TechCrunch Include

Auto Added by WPeMatico

Auto Added by WPeMatico

In the aftermath of George Floyd’s death and widespread protests for racial justice, a number of venture capitalists made public statements about wanting to improve diversity in the tech industry — and more specifically to fund more diverse founders.

Their comments are certainly worth applauding, but actual change is a lot harder. And if it comes at all, it will take time. In the meantime, how can Black founders navigate a tech and venture capital industry where they have historically been underrepresented, overlooked and worse?

To answer that question, we’ll bring three Black founders together at Disrupt 2020 from September 14-18 who can speak directly about their experience raising funding and launching startups.

One of our speakers, Michael Seibel, is now funding startups himself as partner and CEO of startup accelerator Y Combinator. Before that, however, he was co-founder and CEO at Justin.tv (which became game streaming giant Twitch) and then at its spin-off, Socialcam (which was acquired by Autodesk). So he can talk about both sides, as both a founder and investor.

Joining Seibel will be two YC startup founders — Reham Fagiri of furniture marketplace AptDeco and Songe LaRon of barbershop software maker Squire. We’ll talk to all three of them on the Extra Crunch stage, getting as specific and tactical as possible about what Black founders can expect and what steps they can take to succeed.

Learn more at Disrupt 2020, which runs from September 14-18. Buy the Disrupt Digital Pro Pass, or if you’re an early-stage founder a Digital Startup Alley Exhibitor Package, today and get access to all the interviews on our Main Stage, workshops over on the Extra Crunch Stage, where you can get actionable tips, as well as CrunchMatch, our free, AI-powered networking platform. As soon as you register for Disrupt, you will have access to CrunchMatch and can start connecting with people. Use the tool to schedule one-on-one video calls with potential customers and investors or to recruit and interview prospective employees.

Powered by WPeMatico

A few years ago, I came to the realization that my company, an HR consulting firm, was not as diverse as I wanted it to be. I value diversity because I know it makes teams better — more creative, more productive and more nimble. It helps my firm represent our community and serve our clients.

Though I tried to be inclusive in the language and the images I used on my website, in social media and when posting job openings, clearly something wasn’t working. I’m fortunate to know many talented diversity, equity and inclusion (DEI) experts. I asked them what I needed to do differently to attract a broader and more diverse pool of candidates. Here’s what they told me.

This may seem obvious, but it’s actually something many companies don’t do. When we talk about diversity, people tend to think only of race and gender. Our definition of diversity can be narrow, and we fail not only to include physical ability, gender identity and a host of other underestimated groups, but to recognize that even within a company, who is well represented versus underrepresented can vary by team or department.

I noticed a lack of diversity among my team of coaches; it was all women, but there were few women of color. The gender imbalance is not a surprise; according to the International Coaching Federation (ICF), approximately two-thirds of coaches are women. It would have been all too easy to throw up my hands and say “Well, there just aren’t enough qualified male coaches.” But blaming the pipeline is not a valid excuse and doesn’t fix the problem.

If I told people, “I’m trying to increase diversity on my team,” they would not have known what I meant; they would have been left to assume. Instead, I reached out to a small group of coaches who I know and trust, and told them “I’m looking for more coaches. Specifically, I would like to add women of color and I’d also like to have more men on the team.”

In the U.S., where we’ve been taught for so long not to talk about race or gender while hiring, this felt awkward. I had to push past that, and I’m thankful I did. The result was that I was not only able to add a number of experienced coaches to my team, I also built a whole new network of talented, diverse coaches from whom I continue to learn.

When you want to appeal to the most diverse candidates, language matters. It is (hopefully) obvious that terms like rock star, stud and ninja, which have been used all too frequently in job descriptions, are exclusive and off-putting to many candidates. But other words and phrases to use or avoid aren’t always common sense. The most appealing language can vary by job level, title and even geography.

Using a tool like Textio will help you create a job description that welcomes the most candidates to apply. Textio uses machine learning and algorithms from millions of job descriptions to help you spot and remove language that can unintentionally narrow your pool. Pop in your job description and you’ll get recommendations about the optimal length of your JD, word choices that skew masculine or feminine, sentence length and even whether your job suggests a fixed or growth mindset.

We’ve all seen the old equal employment opportunity (EEO) statement at the end of a job posting, which reads: “We’re an equal opportunity employer. All applicants will be considered for employment without attention to race, color, religion, sex, sexual orientation, gender identity, national origin, veteran or disability status.” It sounds like it came right off the government website, which it probably did. And that’s exactly how it comes across to candidates — like a canned message that you’ve added just to make sure you’re in compliance.

Did you know that you can customize your EEO statement? People do read it, and sticking with the legal jargon can be off-putting. A generic statement doesn’t say anything positive about your brand, and it doesn’t demonstrate a true commitment to diversity. If you haven’t already, now is the perfect time to update your statement, making it more reflective of your culture and values. For example:

“SurveyMonkey is an equal opportunity employer. We celebrate diversity and are committed to creating an inclusive environment for all employees.”

Is it worth the effort? According to FairyGodboss, these personalized EEO statements “…communicate an employer’s dedication to unbiased recruiting, hiring and employment practices, which may encourage traditionally marginalized groups to seek employment within the organization.”

Most people are familiar with unconscious bias, and how it can negatively impact every step of the hiring process. Even as early as the resume review, bias causes recruiters and hiring managers to favor resumes of candidates who are in the majority. Bias can result from information ranging from a candidate’s name to which college they attended or which sports they played.

For instance, those with white-sounding names receive preference. The National Bureau of Economic Research found that “Job applicants with white names needed to send about 10 resumes to get one callback; those with African-American names needed to send around 15 resumes to get one callback.” I have a friend from India who received similar treatment. Even though she had worked with well-known companies, including Google and Deloitte, she had difficulty landing a job when she first came to the U.S. When she was ready to change employers, she adopted an American nickname on her resume and LinkedIn profile, and promptly got five callbacks.

In a blind resume review, identity cues that indicate race or gender are hidden. Tools like TalVista do this automatically, or your team can do it manually by hiding the information. While this helps increase the number of diverse candidates who make it to the next step, it does not address bias that occurs during interviews or later in your hiring process. That’s going to require training.

