special-purpose acquisition company

Auto Added by WPeMatico

Auto Added by WPeMatico

Metromile began trading as a public company yesterday. Its exit from the private market was accelerated by its decision to combine with a special purpose acquisition company, or SPAC.

Such transactions have exploded in popularity in recent years, bridging the gap between a host of richly valued private companies and endless bored capital. SPACs raise cash, go public and then merge with a private entity. The SPAC then dissolves itself into the combined entity, a process that often includes an additional slug of money (PIPE) for good measure.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

SPAC-led debuts can move faster than a traditional IPO, making them attractive to companies in a hurry. And with more visibility into how much capital might be raised than during a traditional public-offering pricing run, they can smooth worries amongst target-companies regarding how much cash they can attract by leaving the private-market fold.

Metromile is hardly the final company we expect to debut this year via a SPAC. The list is long and may include fellow neoinsurance company Hippo. (Hippo declined to comment on the matter.)

Metromile is hardly the final company we expect to debut this year via a SPAC. The list is long and may include fellow neoinsurance company Hippo. (Hippo declined to comment on the matter.)

But with many more SPACs coming our way, we took Metromile’s debut as a learning moment. To that end, we got on the horn with CEO Dan Preston to chat about what the day meant for his company, and to elicit a note or two on the SPAC process for our own enjoyment.

TechCrunch asked Preston about the SPAC world and how his combination came about. He said his firm started by dipping its toe into the blank-check waters, kicking off with a small set of conversations, chats that quickly gathered traction.

But don’t take that to mean that any company will elicit a similar market response. Preston said SPACs are designed for a specific class of company; namely those that want or need to share a bit more story when they go public. Younger companies, in other words, for whom a traditional S-1 filing might not be provide a sufficient summation of its potential.

Powered by WPeMatico

Shell’s plan to roll out 500,000 electric charging stations in just four years is the latest sign of an EV charging infrastructure boom that has prompted investors to pour cash into the industry and inspired a few companies to become public companies in search of the capital needed to meet demand.

Since the beginning of the year, three companies have been acquired by special purpose acquisition vehicles and are on a path to go public, while a third has raised tens of millions from some of the biggest names in private equity investing for its own path to commercial viability.

The SPAC attack began in September when an electric vehicle charging network ChargePoint struck a deal to merge with special purpose acquisition company Switchback Energy Acquisition Corporation, with a market valuation of $2.4 billion. The company’s public listing will debut February 16 on the New York Stock Exchange.

In January, EVgo, an owner and operator of electric vehicle charging infrastructure, agreed to merge with the SPAC Climate Change Crisis Real Impact I Acquisition for a valuation of $2.6 billion — a huge win for the company’s privately held owner, the power development and investment company LS Power. LS Power and EVgo management, which today own 100% of the company, will be rolling all of its equity into the transaction. Once the transaction closes in the second quarter, LS Power and EVgo will hold a 74% stake in the newly combined company.

One more deal soon followed. Volta Industries agreed to merge this month with Tortoise Acquisition II, a tie-up that would give the charging company named after battery inventor Alessandro Volta a $1.4 billion valuation. The deal sent shares of the SPAC company, trading under the ticker SNPR, rocketing up 31.9% in trading earlier this week to $17.01. The stock is currently trading around $15 per share.

Not to be outdone, private equity firms are also getting into the game. Riverstone Holdings, one of the biggest names in private equity energy investment, placed its own bet on the charging space with an investment in FreeWire. That company raised $50 million in a new round of funding earlier this year.

“The writing is on the wall and the investors have to take the time. There’s been a flight out of the traditional investment opportunities in markets,” said FreeWire chief executive Arcady Sosinov, in an interview. “There’s been a flight out of the oil and gas companies and out of the traditional utilities. You have to look at other opportunities… This is going to be the largest growth opportunity of the next 10 years.”

