Softbank

Auto Added by WPeMatico

Auto Added by WPeMatico

This week we’ve covered layoffs at unicorns both inside the Vision Fund and out. This afternoon we add two more to our list: Oyo and Rappi.

The staff reductions are surprising — and not. They are surprising, as Oyo (India-based, low-cost hotels) and Rappi (Latin America-focused e-commerce) were bright lights in the Vision Fund’s crown. And the layoffs are not surprising as other famous unicorns have recently cut staff in a bid to reduce costs, diminish losses and aim closer to profitability.

Our net lack of shock is underscored by the Vision Fund itself, which signaled late last year that it wants portfolio companies to get profitable and get public. The cuts are therefore a little more than unsurprising; we should have anticipated them.

Powered by WPeMatico

Hello and welcome back to our regular morning look at private companies, public markets and the gray space in between.

A million dollars isn’t cool. You know what’s cool? Positive adjusted EBITDA, or something close to it.

That’s the message from scooter unicorn Lime, which announced this week that it was cutting about 14% of its staff and closing a dozen markets. The staff reductions, numbering about 100, come as the company has touted efforts to improve its profitability — going as far as setting targets for when it might reach capital freedom, as well as highlighting the matter in a recent corporate blog post.

(Bird, a Lime competitor, also underwent layoffs this year.)

What’s going on? Unicorns, once hungry for growth, are now hell-bent to show current (and future) investors that their businesses aren’t unprofitable quagmires. Profitability, or movement towards it, is hot, and Lime is a good example of the trend — as is Getaround, which also wrote about its own layoffs this week. Let’s dig in.

Powered by WPeMatico

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

This week we had TechCrunch’s Alex Wilhelm and Danny Crichton on hand to dig into the news, with Chris Gates on the dials and more news than we could possibly cram into 30 minutes. So we went a bit over; sorry about that.

We kicked off by running through a few short-forms to get things going, including:

Turning to longer cuts, the team dug into the latest from SoftBank, its Vision Fund and the successes and struggles of its enormous startup bets. Leading the news cycle this week were layoffs at Zume, a robotic pizza delivery venture that is no longer pursuing robotic pizza delivery. Now it’s working on sustainable packaging. Cool, but it’s going to be hard for the company to grow into its valuation while pivoting.

Other issues have come up — more here — that paint some cracks onto the Vision Fund’s sunny exterior. Don’t be too beguiled by the bad news, Danny says; venture funds run like J-Curves, and there are still winners in that particular portfolio.

After that, we turned to China, in particular its venture slowdown. The bubble, in Danny’s view, has burst. The story discussed is here, if you want to read it. The short version for the lazy is that not only has China’s venture scene slowed down dramatically, but startups — even those with ample capital raised — are dying by the hundred. But one highly caffeinated Chinese startup continues to find growth in the world’s greatest tea market.

Finally we hit on the Sam Altman wager and the latest from Sisense, which is now a unicorn. All that and we had some fun.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week I wrote about the startups we lost in 2019. Before that, I noted the defining moments of VC in 2019.

Unfortunately, this will be my last newsletter, as I am leaving TechCrunch for a new opportunity. Don’t worry, Startups Weekly isn’t going anywhere. We’ll have a new writer taking over the weekly update soon enough; in the meantime, TechCrunch editor Henry Pickavet will be at the helm. You can still get in touch with me on Twitter @KateClarkTweets.

If you’re new here, you can subscribe to Startups Weekly here. Lots of good content will be coming your way in 2020.

TechCrunch reporter Manish Singh penned an interesting piece on the state of Indian startups this week: As Indian startups raise record capital, losses are widening (Extra Crunch membership required). In it, he claims the financial performance of India’s largest startups are cause for concern. Gems like Flipkart, BigBasket and Paytm have lost a collective $3 billion in the last year.

“What is especially troublesome for startups is that there is no clear path for how they would ever generate big profits,” he writes. “Silicon Valley companies, for instance, have entered and expanded into India in recent years, investing billions of dollars in local operations, but yet, India has yet to make any substantial contribution to their bottom lines. If that wasn’t challenging enough, many Indian startups compete directly with Silicon Valley giants, which while impressive, is an expensive endeavor.”

