SPAC

Auto Added by WPeMatico

Auto Added by WPeMatico

Gingko Bioworks, a synthetic biology company now valued at around $15 billion, begins trading on the New York Stock Exchange today.

Gingko’s market debut is one of the largest in biotech history. It’s expected to raise about $1.6 billion for the company. It’s also one of the biggest SPAC deals done to date — Gingko is going public through a merger with Soaring Eagle Acquisition Corp., which was announced in May.

Shares opened at $11.15 each this morning under the ticker DNA — biotech dieharders will recognize it as the former ticker used by Genentech.

The exterior of the NYSE is decked out in Gingko décor. The imagery is clearly sporting Jurassic Park themes, as MIT Tech Review’s Antonio Regalado pointed out. It’s probably intentional: Jason Kelly, the CEO of Ginkgo Bioworks, has been re-reading “Jurassic Park” this week, he tells TechCrunch.

The décor also sports a company motto: “Grow everything.”

Ginkgo was founded in 2009, and now bills itself as a synthetic biology platform. That’s essentially premised on the idea that one day, we’ll use cells to “grow everything,” and Gingko’s plan is to be that platform used to do that growing.

Kelly, who often uses language borrowed from computing to describe his company, likens DNA to code. Gingko, he says, aims to “program cells like you can program computers.” Ultimately, those cells can be used to make stuff: like fragrances, flavors, materials, drugs or food products.

The biggest lingering question over Gingko, ever since the SPAC deal was announced, has centered on its massively high valuation. When Moderna, now a household name thanks to its COVID-19 vaccines, went public in 2018, the company was valued at $7.5 billion. Gingko’s valuation is double that number.

“I think that surprises people to be honest,” Kelly says.

Ginkgo’s massive valuation seems even starker when you look at its existing revenues. SEC documents show that the company pulled in $77 million in revenue in 2020, which increased to about $88 million in the first six months of 2021 (per an August investor call). The company has also reported losses: including $126.6 million in December 2020 and $119.3 million in 2019.

Gingko is aiming to increase revenue a significant amount in 2021. SEC documents initially noted that the company aimed to draw about $150 million in revenue in 2021, but the August earning call updated that total for the year to over $175 million.

Gingko aims to make money in two ways: first it contracts with manufacturers during the research and development phase (i.e. while the company works out how to manufacture a cell that spits out a certain fragrance, bio-based nylon or meatless burger). That process happens in Gingko’s “foundry,” a massive factory for bioengineering projects.

This source of money is already starting to flow. Gingko reported $59 million in foundry revenue for 2020, and anticipates $100 million in 2021, per the August investor call.

This revenue, though, isn’t covering the full costs of Gingko’s operations, according to the information shared by the company in SEC documents. It is covering an increasing share, though, and as Gingko scales up its platform, costs will come down. Based on fees alone, Kelly projects Gingko will break even by 2024 or 2025.

The second type of revenue comes from royalties, milestone payments or, in some cases, equity stakes in the companies that go on to sell products, like fragrances or meatless burgers, made using Gingko’s facilities or know-how. It’s this source of income that will make up the vast majority of the company’s future worth, according to its expectations.

Once the product is made and marketed by another company, it requires little to no more work on Gingko’s part — all the company does is collect cash.

The company is often hesitant to incorporate these earnings into projections, because they rely on other companies bringing products to market. That means it’s hard to know for sure when these downstream payments will emerge. “In our models, we are very sensitive that, at the end of the day, they’re not our products. I cannot predict when Roche might bring a drug to market and give me my milestones,” says Kelly.

Kelly says there’s evidence this model will start to work in the near-term.

Gingko earned a “bolus” milestone payment of 1.5 million shares of The Cronos Group, a cannabis company, for developing a commercially viable, lab-grown rare cannabinoid called CBG for commercial use (there are seven more in strains development, says Kelly). These milestone payments (in cash or shares) are earned when a company achieves some predetermined goal using Gingko’s platform.

Gingko has also worked with Aldevron to manufacture an enzyme critical to the production of mRNA vaccines, and plans to collect royalty payments from that relationship — though no foundry fees were collected from this project.

Finally, Gingko has negotiated an equity stake in Motif Foodworks, a spinout company based on its technology. That company has so far raised about $226 million, and will aim to launch a lab-grown beef product developed at Gingko’s foundry, paying Gingko the aforementioned foundry fees already for this contribution.

