Software

Auto Added by WPeMatico

Auto Added by WPeMatico

A new voice-based social app that cites Clubhouse as its biggest inspiration offers a playful new way to stay in touch with close friends and family. Zebra leaves video out of the equation altogether, inviting users to snap on-the-fly photos and send them off paired with casual voice updates.

Zebra focuses on asynchronous sharing, but it also lets users call one another if they’re both already hanging out on the app. The result is a fun and casual way to stay in touch for anyone who doesn’t feel like accidentally getting sucked into Instagram’s endless, ad-strewn feed every time they want to give a friend a quick update.

For now Zebra is a two-person team consisting of CEO Dennis Gecaj, a product designer based in Berlin, and Amer Shahnawaz, Zebra’s head of engineering, who previously worked on Snap Maps at Snapchat. The pre-seed funding was led by Alexis Ohanian’s fresh early-stage venture firm Seven Seven Six, which the Reddit co-founder announced in June. The app will launch formally in August but is now open for preorders through the App Store and as a beta in TestFlight.

“It’s no secret that we are in the midst of an audio revolution, one that has ushered in a series of new audio-first social platforms and content vehicles,” Ohanian said, noting that Zebra’s unique blend of photos and voice is what caught his eye.

Gecaj sees voice-based social networking as a much richer alternative to text-dominant platforms. While products like Instagram allow voice messages and technically let users make voice calls by disabling the camera, voice usually plays second fiddle to video. But video calls are more taxing and require more commitment — it’s no coincidence more and more Zoom cameras blinked offline as the pandemic dragged on.

Unlike Clubhouse, which Gecaj calls a “huge inspiration, Zebra is social audio designed for your inner circle. “With everything opening back up we saw an incredible opportunity for an asynchronous format for that,” he told TechCrunch.

Gecaj hopes that Zebra’s “talking photos” can capture the collective imagination in a way that makes early growth natural. Anyone who downloads Zebra can invite friends individually without needing to share their full contact list (and they’ll need to — you can’t do anything on the app without friends). Because Zebra’s interface is so clean and streamlined, this process is painless and doesn’t necessitate any extra digging through menus.

The idea of a “zebra” — naturally, Zebra is trying to make “zebra” happen — is that people like to see what they are talking about. On a different messaging app, this would require sending a photo and then sending a voice message in quick succession. But on Zebra, sending a photo is the main thing you can do. The app opens right to the camera where you snap a picture. You then hold the photo to record a snippet of voice to go along with it and send it off to friends and family, who appear in a row beneath the camera.

Zebra isn’t worried about the prospect of talking people into downloading another app. Gecaj sees a natural split emerging as creators and audiences increasingly become the focus of social platforms that were initially designed to help friends stay in touch.

“I think the trend is a division between creator platforms where you go to be entertained and platforms you go to hang out with your friends,” Gecaj told TechCrunch.

On top of that, he hopes that Zebra’s dual focus on voice and photos, two aspects of social networking that platforms either don’t prioritize or are actively abandoning, can make it appealing for people who aren’t as interested in video.

“We really also think that text messaging doesn’t have the same emotion as voice… and voice has been really neglected,” Gecaj said. “There’s really a richness to voice, a power to voice that nothing else has.”

Powered by WPeMatico

Mortgages may not be considered sexy, but they are a big business.

If you’ve refinanced or purchased a home digitally lately, you may not have noticed the company powering the software behind it — but there’s a good chance that company is Blend.

Founded in 2012, the startup has steadily grown to be a leader in the mortgage tech industry. Blend’s white label technology powers mortgage applications on the site of banks including Wells Fargo and U.S. Bank, for example, with the goal of making the process faster, simpler and more transparent.

The San Francisco-based startup’s SaaS (software-as-a-service) platform currently processes over $5 billion in mortgages and consumer loans per day, up from nearly $3 billion last July.

Today, Blend made its debut as a publicly traded company on the New York Stock Exchange, trading under the symbol “BLND.” As of early afternoon, Eastern Time, the stock was trading up over 13% at $20.36.

On Thursday night, the company had said it would offer 20 million shares at a price of $18 per share, indicating the company was targeting a valuation of $3.6 billion.

That compares to a $3.3 billion valuation at the time of its last raise in January — a $300 million Series G funding round that included participation from Coatue and Tiger Global Management. Also, let’s not forget that Blend only became a unicorn last August when it raised a $75 million Series F. Over its lifetime, Blend had raised $665 million before Friday’s public market debut.

In filing its S-1 on June 21, Blend revealed that its revenue had climbed to $96 million in 2020 from $50.7 million in 2019. Meanwhile, its net loss narrowed from $81.5 million in 2019 to $74.6 million in 2020.

In 2020, the San Francisco-based startup significantly expanded its digital consumer lending platform. With that expansion, Blend began offering its lender customers new configuration capabilities so that they could launch any consumer banking product “in days rather than months.”

Looking ahead, the company had said it expects its revenue growth rate “to decline in future periods.” It also doesn’t envision achieving profitability anytime soon as it continues to focus on growth. Blend also revealed that in 2020, its top five customers accounted for 34% of its revenue.

Today, TechCrunch spoke with co-founder and CEO Nima Ghamsari about the company’s decision to go with a traditional IPO versus the ubiquitous SPAC or even a direct listing.

