SPAC

Auto Added by WPeMatico

Auto Added by WPeMatico

Tech stocks are getting hammered today, with previously high-flying shares of software companies taking even more damage.

For a sector that has enjoyed a year in the sun, recent trading sessions have punctured a period of market adoration. It is too soon to say that the market is repricing tech stocks, but the selloff has reached the point of materiality and is therefore something we need to note.

As we write, the tech-heavy Nasdaq Composite is off another 1.2% today after previous declines. The now-infamous ARK Innovation ETF is off 6.5% and the list of individual declines worth noting in the tech sector is very long indeed.

The change in sentiment is clear in recent results. Here’s the tech-heavy Nasdaq Composite:

And the damage intensifies if we consider just SaaS and cloud stocks. Here’s the Bessemer cloud index:

In more prosaic terms, the Nasdaq is in a technical correction, while SaaS stocks have reached bear-market territory. That’s quite a turnabout from recent all-time highs for both.

Lost on the TechCrunch editing floor from late yesterday is a post we wrote noting the sharp declines in the value of insurtech stocks ahead of the impending public debut of Hippo, another neo-insurance company. The SPAC-led Hippo flotation will not touch down in a warm market. Instead, its contemporaries look like this today:

The damage is widespread. Hell, recent IPO success-story Snowflake announced yesterday that it grew from revenues of $88 million in its year-ago quarter to $190 million in its most recent. And its stock is off more than 7% today.

We’ll leave it to you whether the changing public valuations are just a blip or a more staid change in the winds. But it does feel different out there.

For startups, this is all somewhat poor news. Valuations for public comps were strong in 2020. To lose that halo in 2021 could crimp late-stage valuations, perhaps even reaching back to Series A and B rounds to limit some upside for growing upstarts. But such an impact will lag the public markets, so don’t expect things to change quite yet.

Still, every private investor has their eye on the exit when it comes to their deals. And if that exit is suddenly shrinking, so too might their interest in paying for quite so great a markup on their next deal.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion.

Powered by WPeMatico

Real estate tech startup Doma, formerly known as States Title, announced Tuesday it will go public through a merger with SPAC Capitol Investment Corp. V in a deal valued at $3 billion, including debt.

SPACs, often called blank-check companies, are increasingly common. They exist as publicly traded entities in search of a private company to combine with, taking the private entity public without the hassle of an IPO.

When it floats later this year, Doma will trade on the New York Stock Exchange under the ticker symbol DOMA. The transaction is expected to provide up to $645 million in cash proceeds, including a fully committed PIPE of $300 million and up to $345 million of cash held in the trust account of Capitol Investment Corp. V.

CEO Max Simkoff founded San Francisco-based Doma in September 2016 with the aim of creating a technology-driven solution for “closing mortgages instantly.” While it initially was founded to instantly underwrite title insurance, the company has expanded that same approach to handle “every aspect” of closing and escrow.

Doma has developed patented machine learning technology that it says reduces title processing time from five days to “as little as one minute” and cuts down the entire mortgage closing process “from a 50+ day ordeal to less than a week.” The startup has facilitated over 800,000 real estate closings for lenders such as Chase, Homepoint, Sierra Pacific Mortgage and others.

The name change is designed to more accurately reflect its intention to expand “well beyond” title into areas such as appraisals and home warranties.

Its goal with going public is to be able to “continue to invest in growth, market expansion and new products.”

Anchoring the PIPE include funds and accounts managed by BlackRock, Fidelity Management & Research Company LLC, SB Management (a subsidiary of SoftBank Group), Gores, Hedosophia, and Wells Capital. Existing Doma shareholder Lennar has also committed to the PIPE and Spencer Rascoff, co-founder and former CEO of Zillow Group, has committed a personal investment to the PIPE.

Up to approximately $510 million of cash proceeds are expected to be retained by Doma, and existing Doma shareholders will own no less than approximately 80 percent of the equity of the new combined company, subject to redemptions by the public stockholders of Capitol and payment of transaction expenses.

In mid-February, Doma announced it had closed on $150 million in debt financing from HSCM Bermuda, which had previously invested in the company. And last May, it announced a massive $123 million Series C round of funding at a valuation of $623 million.