This rich source of cash will depend a lot on the outside contractor’s ability to manufacture and sell products made using Gingko’s platform. This opens the company up to some risk that’s beyond its control. Maybe, for instance, it turns people don’t want bio-manufactured meat as much as many anticipated — that means some types of downstream payments may not materialize.

Kelly says he’s not particularly worried about this. Even if one particular program fails, he’s planning on having so many programs running that one or two are bound to succeed.

“I’m just sorta like: some will work, some won’t work. Some will take a year, some will take three years. It doesn’t really matter, as long as everybody is working with us,” he says. “Apple doesn’t stress about what apps are going to be the next big app in the app store,” he continues.

One key metric to watch for Gingko going forward will be how many new cell programs they’re managing to close. So far, Gingko has added 30 programs this year, says Kelly. Last year, there were 50 programs.

Remember: Some of the projects are Gingko spinouts, like Motif Foodworks, not customers that come to the platform on their own. And historically, the number of companies Gingko has partnered with has been a point of criticism. Per SEC documents, the majority of revenue came from two large partners in 2020 — though Kelly told Business Insider that this was a pandemic-related downturn.

The more programs Gingko has, the more it becomes insulated from the success or failure of any one product. Plus it’s a sign that people are at least using the “app store” for biology.

“The biggest value driver of Gingko is how quickly we add programs,” Kelly says.

Powered by WPeMatico

What a busy week in the world of media liquidity.

That’s a sentence you don’t get to write often. Regardless, news broke this week that Axel Springer is buying U.S. political journalism outfit POLITICO. The transaction was expected, but the eye-popping roughly $1 billion price tag still has tongues wagging. We even got on the podcast to chat about it.

And Forbes announced that it is going public via a SPAC. The business publication’s news follows BuzzFeed’s journey to the public markets through a blank-check company. Hot media liquidity summer? Something like that.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

That TechCrunch is in the process of being sold to private equity, of course, is not something that we should forget. Shoutout to the Verizon bankers who found a way to get rid of us while also deleveraging Verizon’s debt profile. Ten points.

I want to take a quick tour of the Forbes SPAC deck this morning. Our notes on BuzzFeed’s are here, in case you want to run comparisons. This will be easy and fun. Perfect Friday morning fare. Into the data!

I want to take a quick tour of the Forbes SPAC deck this morning. Our notes on BuzzFeed’s are here, in case you want to run comparisons. This will be easy and fun. Perfect Friday morning fare. Into the data!

In corporate-speak, Forbes Global Media Holdings is merging with blank-check company Magnum Opus Acquisition Limited. The transaction will close either Q4 2021 or Q1 2022, Forbes estimates.

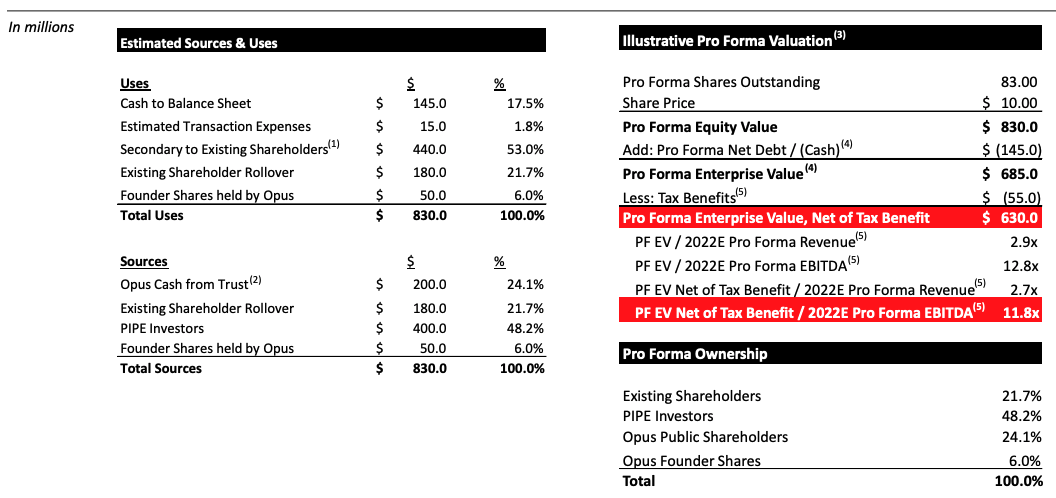

The deal itself is somewhat modest in scale compared with other SPAC deals we’ve recently looked into. Forbes reports that it will sport “an implied pro forma enterprise value of $630 million, net of tax benefits,” after its completion. Some $600 million in gross proceeds will be derived from Magnum Opus funds “and $400 million of additional capital through a private placement of ordinary shares of the combined company,” Forbes writes.