For one, Blend said he wanted to show its customers that it is an “around for a long time company” by making sure there’s enough on its balance sheet to continue to grow.

“We had to talk and convince some of the biggest investors in the world to invest in us, and that speaks to how long we’ll be around to serve these customers,” he said. “So it was a combination of our capital need and wanting to cement ourselves as a really credible software provider to one of the most regulated industries.”

Ghamsari emphasized that Blend is a software company that powers the mortgage process and is not the one offering the mortgages. As such, it works with the flock of fintechs that are working to provide mortgages.

“A lot of them are using Blend under the hood, as the infrastructure layer,” he said.

Overall, Ghamsari believes this is just the beginning for Blend.

“One of the things about financial services is that it’s still mostly powered by paper. So a lot of Blend’s growth is just going deeper into this process that we got started in years ago,” he said. As mentioned above, the company started out with its mortgage product but just keeps adding to it. Today, it also powers other loans such as auto, personal and home equity.

“A lot of our growth is actually powered by our other lines of business,” Ghamsari told TechCrunch. “There’s a lot to build because the larger digitization trends are just getting started in financial services. It’s a relatively large industry that has lots of change.”

In May, digital mortgage lender Better.com announced it would combine with a SPAC, taking itself public in the second half of 2021.

Powered by WPeMatico

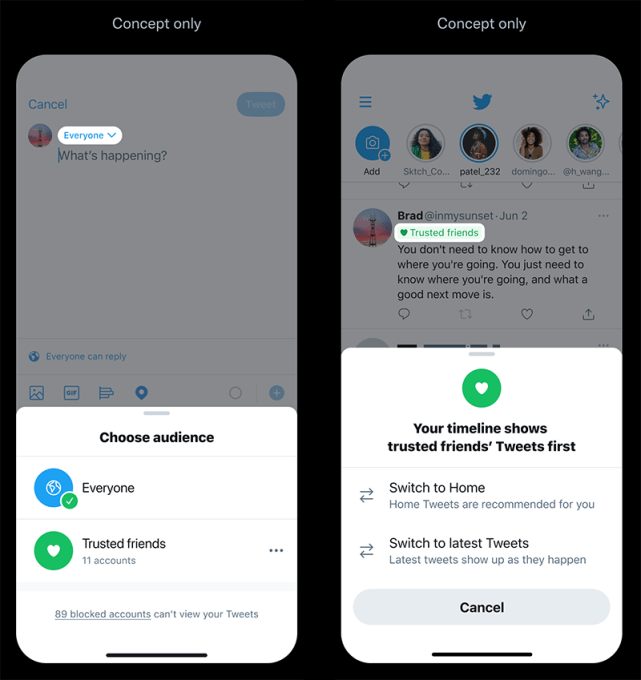

Twitter has a history of sharing feature and design ideas it’s considering at very early stages of development. Earlier this month, for example, it showed off concepts around a potential “unmention” feature that would let users untag themselves from others’ tweets. Today, the company is sharing a few more of its design explorations that would allow users to better control who can see their tweets and who ends up in their replies. The new concepts include a way to tweet only to a group of trusted friends, new prompts that would ask people to reconsider the language they’re using when posting a reply, and a “personas” feature that would allow you to tweet based on your different contexts — like tweets about your work life, your hobbies and interests, and so on.

The company says it’s thinking through these concepts and is looking to now gather feedback to inform what it may later develop.

The first of the new ideas builds on work that began last year with the release of a feature that allows an original poster to choose who’s allowed to reply to their tweet. Today, users can choose to limit replies to only people mentioned in the tweet, only people they follow, or they can leave it defaulted to “everyone.” But even though this allows users to limit who can respond, everyone can see the tweet itself. And they can like, retweet or quote tweet the post.

With the proposed Trusted Friends feature, users could tweet to a group of their own choosing. This could be a way to use Twitter with real-life friends, or some other small network of people you know more personally. Perhaps you could post a tweet that only your New York friends could see when you wanted to let them know you were in town. Or maybe you could post only to those who share your love of a particular TV show, sporting event or hobby.

Image Credits: Twitter

This ability to have private conversations alongside public ones could boost people’s Twitter usage and even encourage some people to try tweeting for the first time. But it also could be disruptive to Twitter, as it would chip away at the company’s original idea of a platform that’s a sort of public message board where everyone is invited into the conversation. Users may begin to think about whether their post is worthy of being shared in public and decide to hold more of their content back from the wider Twitter audience, which could impact Twitter engagement metrics. It also pushes Twitter closer to Facebook territory where only some posts are meant for the world, while more are shared with just friends.

Twitter says the benefit of this private, “friends only” format is that it could save people from the workarounds they’re currently using — like juggling multiple alt accounts or toggling between public to protected tweets.