People from underestimated groups are all too familiar with the phrase “you have to see it to be it.” If I can’t see myself as someone who will be welcome and included in your company, I’m far less likely to join it. Yet too often even when a candidate meets with multiple interviewers, none of those interviewers reflect the candidate’s race or gender.

Imagine a woman of color spending the better part of a day meeting with a potential employer. Over the course of several hours, she meets a number of leaders but she doesn’t meet a single woman of color. She might think there are no women of color in the company, or wonder why they are not included in important decisions like interviewing and hiring.

When Karenga Ross interviewed at Intel after meeting them at a National Society of Black Engineers conference, she was pleasantly surprised to meet two African American women on the interview panel — these were women who looked like her. “It’s nice to be able to look across that table and see someone whom I can aspire to be. I can see someone who looks like me. It was refreshing. It was inspiring.”

One question I get from small companies is how to assemble a diverse interview panel if they don’t yet have diversity within their organization. I encourage them to cast a wide net. Think about who’s affiliated with your company, even if they’re not employees. If you have diverse advisors, investors or board members who are willing to help, invite them to join your panel. It will improve the candidate experience and help eliminate bias from your decision making.

Increasing diversity is an important investment that takes commitment, and a willingness to learn and experiment. You’ll have to try out some new things, and perhaps have conversations that make you uncomfortable. Remember to take one step at a time, and measure your progress and results.

Diverse hiring is one important step toward increasing diversity in your organization. Retention, however, depends on all employees feeling a sense of belonging. Remember to review your internal practices and policies to make sure they too meet the test of inclusion.

Powered by WPeMatico

Valence, the Los Angeles-based online community dedicated to increasing economic opportunity for the Black community, has raised $5.25 million in financing as it looks to continue to expand its network for Black professionals in all fields.

The timing for the investment is critical as the country reckons with the implications and effects of systemic racism. In no field is the under-representation of Black professionals more deeply felt than the tech industry, where lack of diversity can have profound implications on products and services that are becoming increasingly central to large swaths of the economy.

Problems with under-representation and underlying issues of systemic racism manifest in facial recognition technologies, social networking applications and decision-making software for lending and credit that are aspects of how American society functions.

It’s with an eye toward technology and entrepreneurship that Valence raised its most recent round, according to a letter sent to the company’s users by new chief executive officer Guy Primus.

“Now that we have the capital that we were seeking, we will be doing three things. First we will improve the current product. We are very proud of what we have built thus far, but we know there are a few issues. We will continue to address those issues and will accelerate work to enhance technical performance on the platform,” Primus wrote. “Second, we will be expanding the team. We expect the team to more than triple in the coming months so that we can better serve you. Finally, we’ll be adding features and expanding our services. We will be delivering additional tools that facilitate even more meaningful connections and will expand Valence’s scope to include the professional growth and development of our members.”

A lot of that product development will go toward building tools that can help with professional development and career growth.

“We’re being very targeted in how we can drive economic opportunity and wealth creation in the black community,” said Valence co-founder and Upfront Ventures general partner Kobie Fuller.

Already, Valence has brought on some of the top names in Silicon Valley as participants in a program to promote entrepreneurship and career development.

Valence currently has 10,000 people signed up for the platform and is growing at about 20% per month, according to Primus. The goal is to serve educational advice and tools to Valence users while at the same time making that group of career-minded Black professionals available to companies that would want to hire them.

Primus said that Valence will be selling its database and access to companies that would want to find prospective hires on the platform in a per-seat licensing model that would be accessible to headhunters and human resources departments.

The new investment round was led by GGV Capital, the international investment firm whose investments include Slack, Peloton, Wish and StockX. Hans Tung, the managing director who invested in those marquee deals, will be joining the company’s board of directors.

Other investors in the round include Upfront Ventures, along with Maveron, the SoftBank Opportunity Fund and Silicon Valley Bank.

Powered by WPeMatico

“What happens after a company gets called out?” he asked over the phone. “Do you know what happens to the people in-house that come forward?”

I didn’t.

A Black male engineer at a fashion tech company who wished to remain anonymous was telling me how he’d been passed over for promotions white counterparts later received after they’d pursued risky and unsuccessful projects. At one point, he said management tasked him with doing recon on a superior who made disparaging comments about women because his subordinates were uncomfortable reporting it directly to HR.

When human resources eventually took up the matter, the engineer said his participation was used against him.

More recently, his company brought furloughed employees back and managers promoted a younger, white subordinate over him. When he asked about the move, his direct supervisor said he was too aggressive and needed to be more of a role model to be considered in the future.

In the absence of industry leadership, there’s no blueprint to remedy institutional problems like these. The lack of substantial progress toward true representation, diversity and inclusion across several industries illustrates what hasn’t worked.

Audrey Gelman, former CEO of women-focused co-working/community space The Wing, stepped down in June following a virtual employee walkout. Three months earlier, a New York Times exposé interviewed 26 former and current employees there who described systemic discrimination and mistreatment. At the time, about 40% of its executive staff consisted of women of color, the article reported.

Within days, Refinery29’s EIC Christene Barberich also resigned after allegations of racism, bullying and leadership abuses surfaced with hashtag #BlackatR29.

In December 2019, The Verge reported allegations of a toxic work environment at Away under CEO Steph Korey. After a series of updates and corrections in reporting, it seemed she would be stepping away from her role or accelerating an existing plan for a new CEO to take over. But the following month, she returned to the company as co-CEO, sharing the statement: “Frankly, we let some inaccurate reporting influence the timeline of a transition plan that we had.”

Last month, after Korey posted a series of Instagram stories that negatively characterized her media coverage, the company again announced she would step down.

Bon Appétit former editor-in-chief Adam Rapaport resigned his position the same month after news broke that the cooking brand didn’t prioritize representation in its content or hiring, failed to pay women of color equally and freelance writer Tammie Teclemariam shared a 2013 photo of Rappaport in brown face.

In a public apology, staffs of Bon Appétit and Epicurious acknowledged that they had “been complicit with a culture we don’t agree with and are committed to change.”

Removing one problematic employee doesn’t upend company culture or help someone who’s been denied an opportunity. But with so much at stake when it comes to employing Instagram-ready branding, the lane is wide open for companies to meet the moment when it comes to doing the right thing.