Manish’s story came one day after The New York Times published an in-depth report on Oyo, a tech-enabled budget hotel chain and rising star in the Indian tech community. The NYT wrote that Oyo offers unlicensed rooms and has bribed police officials to deter trouble, among other toxic practices.

Whether Oyo, backed by billions from the SoftBank Vision Fund, will become India’s WeWork is the real cause for concern. India’s startup ecosystem is likely to face a number of barriers as it grows to compete with the likes of Silicon Valley.

Follow Manish here or on Twitter for more of TechCrunch’s growing India coverage.

If you’ve still not subscribed to Extra Crunch, now is the time. Longtime TechCrunch reporter and editor Josh Constine is launching a new series to teach you how to pitch your startup. In it he will examine embargoes, exclusives, press kit visuals, interview questions and more. The first of many, How to find the right reporter to pitch your startup, is online now.

Subscribe to Extra Crunch here.

Another week, another new episode of TechCrunch’s venture capital-focused podcast, Equity. This week, we discussed a few of 2019’s largest scandals, Peloton’s strange holiday ad and the controversy over at the luggage startup Away. Listen here and be sure to subscribe, too.

For anyone wondering about changes at Equity following my departure from TechCrunch, the lovely Alex Wilhelm (founding Equity co-host) will keep the show alive and, soon enough, there will be a brand new co-host in my place. Please keep supporting the show and be sure to recommend it to all your podcast-adoring friends.

Powered by WPeMatico

Airbnb has well and truly disrupted the world of travel accommodation, changing the conversation not just around how people discover and book places to stay, but what they expect when they get there, and what they expect to pay. Today, one of the startups riding that wave is announcing a significant round of funding to fuel its own contribution to the marketplace.

Domio, a startup that designs and then rents out apart-hotels with kitchens and other full-home experiences, has raised $100 million ($50 million in equity and $50 million in debt) to expand its business in the U.S. and globally to 25 markets by next year, up from 12 today. Its target customers are millennials traveling in groups or families swayed by the size and scope of the accommodation — typically five times bigger than the average hotel room — as well as the price, which is on average 25% cheaper than a hotel room.

The Series B, which actually closed in August of this year, was led by GGV Capital, with participation from Eldridge Industries, 3L Capital, Tribeca Venture Partners, SoftBank NY, Tenaya Capital and Upper90. Upper90 also led the debt round, which will be used to lease and set up new properties.

Domio is not disclosing its valuation, but Jay Roberts, the founder and CEO, said in an interview that it’s a “huge upround” and around 50x the valuation it had in its seed round and that the company has tripled its revenues in the last year. Prior to this, Domio had only raised around $17 million, according to data from PitchBook.

For some comparisons, Sonder — another company that rents out serviced apartments to the kind of travelers who have a taste for boutique hotels — earlier this year raised $225 million at a valuation north of $1 billion. Others like Guesty, which are building platforms for others to list and manage their apartments on platforms like Airbnb, recently raised $35 million with a valuation likely in the range of $180 million to $200 million. Airbnb is estimated to be valued around $31 billion.

Domio plays in an interesting corner of the market. For starters, it focuses its accommodations at many of the same demographics as Airbnb. But where Airbnb offers a veritable hodgepodge of rooms and homes — some are people’s homes, some are vacation places, some never had and never will have a private occupant, and across all those the range of quality varies wildly — Domio offers predictability and consistency with its (possibly more anodyne) inventory.

“We are competing with amateur hosts on Airbnb,” said Roberts, who previously worked in real estate investment banking. “This is the next step, a modern brand, the next Marriott but with a more tech-powered brain and operating model.” These are not to be confused with something like Hilton’s Homewood Suites, Roberts stressed to me. He referred to Homewood as “a soulless hotel chain.”

“Domio is the anti-hotel chain,” he added.

Roberts is also quick to describe how Domio is not a real estate company as much as it is a tech-powered business. For starters, it uses quant-style algorithms that it’s built in-house to identify regions where it wants to build out its business, basing it not just on what consumers are searching for, but also weather patterns, economic indicators and other factors. After identifying a city or other location, it works on securing properties.