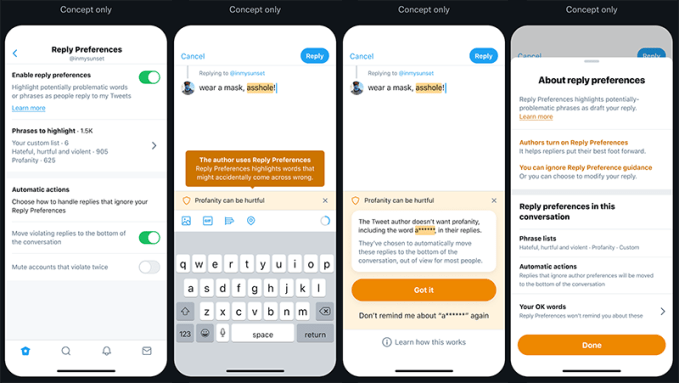

Another new feature under consideration is Reply Language Prompts. This feature would allow Twitter users to choose phrases they don’t want to see in their replies. When someone is writing back to the original poster, these words and phrases would be highlighted and a prompt would explain why the original poster doesn’t want to see that sort of language. For instance, users could configure prompts to appear if someone is using profanity in their reply.

Image Credits: Twitter

The feature wouldn’t stop the poster from tweeting their reply — it’s more a gentle nudge that asks them to be more considerate.

These “nudges” can have impact. For example, when Twitter launched a nudge that suggested users read an article before they amplify it with a retweet, it found that users opened articles before sharing them 40% more often. But in the case of someone determined to troll, it may not do that much good.

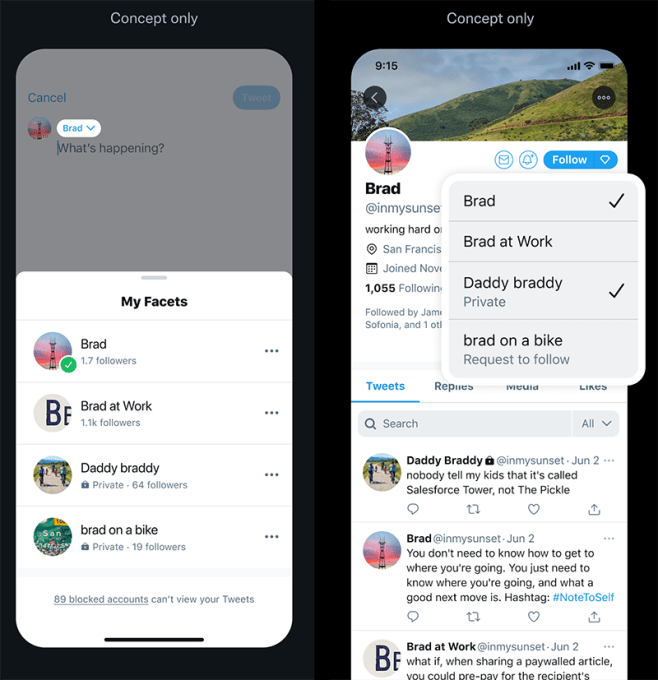

The third, and perhaps most complicated, feature is something Twitter is calling “Facets.”

This is an early idea about tweeting from different personas from one account. The feature would make sense for those who often tweet about different aspects of their lives, including their work life, their side hustles, their personal life or family, their passions and more.

Image Credits: Twitter

Unlike Trusted Friends, which would let you restrict some tweets to a more personal network, Facets would give other users the ability to choose whether they wanted to follow all your tweets, or only those about the “facet” they’re interested in. This way, you could follow someone’s tweets about tech, but ignore their stream of reactions they post when watching their favorite team play. Or you could follow your friend’s personal tweets, but ignore their work-related content. And so on.

This is an interesting idea, as Twitter users have always worried about alienating some of their followers by posting “off-topic” so to speak. But this also puts the problem of determining what tweets to show which users on the end user themselves. Users may be better served by the algorithmic timeline that understands which content they engage with, and which they tend to ignore. (Also: “facets‽”)

Twitter says none of the three features are in the process of being built just yet. These are only design mockups that showcase ideas the company has been considering. It also hasn’t yet made the decision whether any of the three will go under development — that’s what the user feedback it’s hoping to receive will help to determine.

Powered by WPeMatico

Accel announced Tuesday the close of three new funds totaling $3.05 billion, money that it will be using to back early-stage startups, as well as growth rounds for more mature companies. Notably, the 38-year-old Silicon Valley-based venture firm is doubling down on global investing.

The announcement underscores both the robust confidence investors continue to have for backing startups in the tech sector and the amount of money available to startups these days.

Specifically, today Accel is announcing its 15th early-stage U.S. fund at $650 million; its seventh early-stage European and Israeli fund also at $650 million and its sixth global growth stage fund at $1.75 billion. The latter fund is in addition, and designed to complement, a previously unannounced $2.3 billion global “Leaders” fund that is focused on later-stage investing that Accel closed in December.

Accel expects to invest in about 20 to 30 companies per fund on average, according to Partner Rich Wong. Its average investment in its growth fund will be in the $50 million to $75 million range, and $75 million and $100 million out of its global Leaders fund.

But the firm is also still eager and “excited” to incubate companies, Wong said.

“We’ll still write $500,000 to $1 million seed checks,” he told TechCrunch. “It’s important to us to work with companies from the very beginning and support them through their entire journey.”

Indeed, as TechCrunch recently reported, Accel has a history of backing companies that were previously bootstrapped (and often profitable) -– the latest example being Lower, a Columbus, Ohio-based fintech, which just raised a $100 million Series A.

