unicorn

Auto Added by WPeMatico

Auto Added by WPeMatico

China is becoming a superpower in the tech industry. According to Straits Times, China is the only place in the world where it takes less than six years for a startup to become a unicorn — it takes seven years in the U.S., eight years in the U.K. and 11 years in Germany. Despite geopolitical tensions and recent amendments in CFIUS, it is hard to ignore China.

When I joined Runa Capital almost a year ago, my task was to help our portfolio companies enter the Chinese market, find the right partners and raise funding from Chinese investors. And almost on every call with our startups, colleagues from Runa or other global VCs, I heard: Is it a good idea to raise from a Chinese VC? Is it OK to co-invest with Chinese investors? I was surprised to learn that there is little research answering such questions, as there is a lack of adequate information in English about Chinese investments.

Access to the Chinese market seems to be an obvious reason to invite Chinese funds aboard, but only about 20% of Western startups with Chinese capital have operations in China.

So as a Mandarin-speaking specialist, I decided to fill this gap by conducting a study based on Chinese VC database ITjuzi (the Chinese version of Crunchbase) with the help of our powerful data science resources developed by Danil Okhlopkov.

Below, I will try to answer the following questions using statistics and a case-based approach:

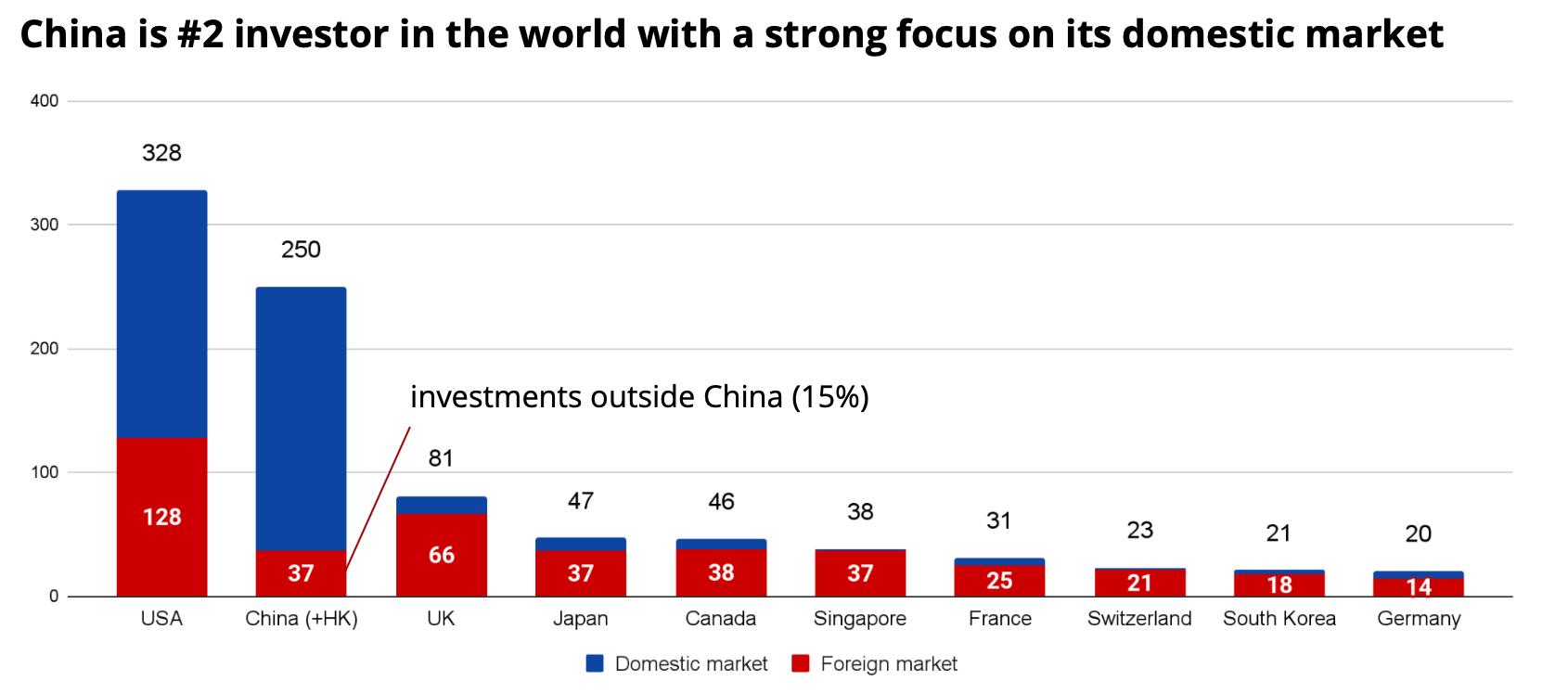

After studying data from ITjuzi, we estimated that Chinese funds invested around $250 billion in 2020 (three times higher than the figure reported in Crunchbase). This figure puts Chinese VC investments only 30% lower than investments by U.S. funds, but three times that of U.K. funds and 12.5 times more than German funds.

