The Exchange

Auto Added by WPeMatico

Auto Added by WPeMatico

Startups are raising record sums around the world, thanks to several contributing factors. As The Exchange explored yesterday, historically low interest rates have helped venture capitalists raise more capital than ever, to pick an example.

Low rates have helped startups in another manner: As yields fell for certain assets, investors chased returns by betting on growth. And in recent years, the investing classes turned their attention to public software companies, bidding up the value of their revenue to record highs.

This raised the worth of startups in general terms, and private tech companies’ comps enjoyed a steady, upward climb in the value of their revenues. If the value of a dollar of SaaS revenue was worth $1 one year and $2 the next, the repricing was good for private companies even if we were tracking the metrics from the perspective of public companies.

The free ride could be ending.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

I’ve held back from covering the value of software (SaaS, largely) revenues for a few months after spending a bit too much time on it in preceding quarters — when VCs begin to point out that you could just swap out numbers quarter to quarter and write the same post, it’s time for a break. But the value of software revenues posted a simply incredible run, and I can’t say “no” to a chart.

The pace at which software revenues were repriced upwards in the last few years is simply astounding. Per the Bessemer Cloud Index, back in 2016, the median revenue multiple for public SaaS companies was around 5x. When 2018 began, median SaaS multiples had expanded to around 7x.

The pace at which software revenues were repriced upwards in the last few years is simply astounding. Per the Bessemer Cloud Index, back in 2016, the median revenue multiple for public SaaS companies was around 5x. When 2018 began, median SaaS multiples had expanded to around 7x.

That’s a 40% climb in pricing, but it proved to be just a foretaste of the feast to come.

By the end of 2019, the median figure had appreciated to around the 9x mark. And today it has shot to just under 18x. That is why software companies have been able to raise so much money, earlier, and in larger chunks. Every dollar of recurring revenue they sold was worth $5 in market cap in mid-2016. At the end of 2019, that same dollar of revenue was worth $9. And today, for the median public software company, it’s valued at around $18.

There are nuances to the data, but we care less about exacting definitions than the directional change it describes: The median value of SaaS revenues more than tripled from 2016 to 2021. That’s an insane amount of growth.

Powered by WPeMatico

Mailchimp is selling itself to Intuit in a transaction valued at $12 billion. The deal is a coup not only for companies that eschew venture capital backing — Mailchimp is famous for its bootstrapping history — but also for the city of its founding, Atlanta.

Mailchimp’s mega-exit comes in the same year that fellow Atlanta-based startup Calendly raised a massive $350 million round that valued the technology company north of $3 billion, per Crunchbase data.

The two companies underscore how possible it is to build large startups in markets outside of the traditional collection of cities most associated with technology entrepreneurship in the United States, like Boston, New York City and San Francisco, to name a few.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Investors are taking note. CB Insights data through Q2 2021 indicates that startups in Atlanta are on a fundraising tear, already surpassing total capital raised in 2020 in just the first half of this year. The city’s venture acceleration is similar to fundraising gains we’ve seen in markets like Chicago.

The Exchange wanted to better understand the Atlanta market, especially regarding how bullish its local inventors are that its current pace of fundraising can continue, and what sort of external interest its startups are enjoying. So, we ran questions by Sean McCormick, the CEO of Atlanta-based SingleOps, a software startup that raised capital earlier this year; Atlanta Ventures’ A.T. Gimbel; and BLH Venture Partners’ Ashish Mistry. We also heard from Paul Noble, CEO of Verusen, a supply chain intelligence startup that raised an $8 million Series A round in January.

The Exchange wanted to better understand the Atlanta market, especially regarding how bullish its local inventors are that its current pace of fundraising can continue, and what sort of external interest its startups are enjoying. So, we ran questions by Sean McCormick, the CEO of Atlanta-based SingleOps, a software startup that raised capital earlier this year; Atlanta Ventures’ A.T. Gimbel; and BLH Venture Partners’ Ashish Mistry. We also heard from Paul Noble, CEO of Verusen, a supply chain intelligence startup that raised an $8 million Series A round in January.

The picture that forms is one of a city enjoying a rising tide of venture activity, boosted by some local dynamics that may have helped some of its earlier-stage companies scale more cheaply than they might have in other markets. And there’s plenty of optimism to be found concerning the near future. Let’s explore.