Interestingly, Accel is often referred to some of these companies by existing portfolio companies (also in the case of Lower, whose CEO was referred to Accel by Galileo Clay Wilkes). More often than not, companies that Accel backs out of its early-stage and growth funds are bootstrapped and located outside of Silicon Valley.

The venture firm has long looked outside of Silicon Valley for opportunities, and has had offices not only in the Bay Area, but in London and Bangalore for years. Part of its investment thesis is to “invest early and locally,” according to Wong. Examples of this philosophy include investments in companies based all over the world — from Mexico to Stockholm to Tel Aviv to Munich.

Since the time of its last fund closure in 2019, the firm has seen 10 portfolio companies go public, including Slack, Austin-based Bumble, Bucharest-based UiPath, CrowdStrike, PagerDuty, Deliveroo and Squarespace, among others.

It also had 40 companies experience an M&A, including Utah-based Qualtrics’s $8 billion acquisition by SAP and Segment’s $3.2 billion acquisition by Twilio. Also, just last week, Rockwell Automation announced it was buying Michigan-based Plex Systems for $2.22 billion in cash. Accel first invested in Plex, which has developed a subscription-based smart manufacturing platform, in 2012.

Recent investments include a number of fintech companies such as LatAm’s Flink, Berlin-based Trade Republic, Unit and Robinhood rival Public. Accel has also backed as existing portfolio companies such as Webflow, a software company that helps businesses build no-code websites and events startup Hopin.

Wong says Accel is “open-minded but thematic” in its investment approach.

Accel Partner Sonali de Rycker, who is based out of London, agrees.

“For example, we’ll look at automation companies, consumer businesses and security companies, but at a global scale. Our goal is to find the best entrepreneurs regardless of where they are,” she said.

That has only been intensified by the recent rise of the smartphone and cloud, Wong said.

“Before, companies were mostly selling to the consumer in their own country,” he added. “But now the size of the market is so dramatically bigger, allowing them to become even larger, which is one of the reasons why I believe we’re seeing investment pace at this speed.”

To support this, it’s notable that Accel’s global Leaders fund is “dramatically” larger than the $500 million Leaders fund the firm closed in 2019.

Also, de Rycker points out, companies are staying private longer so the opportunity to invest in them until they sell or go public is greater.

Accel is also patient. In some cases, the firm’s investors will develop “years-long” relationships with companies they are courting.

“1Password is an example of this approach,” Wong said. “Arun [Mathew] had that relationship for at least six years before that investment was made. Finally, 1Password called and said ‘We’re ready, and we want you to do it.’ ”

And so Accel led the Canadian company’s first external round of funding in its 14-year history — a $200 million Series A — in 2019.

While the firm is open-minded, there are still some industries it has not yet embraced as much as others. For example, Wong said, “We’re not announcing a $2.2 billion crypto fund, but we have done crypto investments, and see some very interesting trends there. We’ll look at where crypto takes us.”

Powered by WPeMatico

Lower, an Ohio-based home finance platform, announced today it has raised $100 million in a Series A funding round led by Accel.

This round is notable for a number of reasons. First off, it’s a large Series A even by today’s standards. The financing also marks the previously bootstrapped Lower’s first external round of funding in its seven-year history. Lower is also something that is kind of rare these days in the startup world: profitable. Silicon Valley-based Accel has a history of backing profitable, bootstrapped companies, having also led large Series A rounds for the likes of 1Password, Atlassian, Qualtrics, Webflow, Tenable and Galileo (which went on to be acquired by SoFi).

In fact, Galileo founder Clay Wilkes introduced the VC firm to Dan Snyder, Lower’s founder and CEO. The two companies have a few things in common besides being profitable: they were both bootstrapped for years before taking institutional capital and both have headquarters outside of Silicon Valley.

“We were immediately intrigued because Ohio-based Lower echoes both of these themes,” said Accel partner John Locke, who led the firm’s investment in Lower and is taking a seat on the company’s board as part of the investment. “Like Galileo, Lower will be one of the most successful bootstrapped fintech companies globally. The combination of a company built in a nontraditional region across the globe and a bootstrapped company reminds us of [other] companies we have partnered with for a large Series A.”

There were other unnamed participants in the round, but Accel provided the “majority” of the investment, according to Lower.

Snyder co-founded Lower in 2014 with the goal of making the home-buying process simpler for consumers. The company launched with Homeside, its retail brand that Snyder describes as “a tech-leveraged retail mortgage bank” that works with realtors and builders, among others.

In 2018, the company launched the website for Lower, its direct-to-consumer digital lending brand with the mission of making its platform a one-stop shop where consumers can go online to save for a home, obtain or refinance a mortgage and get insurance through its marketplace. This year, it launched the Lower mobile app with a savings account.

Sitting (L to R): Co-founders Dan Snyder, Grayson Hanes

Standing (L to R): Co-founders Mike Baynes, Chris Miller

Not pictured: Robert Tyson; Image credit: Lower

Over the years, Lower has funded billions of dollars in loans and notched an impressive $300 million in revenue in 2020 after doubling revenue every year, according to Snyder.

“Our history is maybe a little atypical of fintech companies today,” he told TechCrunch. “We’ve had a view going back to the start of the company that we wanted to run it profitably. That’s been one of our pillars, so that’s what we’ve done. Also, we all grew up in the mortgage industry, so we saw firsthand the size of the market, but also how broken it was, so we wanted to change it.”

