TechCrunch Include

Auto Added by WPeMatico

Auto Added by WPeMatico

The Trump administration’s decision to extend its ban on issuing work visas to the end of this year “would be a blow to very early-stage tech companies trying to get off the ground,” Silicon Valley immigration lawyer Sophie Alcorn told TechCrunch this week.

In 2019, the federal government issued more than 188,000 H-1B visas — thousands of workers who live in the San Francisco Bay Area and other startup hubs hold H-1B and H-2B visas or J and L visas, which are explicitly prohibited under the president’s ban. Normally, the government would process tens of thousands of visa applications and renewals in October at the start of its fiscal year, but the executive order all but guarantees new visas won’t be granted until 2021.

Four TechCrunch staffers analyzed the president’s move in an attempt to see what it portends for the tech industry, the U.S. economy and our national image:

America’s economic supremacy is increasingly precarious.

Outsourcing and offshoring led to a generational loss of manufacturing skills, management incompetence killed off many of the country’s leading businesses and the nation now competes directly with China and other countries in critical emerging industries like 5G, artificial intelligence and the other alphabet soup of technological acronyms.

We have one thing going for us that no other country can rival: our ability to attract top talent. No other country hosts more immigrants, nor does any other country capture the imagination of a greater portion of the world’s top minds. America — whether Silicon Valley, Wall Street, Hollywood, Harvard Square or anywhere in between — is where smart people congregate.

Or at least, it was.

The coronavirus was the first major blow, partially self-inflicted. Remote work pushed employers toward keeping workers where they are (both domestically and overseas) rather than centralizing them in a handful of corporate HQs. Meanwhile, students — the first step for many talented workers to enter the United States — are taking a pause, fearing renewed outbreaks of COVID-19 in America while much of the rest of the developed world reopens with few cases.

The second blow was entirely self-inflicted. Earlier this week, President Donald Trump announced that his administration would halt processing critical worker visas like the H-1B due to the current state of the American economy.

Powered by WPeMatico

Tim O’Reilly has a financial incentive to pooh-pooh the traditional VC model, wherein investors gamble on nascent startups in hopes of seeing many times their money back. Bryce Roberts, who is O’Reilly’s longtime investing partner at the early-stage venture firm O’Reilly AlphaTech Ventures (OATV), now actively steers the partnership away from these riskier investments and into companies around the country that are already generating revenue and don’t necessarily want to be blitzscaled.

Yet in an interview with O’Reilly last week, he nonetheless argued persuasively for why venture capital, in its current iteration, has begun to make less sense for more founders who genuinely want to build sustainable businesses. The way he sees it, the venture industry is no longer as focused on finding small companies that might one day change the world but more on creating financial instruments for the wealthy — and that shift has real consequences.

Below, we’re pulling out parts of that conversation that may be of interest to readers who are either debating raising venture capital, debating raising more venture capital, and even those who have been turned away from VCs and perhaps dodged a bullet in the process. At a minimum, O’Reilly — who bootstrapped his own company, O’Reilly Media, 42 years ago and says it now produces “a couple hundred million dollars in revenue” yearly — provides a lot of food for thought.

TechCrunch: A lot of companies celebrated Juneteenth this year, which is a big deal. There’s been a lot of talk about making the venture industry more inclusive. How far — or not — do you think we’ve come in the venture industry on this front?

Tim O’Reilly: The thing that I would say about VC and about really everything in tech is, this concept of structural racism [is really the problem]. People think that all it matters is, ‘Well, my values are good, my heart’s in the right place, I donate to charities,’ and we don’t actually fix the systems that cause the problems.

With VCs, the networks from which they’re drawing entrepreneurs are not that different [than they have been historically]. But more importantly, the goals of the VC model are not that different. The industry sets a goal, and it has a certain kind of financial shape, which is inherently exclusionary.

How so?

The typical VC model is looking for this high-growth company with exit potential, because it’s looking for this big financial return from an IPO or acquisition, and that selects for a certain type of founder. My partner Bryce decided two funds ago [to] look for companies that are kind of disparaged as lifestyle companies that are trying to build sustainable businesses with cash flow and profits. They’re the kind of small businesses, and small business entrepreneurs, that have vanished from America, partly because of the VC myth, which is really about creating financial instruments for the wealthy.

He came up with a version of a SAFE note that allows the founders to buy out the VC at a predetermined amount if they ever become sufficiently profitable, but also gives them the optionality, because periodically, some of them do end up becoming a rocket ship. But the founder is not on the treadmill of: You have to get out.

When you start saying, ‘Okay, we’re going to look for sustainable businesses,’ you look all over the country, and Bryce ended up [with a portfolio] that’s made up of more than 50% women founders and 30% people of color, and it has been an incredible investment strategy.

That’s not to say that people who are African American or women can’t also lead companies that are part of the high-growth VC model that’s typical of Silicon Valley.

No, of course not. Of course they could lead. The talent pool is just much greater [when you look outside of Silicon Valley]. There’s a certain kind of bro culture in Silicon Valley and if you don’t fit in, sure [you could find a way], but there are a lot of impediments. That’s what we mean by structural racism.

To your point about insular networks, a prominent Black VC, Charles Hudson, has noted that a lot of [traditional VCs] just don’t have regular or professional associations with Black people, which hampers how they find companies. How has Bryce fostered some of these connections? Because it does feel like traditional VCs are right now trying to figure out how to better do this.