It’s cliche at this point to note that a particular geography is experiencing record venture capital results; many cities, regions and countries are seeing startup capital inflows accelerate. But there are markets where the gains still stand out despite the generally warm climate for private capital investments into private companies.

Atlanta is one such market. Per CB Insights data, the U.S. city saw $2.17 billion in total investment during 2020. In the first quarter of 2021, Atlanta nearly matched its 2020 tally, with its startups collecting some $2.07 billion in total capital. Another $953 million was invested in the second quarter of the year; keep in mind that venture capital data is laggy, and thus what may appear to be a sharp decline may be ameliorated by later disclosures.

But with around $3 billion invested in the first half of 2021, already around a 50% gain on 2020’s full-year figures, it’s clear the city is seeing an unprecedented wave of venture investment.

Dollar volume is half the venture capital activity matrix, of course. The other key data line for the investment type is deal volume. There Atlanta’s activity is less superlative; Q1 2021 saw Atlanta startups attract 57 total deals, the second-best results that we have data for, narrowly losing to Q3 2017’s 59 deals.

But Q2 2021 saw Atlanta’s known venture deal volume fall to 42, a figure that is a slight miss from 2020’s average deal volume, measured on a quarterly basis. The same caveat regarding delayed data applies here, but perhaps not enough to completely close the gap between what we might have expected from Atlanta startups in terms of Q2 deal volume in the wake of the city’s super-active Q1.

Despite the somewhat slack Q2 2021 deal count in Atlanta, per current data, it’s clear that the city is enjoying record venture capital attention. What’s driving the uptick? Let’s find out.

Powered by WPeMatico

It’s a two-Exchange Tuesday, everyone. First up, we’re talking fintech valuations. Next up, we’re digging into Atlanta.

Last week’s news that PayPal intends to buy Japanese startup Paidy marked the second major acquisition of a buy now, pay later (BNPL) company this year. PayPal’s news followed an even larger deal by Square for the Australian BNPL company Afterpay.

The multibillion-dollar exits provided hard market proof that what BNPL startups are building has value beyond simple operating results; major fintech platforms are willing to shell out large sums for their revenues and possible strategic value.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Because both deals happened in 2021, they provide two data points for the value of BNPL companies operating at scale. And because both Square and PayPal provided some information to their investors concerning their transactions, we have a little bit of comparative work to do.

Let’s do a little math and figure out how much PayPal and Square investors are paying for transaction volume across both platforms. Then, we’ll peek at what Affirm is worth along similar lines. We’ll wrap with a look at Klarna’s numbers to see if there’s anything we can dig up there.

Our goal is to find out what sort of price floor or ceiling the Paidy and Afterpay deals imply, if other players in their space are matching that figure, and why. This will be fun!

Square’s Afterpay deal is worth some $29 billion, a huge sum. It isn’t hard to see why the U.S. consumer- and business-focused fintech is willing to write so large a check — Afterpay does volume.

Powered by WPeMatico

What a busy week in the world of media liquidity.

That’s a sentence you don’t get to write often. Regardless, news broke this week that Axel Springer is buying U.S. political journalism outfit POLITICO. The transaction was expected, but the eye-popping roughly $1 billion price tag still has tongues wagging. We even got on the podcast to chat about it.

And Forbes announced that it is going public via a SPAC. The business publication’s news follows BuzzFeed’s journey to the public markets through a blank-check company. Hot media liquidity summer? Something like that.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

That TechCrunch is in the process of being sold to private equity, of course, is not something that we should forget. Shoutout to the Verizon bankers who found a way to get rid of us while also deleveraging Verizon’s debt profile. Ten points.

I want to take a quick tour of the Forbes SPAC deck this morning. Our notes on BuzzFeed’s are here, in case you want to run comparisons. This will be easy and fun. Perfect Friday morning fare. Into the data!

I want to take a quick tour of the Forbes SPAC deck this morning. Our notes on BuzzFeed’s are here, in case you want to run comparisons. This will be easy and fun. Perfect Friday morning fare. Into the data!