A 2017 report by the Ascend Foundation found few Asian, Black and Latinx people were represented in leadership pipelines, and at that point, the numbers were actually getting worse. Seemingly, in an effort for transparency and accountability to do better, 17 tech companies shared diversity statistics and their plans to improve with Business Insider in June 2020. The numbers were staggering, especially for an initiative supposedly prioritized industry-wide in 2014:

Underrepresented minorities like Black and Latinx people still only make up single-digit percentages of the workforce at many major tech companies. When you look at the leadership statistics, the numbers are even bleaker.

While tech’s shortcomings show up clearly in a longstanding lack of diversity, companies in other industries polished their brands sufficiently to skate by — until COVID-19 and the call for racial justice after George Floyd’s murder called for lasting change.

In June, Adidas employees protested outside the company’s U.S. headquarters in Portland, Oregon and shared stories about internal racism. Just a year ago, The New York Times interviewed current and former employees about “the company’s predominantly white leadership struggling with issues of race and discrimination.”

In 2000, an Adidas employee filed a federal discrimination suit alleging that his supervisor called him a “monkey” and described his output as “monkey work.” When spokesperson Kanye West said in 2018 that he believed slavery was a choice, CEO Kasper Rorsted discussed his positive financial impact on the brand and avoided commenting on West’s statement.

In response to the internal turmoil at Adidas, the brand originally pledged to invest $20 million into Black communities in the U.S. over the next four years, increasing it to $120 million and releasing an outline of what they plan to do internally, Footwear News reported.

On June 30, Karen Parkin stepped down from her role as Adidas’ global head of HR in mutual agreement with the brand. In an all-employee meeting in August 2019, she reportedly described concerns about racism as “noise” that only Americans deal with. She’d been with the brand for 23 years.

Routinely protecting employees perceived as racist, misogynistic or abusive is bad for business. According to a 2017 “tech leavers” study conducted by the Kapor Center, employee turnover and its associated costs set the tech industry back $16 billion.

POC experience-centered social and wellness club Ethel’s Club invested into its community’s well-being and has not only managed to stay open (virtually) through the COVID-19 pandemic, it has managed to grow. Meanwhile, The Wing lost 95% of its business.

So, what really happens after the companies are called out? Often, the bare minimum. While the perpetrators of the injustice may endure backlash, abusers in corporate structures are often shifted into other roles.

Tiffany Wines, a former social media and editorial staffer at media/entertainment company Complex, posted an open letter to Twitter on June 19 alleging that Black women at the outlet were mistreated, sharing a story in which she claimed to have ingested marijuana brownies left in an office that was billed as a drug-free environment. Wines said she blacked out and accused superiors of covering up the incident after she reported it.

Her decision to speak up prompted other former employees to share stories alleging misogyny, racism, sexual assault and protection of abusers. One anonymous editor said she was asked if she would be comfortable with a workplace that had a “locker room culture” during a 2010 interview. (She did not end up working there.)

Complex Media Group put out a statement four days later on its corporate Twitter account, which had approximately 100 followers — as opposed to its main account, which has 2.3 million followers.

“We believe Complex Networks is a great place to work, but it is by no means perfect,” read the statement. “It’s our passion for our brands, communities, colleagues, and the belief that a safe and inclusive workplace should be the expectation for everyone.” It went on to state that they’ve taken immediate action, but it’s unclear if anyone has been terminated. [Complex is co-owned by Verizon Media, TechCrunch’s parent company.]

Members of the fashion community have formed multiple groups to combat systemic racism, establish accountability and advance Black people in the industry.

Set to launch in July 2020, The Black In Fashion Council, founded by Teen Vogue editor-in-chief Lindsay Peoples Wagner and fashion publicist Sandrine Charles, works to advance Black individuals in fashion and beauty.

The Kelly Initiative is comprised of 250 Black fashion professionals hoping to blaze equitable inroads, and they’ve publicly addressed the Council of Fashion Designers of America in a letter accusing them of “exploitative cultures of prejudice, tokenism and employment discrimination to thrive.”

Co-founders of True To Size, Jazerai Allen-Lord and Mazin Melegy, an extension of the New York-based branding agency Crush & Lovely, started offering their Check The Fit solutions to the brands they were working with in 2019. The initiative is an audit process created to align in-house teams and ensure sufficient representation is in place for brands’ storytelling.

Check The Fit determines who the consumer is, what the internal team’s history is with that demographic and the message they’re trying to communicate to them, and how the team engage’s with that subject matter in everyday life and in the office. Melegy says, “that look inward is a step that is overlooked almost everywhere.”

“At most companies, we’ve seen a lack of coherence within the organization, because each department’s director is approaching the problem from a siloed perspective. We were able to bring 15 leaders across departments together, distill through a list of concerns, find points of leverage and agree on a common goal. It was noted that it was the first time they were able to feel unified in their mission and felt prepared to move forward,” Lord says of their work with Reebok last year.

Brooklyn-based retailer Aurora James established the 15 Percent Pledge campaign, which urges retailers to have merchandise that reflects today’s demographics: 15% of the population should represent 15% of the shelves.

During the melee that transpired largely on Twitter and Instagram only to attempt to be reconciled in boardrooms, one Condé Nast employee and ally has been suspended. On June 12, Bon Appétit video editor Matt Hunziker tweeted, “Why would we hire someone who’s not racist when we could simply [checks industry handbook] uhh hire a racist and provide them with anti-racism training…” As his colleagues shared an outpouring of support online, a Condé Nast representative said in a statement, “There have been many concerns raised about Matt that the company is obligated to investigate and he has been suspended until we reach a resolution.”

Simply reading through accusers’ first-person accounts, it often seems like these stories end up on public forums because little to nothing is done in favor of the people who step forward. The protection has consistently been of the company.

The Black engineer I spoke to escalated his concerns to his company’s CEO and said the executive was unaware of the allegations and seemed deeply concerned.

Seeing someone who seemed genuinely invested in doing the right thing “obviously, means a lot,” he said.

“But at the same time, I’m still really concerned knowing the broader environment of the company, and it’s never just one person.”

Powered by WPeMatico

From healthcare, to education, to human rights, tech has the potential to drive social impact at scale. In this moment of global pandemic, growing economic insecurity and an uprising against racial injustice, the need for scalable solutions is greater than ever. But there are lessons we’ve seen founders learn the hard way time and again.