It’s breaking the geographic isolationism of Silicon Valley. It’s breaking the business model isolationism of Silicon Valley that says: Only things that fit this particular profile are worth investing in. Bryce didn’t go out there and say, ‘I want to go find people of color to invest in.’ What he said was, ‘I want to have a different kind of investment in different places in the United States.’ And when he did that, he naturally found entrepreneurs who reflect the diversity of America.

That’s what we have to really think about. It’s not: How do we get more Black and brown founders into this broken Silicon Valley model? It’s: How do we go figure out what the opportunities are helping them to grow businesses in their communities?

Are LPs interested in this kind of model? Does it have the kind of growth potential that they need to service their endowments?

It was a bit of a struggle when we did fund four, which was focused on [this newer model]. It was about a third of the size of fund three. But for fund five, the fundraising is [going] like gangbusters. Everybody wants in because the model has proven itself.

I don’t want to name names, but there are two companies [in the portfolio] that are kind of in similar businesses. One was in our third fund and was sort of a traditional Silicon Valley-style investment. And the other was an investment in Idaho, of all places. The first company, which involved a more traditional seed round, we’ve ended up putting in $2.5 million for a 25% stake. The one in Idaho we put in $500,000 for a 25% stake, and the one in Idaho is now twice the size of the Silicon Valley one and growing much faster.

So from what you’re seeing, the returns are actually going to be better than with a traditional Silicon Valley venture [approach].

As I said, I’ve been really disillusioned with Silicon Valley investing for a long time. It reminds me of Wall Street going up to 2008. The idea was, ‘As long as someone wants to buy this [collateralized debt obligation], we’re good.’ Nobody is thinking about: Is this a good product?

So many things that what VCs have created are really financial instruments like those CDOs. They aren’t really thinking about whether this is a company that could survive on revenue from its customers. Deals are designed entirely around an exit. As long as you can get some sucker to take them, [you’re good]. So many acquisitions fail, for example, but the VCs are happy because — guess what? — they got their exit.

But now, because funds are raised so quickly, VCs have to show much more traction, which is where things like blitzscaling come in.

Just the way you’re describing it. Can’t you hear what’s wrong with that? It’s for the benefit of the VCs, the VCs have to show, not the entrepreneurs have to show.

Aren’t the LPs addicted to that crack? Don’t they want to see that quick financial traction?

Yeah, but you know that VC returns have actually lagged public markets for four decades now. It’s a little bit like the lottery. The only sure winners are the VCs because the VCs who don’t return their fund get their management fees every year.

A huge amount of the VC capital doesn’t return. Everybody just sees the really big wins. And I know when they happen, it’s really wonderful. But I think [those rare wins] have gotten an outsize place, and they’ve displaced other kinds of investment. It’s part of the structural inequality in our society, where we’re building businesses that are optimized for their financial return rather than their return to society.

Powered by WPeMatico

SoftBank Investment Advisers and WeWork Labs say they’ve officially kicked off the first session of Emerge, an accelerator program designed for underrepresented founders.

In their press release, the companies describe Emerge as “launched by SoftBank with support from WeWork Labs” (that’s the co-working company’s global accelerator program), with a goal of bringing more equality to tech and venture capital.

It’s an equity-free, eight-week program that includes workshops, access to mentors from SoftBank and the WeWork community and sessions with SoftBank executives. It all culminates in a showcase event for investors and SoftBank partners.

The Emerge website describes the program as based in San Mateo, Calif. — but given COVID-19, the sessions and programming are all virtual.

“Supporting underrepresented founders is a top priority for us, ensuring we see more diverse startups across the tech ecosystem,” said Catherine Lenson, managing partner and chief human resources officer at SoftBank Investment Advisers, in a statement. “There is a lack of diversity in the sector as a whole, and we need to do more to address it. That is why we’re excited to launch this program and to see the positive impact that these inspiring founders will have.”

This is also a reminder that while the larger corporate entities are currently embroiled in a legal and financial dispute, WeWork and its largest investor remain closely intertwined.

Here are the 14 startups in the initial program:

Powered by WPeMatico

This isn’t the first economic downturn All Raise CEO Pam Kostka has been through.

“I was here during the dot-com bust and rush, and here during the financial fallout that happened, so we’re a little overdue for some corrective action in the market,” Kostka said. “While I’ve been through boom and bust cycles before, this one is more meaningful because life and death are associated with it.”

All Raise is a nonprofit that focuses on increasing diversity within venture capital, both from a decision-maker and a deal perspective. It recently released its annual report, and we covered how female-founded startups landed more deals than ever before in 2019, per PitchBook data.

After our piece looking at the numbers came out, however, some readers weighed in that our coverage missed the mark: In the headline, did we focus too much on progress and not enough on what is left to be done?

Because we’re both social distancing, I caught up with Kostka on the phone and got her take on how to report numbers around diversity without glossing over the work that remains to be accomplished. We also discussed how to stay optimistic during a downturn, potential innovation that might come out of COVID-19 and why diversity matters now more than ever.

Powered by WPeMatico

Like most investors, I am a little too obsessed with unicorns.

But not just the Silicon Valley kind. As the mother of a five-year-old daughter, my interests also veer in a pink, sparkly direction. So it should not be all that surprising that I recently found myself in a dusty corner of the internet where die-hard unicorn fans go to spread their wings.