Fig. 1 — Comparison of investment from different countries in 2020, $bn. Source: Crunchbase, ITjuzi. Image Credits: Denis Kalinin

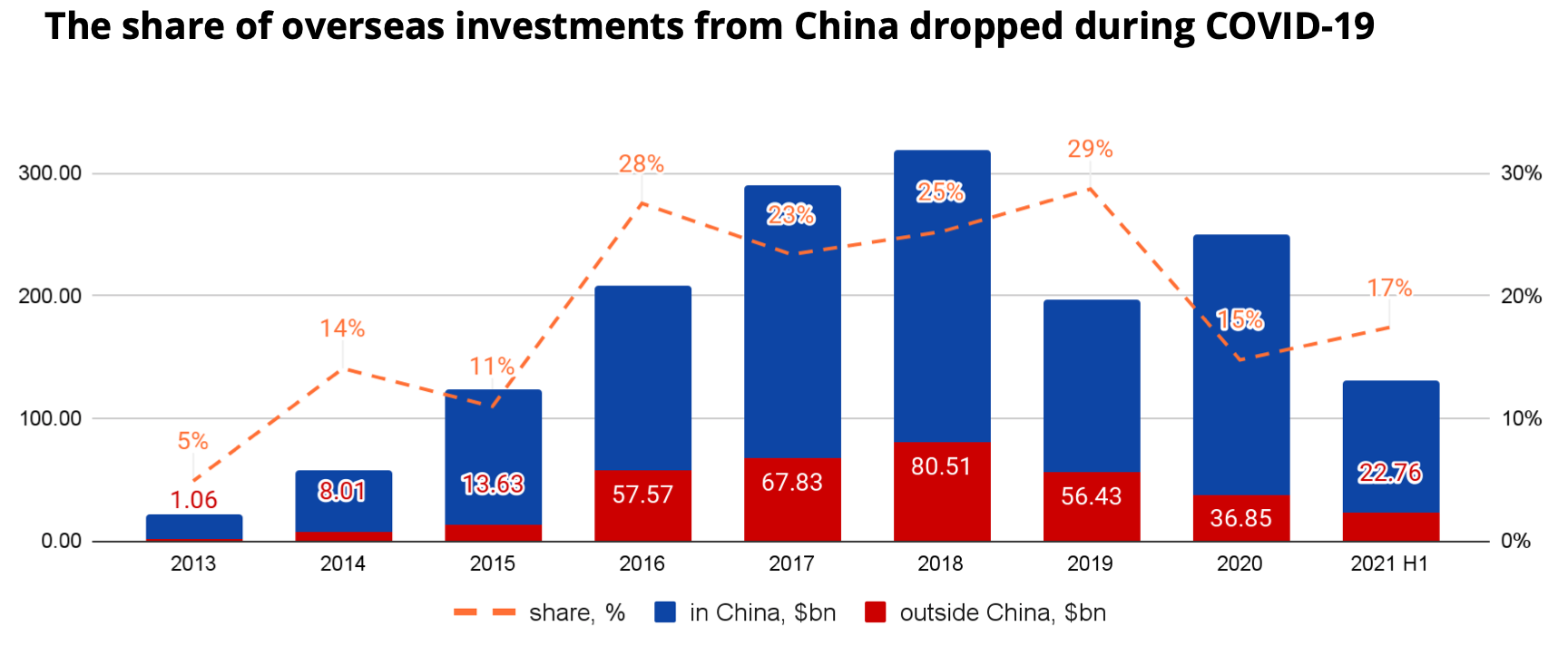

However, only 15% of investments in 2020 and 17% of investments in the first half of 2021 were in companies outside China, significantly lower than in 2019. This appears to be because during COVID, China’s economy recovered much faster than other countries’, so many Chinese investors preferred to redirect their capital flows to the domestic market.

On the other hand, there is great potential for overseas investments to rebound as soon as the borders reopen and the global economy starts to recover.

Fig. 2 — Dynamics of Chinese investments. $bn. Source: Crunchbase, ITjuzi. Image Credits: Denis Kalinin

We can also see that Chinese investors are eyeing European startups favorably, which is related to U.S.-China geopolitical tensions as well as the fact that the European VC market is becoming mature.

Powered by WPeMatico

Marshmallow — a U.K.-based car insurance provider that has made a name for itself in the market by providing a new approach to car insurance aimed at using a wider set of data points and clever algorithms to net a more diverse set of customers and provide more competitive rates — is announcing a milestone today in its life as a startup, as well as in the bigger U.K. tech world.

