Square

Auto Added by WPeMatico

Auto Added by WPeMatico

It’s a two-Exchange Tuesday, everyone. First up, we’re talking fintech valuations. Next up, we’re digging into Atlanta.

Last week’s news that PayPal intends to buy Japanese startup Paidy marked the second major acquisition of a buy now, pay later (BNPL) company this year. PayPal’s news followed an even larger deal by Square for the Australian BNPL company Afterpay.

The multibillion-dollar exits provided hard market proof that what BNPL startups are building has value beyond simple operating results; major fintech platforms are willing to shell out large sums for their revenues and possible strategic value.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Because both deals happened in 2021, they provide two data points for the value of BNPL companies operating at scale. And because both Square and PayPal provided some information to their investors concerning their transactions, we have a little bit of comparative work to do.

Let’s do a little math and figure out how much PayPal and Square investors are paying for transaction volume across both platforms. Then, we’ll peek at what Affirm is worth along similar lines. We’ll wrap with a look at Klarna’s numbers to see if there’s anything we can dig up there.

Our goal is to find out what sort of price floor or ceiling the Paidy and Afterpay deals imply, if other players in their space are matching that figure, and why. This will be fun!

Our goal is to find out what sort of price floor or ceiling the Paidy and Afterpay deals imply, if other players in their space are matching that figure, and why. This will be fun!

