative influence on the accelerator during his presidency. Altman was part of the first YC startup class in 2005 and began working part-time as a YC partner in 2011. He was ultimately made the head of the organization five years ago.

Brian O’Malley’s HotelTonight win

Forerunner Ventures general partner Brian O’Malley went long on HotelTonight and it paid off. For your weekend reading, we thought you might enjoy an oral history from O’Malley about how he stumbled upon HotelTonight and remained connected to the company across its nine-year history.

In an announcement that shocked VC Twitter, Tiger Global announced that Lee Fixel, whom Bill Gurley once said is one of the smartest investors on the scene, is leaving the firm at the end of June. Scott Shleifer and Chase Coleman will continue as co-managers of the portfolios Fixel has overseen, with Shleifer taking over as its head. “Lee has been a driving force behind the expansion of Tiger Global’s private equity investing activities in the United States and India, and he has distinguished himself as a world-class investor across multiple sectors and stages,” the firm stated. And on the hiring front, Canvas Ventures is expanding its team of three general partners to four with the hiring of Mike Ghaffary, a former general partner at Social Capital.

Subscribers to TechCrunch’s premium content can learn which types of startups are most often profitable.

YC demo days are coming up quick. The TechCrunch staff has been meeting with YC startups and documenting their journey through the startup accelerator. I spoke to YourChoice Therapeutics, a startup developing unisex, non-hormonal birth control, and Bottomless, which operates a direct-to-consumer coffee delivery service. TechCrunch’s Lucas Matney wrote about Jetpack Aviation, a YC startup, and its $380,000 flying motorcycle, and Adventurous, an augmented reality scavenger hunt crafted for families. TechCrunch’s Megan Rose Dickey spoke to Ysplit, which wants to make it so you never have to owe anyone money ever again.

This week on Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines, Crunchbase News’ editor-in-chief Alex Wilhelm and TechCrunch’s Connie Loizos discuss Uber’s IPO and Stash’s big round. Listen here.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

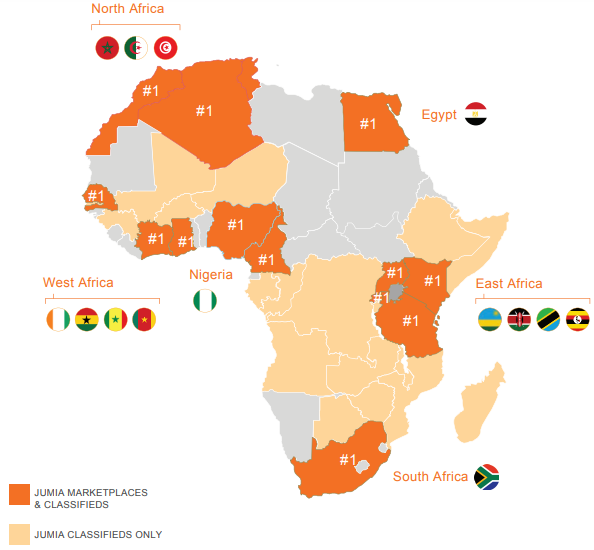

Pan-African e-commerce company Jumia filed for an IPO on the New York Stock Exchange today, per SEC documents and confirmation from CEO Sacha Poignonnec to TechCrunch.

The valuation, share price and timeline for public stock sales will be determined over the coming weeks for the Nigeria-headquartered company.

With a smooth filing process, Jumia will become the first African tech startup to list on a major global exchange.

Poignonnec would not pinpoint a date for the actual IPO, but noted the minimum SEC timeline for beginning sales activities (such as road shows) is 15 days after submitting first documents. Lead adviser on the listing is Morgan Stanley .

There have been numerous press reports on an anticipated Jumia IPO, but none of them confirmed by Jumia execs or an actual SEC, S-1 filing until today.

Jumia’s move to go public comes as several notable consumer digital sales startups have faltered in Nigeria — Africa’s most populous nation, largest economy and unofficial bellwether for e-commerce startup development on the continent. Konga.com, an early Jumia competitor in the race to wire African online retail, was sold in a distressed acquisition in 2018.

With the imminent IPO capital, Jumia will double down on its current strategy and regional focus.

“You’ll see in the prospectus that last year Jumia had 4 million consumers in countries that cover the vast majority of Africa. We’re really focused on growing our existing business, leadership position, number of sellers and consumer adoption in those markets,” Poignonnec said.

The pending IPO creates another milestone for Jumia. The venture became the first African startup unicorn in 2016, achieving a $1 billion valuation after a $326 funding round that included Goldman Sachs, AXA and MTN.

Founded in Lagos in 2012 with Rocket Internet backing, Jumia now operates multiple online verticals in 14 African countries, spanning Ghana, Kenya, Ivory Coast, Morocco and Egypt. Goods and services lines include Jumia Food (an online takeout service), Jumia Flights (for travel bookings) and Jumia Deals (for classifieds). Jumia processed more than 13 million packages in 2018, according to company data.