The London company — co-founded by identical twins Oliver and Alexander Kent-Braham and David Goaté — has raised $85 million in a new round of funding. The Series B valuation is significant on two counts: it catapults Marshmallow to a “unicorn” valuation above $1 billion — specifically, $1.25 billion; and Marshmallow itself becomes one of a very small group of U.K. startups founded by Black people — Oliver and Alexander — to reach that figure.

(To be clear, Marshmallow describes itself as “the first UK unicorn to be founded by individuals that are Black or have Black heritage”, although I can think of at least one that preceded it: WorldRemit, which last month rebranded to Zepz, and is currently valued at $5 billion; co-founder and chairman Ismail Ahmed has been described as the most influential Black Briton.)

Regardless of whether Marshmallow is the first or one of the first, given the dearth of diversity in the U.K. technology industry, in particular in the upper ranks of it, it’s a notable detail worth pointing out, even as I hope that one day it will be less of a rarity.

Meanwhile, Marshmallow’s novel, big-data approach and successful traction in the market speak for themselves. When we covered the company’s most recent funding round before this — a $30 million raise in November 2020 — the startup was valued at $310 million. Now less than a year later, Marshmallow’s valuation has nearly quadrupled, and it has passed 100,000 policies sold in its home country, growing 100% over the last six months.

The plan now, Oliver told me in an interview, will be to deepen its relationships with customers, in part by providing more engagement to make them better drivers, but also potentially selling more services to them, too.

In this, the startup will be tapping into a new approach that other insurtech startups are taking as they rethink traditional insurance models, much like YuLife is positioning its life insurance products within a bigger wellness and personal improvement business. Currently, the average age of Marshmallow’s customers is 20 to 40, Oliver said — and there are thoughts of potentially new products aimed at even younger users. That means there is long-term value in improving loyalty and keeping those customers for many years to come.

Alongside that, Marshmallow will also use the funding to inch closer to its plan to expand to markets outside of the U.K. — a strategy that has been in the works for a while. Marshmallow talked up international expansion in its last round but has yet to announce which markets it will seek to tackle first.

Insurance — and in particular insurance startups — are often thought of together with fintech startups, not least because the two industries have a lot in common: they both operate in areas of assessing and mitigating risk and fraud; they are in many cases discretionary investments on the part of the customers; and they are both highly regulated and require watertight data protection for their users.

Perhaps because so much of the hard work is the same for both, it’s not uncommon to see services built to serve both sectors (FintechOS and Shift Technology being two examples), for fintech companies to dabble in insurance services, and so on.

But in reality, insurance — and specifically car insurance — has seen a massive impact from COVID-19 unique to that industry. Separate reports from EY and the Association of British Insurers noted that 2020 actually saw a lift for many car insurance companies: lockdowns meant that fewer people were driving, and therefore fewer were getting into accidents and making fewer claims.

2021, however, has been a different story: new pricing rules being put into place will likely see a number of providers tip into the red for the year. And the Chartered Insurance Institute points out that it will also be worth watching to see how the low use of cars in one year will impact use going forward: some car owners, especially in urban areas where keeping a car is expensive, will inevitably start to question whether they need to own and insure a car at all.

All of this, ironically, actually plays into the hand of a company like Marshmallow, which is providing a more flexible approach to customers who might otherwise be rejected by more traditional companies, or might be priced out of offerings from them. Interestingly, while neobanks have definitely spurred more traditional institutions to try to update their products to compete, the same hasn’t really happened in insurance — not yet, at least.

“We started with the idea of the power of data and using a wider range of resources [than incumbents], and using that in our pricing led us to be able to offer better rates to more people,” Oliver said, but that hasn’t led to Marshmallow seeing sharper competition from older incumbents. “They are big companies and stuck in their ways. These companies have been around for decades, some for centuries. Change is not happening quickly.”

That leaves a big opportunity for companies like Marshmallow and other newer players like Lemonade, Hippo and Jerry (not an insurance startup per se but also dabbling in the space), and a big opening for investors to back new ideas in an industry estimated to be worth $5 trillion.

“The traction the team has achieved demonstrates the demand for a new kind of insurance provider, one that focuses more on consumer experience and uses the latest technology and data to give fair prices,” said Eileen Burbidge, a partner at Passion Capital, in a statement. “We’ve been proud to support the team’s ambitions since the start, and now look forward to its next chapter in Europe as it continues its mission to change the industry for the better.”

Powered by WPeMatico

Singapore is home to fewer than six million people, making it one of the smallest ASEAN countries, in terms of population. It is a young country as well — having gained independence in 1963 — and resides in a neighborhood with far larger economies, including China, Indonesia, and Vietnam. When the country first became independent, its mandate was to simply survive rather than thrive.

So how does a country evolve from a position of relative uncertainty, with comparatively few resources, to one that leads the ASEAN region in venture capital investment and has been home to 10 unicorns?

