special-purpose acquisition company

Auto Added by WPeMatico

Auto Added by WPeMatico

What a busy week in the world of media liquidity.

That’s a sentence you don’t get to write often. Regardless, news broke this week that Axel Springer is buying U.S. political journalism outfit POLITICO. The transaction was expected, but the eye-popping roughly $1 billion price tag still has tongues wagging. We even got on the podcast to chat about it.

And Forbes announced that it is going public via a SPAC. The business publication’s news follows BuzzFeed’s journey to the public markets through a blank-check company. Hot media liquidity summer? Something like that.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

That TechCrunch is in the process of being sold to private equity, of course, is not something that we should forget. Shoutout to the Verizon bankers who found a way to get rid of us while also deleveraging Verizon’s debt profile. Ten points.

I want to take a quick tour of the Forbes SPAC deck this morning. Our notes on BuzzFeed’s are here, in case you want to run comparisons. This will be easy and fun. Perfect Friday morning fare. Into the data!

I want to take a quick tour of the Forbes SPAC deck this morning. Our notes on BuzzFeed’s are here, in case you want to run comparisons. This will be easy and fun. Perfect Friday morning fare. Into the data!

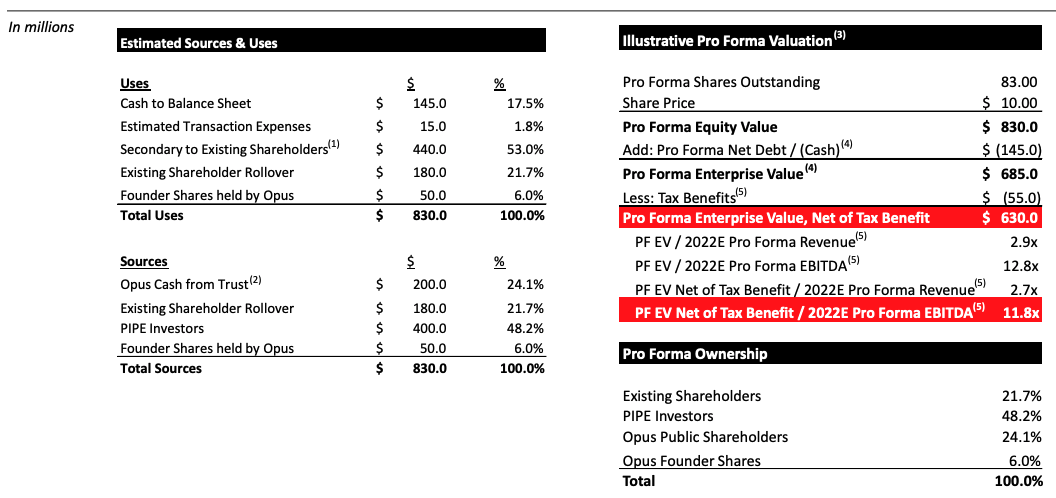

In corporate-speak, Forbes Global Media Holdings is merging with blank-check company Magnum Opus Acquisition Limited. The transaction will close either Q4 2021 or Q1 2022, Forbes estimates.

The deal itself is somewhat modest in scale compared with other SPAC deals we’ve recently looked into. Forbes reports that it will sport “an implied pro forma enterprise value of $630 million, net of tax benefits,” after its completion. Some $600 million in gross proceeds will be derived from Magnum Opus funds “and $400 million of additional capital through a private placement of ordinary shares of the combined company,” Forbes writes.

The company will sport an equity valuation of $830 million after the deal closes, per its own calculations. That number will change some depending on redemptions ahead of the combination. The gap between the large dollars going into the deal and the modest final valuation of the public Forbes entity is due to some $440 million in secondary transactions for existing Forbes shareholders.

In case you’d prefer all of that in table form, here’s the Forbes investor deck:

Image Credits: Forbes SPAC deck

Is $830 million a fair price? Let’s dig into Forbes’ results.

Powered by WPeMatico

Cairo and Dubai-based ride-sharing company Swvl plans to go public in a merger with special purpose acquisition company Queen’s Gambit Growth Capital, Swvl said Tuesday. The deal will see Swvl valued at roughly $1.5 billion.

Swvl was founded by Mostafa Kandil, Mahmoud Nouh and Ahmed Sabbah in 2017. The trio started the company as a bus-hailing service in Egypt and other ride-sharing services in emerging markets with fragmented public transportation.

Its services, mainly bus-hailing, enables users to make intra-state journeys by booking seats on buses running a fixed route. This is pocket-friendly for residents in these markets compared to single-rider options and helps reduce emissions (Swvl claims it has prevented over 240 million pounds of carbon emission since inception).

After its Egypt launch, Swvl expanded to Kenya, Pakistan, Jordan and Saudi Arabia. The company also moved its headquarters to Dubai as part of its strategy to become a global company.

Swvl offerings have expanded beyond bus-hailing services. Now, the company offers inter-city rides, car ride-sharing, and corporate services across the 10 cities it operates in across Africa and the Middle East.

Queen’s Gambit, the women-led SPAC in charge of the deal, raised $300 million in January and added $45 million via an underwriters’ overallotment option focusing on startups in clean energy, healthcare and mobility sectors.

The statement also mentions a group of investors — Agility, Luxor Capital and Zain Group — which will contribute $100 million through a private investment in public equity, or PIPE.

Per Crunchbase, Swvl has raised over $170 million. From an African perspective, Swvl features as one of the most venture-backed startups on the continent. The company has been touted to reach unicorn status in the past and will when this SPAC merger is completed.