Starting in Nigeria, the company created many of the components for its digital sales operations. This includes its JumiaPay payment platform and a delivery service of trucks and motorbikes that have become ubiquitous with the Lagos landscape.

Starting in Nigeria, the company created many of the components for its digital sales operations. This includes its JumiaPay payment platform and a delivery service of trucks and motorbikes that have become ubiquitous with the Lagos landscape.

Jumia has also opened itself up to traders and SMEs by allowing local merchants to harness Jumia to sell online. “There are over 81,000 active sellers on our platform. There’s a dedicated sellers page where they can sign-up and have access to our payment and delivery network, data, and analytic services,” Jumia Nigeria CEO Juliet Anammah told TechCrunch.

The most popular goods on Jumia’s shopping mall site include smartphones (priced in the $80 to $100 range), washing machines, fashion items, women’s hair care products and 32-inch TVs, according to Anammah.

E-commerce ventures, particularly in Nigeria, have captured the attention of VC investors looking to tap into Africa’s growing consumer markets. McKinsey & Company projects consumer spending on the continent to reach $2.1 trillion by 2025, with African e-commerce accounting for up to 10 percent of retail sales.

Jumia has not yet turned a profit, but a snapshot of the company’s performance from shareholder Rocket Internet’s latest annual report shows an improving revenue profile. The company generated €93.8 million in revenues in 2017, up 11 percent from 2016, though its losses widened (with a negative EBITDA of €120 million). Rocket Internet is set to release full 2018 results (with updated Jumia figures) April 4, 2019.

Jumia’s move to list on the NYSE comes during an up and down period for B2C digital commerce in Nigeria. The distressed acquisition of Konga.com, backed by roughly $100 million in VC, created losses for investors, such as South African media, internet and investment company Naspers .

In late 2018, Nigerian online sales platform DealDey shut down. And TechCrunch reported this week that consumer-focused venture Gloo.ng has dropped B2C e-commerce altogether to pivot to e-procurement. The CEO cited better unit economics from B2B sales.

In late 2018, Nigerian online sales platform DealDey shut down. And TechCrunch reported this week that consumer-focused venture Gloo.ng has dropped B2C e-commerce altogether to pivot to e-procurement. The CEO cited better unit economics from B2B sales.

As demonstrated in other global startup markets, consumer-focused online retail can be a game of capital attrition to outpace competitors and reach critical mass before turning a profit. With its unicorn status and pending windfall from an NYSE listing, Jumia could be better positioned than any venture to win on e-commerce at scale in Africa.

Powered by WPeMatico

It takes a lot more than a good idea and the right timing to build a billion-dollar company. Talent, focus, operational effectiveness and a healthy dose of luck are all components of a successful tech startup. Many of the most successful (or, at least, highest-valued) tech unicorns today didn’t get there alone.

Mergers and acquisitions (M&A) can be a major growth vector for rapidly scaling, highly valued technology companies. It’s a topic that we’ve covered off and on since the very first post on Crunchbase News in March 2017. Nearly two years later, we wanted to revisit that first post because things move quickly, and there is a new crop of companies in the unicorn spotlight these days. Which ones are the most active in the M&A market these days?

Before displaying the U.S. unicorns with the most acquisitions to date, we first have to answer the question, “What is a unicorn?” The term is generally applied to venture-backed technology companies that have earned a valuation of $1 billion or more. Crunchbase tracks these companies in its Unicorns hub. The original definition of the term, first applied in a VC setting by Aileen Lee of Cowboy Ventures back in late 2011, specifies that unicorns were founded in or after 2003, following the first tech bubble. That’s the working definition we’ll be using here.

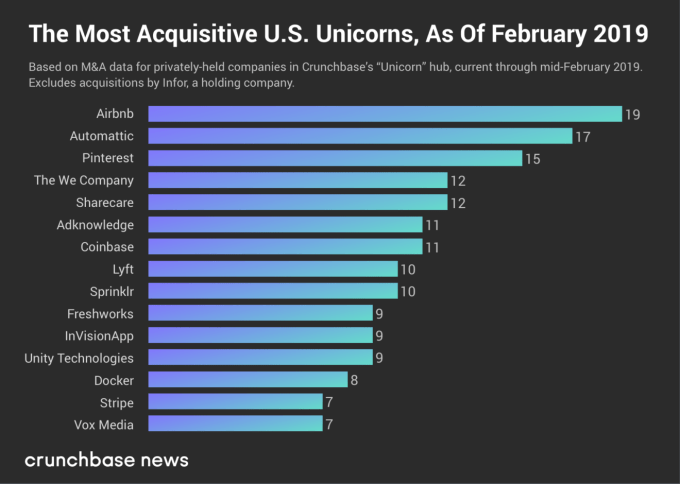

In the chart below, we display the number of known acquisitions made by U.S.-based unicorns that haven’t gone public or gotten acquired (yet). Keep in mind this is based on a snapshot of Crunchbase data, so the numbers and ranking may have changed by the time you read this. To maintain legibility and a reasonable size, we cut off the chart at companies that made seven or more acquisitions.