FreeWire deploys its infrastructure with BP currently, but the company’s charging technology can be rolled out to fast food companies, post offices, grocery stores or anywhere people go and spend somewhere between 20 minutes and an hour. With the Biden administration’s plan to boost EV adoption in federal fleets, post offices actually represent another big opportunity for charging networks, Sosinov said.

“One of the reasons we find electrification of mobility so attractive is because it’s not if or how, it’s when,” said Robert Tichio, a partner at Riverstone in charge of the firm’s ESG efforts. “Penetration rates are incredibly low… compare that to Norway or Northern Europe. They have already achieved double-digit percentages.”

A recent Super Bowl commercial from GM featuring Will Farrell showed just how far ahead Norway is when it comes to electric vehicle adoption.

“The demands on capital in the electrification of transport will begin to approach three quarters of a trillion annually,” Tichio said. “The short answer to your question is that the needs for capital now that we have collectively, politically, socially economically come to a consensus in terms of where we’re going and we couldn’t say that 18 months ago is going to be at a tipping point.”

Shell already has electric vehicle charging infrastructure that it has deployed in some markets. Back in 2019 the company acquired the Los Angeles-based company Greenlots, an EV charging developer. And earlier this year Shell made another move into electric vehicle charging with the acquisition of Ubitricity in the U.K.

“As our customers’ needs evolve, we will increasingly offer a range of alternative energy sources, supported by digital technologies, to give people choice and the flexibility, wherever they need to go and whatever they drive,” said Mark Gainsborough, executive vice president, New Energies for Shell, in a statement at the time of the Greenlots acquisition. “This latest investment in meeting the low-carbon energy needs of US drivers today is part of our wider efforts to make a better tomorrow. It is a step towards making EV charging more accessible and more attractive to utilities, businesses and communities.”

Powered by WPeMatico

Micromobility startup Helbiz, which now operates across Europe and the USA, is merging with a special purpose acquisition company (SPAC) to become a publicly listed company, giving it a war chest to potentially roll-up smaller competitors in the space, as well as the resources to expand into “cloud” or “ghost” kitchens as part of a move into food delivery.

Helbiz intends to merge with GreenVision Acquisition Corp. (Nasdaq: GRNV) in the second quarter of 2021. The combined entity will be named Helbiz Inc. and will be listed on the Nasdaq Capital Market under the new ticker symbol, “HLBZ.”

The transaction includes $30 million PIPE anchored by institutional investors and approximately $80 million in net proceeds will be fed into Helbiz’s micromobility and advertising businesses, which have 2.7 million users.

Helbiz says the merged entity will have a valuation of $408 million, and by run Helbiz’s existing management under CEO Salvatore Palella.

Palella said: “Through this transaction, we’re committed to fulfilling our vision in revolutionizing transport by using micromobility to become a seamless last-mile solution.”

He further revealed to me that the company plans to establish “ghost kitchens” in Milan and Washington, DC later this year, with the aim of introducing a five-minute delivery time.

Helbiz has tried to differentiate itself from other players like Lime and Bird by offering e-scooters, e-bicycles and e-mopeds all on one platform.

Key to Helbiz’s offering is an integrated geofencing platform that tends to appeal to city authorities who don’t want scooters left in random places, as well as a swappable battery that enables easier charging of the devices. Its subscription service allows users to take unlimited 30-minute trips on its e-bikes and e-scooters every month.

In Europe the company currently operates a fleet of e-scooters and e-bicycles in Milan, Turin, Verona, Rome, Madrid and Belgrade, and in the U.S. it operates in Washington, DC, Alexandria, Arlington and Miami.

David Fu, chairman, and CEO of GreenVision, commented: “Helbiz has distinguished itself as the only company to offer e-scooters, e-bicycles, and e-mopeds all on one user-friendly platform… Helbiz has a proven and capital-light business model that combines hardware, software, and services with extensive customer relationships.”

Powered by WPeMatico

In light of climate change and escalating global energy demand, more emphasis is being placed on emerging clean technologies — ranging from renewables and energy storage to nuclear power. Although these technologies have tremendous potential, they require lots of innovation, and innovation needs abundant capital.