The company will aptly trade under the ticker SWVL. The listing will make it the first Egyptian startup to go public outside Egypt and the second to go public after Fawry. It will also make the mobility company the largest African unicorn debut on any U.S.-listed exchange, beating Jumia’s debut of $1.1 billion on the NYSE. In the Middle East, Swvl joins music-streaming platform Anghami as the second startup to go public via a SPAC merger.

Swvl had annual gross revenue of $26 million in 2020, according to the statement, and the company expects its annual gross revenue to increase to $79 million this year and $1 billion by 2025 after expanding to 20 countries across five continents.

On why Queen’s Gambit picked Swvl for this deal, Victoria Grace, founder and CEO, said in a statement that the company fit the profile of what she was looking for: “a disruptive platform that solves complex challenges and empowers underserved populations.”

“Having established a leadership position in key emerging markets, we believe Swvl is ready to capitalize on a truly global market opportunity,” she added.

In May, TechCrunch wrote that SPACs didn’t target African startups for several reasons, including a lack of global appeal and private capital and market satisfaction. Judging by Grace’s comments, Swvl has that global appeal and is ready to venture into the public market despite being in operation for just four years.

Powered by WPeMatico

Despite the plentiful headlines about mega billion-dollar M&A transactions, record IPOs and the rapid growth of SPACs, small deals will continue to be the most likely exit for the vast majority of tech startups. In the over 30 years I’ve worked on M&A at White & Case, Barclays and my current firm Ascento Capital, I have seen too many startups that are not prepared for an exit via a merger or sale. This article will provide specific recommendations on how to prepare your startup for M&A.

While it is good to strive for a billion-dollar-plus sale, a successful IPO or a SPAC deal, it is practical to prepare your startup for a smaller transaction.

Global M&A hit record highs in the second quarter with a total deal value of $1.5 trillion, but smaller transactions vastly outnumber mega billion-dollar deals. The U.S. saw a total of 16,672 deals in the year ended June 31, but only 583, or 3% of that number, were valued at more than a billion dollars (FactSet). The IPO market is healthy again, but M&A still represents 88% of exits: So far this year, there were 503 IPOs and 5,203 deals, according to the CB Insights Q2 2021 State of Venture Report. After the SEC announced in early April that it was considering new guidance on SPAC IPOs, the rate of new SPAC issuances fell by around 90%.

While it is good to strive for a billion-dollar-plus sale, a successful IPO or a SPAC deal, it is practical to prepare your startup for a smaller transaction.

Here are a few recommendations that will prepare your startup for an M&A exit:

Set up an alert on Google News for M&A activity in your subsector. For example, if your startup is in the IoT subsector, search for “IoT acqui” and this will pick up news stories on acquisitions in the IoT space. Save the search so you can go to Google News on a regular basis. Also track your closest competitors on Google News, particularly to see who is selling their company.

Prepare a list of the companies or firms most likely to buy your startup. This list should include domestic and international companies, businesses in non-tech industries, private equity firms and their portfolio companies, as well as VC-backed companies. Track these likely acquirers on Google News as well.

Consider approaching the top 10 likely acquirers when you are raising the next round of capital. If your startup gets M&A offers and VC term sheets at the same time, this will provide your board of directors choices on the path ahead. Knowing the M&A activity in your startup’s subsector and the 10 most likely acquirers will impress VCs and increase the chances of being funded.

Powered by WPeMatico

Mortgages may not be considered sexy, but they are a big business.

If you’ve refinanced or purchased a home digitally lately, you may not have noticed the company powering the software behind it — but there’s a good chance that company is Blend.

Founded in 2012, the startup has steadily grown to be a leader in the mortgage tech industry. Blend’s white label technology powers mortgage applications on the site of banks including Wells Fargo and U.S. Bank, for example, with the goal of making the process faster, simpler and more transparent.

The San Francisco-based startup’s SaaS (software-as-a-service) platform currently processes over $5 billion in mortgages and consumer loans per day, up from nearly $3 billion last July.

Today, Blend made its debut as a publicly traded company on the New York Stock Exchange, trading under the symbol “BLND.” As of early afternoon, Eastern Time, the stock was trading up over 13% at $20.36.

On Thursday night, the company had said it would offer 20 million shares at a price of $18 per share, indicating the company was targeting a valuation of $3.6 billion.

That compares to a $3.3 billion valuation at the time of its last raise in January — a $300 million Series G funding round that included participation from Coatue and Tiger Global Management. Also, let’s not forget that Blend only became a unicorn last August when it raised a $75 million Series F. Over its lifetime, Blend had raised $665 million before Friday’s public market debut.

In filing its S-1 on June 21, Blend revealed that its revenue had climbed to $96 million in 2020 from $50.7 million in 2019. Meanwhile, its net loss narrowed from $81.5 million in 2019 to $74.6 million in 2020.

In 2020, the San Francisco-based startup significantly expanded its digital consumer lending platform. With that expansion, Blend began offering its lender customers new configuration capabilities so that they could launch any consumer banking product “in days rather than months.”

Looking ahead, the company had said it expects its revenue growth rate “to decline in future periods.” It also doesn’t envision achieving profitability anytime soon as it continues to focus on growth. Blend also revealed that in 2020, its top five customers accounted for 34% of its revenue.

Today, TechCrunch spoke with co-founder and CEO Nima Ghamsari about the company’s decision to go with a traditional IPO versus the ubiquitous SPAC or even a direct listing.