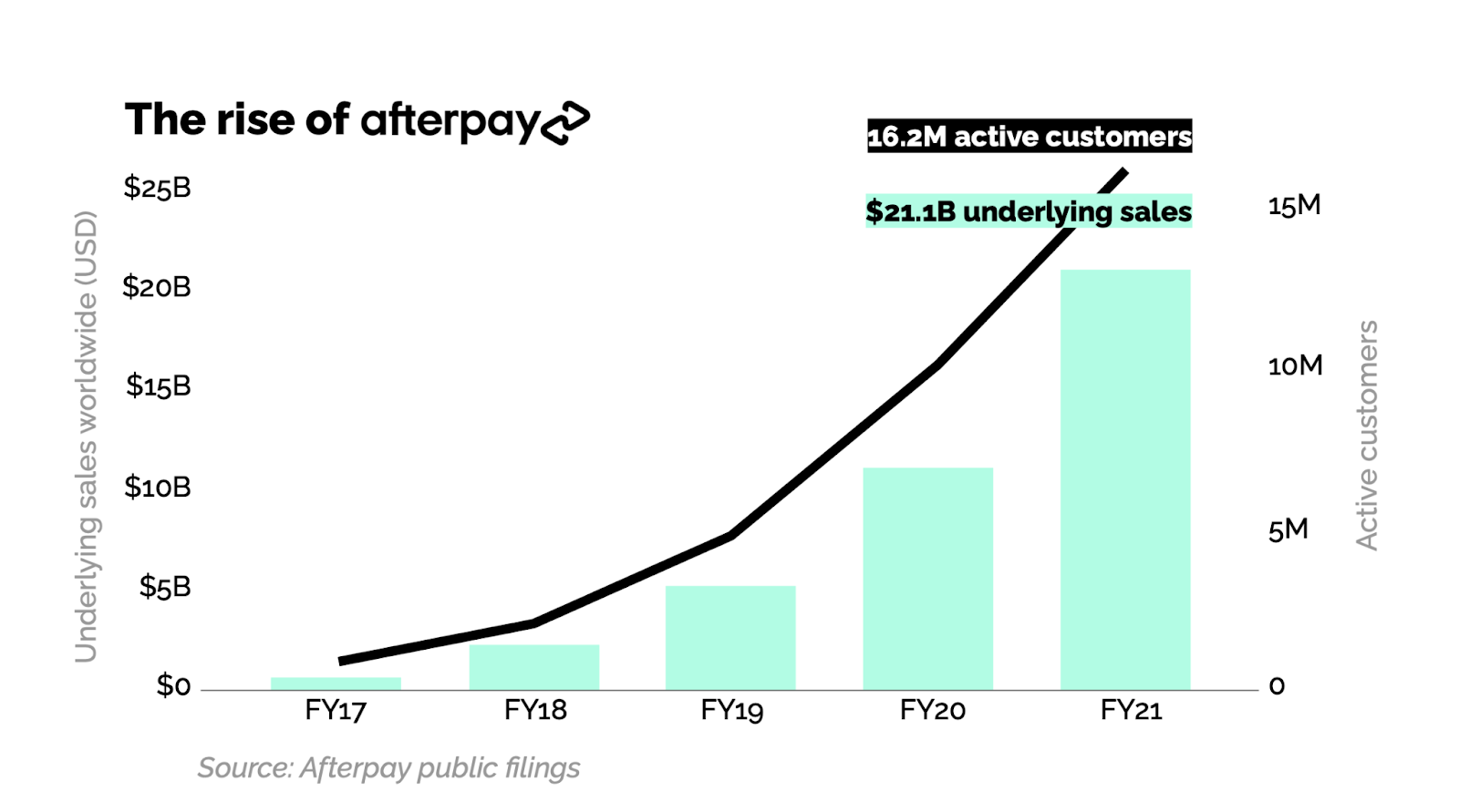

Square’s Afterpay deal is worth some $29 billion, a huge sum. It isn’t hard to see why the U.S. consumer- and business-focused fintech is willing to write so large a check — Afterpay does volume.

Powered by WPeMatico

Sunday was a big day in fintech: Afterpay has agreed to merge with Square. This agreement sets two of the most admired financial technology companies in recent history on a path to becoming one.

Afterpay and Square have the potential to build one of the world’s most important payments networks. Square has built a very significant merchant payment network, and, via Cash App, a thriving high-growth consumer payment service. However, these two lines of business have historically not been integrated. Together, Square and Afterpay will be able to weave all of these services together into a single integrated experience.

Afterpay and Cash App each have double-digit millions of consumers, and Square’s seller ecosystem and Afterpay’s merchant network both record double-digit billions of payment volume per year. From the offline register and the online checkout flow to sending money in just a few taps, Square and Afterpay will tell a complete story of next-generation economic empowerment.

As Afterpay’s only institutional venture investor, I wanted to share some perspective on how we got here and what this merger means for the future of consumer finance and the payments industry.

Afterpay and Square have the potential to build one of the world’s most important payments networks.

Every five to 10 years, the global payments industry undergoes a critical innovation cycle that determines the winners and losers for the next several decades. The last major transition was the shift to NFC-based mobile payments, which I wrote about in 2015. The major mobile OS vendors (Apple and Google) cemented their position in the global payments stack by deftly bridging the needs of the networks (Visa, Mastercard, etc.) and consumers by way of the mobile devices in their pockets.

Afterpay sparked the latest critical innovation cycle. Conceived in a living room in Sydney by a millennial, Nick Molnar, for millennials, Afterpay had a key insight: Millennials don’t like credit.

Millennials came of age during the global mortgage crisis of 2008. As young adults, they watched their friends and family lose their homes by overextending on mortgage debt, bolstering their already lower trust for banks. They also have record levels of student debt. Therefore, it’s no surprise that millennials (and Gen Z right behind them) strongly prefer debit cards over credit cards.

But it’s one thing to recognize the paradigm shift and quite another to do something about it. Nick Molnar and Anthony Eisen did something, ultimately building one of the fastest-growing payments startups in history on their core product: Buy now, pay later … and never any interest.

Afterpay’s product is simple. If you have $100 in your cart and choose to pay with Afterpay, it will charge your bank card (typically a debit card) $25 every two weeks in four installments. No interest, no revolving debt and no fees with on-time payments. For the millennial consumer, this meant they could get the primary benefit of a credit card (the ability to pay later) with their debit card, without the need to worry about all the bad things that come with credit cards — high interest rates and revolving debt.