Countries around the world examine Singapore’s ecosystem from a distance, hoping to learn from, and emulate, its story. The World Bank Group recently published a report, The Evolution and State of Singapore’s Start-up Ecosystem, documenting the country’s experience in building its startup ecosystem and the challenges facing it.

This article presents an overview of the report’s key findings and offers a few key recommendations on what other countries can learn from Singapore’s experience, as well as what Singapore itself can do to maintain progress.

As of 2019, Singapore had over $19 billion in PE and VC assets under management, more than twice that of neighboring Indonesia, Philippines, Vietnam, Malaysia, and Thailand combined. In that same year, the country was home to an estimated 3,600 tech startups and nearly 200 different intermediary and supporting organizations (accelerators, co-working spaces, coding academies, etc.) – some which have a multinational presence, such as Blk71, whose Singapore headquarters has been referred to as “the world’s most tightly packed entrepreneurial ecosystem.”

While assessing the size and strength of startup ecosystems is an evolving method, Start-up Genome priced Singapore’s ecosystem at over $25 billion, five times the global median.

Arguably, the most eye-catching hallmark of this ecosystem is its population of current and former unicorns. Collectively, Singapore has been home to ten unicorns, three of which have offered an IPO (Nanofilm, Razer and Sea) and two of which have been acquired – one by giant Alibaba (Lazada) and one by Chinese streaming powerhouse YY (Bigo Live). The remaining five are Trax, Acronis, JustCo, PatSnap, and Grab – the ASEAN region’s largest unicorn to date.

The education sector is also prominent in Singapore’s ecosystem. Universities like the National University of Singapore (NUS) and Nanyang Technological University (NTU) are deeply embedded into this ecosystem, helping with R&D commercialization linkages, incubation, talent/knowledge transfer, and other areas.

Numerous factors have contributed to building Singapore’s startup ecosystem, with government intervention and leadership being the dominant driving forces. The government has spent more than USD60 billion over the past several decades to enhance the country’s R&D infrastructure, create VC funds, and launch accelerators and other support organizations.

Powered by WPeMatico

Didi filed to go public in the United States last night, providing a look into the Chinese ride-hailing company’s business. This morning, we’re extending our earlier reporting on the company to dive into its numerical performance, economic health and possible valuation.

Recall that Didi has raised tens of billions worth of private capital from venture capitalists, private equity firms, corporations and other sources. The size of the bet riding on Didi is simply massive.

Didi is approaching the American public markets at a fortuitous moment. While the late-2020 IPO fervor, which sent offerings from DoorDash and others skyrocketing after their debuts, has cooled, valuations for public companies remain high compared to historical norms. And Uber and Lyft, two American ride-hailing companies, have been posting numbers that point to at least a modest recovery in the ride-hailing industry as COVID-19 abates in many parts of the world.

As further grounding, recall that Didi has raised tens of billions worth of private capital from venture capitalists, private equity firms, corporations and other sources. The size of the bet riding on Didi is simply massive. As we explore the company’s finances, then, we’re more than vetting a single company’s performance; we’re examining what sort of returns an ocean of capital may be able to derive from its exit.

In that vein, we’ll consider GMV results, revenue growth, historical profitability, present-day profitability and what Didi may be worth on the American markets, given current comps. Sound good? Into the breach!

Starting at the highest level, how quickly has gross transaction volume (GTV) scaled at the company?

Didi is historically a business that operates in China but has operations today in more than a dozen countries. The impact and recovery of China’s bout with COVID-19 is therefore not the whole picture of the company’s GTV results.

COVID-19 began to affect the company starting in the first quarter of 2020. From the Didi F-1 filing:

Core Platform GTV fell by 32.8% in the first quarter of 2020 as compared to the first quarter of 2019, and then by 16.0% in the second quarter of 2020 as compared to the second quarter of 2019.

The dips were short-lived, however, with Didi quickly returning to growth in the second half of the year:

Our businesses resumed growth in the second half of 2020, which moderated the impact on a year-on-year basis. Our Core Platform GTV for the full year 2020 decreased by 4.8% as compared to the full year 2019. Both our China Mobility and International segments were impacted, but whereas the GTV for our China Mobility segment decreased by 6.6% from 2019 to 2020, the GTV for our International segment increased by 11.4% from 2019 to 2020.

Holding to just the Chinese market, we can see how rapidly Didi managed to pick itself up over the last year. Chinese GTV at Didi grew from 25.7 billion RMB to 54.6 billion RMB from the first quarter of 2020 to the first quarter of 2021; naturally, we’re comparing a more pandemic-impacted quarter at the company to a less-affected period, but the comparison is still useful for showing how the company recovered from early-2020 lows.

The number of transactions that Didi recorded in China during the first quarter of this year was also up more than 2x year over year.