For one, Blend said he wanted to show its customers that it is an “around for a long time company” by making sure there’s enough on its balance sheet to continue to grow.

“We had to talk and convince some of the biggest investors in the world to invest in us, and that speaks to how long we’ll be around to serve these customers,” he said. “So it was a combination of our capital need and wanting to cement ourselves as a really credible software provider to one of the most regulated industries.”

Ghamsari emphasized that Blend is a software company that powers the mortgage process and is not the one offering the mortgages. As such, it works with the flock of fintechs that are working to provide mortgages.

“A lot of them are using Blend under the hood, as the infrastructure layer,” he said.

Overall, Ghamsari believes this is just the beginning for Blend.

“One of the things about financial services is that it’s still mostly powered by paper. So a lot of Blend’s growth is just going deeper into this process that we got started in years ago,” he said. As mentioned above, the company started out with its mortgage product but just keeps adding to it. Today, it also powers other loans such as auto, personal and home equity.

“A lot of our growth is actually powered by our other lines of business,” Ghamsari told TechCrunch. “There’s a lot to build because the larger digitization trends are just getting started in financial services. It’s a relatively large industry that has lots of change.”

In May, digital mortgage lender Better.com announced it would combine with a SPAC, taking itself public in the second half of 2021.

Powered by WPeMatico

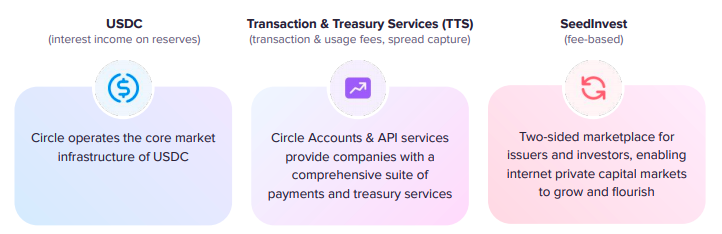

In the wake of Coinbase’s direct listing earlier this year, other crypto companies may be looking to go public sooner than later. That appears to be the case with Circle, a Boston-based technology company that provides API-delivered financial services and a stablecoin.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Circle will not direct list or pursue a traditional IPO. Instead, the company is combining with Concord Acquisition Corp., a SPAC, or blank-check company. The transaction values the crypto shop at an enterprise value of $4.5 billion and an equity value of around $5.4 billion.

The offering marks an interesting moment for the crypto market. Unlike Coinbase, which operates a trading platform and generates fees in a manner that is widely understood by public-market investors, Circle’s offerings are a bit more exotic.

Circle’s SPAC presentation details a company whose core business deals with a stablecoin — a crypto asset pegged to an external currency, in this case, the U.S. dollar — and a set of APIs that provide crypto-powered financial services to other companies. It also owns SeedInvest, an equity crowdfunding platform, though Circle appears to generate the bulk of its anticipated revenues from its other businesses.

For more on the deal itself, TechCrunch’s Romain Dillet has a piece focused on the transaction. Here, we’ll dig into the company’s investor presentation, talk about its business model, and riff on its historical and anticipated results and valuation multiples.

In short, we get to have a little fun. Let’s begin.

As noted above, Circle has three main business operations. Here’s how it describes them in its deck:

Image Credits: Circle investor presentation

Let’s consider each one, starting with USDC.

Stablecoins have become popular in recent quarters. Because they are pegged to an external currency, they operate as an interesting form of cash inside the crypto world. If you want to have on-chain buying power, but don’t want to have all your value stored in more volatile, and tax-inducing, cryptos that you might have to sell to buy anything else, stablecoins can operate as a more stable sort of liquid currency. They can combine the stability of the U.S. dollar, say, and the crypto world’s interesting financial web.

Powered by WPeMatico

The SPAC parade continues in this shortened week with news that community social network Nextdoor will go public via a blank-check company. The unicorn will merge with Khosla Ventures Acquisition Co. II, taking itself public and raising capital at the same time.

Per the former startup, the transaction with the Khosla-affiliated SPAC will generate gross proceeds of around $686 million, inclusive of a $270 million private investment in public equity, or PIPE, which is being funded by a collection of capital pools, some prior Nextdoor investors (including Tiger), Nextdoor CEO Sarah Friar and Khosla Ventures itself.

Notably, Khosla is not a listed investor in the company per Crunchbase or PitchBook, indicating that even SPACs formed by venture capital firms can hunt for deals outside their parent’s portfolio.

Per a Nextdoor release, the transaction will value the company at a “pro forma equity [valuation] of approximately $4.3 billion.” That’s a great price for the firm that was most recently valued at $2.17 billion in a late 2019-era Series H worth $170 million, per PitchBook data. Those funds were invested at a flat $2 billion pre-money valuation.

So, what will public investors get the chance to buy into at the new, higher price? To answer that we’ll have to turn to the company’s SPAC investor deck.

Our general observations are that while Nextdoor’s SPAC deck does have some regular annoyances, it offers a clear-eyed look at the company’s financial performance both in historical terms and in terms of what it might accomplish in the future. Our usual mockery of SPAC charts mostly doesn’t apply. Let’s begin.

We’ll proceed through the deck in its original slide order to better understand the company’s argument for its value today, as well as its future worth.

The company kicks off with a note that it has 27 million weekly active users (neighbors, in its own parlance), and claims users in around one in three U.S. households. The argument, then, is that Nextdoor has scale.