All upside, no downside. Who could resist? For the early merchants, virtually all of whom relied on millennials as their key growth segment, they got a fair trade: Pay a small fee above payment processing to Afterpay, get significantly higher average order values and conversions to purchase. It was a win-win proposition and, with lots of execution, a new payment network was born.

Image Credits: Matrix Partners

Afterpay went somewhat unnoticed outside Australia in 2016 and 2017, but once it came to the U.S. in 2018 and built a business there that broke $100 million net revenues in only its second year, it got attention.

Klarna, which had struggled with product-market fit in the U.S., pivoted their business to emulate Afterpay. And Affirm, which had always been about traditional credit — generating a significant portion of their revenue from consumer interest — also noticed and introduced their own BNPL offering. Then came PayPal with “Pay in 4,” and just a few weeks ago, there has been news that Apple is expected to enter the space.

Afterpay created a global phenomenon that has now become a category embraced by mainstream players across the industry — a category that is on track to take a meaningful share of global retail payments over the next 10 years.

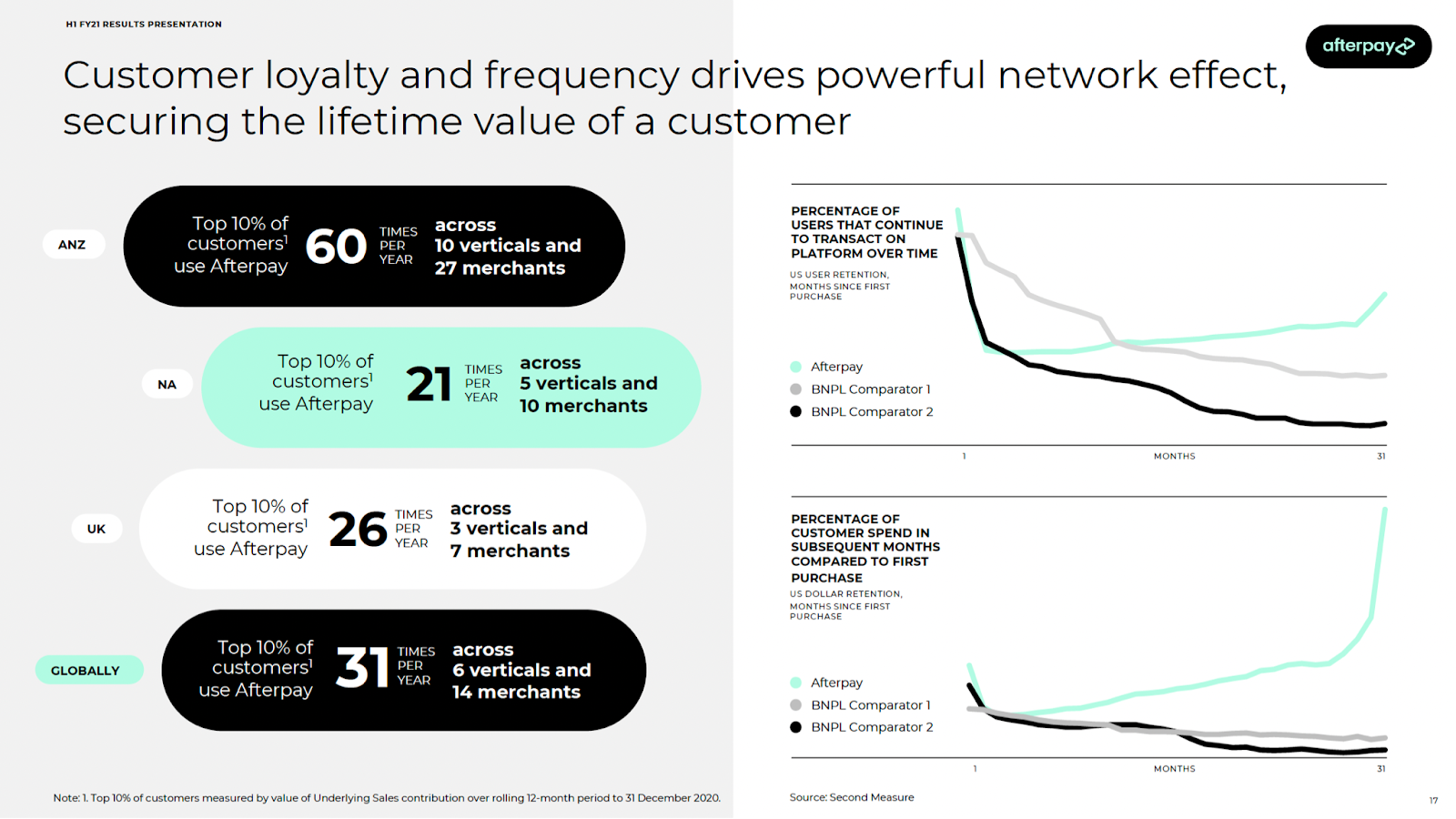

Afterpay stands apart. It has always been the BNPL leader by virtually every measure, and it has done it by staying true to their customers’ needs. The company is great at understanding the millennial and Gen Z consumer. It’s evident in the voice, tone and lifestyle brand you experience as an Afterpay user, and in the merchant network it continues to build strategically. It’s also evident in the simple fact that it doesn’t try to cross-sell users revolving debt products.

Most importantly, it’s evident in the usage metrics relative to competition. This is a product that people love, use and have come to rely on, all with better, fairer terms than were ever available to them than with traditional consumer credit.

Image Credits: Afterpay H1 FY21 results presentation

I’ve been building payment companies for over 15 years now, initially in the early days of PayPal and more recently as a venture investor at Matrix Partners. I’ve never seen a combination that has such potential to deliver extraordinary value to consumers and merchants. Even more so than eBay + PayPal.