It typically sets up its accommodations in newer or completely new buildings, where developers — at least up to now — are not usually constructing with short-term rentals in mind. Instead, they are considering an option like Domio as an alternative to selling as condominiums or apartments, something that might come up if they are sensing that there is a softening in the market. “We typically have 75%-78% occupancy,” Roberts said. He added that hotels on average have occupancy rates in the high 60% nationally.

As Domio lengthens its track record — its 12 U.S. markets include Miami, Los Angeles, Philadelphia and Phoenix — Roberts says that they’re getting a more select seat at the table in conversations.

“Investors are starting to go out to buy properties on our behalf and lease them to us,” he said. This gives the startup a much more favorable rate and terms on those deals. “The next step is that Domio will manage these directly.” The most recent property it signed, he noted, includes a Whole Foods at the ground level, and a gym.

Using technology to identify where to grow is not the only area where tech plays a role. Roberts said that the company is now working on an app — yet to be released — that will be the epicenter of how guests interact to book places and manage their experience once there.

“Everything you can do by speaking to a human in a traditional hotel you will be able to do with the Domio app,” he said. That will include ordering room service, getting more towels, booking experiences and getting restaurant recommendations. “You can book your Uber through the Domio app, or sync your Spotify account to play music in the apartment.

Ans there are plans to extend the retail experience using the app. Roberts says it will be a “shoppable” experience where, if you like a sofa or piece of art in the place where you’re staying, you can order it for your own home. You can even order the same wallpaper that’s been designed to decorate Domio apartments.

Although Airbnb has grown to be nearly as ubiquitous as hotels (and perhaps even more prominent, depending on who you are talking to), the wider travel and accommodation market is still ripe for the taking, estimated to reach $171 billion by 2023 and the highest growth sector in the travel industry.

“Airbnb has taught us that hotels are not the only place to stay,” said Hans Tung, GGV’s managing partner. “Domio is capitalizing on the global shift in short-term travel and the consumer demand for branded experiences. From my travels around the world, there is a large, underserved audience — millennials, families, business teams — who prefer the combined benefits of an apartment and hotel in a single branded experience.”

I mentioned to Roberts that the leasing model reminded me a little of WeWork, which itself does not own the property it curates and turns into office space for its tenants. (The SoftBank investor connection is interesting in that regard.) Roberts was very quick to say that it’s not the same kind of business, even if both are based around leased property re-rented out to tenants.

“One of the things we liked about Domio is that is very capital-efficient,” said Tung, “focusing on the model and payback period. The short-term nature of customer stays and the combination of experience/price required to maintain loyal customers are natural enforcers of efficient unit economics.”

“For GGV, Domio stands out in two ways,” he continued. “First, CEO Jay Roberts and the Domio team’s emphasis on execution is impressive, with expansion into 12 cities in just three years. They have the right combination of vision, speed and agility. Domio’s model can readily tap into the global opportunity as they have ambition to scale to new markets. The global travel and tourism spend is $2.8 trillion with 5 billion annual tourists. Global travelers like having the flexibility and convenience of both an apartment and hotel — with Domio they can have both.”

Powered by WPeMatico

Gecko Robotics has landed $40 million in financing as it looks to build an additional 40 robots over the next year to meet what the company sees as growing demand for its safety and infrastructure monitoring services.

“We are growing fast solving critical infrastructure problems that affect our lives, and can even save lives,” says Jake Loosararian, Gecko Robotics’ 28-year-old co-founder and chief executive officer, in a statement. “At our core, we are a robot-enabled software company that helps stop life-threatening catastrophes. We’ve developed a revolutionary way to use robots as an enabler to capture data for predictability of infrastructure; reducing failure, explosions, emissions and billions of dollars of loss each year.”

In the three years since its launch in 2016, Gecko Robotics has managed to grow from a small team of Pittsburgh robotics experts hailing from Carnegie Mellon. Indeed, the company has added more than 100 new employees. The hiring push has been largely around creating a team of qualified experts in particular market segments who can operate the robots that Gecko deploys to industrial work sites.