A few slides later, Nextdoor details its mission: “To cultivate a kinder world where everyone has a neighborhood they can rely on.” While accounts like @BestOfNextdoor might make this mission statement as coherent as ExxonMobil saying that its core purpose was, say, atmospheric carbon reduction, we have to take it seriously. The company wants to bring people together. It can’t control what they do from there, as we’ve all seen. But the fact that rude people on Nextdoor is a meme stems from the same scale that the company was just crowing about.

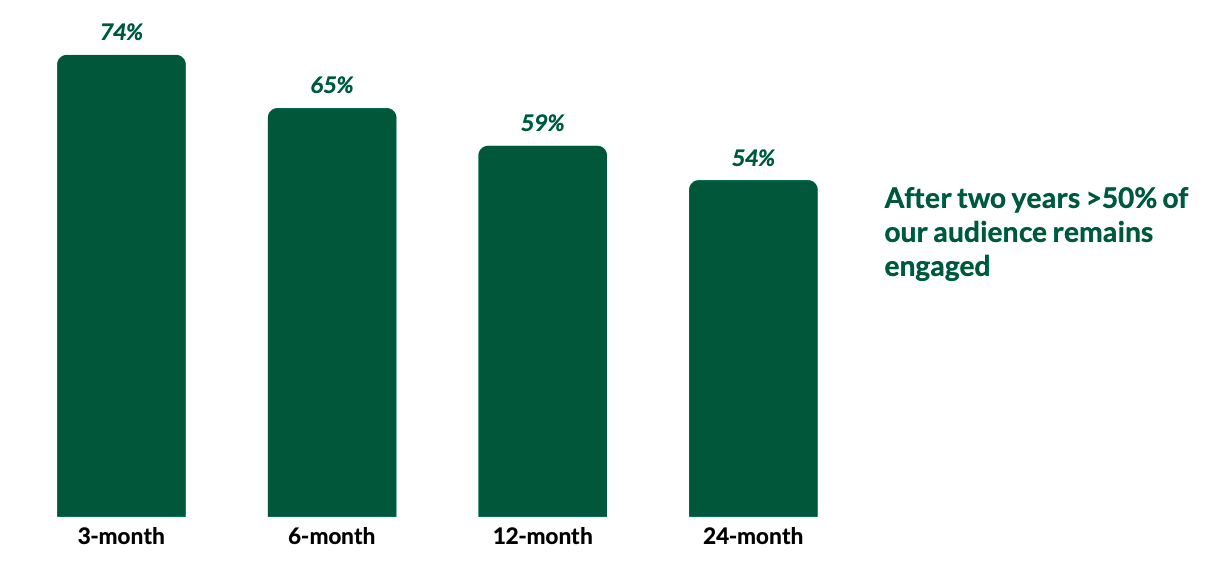

Underscoring its active user counts are Nextdoor’s retention figures. Here’s how it describes that metric:

Image Credits: Nextdoor SPAC investor deck

These are monthly active users, mind, not weekly active, the figure that the company cited up top. So, the metrics are looser here. And the company is counting users as active if they have “started a session or opened a content email over the trailing 30 days.” How conservative is that metric? We’ll leave that for you to decide.

The company’s argument for its value continues in the following slide, with Nextdoor noting that users become more active as more people use the service in a neighborhood. This feels obvious, though it is nice, we suppose, to see the company codify our expectations in data.

Nextdoor then argues that its user base is distinct from that of other social networks and that its users are about as active as those on Twitter, albeit less active than on the major U.S. social networks (Facebook, Snap, Instagram).

Why go through the exercise of sorting Nextdoor into a cabal of social networks? Well, here’s why:

Powered by WPeMatico

Meetings should have a clear purpose, but instead, they’ve become a way to measure status and reinforce what is colloquially referred to as CYA culture.

There’s a kernel of truth in every joke, so whenever someone quips, “This meeting could have been an email!” you can bet that some small part of them meant it sincerely.

Few people know how to run meetings effectively and keep conversations on track. Making matters worse, attendees often don’t bother to prepare, which makes a boring session even less productive.

And then there’s the complication of workplace politics: How secure do you feel declining an invitation from a co-worker — or a manager?

“Every time a recurring meeting is added to a calendar, a kitten dies,” says Chuck Phillips, co-founder of MeetWell. “Very few employees decline meetings, even when it’s obvious that the meeting is going to be a doozy.”

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

Changing your meeting culture is difficult, but given that 26% of workers plan to look for a new job when the pandemic ends, startups need to do all they can to retain talent.

Aimed at managers, this post offers several testable strategies that will help you boost productivity and say goodbye to poorly run, lazily planned meetings.

“Declining a bad meeting should never be taboo, and you should reiterate your trust in the team and challenge them to spend their and others’ time with more intention,” Phillips says. “Help them feel empowered to decline a bad meeting.”

Thanks very much for reading Extra Crunch, and have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Shein

In the last year, online apparel shopping app Shein grew active daily users by 130%, reports Apptopia.

Each day, thousands of new products arrive on the app’s virtual shelves. Items are rapidly designed and prototyped before Shein’s contractors put them into production in Guangzhou factories — two weeks later, those SKUs arrive in fulfillment centers around the globe.

TechCrunch reporter Rita Liao examined how the company’s agile supply chain has become hot talk among e-commerce experts, but beyond a strong logistics game and data-driven product development, Shein’s close relationships with suppliers are integral to its success.

She also tried to answer a question many are asking: Is Shein a Chinese company?