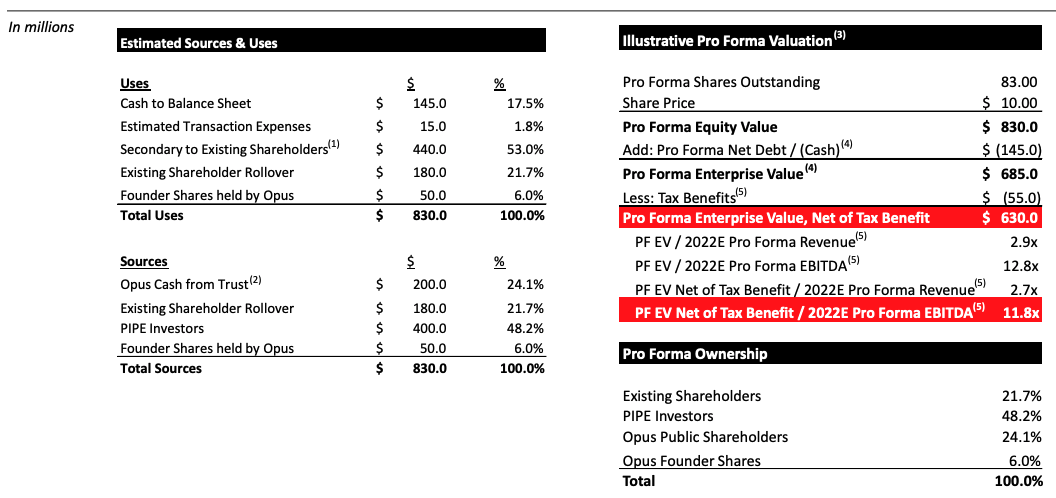

In corporate-speak, Forbes Global Media Holdings is merging with blank-check company Magnum Opus Acquisition Limited. The transaction will close either Q4 2021 or Q1 2022, Forbes estimates.

The deal itself is somewhat modest in scale compared with other SPAC deals we’ve recently looked into. Forbes reports that it will sport “an implied pro forma enterprise value of $630 million, net of tax benefits,” after its completion. Some $600 million in gross proceeds will be derived from Magnum Opus funds “and $400 million of additional capital through a private placement of ordinary shares of the combined company,” Forbes writes.

The company will sport an equity valuation of $830 million after the deal closes, per its own calculations. That number will change some depending on redemptions ahead of the combination. The gap between the large dollars going into the deal and the modest final valuation of the public Forbes entity is due to some $440 million in secondary transactions for existing Forbes shareholders.

In case you’d prefer all of that in table form, here’s the Forbes investor deck:

Image Credits: Forbes SPAC deck

Is $830 million a fair price? Let’s dig into Forbes’ results.

Powered by WPeMatico

Newly reported financial data from Bird, an American scooter sharing service, shows a company with an improving economic model and a multiyear path to profitability. However, that path is fraught unless a number of scenarios all work out in concert and without a glitch.

Bird, well known for its early battles with domestic rival Lime, is pursuing a SPAC-led deal that will see it go public and raise fresh capital. The former startup is merging with Switchback II Corporation in a deal that values it at around $2.3 billion, including a $160 million PIPE (private investment in public equity) component. (Note: The group purchasing TechCrunch’s parent company from its own parent company is part of the Bird PIPE.)

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

COVID-19 hasn’t been kind to Bird and similar companies around the world. As many around the world stayed home, usage of shared-asset services and ride-hail applications fell sharply. Bird saw rides decline. Airbnb took a temporary hit. Uber and Lyft saw ride demand fall.

Responses to the crisis were varied. Airbnb cut costs and raised external capital. Lyft cut expenses and focused on its core model while Uber grew its food delivery business, which saw transaction volume soar as demand fell for its traditional business.

Meanwhile, Bird flipped its entire business model. That decision has helped the scooter outfit improve its economics markedly, giving it a shot at generating profit in the future — provided its forecasts prove achievable.

This morning, let’s talk about how Bird has changed its business, their impacts on its operating results and how long the company thinks its climb to profitability is.

In their initial forms, Bird and Lime bought and deployed large fleets of electric scooters. Not only was this capital intensive, the companies also wound up with costs that were more than sticky — charging wasn’t simple or cheap, moving scooters around to balance demand took both human capital and vehicles, and the list went on.

Throw in vehicle depreciation — the pace at which scooters in the wild degraded from use or abuse — and the businesses proved excellent vehicles for raising capital and throwing that money at more scooters, costs, and, as it turned out, losses.

Results improved somewhat over time, though. As scooter-share companies increasingly built their own hardware, their economics improved. Sturdier scooters meant lower depreciation, and better battery tech could allow for more rides per charge. That sort of thing.