The company posted modest growth from 2019 to 2020, seeing its GAAP revenues rise from $358.1 million to $409.8 million. After removing premiums paid to agents, its revenues (“retained premiums and fees”) decreased to $179.8 million in 2019 and $189.7 million in 2020. (For this section we’re leaning on the reported 2020 numbers that are caveated with an “estimated” tag. As it is March, we expect the final 2020 numbers to come in close enough to what was reported as to make us comfortable citing them.)

In 2021 the company also anticipates modest growth, with GAAP revenues estimated at $416.4 million, and its retained revenue figure landing at $226.4 million. More expansive growth is anticipated and sketched out for 2022 and 2023, though as those figures are far in the future we can discount them for now.

Doma also expects its economics to worsen in 2021, with its adjusted gross profit as a percentage of its retained premiums and fees falling from 48.3% last year to 39.5% this year. Of course we’re so far off the GAAP ranch with that metric as to be lost, but it’s worth noting what the company is telling the street about its impending financial performance.

Other metrics are also pointed in a negative direction, with Doma expecting its adjusted EBITDA to fall from -$19.0 million to -$66.6 million in 2021. The company does predict a rosy 2023 adjusted EBITDA number, for whatever stock you want to put in that.

Without discounting costs, Doma’s 2020 net loss of $35.1 million is expected to expand to $103.1 million this year. Still, as with many entities pursuing a public debut via a SPAC, Doma is debuting while it is still sorting out elements of its business as the pandemic starts to diminish in light of increasingly readily available vaccines. It certainly has high hopes for its future.

Doma joins the growing number of proptech companies going the public route. On Monday, Compass, the real-estate brokerage startup backed by roughly $1.6 billion in venture funding, filed its S-1.

In 2020, Social Capital Hedosophia II, the blank-check company associated with investor Chamath Palihapitiya, announced that it would merge with Opendoor, taking the private real estate startup public in the process.

Porch.com also went public in a SPAC deal in December. And, SoftBank-backed View, a Silicon Valley-based smart window company, will complete a recent SPAC merger to be publicly listed on the NASDAQ stock exchange on March 9. The company is expected to debut trading with a market value of $1.6 billion.

Powered by WPeMatico

Since last year, we’ve been tracking the growing list of capitalists who got into the SPAC game. You can read an interview we conducted with Amish Jani, the co-founder of FirstMark Capital, about his SPAC here. And if you need a refresher on all things SPAC, we have that for you as well.

This morning, I want to better understand the trend by parsing a few new venture capitalist SPACs. We’ll examine Lerer Hippeau Acquisition Corp. and Khosla Ventures Acquisition Co. I, II and III. The SPACs are, somewhat obviously, associated with New York-based Lerer Hippeau and Menlo Park’s Khosla Ventures. And all four dropped formal S-1 filings last week.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Today’s topic may sound dry, but it really does matter. As we’ve reported, Lux Capital is in on the SPAC wager, along with Ribbit and, of course, SoftBank. Adding our latest names to the mix and you have to wonder if every VC worth a damn in the future will have their own raft of SPAC offerings.

In that way, as some late-stage venture capital funds invest earlier — and now later — full-service VC outfits will offer first check to final liquidity, will such a full-stack venture outfit be able to win more deals than a group offering a limited set of financing options? If so, the recent venture capital SPAC wave could become more of a rising tide in time, to torture a metaphor.

In that way, as some late-stage venture capital funds invest earlier — and now later — full-service VC outfits will offer first check to final liquidity, will such a full-stack venture outfit be able to win more deals than a group offering a limited set of financing options? If so, the recent venture capital SPAC wave could become more of a rising tide in time, to torture a metaphor.

Regardless, let’s quickly parse what Khosla and Lerer Hippeau are telling public investors about why they will be great SPACers before working our way backward to what the resulting pitch must be to startups themselves.

The Lerer Hippeau SPAC is the most interesting of the two firms’ combined four offerings, so we’ll start there. That isn’t to diss Khosla, but the Lerer Hippeau blank check has some explicit wording I want to highlight.

From the Lerer Hippeau Acquisition Corp. S-1 filing, read the following (bolding: TechCrunch):

As our seed portfolio matured over the last decade, we added a growth strategy to our platform through our select funds. This capital enables us to continue providing financial support to our top performing early-stage companies as they scale, and to selectively make new investments in later-stage companies in the Lerer Hippeau network. With our portfolio now maturing to the stage at which many are considering the public markets, we view SPACs as a natural next step in the evolution of our platform.