“It’s hard to pin down where Shein is from,” answered Richard Xu from Grand View Capital, a Chinese venture capital firm.

“It’s a company with operations and supply chains in China targeting the global market, with nearly no business in China.”

Image Credits: Chevrolet

GM Vice President of Innovation Pam Fletcher is in charge of the company’s startups that tackle “electrification, connectivity and even insurance — all part of the automaker’s aim to find value (and profits) beyond its traditional business of making, selling and financing vehicles,” Kirsten Korosec writes.

Fletcher joined TechCrunch at a virtual TC Sessions: Mobility 2021 event to discuss what it’s like to launch a slew of startups under the umbrella of a 113-year-old automaker.

Image Credits: MaC Venture Capital / Wonderschool

MaC Venture Capital founding managing partner Marlon Nichols and Wonderschool CEO Chris Bennett joined Extra Crunch Live to tear down the company’s early deck.

“The first thing that jumped out at all of us was just how bare-bones the presentation is: white text on a blue background, largely made up of bullet points,” Brian Heater writes before noting the CEO admitted that “not much changed aesthetically between that first pitch and the Series A deck.”

“It aligned with what we were valuing at the time,” Bennett says. “We were really focused on getting the product-market fit and really trying to understand what our customers needed. And we’re really focused on building the team.”

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

I’ve been working on an H-1B in the U.S. for nearly two years.

While I’m grateful to have made it through the H-1B lottery and to be working, I’m feeling unhappy and frustrated with my job.

I really want to start something of my own and work on my own terms in the United States. Are there any immigration options that would allow me to do that?

— Seeking Satisfaction

Image Credits: Nigel Sussman (opens in a new window)

Alex Wilhelm calls SentinelOne’s looming debut “fascinating.”

“Why? Because the company sports a combination of rapid growth and expanding losses that make it a good heat check for the IPO market,” he writes. “Its debut will allow us to answer whether public investors still value growth above all else.”

Alex delves into an early dataset from SentinelOne and why public market investors still appear to value growth above anything else.

Image Credits: Jenny Dettrick (opens in a new window) / Getty Images

Guest columnist Rob Hudock, a litigator who focuses on helping companies recruit the best talent available while avoiding distracting workplace issues or lawsuits, lays out the importance of putting out any employment-related fires before an exit.

“Inattention to employment issues can have a significant impact on deals — from preventing closings and reducing the deal value to altering the deal terms or significantly limiting the pool of potential buyers,” he writes.

“Fortunately, such issues typically can be resolved well in advance with a little forethought and legal guidance.”

Image Credits: John M Lund Photography Inc (opens in a new window) / Getty Images

Building an excellent product and a standout company culture require the same process, Heap CEO Ken Fine writes in a guest column.

“At Heap, the analytics solution provider I lead, a defining principle is that good ideas should not be lost to top-down dictates and overrigid hierarchies,” he writes. “The best results come when you approach leadership like you would create a great product — you hypothesize, you test and iterate, and once you get it right, you grow it.”

Here, he lays out his method that argues in favor of iterative change, not “one-and-done decrees.”

Image Credits: Nigel Sussman (opens in a new window)

The big news on Thursday was the announcement of Andreessen Horowitz’s new cryptocurrency-focused fund. Most focused on the eye-popping $2.2 billion figure, but Alex Wilhelm dug a bit deeper into the announcement to note that a16z isn’t just pumping a ton of money into the crypto space, it’s putting on gloves to fight for it.

Alex writes that “a16z intends to run defense for crypto in the American, and perhaps global, market. Crypto-focused startups are likely unable to tackle the regulation of their market on their own because they’re more focused on product work in a particular region of the larger crypto economy. The wealthy and connected investment firm that backs them will take on the task for its chosen champions.”

Image Credits: Nicholas Kamm / AFP / Getty Images

Alex Wilhelm dives headfirst into BuzzFeed’s announcement that it plans to go public via a blank check company.

He looked at its historical and anticipated revenue growth (the latter is very sunny, which is not atypical for SPAC presentations), what makes up that revenue (more “commerce” as time goes on), its long-term profitability projections, as well as fun stuff, like the Pulitzer Prize-winning BuzzFeed News.

Admit it. You’re curious.

Image Credits: SaskiaAcht (opens in a new window) / Getty Images

Moving from a pay-as-you-go model to a subscription service is more than just putting a monthly or yearly price tag on a product, CloudBlue’s Jess Warrington writes in a guest column.

“Executives cannot just layer a subscription model on top of an existing business,” Warrington writes. “They need to change the entire operation process, onboard all stakeholders, recalibrate their strategy and create a subscription culture.”

Warrington says that in his role at CloudBlue, companies often approach him for “help with solving technology challenges while shifting to a subscription business model, only to realize that they have not taken crucial organizational steps necessary to ensure a successful transition.”

Here’s how to avoid that situation.

Image Credits: Bryce Durbin

Rebecca Bellan interviewed Veo CEO Candice Xie about the micromobility startup’s “old-fashioned way” of doing business.

“I understand people are eager to prove their unit economics, their scalability and also improve their matrix to the VC to raise another round,” Xie says. “I would say that’s OK in the consumer industry, like consumer electronics or SaaS.

“But we are in transportation. It is a different business, and transportation takes years of collaboration and building between private and public partners. … So I don’t see it happening from day one, turning over a billion-dollar company, while simultaneously having it all make sense for the cities and users.”

Image Credits: jayk7 (opens in a new window) / Getty Images

All companies want more or less the same thing: growth. But how do you accomplish it?