In launching the direct-to-consumer digital lending brand, the company was working to make the homebuying process more “digital, transparent and easier for consumers to access,” Snyder said.

At the same time, the company didn’t want to lose the human touch.

“We tried to design the app flow in a way where you can get as far along as you can in the application but if you want, at any point in time, to talk or chat with someone, we’re available,” Snyder added.

Image Credits: Lower

Lower’s typical customer is the millennial and now Gen Z who’s aspiring to own their first home, according to Snyder.

“They might be thinking, ‘OK, I might be living in an apartment now, but in the next few years I’m going to meet someone and/or have a child and I want to unlock the investment that is a home,’” he told TechCrunch. “And we’ll help them on that journey.”

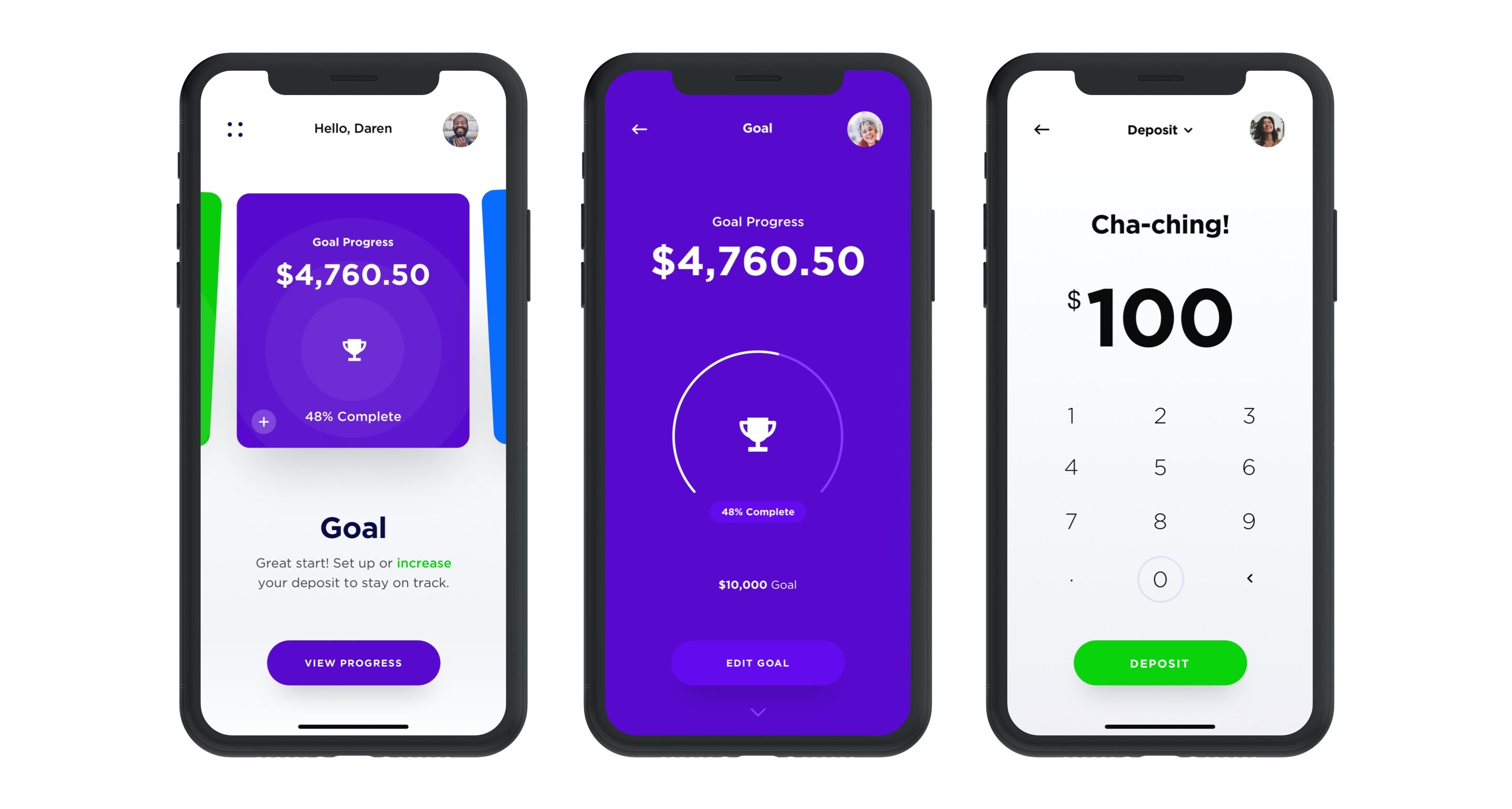

Lower’s recently launched new app offers a deposit account it’s dubbed “HomeFund.” The interest-bearing, FDIC-insured deposit account offers a 0.75% Annual Percentage Yield and is designed to help consumers save for a home with a “dollar-for-dollar match in rewards” up to the first $1,000 saved, Snyder said.

Lower works with more than 35 major insurance carriers nationally, including Nationwide, Liberty Mutual and Allstate. It has more than 1,600 employees, about half of which are based in Lower’s home state. That’s up from about 650 employees in June of 2020.