In the spirit of reaching impact at scale faster, we rounded up our top five lessons to take to heart if you want to turn your world-changing idea into a tech nonprofit. Distilled from The Tech Nonprofit Playbook, a free guide to starting a social impact startup, we drew from the learnings of tech nonprofits whose work has transformed their sectors.

You have a big idea. You’ve identified a social problem you can’t help but try to fix, and you think you just might have a world-changing, tech-driven solution. But you can’t solve the issue you’ve identified without a deep understanding of the community you’re serving. Not doing so is a recipe for failure. If you haven’t lived the problem, bring on a co-founder who has. Then, go meet others who have firsthand experience with the problem. Interview these individuals with a user-centered lens to allow insights and opportunities to reveal themselves.

To see this in action, consider Upsolve, the TurboTax for chapter 7 bankruptcy, helping low-income Americans recover from crippling financial crises. During their user research phase, the co-founders asked brick and mortar legal aid organizations for their waitlists, and passed out their cards in legal aid clinics where people were seeking help around debt lawsuits. These strategies enabled Upsolve to consider a broad sample of perspectives and develop a deep understanding of the problem from the users’ point of view. Don’t skimp on this — your user research should inspire and inform your initial product idea.

Now, it’s time to put your product idea to the test by piloting a minimum viable product, or MVP — an early version of a product that surfaces learnings about your users with little effort. Your MVP needn’t be a fully fleshed-out product. In Upsolve’s case, it was a physical space where they helped users file for bankruptcy in real life. Run a small-scale pilot of your MVP to confirm, deny or alter your hypothesis. Once you’ve piloted your MVP for enough time that you’re confident you have a viable solution, it’s time to build a beta product.

To build your beta product, or an almost ready-to-launch product, leverage existing tech solutions to address your new use case — don’t start from scratch. For Upsolve, it was a Typeform, an online plug-and-play form. From less technical products like website and communication tools, to more technical ones like app development tools, databases and APIs, piecing together existing tech building blocks will drive your startup costs down and ultimately make it easier to maintain your product. With your solution out in the world, build user feedback into your product as you continue testing, refining and iterating to more closely serve your mission.

Being a tech nonprofit comes with a pretty unique set of advantages that, when leveraged, are what we like to call nonprofit judo. A critical nonprofit judo tactic is forging aligned partnerships with other organizations, funders and companies to create mutually beneficial relationships that drive sustainability for your tech nonprofit and increase user acquisition.

Take CareerVillage.org, which crowdsources career advice for millions of underserved youth. For the first few years, recruiting volunteers and fundraising each took a lot of the founding team’s time. But a solution arose when they learned that Fortune 500 companies were looking for easy and scalable volunteering programs for their employees. CareerVillage.org built a sustainable “earned income” revenue model centered around volunteering engagements for corporate employees.

This nonprofit judo has become a major driver of the organization’s rapid growth. Win-win.The Tech Nonprofit Playbook digs into more strategic advantages nonprofits can leverage, and shares real-world examples of nonprofit judo. Rather than going into your tech nonprofit journey imagining an uphill battle, turn the scenario around by tapping into the unique opportunities it presents.

To achieve your mission, find the people who believe in your cause and can help you get there.

Most importantly, find a complementary co-founder early on who is either technical or an issue expert. Co-founders fill in each other’s gaps, distribute the work and build a strong foundation for the team.

Next, focus on hiring talented, mission-driven people (they exist!) who can help you build and scale. This doesn’t mean hiring as many people as possible once you have the funding for it — something CommonLit, the free reading platform for students, learned the hard way. After winning a $4 million grant, founder Michelle Brown raced to hire 15 people in 40 days. After the fact, Brown realized that you cannot hire people as individuals, you must hire a team. The individuals powering your organization will define what it becomes. Choose wisely.

Impact is a tech nonprofit’s true north. Before you can get down to creating impact, you have to figure out your “who” and your “why,” or distribution ethics. Distribution ethics, the framework shared by Josh Nesbit, founder of Medic Mobile, is the concept that deciding who you are going to help and why they need your help over others is an ethical stance — and will impact everything you do as an organization.

When Nesbit first launched Medic Mobile, the organization was implementing healthcare tools in partnership with on-the-ground organizations. In doing so, he was providing tools to local partners who already had human and financial capital. Nesbit realized this framework wasn’t reflective of his moral stance — he wanted to help those with the least access to medical care. This realization helped him refocus the organization and redefine its product vision to serve those most in need. Since then, Medic Mobile has been building open-source tools that enable a decentralized network of community health workers to deliver effective last-mile healthcare. And it has made a huge impact: Last year, Medic Mobile supported a global network of 27,477 health workers, which provided more than 11 million services for their community.

As you grow, be intentional about how you measure your impact. Impact measurement dictates your organization’s architecture by aligning your work with the value you want to create for the world. It’s a critical practice that not only centers your output around your mission, but helps you raise support for your work through funding and partnerships.

Powered by WPeMatico

I have struggled for years about whether or not to write a piece like this.

Speaking out about racism goes against every lesson I have learned since I was the only Black kid in my first-grade class in the Boston suburbs:

Save candid conversations about race for Black people. You’re being a victim. People will think you’re whining or making excuses. They’re not interested. Don’t make white people feel uncomfortable.

In a professional environment, speaking up could be career suicide. But now is not the time to be silent.

The startup I founded, Indenseo, is a data and analytics software insurtech company that provides automated underwriting services, software and analytics services to the insurance industry.

Despite strong customer relationships and support from angel investors, we didn’t complete building solutions and moving the company forward until we stopped taking unproductive pitch meetings with VCs. Some of my [white] colleagues who attended those meetings characterized these encounters as disrespectful and dismissive, but for me, they were par for the course.

I was raised by a single mother in West Medford, Massachusetts, and worked my way through Harvard, located about five miles away. Before starting Indenseo, I worked for @Road, a fleet management telematics company that was acquired by Trimble, a company that says it transforms “the way the world works by delivering products and services that connect the physical and digital worlds.” There, I led a team that pioneered the sale of telematics data, which started with using data for traffic predictions and expanded to other markets, including insurance.

At Trimble, I saw the difficulty legacy insurance carriers faced when they tried to incorporate new types of data into their underwriting and business processes; I started Indenseo to solve this problem by combining deep insurance industry experience with the nimbleness of a startup.