Ideally, don’t start from scratch.

The race to grow faster is more pressing than ever before. … “[F]orward-thinking entrepreneurs and growth marketers simply must make time to study their competition, learn best practices and apply them to their own business growth,” Mark Spera, the head of growth marketing at Minted, writes in a guest column.

“Of course, you should still run your own experiments, but it’s just more capital-efficient to emulate than to trial-and-error from scratch. Here are five companies with growth strategies worth emulating — including the most important lessons you can begin applying to your business today.”

Image Credits: ChrisChrisW (opens in a new window) / Getty Images

With more than 50 million Americans suffering from chronic pain and musculoskeletal (MSK) medical problems, a number of startups are offering patients new products “that don’t resemble the cookie-cutter status quo,” reports Natasha Mascarenhas.

Startups hoping to enter this space have an uphill climb. Setting aside regulations that cover aspects like product packaging and marketing, they must compete with well-entrenched competition from Big Pharma as they try to partner with health insurance companies.

Natasha profiles three companies that are each taking a different approach to personalized health: Clear, Hinge Health and PeerWell.

Image Credits: Nigel Sussman (opens in a new window)

In the second part of an Exchange series looking at the global early-stage venture capital market, Alex Wilhelm and Anna Heim unpacked the scene in Latin America, discovering it looked a lot like the situation in the United States: slow Series A rounds, fast B rounds.

“Mega-rounds are no longer an exception in Latin America; in fact, they have become a trend, with ever-larger rounds being announced over the last few months,” they write.

Despite that, the funds aren’t being equitably distributed, and the region still lags behind its peers: Brazil has the most $1 billion startups in Latin America, with 12. The U.S., meanwhile, has 369, and China has 159.

But the Latin American market remains hot, if not quite as scorching as the U.S. and China.

Powered by WPeMatico

Before Twilio had a market cap approaching $56 billion and more than 200,000 customers, the cloud-communications platform developed a secret sauce to fuel its growth: a developer-focused model that dispensed with traditional marketing rules.

Software companies that sell directly to end users share a simple framework for managing growth that leverages discoverability, desirability and do-ability — the “aha!” moment where a consumer is able to incorporate a new product into their workflow.

Data show that traditional marketing doesn’t work on developers, and it’s not because they’re impervious to a sales pitch. Builders just want reliable tools that are easy to use.

As a result, companies that are looking to create and sell software to developers at scale must toss their B2B playbooks and meet their customers where they are.

Attorney Sophie Alcorn, our in-house immigration law expert, submitted two columns: On Monday, she analyzed a decision by the U.S. Department of Homeland Security not to cancel the International Entrepreneur Parole program, which potentially allows founders from other countries to stay in the U.S. for as long as 60 months.

On Wednesday, she responded to a question from an entrepreneur who asked whether it made sense to sponsor visas for workers who are working remotely inside the U.S.

Thanks very much for reading Extra Crunch this week, and have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: Peter Finch (opens in a new window) / Getty Images

Can you imagine making 13 attempts at something before attaining a successful outcome?

Alex Circei, CEO and co-founder of Git analytics tool Waydev, applied 13 times to Y Combinator before his team was accepted. Each year, the accelerator admits only about 5% of the startups that seek to join.

“Competition may be fierce, but it’s not impossible,” says Circei. “Jumping through some hoops is not only worth the potential payoff but is ultimately a valuable learning curve for any startup.”

In an exclusive exposé for TechCrunch, he shares four key lessons he learned while steering his startup through YC’s stringent selection process.

The first? “Put your business value before your personal vanity.”

Image Credits: Illustration by Nigel Sussman, art design by Bryce Durbin

In March, TechCrunch Daily Reporter Anna Heim was interviewing executives at Expensify to learn more about the company’s history and operations when they unexpectedly made themselves less available.

Our suspicions about their change of heart were confirmed on May 3 when the expense report management company confidentially filed to go public.

With a founding team comprised mainly of P2P hackers, it’s perhaps inevitable that Expensify doesn’t look and feel like something an MBA might envision.

“We hire in a super different way. We have a very unusual internal management structure,” said founder and CEO David Barrett. “Our business model itself is very unusual. We don’t have any salespeople, for example.”

Similar to the way companies must file a Form S-1 that describes their operations and how they plan to spend capital, TechCrunch EC-1s are part origin story, part X-ray. We published the first article in a series on Expensify on Monday:

We’ll publish the remainder of Anna’s series on Expensify in the coming weeks, so stay tuned.

Image Credits: Nigel Sussman (opens in a new window)

Construction tech unicorn Procore Technologies this week set a price range for its impending public offering. The news comes after the company initially filed to go public in February of 2020, a move delayed by the pandemic.

In March 2021, Procore filed again for a public offering, but its second shot ran into a cooling IPO market. The company filed another S-1/A in April, and then another in early May. This week’s filing is the first that sets a price for the Carpinteria, California-based software upstart.

But Procore is not the only company that filed and later put on hold an IPO to get back to work on floating. Kaltura, a software company focused on video distribution, also recently got its IPO back on track. Are we seeing a reacceleration of the IPO market? Perhaps.

Image Credits: Patcharin Saenlakon/EyeEm (opens in a new window) / Getty Images

Family physician Bobbie Kumar lays out the golden rules to ensure your healthcare product, service or innovation is on the right track.

Rule 1: “It’s not enough to develop a ‘new tool’ to use in a health setting,” Dr. Kumar writes. “Maybe it has a purpose, but does it meaningfully address a need, or solve a problem, in a way that measurably improves outcomes? In other words: Does it have value?”