The company will sport an equity valuation of $830 million after the deal closes, per its own calculations. That number will change some depending on redemptions ahead of the combination. The gap between the large dollars going into the deal and the modest final valuation of the public Forbes entity is due to some $440 million in secondary transactions for existing Forbes shareholders.

In case you’d prefer all of that in table form, here’s the Forbes investor deck:

Image Credits: Forbes SPAC deck

Is $830 million a fair price? Let’s dig into Forbes’ results.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here. I also tweet.

Today’s show was good fun to put together. Here’s what we got to:

Woo! And that’s the start to the week. Hugs from here, and we’ll chat you on Wednesday!

Equity drops every Monday at 7:00 a.m. PST, Wednesday, and Friday at 6:00 a.m. PST, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts!

Powered by WPeMatico

Newly reported financial data from Bird, an American scooter sharing service, shows a company with an improving economic model and a multiyear path to profitability. However, that path is fraught unless a number of scenarios all work out in concert and without a glitch.

Bird, well known for its early battles with domestic rival Lime, is pursuing a SPAC-led deal that will see it go public and raise fresh capital. The former startup is merging with Switchback II Corporation in a deal that values it at around $2.3 billion, including a $160 million PIPE (private investment in public equity) component. (Note: The group purchasing TechCrunch’s parent company from its own parent company is part of the Bird PIPE.)

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

COVID-19 hasn’t been kind to Bird and similar companies around the world. As many around the world stayed home, usage of shared-asset services and ride-hail applications fell sharply. Bird saw rides decline. Airbnb took a temporary hit. Uber and Lyft saw ride demand fall.

Responses to the crisis were varied. Airbnb cut costs and raised external capital. Lyft cut expenses and focused on its core model while Uber grew its food delivery business, which saw transaction volume soar as demand fell for its traditional business.

Responses to the crisis were varied. Airbnb cut costs and raised external capital. Lyft cut expenses and focused on its core model while Uber grew its food delivery business, which saw transaction volume soar as demand fell for its traditional business.

Meanwhile, Bird flipped its entire business model. That decision has helped the scooter outfit improve its economics markedly, giving it a shot at generating profit in the future — provided its forecasts prove achievable.

This morning, let’s talk about how Bird has changed its business, their impacts on its operating results and how long the company thinks its climb to profitability is.

In their initial forms, Bird and Lime bought and deployed large fleets of electric scooters. Not only was this capital intensive, the companies also wound up with costs that were more than sticky — charging wasn’t simple or cheap, moving scooters around to balance demand took both human capital and vehicles, and the list went on.

Throw in vehicle depreciation — the pace at which scooters in the wild degraded from use or abuse — and the businesses proved excellent vehicles for raising capital and throwing that money at more scooters, costs, and, as it turned out, losses.

Results improved somewhat over time, though. As scooter-share companies increasingly built their own hardware, their economics improved. Sturdier scooters meant lower depreciation, and better battery tech could allow for more rides per charge. That sort of thing.

But the model wasn’t incredibly lucrative even before COVID-19 hit. Costs were high, and the model did not break-even, even on a gross margin basis, let alone when considering all corporate expenses. You can see the financial mess from that period of operations in historical Bird results.

Powered by WPeMatico

Joby Aviation is now public, 12 years after JoeBen Bevirt founded the company at his ranch in the Santa Cruz mountains. The air taxi developer began trading on the New York Stock Exchange on Wednesday under the ticker symbol “JOBY,” after completing a merger with special purpose acquisition company Reinvent Technology Partners.

As of 10:00 AM ET, the price per share was at $11.01, up 9.8% from its prior-day closing amount.

Joby’s post-transaction valuation now stands at $4.5 billion, the largest in the industry. It also now has the highest cash balance. All told, Joby has around $1.6 billion in total capital to take its air taxi operations to commercialization in 2024. That includes $835 million of private-investment-in-public-equity, as well as more than $500 million of capital on the balance sheet.

RTP reported to the Securities and Exchange Commission that around 63% of the 69 million ordinary shares were redeemed prior to the public trading debut, giving Joby access to $255 million out of the $690 million of cash held in trust from the blank-check firm.