Looking ahead, the company plans to add more services and has an “aggressive roadmap” for adding new features to its platform. Today, for example, Lower sells primarily to Fannie Mae and Freddie Mac. And while it services the majority of its loans, like many large lenders, it uses a subservicer. That will change, however, in early 2022, when Lower intends to launch its own native servicing platform.

And while the company intends to continue to run profitably, Snyder said he and his co-founders “think the time is now to gain share.”

“We want to become a global brand, raise money and gain market share,” he added. “We’re going to continue to double down on product and build out our capabilities. We are the best-kept secret in fintech and plan to change that with smart branding, advertising and sponsorships.”

And last but not least, Lower is eyeing the public markets as part of its longer-term roadmap.

“Ultimately, we know we can build a great public company,” Snyder told TechCrunch. “We’re of the scale to be a public company right now, but we’re going to keep our heads down and we’re going to keep building for the next few years and then I think we can be in a spot to be a strong public business.”

Accel’s Locke points out that in the U.S., mortgage and home finance are among the largest financial service markets, and they have primarily been handled by large banks.

“For most consumers, getting a mortgage through these banks continues to be an overly complex, slow-moving process,” Locke told TechCrunch. “We believe by providing consumers a great mobile experience, Lower will gain share from incumbent banks, in the same way that companies like Monzo have in banking or Venmo in payments or Trade Republic and Robinhood in stock trading.”

Powered by WPeMatico

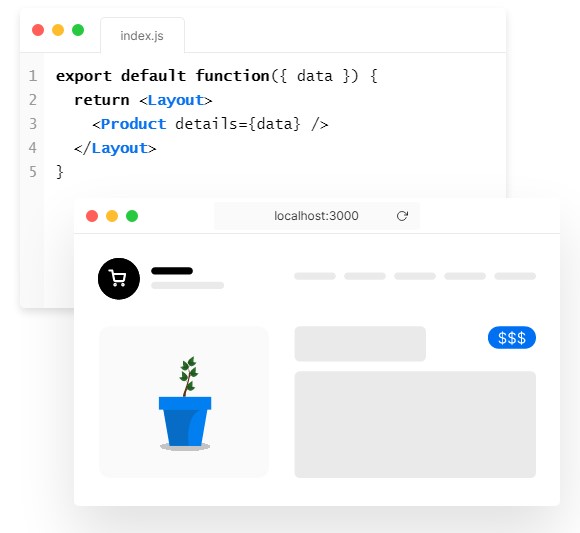

Vercel, the company behind the popular open-source Next.js React framework, today announced that it has raised a $102 million Series C funding round led by Bedrock Capital. Existing investors Accel, CRV, Geodesic Capital, Greenoaks Capital and GV also participated in this round, together with new investors 8VC, Flex Capital, GGV, Latacora, Salesforce Ventures and Tiger Global. In total, the company has now raised $163 million and its current valuation is $1.1 billion.

As Vercel notes, the company saw strong growth in recent months, with traffic to all sites and apps on its network doubling since October 2020. The number of sites among the world’s largest 10,000 websites that use Next.js grew 50% in the same time frame, too.

Image Credits: Vercel

Given the open-source nature of the Next.js framework, not all of these users are obviously Vercel customers, but its current paying customers include the likes of Carhartt, Github, IBM, McDonald’s and Uber.

“For us, it all starts with a front-end developer,” Vercel CEO Guillermo Rauch told me. “Our goal is to create and empower those developers — and their teams — to create delightful, immersive web experiences for their customers.”

With Vercel, Rauch and his team took the Next.js framework and then built a serverless platform that specifically caters to this framework and allows developers to focus on building their front ends without having to worry about scaling and performance.

Older solutions, Rauch argues, were built in isolation from the cloud platforms and serverless technologies, leaving it up to the developers to deploy and scale their solutions. And while some potential users may also be content with using a headless content management system, Rauch argues that increasingly, developers need to be able to build solutions that can go deeper than the off-the-shelf solutions that many businesses use today.

Rauch also noted that developers really like Vercel’s ability to generate a preview URL for a site’s front end every time a developer edits the code. “So instead of just spending all your time in code review, we’re shifting the equation to spending your time reviewing or experiencing your front end. That makes the experience a lot more collaborative,” he said. “So now, designers, marketers, IT, CEOs […] can now come together in this collaboration of building a front end and say, ‘that shade of blue is not the right shade of blue.’”

“Vercel is leading a market transition through which we are seeing the majority of value-add in web and cloud application development being delivered at the front end, closest to the user, where true experiences are made and enjoyed,” said Geoff Lewis, founder and managing partner at Bedrock. “We are extremely enthusiastic to work closely with Guillermo and the peerless team he has assembled to drive this revolution forward and are very pleased to have been able to co-lead this round.”