As one would expect, these rankings are somewhat different from the one we did two years ago. Several companies counted back in early March 2017 have since graduated to public markets or have been acquired.

Dropbox, which had acquired 23 companies at the time of our last analysis, went public weeks later and has since acquired two more companies (HelloSign for $230 million in late January 2019 and Verst for an undisclosed sum in November 2017) since doing so. SurveyMonkey, which went public in September 2018, made six known acquisitions before making its exit via IPO.

Which companies are still in the top ranks? Travel accommodations marketplace giant Airbnb jumped from number four to claim Dropbox’s vacancy as the most acquisitive private U.S. unicorn in the market. Airbnb made six more acquisitions since March 2017, most recently Danish event space and meeting venue marketplace Gaest.com. The still-pending deal was announced in January 2019.

WordPress developer and hosting company Automattic is still ranked number two. Automattic href=”https://www.crunchbase.com/acquisition/automattic-acquires-atavist–912abccd”>acquired one more company — digital publication platform Atavist — since we last profiled unicorn M&A. Open-source software containerization company Docker, photo-sharing and search site Pinterest, enterprise social media management company Sprinklr and venture-backed media company Vox Media remain, as well.

There are some notable newcomers in these rankings. We’ll focus on the most notable three: The We Company, Coinbase and Lyft. (Honorable mention goes to Stripe and Unity Technologies, which are also new to this list.)

The We Company (the holding entity for WeWork) has made 10 acquisitions over the past two years. Earlier this month, The We Company bought Euclid, a company that analyzes physical space utilization and tracks visitors using Wi-Fi fingerprinting. Other buyouts include Meetup (a story broken by Crunchbase News in November 2017) reportedly for $200 million. Also in late 2017, The We Company acquired coding and design training program Flatiron School, giving the company a permanent tenant in some of its commercial spaces.

In its bid to solidify its position as the dominant consumer cryptocurrency player, Coinbase has been on quite the M&A tear lately. The company recently announced its plans to acquire Neutrino, a blockchain analytics and intelligence platform company based in Italy. As we covered, Coinbase likely made the deal to improve its compliance efforts. In January, Coinbase acquired data analysis company Blockspring, also for an undisclosed sum. The crypto company’s other most notable deal to date was its April 2018 buyout of the bitcoin mining hardware turned cryptocurrency micro-transaction platform Earn.com, which Coinbase acquired for $120 million.

And finally, there’s Lyft, the more exclusively U.S.-focused ride-hailing and transportation service company. Lyft has made 10 known acquisitions since it was founded in 2012. Its latest M&A deal was urban bike service Motivate, which Lyft acquired in June 2018. Lyft’s principal rival, Uber, has acquired six companies at the time of writing. Uber bought a bike company of its own, JUMP Bikes, at a price of $200 million, a couple of months prior to Lyft’s Motivate purchase. Here too, the Lyft-Uber rivalry manifests in structural sameness. Fierce competition drove Uber and Lyft to raise money in lock-step with one another, and drove M&A strategy as well.

With long-term business success, it’s often a chicken-and-egg question. Is a company successful because of the startups it bought along the way? Or did it buy companies because it was successful and had an opening to expand? Oftentimes, it’s a little of both.

The unicorn companies that dominate the private funding landscape today (if not in the number of deals, then in dollar volume for sure) continue to raise money in the name of growth. Growth can come the old-fashioned way, by establishing a market position and expanding it. Or, in the name of rapid scaling and ostensibly maximizing investor returns, M&A provides a lateral route into new markets or a way to further entrench the status quo. We’ll see how that strategy pays off when these companies eventually find the exit door .

Powered by WPeMatico

Unlike 2000 and 2008, everyone in the startup world is expecting a crash to come at any moment. But few are taking concrete steps to prepare for it.

If you’re running a venture-backed startup, you should probably get on that. First, go read RIP Good Times from Sequoia to get a sense for how bad it can get, quickly. Then take a look at the checklist below. You don’t need to build a bomb shelter, yet, but adopting a bit of the prepper mentality now will pay dividends down the road.

The first step in preparing for a coming downturn is making a plan for how you’d get to a point of sustainability. Many startups have been lulled into a false sense of confidence that profit is something they can figure out “later.” Keep in mind, it has to be done eventually and it’s easier to do when the broader economy isn’t crashing around you. There are two complicating factors to keep in mind.

In a downturn, business customers skip investing in capital equipment and new software. Likewise, consumer discretionary spending goes way down. The result is you’ll likely have less revenue than you do now. War-game a variety of scenarios — what you’d do if you lost 20 percent, 50 percent or 80 percent of your revenue, and what decisions would have to be taken to survive.