After writing that it has had four portfolio companies “publicly announced business combination agreements with SPACs” and noting that it expects more of the same, Lerer Hippeau added that it considers its “expansion into the SPAC market as a highly complementary element of our strategy to support founders throughout their entrepreneurial journeys.”

Powered by WPeMatico

Micromobility startup Helbiz, which now operates across Europe and the USA, is merging with a special purpose acquisition company (SPAC) to become a publicly listed company, giving it a war chest to potentially roll-up smaller competitors in the space, as well as the resources to expand into “cloud” or “ghost” kitchens as part of a move into food delivery.

Helbiz intends to merge with GreenVision Acquisition Corp. (Nasdaq: GRNV) in the second quarter of 2021. The combined entity will be named Helbiz Inc. and will be listed on the Nasdaq Capital Market under the new ticker symbol, “HLBZ.”

The transaction includes $30 million PIPE anchored by institutional investors and approximately $80 million in net proceeds will be fed into Helbiz’s micromobility and advertising businesses, which have 2.7 million users.

Helbiz says the merged entity will have a valuation of $408 million, and by run Helbiz’s existing management under CEO Salvatore Palella.

Palella said: “Through this transaction, we’re committed to fulfilling our vision in revolutionizing transport by using micromobility to become a seamless last-mile solution.”

He further revealed to me that the company plans to establish “ghost kitchens” in Milan and Washington, DC later this year, with the aim of introducing a five-minute delivery time.

Helbiz has tried to differentiate itself from other players like Lime and Bird by offering e-scooters, e-bicycles and e-mopeds all on one platform.

Key to Helbiz’s offering is an integrated geofencing platform that tends to appeal to city authorities who don’t want scooters left in random places, as well as a swappable battery that enables easier charging of the devices. Its subscription service allows users to take unlimited 30-minute trips on its e-bikes and e-scooters every month.

In Europe the company currently operates a fleet of e-scooters and e-bicycles in Milan, Turin, Verona, Rome, Madrid and Belgrade, and in the U.S. it operates in Washington, DC, Alexandria, Arlington and Miami.

David Fu, chairman, and CEO of GreenVision, commented: “Helbiz has distinguished itself as the only company to offer e-scooters, e-bicycles, and e-mopeds all on one user-friendly platform… Helbiz has a proven and capital-light business model that combines hardware, software, and services with extensive customer relationships.”

Powered by WPeMatico

This week, Latch becomes the latest company to join the SPAC parade. Founded in 2014, the New York-based company came out of stealth two years later, launching a smart lock system. Though, like many companies primarily known for hardware solutions, Latch says it’s more, offering a connected security software platform for owners of apartment buildings.

The company is set to go public courtesy of a merger with blank check company TS Innovation Acquisitions Corp. As far as partners go, Tishman Speyer Properties makes strategic sense here. The New York-based commercial real estate firm is a logical partner for a company whose technology is currently deployed exclusively in residential apartment buildings.

“With a standard IPO, you have all of the banks take you out to all of the big investors,” Latch founder and CEO Luke Schoenfelder tells TechCrunch. “We felt like there was an opportunity here to have an extra level of strategic partnership and an extra level of product expansion that came as part of the process. Our ability to go into Europe and commercial offices is now accelerated meaningfully because of this partnership.

The number of SPAC deals has increased substantially over the past several months, including recent examples like Taboola. According to Crunchbase, Latch has raised $152 million, to date. And the company has seen solid growth over the past year — not something every hardware or hardware adjacent company can say about the pandemic.

As my colleague Alex noted on Extra Crunch today, “Doing some quick match, Latch grew booked revenues 50.5% from 2019 to 2020. Its booked software revenues grew 37.1%, while its booked hardware top line expanded over 70% during the same period.”

“We’ve been a customer and investor in Latch for years,” Tishman Speyer President and CEO Rob Speyer tells TechCrunch. “Our customers — the people who live in our buildings — love the Latch product. So we’ve rolled it out across our residential portfolio […] I hope we can act as both a thought partner and product incubator for them.”

While the company plans to expand to commercial offices, apartment buildings have been a nice vertical thus far — meaning the company doesn’t have to compete as directly in the crowded smart home lock category. Among other things, it’s probably a net positive if you’re going head to head against, say Amazon. That the company has built in partners in real estate firms like Tishman Speyer is also a net positive.