It was there, deep in the My Little Pony forums, that one question stopped me in my tracks: “is a male alicorn possible in the future?1”

An alicorn, for those uninitiated to the mythological particulars, is the rare winged, female version of a traditional unicorn.

My Little Pony popularized the term, and the fan forum on which user “Green Precision” asked his question back in 2015 had some interesting answers to the particulars of this philosophical dilemma.

Shadow Stallion responded immediately, “I don’t think a male Alicorn will be possible in the future. Not because its [sic] not wanted or because its [sic] not genetically possible…but generally when male characters are introduced to a show where female characters are prominent, things get ugly.”

Malinter posited, “they probably do but given the female-to-male ratio of Equestria2 they are probably exceptionally rare. The real problem for a male alicorn is not that they exist but where is their place in the world? …Our male alicorn has some pretty big hoof prints to fill in while at the same time not make a trainwreck of established lore.”

Wind Chaser went straight from unconscious bias to conscious bias in their response: “aesthetically a male alicorn just wouldn’t look right, because their bodies are already naturally larger than females, thus the wings would cause an imbalance to the design.”

But it wasn’t all bad news.

“Until it’s proven otherwise, it’s safe to say that something like a male alicorn is possible,” responded Geek0zoid. Crysahis agreed. “Overall yes, I believe there could be a male alicorn it may just take a while to actually happen!”

It doesn’t take a PhD in philosophy from Stanford or the one lone female investing partner at Sequoia3 to posit that these same conversations were probably happening all over Sandhill Road in December of 2009, as male VCs discussed whether female unicorns could actually happen4.

As we move into 2020, though, we’re about to see a pink, winged stampede.

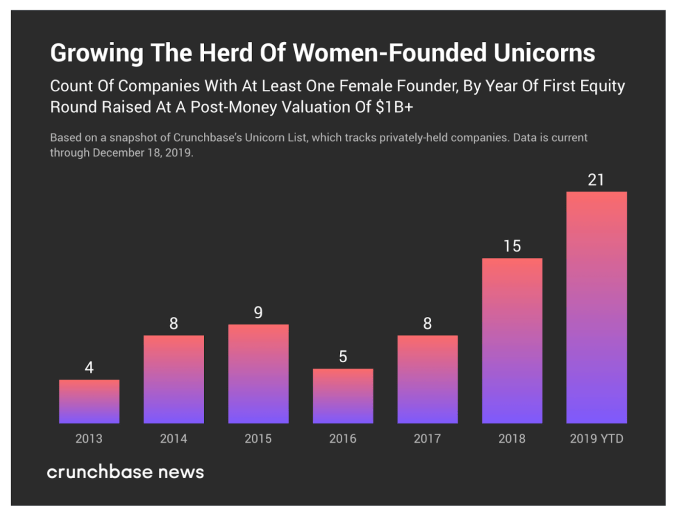

Just look at the recent trends. In 2019, more female-funded unicorns were born than ever before.5 And things are only looking up. (I’m looking at you, ClassPass!)

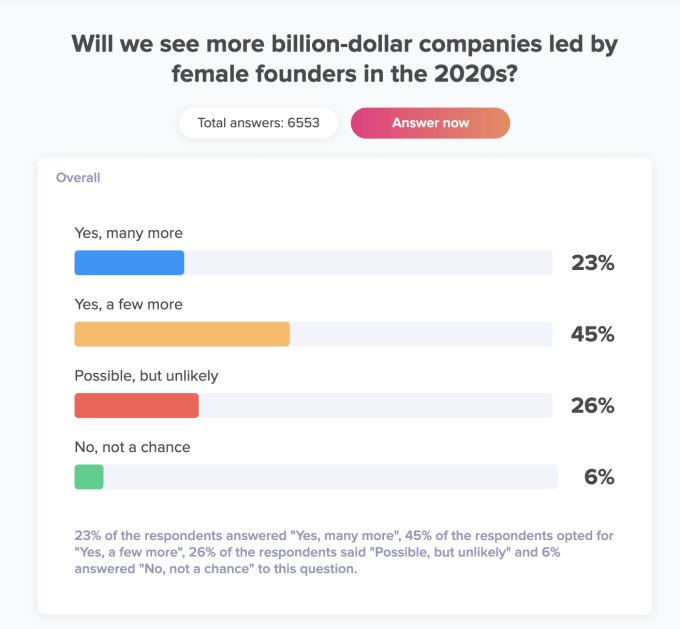

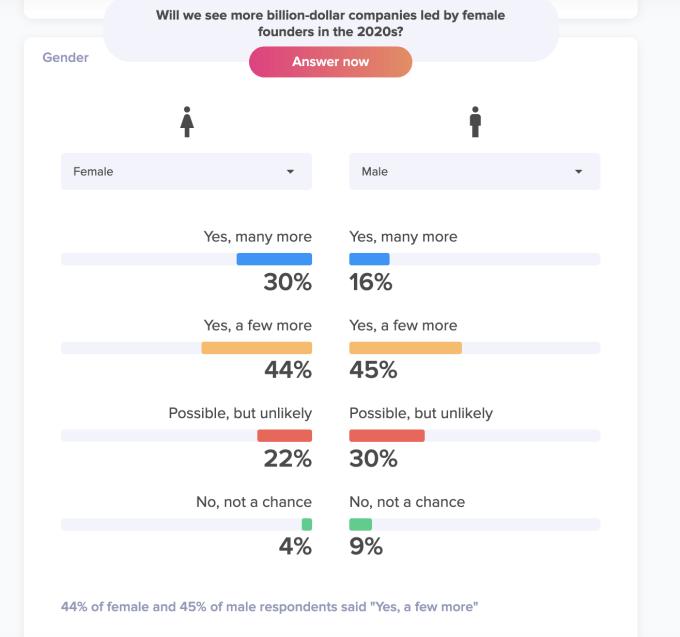

Public opinion agrees. Alongside TruePublic, where I am an advisor and angel investor, I ran a study asking if people believed we would see more female-led unicorns in the 2020s.6 At the time of this article, 68% of the 6,500 respondents said they believed we would see more, with 30% of women responding “many more” (as opposed to only 16% of men). Only 4% of women, but 9% of men, responded “no, not a chance.”7