When a downturn comes, capital markets don’t soften, they seize. Depending on how bad a hypothetical financial crisis got, there’s a good chance that investors would close up their checkbooks and triage. If you aren’t one of your investor’s favorite portfolio companies, there’s a decent chance you may be left in the cold. Don’t even assume you’ll be able to close a down round. Fortunately, showing a plan with a clear path to profitability will allay investors concerns that you’ll need their capital indefinitely and make it more likely you’ll be able to raise.

Planning around these three realities — the need for profits, while experiencing dropping revenue, in a world where capital can’t be had at any valuation — is going to lead to unpleasant conclusions. A dramatically diminished business, major layoffs, and a decisive drop in morale are likely outcomes. Thankfully, you can take steps now to help soften the landing, or if you’re really successful, avoid it entirely.

Getting acquisition costs under control will help you in two ways. First, it’ll lower your burn rate. Chasing growth for growth’s sake is always a short-sighted decision, but especially during the late part of the business cycle. Avoid this even if you’re VC is encouraging it. Second, by carefully analyzing the inputs to your acquisition cost, it will force you to examine the dynamics of your business. It gives you an opportunity to decide if a poorly performing channel or lackluster sales reps are actually smart investments. Even cutting your payback period from 12 months to nine will provide an increased measure of visibility and control.

Instagram took over the web with a team of a dozen. Craigslist is a pillar of the internet with a staff of 40 employees. WhatsApp supported hundreds of millions of daily users with fewer than 50 people. Chances are you need fewer people than you think.

In his new book, Scott Belsky shares an algorithm he used building Behance into a $100M company — automate, automate, then hire. His point was that founders should encourage teams to push hard on improving processes and other labor-saving tools before adding more FTEs.

Don’t institute a hiring freeze or take other actions that might spook the staff, but do send the message that new hires should be the last resort, not the first response to a challenge.

Founders often try to change spending habits, and in turn culture, when it’s too late. Is there a fair bit of business class flying among the executive team? Do your employees stretch your free dinner policy by staying just past the dinner hour to take advantage of free food? At most tech ventures, everyone is truly an owner. Try to help the entire team to internalize that they are spending their own money.

The week the market drops 50 percent is not the week to start a M&A conversation. You should be getting to know the five most likely buyers of your company, now. Find out who the decision makers at each of the companies are and build relationships. Make it a point to catch up with these people at conferences and even consider sending them regular updates about your company’s progress (but not too much data). You’re not running a formal sales process, but helping build up the internal desire to buy your company if the opportunity presents itself. It may not be the exit of your dreams, but it’s nice to have options if you need them.

If you’re coming to a T-juncture regarding office space, you may want to prioritize price and lease flexibility over quality and location. I remember one of our offices at my start-up was a twelve month lease with 6 months free. The landlords were desperate, and so were we!

If you’re in the kind of business that will support annual contracts, figure out a way to offer them. Pre-sell credits to consumers at a discount. More fundamentally, think about how you might be able to adjust your business model so you can get paid before you deliver services. Plenty of viable businesses are asphyxiated by delays in accounts receivable, don’t allow your ambitions to be thwarted by accounting.

One lesson learned in the 2000 bubble was that startups that serve other startups tend to be hit hardest. It’s important to think about how a downturn will impact your customer base. If more than 30 percent of your revenue comes from one industry (perhaps start-ups!), or heaven help you, a single customer, start thinking about managing risk by diversifying your customer base.

Topping up your balance sheet at this point isn’t a bad idea, provided you have the discipline to treat it as a rainy day fund. Communicate this rationale to your investors. It’s also important to use this moment to reflect on valuation. An eye-popping valuation will feel good when you sign the term sheet, but it’s going to feel like a millstone if the economy turns, and the market for blue-chip tech stocks drops precipitously.

Many VCs discourage venture debt. They’ll say “if you need more money, we’ll backstop you.” The problem is when things ugly, they may not be there. Debt providers are a good way to extend the runway. The thing is that it’s best to raise debt capital when you don’t need it. Venture debt can add ⅓ to ½ of additional capital to some funding rounds with minimal dilution and relatively modest interest rates. Do note that when things get bad, some debt funds can get aggressive so do your homework before taking the notes.

It’s tough to predict the top of the market. CNN, Time, The Atlantic, The Wall Street Journal, and many others argued Facebook paying $1 billion for Instagram was a sure sign of a bubble — in 2012. Reputable commentators have claimed that we’re in a bubble every year since, see 2013, 2014, 2015, 2016, 2017, and 2018. Going into survival mode in any of those years would have been a serious mistake for most startups.

Still, we’re only two quarters away from marking the longest economic expansion in US history. The good times have got to end at some point. Venture capital is a hell of a drug and withdrawal can be painful. Keep in mind that there’s no correlation between how much a company raised and how well they did on the public markets. If you’re struggling to make your startup’s economics work, read up on dozens of “invisible unicorns” who show that you can get big without relying on outsized amounts of venture capital.

If your house is in order when the downturn hits, you may actually be able to grow through it. As unprepared competitors go out of business, you’ll find that talent is more plentiful and customer acquisition costs plummet. Some of the best companies have been founded and thrived in the worst of times — if you’re prepared.