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

I’m the founder of an early-stage, two-year-old fintech startup. We really want to move to San Francisco to be near our lead investor.

I heard International Entrepreneur Parole is back. What is it, and how can I apply?

— Joyous in Johannesburg

Image Credits: Nigel Sussman (opens in a new window)

If you have heard of Better.com but really had no idea what it does before this moment, welcome to the club. Mortgage tech is like pre-kindergarten applications — it applies to a very specific set of folks at a very particular moment. And they care a lot about it. But the rest of us aren’t really aware of its existence.

Better.com, a venture-backed digital mortgage lender, announced this week that it will combine with a SPAC, taking itself public in the second half of 2021. The unicorn’s news comes as the American IPO market is showing signs of fresh life after a modest April.

Image Credits: filadendron (opens in a new window) / Getty Images

The pandemic forced many employees to begin working from home, and, in doing so, may have changed the way we think about work. While some businesses have slowly returned to the office, depending on where you live and what you do, many information workers remain at home.

That could change in the coming months as more people get vaccinated and the infection rate begins to drop in the U.S.

Many companies have discovered that their employees work just fine at home. And some workers don’t want to waste time stuck on congested highways or public transportation now that they’ve learned to work remotely. But other employees suffered in small spaces or with constant interruptions from family. Those folks may long to go back to the office.

On balance, it seems clear that whatever happens, for many companies, we probably aren’t going back whole-cloth to the prior model of commuting into the office five days a week.

Image Credits: PM Images (opens in a new window) / Getty Images

On a recent episode of TechCrunch’s Equity podcast, hosts Natasha Mascarenhas and Alex Wilhelm invited Yext CFO Steve Cakebread and Latch CFO Garth Mitchell on to discuss when companies should go public, the costs and benefits of the process and when a SPAC can make sense. Yext pursued a traditional IPO a few years back; Latch is now going public via a blank-check company combination.

The chat was more than illustrative, as we got to hear two CFOs share their views on delayed public offerings and when different types of debuts can make the most sense. While the TechCrunch crew has, at times, made light of certain SPAC-led deals, the pair argued that the transactions can make good sense.

Undergirding the conversation was Cakebread’s recent IPO-focused book, which not only posited that companies going public earlier rather than later is good for their internal operations but also because it can provide the public with a chance to participate in a company’s success.

In today’s hypercharged private markets and frothy public domain, his argument is worth considering.

Image Credits: John Lund (opens in a new window) / Getty Images

Ken Harlan, the founder and CEO of Mobile Fuse, writes about the perks and pitfalls of software development kits.

“The digital media industry often talks about how much influence, dominance and power entities like Google and Facebook have,” Harlan writes. “Generally, the focus is on the vast troves of data and audience reach these companies tout. However, there’s more beneath the surface that strengthens the grip these companies have on both app developers and publishers alike.

“In reality, SDK integrations are a critical component of why these monolith companies have such a prominent presence.”

Image Credits: Nigel Sussman (opens in a new window)

The Exchange caught up with Appian CEO Matt Calkins after his enterprise app software company reported its first-quarter performance to discuss the low-code market and what he’s hearing in customer meetings. To round out our general thesis — and shore up our somewhat bratty headline — we’ve compiled a list of recent low-code and no-code venture capital rounds, of which there are many.

As we’ll show, the pace at which venture capitalists are putting funds into companies that fall into our two categories is pretty damn rapid, which implies that they are doing well as a cohort. We can infer as much because it has become clear in recent quarters that while today’s private capital market is stupendous for some startups, it’s harder than you’d think for others.

A pair of Bird e-scooters parked in Barcelona. Image Credits: Natasha Lomas/TechCrunch

Historically — and based on what we’re seeing in this fantastical filing — Bird proved to be a simply awful business. Its results from 2019 and 2020 describe a company with a huge cost structure and unprofitable revenue, per filings. After posting negative gross profit in both of the most recent full-year periods, Bird’s initial model appears to have been defeated by the market.

What drove the company’s hugely unprofitable revenues and resulting net losses? Unit economics that were nearly comically destructive.

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

My startup is in big-time hiring mode. All of our employees are currently working remotely and will likely continue to do so for the foreseeable future — even after the pandemic ends. We are considering individuals who are living outside of the U.S. for a few of the positions we are looking to fill.

Does it make sense to sponsor them for a visa to work remotely from somewhere in the United States?

— Selective in Silicon Valley

Image Credits: ivan101 / Getty Images

“Today, we live in a world of product-led growth, where engineers (and the software they have built) are the biggest differentiator,” says Coatue Management general partner Caryn Marooney and investor David Cahn. “If your customers love what you’re building, you’re headed in the right direction. If they don’t, you’re not.

“However, even the most successful product-led growth companies will reach a tipping point, because no matter how good their product is, they’ll need to figure out how to expand their customer base and grow from a startup into a $1 billion+ revenue enterprise.

“The answer is the hamburger model. Why call it that? Because the best go-to-market (GTM) strategies for startups are like hamburgers:

Image Credits: belterz (opens in a new window) / Getty Images

Krish Subramanian, the co-founder and CEO of Chargebee, writes that while subscription business models are attractive, there are two major pitfalls: First, payment.

“Regardless of company size, there’s an ongoing need to convince customers to sign up long term,” Subramanian writes. “The second issue: How do businesses cover the funding gap between when customers sign up and when they pay?”