Powered by WPeMatico

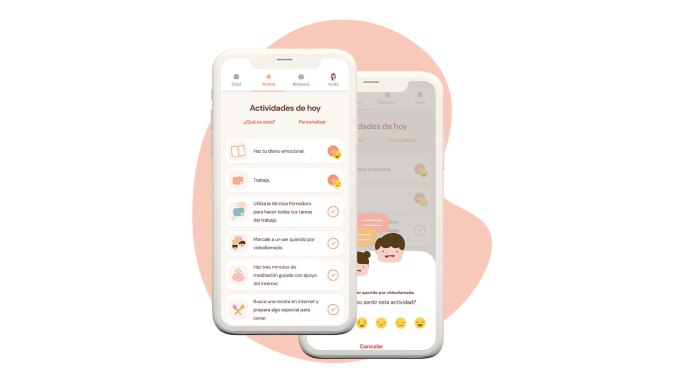

Andrea Campos has struggled with depression since she was eight years old. Over the years, she’s tried all sorts of therapies — from behavioral to pharmacotherapy.

In 2017, when Campos was in her early 20s, she learned to program and created a system to help manage her mental health. It started as a personal project, but as she talked to more people, Campos realized that many others might benefit from the system as well.

So she built an application to provide access to mental health tools for Spanish-speaking people and began testing it with a small group. At first, Campos herself was her own chatbot, texting with users who were tired of dealing with depression.

“During the month, I was pretending I was an app, and would send these people a list of activities they had to complete during the day, such as writing in a gratitude journal, and then asking them how those activities made them feel,” Campos recalls.

Her thinking was that sometimes with depression and anxiety comes “a lot of avoidance,” where people resist potential treatment out of fear.

The results from her small experiment were encouraging. So, Campos set out to conduct a bigger sample of experiments, and raised about $10,000 via a crowdfunding campaign. With that money, she hired a developer to build a chatbot for her app, which was mostly being used via Facebook Messenger.

Then an earthquake hit Mexico City and that developer lost everything — including his home and computer — and had to relocate.

“I was left with nothing,” Campos says. But that developer introduced her to another, who disappeared with his payment, and again, left Campos, “with nothing.”

“I realized at the beginning of 2019, I was going to have to do this by myself,” Campos said. So she used a site that she described as a “Wix for chatbots,” and created one herself.

After experimenting with the app with a sample of 700 people, Campos was even more encouraged and raised an angel round of funding for Yana, the startup behind her app. (Yana is an acronym for “You Are Not Alone.”) By early 2020, with just three months of runway left, she pivoted to create an app with chatbot integration that wasn’t just limited to use via Facebook Messenger.

Campos ended up launching the app more broadly during the same week that her city in Mexico went into quarantine.

Image Credits: Yana

At first, she said, she saw “normal, steady growth.” But then on October 10, 2020, Apple’s App Store highlighted Yana for International Mental Health Day, and the response was overwhelming.

“It was also my birthday so I was at a spa in a nearby town, relaxing, when I started hearing my cell phone go crazy,” Campos recalls. “Everything went nuts. I had to go back to Mexico City because our servers were exploding since they were not used to having that kind of volume.”

As a result of that exposure, Yana went from having around 80,000 users to reaching 1 million users two weeks later. Soon after that, Google highlighted the app as one of best for personal growth in 2020, and that too led to another spike in users. Today, Yana is about to hit the 5 million-user mark and is also announcing it has raised $1.5 million in funding led by Mexico’s ALLVP, which has also invested in the likes of Cornershop, Flink and Nuvocargo.

When the pandemic hit last year, six of Yana’s nine-person team decided to quarantine together in a “startup house” in Cancun to focus on building the company. Earlier this year, the company had raised $315,000 from investors such as 500 Startups, Magma and Hustle Fund. The company had pitched ALLVP, which was intrigued but wanted to wait until it could write a bigger check.

That time is now, and Yana is now among the top three downloaded apps in Mexico and 12 countries, including Spain, Chile, Ecuador and Venezuela.

With its new capital, Yana is planning to “move away from the depression/anxiety narrative,” according to Campos.

“We want to compete in the wellness space,” she told TechCrunch. “A lot of people were looking for us to deal with crises such as a breakup or a loss but then they didn’t always see a necessity to keep using Yana for longer than the crisis lasted.”

Some of those people would download the app again months later when hit with another crisis.

“We don’t want to be that app anymore,” Campos said. “We want to focus on whole wellness and mental health and transmit something that needs to be built every single day, just like we do with exercise.”

Moving forward, Yana aims to help people with their mental health not just during a crisis but with activities they can do on a daily basis, including a gratitude journal, a mood tracker and meditation — “things that prevent depression and anxiety,” Campos said.

“We want to be a vitamin for our soul, and keeping people mentally healthy on an ongoing basis,” she said. “We also want to include a community inside our application.”

ALLVP’s Federico Antoni is enthusiastic about the startup’s potential. He first met Campos when she was participating in an accelerator program in 2017, and then again recently.

The firm led Yana’s latest round because it “wanted to be on her team.”

“She [Campos] has turned into an amazing leader, and we realized her potential and strength,” he said. “Plus, Yana is an amazing product. When you download it, it’s almost like you can see a soul in there.”

Powered by WPeMatico

Productivity analytics startup Time is Ltd. wants to be the Google Analytics for company time. Or perhaps a sort of “Apple Screen Time” for companies. Whatever the case, the founders reckon that if you can map how time is spent in a company, enormous productivity gains can be unlocked and money better spent.