Beyond the clear product and network complementarity, what’s most exciting to me and my partners is the alignment of values and culture. Square and Afterpay share a vision of a future with more opportunity and fewer economic hurdles for all. As they build toward that future together, I’m confident that this combination is a winner. Square and Afterpay together will become the world’s next generation payment provider.

Powered by WPeMatico

Shares of Square are up this morning after the company announced its second-quarter earnings and that it will buy Afterpay, an Australian buy now, pay later (BNPL) player in a $29 billion deal. As TechCrunch reported this morning, Afterpay shareholders will receive 0.375 shares of Square in exchange for their existing equity.

Shares of Afterpay are sharply higher after the deal was announced thanks to its implied premium, while shares of Square are up 7% in early-morning trading.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Over the past year, we’ve written extensively about the BNPL market, usually from the perspective of earnings from companies in the space. Afterpay has been a key data source, along with the yet-private Klarna and U.S. public BNPL outfit Affirm. Recall that each company has posted strong growth in recent periods, with the United States arising as a prime competitive market.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

Most recently, consumer hardware and services giant Apple is reportedly preparing a move into the BNPL space. Our read at the time was that any such movement by Cupertino would impact mass-market BNPL players more than niche-focused companies. Apple has a fintech base and broad IRL payment acceptance, making it a potentially strong competitor for BNPL services aimed at consumers; BNPL services targeted at particular industries or niches would likely see less competition from Apple.

From that landscape, let’s explore the Square-Afterpay deal. We want to know what Afterpay brings to Square in terms of revenue, growth and reach. We also want to do some math on the price Square is willing to pay for the company — and what that might tell us about the value of BNPL and fintech revenues more broadly. Then we’ll eyeball the numbers and try to decide if Square is overpaying for Afterpay.

As with most major deals these days, Square and Afterpay released an investor presentation detailing their argument in favor of their combination. Let’s dig through it.