We have been working for over a decade to get our technology ready for market and are excited to take this moment to celebrate our achievements so far. #nyse #experiencesquare #eVTOL @NYSE pic.twitter.com/XlpxXiA1Pa

— Joby Aviation (@jobyaviation) August 11, 2021

It’s a sizable amount, but creating an entirely new form of transportation is a capital-intensive business. Joby’s executive chairman Paul Sciarra told TechCrunch he thinks $1.6 billion will be enough to prepare the company for launch.

“We think that’s enough to execute on the things that matter over the next few years, and those are […] one, ensuring that we execute on the certification program; two, showing we can demonstrate our ability to repeatedly manufacturing these aircraft in a certifiable way; and then third and finally, the opportunity to lay the groundwork for commercial launch,” Sciarra said.

Joby is developing a five-seat electric vertical take-off and landing aircraft, which it unveiled to much anticipation in February. The company, which has backing from Toyota and JetBlue, has released a slew of announcements in recent months as it geared up for the public listing.

“A lot of people talk about us as a secretive company,” Bevirt said in an interview with TechCrunch. “We’re not actually a secretive company, we just choose to do the work and then show our work, rather than talking about it and then doing it.”

Joby’s merger with blank-check firm Reinvent, headed by LinkedIn co-founder Reid Hoffman, was announced in February. The transaction includes a few provisions to ensure longer-term collaboration, including a lock-up on founder shares for up to five years, as well as vesting provision with earnout not realized until the price per share reaches $50 — a $30 billion market cap.

SPACs are not a new instrument for going public, but they have gained a widespread presence in the transportation space, particularly amongst eVTOL startups looking to secure amounts of capital. Archer Aviation was the first developer to announce it would merge with a blank-check firm, followed by Joby, Lilium and Vertical Aerospace. But there are signs that the investment bubble may be starting to deflate: late last month, Archer cut its valuation by $1 billion in a “strategic reset” of the transaction terms with Atlas Crest Investment Corp.

Such turbulence is not uncommon in markets populated by pre-revenue companies. But despite now being a public company — and having shareholders to answer to — Sciarra said Joby’s task remains unchanged. “We can’t control the markets,” he said. “[Joby] is a company that’s been executing quietly for a very long time on things that matter. I think it’s going to be incumbent upon us to do the same as we make this transition to a public company: tell folks what we’re going to do, and then go out and do them. That, quarter by quarter, is what builds credibility, what combats skepticism, and what gives investors and frankly, the broader public, confidence that this is a company that means what it says.”

One way to frame the fate of air taxis is whether they will be more like autonomous vehicles or electric vehicles. The AV space circa five years ago was filled with companies setting ambitious expectations about when true self-driving cars would be on the roads, only to have multiple companies collapse or sell under the weight of overshot expectations.

But Sciarra suggested that a better analogy to the eVTOL industry as it currently stands is the early days of electric vehicles. He pointed out that Joby’s aircraft is designed to conform to existing safety and certification standards, with a trained pilot onboard, similar to how helicopters and planes operate today. “We didn’t want to compound the technical risk of developing a new aircraft with the technical and regulatory risk of developing full autonomy from day one.”

“We think about our approach as a little bit more Tesla versus, say, Waymo,” he added.

Powered by WPeMatico

Despite the plentiful headlines about mega billion-dollar M&A transactions, record IPOs and the rapid growth of SPACs, small deals will continue to be the most likely exit for the vast majority of tech startups. In the over 30 years I’ve worked on M&A at White & Case, Barclays and my current firm Ascento Capital, I have seen too many startups that are not prepared for an exit via a merger or sale. This article will provide specific recommendations on how to prepare your startup for M&A.

While it is good to strive for a billion-dollar-plus sale, a successful IPO or a SPAC deal, it is practical to prepare your startup for a smaller transaction.

Global M&A hit record highs in the second quarter with a total deal value of $1.5 trillion, but smaller transactions vastly outnumber mega billion-dollar deals. The U.S. saw a total of 16,672 deals in the year ended June 31, but only 583, or 3% of that number, were valued at more than a billion dollars (FactSet). The IPO market is healthy again, but M&A still represents 88% of exits: So far this year, there were 503 IPOs and 5,203 deals, according to the CB Insights Q2 2021 State of Venture Report. After the SEC announced in early April that it was considering new guidance on SPAC IPOs, the rate of new SPAC issuances fell by around 90%.