But the model wasn’t incredibly lucrative even before COVID-19 hit. Costs were high, and the model did not break-even, even on a gross margin basis, let alone when considering all corporate expenses. You can see the financial mess from that period of operations in historical Bird results.

Powered by WPeMatico

China’s technology scene has been in the news for all the wrong reasons in recent months. In the wake of the scuttling of Ant Group’s IPO, the Chinese government has gone on a regulatory offensive against a host of technology companies. Edtech got hit. On-demand companies took incoming fire. Ride-hailing? Check. Gaming? You bet.

The result of the government fusillade against some of the best-known companies in China was falling share prices. The damage topped $1 trillion among just public Chinese companies listed abroad.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

What about startups in sectors that were reformed overnight? If their public comps are any indication, even more wealth was deleted in the recent wave of crackdowns.

The Exchange was curious about the impact of the Chinese government’s actions on the venture capital market. The Chinese startup economy has produced a number of world-leading companies. Tencent and Alibaba, yes, and even Baidu have become well-known for a reason. Could regulatory changes shake up the venture model that helped grow the country’s largest tech concerns?

After we checked in on the same question this Monday, SoftBank provided a partial answer, noting yesterday that it is pausing investments in China. The Japanese teleco, conglomerate and investing powerhouse has been deploying capital at a rapid pace in recent weeks. That will slow, at least in China. Here’s the WSJ:

The regulatory initiative in China has become so unpredictable and widespread that SoftBank and its funds are planning to hold off on investing much more there until the risks become clearer, [SoftBank CEO Masayoshi Son] said at an earnings press conference in Tokyo.

Is SoftBank early to its decision to shake up its investing strategy, missing Chinese deals for some time? Or is it late? We secured data from PitchBook and Traxcn that paints a somewhat surprising picture of venture capital activity at least thus far in Q3 2021.

But first, a reminder of how well China’s venture capital market was performing as 2020 eased its way into 2021.

But first, a reminder of how well China’s venture capital market was performing as 2020 eased its way into 2021.

China had a reasonably good Q2 2021 despite the turmoil.

Sure, funding flowing into Chinese startups was down 18% compared to Q4 2020, per CB Insights, but that quarter had recorded an all-time high of $27.7 billion. With $22.8 billion raised, Q2 2021 still did better than every other quarter since Q2 2016 with the exception of Q2 2018, Q4 2020 and Q1 2021. Indeed, the ecosystem had started to cool down in late 2018 before picking up pace again at the end of 2020.

However, that’s only one way to look at the numbers. If you compare recent Chinese venture results with other regions, it underperformed. During Q2 2021, U.S. funding reached a new high of $70.4 billion, with places like Latin America, Canada and India also establishing new records.

This also means that China lost ground as to its share of global startup deal-making, and the same goes for unicorn creation. According to Tech Buzz China’s summary of CB Insights data, the U.S. accounted for 132 unicorn births between January 1 and June 16, 2021, compared with just three in China.

Slightly falling quarterly venture capital totals and a notable decline in unicorn formation does not a startup winter make. So let’s look at what’s happened more recently.

The thesis that there would be an instantly obvious slowdown in Chinese venture capital activity is not supported by the data we secured.

Powered by WPeMatico

The Chinese government’s crackdown on its domestic technology industry continues, with Tencent under fresh pressure despite the company’s efforts to follow changing regulatory expectations.

News broke over the weekend that Beijing filed a civil suit against Tencent “over claims its messaging-app WeChat’s Youth Mode does not comply with laws protecting minors,” per the BBC. And NetEase, a major Chinese technology company, will delay the IPO of its music arm in Hong Kong. Why? Uncertain regulations, per Reuters.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The latest spate of bad news for China’s technology industry follows a raft of regulatory changes and actions by the nation’s government that have deleted an enormous quantity of equity value. After a period of relatively light-touch regulatory oversight, domestic Chinese technology companies have found themselves on defense after the Chinese Communist Party (CCP) came after their market power in antitrust terms — and some of their business operations from other perspectives. Sectors hit the hardest include fintech and edtech.

Gaming is also in the CCP crosshairs.