There’s been something of a robotics revolution in the safety and compliance market over the past few years. From automated assembly lines to warehouses and now to chemical plants and refineries, robots are making their presence felt.

And Gecko isn’t the only company that’s trying to tackle the market. Other companies like Invert Robotics, a Christchurch, New Zealand-based company, has built its own competitive robotic safety inspector.

The initial pitch from Gecko managed to attract angel investors like Mark Cuban, Deep Nishar (a managing partner at SoftBank), Josh Reeves and Jake Seid, the managing director at Stone Bridge Ventures.

Now the company adds the Midwestern venture capital juggernaut Drive Capital to its stable of investors.

“We are very excited for the future of robotics in industrial inspection. The Gecko Robotics team are revolutionizing an industry that is in need of a real upgrade and will save lives,” said Mark Kvamme, lead investor and partner at Drive Capital. “I see amazing potential for Gecko’s business model, they are on the path to become a market leader in their industry.”

Gecko Robotics has already opened a 20,000-square-foot office in Houston, and has offices in Houston, Austin and Pittsburgh.

“The robots are amazing, but they’re not going to be able to complete the job done by these experts who have experience of 30 to 40 years,” says Loosararian. “We have thought leaders who go out in the field… they take the robots out and they use their own manual ability and knowledge to provide the expertise to the clients.”

Gecko currently has 60 robots in its stable of robots and will add at least another 40 over the course of the year. “The product at the end is the software license that they pay for annually,” Loosararian says.

Powered by WPeMatico

OneConnect’s U.S.-listed IPO flew under our radar last week, which won’t do. The company’s public offering is both interesting and important, so let’s take a few minutes this morning to understand what we missed and why we care.

The now-public company sells financial technology that banks in China and select foreign countries can use to bring their services into the modern era. OneConnect charges mostly for usage of its products, driving over three-quarters of its revenue from transactions, including API calls.

After pricing its shares at $10 apiece, the SoftBank Vision Fund-backed company wrapped last week worth the same: $10 per share.

One one hand, OneConnect is merely another China-based IPO listing domestically here in the United States, making it merely one member of a crowd. So, why do we care about its listing?

A few reasons. We care because the listing is another liquidity event for SoftBank and its Vision Fund. As the Japanese conglomerate revs up its second Vision Fund cycle (Vision Fund 2, more here), returns and proof of its ability to pick winners and fuel them with capital are key. OneConnect’s success as a public company, therefore, matters.

And for us market observers, the debut is doubly exciting from a financial perspective. No, OneConnect doesn’t make money (very much the opposite). What’s curious about the company is that it brought huge losses to sale when it was pitching its equity. Which, in a post-WeWork world, are supposed to be out of style. Let’s see how well it priced.

OneConnect targeted a $9 to $10 per-share IPO price. That makes its final, $10 per-share pricing the top of its range. That said, given how narrow its range was, the result doesn’t look like much of a coup for the company. That’s doubly true when we recall that OneConnect lowered its IPO price range from $12 to $14 per share (a more standard price band) to the lower figures. So, the company managed to price at the top of its expectations, but only after those were cut to size.

When it all wrapped, OneConnect was worth about $3.7 billion at its IPO price, according to math from The New York Times. TechCrunch’s own calculations value the firm at a slightly richer $3.8 billion. Regardless, the figure was a disappointment.

When OneConnect raised from SoftBank’s Vision Fund in early 2018, $650 million was invested at a $6.8 billion pre-money valuation, according to Crunchbase data. That put a $7.45 billion post-money price tag on the Ping An-sourced business. To see the company forced to cut its IPO valuation so far is difficult for OneConnect itself, its parent Ping An and its backer SoftBank.

I promised to be brief when we started, so let’s stay curt: OneConnect’s business was worth far less than expected because while it posted impressive revenue gains, the company’s deep unprofitability made it less palatable than expected to public investors.

OneConnect managed to post revenue growth of more than 70% in the first three quarters of 2019, expanding top line to $217.5 million in the period. However, during that time it generated just $70.9 million in gross profit, the sum it could use to cover its operating costs. The company’s cost structure, however, was far larger than its gross profit.