While it is good to strive for a billion-dollar-plus sale, a successful IPO or a SPAC deal, it is practical to prepare your startup for a smaller transaction.

Here are a few recommendations that will prepare your startup for an M&A exit:

Set up an alert on Google News for M&A activity in your subsector. For example, if your startup is in the IoT subsector, search for “IoT acqui” and this will pick up news stories on acquisitions in the IoT space. Save the search so you can go to Google News on a regular basis. Also track your closest competitors on Google News, particularly to see who is selling their company.

Prepare a list of the companies or firms most likely to buy your startup. This list should include domestic and international companies, businesses in non-tech industries, private equity firms and their portfolio companies, as well as VC-backed companies. Track these likely acquirers on Google News as well.

Consider approaching the top 10 likely acquirers when you are raising the next round of capital. If your startup gets M&A offers and VC term sheets at the same time, this will provide your board of directors choices on the path ahead. Knowing the M&A activity in your startup’s subsector and the 10 most likely acquirers will impress VCs and increase the chances of being funded.

Powered by WPeMatico

The SPAC parade continues in this shortened week with news that community social network Nextdoor will go public via a blank-check company. The unicorn will merge with Khosla Ventures Acquisition Co. II, taking itself public and raising capital at the same time.

Per the former startup, the transaction with the Khosla-affiliated SPAC will generate gross proceeds of around $686 million, inclusive of a $270 million private investment in public equity, or PIPE, which is being funded by a collection of capital pools, some prior Nextdoor investors (including Tiger), Nextdoor CEO Sarah Friar and Khosla Ventures itself.

Notably, Khosla is not a listed investor in the company per Crunchbase or PitchBook, indicating that even SPACs formed by venture capital firms can hunt for deals outside their parent’s portfolio.

Per a Nextdoor release, the transaction will value the company at a “pro forma equity [valuation] of approximately $4.3 billion.” That’s a great price for the firm that was most recently valued at $2.17 billion in a late 2019-era Series H worth $170 million, per PitchBook data. Those funds were invested at a flat $2 billion pre-money valuation.

So, what will public investors get the chance to buy into at the new, higher price? To answer that we’ll have to turn to the company’s SPAC investor deck.

Our general observations are that while Nextdoor’s SPAC deck does have some regular annoyances, it offers a clear-eyed look at the company’s financial performance both in historical terms and in terms of what it might accomplish in the future. Our usual mockery of SPAC charts mostly doesn’t apply. Let’s begin.

We’ll proceed through the deck in its original slide order to better understand the company’s argument for its value today, as well as its future worth.

The company kicks off with a note that it has 27 million weekly active users (neighbors, in its own parlance), and claims users in around one in three U.S. households. The argument, then, is that Nextdoor has scale.

A few slides later, Nextdoor details its mission: “To cultivate a kinder world where everyone has a neighborhood they can rely on.” While accounts like @BestOfNextdoor might make this mission statement as coherent as ExxonMobil saying that its core purpose was, say, atmospheric carbon reduction, we have to take it seriously. The company wants to bring people together. It can’t control what they do from there, as we’ve all seen. But the fact that rude people on Nextdoor is a meme stems from the same scale that the company was just crowing about.