On a whole-company basis, Didi’s “core platform GTV,” or the “sum of GTV for our China Mobility and International segments,” posted numbers that are less impressive in growth terms:

Image Credits: Didi F-1 filing

You can see how quickly and painfully COVID-19 blunted Didi’s global operations. But seeing the company settle back to late-2019 GTV numbers in 2021 is not super bullish.

Takeaway: While Didi managed an impressive GTV recovery in China, its aggregate numbers are flatter, and recent quarterly trends are not incredibly attractive.

Powered by WPeMatico

It’s an entrepreneur’s market in digital health today, with startups raising record-breaking funding at soaring valuations and debuting on public markets to eager investors.

According to CB Insights, as of March 3, 2021, there are 51 healthcare unicorns — “startups” — worth $1 billion or more around the world. Global venture capital funding, including private equity and corporate VC, into digital health was the highest ever in the first quarter 2021 at $7.2 billion, according to Mercom Capital Group.

The massive influx of capital to healthcare should not be surprising; the pandemic has made it starkly clear that digital health is the future of healthcare. To that end, we should anticipate additional healthcare exits worth more than $1 billion in the near term. Which again, is great for entrepreneurs — as long as they understand how hard it is to build a unicorn in healthcare. Today, becoming a unicorn requires founders who are long on vision and operational experience.

Today, becoming a unicorn requires founders who are long on vision and operational experience.

Company founders most often turn to veteran investors for help with grand-slam strategies to create the next healthcare unicorn. That’s why many of them seek counsel from the Merck Global Health Innovation Fund: Because we have the experience, resources, successful track record and networks to build real scale in digital health.

During the pandemic, lots of investors jumped in to invest in digital health for the first time. But we’ve been investing for more than a decade. Two of our portfolio companies, Preventice Solutions and Livongo, exited last year as unicorns, rounding out the $6.2 billion in digital health market value MGHIF has exited over the last two years. And we are expecting two more unicorn exits in 2021. But we’re not stopping there; we’ll be investing our $500 million fund in drone-supported supply chain technologies, telehealth, AI, digital pathology, remote clinical trials and Internet of Medical Things (IoMT).

Given our success, here are four instrumental strategies to building a unicorn in digital health that we know work.

We often ask entrepreneurs: Would you rather own 20% of a $50 million company or 5% of a $1 billion company? To most, the answer is obvious. In our experience, too many entrepreneurs worry about dilution and never raise the right amount of capital.

It’s well known that companies with rapidly growing revenues are valued at a premium — but it’s important to remember that this is hard to do in healthcare. Getting to scale takes time because healthcare is so complicated and involves so many stakeholders.

Powered by WPeMatico

MasterClass, which sells a subscription to celebrity-taught classes, sits on the cusp of entertainment and education. It offers virtual, yet aspirational learning: an online tennis class with Serena Williams, a cooking session with Gordon Ramsay. While there’s the off chance that an instructor might actually talk to you — it has happened before — the platform mostly just offers paywalled documentary-style content.

The vision has received attention. MasterClass is raising funding that would value it at $2.5 billion, as scooped by Axios and confirmed independently by a source to TechCrunch. But while MasterClass has found a sweet spot, can the success be replicated?

Investors certainly think so. Outlier, founded by MasterClass’ co-founder, closed a $30 million Series C this week, for affordable, digital college courses. The similarities between Outlier and its founder’s alma mater aren’t subtle: It’s literally trying to apply MasterClass’ high-quality videography to college classes. This comes a week after I wrote about a “MasterClass for Chess lovers” platform launched by former Chess World Champion Garry Kasparov.

Two back-to-back MasterClass copycats raising millions in venture capital makes me think about if the model can truly be verticalized and focused down into specific niches. After 2020 and the rise of Zoom University, we know edtech needs to be more engaging, but we don’t know the exact way to get there. Is it by creating micro-learning communities around shared loves? Is it about gamification? Aspirational learning has different incentives than for-credit learning. In order to be successful, Outlier needs to prove to universities it can use MasterClass magic for true outcomes that rival in-person lectures. It’s a harder, and more ambtious promise.

My riff aside, I turned to two edtech founders to understand how they see the MasterClass effect panning out, and to cross-check my gut reaction.

Taylor Nieman, the founder of language learning startup Toucan:

Although I do love how these models try to lean into this theme of “invisible learning” like we leverage with Toucan, it faces the same issues as so many other consumer products that try to steal time out of people’s very busy days. Constantly competing for time leads to terrible engagement metrics and very high churn. That leads me to question what true learning outcomes could occur from little to no usage of the product itself.

Amanda DoAmaral, the founder of Fiveable, a learning platform for high school students:

Masterclass is important for showing us why educational content should be treated more like entertainment. All of our bars for content quality is much higher now than it ever was before and I’m excited to see how that affects learning across the board.