Powered by WPeMatico

Are more Theranos -style scandals looming for investors in healthcare startups?

A team of researchers associated with the Meta-Research Innovation Center at Stanford thinks so. They’ve published a paper warning investors in life sciences startups that a systemic lack of transparency exists in their portfolio companies — creating the possibility for more multi-billion-dollar implosions and scandals like the one that toppled Theranos and its charismatic founder, Elizabeth Holmes.

Indeed, one of the study’s authors, Dr. John Ioannidis, the co-director of the Meta-Research Innovation Center at Stanford and director of the University’s PhD program in Epidemiology and Clinical Research, was among the first people to identify the risks associated with Theranos and its “stealth research.”

Now Dr. Ioannidis and his co-authors, Ioana A. Cristea and Eli M. Cahan, have published a study surveying the publicly available research from the largest privately held companies in the healthcare space, and found them lacking.

Most of the highest-valued startups in healthcare have not published any significant scientific literature, the study found. Nearly half of the publications from companies worth more than $1 billion came from only two startups — 23andMe and Adaptive Biotechnologies, according to the paper.

“Many years ago I was the first person to say that Theranos had a problem,” says Ioannidis. “The problem that I had then was that Theranos did not have any peer-reviewed evidence to show.”

In an interview and in their paper, Ioannidis and Cahan warn that investors have overlooked systemic problems created by the lack of transparency among healthcare startups.

They write:

It would be tempting to dismiss the Theranos case as just one rotten apple. However, we worry that the focus on fraud puts aside a more fundamental concern. Fraud is making waves in the news, but stealth research may have a more detrimental impact.

According to the study’s findings, more than half of the healthcare startups that are worth more than $1 billion have published no highly cited papers at all. For companies that were acquired or are publicly traded that number is around 40 percent.

In all, healthcare startups that are currently valued at more than $1 billion published 425 Pubmed papers. And of those papers only 34 (8 percent, including two reviews) were highly cited. For companies with valuations of more than $1 billion that had been acquired or are publicly traded on stock exchanges, the researchers counted 413 papers, of which 47 (11 percent, including nine reviews) were highly cited.

Digging deeper into some of the companies that had high valuations but little or no published research revealed scores of operational and technological issues for the researchers.

For instance, StemCentrx, which was bought for $10.2 billion in 2016 by AbbVie, had published 16 papers — and only one highly cited paper. Since the acquisition, the Food and Drug Administration had imposed a delay on the readout of the company’s phase II trial for its Rova T targeted antibody drug for cancer treatment. In December, a Phase III trial for Rova T as a second-line treatment for patients with advanced small cell lung cancer was halted because the treatment wasn’t working, according to a report in Targeted Oncology.

Acerta Pharma, another healthcare-focused startup focused on cancer treatments, was bought by AstraZeneca for $7.3 billion. That company published nine articles and had one highly cited paper for a very early study of a potential treatment for relapsed chronic lymphocytic leukemia. Acerta received accelerated approval for a drug called acalabrutinib, which treats a rare form of lymphoma called mantle cell lymphoma. Two years ago, AstraZeneca had to retract data and admit that Acerta falsified preclinical data for its drug.

Then there’s Intarcia, the developer of a device for diabetes treatment that’s worth $5.5 billion. That company had its device rejected by the FDA and was forced to lay off staff and halt a couple of later-stage trials. It had only published six papers — none of them very highly cited.

Ultimately, the researchers concluded that highly valued healthcare startups don’t contribute to published research and that the valuation of these companies by investors is divorced from any externally validated data.

For the researchers (and for investors) this should present a problem.

“Many unicorns may be overvalued [21] and subject to unrealistic scientific expectations,” the study’s authors write. And they reject the argument that simply applying for — and receiving — patents is enough to prove that a technology in the healthcare space has been thoroughly vetted. “[Patents] do not offer the same level of documentation as peer-reviewed articles. For example, Theranos had over 100 patents [1], but these were unable to supplant the vacuum in their evidence,” the researchers wrote.

Even if companies want to protect their technology, there are still ways for them to be more transparent about the results or benefits of their technology. The authors acknowledge that publishing isn’t the primary mission of startups. They can, however publish a few high-value articles, secure their technology through patents and then work with researchers, universities or hospitals to validate the technology and have those organizations publish results of the tests, the authors argue.

As the authors conclude:

Start-ups are key purveyors of innovation and disruption. Consequently, holding them to a minimal standard of evaluation from the scientific community is crucial. Participation in peer review, with all its limitations, is the best way we have to uphold this standard. We are not arguing that start-ups should divert excessive resources to having peer-reviewed papers. However, when their products are destined to affect patient health, they should neither be solely doing marketing. Confidential data sharing with potential investors or regulators cannot replace more open scrutiny by the scientific community.

Powered by WPeMatico

We’re three weeks into January. We’ve recovered from our CES hangover and, hopefully, from the CES flu. We’ve started writing the correct year, 2019, not 2018.