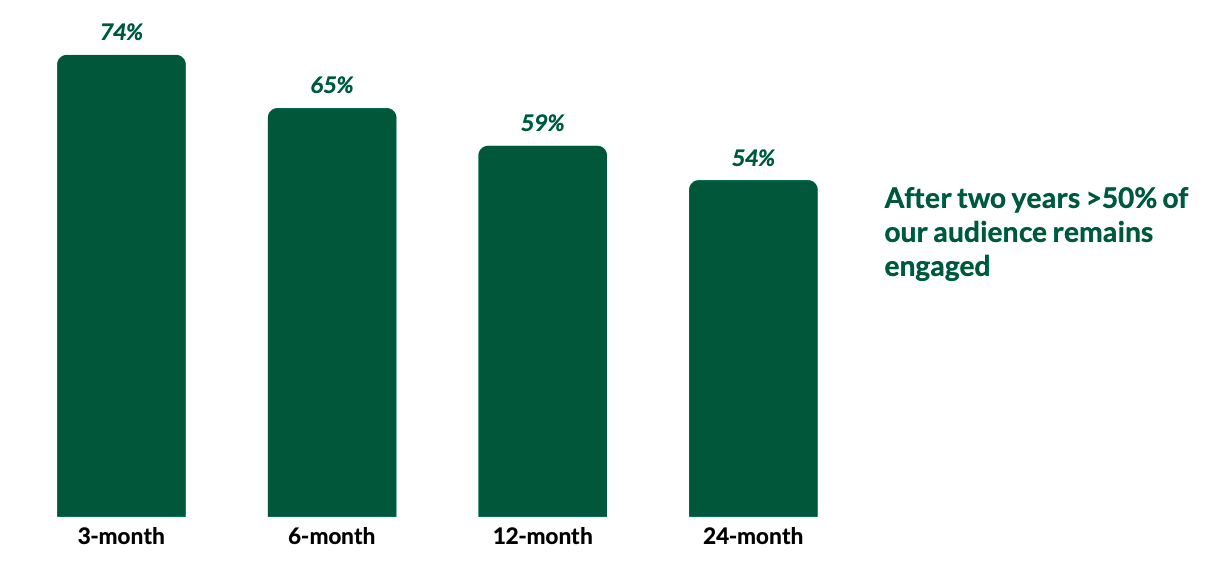

Underscoring its active user counts are Nextdoor’s retention figures. Here’s how it describes that metric:

Image Credits: Nextdoor SPAC investor deck

These are monthly active users, mind, not weekly active, the figure that the company cited up top. So, the metrics are looser here. And the company is counting users as active if they have “started a session or opened a content email over the trailing 30 days.” How conservative is that metric? We’ll leave that for you to decide.

The company’s argument for its value continues in the following slide, with Nextdoor noting that users become more active as more people use the service in a neighborhood. This feels obvious, though it is nice, we suppose, to see the company codify our expectations in data.

Nextdoor then argues that its user base is distinct from that of other social networks and that its users are about as active as those on Twitter, albeit less active than on the major U.S. social networks (Facebook, Snap, Instagram).

Why go through the exercise of sorting Nextdoor into a cabal of social networks? Well, here’s why:

Powered by WPeMatico

Five-year old self-driving truck startup Embark Trucks Inc. said Wednesday it would merge with special purpose acquisition company Northern Genesis Acquisition Corp. II in a deal valued at $5.2 billion.

Embark takes a different approach to autonomous trucking: As opposed to manufacturing and operating a fleet of trucks themselves, which is the route rival TuSimple is taking, Embark offers its AV software as a service. Carriers and fleets can pay a per-mile subscription fee to access it. The company includes carriers Mesilla Valley Transportation and Bison Transport, and companies Anheuser-Busch InBev and HP Inc., among its partners.

Carriers purchase trucks with compatible hardware directly from OEMs, so Embark says it has designed its system to be “platform agnostic” across multiple components and manufacturers. The company says its software can simulate up to 1,200, 60-second scenarios per second, and make adaptive predictions using those scenarios for the behavior of other vehicles on the road.

Embark said in an investor presentation for the SPAC deal that it was targeting “driver-out,” or operating on roads without a safety driver, by 2023 and launching at a commercial scale across the American sunbelt the following year. However, Embark still has technical milestones yet to achieve, noting in the presentation that the software still needs to accomplish actions, such as interactions with emergency vehicles and responding to blown tires and other mechanical failures.

Upon closing, the transaction will inject Embark with around $615 million in gross cash proceeds, including $200 million in private investment in public equity (PIPE) funding from investors, including CPP Investments, Knight-Swift Transportation, Mubadala Capital, Sequoia Capital and Tiger Global Management.

Embark also said former Department of Transportation Secretary Elaine Chao was joining its board, likely a boon for a company operating in the autonomous trucking industry, which is still only authorized for commercial deployment in 24 states.

Embark was founded in 2016 by CEO Alex Rodrigues and CTO Brandon Moak, who worked together on autonomous driving while completing engineering degrees from Canada’s University of Waterloo. After launching out of Y Combinator, the company quickly went on to raise $117 million in total funding, including a $30 million Series B led by Sequoia Capital and a $70 million Series C led by Tiger Global Management.

The transaction is anticipated to close in the second half of 2021. The company joins competitor AV trucking developer Plus in going public via a SPAC merger. TuSimple opted for a traditional initial public offering in March.

Powered by WPeMatico

Sohail Prasad and Samvit Ramadurgam are cofounders who met during Y Combinator’s 2012 summer batch and went on to cofound Forge, which helps accredited investors and institutions buy and sell private company shares and which most recently raised $150 million in new funding in May.