Image Credits: Aimee Blasee (opens in a new window)

Scott Lenet, the president of Touchdown Ventures, asks how deal-makers should think about how to handle themselves when counter-parties attempt to change an agreement. “When is it OK to modify terms, and when should deal-makers stand firm?” he asks.

“Entrepreneurs and investors should recognize that contracts are worth very little without the ongoing relationship management that keeps all parties aligned. Enforcement is so unusual in the world of startups that I consider it a mostly dead-end path. In my experience, good communication is the only reliable remedy. This is the way.”

Image Credits: Ray Massey / Getty Images

“Search engine optimization, PR, paid marketing, emails, social — marketing and communications is crowded with techniques, channels, solutions and acronyms,” writes Dominik Angerer, CEO and co-founder of Storyblok, which provides best practice guidance for startups on how to build a sustainable approach to marketing their content. “It’s little wonder that many startups strapped for time and money find defining and executing a sustainable marketing campaign a daunting prospect.

“The sheer number of options makes it difficult to determine an effective approach, and my view is that this complexity often obscures the obvious answer: A startup’s best marketing asset is its story.”

Powered by WPeMatico

The number of SPACs in the deep tech sector was skyrocketing, but a combination of increased SEC scrutiny and market forces over the past few weeks has slowed the pace of new SPAC transactions. The correction is an inevitable step on the path to mainstreaming SPACs as an alternative to IPOs, but it won’t cause them to go away. Instead, blank-check vehicles will evolve and will occupy a small and specialized — but important — part of the startup financing landscape.

I believe that SPAC financings can solve a major problem for all capital-intensive technology startups: the need for faster — and potentially cheaper — access to large amounts of capital to fund product development over multiple years.

The tsunami of SPAC financings sparked commentary from all corners of the capital markets community, from equity analysts and securities lawyers to VCs and fund managers — and even central bankers. That’s understandable, as more than $60 billion of SPAC deals have been announced since the beginning of 2020, plus $55 billion in PIPE capital, according to investment bank PJT Partners.

The views debated by finance experts often relate to the reasonableness of SPAC pricing and transaction structures, the alignment of incentives for stakeholders, and post-merger financial and stock price performance. But I’m not going to add another voice to the debate on the risk-reward calculus.

As the co-founder of a quantum computing software startup who worked in financial markets for two decades, I’d like to offer my perspective on two issues that I think my peers care more about: Can SPACs still solve the funding problem for capital-intensive, deep tech startups? And will they become a permanent financing option?

I believe that SPAC financings can solve a major problem for all capital-intensive technology startups: the need for faster — and potentially cheaper — access to large amounts of capital to fund product development over multiple years.

SPACs have created a limitless well of capital that deep tech startups are diving into. That’s because they are proving to be more attractive than other sources of financing, such as taking investments from later-stage VC funds or growth equity funds with finite fund sizes and specific investment themes.

The supply of growth capital from these vehicles has been astounding. In 2020, SPACs alone raised more than $83 billion via 248 IPOs, which is equal to a third of the total $300 billion raised by the entire global VC community. If the present rate of financings had continued, the annual amount of SPAC financings would have been on par with the total R&D expenditure of the U.S. government — roughly $130 billion to $150 billion.

This new supply of capital can let startups keep the lights on, helping them address a practical need while they develop products that may take a decade to field. Before SPACs, any startup that wanted to remain independent had to lurch from one round of VC financing to the next. That, as well as the intense IPO process, is a major time sink for management teams and distracts them from focusing on product development.

Powered by WPeMatico

The latest in a string of space tech SPACs announced this year is Redwire, an entity created by a PE firm in 2020, which has acquired a number of smaller companies including Adcole Space, Roccor, Made in Space, LoadPath, Oakman Aerospace, Deployable Space Systems and more — all within the last year or so. Redwire announced that it will go public through a merger with special purpose acquisition company Genesis Park Acquisition Corp., and the combined company will list on the NYSE.

The deal puts Redwire’s pro forma enterprise value at $615 million, and is expected to provide an additional $170 million to Redwire’s coffers post-merger, including a PIPE valued at over $100 million. Unsurprisingly, one of the uses of the proceeds that Redwire intends to pursue is continued M&A activity to build out its list of service offerings in the space domain.

Redwire’s mandate isn’t specifically to go after new space companies, and instead its targets share in common expertise in a particular, rather narrow slice of the severally crowded space market. It’s capabilities include on-orbit manufacturing and servicing; satellite design, manufacture and assembly; payload integration; sensor design and development; and more. The idea appears to be to build a full-stack infrastructure company that can offer tip-to-tail space technology services, exclusive really only of launch and ground station components (for now).

It’s a smart approach for a bourgeoning new space economy where increasingly, technology companies who want to operate in space would rather focus on their unique value proposition, and outsource the complex, but mostly settled business of actually getting to, and operating in, space. Other companies are addressing the market in similar ways, with launchers bringing more of that part of the process in-house so their payload customers basically only have to show up with the sensor or communication device they want to send to space, and the launcher providing everything else — including even the satellite, in the relatively near future.

Redwire has proven revenue-generating power, with projected 2021 revenue of $163 million, and many of the companies now operating under its umbrella are fairly mature and have been operating cash flow positive for many years. Accordingly, a SPAC as a path to public markets likely does make sense in this particular instance, but the increasing frequency and volume of space companies choosing this route, is, on the whole, a trend to watch with healthy skepticism.

Powered by WPeMatico