The issue: early-stage financing for clean tech hasn’t been plentiful, and it’s stifling the growth of new energy companies. Why is this? In general, clean tech companies lack the startup advantages of agility and flexibility.

“Moving fast” works for products such as consumer mobile apps and SaaS solutions. The clean tech sector, on the other hand, tends to involve highly regulated, capital-intensive, mission-critical infrastructure.

That has hurt both returns and well-intentioned impact. According to Cambridge Associates, venture-backed companies have returned, on average, -15% internal rate of return (IRR) since 2000. Contrast that to venture-backed companies in healthcare, which returned 24% in IRR over the same time period.

While noble in its aims to make the world a better, cleaner, safer, healthier place through technology, clean tech venture capital has suffered simply because clean tech does not fit the traditional venture capital model. Central to the venture capital model is the ability to de-risk new ideas and significantly capitalize the most promising ones, allowing for liquidity via M&A or initial public offering (IPO).

Early-stage financing for clean tech hasn’t been plentiful, and it’s stifling the growth of new energy companies.

This construct allows for the return of venture capital dollars, plus appreciation that enables VC firms to raise new funds. These capitalization events also allow the venture-backed company to accelerate growth and maximize market impact.

How this construct works is evident when comparing healthcare and clean tech. In healthcare, new innovations are de-risked by VCs. More mature innovations are acquired or reach IPO every year. As a result, the average annual ratio of dollars raised via an exit to VC-invested dollars since 2012 is 1.8. This ratio is only 0.2 for clean tech, an 800-plus percent difference in the wrong direction. This has resulted in poor returns and limited capitalization of clean tech companies.

Given the state of the world’s environment and lack of abundant energy in emerging economies, we need to collectively fix this issue. Special purpose acquisition companies (SPACs) are significantly improving clean tech’s venture capital construct. According to Investopedia:

SPACs are companies with no commercial operations that are formed strictly to raise capital through an initial public offering (IPO) for the purpose of acquiring an existing company.

Also known as “blank-check companies,” SPACs have been around for decades. In recent years, they’ve become more popular, attracting big-name underwriters and investors and raising a record amount of IPO money in 2019.

In 2020, more than 110 SPACs completed transactions in the U.S., capitalizing these companies with more than $29 billion.

In 2020, SPACs capitalized clean tech companies with almost $4 billion of capital, including Fisker, Lordstown Motors, QuantumScape, Hyliion, XL Fleet and others. This helped push the ratio of funds raised at exit to venture capital invested in 2020 from the previous 0.2 average to a much healthier 0.6, a 200% improvement.

In 2021, we will likely see even further improvement. Why? Because there are 43 active SPACs looking toward or finalizing merger targets with a clean tech focus, potentially providing $12 billion in growth capital. Even if there are no more new SPACs in 2021 and a historically low average of M&As and IPOs, 2021 promises continued improvement for clean tech investment.

One of the most high-profile clean tech SPACs was Nikola Corporation. The battery-electric and hydrogen-powered truck maker has attracted much fanfare since going public last June through a reverse merger with special purpose acquisition company VectoIQ. The company’s market capitalization soared and things seemed to be going well, but things became controversial later in the year when the company was accused of making false statements about its technology and other things.

Although examples such as Nikola have the potential to tarnish the emergence of SPACs as a way to spur clean tech investing, they shouldn’t. There are plenty of examples of emerging companies that scream quality and integrity. For example, Stem*, a leader in the energy storage optimization space, is now going public, pending SEC approval, via the Star Peak SPAC.

Public markets are receiving the SPAC with enthusiasm. Assuming the merger happens, Stem will be capitalized with greater than $450 million of cash to accelerate growth and drive impact. It’s an illustration of SPACs as a positive venture capital construct that is needed to make clean tech work and become a thriving sector.

As a long-time clean tech venture capitalist myself, it is interesting that public investment via the SPAC may be the correcting element for the clean tech VC construct. For years, I assumed that corporates would step up their M&A activity at premium valuations to solve this issue, but I’ve spent a long time waiting.