For students, it’s about creating environments that support them holistically and giving them space to collaborate openly. It feels so obvious that these spaces should exist for young people, but we’ve lost sight of what students actually need. At my school, we built policies that assumed the worst in students. I want to flip that. Assume the best, be proactive to keep them safe, and create ways to react when we need to.

Anyways, that’s just some nuance to chew on during this fine day. In the rest of this newsletter, we will focus a lot on tactical advice for founders, from the money they raise to the peacock dance they might want to do one day. Make sure to follow me on Twitter @nmasc_ so we can talk during the week, too!

You know when male peacocks fan their feathers to court a lover? That, but for startups trying to get acquired. As one of our many rabbit holes on Equity this week, we talk about Discord walking away from a Microsoft deal, and if that deal ever existed in the first place or if it was just a way to drum up investor excitement in the audio gaming platform.

Here’s what to know: Discord is reportedly pursuing an IPO after walking away from talks with multiple companies that were looking to acquire the audio gaming giant.

Discord aside, the consolidation environment continues to be hot for some sectors.

Image Credits: VectorInspiration / Getty Images

Clearbanc, a Toronto-based fintech startup that gives non-dilutive financing to businesses, has rebranded alongside a $100 million financing that valued it at $2 billion. Now rebranded as Clearco, the startup wants to be more than just a capital provider, but a services provider, too.

Here’s what to know: The startup has been on a tear of product development for the past year, launching services such as valuation calculators or runway tools. It’s a step away from what Clearbanc originally flexed: the 20-minute term sheet and rapid-fire investment. I talk about some of the levers at play in my piece:

Many of Clearco’s newest products are still in their infancy, but the potential success of the startup could nearly be tied to the general growth of startups looking for alternatives to venture capital when financing their startups. Similar to how AngelList’s growth is neatly tied to the growth of emerging fund managers, Clearco’s growth is cleanly related to the growth of founders who see financing as beyond a seed check from Y Combinator.

Abstract human brain made out of dollar bills isolated on white background. Image Credits: Iaremenko / Getty Images

Keeping on the theme of tactical advice for founders, let’s move onto talking about marketing. Tim Parkin, president of Parkin Consulting, explained how startup founders can use marketing as a tool to stand out in the noisy environment. Differentiation has never been harder, but also more imperative.

Here’s what to know: Parkin outlines four ways that martech will shift in 2021, strapped with anecdotes and a nod to the importance of investing in influencers.

Red ball on curved light blue paper, blue background. Image Credits: PM Images / Getty Images

Your humble yet favorite startup podcast, Equity, got nominated for a Webby! Me and the team need your help to win, so please vote for us here. Your support means a ton.

This newsletter will always be free, but if you do want to support me, feel free to use code STARTUPSWEEKLY for 25% off a subscription to Extra Crunch.

Seen on TechCrunch

The rise of the next Coinbase, thanks to Coinbase

Tiger Global backs Indian crypto startup at over $500M valuation

Early Coinbase backer Garry Tan is keeping the ‘vast majority’ of his shares because of this deal

Seen on Extra Crunch

Dear Sophie: How can I get my startup off the ground and visit the US?

How to pivot your startup, save cash and maintain trust with investors and customers

How startups can ensure CCPA and GDPR compliance in 2021

Image Credits: TechCrunch

Thanks for reading along today and everyday. Sending love to my readers in India and everyone around the world that is facing yet another deadly surge of this horrible disease. I’m rooting for you.

Powered by WPeMatico

Kavak, the Mexican startup that’s disrupted the used car market in Mexico and Argentina, today announced its Series D of $485 million, which now values the company at $4 billion. This round more than triples their previous valuation of $1.15 billion, which established them as a unicorn just a couple of months ago in October of 2020. Kavak is now one of the top five highest-valued startups in Latin America.

The round was led by D1 Capital Partners, Founders Fund, Ribbit and BOND, and brings Kavak’s total capital raised to date to more than $900 million. Kavak recently soft-launched in Brazil, and this new round of funding will be used to build out the Brazilian market and beyond, said Carlos García Ottati, Kavak’s CEO and co-founder. The company plans to do a full launch in Brazil in the next 60 days, García said, and we can expect to see Kavak in markets outside Latin America in the next 24 months, he added.

“We were built to solve emerging market problems,” García said.

Kavak, which was founded in 2016, is an online marketplace that aims to bring transparency, security and access to financing to the used car market. The company also offers its own financing through its fintech arm, Kavak Capital, and counts more than 2,500 employees and 20 logistics and reconditioning hubs in Mexico and Argentina.

“In Latin America, 90% of the [used car] transactions are informal, which leads to a 40% fraud rate,” said García, who experienced these challenges firsthand when he moved to Mexico from Colombia a couple of years ago and bought a used car.

“My budget allowed me to buy a used car, but there was no infrastructure around it. It took me six months to buy the car, and then the car had legal and mechanical issues and I lost most of my money,” he said. Kavak buys cars from individuals, refurbishes them and offers warranties to buyers.