Forge — originally known as Equidate — has taken off as demand for private company shares has ballooned. The company, launched in 2014, has now raised $250 million altogether, including from, Deutsche Börse, Temasek, Wells Fargo, BNP Paribas, and Munich Re. It acquired rival SharesPost last year for $160 million in cash and stock. According to the company, it now has more than $14 billion in assets under custody.

Prasad and Ramadurgam — who helped hire Forge CEO Kelly Rodriques back in 2018 — say they’re excited about that success. They still own a stake in the company; they remain non-voting board members.

But after spending 18 months as co-president of Forge at the outset of Rodrigues’s tenure, they left early last year to begin tinkering on a new idea, one that Prasad says is centered around giving a much wider pool of people access to private company shares. Called D/XYZ (pronounced “Destiny”), the idea is to enable any investor — not just the 1% — to invest in startups whose services they use and love.

Unfortunately, the two aren’t offering much more of a curtain raiser than that right now, though Prasad suggests D/XYZ is neither a new fund nor a crowdfunding vehicle. It’s also not selling any tokens, we gather. Instead, Prasad hints at an entirely new product, saying the company is being cautious in how much it shares publicly because it first wants to “get the go-ahead from regulators, as well as to ensure we have a clear path to market,” he says.

In the meantime, the two have raised $5 million in seed funding from numerous founders who like the idea of making private company shares easier for their parents, friends, customers, partners, and everyone else who likes what they’re building. Among the round’s participants is Coinbase cofounder Fred Ehrsam; Plaid cofounder and CEO Zach Perret; Quora and Expo cofounder Charlie Cheever; Superhuman founder and CEO Rahul Vohra; and serial entrepreneur Siqi Chen, who most recently founded a finance software company called Runway.

As for some of the nascent startup’s most obvious competition, Prasad doesn’t sound concerned. Asked, for example, about Carta, a well-funded company that helps private companies and their employees manage and sell their stock and options and that has long talked about democratizing access to private company shares, Prasad says it remains very much a direct competitor instead to Forge given that both cater first and foremost to companies, not individuals.

And what of SPACs, the special purpose acquisition companies that are moving private companies onto the public market faster, allowing (at least in theory) more people to access high-growth companies at earlier stages? It’s a partial solution, says Prasad. But the way he sees it, “SPACs are more a reflection that people want late-stage access to private tech and their best option right now is giving money to a SPAC manager who will hopefully find a promising company to merge with in two years or less.” He calls them a “layer of abstraction.”

Of course, there’s also the question of whether Forge will be a friend of foe if whatever Prasad and Ramadurgam are building succeeds. Could their tech be sold back to their first company? Could Forge come to see them as a rival to its business?

“What we’re doing now is not competitive,” insists Prasad. “It’s more picking up the mantle where we left off. Forge is focused on trading, custody, company solutions and data. It has built what some call boring plumbing.” Now that the plumbing has been erected, it has “enabled a lot of other interesting things to be built, too.”

So is D/XYZ working with Forge in some capacity? Prasad demurs. “Potentially,” he says.

In other words, stay tuned.

Pictured above, left to right: Sohail Prasad and Samvit Ramadurgam.

Powered by WPeMatico

The continuing saga of Lordstown Motor’s struggles as a public company took a new turn today as the electric truck manufacturer made yet more news. Bad news.

Shares of Lordstown are down sharply today after the company reported in an SEC filing that it does not have enough capital to build and launch its electric truck. Here’s the official verbiage (formatting, bolding: TechCrunch):

Since inception, the Company has been developing its flagship vehicle, the Endurance, an electric full-size pickup truck. The Company’s ability to continue as a going concern is dependent on its ability to complete the development of its electric vehicles, obtain regulatory approval, begin commercial scale production and launch the sale of such vehicles.

The Company believes that its current level of cash and cash equivalents are not sufficient to fund commercial scale production and the launch of sale of such vehicles. These conditions raise substantial doubt regarding our ability to continue as a going concern for a period of at least one year from the date of issuance of these unaudited condensed consolidated financial statements.

Now, companies that are trying to invent the future are more risky than, say, established banking concerns that are generating stable GAAP net income. I’m sure that SpaceX looked dicey at times when it was busy crashing rockets on its way to learning how to land them on drone ships.

But in the case of Lordstown’s admission that it cannot “fund commercial scale production and the launch of sale” of its Endurance pickup are fucking galling.