Judging by activity, corporates seem content to continue playing the still very important investor/nurturer role, versus the “owning” role. Regardless, capitalizing promising clean tech companies can only mean one thing: clean-tech-related impact is coming like never before as these companies require and use capital to scale.

New and more diverse approaches to finding and funding new, great clean tech companies are sorely needed. SPACs are going to be the tool needed to bring clean tech up to par with sectors such as healthcare. It’s a development that will benefit all of us.

*Stem is a Wind Ventures portfolio company.

Powered by WPeMatico

Taboola is the latest company seeking to go public via special purpose acquisition company — more commonly known as a SPAC.

To achieve this, it will merge with ION Acquisition Corp., which went public in 2020 with the aim of funding an Israeli tech acquisition (Haaretz reported last month that Taboola was in talks with ION). The transaction is expected to close in the second quarter, and the combined company will trade on the New York Stock Exchange under the ticker symbol TBLA.

Founded in 2007, Taboola powers content recommendation widgets (and advertising on those widgets) across 9,000 websites for publishers including CNBC, NBC News, Business Insider, The Independent and El Mundo. It says it reaches 516 million daily active users while working with more than 13,000 advertisers.

The company had previously planned to merge with competitor Outbrain before the deal was canceled last fall, with sources pointing to the market impact of the COVID-19 pandemic, a “challenging culture fit” and regulatory issues to explain the deal’s end.

Taboola’s founder and CEO Adam Singolda (pictured above, left) told me that this didn’t lead directly to the SPAC deal. But he said, “I always wanted to go public,” which wasn’t possible while the merger was in the works. Once that deal was called off, and with 2020 turning out to be a strong year for Taboola — it’s projecting revenue of $1.2 billion, including $375 million ex-TAC revenue (revenue after paying publishers), with over $100 million in adjusted EBITDA — the time seemed right, and ION seemed like the right partner.

“We believe Taboola is an open web recommendation leader which is well positioned to challenge the walled gardens,” said ION CEO Gilad Shany in a statement. “We were looking to merge with a global technology leader with Israeli DNA and we found that in Taboola. The combination of long-term partnerships built by the company with thousands of open web digital properties, their direct access to advertisers, massive global reach and proven AI technology, allows Taboola to provide significant value to their partners while also achieving attractive unit economics as the company grows.”

The deal will value Taboola at $2.6 billion. Through this transaction, the company plans to raise a total of $545 million, including $285 million in PIPE financing secured from Fidelity Management & Research Company, Baron Capital Group, funds and accounts managed by Hedosophia, the Federated Hermes Kaufmann Funds and others.

Singolda said that the company plans to invest $100 million in R&D this year, and that he hopes to expand the technology into areas like e-commerce and TV advertising, with the goal of moving “beyond the browser.” More broadly, he said he wants Taboola to be “a strong public company that champions the open web.”

“The open web is a $64 billion advertising market [according to Taboola estimates], but there’s no Google for the open web,” he said.

Yes, Google itself spends plenty of time talking about similar ideas, but Singolda argued that while Google has consumer products like search and YouTube that compete with other publishers for time and attention, “Taboola is not in the consumer business … We serve our partners, and it’s in our identity to drive audience growth, engagement and revenue.”

Powered by WPeMatico

There’s no denying that 2020 has been the year of the special purpose acquisition company.

Since the beginning of the year, 219 SPACs have raised $73 billion, according to widely reported market research from Goldman Sachs. That’s a 462% jump from 2019 and more than traditional public offerings raised by about $6 billion. By some counts, roughly one quarter of the SPACs that have been announced will target climate-related businesses.

Since the beginning of the year, 219 SPACs have raised $73 billion.

Already, of the 78 deals that have either completed or announced a merger since 2018, just over one-third have been climate-related, as tallied by Climate Tech VC. And these SPACs have outperformed the broader technology market, with the 10 climate tech companies that have completed mergers averaging a 131% return on investment versus the 50% return of the total SPAC market (assuming average offering prices of $10 per share).