I knew fundraising would be a challenge: Commercial auto insurance has been unprofitable for years, and industry executives would be naturally skeptical that my solution would make it better. As my insurance industry friends said, “you sure picked a hard problem to solve.”

Even as a first-time founder, I did not anticipate how difficult it would be to raise venture funding, but the experience offered some insights into why so few Black entrepreneurs are funded by VCs.

Insurance is not the most mainstream venture category, though in recent years many insurtech companies have received funding. And VCs are not accustomed to seeing Black founders in this space. The overall scarcity of Black founders suggests that they’re not used to seeing many of us, period.

The odds of winning a venture round are low for everyone, but Black founders have a better chance playing pro sports than they do landing venture investments.

The odds of winning a venture round are low for everyone, but Black founders have a better chance playing pro sports than they do landing venture investments.

According to a Harvard study, between 1990 and 2016, just 0.4% of the entrepreneurs who received funding were Black. That’s 188 Black entrepreneurs, versus 34,000 white entrepreneurs in total, or about seven per year. In 2016, nine Black NFL quarterbacks started at least one game during the season. Should anyone wonder why ambitious young Black men pursue sports careers?

I got the meetings and pitched Indenseo to investors in Silicon Valley, New York City, Chicago and Boston. I expected that my experience, my best-in-class team, the compelling Indeseo proposition, market fit, and the financial and advisory backing of notable insurance executives would land the dollars, despite the odds. I was wrong.

One recurring phenomenon we frequently encountered were dismissive and disrespectful investors (in the words of a white colleague). When I had one disappointing meeting after another, people in my multiracial network — many with extensive fundraising experience — told me it didn’t make sense. I’d resisted getting distracted by race as a factor, but white colleagues were saying that something wasn’t adding up.

As Toni Morrison said, “The very serious function of racism is distraction. It keeps you from doing your work.” My own lived experience is that it’s an added factor that Black entrepreneurs have to manage.

I followed advice given to many Black founders: take a white colleague to your pitch meeting. I brought colleagues who had done a lot of fundraising themselves; some of these meetings were with their contacts. I tried this strategy dozens of times, and my colleagues were repeatedly shocked at the treatment we received.

I assumed most investors were jerks in pitch meetings, but they told me the level of disrespect and dismissiveness I received was not typical.

But if I lose my temper, I’d likely be labeled as just another angry Black man.

I did let my frustration show once when I directed a VC’s attention to the milestones we’d met and industry support we had gathered.

“What does it take for us to get a check from you?” I asked. His response: There is nothing you can say or do to get me to invest, but if you get another VC to lead the round, call me.

In another conversation with a VC, I pointed out the lack of diversity in both the ranks of investors and the entrepreneurs they choose to fund. He replied that Silicon Valley has produced the greatest accumulation of wealth in human history in the last 25 years. Why do we need to change anything?

GW Chew is a friend and a Black founder who was also having difficulty getting VC funding for his vegan meat company, Something Better Foods. He approached investors to raise funds to meet the fast expanding demand for his products. Talk about traction.

A white investor told Chew that if the founder/CEO were white, the company would have raised millions already. My friend told me he’s no longer talking to VCs and is raising funds from alternative sources.

Then there are the grifters. I don’t think Black founders are the only ones whose ideas get stolen after pitch meetings, but it happened to me.

We pitched a VC firm that had a consultant with an insurance background on their team to help evaluate the Indenseo opportunity. VCs don’t sign NDAs, but we did sign one with the consultant, who said Black founders can’t get companies funded but white founders can. (Yes, he said it.)

He later tried to ingratiate himself by saying he was considering investing too. Instead, he founded a company that copied our ideas. (So much for our NDA.)

Eventually, he told me, “I like your team. Call me when the wheels fall off.” When he announced his new company, we saw that he was backed by the VC who brought him into our meeting. He has since gone on to raise more than $40 million.

So why didn’t I sue him for violating the NDA? I consulted with some of our angel investors and they said we would be better off fighting them in the marketplace, given our limited time and resources. It wasn’t the first time our ideas were stolen.

When another company we pitched appropriated some of our ideas, my contact there informed his executives that they’d signed an NDA with Indenseo. Their reply: Indenseo doesn’t have the money to sue us. But they weren’t domain experts and we had left out much about our plans: They announced their launch in The Wall Street Journal, but as I expected, they failed.

Am I calling VCs racists? I don’t know what’s in their hearts, but I do know what’s in their numbers. Dealing with unconscious bias is difficult because as a Black entrepreneur trying to build a company, you know it exists and you have to figure out a way to manage around it. But it’s a subtle problem.

I don’t think VCs wake up in the morning and consciously decide not to invest in Black entrepreneurs or businesses intentionally choose not to buy from companies founded by Black entrepreneurs. But, the results of who receives investment and who doesn’t are quantifiable: few VC funds have Black employees or invest in companies started by Black founders.

I have never pitched at a VC firm that had a Black person in the room. And the pipeline excuse doesn’t work. There are Black people with technical degrees who aren’t hired at VC firms and white VC investment partners who earned liberal arts degrees.

Sure, there are funds started by Black VCs, but they encounter unconscious bias too when raising money. While more Black VCs with more capital is a crucial element of addressing underrepresentation, does that mean VC firms that aren’t founded by Black investors don’t have to change anything?

Deciding to stop the time-consuming VC pitch process and go in another direction to fund and develop the company was quite liberating. Moving forward, we’re free to manage our startup without wondering how VCs will view our decisions in the future when we seek funding.

We raised money from angel investors (including the former CEO of one of the world’s leading analytics software companies and his wife). In addition to money, it expanded our knowledge and it improved our products. Another lesson learned: Angel investors may be more helpful to your company than VCs.

The ultimate judgment on Indenseo’s products and team will be rendered by customers, partners and domain experts. The insurance industry has unique metrics that determine a company’s profitability. If you’re selling analytics software and services, either your solution is helping improve those metrics or it isn’t. The insurance industry is validating our market fit and survival skills.

I was able to build Indenseo without VCs because the insurance industry operates differently from VCs. One of the keys to success in the insurance industry is developing trust. Insurance isn’t a tangible product. It offers the promise that when a customer pays its premiums the insurance company will be able to support them when they file a claim. Without trust, a company can’t succeed in the industry.