Kaben Clauson, founder and CEO, says “to represent Gen Z, Millennials and Gen X, TruePublic needs a weighted sample of roughly one thousand Americans to represent that population of the USA.” This particular study already has 6,500 respondents, making it statistically significant.

In fact, female-founded and female co-founded companies are actually over-indexing for unicorn status despite a lack of investment dollars.

Shelby Porges, co-founder of The Billion Dollar Fund for Women, explains: “Recent tracking has shown that female-founded companies represent 4% of all unicorns. That’s astonishing considering that in the past couple of years, they have gotten only slightly more than 2% of all venture funding.” Porges, whose group has mobilized more than 80 venture funds to pledge to invest over a billion dollars into women-founded companies, continues, “It demonstrates why we say, ‘when you invest in women, you’re in good company.’ ”

Here are the three reasons I believe a herd of winged female unicorns (OK, alicorns) is coming down the pipeline in the 2020s:

New data reveals that women invest in women at nearly three times the rate that men do and with the (slow) rise in the number of female investing partners at VCV firms, we are poised to see more and more gender-balanced founding teams getting funding.8 Like one male GP at one of the world’s top VC funds said to me when discussing one of the few female partners at his firm, “she always brings us parenting companies.” It might be cringe-worthy if TechCrunch hadn’t declared 2020 “a big year for online childcare” and that same female partner weren’t about to make a big chunk of cash thanks to all the upcoming parenting alicorns she was smartly funding.

Sophia Bendz, a partner at Atomico who also leads the Atomico Angel Program, said, “I’m confident we’ll see more female unicorns in the next decade because there’s a growing wave of ambitious female founders building incredible products and services. There are also more women in VC now and I’ve seen first-hand the impact having female investment partners can have on increasing the amount of investment into female-led companies. The data shows that women invest in women at three times the rate as male investment partners.”

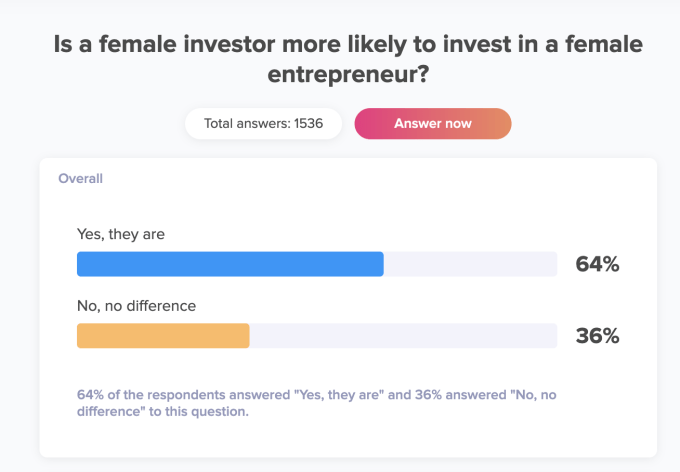

My study at TruePublic coincided with these findings. When asked if a female investor was more likely to invest in a female entrepreneur, 64% of people responded affirmatively (64% of these individuals were women and 63% were men).9

Jomayra Herrera agrees. An investor at Cowboy Ventures (which thanks to Aileen Lee coined the term “unicorn” in the first place), and a volunteer with AllRaise, a nonprofit promoting women in VC, she says: “As the venture industry continues to diversify, especially as it relates to gender and race/ethnicity, I am optimistic that we will see more female-led and people of color-led unicorns over the next decade. We know that diverse teams not only function better, but they are able to see areas of opportunities that more homogenous teams might miss. I think the next generation of investors are more likely to question conventional wisdom, forms of pattern recognition that may lead to bias, and other structural barriers that have historically left out promising entrepreneurs.”

Camila Farani is a well-known investor in Brazil. As founder of G2 Capital, former president of Gavea Angels and a personality on Brazil’s “Shark Tank,” she says “having diverse points of view at the table makes the decision clearer and more certain. People who think differently than you and have other visions of the market, sometimes can show you what you can’t see by yourself.”

She also reminds us not to forget the impact that angel investors can have. “The investments market is still made up mostly of men, but this landscape is changing gradually. It is interesting to see that angel investing is being the most common choice for women who want to make their first investments.”

This trend of investing more in women isn’t just limited to female investors. Susana Robles has spent two decades leading the charge to invest in women in Latin America and alongside Marta Cruz of NXTP Labs is co-founder of WeXchange, a platform that connects women entrepreneurs from Latin America and the Caribbean with mentors and investors.