Venture capitalists have gone full steam ahead with fundraising efforts, several startups have closed multi-hundred million dollar rounds, a virtual influencer raised equity funding and yet, all anyone wants to talk about is Slack’s new logo… As part of its public listing prep, Slack announced some changes to its branding this week, including a vaguely different looking logo. Considering the flack the $7 billion startup received instantaneously and accusations that the negative space in the logo resembled a swastika — Slack would’ve been better off leaving its original logo alone; alas…

On to more important matters.

Rubrik more than doubled its valuation

The data management startup raised a $261 million Series E funding at a $3.3 billion valuation, an increase from the $1.3 billion valuation it garnered with a previous round. In true unicorn form, Rubrik’s CEO told TechCrunch’s Ingrid Lunden it’s intentionally unprofitable: “Our goal is to build a long-term, iconic company, and so we want to become profitable but not at the cost of growth,” he said. “We are leading this market transformation while it continues to grow.”

Deal of the week: Knock gets $400M to take on Opendoor

Will 2019 be a banner year for real estate tech investment? As $4.65 billion was funneled into the space in 2018 across more than 350 deals and with high-flying startups attracting investors (Compass, Opendoor, Knock), the excitement is poised to continue. This week, Knock brought in $400 million at an undisclosed valuation to accelerate its national expansion. “We are trying to make it as easy to trade in your house as it is to trade in your car,” Knock CEO Sean Black told me.

While we’re on the subject of VCs’ favorite industries, TechCrunch cybersecurity reporter Zack Whittaker highlights some new data on venture investment in the industry. Strategic Cyber Ventures says more than $5.3 billion was funneled into companies focused on protecting networks, systems and data across the world, despite fewer deals done during the year. We can thank Tanium, CrowdStrike and Anchorfree’s massive deals for a good chunk of that activity.

Send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

I would be remiss not to highlight a slew of venture firms that made public their intent to raise new funds this week. Peter Thiel’s Valar Ventures filed to raise $350 million across two new funds and Redpoint Ventures set a $400 million target for two new China-focused funds. Meanwhile, Resolute Ventures closed on $75 million for its fourth early-stage fund, BlueRun Ventures nabbed $130 million for its sixth effort, Maverick Ventures announced a $382 million evergreen fund, First Round Capital introduced a new pre-seed fund that will target recent graduates, Techstars decided to double down on its corporate connections with the launch of a new venture studio and, last but not least, Lance Armstrong wrote his very first check as a VC out of his new fund, Next Ventures.

More money goes toward scooters

In case you were concerned there wasn’t enough VC investment in electric scooter startups, worry no more! Flash, a Berlin-based micro-mobility company, emerged from stealth this week with a whopping €55 million in Series A funding. Flash is already operating in Switzerland and Portugal, with plans to launch into France, Italy and Spain in 2019. Bird and Lime are in the process of raising $700 million between them, too, indicating the scooter funding extravaganza of 2018 will extend into 2019 — oh boy!

TechCrunch’s Josh Constine introduced readers to Squad this week, a screensharing app for social phone addicts.

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase editor-in-chief Alex Wilhelm and I marveled at the dollars going into scooter startups, discussed Slack’s upcoming direct listing and debated how the government shutdown might impact the IPO market.

Powered by WPeMatico

About 13 years ago I faced an excruciating decision: whether to sell my company, Pinnacle Systems, to a private equity firm or to another large public company. I felt that both suitors would treat my employees well (and I negotiated hard to make sure that was the case), and both offered a good asking price well above our value on NASDAQ.

After raising what at the time felt like my first child, born in my living room and nurtured into a publicly traded entity, I was ready for it to take its next step and for me to take mine. I ultimately opted for the strategic sale, but I left the process intrigued by what was already an evolving dynamic between private equity firms and tech exits.

In years past, stigma often accompanied private equity sales. I know I felt that way, even under strong deal terms. Plus, private equity exits were only available to companies generating substantial annual revenues and often profits, making this exit option inaccessible for many startups. Today, private equity buyout firms can provide a solid (and on occasion excellent) exit route — as well as an increasingly common one, accounting for 18.5 percent of VC-backed exits in 2017.

Private equity firms are investing in a broad array of technology companies, including highly valued unicorns, but also early- to mid-stage profitable and unprofitable companies that a few years ago would have been unable to secure interest from these buyout firms.

In addition, the lines between venture capital and private equity are increasingly blurring, with more private equity investments in tech, and several-late stage VC firms creating large, billion-dollar plus late-stage growth funds. Further blurring the lines, some of the late-stage VC firms are taking controlling interests in startups, a strategy typically associated with private equity. Recently, one of our portfolio companies received an investment from a late-stage VC firm that acquired a majority stake by providing liquidity to some existing shareholders and investing in the company, utilizing a strategy typically associated with PE buyout firms.

The rise of private equity buyouts within the tech sector presents a viable exit option for founders, given the reality that most startups won’t ultimately IPO. (According to PitchBook, only 3 percent of venture-backed companies in the last decade eventually went public.)