Over the same nine-month period, OneConnect’s sales and marketing costs alone outstripped its total gross profit. All told, OneConnect posted operating costs of $227.6 million in the first three quarters of 2019, leading to an operating loss of $156.6 million in the period.

The company will, therefore, burn lots of cash as it grows; OneConnect is still deep in its investment motion, and far from the sort of near-profitability that we hear is in vogue. In a sense, OneConnect bears the narrative out. It had to endure a sharp valuation reduction to get out. You can see the market’s changed mood in that fact alone.

Photo by Roberto Júnior on Unsplash

Powered by WPeMatico

Three months after Goldman Sachs lent $100 million to Mexican fintech Konfio, SoftBank has invested another $100 million into the financial services company. The investment confirms Reuters’ August report that SoftBank was in advanced talks with the startup — now one of the most heavily funded fintechs in Mexico.

SoftBank is continuing to expand its Mexican portfolio, which now includes used car buying platform Kavak and payments startup Clip. Aside from Mexico, SoftBank has primarily focused its $5 billion Latin America fund on Brazil — and recently marked its entry into Argentina with an injection into financial services company Uala in a $150 million investment co-led by Tencent.

As traditional banks shy away from small to medium-sized business loans in Mexico, Konfio’s credit underwriting service provides a faster alternative. Konfio uses a data-first approach to enable fast credit assessment for SMBs looking to grow their businesses. The service can disburse credit in a one-day turnaround, as opposed to locking users into a traditional months-long approval process that can often require collateral.

Meanwhile, if you’re a startup gathering massive amounts of data on Latin America’s growing middle class, SoftBank might be interested in your growth funding. The Japanese conglomerate seems to want to know everything it can about Latin America’s consumer spending habits, mobile usage and personal banking user behavior.

Watch Konfio founder and CEO David Arana’s panel at TechCrunch’s São Paulo event here.

Powered by WPeMatico

Work tools startup Notion, which recently reached a reported $800 million valuation, isn’t on the verge of a big SoftBank round. In fact, COO Akshay Kothari says the startup has “never felt like if we had more money we could grow faster.”

The company, centered around an app that helps non-developers build collaboration tools, has more than one million users and has scaled its product quickly despite having a team of just 27.

I wrote about the company’s partnership with some of tech’s top accelerators and venture capital firms last month. People are very curious about this small company and how it is run, so here’s more from my recent interview with COO Akshay Kothari in which we discussed the hyped startup’s philosophy of staying small and some of the challenges it may have ahead with this brand of thinking as competitors are raising massive sums.

This interview has been edited for length and clarity.

Notion COO Akshay Kothari (Photo: Notion)

Where does your story begin with Notion? Give me a snapshot of where the team is now.

Akshay Kothari: [Notion co-founders Ivan Zhao and Simon Last] started Notion six years ago and that’s when I invested. I had sold my previous company and I had this newfound money that I didn’t know what to do with. I invested in Notion, so that’s my connection.

We were kind of in research mode for many years trying to uncover what the market needs were. We launched about two years ago; 1.0 was just notes that you could take and a wiki so that you could collaborate with people. And then last year we launched databases and that was the 2.0 version, which kind of seemed like an inflection point, where now you could not only have your notes and your wiki, but also manage your tasks, manage your projects, manage candidates and recruiting, all in a single tool.

Over the last year and a half, the company has grown extremely fast. I joined about a year ago, there were about 10 people at the beginning of this year and now we’re close to 30. It’s still a really small engineering team. We’re 9 engineers, we don’t have any product managers, and we’re 2 designers. So there are about 10 people that are building the product, and 10 people on community and support teams, something that we’ve invested very heavily in. We’re starting to have a sales and marketing team. We have 2 people in marketing and 2 people in sales. That all rounds up to about 27 which is where we are now.

Since you joined do you think the idea has shifted at all?

In terms of the original idea, we were thinking about how people who didn’t know how to code could build things like tools and software that were really useful. I guess the only realization has been that not everyone wakes up wanting to build software, but everyone wakes to solve problems. That was the pivot to focusing on notes, wikis and tasks, because that’s actually something that every team needs.

Are those needs universal for big and small teams?