As Robles says, “I think the world is finally waking up to the fact that there is serious research proving that startups with women co-founders win in all aspects: profitability, as well as greater social and environmental awareness. Investors should want to have this triple win.” She continues, “women tend to return money to investors faster than men, and at the same time, they obtain higher returns. Women are in charge of 64% of all global purchasing decisions on products and services, so having women on C-level positions increases the chance that a startup [will] be highly attractive to a massive market and become a unicorn.”

It also extends to the LPs in the funds. “I also think many investors in funds (mostly DFIs [development finance institutions] but not exclusively) have become more vocal in stating that they don’t want any more to invest in teams led by an all-white, all-male cast who choose startups with all-white, all-male founders.” Jennifer Neundorfer is the co-founder of Jane VC and an investor in Kinside, a parenting app that just raised a $3 million seed round. When describing her fund’s rationale for focusing on female founders, she drops the mic: “we’re going to invest in an under-looked asset class that is overperforming.” Boom.

Another reason we’ll see more female-founded “alicorns” in the 2020s has everything to do with the new markets that female founders are creating. Hunter Walk of Homebrew was one of the initial seed investors in Winnie, an online marketplace for childcare that recently raised a $9 million Series A. At the time, he saw something that others investors didn’t. Winnie co-founder Sara Mauskopf explains, “Four years ago when we started Winnie, parenting and especially child care were not hot investment areas. This has been changing. It certainly helps that more investors are women and are in the thick of their child-bearing and rearing years.”

Part of what Walk says he recognized was the clear founder-market fit displayed by Mauskopf and her co-founder Annie Halsall. As Mauskopf says, “With Winnie, we saw an opportunity to solve the child-care crisis that other founders either did not recognize or did not care to solve. While everyone else was starting crypto and scooter companies, we were building the first-ever tech platform for $57 billion child care industry. Lack of access to quality child care disproportionately impacts women, so it shouldn’t be surprising that it took a female led team to capitalize on this opportunity.” Expanding on the concept of founder-market fit, Walk says, “I love to come away thinking, these are the absolute right founders to build this business.”10

Bendz, the Atomico partner who specializes in femtech and is also an avid angel investor, agrees. “Often I meet founders that you can tell are at the right place at the right time with the right mindset and the right team. It’s almost like all of the experiences they have had prior to launching a company have been preparing them to create that business at that time. These are the kind of founders who I know are in it for the long haul, and who are going to weather the ups and downs.” As a woman who uses the products and services she invests in, Bendz is also an example of investor-market fit, which I believe will open new markets in the decades to come.

Something else investors like Walk and Bendz believe in? Outsized opportunities. And the potential for outsized opportunities are especially ripe in untapped markets. The rise of femtech is yet another example of how the intuitive success of the concept of founder-market fit ultimately needed more female founders for certain markets to blossom. As Bendz explains, “Throughout a woman’s life there are many big events that have a big impact on our overall health — from childbirth to menopause. I know all women are tired of poor or non-existent solutions for women surrounding those life events, and that’s why we are seeing so many companies launching to better serve women’s needs. When you think about the fact that women have only had the right to vote and educate themselves for 100 years, it’s mind-blowing how long the world was operating with only 50% of the population in control. That’s reflected in the products and services we as a society have funded.”

Women’s consumer products are another area. Ornella Moraes is one of four female co-founders of Brazilian-led Sousmile, which recently raised a $6 million USD Series A led by Kaszek Ventures. “Our brand is a woman,” Moraes says of her dental beauty startup that retails throughout São Paulo. And so are the leaders of the company. At Sousmile, there are four female co-founders and two male co-founders. “More dentists in the world are women than men, so it’s been critical for our team to have more female founders,” she says. In this way, the rise of female founders and co-founders can completely change markets. “We believe this will fundamentally create a different type of product,” says Walk.

Finally, certain emerging markets pose a particular opportunity for female founders by over-indexing for both large IPOs and female founders. 2017 was the first year that more of the largest IPOs in the internet sector globally came from emerging markets. Nazar Yasin, founder of Rise Capital, which invests in emerging markets, says “This trend isn’t going away.” After all, most GDP growth comes from emerging markets, where most global internet users live. As he explains, “the future of market capitalization growth in the internet sector globally belongs to emerging markets.” And yet this type of innovation takes resilience. “If you’re a startup in one of these markets, it’s like trying to grow a plant in the desert.”11 In an environment that demands more daily resilience, there is a different appetite for risk and innovation. (I call this resilience innovation.)

Perhaps the easiest example of emerging market innovation fueled by resilience is fintech. Emerging markets and their often unstable economies boast a much higher number of frustratingly unbanked individuals. This brings about innovation. Hanna Schiuma, the Brazilian-born fintech founder of ElasBank, where I am an angel investor and advisor, explains how ubiquitous such fintech innovation is becoming.

“Soon all finance will be tailor-made and fintech will be common ground because all financial services will be technology-intensive.” She also argues that the nature of such an innovation allows the industry to become more innovative, and thus inclusive, which is exactly what is happening with her own women’s bank, launching in 2020. “That means great opportunities to better serve women’s financial needs to offer dedicated products, and to gather female talent to build those products from a diverse and innovative perspective.” Ultimately, “resilience is key for us to build that pool of talent and open the doors for gender balance and financial inclusion.”

Furthermore, data shows Africa and Latin America both beat global averages for percentages of startup female founders. Laura Stebbing is co-CEO of accelerateHER, a global community of leaders addressing the under-representation of women in tech through action. Raised in Southern Africa, Stebbing is passionate about Africa’s rise as a hub of female entrepreneurship.