There is a process to get insurance industry trust, and many senior executives in the industry are reluctant to invest the time in startups that’s necessary for them to get that trust. That’s because they aren’t convinced the startup will persevere to get through the process of getting that trust. We are able to get time with those executives because they trust our team and they don’t doubt that it’s worth their time to talk to Indenseo. They know we won’t fold when times are difficult.

A change I’ve seen since I started Indenseo that works in our favor is insurers don’t rely on VCs to act as a de facto screen for which insurtechs have the best teams and solutions. That’s because they don’t have confidence in investors’ judgments about insurtech companies.

Another lesson I’ve learned from my experiences: Don’t let VCs be the gatekeepers of your success. There are other funding sources, such as angel investors, corporate strategic investors, crowdfunding and more. There is funding outside the United States. Don’t overlook international investors: There is wealth in African countries. I found a way of funding the company that works for Indenseo.

We’ve developed Indenseo with angel investors and sweat equity. The key to our success is the amazing team, our advisory board and using capital efficiently. They remind me that you’re not the only one with an emotional investment in this company. When I started this company the only people in the insurance industry I knew were the people I had interacted with when I worked at Trimble.

Most of the people on our advisory board and team with insurance industry backgrounds are people I’ve met since I started Indenseo. It takes time to build those relationships. Because of them there is no corner of the commercial property casualty insurance industry we can’t access. The head of insurtech at a global reinsurance company told me that ours is the best balanced team of any insurtech company they’ve seen.

We are in the early stages of showing our flagship product, and it isn’t available for general release yet. Our VP of Engineering is telling me about a new concern: that we don’t take on too many customers too quickly.

Powered by WPeMatico

While it’s no secret Hispanics represent unparalleled growth opportunities for the U.S. economy, most startups don’t realize Hispanic youth means an abundance of prime spending years (translation: dollars for businesses). The average age of a Hispanic living in the U.S. is 28. Meanwhile, the average age of their white counterpart is 42. Nearly one in every five people in the U.S. identifies as Hispanic.

Those few companies that do notice Hispanics and their massive purchasing power (~$1.5 trillion) tend to be legacy companies doing a subpar job at capturing the Hispanic consumer. Furthermore, they don’t target the most valuable member of the Hispanic community — what I call, the “Hypercultural Latinx.” They are where tons of unspent dollars lie.

As an investor and member of the Hispanic community, I’m confident the startups solving problems for this Hypercultural Latinx member will have the potential to create companies with venture-like returns.

The Hypercultural Latinx is a second-generation Hispanic who is 100% Hispanic and 100% American. And while that might sometimes lead to misunderstandings and conflicts with her white counterparts, it also means she excels by creating a pseudo culture where she can thrive best. She brings her unique characteristics to this self-created culture — a culture where her customs, language and values shine through. Furthermore, this person, who often identifies as a Gen Zer or young millennial, is a fanatic of mobile. After all, across socioeconomic classes, their disposable income is disproportionately going to screens (of all types) and tech toys.

I mean, just go into your Hispanic friend’s home: They are likely to have more TV screens than people residing in that household. In fact, a bewildering 29% of U.S. Hispanics planned to purchase a new TV set just ahead of the Super Bowl (guilty as charged). For reference, of the 30% of overall Americans that planned to buy a TV in 2017, only 2.8% purchased in the days before the Super Bowl. Heck, when my family moved, we bought TV screens for every room even before the living room was furnished. Technology — especially newer tech, is significantly more tempting to Hispanics.

The Hypercultural Latinx should be top of mind for venture investors and founders. She desires to test the untested, and thus, is likely to cross the chasm before the early majority. This makes her an ideal customer segment for consumer startups.

Image Credits: Ilsa Calderon

Startup founders and VCs alike are missing out. As an investor, I often find myself reduced to frustration with the lack of founders and investors committed to exploring audience segments outside cookie-cutter ones. We might not need another consumer vertical product solving a half-felt pain point for the highly educated, white female with a $100,000+ salary living in NYC, SF or LA. However, we do need more products catered toward the Hypercultural Latinx who, by the way, outspend their white counterparts across most categories. In the same way Fenty Beauty exists to solve the make-up needs of primarily Black women, we need that for the Hypercultural Latinx population.

Numbers aside, investors should care about Hypercultural Latinx because they are tech-forward trendsetters who adopt social media at higher rates than their white peers. For example, a Hispanic youth is 87% more likely to use WhatsApp. Additionally, they produce an exorbitant amount of videos on Tik Tok. Several Tik Tok Hispanic-centric hashtags, such as #hispanicmom, are wildly popular and boost over 44 million views. For reference, the most followed Tik Tok stars, like Addison Rae, have just over 47 million followers. In fact, one Hispanic Tik Tok queen, Rosa, has already reached pop culture peak.

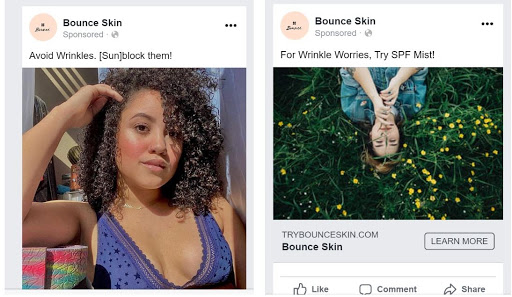

Examples of ads I ran. (Image Credits: Ilse Calderon )

If you are more driven by quantitative data, know that paid spend targeting this Hypercultural Latinx could result in lower click cost rates and higher engagement. I ran a two-week experiment on Facebook to prove out this hypothesis. I created a landing page for a fake sunscreen brand, Bounce Skin, with a fake first product, an SPF mist. I created a couple of ads. Then, I ran ads on Facebook targeting two audiences: young Hispanic girls (the Hypercultural Latinx audience) and white girls. The average click cost for the young Hispanic girl audience was $0.06 per click; for white girls, it was $0.33 per click. Of course, my experiment was limited, but it did demonstrate that the Hypercultural Latinx is out there and craving content that tells the narrative of her life. (For more details, please check out this Medium post).

Three key reasons: fear, the subpar state of Hispanic marketing and white men cannot relate to the Hypercultural Latinx.