Schoenfelder says the company is looking toward such partnerships as test beds for its technology. “Our products have been in the field for many years in multifamily. The usage patterns are going to be slightly different in commercial offices. We think we know how they’re going to be different, but being able to get them up and running and observe the interaction with products in the wild is going to be really important.”

The deal values Latch at $1.56 billion and is expected to close in Q2.

Powered by WPeMatico

This morning, investor and SPAC raconteur Chamath Palihapitiya announced two new blank-check deals involving Latch and Sunlight Financial.

Latch, an enterprise SaaS company that makes keyless-entry systems, has raised $152 million in private capital, according to Crunchbase. Sunlight Financial, which offers point-of-sale financing for residential solar systems, has raised north of $700 million in venture capital, private equity and debt.

We’re going to chat about the two transactions.

There’s no escaping SPACs for a bit, so if you are tired of watching blind pools rip private companies into the public markets, you are not going to have a very good next few months. Why? There are nearly 300 SPACs in the market today looking for deals, and many will find one.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

Think of SPACs are increasingly hungry sharks. As a shark get hungrier while the clock winds down on its deal-making window, it may get less choosy about what it eats (take public). There are enough SPACs on the hunt today that they would be noisy even if they were not time-constrained investment vehicles. But as their timers tick, expect their deal-making to get all the more creative.

This brings us back to Chamath’s two deals. Are they more like the Bakkt SPAC, which led us to raise a few questions? Or more akin to the Talkspace SPAC, which we found pretty reasonable? Let’s find out.

Let’s start with the Latch deal.

New York-based Latch sells “LatchOS,” a hardware and software system that works in buildings where access and amenities matter. Latch’s hardware works with doors, sensors and internet connectivity.

The company has raised a number of private rounds, including a $126 million deal in August of 2019 that valued the company at $454.3 million on a post-money basis, according to PitchBook data. The company raised another $30 million in October of 2020, though its final private valuation is not known.

As Chamath tweeted this morning, Latch is merging with TS Innovation Acquisitions Corp, or $TSIA. The SPAC is associated with Tishman Speyer, a commercial real estate investor. You can see the synergies, as Latch’s products fit into the commercial real estate space.

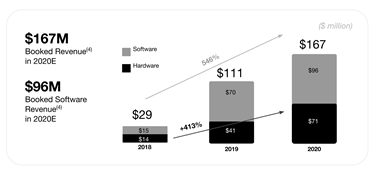

Up front, Latch is not a company that is only reporting future revenues. It has a history as an operating entity. Indeed, here’s its financial data per its investor presentation:

Image Credits: Latch

Doing some quick match, Latch grew booked revenues 50.5% from 2019 to 2020. Its booked software revenues grew 37.1%, while its booked hardware top line expanded over 70% during the same period.

That could be due to strong hardware installation fees, which could later result in software revenues; the company claims an average of a six-year software deal, so hardware revenues that are attached to new software incomes could low key declaim long-term SaaS revenues.

Update: Adding some clarity here, the above are “booked” revenues, which I’ve made more clear, not actual revenues. Its net revenues, better known as actual revenues, were $18 million, with $14 million of that coming from hardware. So, today, the company is certainly more hardware-heavy than I first thought. Damn non-S-1 filings!

While some were quick to note that the company is far from pure-SaaS — correct — I suspect that the model that could get some traction amongst investors is that this feels a bit like Peloton for real estate. How so? Peloton has large hardware incomes up front from new users, which convert to long-term subscription revenues. Latch may prove similar, albeit for a different customer base and market.

Per the deal’s reported terms, Latch will be worth $1.56 billion after the transaction. The combined entity will have $510 million in cash, including $190 million from a PIPE — a method of putting private money into a public entity — from “BlackRock, D1 Capital Partners, Durable Capital Partners LP, Fidelity Management & Research Company LLC, Chamath Palihapitiya, The Spruce House Partnership, Wellington Management, ArrowMark Partners, Avenir and Lux Capital.”

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast where we unpack the numbers behind the headlines.

This is Equity Monday, our weekly kickoff that tracks the latest private market news, talks about the coming week, digs into some recent funding rounds and mulls over a larger theme or narrative from the private markets. You can follow the show on Twitter here and myself here — and make sure to check out last week’s main ep, which was super-packed and a real treat.