“Africa has both the highest proportion of women founders at 26% [Latam comes in second]12 and a $42 billion funding gap. There’s clearly no lack of talent across Africa’s 54 countries, so for the investors, corporate executives, policy makers and established founders that aren’t moved by the moral arguments for gender parity, notice the enormous business opportunity. We will start to see a higher volume of resilient, scalable companies emerge as leaders build more diverse networks and ecosystems that support women to unlock their entrepreneurial potential.” Nathan Lustig, founder of Magma Partners, a VC firm in Latin America which invests in female founders above the regional average, explains, “investing in and empowering resilient women entrepreneurs is just good business, and is one of the biggest investment opportunities, especially in emerging markets.”

I believe Latin American can have an edge. I am a Silicon Valley-born investor now living in “Silicon Aires,” where I have been thrilled to see exciting numbers of female founders in Latin America. Susana Robles agrees, and says the reason is in part due to the nature of a committed ecosystem to support one another. “It’s the sheer need that forces you to collaborate.” An ecosystem like Silicon Valley doesn’t have the same need to do so. Of Latin America, Robles says, “In 10 years, we will have created a much more collaborative market than the developed ones.” And that collaboration is leading to great female founders. 2019, in fact, saw more funding going to female co-founders in Latin America than in Europe or the USA.13

This will lead to future alicorns. Ann Williams, COO of Creditas, a Brazilian fintech currently closing in on its own unicorn status, says “the conversion funnel for unicorns works just like any other selection process. We fill the top with a bunch of great women in supporting roles in emerging market startups, these women take their experiences and found rocking new companies. A percentage of these will convert to scaleups raising Series C and D rounds with valuations at $1 billion or higher. And voila! we get women-led unicorns.” She continues, “the odds are with us and I am sure the talent is too!”

Juliane Butty, startup head at Platzi and former regional manager of Seedstars, one of the leading accelerators and investors fostering female entrepreneurship in emerging markets, joins Williams. “We have definitely seen the rise of female founders and investors in emerging markets in the last decade. One supports the other. And we know that success breeds success.”

Perhaps My Little Pony fan Malinter said it best when he suggested how a male version of the alicorn could finally emerge in such a female-dominated space: “The simplest way they could probably add one in would be to make said alicorn the ruler of a neighboring nation.” In the same way, emerging markets may just hold the key for female unicorns.

No matter the region, Robles says “if we keep opening doors to women entrepreneurs who are as ambitious as men in growing their companies, we’ll begin to see many more unicorns with gender diversified teams.” Hanna Schiuma, the Elasbank founder who just might be building the next female-founded unicorn, agrees. “The alicorns are coming. And we’re ready to fly.”

2Equestria is of course where the My Little Ponies and their assorted unicorns, alicorns and friends all live.

3Go Jess Lee!

4Yes, Aileen Lee of Cowboy VC first invented the term in her 2013 TechCrunch piece, but we’re in a unicorn-fueled time machine, people.

8“Do Female Investors Support Female Entrepreneurs? An Empirical Analysis of Angel Investor Behavior,” Seth C. Oranburg, Duquesne University School of Law, Pittsburgh PA, USA and Mark Geiger, Duquesne University School of Business, Pittsburgh PA, USA

12Forthcoming research from TechCrunch/Crunchbase

13Forthcoming research from TechCrunch/Crunchbase

Powered by WPeMatico

Seattle’s Female Founders Alliance, which runs the Ready Set Raise accelerator for women and non-binary founders, has acquired New York’s Monarq, an incubator with similar goals and origins. The latter will be integrated into the former, but it seems to be a happy collaboration rather than a consolidation of necessity.

Monarq was founded three years ago by Irene Ryabaya and Diana Murakhovskaya, and 32 companies have gone through its process. FFA has accepted half that number into its program as of the second cohort, with a third underway for 2020. I covered graduate Give InKind in November when it raised a $1.5 million seed round.

“Monarq and FFA share a common sponsor that introduced us years ago, and we’ve been connected and supportive of each other since,” explained FFA CEO Leslie Feinzaig to TechCrunch. “This year, Diana and Irena’s side gigs started to take off — Diana raised a $20 million VC fund, and Irena’s startup, WarmIntro, started signing up substantial customers. It made strategic sense for FFA to solidify our national expansion and strengthen our network of investors and mentors that are East Coast based.”

Ryabaya and Murakhovskaya will be focusing on The Artemis Fund and WarmIntro respectively, and Monarq’s accelerator will be tucked into the Ready Set Raise brand. The merge will create what FFA claims is the country’s largest network of female and non-binary industry folks, which should prove an asset for those in the program.

It’s possible to see this as consolidation within a specialized branch of the startup industry, but Feinzaig said business is booming.

“The market for women’s leadership is absolutely growing, and creating a lot of opportunities in the process,” she said. “What’s different now is that there is a recognition that this is good business, not a charitable cause.”

The FFA’s stated goal of gender parity among founders only grows more achievable with increased reach. It may be that the increased scale also improves results in an already impressive portfolio.

Powered by WPeMatico

Venture capital investment in all-female founding teams hit $3.3 billion in 2019, representing 2.8% of capital invested across the entire U.S. startup ecosystem this year, according to the latest data collected by PitchBook.