“Instead of buying a new car, they can buy a better car that still has all the warranties. It’s a really aspirational process,” said García. The company, which really amounts to four companies in one given its areas of focus, was built to be comprehensive by design in order to meet the various gaps in the market, García said.

“When you’re building a business here [Latin America], you need to build several businesses because so many things are broken,” he said. That’s why the financing option, for example, has been a key to their success, according to García.

Financing has traditionally been hard to come by in Brazil, and as García said, the used car market lacks infrastructure there, too. That being said, Brazil is Latin America’s fintech hub, and the space has made leaps and bounds over the last 7-10 years with companies such as Nubank, PagSeguro, Creditas, PicPay, and others leading the way. As a result, credit cards and loans are more widely available today in the region, offering competition for Kavak Capital. While Kavak has localized some of its product for the Brazilian market — namely building out a Portuguese language version of the app and website — García said the markets are very similar.

“In Brazil, you still have the same problems that you have in Mexico, but Brazil is a little more developed, especially in fintech, which is light years ahead of Mexico,” he said.

With the Brazilian product heading to the races, García said they already have plans for other regions, though he declined to name them.

“80% of people in emerging markets don’t have access to a car,” García said of the global market size. “We want to go into big markets where customers are facing similar problems and where Kavak can really change their lives,” he added.

Powered by WPeMatico

Welcome to 2021, a year that could extend 2020’s startup market disruptions and excesses — or change patterns that previously performed well for early-stage tech companies and their investors.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

As we turn the page, I have a number of questions worth raising as we muck into 2021.

Each relates to a 2020 change that is expected to persist, by either the general market or those bullish on startups. I want to know what would need to change to shake up what became the new normal last year. After all, it’s precisely when it feels like nothing could shake up a downturn (or a boom) that things often do.

Today, let’s discuss seed deals, venture investing cadence, the resulting valuation pressures from rapid-fire bets, current IPO expectations and what happens to software sales when remote work begins to fade.

Today, let’s discuss seed deals, venture investing cadence, the resulting valuation pressures from rapid-fire bets, current IPO expectations and what happens to software sales when remote work begins to fade.

As 2020 came to a close, Natasha Mascarenhas and I reported on seed investing’s strong year and its especially strong second half. How long can that pace keep up?

Nearly all our questions today deal with the endurance of certain conditions, namely: how long the market can keep parts of startup land red-hot.

When it comes to seed deal-making, Q1 and Q2 2020 saw similar levels of investment in the United States. But Q3 proved explosive, with money invested into domestic seed deals rising from around $1.5 to $1.6 billion during the first two quarters to $2.2 billion in the July-September period.

Q4 numbers are yet to fully come in, but it’s clear that private investors were incredibly bullish on early-stage startups in the second half of 2020. How long can that keep up? I think the answer is for a while yet, as investors have shown scant enthusiasm for slowing down their dealmaking cadence.

While cadence remains hot generally, seed deals should stay heated as the number of investors who are willing to invest early has increased.

Which brings us to our second question:

A theme that cropped up in the second half of 2020 was the pace at which investors were conducting venture capital deals. This was for a few reasons. To start, venture capitalists have raised larger funds in recent years, meaning that they need larger returns to make the math work out. This led to many investors putting money to work in younger and younger companies, hoping to get in early on a big win. That setup led to more deal competition and faster deal-making.

How? Two things. Investors who were already on a startup’s cap table — already part-owners, in other words — led preemptive rounds, in part to get ahead of other investors who might want to poach the succeeding deal. Other investors, knowing this, seemed to do the same math and move even faster, and earlier, to get around the defense.

So how long can the trend keep up? Given that many big VC firms raised in 2020, many startups picked up some tailwinds from the COVID-19 economy and exits have been strong, forever? Until something stops things? Think of it as Newton’s First Law of startup investing.

What could be the sudden impact to shake up the current set of conditions boosting the pace at which seed and later deals occur? An asteroid strike is probably too extreme, but inertia is one hell of a drug and markets love to stay happy.

Moving along, all the competition to get money to work in hot startups now has had another effect than the mere speed of deal-making; it has also pushed prices higher.

Powered by WPeMatico

Silicon Valley has a unicorn problem.

While no one is calling for startups with high valuations to go extinct, there ought to be a lot fewer of them. At least that’s what many young founders have concluded after looking at the trials and travails of billion-plus-dollar private companies.

A unicorn is a mythical animal, so investors expect magical results: Lightning growth, near-monopolies and a record-setter IPO yielding 100x or 1,000x returns. A “zebra” company is different. Zebras are real animals that have evolved to fill and thrive in a particular niche. Unlike unicorn companies, zebras are lean, efficient and consistent.

Exponential growth is neither the best nor the only way for businesses to operate.