Square is a two-part company. It has a large consumer business via Cash App, and it has a large business division that offers payments tech and other fintech services to corporate customers. Recall that Square is also building out banking services for its business customers and that Cash App also serves some banking and investing functionality for consumers.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and myself here.

This morning was a notable one in the life of TechCrunch the publication, as our parent company’s parent company decided to sell our parent company to a different parent company. And now we’re going to have to get new corporate IDs, again, as it appears that our new parent company’s parent company wants to rebrand our parent company. As Yahoo.

Cool.

Anyway, a bunch of other stuff happened as well:

We’re back Wednesday with something special. Chat then!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 AM PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Natasha and Danny and Alex and Grace were all here to chat through the week’s biggest tech happenings. It was yet another crazy week, but we did our best to get through as much of it as we could. Here’s the rundown, in case you are reading along with us!

And with that we are back on Monday. Have a rocking weekend!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 AM PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion.

Powered by WPeMatico

This morning Square, a fintech company that serves both individuals and companies, announced that it has purchased a majority stake in Tidal, a music streaming service. The deal, worth some $297 million, will allow artist-partners to keep their ownership in the music company.

Square CEO Jack Dorsey used his other company, Twitter, this morning to explain the deal. Dorsey seemed to expect the transaction to generate skepticism — which it definitely has. In his opening message, he asked a rhetorical question: “Why would a music streaming company and a financial services company join forces?!”

Why indeed. Dorsey’s expectation is that his company can replicate the success of Cash App and other Square products in the world of music. Noting that “new ideas are found at the intersection,” Dorsey argued that the confluence of “music and the economy” is one such point of convergence.

The deal also installs musician and businessperson Jay-Z on Square’s board.

Some early reaction to the deal has proved negative. It’s not hard to riff on the seeming strangeness of Square and Tidal as a pair. And Square has made acquisitions in the past that appeared adjacent and failed to stick. The company bought food-delivery service Caviar in 2014 before selling it to DoorDash in 2019, for example; that Square appears to have made a venture-level return on the transaction is immaterial to the focus argument.

But the bull-case for the Square-Tidal tie-up is easy to make as well. The American fintech just spent a minute fraction of a single percent of its market capitalization on the smaller company, and through its choice to let artists keep their stake, has effectively onboarded a host of ambassadors for its brand.

And Dorsey is not wrong that Square did shake up the commerce game for many offline businesses with its original card reader. Why not take a swing at a part of the economy — music — that has migrated from the physical world to the digital in the past few years, much like small businesses in recent quarters?

Square’s business users, its “seller ecosystem,” as it likes to call it, are increasingly digital. In its most recent quarterly earnings report, “in-person only” usage is falling as a percentage of seller gross payment volume (GPV), while “online only” and “omnichannel” GPV are taking up the slack.

Square has a known win in its consumer-focused Cash App service, which reached 36 million monthly actives in December of 2020, up from 24 million in the same period one year prior. You can imagine tie-ups between the music company and the youth-skewing Cash App audience. And having Jay-Z at the Square boardroom table will hardly make the company less innovative; he may bring fresh perspective.

And then there’s the question of NFTs, or non-fungible tokens, a new form of digital asset that have recently become the cause célèbre of the cryptocurrency community. Given that Square has a growing cryptocurrency business via Cash App, and has invested hundreds of millions of dollars into bitcoin itself. If there is space in the market for Square to bring music-based NFTs to its larger consumer user base is an interesting question. If the answer is yes, Square could now be in a leading position to create that market.

Perhaps the Square-Tidal deal won’t generate the future growth that Square imagines. But the deal is cheap, snagging Jay-Z as a leader is a win and it’s hard to win by only playing corporate defense.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion.

Powered by WPeMatico

Known for its innovations in the payments sector, Square is now officially a bank.