While that number may seem insubstantial, it’s a step up from last year’s total. In 2018, venture capitalists struck 580 deals worth $3 billion — up from just $2.1 billion in 2017 — for all-female teams, or only 2.2% of all U.S. deal activity. So far, female-founded and mixed-gender teams have raised a total of $17.2 billion, with roughly three weeks remaining in 2019. That’s 11.5% of all venture capital investment, an increase from 10.6% last year, when those groups attracted $17 billion across some 2,000 deals.

Crunchbase, another organization focused on tracking and analyzing fundraising data, reported in October that $20 billion in global capital was invested in female-founded and female co-founded startups so far this year. Three percent of global venture dollar volume was funneled toward female teams, Crunchbase said, and 10% toward teams of women and men.

Despite efforts from female founders, venture capitalists and diversity advocates in Silicon Valley and beyond, female entrepreneurs continue to struggle to raise as much capital as their male counterparts. The lack of equity in VC is in part caused by the lack of women on the other side of the table; venture capital funds still employ very few women.

Although dozens of firms have made concerted efforts to diversify their ranks, fewer than 10% of decision-makers at U.S. VC firms are women, according to a 2019 Axios analysis, which determined just 105 investors out of 1,088 were female. While the study noted an increase from the previous year’s 8.93% and 2017’s 7%, it proved venture capital is still very much a male-dominated industry.

Carta, a venture-backed company that provides startups tools to manage their equity, released its second annual gender equity gap study last month, noting that male founders and employees still receive significantly more equity wealth than women. Men have 64% of all startup equity, according to Carta’s findings, and represent 80% of cap table millionaires. Carta used data from 320,000 employees, some 10,000 companies and 25,000 founders to determine these results, which paint a disappointing picture for women at startups.

Another venture-backed company, Tide, conducted its own study around female founders this year. The study focused on entrepreneurs in the U.K. and U.S., which both struggle with diversity in entrepreneurship. Tide determined that of the 403 degrees obtained from universities in the U.K. by female founders, roughly a quarter were from the University of Cambridge and the University of Oxford, the country’s top schools. Of the American entrepreneurs included in the study, most went to Stanford University, MIT or Harvard University. The conclusion? Of the female founders who ultimately succeed in raising funding from private investors, most are graduates of elite universities, suggesting a certain socio-economic status. Of course, accessing capital is even more difficult for entrepreneurs who do not attend top universities and who therefore struggle to gain access to investor-friendly networks.

New analysis on the backgrounds of female founders with at least $1M in backing. Turns out going to Stanford is helpful! https://t.co/YaP3b8u1QM @TideBanking pic.twitter.com/u2vcMKrfGJ

— Kate Clark (@KateClarkTweets) September 10, 2019

The diversity issue in VC expands beyond women. While several funds have cropped up with a mission to back female founders exclusively, including Female Founders Fund, BBG Ventures, Halogen Ventures, Jane VC, Cleo Capital, accelerator program Ready Set Raise or XFactor Ventures, minority entrepreneurs, including men of color, struggle to secure financing. And while companies like PitchBook and Crunchbase track gender, they do not track race, making it difficult to understand the size and scale of the race funding gap.

On a mission to close that gap, firms like Harlem Capital invest in minority entrepreneurs and organizations like BLCK VC seek to provide community for black venture investors. The New York-based team behind Harlem Capital announced a $40 million debut fundraise last month, one of the largest-ever pools of capital for a fund with a diversity mandate. Harlem, similar to BLCK VC, hopes to attract more minorities to venture capital, where the vast majority of deal makers are white or Asian men.

“You need diversity funds like ourselves to get this market anywhere close to parity,” Harlem Capital managing partner Jarrid Tingle told TechCrunch last month.

Other efforts focused on women in VC and technology include All Raise, which hired its first chief executive officer in Pam Kostka earlier this year. 2019 has been a banner year for the nonprofit organization focused on increasing representation across the entire tech ecosystem. Not only did it bring its first official leader and several employees, it announced new chapters in Los Angeles and Boston, launched a program called VC Cohorts and hosted its annual conference, several in-person and virtual fundraising workshops and networking sessions.

“Women are hungry for the support and guidance we provide,” All Raise’s Kostka told TechCrunch in October. “I think the movement is just gathering momentum.”

Large and growing “unicorn” startups founded by women have also helped move the needle this year, proving companies led by women can gain support from Silicon Valley’s elite. PitchBook notes Glossier and Rent the Runway, two companies founded and led by women, as examples of new entrants to the unicorn club (companies with valuations of $1 billion or larger).

Glossier landed a $100 million Series D led by Sequoia Capital, with participation from Tiger Global and Spark Capital in March. The round valued Emily Weiss’ business at a whopping $1.2 billion. News of Rent the Runway’s $125 million round led by Franklin Templeton Investments and Bain Capital Ventures came just a couple of days later. The deal valued the clothing rental company at $1 billion.

The newest data may indicate progress, but all-male teams still raised more than 85% of all U.S. venture capital dollars in 2019, while decision makers at venture capital firms were still more than 90% male. The venture capital industry, as it stands, is still a boy’s club.

Powered by WPeMatico

As the world grows increasingly digital, the craving for face-to-face connections is surging. Squad, an invite-only community and app, is trying to fill the need for offline connections by curating tight-knit events for Gen Z and Millennials.

“It mimics building relationships in real life,” says founder and CEO Isa Watson.