Fear. There’s always risk associated with offending the same audience you are trying to captivate. Just take a look at the beauty industry and its frequently associated race problem. The world is not white, and beauty brands that think it is have lived through PR nightmares. Even beyond beauty, tech startups fear negative press cutting short the life of their business. However, it is this gap that creates opportunity.

I encourage the right set of up and coming startups to authentically pursue the Hypercultural Latinx. Even though legacy companies might have heavier balance sheets, they don’t have the clout to lure this young, bicultural consumer. Let’s just say, no 18-year-old is going to be rushing to the Walmarts of the world looking for aspirational goods. They are even less likely to browse Walmart.com for content.

The state of U.S. Hispanic marketing is ridiculous. In fact, there’s a graveyard of failed marketing attempts to the Hispanic community. Most recently, there was a Mother’s Day Kmart ad that blended two Spanish words (Mama + Namaste) to accidentally create a word translating into a very vulgar and offensive word. Furthermore, given most businesses’ “one size fits all” approach to Hispanic marketing, it’s no surprise they keep getting it wrong. However, if anyone is best positioned to take Hispanic marketing out of the 20th century, it’s small, nimble startups with no history of bad marketing or image problems.

Perhaps the biggest reason the tech community isn’t approaching the Hypercultural Latinx is because most venture-backed founders and investors are white men. These white men cannot possibly relate to the life experiences of young, biracial teenagers and young adults living in white America. Last year, a measly less than 2% of venture funding went to Hispanic founders — those are the founders best suited to be able to genuinely capture the eyeballs and wallets of this Hispanic youth. On the investor side, it’s even worse with only 1% of venture investors identifying as Hispanic.

The solution is complex, and frankly, I can’t provide a solution with clarity. However, we can start by building goodwill and non-transactional relationships with those role models Hypercultural Latinx admire. I’ve found that these role models are usually under-the-radar influencers, like Glenda. We as investors can also diversify our top of funnel deal flow to include more underrepresented founders. Lastly, founders with a reach and network of Hispanic youth should consider diving deep into the pain points of Hypercultural Latinx lives.

In order to become this new VC darling, founders approaching the Hypercultural Latinx should consider two suggestions: a platform play and an army of social guides.

The platform approach entails creating an organization of brands that later spew out new brands horizontally or vertically. An example of this is the company behind my favorite over-priced lemon drink, Iris Nova, or Glossier-team spin-off, Arfa.

The second approach, an army of social guides, means combining elements of affiliate marketing with a kick-ass referral program to create loyal fans that are financially incentivized to sell your products. Sequoia-backed Stella & Dot built out their version of social guides that ultimately became its most defensible strategy. Additionally, in a post-coronavirus world, this strategy is a way for an ever-increasing labor force to get back on their feet.

At the end of the day, the Hypercultural Latinx demographic is only increasing, and so are its needs. For founders who truly care about the U.S. Hispanic market, pay attention to this hidden generation. For investors, look beyond solutions for your own problems. Winning over the multi-faceted Hypercultural Latinx is not easy, but startups that successfully do so attract my attention and my investment dollars.

Powered by WPeMatico

When Mallun Yen started Operator Collective last year, she wanted to build an investment firm for people who didn’t have a voice in Silicon Valley. That meant connecting women and people of color with operators who have been intimately involved in building companies from the ground up, then providing early-stage investment.

She then brought in Leyla Seka as a partner. Seka helped build the AppExchange at Salesforce into a powerful marketplace for companies built on top of the Salesforce platform, or that plugged into the platform in some meaningful way to sell their offerings directly to Salesforce customers. Through that role, she met a lot of people in the startup world, and she saw a lot of inequities.

Yen, whose background includes eight years as a VP at Cisco, and co-founder of Saastr with Jason Lemkin, wanted to build a different kind of firm, one that connected these operators — women like herself and Seka, who had walked the walk of running substantial businesses — with people who didn’t typically get heard in the corridors of VC firms.

Those operators themselves tend to be underrepresented at investment shops. The firm today consists of 130 operator LPs, 90% of whom are women and 40% people of color (which includes Asians). One way that the company can do this is by removing rigid buy-in requirements. LPs can contribute as little as $10,000, all the way up to millions of dollars, depending on their means, and that makes for a much more diverse pool of LPs.

While Seka admits they are far from perfect, she says they are fighting the good fight. So far, the company has invested in 18 startups with a more diverse set of founders and executives than you find at most firms that invest in enterprise startups. That means that 67% of their investments include people of color (which breaks down to 44% Asian, 17% Latinx and 6% Black), 56% include a female founder, 56% have an immigrant founder and 33% have a female CEO.

I sat down with Yen and Seka to discuss their thinking about enterprise investing. While they have a far more inclusive philosophy than most, their general approach to enterprise investing isn’t all that different than what we’ve seen in previous surveys with enterprise investors.

Which trends are you most excited about in the enterprise from an investing perspective?

Powered by WPeMatico

Meet Envision, a new startup accelerator. The group, built and run by a collection of students and recent graduates, just closed the application process for its first cohort of startups.

Its goal isn’t merely to find some companies and give them a boost, however. According to Annabel Strauss and Eliana Berger, two co-founders of Envision, it’s to shake up the diversity stats that we’ve all come to know.

“We started Envision because we believe in a future where womxn, Black, and Latinx founders receive more than 3% and 1% of venture funding, respectively,” they said in an email. “As a team of students, we wanted to take matters into our own hands to help founders succeed — it’s our mission to support entrepreneurs early in their journeys, and amplify voices that are often underestimated.”

According to its own data, Envision attracted 190 applications, far above its initial, stretch-goal of 100. From its nearly 200 submissions, the group intends to select 15 entrants. According to Strauss and Berger, their initial goal was to winnow it to just 10. But, the pair told TechCrunch in an interview, they doubled the starting cohort size based on the strength of applications.

Envision will provide an eight-week curriculum and around $10,000 in equity-free capital to companies taking part (the group is still closing on part of the capital it needs, but appears to be making quick progress based on numbers shared with TechCrunch).

Each of the eight weeks that Envision lasts will feature a theme, 1:1 mentorship, office hours with startup veterans and, at the end, a blitz of investor-focused mentorship, and an invite-only demo day. The core of the Envision accelerator rotates around the mentors and other helpers it has accreted since coming into existence in early June.