If an IPO is not a realistic long-term option, the remaining primary exit option has typically been a sale to another company (a strategic buyer, in venture parlance). However, in the past few years, private equity firms have become aggressive buyers of private companies, sometimes bidding as high as or higher than strategic buyers. With one of my portfolio companies, a private equity buyer placed the second highest bid ahead of all but one strategic buyer and helped raise the final price from the strategic buyer just by being in the bidding process.

Founders who find themselves in negotiations with strategic buyers should also reach out to PE firms to optimize the outcome. Silver Lake, Francisco Partners, Thoma Bravo and Vista are a few technology-focused PE firms, and PitchBook’s annual liquidity report lists other firms. Vista has been especially active, acquiring many technology companies, including Infoblox, Lithium and Marketo. Not all PE firms are the same, just like not all VCs and strategic buyers are the same.

Years ago, when private equity buyouts were typically only large deals, new management teams were almost always brought in to tweak the edges of already successful companies. Today, each private equity firm has its own strategy — some only buy large profitable companies, others focus on mid-size acquisitions and some only buy early-stage (typically unprofitable) companies, which brings us to the next point.

Even early-stage startups can explore a PE exit, especially if things are not going well

While most readers are familiar with private equity buyers at later stages, what’s new is the emergence of PE activity at early stages. These firms acquire majority stakes in startups that have only raised early-stage investments but are having trouble scaling or raising the next round.

After a buyout, these private equity firms typically provide value by adding the missing elements, such as marketing or sales know-how, in order to kick-start the business and achieve scale. Their goal is to increase the value of the underlying asset by augmenting founder teams with the buyout firm’s own operational experts, sometimes combining newly acquired assets with already existing assets to create a stronger whole, or doubling-down on promising products (while shedding less promising offerings) to unlock potential.

Typically, these PE firms then sell the company to another company (usually a strategic buyer) for greater value. In some cases, these early-stage PE firms sell to another PE buyout firm further up market. In some of these acquisitions, founders can maintain minority ownership in the company (though not a controlling stake), which they can carry through to their “next exit.”

Unlike PE buyouts at later stages, PE buyouts at the earlier stages are not usually high-value exits; they are mostly an avenue to provide the founders some return for their hard work, rather than the disappointing returns they can expect from an acqui-hire or, even worse, a shutdown. If negotiated correctly, a private equity deal can give founders an opportunity to play another hand to the next exit.

Few founders create companies in order to flip them. Strong entrepreneurs create companies to transform their missions into reality and positively impact the world. Steve Jobs said, “I’m convinced that about half of what separates the successful entrepreneurs from the non-successful ones is pure perseverance.” An acquisition — particularly to private equity — may not have been the original goal, but it may fuel the continued pursuit of the founder’s mission. Or, perhaps it will enable the pursuit of a new and worthy mission.

Powered by WPeMatico

")

There’s been plenty of fanfare surrounding Uber and Lyft’s initial public offerings — slated for early 2019 — since the two companies filed confidential IPO paperwork with the U.S. Securities and Exchange Commission in early December. On top of that, public and private investors have had plenty to say about Slack and Pinterest’s rumored 2019 IPOs but those aren’t the only “unicorn” exits we should expect to witness in the year ahead.

Using its proprietary company rating algorithm, data provider CB Insights ranked five billion dollar companies most likely to perform IPOs next year in its latest tech IPO report. The algorithm analyzes non-traditional public signals, including hiring activity, web traffic and mobile app data to make its predictions. These are the startups that topped their list.

Peloton Co-Founder and CEO John Foley speaks onstage during TechCrunch Disrupt SF 2018 on September 6, 2018 in San Francisco, California. (Photo by Kimberly White/Getty Images for TechCrunch).

Peloton, dubbed the “Netflix of fitness,” has raised nearly $1 billion in venture capital funding in the six years since it was founded by John Foley, most recently raising $550 million at a $4 billion valuation. The manufacturer of tech-enabled exercise equipment is more than doubling in size every year and is “weirdly profitable,” an unusual characteristic for a venture-backed business of its age. Headquartered in New York, Peloton doesn’t have any public IPO plans, though Foley recently told The Wall Street Journal that 2019 “makes a lot of sense” for its stock market debut.

Select investors: L Catterton, True Ventures, Tiger Global

Cloudflare co-founder and CEO Matthew Prince appears on stage at the 2014 TechCrunch Disrupt Europe/London. (Photo by Anthony Harvey/Getty Images for TechCrunch)

Cybersecurity unicorn Cloudflare is likely to transition to the public markets in the first half of 2019 in what is poised to be a strong year for IPOs in the security industry. The web performance and security platform is said to be preparing for an IPO at a potential valuation of more than $3.5 billion after last raising capital in 2015 at a $1.8 billion valuation. Since it was founded in 2009, the San Francisco-based company has raised just north of $250 million in VC funding. CrowdStrike, another security unicorn, is also on track to go public next year and it wouldn’t be surprising to see Illumio and Lookout make the jump to the public markets as well.