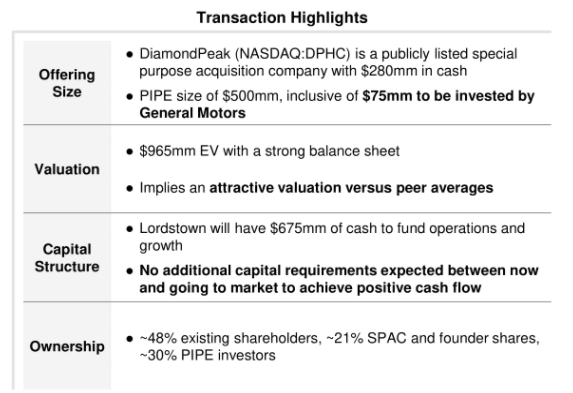

Why? Because when the company pitched its SPAC-led combination and public debut, it was pretty freaking confident that it would have enough cash to do so.

Don’t take my word for it. Here’s an excerpt from Lordstown’s investor deck:

You will note in the “Capital Structure” section that the company claimed that it would not need more funding to go to market.

Now Lordstown is pretty sure it’s going to need more money. If it’s putting the possible need in a filing, it means it.

Here’s what the company may do to solve its problems (formatting, bolding: TechCrunch):

To alleviate these conditions, management is currently evaluating various funding alternatives and may seek to raise additional funds through the issuance of equity, mezzanine or debt securities, through arrangements with strategic partners or through obtaining credit from government or financial institutions.

As we seek additional sources of financing, there can be no assurance that such financing would be available to us on favorable terms or at all. Our ability to obtain additional financing in the debt and equity capital markets is subject to several factors, including market and economic conditions, our performance and investor sentiment with respect to us and our industry.

In other words, the company is going to have to lever itself using debt, or dilute existing shareholders through the sale of equity, and Lordstown can’t promise that it will be able to do either “on favorable terms or at all.”

What we’re seeing here is the difference between SEC filings, which are no-bullshit zones, and SPAC decks, which are business propaganda. Shares of Lordstown fell more than 16% during regular trading, and another 6.9% in after-hours trading, as of the time of writing.

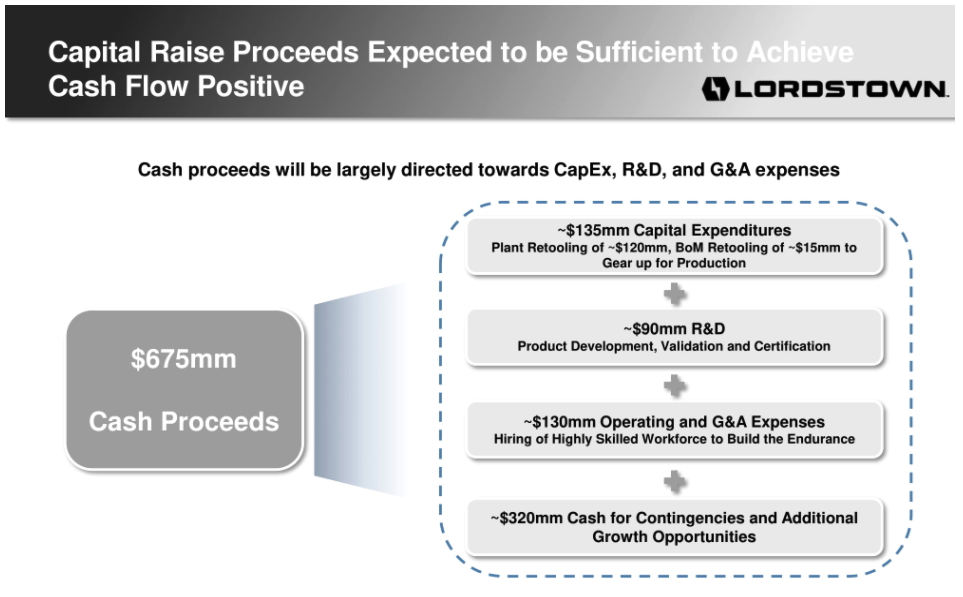

This mess from the company that put out this diagram in its investor deck:

In separate news, TechCrunch received an invite to a media availability to visit Lordstown’s operations in May, which included a note that the company “look[s] forward to opening [its] doors and showing you the latest progress from Lordstown Motors as [it] prepare[s] for the beginning of production in late September.” In a new missive sent today concerning the same event, the production timeline was not present.

So, yeah, maybe don’t trust SPAC decks much, if at all.

Powered by WPeMatico