For the first 100 people you can actually do a lot with Notion. With 30 people, we pretty much run the entire company, except for using Slack for internal communication and Intercom for external communication like talking to customers. Everything else is actually on Notion, like our application tracking system for recruiting inside Notion, our sales CRM is in Notion, our wiki obviously is, our project management as well — no, we don’t use Jira.

For sub-100 businesses, you actually don’t need another tool. When you get to hundreds of people what tends to happens is that some person or some team tends to have a preference for a specific tool. In those situations, Notion plays well with other tools. You can embed things easily. So let’s say Excel or Google Sheets is something that you want to use, you can just embed that inside Notion. So Notion becomes this kind of central nervous system for all of the work that people are doing.

Building on that, one of the things we haven’t done is we don’t do synchronous communication so we’ve stayed away from that because I feel like people like using Slack. On Slack, you can’t actually collaborate on a project… Notion has become a place where you can actually do a lot of your work alongside the synchronous communication.

So, no interest in building a chat or video chat product?

Not in the near term. I think Slack is one of those enterprise tools that people at companies actually like. For a lot of these other tools, we just have to use it, not because we love it but because that that’s what exists.

Notion’s headquarters (Photo: Notion)

What are the barriers for satisfying the customers with 100+ employees?

Powered by WPeMatico

Accel, one of the world’s most influential venture capitalist firms, is getting more bullish on India.

The Silicon Valley-headquartered firm, which largely focuses on early-stage investments, said today it has closed $550 million for its sixth venture fund in India.

This is a significant amount of capital for Accel’s efforts in the country, where it began investing 15 years ago and has infused roughly $1 billion through all its previous funds.

Anand Daniel, a partner for Accel in India, told TechCrunch in an interview that the VC fund will continue to focus on identifying and investing in seed and early-stage startups.

But the fund realized it needed more money so it could actively participate in follow-on rounds (later-stage financing rounds) of its portfolio startups. The announcement today follows Accel’s similar recent push in Europe and Israel, where it closed a $575 million fund.

“We also selectively do growth investments for companies that are scaling well, such as Swiggy, UrbanClap, BlackStone and Bounce. We have continued to back them through Series B and Series C rounds,” he said.

At the risk of being accused of bias, I’ll say this: Accel India is a rare Indian fund that had credible exits and more promising exits in the pipeline. They’re also some of the nicest people to work with. https://t.co/aZGjDgSQKe

— JPK (@therealjpk) December 2, 2019

Like in many other markets, Accel’s track record in India is quite impressive. It participated in the seed financing round of e-commerce firm Flipkart, which was then valued at $4 million post-money. Walmart bought a majority stake in Flipkart last year for $16 billion. (This helped Accel net more than $1 billion in return from Flipkart.)