Clearly this has been a banner year for companies that are tackling the climate crisis across a number of verticals, but can it last?

There are a few reasons to think that it can — led chiefly by the demand for these kinds of public offerings from institutional investors, including the pension funds, mutual funds and asset managers handling trillions of investment dollars.

“[The] current wave [of SPACs] is because over the past 24 months the institutional investor universe has come fully into believing that climate solutions are going to be a major growth area in the 2020s and beyond, but they weren’t seeing options available to them for investing into,” wrote longtime clean technology investor, Rob Day, in a DM.

“The available publicly traded ‘green’ companies were already getting really bought up, and the private equity options were underwhelming as well (smallish in the case of VC, low returns in the case of large-format projects). Throw in a Robinhood market of retail investors with a lot of enthusiasm for EVs and such, and you have a nice recipe for this to happen.”

Powered by WPeMatico

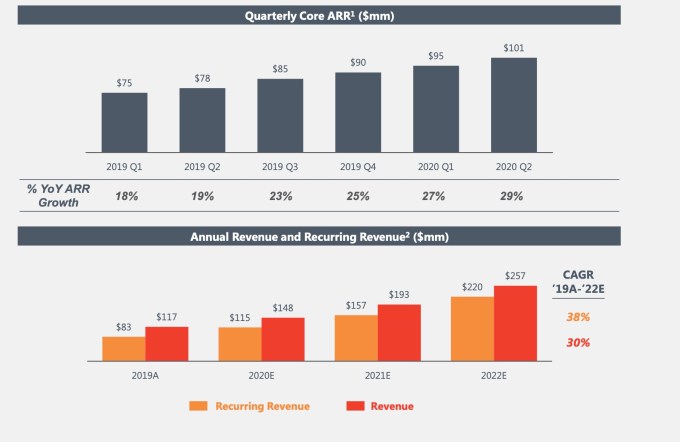

AvePoint, a company that gives enterprises using Microsoft Office 365, SharePoint and Teams a control layer on top of these tools, announced today that it would be going public via a SPAC merger with Apex Technology Acquisition Corporation in a deal that values AvePoint at around $2 billion.

The acquisition brings together some powerful technology executives, with Apex run by former Oracle CFO Jeff Epstein and former Goldman Sachs head of technology investment banking Brad Koenig, who will now be working closely with AvePoint’s CEO Tianyi Jiang. Apex filed for a $305 million SPAC in September 2019.

Under the terms of the transaction, Apex’s balance of $352 million plus a $140 million additional private investment will be handed over to AvePoint. Once transaction fees and other considerations are paid for, AvePoint is expected to have $252 million on its balance sheet. Existing AvePoint shareholders will own approximately 72% of the combined entity, with the balance held by the Apex SPAC and the private investment owners.

Jiang sees this as a way to keep growing the company. “Going public now gives us the ability to meet this demand and scale up faster across product innovation, channel marketing, international markets and customer success initiatives,” he said in a statement.

AvePoint was founded in 2001 as a company to help ease the complexity of SharePoint installations, which at the time were all on-premise. Today, it has adapted to the shift to the cloud as a SaaS tool and primarily acts as a policy layer enabling companies to make sure employees are using these tools in a compliant way.

The company raised $200 million in January this year led by Sixth Street Partners (formerly TPG Sixth Street Partners), with additional participation from prior investor Goldman Sachs, meaning that Koenig was probably familiar with the company based on his previous role.

The company has raised a total of $294 million in capital before today’s announcement. It expects to generate almost $150 million in revenue by the end of this year, with ARR growing at over 30%. It’s worth noting that the company’s ARR and revenue has been growing steadily since Q12019. The company is projecting significant growth for the next two years with revenue estimates of $257 million and ARR of $220 million by the end of 2022.

Image Credits: AvePoint

The deal is expected to close in the first quarter of next year. Upon close the company will continue to be known as AvePoint and be publicly traded on Nasdaq under the new ticker symbol AVPT.

Powered by WPeMatico