Envision, run by 11 college students and recent graduates, quickly picked up enough startup veterans to run its program (names like Ryan Hoover, Arlan Hamilton, Alexia Tsotsis), and seemingly ample corporate support. In an email this morning, Envision told TechCrunch that Soma Capital, Underscore VC, Breyer Capital, Grasshopper Bank and Lerer Hippeau have joined as sponsors. Indeed, looking at Envision’s partner page reads a bit like a who’s who of Silicon Valley and startup names that you know.

Talking to Envision I was slightly surprised how many students are involved in venture capital today. The Envision team is a good example of the trend. Strauss is involved with Rough Draft Ventures, for example, which is “powered” by General Catalyst. Quinn Litherland from the Envision team is also part of the Rough Draft crew. Contrary Capital, which TechCrunch covered this morning and focuses on student founders, is represented by Timi Dayo-Kayode, James Rogers, Eliana Berger, and Gefen Skolnick on the team. The list goes on, with Danielle Lomax, Angel Onuoha, and Kim Patel all involved, and active in the VC world.

For Strauss, Berger and the rest of the Envision team the pressure is now on to select intelligently from their 190 applications, and provide maximum boost to their first cohort. If the program goes well, and the demo day it has planned in two months proves useful to both startups and investors alike, I don’t see why Envision wouldn’t stage another class down the road. Though of course, it might want to follow in the footsteps of Y Combinator, TechStars and 500 Startups at that point and take an equity stake in the companies it works with.

Envision says in large letters at the top of its website that it is “helping diverse founders build their companies.” If the group succeeds in meeting that mark, it will be an implicit critique of the old-fashioned venture capital world that has historically not invested in diverse founders.

If a dozen college students and recent grads can spin up an accelerator in a few weeks, get nearly 200 applications, and select a diverse cohort to support, then what’s everyone else’s excuse.

Powered by WPeMatico

Venture capital has a long way to go when it comes to investing in underrepresented founders in a meaningful way. But according to The Venture Collective’s Cat Hernandez, the issue is too complex to solve by just cutting checks and spending time with entrepreneurs.

“You have to be maniacally focused on solutions,” Hernandez said.

So, Hernandez has teamed up with a number of operators-turned-investors to tackle tech’s diversity problem from a creative angle.

The Venture Collective, based in London and New York, launches today to make access to capital more equal. Fair warning: its experimental structure is knotty, as TVC is part investment vehicle and part management company. But it’s a creative strategy in a deserving sector that tech struggles to make progress within.

The team is stacked with a variety of experience: Founding partner Nick Shekerdemian is a former YC startup founder who launched a diversity recruitment platform, and his co-founder, Gina Kirch, was one of his investors, as well as a former director at BlackRock. Other partners include former Primary Venture Partners investor Cat Hernandez and Elliot Richmond, who invests out of the United Kingdom and previously worked at Moelis & Company.

The team was finalized during COVID-19.

TVC’s funding model has two customer bases: startup founders and family offices.

For startups, the business will invest a $100,000 check into one company per month, with the flexibility to do more. TVC intends to reserve between $1 to $5 million for follow-on rounds.

For family offices, TVC charges an annual fee to serve as intel for what they think are lucrative pre-seed deals in the Valley. If a family office or someone within its network wants to invest, TVC will ultimately deploy an allocated amount of capital. It hopes that total capital commitments will increase over time.

While TVC says the structure model is in stealth, it is reasonable to compare the structures of these family office investments to the structures of special purpose vehicles. SPVs are investment vehicles that exist outside a fund’s capital allotment and are more spur of the moment, versus traditionally syndicated.

The biggest difference is that SPV structure is centered around deals, but TVC’s structure is centered around a capital allotment, deployed into multiple deals. They essentially act as middlemen between promising startups and family offices.

It’s good news for family offices, as they often take the role of institutional investors, which are decade-long relationships. The problem with lengthy bets is that what was hot in 2010 might not be hot in 2020. TVC’s model lets LPs deploy capital in their interest areas on a year by year basis. So an LP who is newly bullish on remote work (for some wild reason) could get their hands in early deals instead of waiting for the AR/VR fund they invested in years ago to make that move.

Putting all these pieces together, TVC gets more funds by:

Because of all of these mechanisms, TVC’s total “fund size” will change depending on the week. It’s a unique example of how first-time fund managers are tackling investing in a volatile landscape.

Today TVC launches with an undisclosed amount of equity-based financing. The company declined to share total assets under management.

So a big factor in TVC’s success is if it can convince both founders and family offices that its perspective is worth the set up. TVC’s flexibility can be a blessing, but it also can be risky and unreliable in case family offices pull out. Or if there is an extended recession, for example.

As a sweetener, the company says that it will donate two-thirds of partner time to helping portfolio companies.

But how does this fit into diversity? It all goes back to TVC’s goal to make access to capital more equal.

According to the team, pre-seed to Series A is where most companies fail, but the very funds that back pre-seed are also the most strapped for resources (small fund sizes, fixed management fees). Thus, firms have to selectively pick the companies they think are outliers and spend time with those companies on a more regular basis. This disproportionately impacts underrepresented founders, who might have a slower start due to lack of access to resources.

TVC thinks its strategy will help grow the number of startups that are venture-backable by heavily supporting them through this time, without competing and driving up valuations for only a few outliers.

The company defined underrepresented founders through diversity, geography, age and social background. When asked if they will publicly disclose diversity metrics, TVC said “it wants to be thoughtful about how we hold our investments accountable in the long-term and we are balancing that with a desire to not be prescriptive.”

“We believe that part of our job as early investors is to ensure that this intent is top of mind as the business scales. That can come in many forms — tracking/reporting on diversity metrics being one of them. At its core, this isn’t about window dressing,” the firm told TechCrunch. Generally, TVC is focused on helping more people get funding, and pointed toward financial optionality as the “flywheel we’re playing for.”

In terms of sourcing, TVC is partnering with tech-focused groups in New York and London and will identify talent at the university and college level. It also said it will build relationships with underrepresented operators “at the most prominent tech companies” and co-invest with diversity-focused founders.

TVC also launched a group called “The Collective” that includes diverse founders, operators and investors, who will help as a deal flow channel.

Powered by WPeMatico