Nearly one year after receiving conditional approval, Square said Monday afternoon that its industrial bank, Square Financial Services, has begun operations. Square Financial Services completed the charter approval process with the FDIC and Utah Department of Financial Institutions, meaning its ready for business.

The bank, which is headquartered in Salt Lake City, Utah, will offer business loan and deposit products, starting with underwriting, and originating business loans for Square Capital’s existing lending product.

Historically, Square has been known for its card reader and point-of-sale payment system, used largely by small businesses – but it has also begun facilitating credit for the entrepreneurs and smalls businesses who use its products in recent years.

Moving forward, Square said its bank will be the “primary provider of financing for Square sellers across the U.S.”

In a statement, Square CFO and executive chairman for Square Financial Services, Amrita Ahuja said that bringing banking capability in house will allow the fintech to “operate more nimbly.”

Square Financial Services will continue to sell loans to third-party investors and limit balance sheet exposure. The company said it does not expect the bank to have a material impact on its consolidated balance sheet, total net revenue, gross profit, or adjusted EBITDA in 2021.

Opening the bank “deepens Square’s unique ability to expand access to loans and banking tools to underserved populations,” the company said.

Lewis Goodwin had been tapped to serve as the bank’s CEO, and Brandon Soto its CFO. With today’s announcement, Square also announced the following new appointments:

The trend of fintechs becoming bank continues. In February, TechCrunch reported on the fact that Brex had applied for a bank charter.

The fast-growing company, which sells a credit card tailored for startups with Emigrant Bank currently acting as the issuer, said that it had submitted an application with the Federal Deposit Insurance Corporation (FDIC) and the Utah Department of Financial Institutions (UDFI) to establish Brex Bank.

A number of fintech companies, or those with fintech services, have spun up products typically offered by banks, including deposit and chequings accounts as well as credit offerings. Often, these are designed to provide capital to customers who might not be able to get funding on favorable terms from traditional banking institutions, but who might qualify for business-building loans from a provider who knows their company, like Square, inside and out.

Powered by WPeMatico

This is The TechCrunch Exchange, a newsletter that goes out on Saturdays, based on the column of the same name. You can sign up for the email here.

Welcome to a special Thanksgiving edition of The Exchange. Today we will be brief. But not silent, as there is much to talk about.

Up top, The Exchange noodled on the Slack-Salesforce deal here, so please catch up if you missed that while eating pie for breakfast yesterday. And, sadly, I have no idea why Palantir is seeing its value skyrocket. Normally we’d discuss it, asking ourselves what its gains could mean for the lower tiers of private SaaS companies. But as its public market movement appears to be an artificial bump in value, we’ll just wait.

Here’s what I want to talk about this fine Saturday: Bloomberg reporting that Stripe is in the market for more money, at a price that could value the company at “more than $70 billion or significantly higher, at as much as $100 billion.”

Hot damn. Stripe would become the first or second most valuable startup in the world at those prices, depending on how you count. Startup is a weird word to use for a company worth that much, but as Stripe is still clinging to the private markets like some sort of liferaft, keeps raising external funds, and is presumably more focused on growth than profitability, it retains the hallmark qualities of a tech startup, so, sure, we can call it one.

Which is odd, because Stripe is a huge concern that could be worth twelve-figures, provided that gets that $100 billion price tag. It’s hard to come up with a good reason for why it’s still private, other than the fact that it can get away with it.

Anyhoo, are those reported, possible prices bonkers? Maybe. But there is some logic to them. Recall that Square and PayPal earnings pointed to strong payments volume in recent quarters, which bodes well for Stripe’s own recent growth. Also note that 14 months ago or so, Stripe was already processing “hundreds of billions of dollars of transactions a year.”

You can do fun math at this juncture. Let’s say Stripe’s processing volume was $200 billion last September, and $400 billion today, thinking of the number as an annualized metric. Stripe charges 2.9% plus $0.30 for a transaction, so let’s call it 3% for the sake of simplicity and being conservative. That math shakes out to a run rate of $12 billion.