Too often, a company’s name or perceived cachet — rather than its actual product or realistic business prospects — becomes the thing it is selling. For the most recent, and maybe most damning, example of this trend, look at WeWork .

The company’s 2019 failed IPO was the corporate debacle of the decade; few businesses since Enron have fallen so far so quickly. When the market got a chance to examine the unicorn, they discovered it was really a one-trick pony with a cardboard horn. Adam Neumann built his company for net worth, not actual value, and his employees and supporters paid the price. Then again, imagine if the IPO had been a success: How much of the company’s worth would have evaporated when COVID-19 rolled around in March?

Although most tech innovation requires venture capital in today’s economy, unicorns sometimes become case studies in taking too much of a good thing. Round after round of funding can, as in the case of WeWork, disguise rickety foundations and unsound business plans.

Earlier this month, the mobile video unicorn Quibi folded less than a year after its launch. Film and TV critics weren’t surprised, and neither were those few consumers who’d heard of the company.

Well before its ill-timed launch in early April, most observers knew it was a bad idea. So why did Quibi receive so much funding? The big names attached to the company, including Dreamworks co-founder Jeffrey Katzenberg and one-time HP CEO Meg Whitman, attracted investors who somehow didn’t realize that everything about the product, from its name to its pricing, was wrong.

What a unicorn offers isn’t as important as the fact that it’s a unicorn. The opposite of a unicorn company, to my mind, is a zebra company. They may be a little odd, they may not get the front-page headlines or breathless news coverage, but they’re built to last and built to do something.

Unicorns thrive so long as they remain in the enchanted forest of endless venture rounds; zebras tough it out in the savannas of the free market. A zebra company won’t become the next behemoth like Facebook or Amazon, but neither will it become the next Quibi or WeWork.

The emergence of zebra companies like Handshake and Turo, and to some extent corporations like Ben and Jerry’s and Patagonia, speaks to a broader change in our business and economic understanding. Even before the coronavirus shut down much of the world, endless growth was looking less and less attractive.

Instead of extracting ever more value from the economy, companies like Patreon realize that the same dollar can be earned multiple times as it circulates through the economy. One-way extraction of value is replaced with a circular flow of value. Exponential growth is neither the best nor the only way for businesses to operate.

For most of us, the new year will be a relief: 2020, over at last. But we shouldn’t neglect the opportunity to reflect on the past and plan for the future that a new year offers. The mistakes of WeWork and Quibi are all too easy to repeat; chances are that somewhere in Silicon Valley, a venture capitalist is giving too much money to a doomed business. We’ve been too focused on the unicorns. It’s time to give the zebras the attention they deserve.

Powered by WPeMatico

Eneba, a marketplace for gamers that sells games and other products, has raised an $8 million round of funding from Practica Capital and InReach Ventures. The funding is described as a “combination” of a seed and Series A round. Also participating in the funding for the Lithuanian startup was FJ Labs and a group of angel investors, including Mantas Mikuckas, COO of Vinted. The investment highlights once again the strength of the Baltics region as a tech ecosystem, after Lithuania produced its first Unicorn in the shape of Vinted, and Estonia added Pipedrive to its unicorns list.

With the increased shift to digital entertainment during the pandemic, the startup has managed to garner much more U.S. traffic. Launched in 2018 by two Lithuanian school friends, Vytis Uogintas and Žygimantas Mikšta, Eneba says it has attracted 26 million unique users because of its security features, “one-click to buy” gamer experience and fingerprinting technology. The site also optimizes its localized gaming experiences to show locally trending gaming products. Eneba’s platform is designed to reduce risky transactions, simplify the refunding process and deal with fraud threats.

Co-founder and CMO Žygimantas Mikšta said: “We had a lot of new users coming to Eneba during these uncertain times. While it was extremely satisfying to see our numbers increasing tenfold, there was a challenge to meet the demand. To better reflect our user numbers, we had to quickly expand our team to 130.”

Security has risen up the agenda in online gaming as virtual goods and services connected to games can be highly susceptible to fraud or theft. Although it competes with outlets like Amazon, eBay and retailers like GameStop and Game.co.uk, Eneba thinks it has found a better, tailored online pre/post-buying experience for gamers, while addressing the risk problems for sellers and buyers in the gaming world.

Donatas Keras, partner at Practica Capital said: “We are thrilled to be backing Vytis and Žygimantas. We’ve been impressed by their ability to execute at such speed as their company quickly scales, and to drive an incredible product with a unique value proposition for gamers.”

Co-founder of InReach Ventures, Roberto Bonanzinga, said: “In Europe we have a tradition of building successful companies in the gaming space. We are very excited to have discovered Eneba thanks to our AI platform when the company was unknown and under the radar. We have been extremely impressed by what the founders have been able to build in such a short amount of time.”

Powered by WPeMatico

{kind=link}