After state media criticized the gaming industry as providing the digital equivalent of drugs to the nation’s youth last week, shares of companies like Tencent and NetEase fell. Tencent owns Riot Games, makers of the popular League of Legends title. NetEase generated $2.3 billion in gaming revenue out of total revenues of $3.1 billion in its most recent quarter.

After state media criticized the gaming industry as providing the digital equivalent of drugs to the nation’s youth last week, shares of companies like Tencent and NetEase fell. Tencent owns Riot Games, makers of the popular League of Legends title. NetEase generated $2.3 billion in gaming revenue out of total revenues of $3.1 billion in its most recent quarter.

NetEase stock traded around $110 per share in late July. It’s now worth around $90 per share after expectations shifted in light of the gaming news, indicating that investors are concerned about its future performance. Tencent’s Hong Kong-listed stock has also fallen, from HK$775.50 to HK$461.60 this morning.

Tencent tried to head off regulatory pressure, announcing changes to how it controls access to its games after the government’s shot across the bow. The effort doesn’t appear to have worked. That Tencent is being sued by the government despite its publicly announced changes implies that its proposed curbs to youth gaming were either insufficient or perhaps moot from the beginning.

Powered by WPeMatico

Last week, Deliveroo made news when it announced it was preparing to leave the Spanish market. The recently listed Deliveroo couched its explanation in market terms, noting its market position in Spanish on-demand delivery wasn’t sufficient to warrant continued investment. Left unmentioned: A Spanish legal change requiring companies that previously depended on freelance couriers to hire their delivery staff.

Race Capital’s Edith Yeung helped explain the Deliveroo choice to The Exchange, saying the Spanish market doesn’t have a very large population, which may mean that the “potential upside for being #1 in Spain has [a] ceiling.”

While she noted that she doesn’t have access to Deliveroo data, her statement jibes with the company’s own comment that Spain made up less than 2% of its aggregate gross transaction value (GTV) in the first half of 2021.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

One company exiting a market is not a big deal, but we were curious about Deliveroo’s comments regarding the need for market leadership — or something close to it — to warrant continued investment. Is this the common reality for startups battling for market position, no matter if those markets are cities or countries?

Some startup markets have trended toward monopolies or duopolies. The Uber-Didi battle in China led to the companies agreeing to stop competing. Uber also recently sold its Uber Eats business in India to Zomato. In the United States, Uber and Lyft’s smaller competitors have long been forgotten and both the American ride-hailing giants continue to battle for dominance.

There are other familiar examples of this trend of consolidation. The food delivery game is concentrated amongst leading players. Postmates failed to survive as an independent company, winding up as part of Uber’s operations. Perhaps Gopuff will manage to claw out a spot in the market, but DoorDash and Uber Eats together accounted for 83% of the U.S. food delivery business in June this year, per Second Measure data.

It’s no surprise that some startup markets lean toward monopolies or duopolies. Many countries protect intellectual property via patents that can constrain new innovation to one or two players for an extended period of time. Monopolies can also arise when a new technology or method of business is invented — Google’s internet parsing search tech led to a nigh-monopoly in many markets, for example.

In businesses where efficiencies of scale have a large effect, monopolies can form when leading players consolidate smaller competitors until just one or two companies remain. Standard Oil is the canonical example of this process.

What’s interesting about the on-demand delivery market is that it is both incredibly expensive but isn’t very technologically difficult to get into, which has meant that many companies have jumped into the sector around the world. This means on-demand delivery is the opposite of other patent-protected markets from which we might expect monopolies to form or competition to be extinguished past the top two players.

Yet, it’s also an industry where economies of scale can play a key role in profit generation, and increased competition can lead to price wars and advertising tussles. It’s a ripe market, then, for consolidation, even if it lacks an exploitable IP base.

Powered by WPeMatico

The global venture capital bet on neobanks is massive. London-based Starling Bank has raised more than $900 million, per Crunchbase. The same data source indicates that Chime has raised $1.5 billion. Monzo has raised nearly $650 million. And the list goes on: E-commerce-focused neobank Juni raised $21.5 million last month. Novo, an SMB-focused neobank, raised $41 million in June. Nubank has raised $2.3 billion. And FairMoney has locked down more than $50 million.

On and on and on.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

But despite our general inclination to lump banking-focused fintech providers that serve consumers, business customers or both into a single bucket, there’s wide divergence in how the various neobank players are performing in the market.