Now, the company’s actual numbers could be closer to $100 billion, $150 billion and $4.5 billion, right? And Stripe won’t have the same gross margins as Slack .

But you can start to see why Stripe’s new rumored prices aren’t 100% wild. You can make the multiples work if you are a believer in the company’s growth story. And helping the argument are its public comps. Square’s stock has more than tripled this year. PayPal’s value has more than doubled. Adyen’s shares have almost doubled. That’s the sort of public market pull that can really help a super-late-stage startup looking to raise new capital and secure an aggressive price.

To wrap, Stripe’s possible new valuation could make some sense. The fact that it is still a private company does not.

And speaking of edtech, Equity’s Natasha Mascarenhas and our intrepid producer Chris Gates put together a special ep on the education technology market. You can listen to it here. It’s good.

Hugs and let’s both go do some cardio,

Powered by WPeMatico

Earnings season is racing past us, with the big ride-hailing companies’ numbers in, all of the Big Five having wrapped their reporting and lots of SaaS numbers in the market. But amidst all the noise, The Exchange has kept an eye on two companies in particular: PayPal and Square.

We’re not really concerned with their overall revenue and profit metrics. Instead, we’ve been hunting around in their numbers for hints and notes about what is going on inside of fintech itself. Why? There are a host of hugely valuable fintech unicorns that have to go public in the future that also share some market space with one or both of our public charges.

What can we learn from looking at what PayPal and Square reported to their own investors?

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Lots, it turns out.

As TechCrunch reported when PayPal dropped its Q3 numbers, the public company had bullish results from its Venmo service, payment processing and consumer activity metrics. The numbers pointed to strong consumer adoption of fintech services during the pandemic, something that we presumed was not unique to PayPal itself, but was likely indicative of a generally warm environment for consumer fintech services.

Square continued the trend, posting a set of results that contains nearly all positive data for consumer fintech activity — with one critical caveat for Q4 that we’ll get to at the end.

Square continued the trend, posting a set of results that contains nearly all positive data for consumer fintech activity — with one critical caveat for Q4 that we’ll get to at the end.

Still, what the majors tell us about the fintech space indicates a warmth in activity that explains why Chime, Robinhood and others have had such fun in 2020, accreting tectonic capital to keep their growth hot.

Digging through Square’s earnings gives us a window into consumer payment activity, card usage, stock purchases and more. Let’s see what we can learn, and to which unicorns it might apply.

Let’s start by talking about the broader fintech market before niching down.

Powered by WPeMatico

Cash App, the peer-to-peer payments service from Square, is giving select users a way to get short-term loans.

The company said it’s only testing the feature with around 1,000 users for now. But it could become more broadly available — and there are probably plenty of people who could use the money, given the state of the U.S. and global economy, not to mention the current uncertainty about further stimulus plans.

Cash App is starting out by offering loans for any amount between $20 and $200. You’ll be expected to pay the loan back in four weeks, along with a flat fee of 5%. (Multiplied over a year, that turns into a 60% APR — which sounds high, but at least it’s significantly lower than the average payday loan.)

If you don’t pay off the loan after four weeks, you’ll get an additional one-week grace period, then Square and Cash App will start adding 1.25% (non-compounding) interest each week. You also won’t be able to take out an additional loan if you’ve previously defaulted.

“We are always testing new features in Cash App, and recently began testing the ability to borrow money with about 1,000 Cash App customers,” a company spokesperson said in a statement. “We look forward to hearing their feedback and learning from this experiment.”

Square has already been expanding Cash App’s features beyond simple peer-to-peer money transfer with things like the Cash Card (a free debit card), Cash Boost (rewards) and Cash App Investing. And beyond Cash App, Square has been offering loans to small businesses through its Square Capital arm.

Powered by WPeMatico