This morning the news was heavy, so here’s your rundown to get you into the show:

Hugs, and we are back Thursday, if not before. Stay safe!

Equity drops every Monday at 7:00 a.m. PST and Thursday afternoon as fast as we can get it out, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Hims & Hers, a San Francisco-based telehealth startup that sells sexual wellness and other health products and services to millennials, began trading publicly today on the NYSE after completing a reverse merger with the blank-check company Oaktree Acquisition Corp.

Its shares slipped a bit, ending the day down 5% from where they started, but the company, which was founded in 2017 and now claims nearly 300,000 paying subscribers for its various offerings, has never been focused on a splashy headline about its first-day performance, co-founder and CEO Andrew Dudum told us earlier today.

On the contrary, Dudum says that while Hims might have once imagined a traditional IPO, it decided to go the special purpose acquisition company (SPAC) route because of their pricing mechanisms and because it was approached by a SPAC led by renowned money manager Howard Marks, the founder of the global alternative investment firm Oaktree Capital Management. (“We fell in love with the Oaktree team and the capital market experience and deep resources they have.”)

We talked with Dudum about that SPAC’s structure; the lockups involved now that Hims’ shares are trading; and how much of the business still centers around one of its first offerings, which was a generic version of erectile dysfunction pills. Our conversation has been edited lightly for length and clarity.

TC: You’re a Bay Area-based company selling to a mostly U.S. audience. How are you thinking about expanding that footprint geographically?

AD: We do have a small operation selling in the U.K.; we’re getting our feet wet in that market and building out a team and infrastructure and fulfillment. If you look at the regulatory landscape, there’s a huge amount of room [to grow] in Europe, Australia, Canada, the Middle East and Asia, and so in that order, we’ll start to [move into those markets].

TC: What is your average customer cost?

AD: It has come down from $200 when we first launched, to roughly $100 last year, and we make, on average, close to $300 in the first couple of years in terms of a patient’s lifetime value.

TC: How quickly do customers churn?

AD: We break down lifetime value projections by quarter cohorts, and quarter over quarter, year over year, we’re monetizing each of these cohorts better, with high-margin profiles.

As of last quarter, the business was growing 90% year-over-year, with 76% gross margins and greater cash efficiency, and that’s because as we provide more offerings, there is more cross-purchasing. Also, word of mouth is becoming more of a dynamic, with more than 50% of the traffic to the site free at this point because we have built a brand with a young demographic.

TC: When are you projecting that you’ll turn profitable?

AD: We’ve reduced our annual burn and increased our margin efficiency and organic growth, so on a quarterly basis, we think in the next couple of years is a real possibility.

Image Credits: Hims & Hers

TC: Hims’ first wellness offerings included pills for male pattern hair loss and erectile dysfunction. How much revenue does that ED business account for?

AD: What we’ve disclosed is that roughly half [of our revenue] is that sexual health category — which includes [medicines for] generic erectile dysfunction, birth control, STDs, UTIs and premature ejaculation. The other half is predominately dermatology, including hair care [to address hair loss] and acne, and we’ve more recently moved into primary care and behavioral health.

TC: For retail investors, how do you differentiate the business from that of your rival Ro, which heavily promotes its ED products?

AD: There are a number of core differences between us and public and private players. First is our real focus on diversifying our offerings. With our focus on sexual health, dermatology, primary care and behavioral health, it’s in our DNA to quickly expand into new businesses.

We also think we’re different from most [rivals] in that we really invest time in building deep relationships with [those who represent] the future of healthcare markets — people in their teens, 20s and 30s. This demographic has a different set of tech expectations and consumer expectations than people in their 40s, 50s and 60s, and if we want to build for the future, that means building for the largest body of payers in the future.

Traditional healthcare companies monetize only the sick, but optimizing around that demographic precludes you from understanding what the next generation really needs and wants. I’ve never seen such a divergence between a patient population and legacy experience, and that’s a real advantage to us as a business.

TC: Hims just went public through a SPAC in a deal that gives the company around $280 million in cash — $205 million of that from Oaktree’s blank-check company and another $75 million through a private placement deal. How much runway does that give you?

AD: The company doesn’t burn a tremendous amount — between $10 million and $20 million a year — so a relatively long runway if we keep operating the business as is. But it does allow us to expand and grow into new businesses, too, including into big categories like sleep, infertility, diabetes and other chronic conditions.