Back in August 2020, The Exchange noted that many neobanks were racking up steep losses. Our read at the time was that the capital being poured into the fintech category was being invested aggressively in the name of growth. Based on recent results, that view is holding up.

But not all neobanks are the unprofitable enterprises that they once were. Chime indicated in September 2020 that it generates positive, unadjusted EBITDA. That’s a stricter profit metric than the one that Lyft used recently to claim its ascendance into the realm of profitable companies; Lyft posted positive adjusted EBITDA in its most recent quarter, but burned cash to fund its operations and posted a wide net loss in the period.

And Starling Bank reached what it describes as profitable territory in October 2020. Things have changed since our first look into neobank results.

The trend of positive neobank news continued this June, when Revolut reported its recent financial performance. The company did post rather negative aggregate results for the 2020 period. But when we drilled down into its quarterly results, we saw the picture of a fintech company scaling its gross margins and revenues while nearly reaching adjusted net income neutrality by Q4 2020. We were impressed.

This morning, let’s add to our running dig into neobank results by parsing recently released data from Starling Bank and Monzo. As we’ll see, although some neobanks are managing to clean up their ledgers and work toward profits — or reach profitability — not all are in the black.

Powered by WPeMatico

British venture capital firm Draper Esprit recently moved its listing from the AIM to the main board in London, the LSE. The investing group also moved its secondary listing from Dublin’s Euronext Growth Market to its larger sister exchange, Euronext Dublin, which makes sense given its long connection to Irish capital.

Draper has always felt like something of an anomaly from our perspective, a generalist venture capital firm that was itself public. But this July, Forward Partners listed its shares on the AIM, and there are other venture firms in Europe that are also listed.

At first blush, the setup may seem odd; venture capital firms invest in companies that they hope to see go public one day — why would they float themselves? But Draper Esprit co-founder Stuart Chapman told TechCrunch in an interview that he finds it shocking “that venture capital backs some of the most mind-blowing tech advances in our history over the last 70 years, using the same legal structure as a 1958 property vehicle in New York.” It’s a reasonable point.

Perhaps fundraising success is part of why the venture model has not seen much disruption in recent decades, apart from rising fund sizes. But the model is not perfect. It can foist artificial time constraints on investors and force them to focus their deal flow into particular stages for fund-construction reasons. As we found out researching this piece, the public venture model highlights some of these limitations — and may be able to alleviate them in part.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

And yet we can’t come up with a single U.S. venture capital firm, for example, that has publicly listed in the same manner as Draper Esprit or Forward Partners.

To better understand why we’re seeing European VCs float, and not their peers in other markets, The Exchange reached out to Draper Esprit, Forward Partners, and fellow listed venture investors Mercia and Augmentum Fintech. From the group, we’ve learned that there are plenty of reasons why the model may be popular in the U.K. and not in the U.S.

But there are also reasons why being a public venture capitalist can make the VC game a rather different, longer-term effort. The firms in question did not go public on a whim.

So let’s talk about the good, the bad, and the regulatory concerning publicly listed venture capital firms. The future? Or just a regional quirk?

Following its move, Draper Esprit is now the largest “purely tech VC” listed on London’s Main Market. Its initial listing had also been a market milestone: “Listing Draper Esprit five years ago was a radical and unusual step for a venture capital business,” Chapman said of Draper’s 2016 dual-listing on London’s AIM and Dublin’s Enterprise Securities Market (ESM) — now Euronext Growth.

Just last month, two tech-related investment funds IPO’d on the London Stock Exchange: space-focused Seraphim Capital and Nic Brisbourne’s Forward Partners. In both cases, Draper Esprit was happy to assist with information, Chapman told us, adding that the firm also invested in Forward via its fund-of-funds effort.

The news adds up to a roster of listed investors that also includes fintech fund Augmentum Fintech, asset manager Mercia Asset Management PLC and intellectual property commercialization company IP Group. “We’re supportive of others following in our footsteps and we will be big fans of having much wider diversity,” Chapman told TechCrunch in an interview, which you can read in full here.

Having recently joined the club, Forward Partners’ founder and CEO Nic Brisbourne gave us a good overview of the three high-level reasons that could lead a fund to list: open opportunities to create more value from new initiatives that sit outside traditional investment capital; breaking the cycle of fundraising; and opening access to the early-stage venture capital asset class. Let’s take a closer look.

Powered by WPeMatico