It’s now raised a $5.6 million late-seed funding round led by Mike Chalfen, of London-based Chalfen Ventures, with participation from Illuminate Financial Management and existing investor Accel. Acequia Capital and former Seal Software chairman Paul Sallaberry are also contributing to the new round, as is former Seal board member Clark Golestani. Furthermore, Ulf Zetterberg, founder and former CEO of contract discovery and analytics company Seal Software, is joining as president and co-founder.

The venture is the latest from serial entrepreneur Jan Rezab, better known for founding SocialBakers, which was acquired last year.

We are all familiar with inefficient meetings, pestering notifications chat, video conferencing tools and the deluge of emails. Time is Ltd. says it plans to address this by acquiring insights and data platforms such as Microsoft 365, Google Workspace, Zoom, Webex, MS Teams, Slack and more. The data and insights gathered would then help managers to understand and take a new approach to measure productivity, engagement and collaboration, the startup says.

The startup says it has now gathered 400 indicators that companies can choose from. For example, a task set by The Wall Street Journal for Time is Ltd. found the average response time for Slack users versus email was 16.3 minutes, comparing to emails which was 72 minutes.

Chalfen commented: “Measuring hybrid and distributed work patterns is critical for every business. Time Is Ltd.’s platform makes such measurement easily available and actionable for so many different types of organizations that I believe it could make work better for every business in the world.”

Rezab said: “The opportunity to analyze these kinds of collaboration and communication data in a privacy-compliant way alongside existing business metrics is the future of understanding the heartbeat of every company — I believe in 10 years time we will be looking at how we could have ignored insights from these platforms.”

Tomas Cupr, founder and Group CEO of Rohlik Group, the European leader of e-grocery, said: “Alongside our traditional BI approaches using performance data, we use Time is Ltd. to help improve the way we collaborate in our teams and improve the way we work both internally and with our vendors — data that Time is Ltd. provides is a must-have for business leaders.”

Powered by WPeMatico

This spring, Facebook confirmed it was testing Venmo-like QR codes for person-to-person payments inside its app in the U.S. Today, the company announced those codes are now launching publicly to all U.S. users, allowing anyone to send or request money through Facebook Pay — even if they’re not Facebook friends.

The QR codes work similarly to those found in other payment apps, like Venmo.

The feature can be found under the “Facebook Pay” section in Messenger’s settings, accessed by tapping on your profile icon at the top left of the screen. Here, you’ll be presented with your personalized QR code which looks much like a regular QR code except that it features your profile icon in the middle.

Underneath, you’ll be shown your personal Facebook Pay UR which is in the format of “https://m.me/pay/UserName.” This can also be copied and sent to other users when you’re requesting a payment.

Facebook notes that the codes will work between any U.S. Messenger users, and won’t require a separate payment app or any sort of contact entry or upload process to get started.

Users who want to be able to send and receive money in Messenger have to be at least 18 years old, and will have to have a Visa or Mastercard debit card, a PayPal account or one of the supported prepaid cards or government-issued cards, in order to use the payments feature. They’ll also need to set their preferred currency to U.S. dollars in the app.

After setup is complete, you can choose which payment method you want as your default and optionally protect payments behind a PIN code of your choosing.

The QR code is also available from the Facebook Pay section of the main Facebook app, in a carousel at the top of the screen.

Facebook Pay first launched in November 2019, as a way to establish a payment system that extends across the company’s apps for not just person-to-person payments, but also other features, like donations, Stars and e-commerce, among other things. Though the QR codes take cues from Venmo and others, the service as it stands today is not necessarily a rival to payment apps because Facebook partners with PayPal as one of the supported payment methods.

However, although the payments experience is separate from Facebook’s cryptocurrency wallet, Novi, that’s something that could perhaps change in the future.

Image Credits: Facebook

The feature was introduced alongside a few other Messenger updates, including a new Quick Reply bar that makes it easier to respond to a photo or video without having to return to the main chat thread. Facebook also added new chat themes including one for Olivia Rodrigo fans, another for World Oceans Day, and one that promotes the new F9 movie.

Powered by WPeMatico

Facebook has been making plenty of one-off virtual reality studio acquisitions lately, but today the company announced that they’re buying something with wider ambitions — a Roblox-like game creation platform.

Facebook shared that they’re buying Unit 2 Games, which builds a platform called Crayta. Like some other platforms out there, it builds on top of the Unreal Engine and gives users a more simple creation interface teamed with discovery and community features. Crayta has cornered its own niche pushing monetization paths like Battle Pass seasons, giving the platform a more Fortnite-like vibe as well.

Unit 2 has been around for just over three years, and Crayta launched just last July. Its audience has likely been limited by the studio’s deal to exclusively launch on Google’s cloud-streaming platform Stadia, though it’s also available on the Epic Games Store as of March.

The title feels designed for the lightweight nature of cloud-gaming platforms, with users able to share access to games just by linking other users, and Facebook seems keen to use Crayta to push forward their own efforts in the gaming sphere.

“Crayta has maximized current cloud-streaming technology to make game creation more accessible and easy to use. We plan to integrate Crayta’s creation toolset into Facebook Gaming’s cloud platform to instantly deliver new experiences on Facebook,” Facebook Gaming VP Vivek Sharma wrote in an announcement post.

The entire team will be coming on as part of the acquisition, though financial terms of the deal weren’t shared.

Powered by WPeMatico