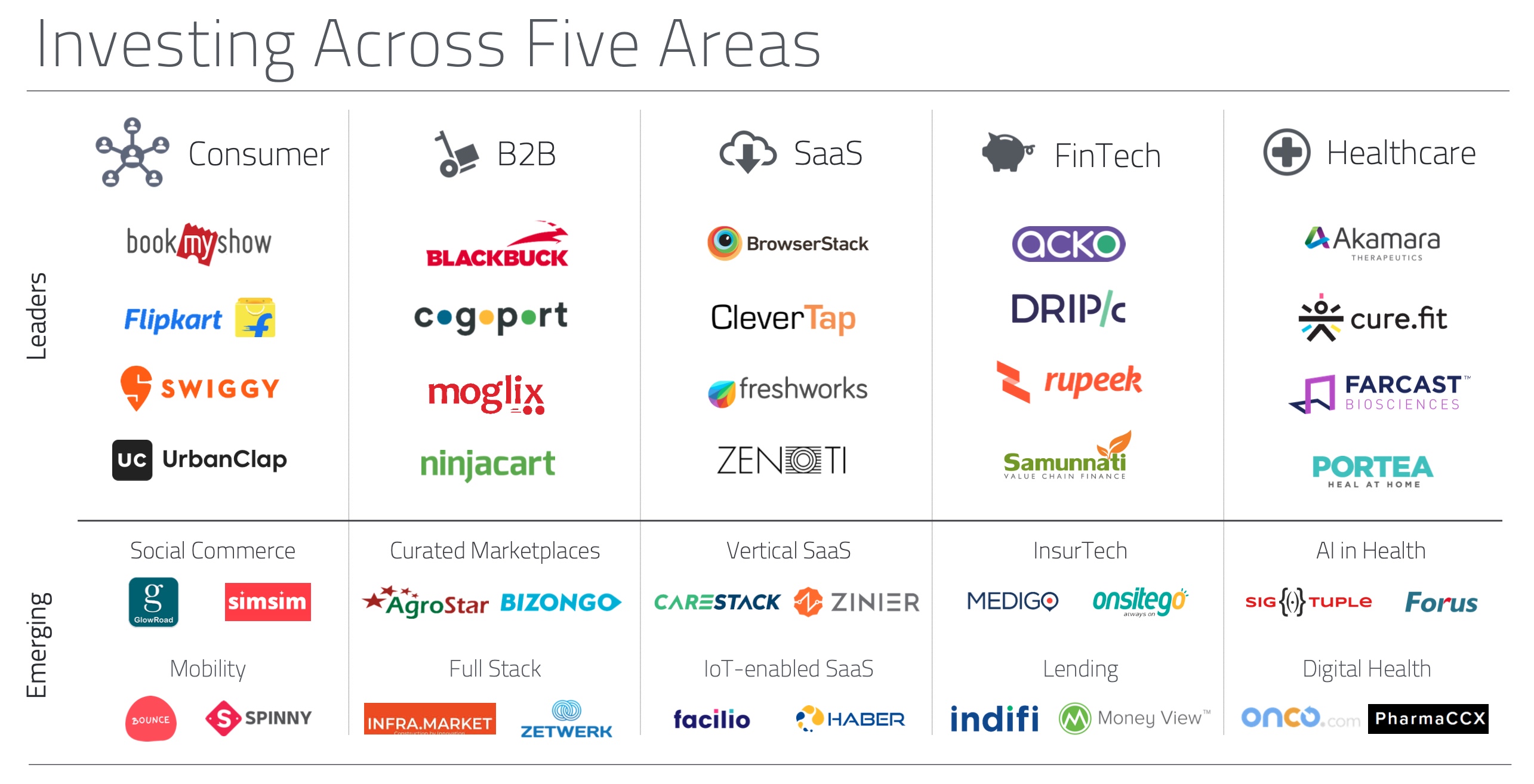

Accel, which has nine partners and more than 50 members in total in India, also invested in the seed round of SaaS giant Freshworks, which is now valued at more than $3 billion, food delivery startup Swiggy, also valued at north of $3 billion, and recently turned unicorn BlackBuck. Accel has been the first institutional investor for 85% of startups in its portfolio.

The VC firm says 44 of the 100-odd startups in its India portfolio today are valued at over $100 million each. In total, including Flipkart’s $21 billion market value, Accel’s portfolio firms have created $44 billion in market value.

Some of the investments Accel has made in India

“When we started our first fund in India in 2005, the world was a very different place. Just 1 in 50 Indians had access to the internet and mobile phone ownership was nascent. Yet we firmly believed that India was on the cusp of a big change,” the firm said in a statement.

“Today, the opportunity ahead is significantly bigger than when we started in 2005: India can now digitally identify 1.3 billion people, has 600 million internet users and 150 million online transacting customers with a national payments platform that processes $20 billion a month.”

Daniel said moving forward Accel will continue to focus on consumer, business-to-business, fintech, healthcare and global SaaS categories. “We have nine partners with their own areas of interest. They invest from their own conviction and finance seed rounds. If we see a particular sector evolving, then we do a deeper thesis work,” he said.

“We then develop deeper confidence for the space. For example, back in the day we invested in mobility startup TaxiForSure, long before Uber had arrived in India. That helped us understand mobility well. We have used those learnings to invest in several more mobility startups.”

Accel’s growing interest in India comes at a time when several other giants, including SoftBank and Prosus Ventures, have also become more active in the nation — though they tend to finance later-stage rounds.

For Indian startups that are already having their best year, this can only be good news.

Powered by WPeMatico