It’s an idea that investors are already backing: Squad closed a $3.5 million seed round and plans to raise its Series A in early 2020, but the road to securing that round was anything but easy. During a conversation on the How I Raised It podcast, Watson shared the ups and downs of her unique path to fundraising.

She started by putting some of the earliest capital into the business herself with support from her family. She then worked her way through more than 200 meetings in Silicon Valley to build up her credibility as a founder — a step that she can’t stress enough — before Squad even started its official seed round.

“Despite the fact that I went to MIT, despite the fact that I managed a billion-dollar product at JPMorgan Chase and even built a huge digital product, I was still a Silicon Valley outsider,” Watson says.

People sometimes have the perception that being an alumni at a top U.S. university will mean they can go to Silicon Valley and just be “in,” Watson explains, but that’s not quite how it works.

“It takes a lot of work and a lot of credibility building,” she says. “That’s what I was doing for a few years before we actually did our official seed round. By the time I did it, it was like my reputation preceded me and there was enough familiarity with me.”

Isa Watson, Squad founder and CEO

Despite taking more than 200 meetings in her efforts to crack Silicon Valley, Watson never took a cold meeting.

“Cold outreach is a tactic that I see a lot of founders using,” she says, “whereas I would argue that the more effective introduction comes from someone who knows someone.”

Leveraging the connections she built was critical in connecting Watson to her eventual funders. “They’re all referring you to the next three people to talk to,” Watson says. “It becomes like tree branches and then a network that’s growing in a multiplicative fashion.”

One of Squad’s earliest investors was Steven Aldrich, who at the time was working as chief product officer at GoDaddy . Both Aldrich and Watson grew up in North Carolina, and Steven’s father shared hometown roots with her, which helped her make the initial connection.

“It was about consistently making connections like that,” she says. “Steven introduced me to three people, and then those three other people introduced me to two people. And that’s essentially how I got the ball rolling.”

Not all meetings need to be about meeting for coffees or lunches, either — Watson took plenty of calls while expanding her network, as well. But the important step was making those connections, which was “a really hard hustle and grind, head down,” for the first two years.

When meeting people in Silicon Valley or expanding her network of prospective funders, Watson didn’t tease future funding rounds or send off vague meeting requests.

In trying to build out her network, she first researched a couple of key things: who did she need to know in order to build a really strong product, and who did she need to know in order to have solid distribution or growth marketing? Once she identified those folks, she would reach out to them individually and ask them for specific advice in their area of expertise.

“People always say, ‘When you want money, ask for advice. If you want advice, ask for money,’” Watson says. “Being super-explicit in the ask and explaining how you’ll spend their time and their brain space is super important.” No one has time for a generic request like, “Hey, can I pick your brain?”

When you’ve connected with someone, you should always ask them for recommendations for experts in specific areas — like growth marketing, product, etc. If they volunteer a few names, ask if you can send an email that they could forward on to introduce you to those individuals.

Following the introductions, it’s important to remember that it’s not just a “one and done,” as she says. Once you’ve met with someone through an introduction, follow up: let them know how the meetings went and thank them again.

“It’s like really, really intense relationship management, and it’s something that people with the highest EQ do best,” says Watson. “I would identify my needs, make specific asks … and then I would make sure to explicitly ask if they did not offer for three other intros for people that could be helpful, that would be excited about what we’re doing.”

When she realized it was time to start raising money for Squad, her first move was to identify her “quarterback for fundraising” — in this case, Charles Hudson from Precursor Ventures. It’s helpful, according to Watson, to not have “too many cooks in the kitchen,” or else you’ll end up with far too many opinions that don’t align.

Hudson had already invested a small amount of money in Squad at the time, but he quickly became the person Watson went to for feedback on her pitches. He counseled her on other aspects of running a process.

“One thing Charles tells me is that, with fundraising, you’re likely only going to be successful if that’s your core focus at that time,” Watson says. “It’s not something you can do passively.”

So Hudson and Watson sat down and came up with a list of 35 target venture capitalists. He introduced her to five who she didn’t expect to be a good fit. They first went with the ones they didn’t expect would be a perfect match so she could gather feedback and see if Squad was actually ready to raise capital.

Of those first five meetings, one or two “were complete dings” and turned Squad down outright — but Watson made it to partner meetings in the three other meetings, a sign that VCs were seriously considering Squad.

Based on that feedback, Hudson introduced Watson to 10 more VCs — and shortly after, she met Michael Dearing at Harrison Metal, who led Squad’s seed round.

After Dearing offered up a term sheet of $3 million, Watson quickly had offers from other VCs.

“It’s funny because it took me deliberately being in the market for fundraising for like two and a half months to get that ‘yes’ from Michael. Before that, I had no cash really committed,” she says. “And then after just a few days of letting people know I had a term sheet for $3 million, I had like $6 million on a table. VCs are such followers.”

With that many offers on the table following Dearing’s lead, Watson was in the enviable position of needing to pick who she’d let into the seed round. So how did she choose?

“The first thing is value add,” Watson says. She asked herself: “did I feel like I had the right assortment of value? I maybe want someone in there who’s really strong on product; I may want someone who’s really strong at growth, strong at marketing.”

Her second criteria for making the decision was a less resume-focused. Simply put, she went with her gut.

“One thing that founders really, really underestimate is — is this person a good human being? I went with the people that I had felt most comfortable with, the people who I felt I could trust based on my interactions with them, and who were just supportive along the way.”

Powered by WPeMatico