Select investors: Pelion Venture Partners, NEA, Venrock

San Jose-based Zoom Video Communications has reportedly tapped Morgan Stanley to lead its upcoming IPO.

Zoom, a provider of video conferencing services, online meeting and group messaging tools that’s raised $160 million in VC cash to date, is eyeing a multi-billion IPO in 2019 and has reportedly hired Morgan Stanley to lead the offering. Founded in 2011, the company most recently brought in a $100 million Series D financing, entirely funded by Sequoia, at a $1 billion valuation in early 2017. Based in San Jose, Zoom is hoping to garner a valuation significantly larger than $1 billion when it IPOs, according to Reuters.

Select investors: Sequoia, Emergence Capital Partners, Horizons Ventures

Data management company Rubrik co-founder and CEO Bipul Sinha.

Data management company Rubrik has quietly made moves indicative of an impending IPO. The startup, which provides data backup and recovery services for businesses across cloud and on-premises environments, hired former Atlassian chief financial officer Murray Demo as its CFO earlier this year, as well as its first chief legal officer, Peter McGoff. Palo Alto-based Rubrik was valued at over of $1 billion with a $180 million funding round in 2017. The company has raised nearly $300 million to date.

Select investors: Lightspeed Venture Partners, Greylock, Khosla Ventures

Medallia, a customer experience management platform that’s nearly two decades old, may finally become a public company in 2019. The San Mateo-based company, which has been rumored to be planning an IPO for several years, hired a new CEO this year and reported $250 million in GAAP revenue for the year ending Jan. 31, 2018, according to Forbes. Medallia hasn’t raised capital since 2015, when it secured a $150 million funding deal at a $1.2 billion valuation. It has raised a total of just over $250 million.

Select investor: Sequoia

Powered by WPeMatico

The second wave of Internet-era travel companies has captured the attention of venture capitalists.

In the last five years, travel companies have raised more than $1 billion in venture capital funding. That includes short-term rental startups, travel and tourism apps, marketplaces for “experiences” and other travel or hospitality tech platforms. Airbnb, a $38 billion company and an anomaly in the category, has raised $3 billion in that same time frame, according to PitchBook.

In the last few months alone, aspiring Concur-competitor TripActions and travel activities platform Klook entered the “unicorn” club with large venture rounds that valued both of the businesses at more than $1 billion. Meanwhile, luggage maker Away raised $50 million at a $400 million valuation and smaller startups in the space like Freebirds, IfOnly, KKDay, Duffel and RedDoorz all closed modest funding rounds.

“Something is really happening in the industry; something bigger than us,” TripActions co-founder Ariel Cohen said in a recent conversation with TechCrunch about his company’s $154 million Series C financing. “Different startups are identifying the opportunity here and the fact that companies want to make sure their employees are happy while they are on the go. That’s why you see investments in companies like Brex and like TripActions.”

Brex, though not classified as a travel startup, lets startup employees earn extra points on business travel with its corporate credit card for startups. It recently raised a $125 million Series C at a $1.1 billion valuation.

Global travel and tourism is one of the most valuable industries worth some $7 trillion. The online travel market, in particular, is expected to grow to $817 billion by 2020. VCs are hunting for tech-enabled startups poised to dominate that slice.

“You have a new wave of businesses where all of that digital infrastructure is set up, so the focus can be on things like efficiency, improved customer service, scale and growth — you have a ton of companies popping up catering to those needs,” Defy Partners co-founder Neil Sequeira told TechCrunch. Sequeira was a managing director at General Catalyst when the firm made its first investment in Airbnb.

On the other hand, you have a whole cohort of travel business founded amid the dot-com boom that are looking to technology startups for a much-needed infusion of innovation. Many of those larger companies have become active acquirers, fueling VC interest in the space. SAP Concur, for example, acquired the formerly VC-backed travel-booking startup Hipmunk in 2016. Before that, it bought travel planning company TripIt for $120 million, among others.

Expedia has gobbled up a number of travel brands too, like travel photography community Trover; Airbnb-competitor HomeAway, which it paid a whopping $3.9 billion for in 2015; and most recently, both Pillow and ApartmentJet.

Many of these acquisitions are for peanuts, which is far from ideal for a venture-funded company. And building a travel business is cash intensive, hence the $4.4 billion Airbnb has raised to date or even TripActions’ $236 million in total VC funding. To keep momentum in the space, companies need to be striking larger M&A deals.

It doesn’t help that many in and around the venture capital industry are predicting an imminent turn in the market. Travel companies, which are reliant upon a consumer’s tendency to spend excess cash, will be among the first sectors to be impacted by hostile economic conditions.

“If the market turns, people aren’t going to spend $10,000 on a trip to Zimbabwe,” Sequeira said, referencing companies like IfOnly, which sells curated experiences.

Travel startups should raise now while the market is hot. The conditions may not remain favorable for long.

Powered by WPeMatico