TC: What about acquisitions?

AD: We’ll keep an eye open for strategic opportunities and consolidation opportunities. More than a dozen businesses a month come to us to be consolidated into the brand, but generally speaking, we’ve had the belief that so much is in front of us that we don’t want to be distracted.

TC: Is there a lockup period for anyone?

AD: There’s a traditional lockup for executives and employees and the board.

TC: Did your SPAC sponsors get a board seat?

AD: No.

TC: How much do they now own of the company, and can they sell?

AD: Oaktree owns a couple percent and [the syndicate they brought to do the private placement] [owns] 12%. But the very reason we went with them was the quality of the team and the organization . . . and they have the added incentive for the next year or two from a compensation standpoint for the company to succeed and to prove [out their thesis that Hims is a smart investment].

TC: Do you think the traditional IPO process is broken?

AD: The traditional IPO market hasn’t changed. It takes 12 to 18 months of preparation, which is a crazy amount of time for management to be distracted, then there’s this one-day PIPE that gives institutions a tremendous amount of money instantaneously. Maybe it makes for a good CNBC headline, but at tremendous cost to the company. It’s atrocious. If you were a founder or employee and getting diluted twice as much as you have to be, you’d be really upset. It’s no surprise to me that founders like myself are looking at other modalities with better pricing and better structures.

Powered by WPeMatico

Group Nine Media — which owns Thrillist, NowThis, The Dodo, Seeker and PopSugar — is the latest company to form a SPAC, according to a filing with the SEC.

These blank-check corporations, as they’re also known, have become a popular way to raise money from the public markets. The filing says that Group Nine is creating a SPAC “for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination.”

The company goes on to claim that it doesn’t have any specific acquisition targets in mind, and that there have not been “any substantive discussions.” But it says it’s interested in digital media companies, as well as those in “adjacent industries” such as social media, e-commerce, events, digital publishing and marketing.

The idea of consolidating digital media properties has been a recurring theme from executives over the past few years. BuzzFeed CEO Jonah Peretti, for example, has said that a consolidated digital media entity could have more clout in negotiations with Facebook and Google, and he recently struck a deal to acquire HuffPost from Verizon Media (which also owns TechCrunch).

Group Nine is itself a roll-up of previously independent digital media companies, led by CEO Ben Lerer (pictured above) and growing last year with the acquisition of PopSugar. The Wall Street Journal reported recently that the company was exploring a SPAC.

“We believe the digital media sector is primed for consolidation, as digital media companies need a scaled platform with efficient portfolio infrastructure to compete in the ecosystem and return value to shareholders in the long-term,” Group Nine says in the filing.

Powered by WPeMatico

Jason Green has a pretty solid reputation as venture capitalists go. The enterprise-focused firm he co-founded 17 years ago, Emergence Capital, has backed Saleforce, Box and Zoom, among many other companies, and even while every firm is now investing in software-as-a-service startups, his remains a go-to for many top founders selling business products and services.

To learn more about the trends impacting Green’s slice of the investing universe, we talked with him late last week about everything from SPACs to valuations to how the firm differentiates itself from the many rivals with which it’s now competing. Below are some outtakes edited lightly for length.

TC: What do you make of the assessment that SPACs are for companies that aren’t generating enough revenue to go public the traditional route?

JG: Well, yeah, it’ll be really interesting. This has been quite a year for SPACs, right? I can’t remember the number, but it’s been something like $50 billion of capital raised this year in SPACs, and all of those have to put that money to work within the next 12 to 18 months or they give it back. So there’s this incredible pent-up demand to find opportunities for those SPACs to convert into companies. And the companies that are at the top of the charts, the ones that are the high-growth and profitable companies, will probably do a traditional IPO, I would imagine.

So [SPAC candidates are] going to be companies that are growing fast enough to be attractive as a potential public company but not top of the charts. So I do think [sponsors are] going to target companies that are probably either growing slightly slower than the top-quartile public companies but slightly profitable, or companies that are growing faster but still burning a lot of cash and might actually scare all the traditional IPO investors.

TC: Are you having conversations with CEOs about whether or not they should pursue this avenue?

JG: We just started having those conversations now. There are several companies in the portfolio that will probably be public companies in the next year or two, so it’s definitely an alternative to consider. I would say there’s nothing impending I see in the portfolio. With most entrepreneurs, there’s a little bit of this dream of going public the traditional way, where SPACs tend to be a little bit less exciting from that perspective. So for a company that maybe is thinking about another private round before going public, it’s like a private-plus round. I would say it’s a tweener, so the companies that are considering it are probably ones that are not quite ready to go public yet.

TC: A lot of the SPAC fundraising has seemed like a reaction to uncertainty around when the public window might close. With the election behind us, do you think there’s less uncertainty?

JG: I don’t think risk and uncertainty has decreased since the election. There’s still uncertainty right now politically. The pandemic has reemerged in a significant way, even though we have some really good announcements recently regarding vaccines or potential vaccines. So there’s just a lot of potential directions things could head in.

It’s an environment generally where the public markets tend to gravitate more toward higher-quality opportunities, so fewer companies but higher quality, and that’s where I think SPACs could play a role. I’d say first half of next year, I could easily see SPACs being the more likely go-to-market for a public company, then the latter half of next year, once the vaccines have kicked in and people feel like we’re returning to somewhat normal, I could see the traditional IPO coming back.

TC: When we sat down in person about a year ago, you said Emergence looks at maybe 1,000 deals a year, does deep due diligence on 25 and funds just a handful or so of these startups every year. How has that changed in 2020?

JG: I would say that over the last five years, we’ve made almost a total transition. Now we’re very much a data-driven, thesis-driven outbound firm, where we’re reaching out to entrepreneurs soon after they’ve started their companies or gotten seed financing. The last three investments that we made were all relationships that [date back] a year to 18 months before we started engaging in the actual financing process with them. I think that’s what’s required to build a relationship and the conviction, because financings are happening so fast.

I think we’re going to actually do more investments this year than we maybe have ever done in the history of the firm, which is amazing to me [considering] COVID. I think we’ve really honed our ability to build this pipeline and have conviction, and then in this market environment, Zoom is actually helping expand the landscape that we’re willing to invest in. We’re probably seeing 50% to 100% more companies and trying to whittle them down over time and really focus on the 20 to 25 that we want to dig deep on as a team.

TC: For founders trying to understand your thinking, what’s interesting to you right now?

JG: We tend to focus on three major themes at any one time as a firm, and one we’ve termed ‘coaching networks.’ This is this intersection between AI and machine learning and human interaction. Companies like [the sales engagement platform] SalesLoft or [the knowledge management system] Guru or Drishti [which sells video analytics for manual factory assembly lines] fall into this category, where it’s really intelligent software going deep into a specific functional area and unleashing data in a way that’s never been available before.

The second [theme] is going deep into more specific industry verticals. Veeva was the best example of this early on with with healthcare and life sciences, but we now have one called p44 in the transportation space that’s doing incredibly well. Doximity is in the healthcare space and going deep like a LinkedIn for physicians, with some remote health capabilities, as well. And then [lending company] Blend, which is in the financial services area. These companies are taking cloud software and just going deep into the most important problems of their industries.

The third of them [centers around] remote work. Zoom, which has obviously has been [among our] best investments is almost as a platform, just like Salesforce became a platform after many years. We just funded a company called ClassEDU, which is a Zoom-specific offering for the education market. Snowflake is becoming a platform. So another opportunity is is not just trying to come up with another collaboration tool, but really going deep into a specific use case or vertical.

TC: What’s a company you’ve missed in recent years and were any lessons learned?

JG: We have our hall of shame. [Laughs.] I do think it’s dangerous to assume that things would have turned out the same if if we had been investors in the company. I believe the kinds of investors you put around the table make a difference in terms of the outcome of your company, so I try to not beat myself up too much on the missed opportunities because maybe they found a better fit or a better investor for them to be successful.

But Rob Bernshteyn of Coupa is one where I knew Rob from SuccessFactors [where he was a product marketing VP], and I just always respected and liked him. And we were always chasing it on valuation. And I think I think we probably turned it down at an $80 million or $100 million valuation [and it’s valued at] $20 billion today. That can keep you up at night.

Sometimes, in the moment, there are some risks and concerns about the business and there are other people who are willing to be more aggressive and so you lose out on some of those opportunities. The beautiful thing about our business is that it’s not a zero-sum game.

Powered by WPeMatico