Softbank

Auto Added by WPeMatico

Auto Added by WPeMatico

SoftBank Investment Advisers and WeWork Labs say they’ve officially kicked off the first session of Emerge, an accelerator program designed for underrepresented founders.

In their press release, the companies describe Emerge as “launched by SoftBank with support from WeWork Labs” (that’s the co-working company’s global accelerator program), with a goal of bringing more equality to tech and venture capital.

It’s an equity-free, eight-week program that includes workshops, access to mentors from SoftBank and the WeWork community and sessions with SoftBank executives. It all culminates in a showcase event for investors and SoftBank partners.

The Emerge website describes the program as based in San Mateo, Calif. — but given COVID-19, the sessions and programming are all virtual.

“Supporting underrepresented founders is a top priority for us, ensuring we see more diverse startups across the tech ecosystem,” said Catherine Lenson, managing partner and chief human resources officer at SoftBank Investment Advisers, in a statement. “There is a lack of diversity in the sector as a whole, and we need to do more to address it. That is why we’re excited to launch this program and to see the positive impact that these inspiring founders will have.”

This is also a reminder that while the larger corporate entities are currently embroiled in a legal and financial dispute, WeWork and its largest investor remain closely intertwined.

Here are the 14 startups in the initial program:

Powered by WPeMatico

Earlier today a grip of new data presented a sharply negative picture of the American economy. And this afternoon, news broke that a trio of well-known, heavily-backed unicorns were cutting staff.

With stocks down as well, we’ve received negative signals from the private market, the public market and the economy as a whole in the same day. Let’s take a minute to set the macro stage, and then go over the latest cuts from Carta (first reported by Bloomberg), Zume (Business Insider broke that particular story) and Opendoor (via The Information).

The backdrop for today’s cuts is a faltering American economy. A glance at recent news is sufficient. In the last few hours, home builder confidence recorded the “biggest drop in history,” while retail sales fell 8.7% in March, what CNBC noted was “the most ever in government data,” and CNN Business reported that American factories’ output fell 5.4% in March, “their steepest one-month slowdown since 1946.”

It’s perhaps no surprise, then, that we’ve seen unicorn layoffs all year. In January the news was Vision Fund-backed companies cutting burn to skate closer to profitability. Then, the first round of COVID-19-forced staff cuts landed at big companies; firms like Bird and TripActions slashed staff as their companies were rent by a slowdown in their core operations by the pandemic and its related economic and social changes.

Slimmer cuts at smaller companies have happened on a nearly chronic basis, something that TechCrunch has covered, as well.

Today, however, saw three cuts from three unicorns (private companies worth $1 billion or more) that have long been objects of TechCrunch’s attention. So, let’s talk about them briefly:

It’s getting hard to keep track of all the cuts. Heck, I helped break Modsy layoffs recently with TechCrunch’s Natasha Mascarenhas, and we were first to the BounceX cuts as well. It’s a rough, bad economy, and it’s harming growth-oriented companies that like startup unicorns.

More when we have it, probably sooner than we’d like to report.

Powered by WPeMatico

Good morning friends, and welcome back to TechCrunch’s Equity Monday, a short-form audio hit to kickstart your week.

Before we jump into today’s show, don’t forget that the long-form Equity that started in the unicorn era and continue in today’s changed world still drops on Friday. We had a blast last week, so make sure to catch up.

That said, there was a lot to go over this morning, so let’s get into what we had to discuss:

And that’s the show for today. Stay safe, and we’ll be back Friday morning to cap off whatever this week winds up becoming.

Equity drops every Monday at 7:00 AM PT and Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Spotify and all the casts.

Powered by WPeMatico

Vijay Shekhar Sharma, founder and chief executive of India’s most valuable startup, Paytm, posed an existential question in a recent press conference.

“What do you think of the commercial model for digital mobile payments. How do we make money?” Sharma asked Nandan Nilekani, one of the key architects of the Universal Payments Infrastructure that created a digital payments revolution in the country.

It’s the multi-billion-dollar question that scores of local startups and international giants have been scrambling to answer as many of them aggressively shift their focus to serving merchants and building lending products and other financial services .

New Delhi’s abrupt move to invalidate much of the paper bills in the cash-dominated nation in late 2016 sent hundreds of millions of people to cash machines for months to follow.

For a handful of startups such as Paytm and MobiKwik, this cash crunch meant netting tens of millions of new users in a span of a few months.

India then moved to work with a coalition of banks to develop the payments infrastructure that, unlike Paytm and MobiKwik’s earlier system, did not act as an intermediary “mobile wallet” to serve as an intermediary between users and their banks, but facilitated direct transaction between two users’ bank accounts.

Silicon Valley companies quickly took notice. For years, Google and the likes have attempted to change the purchasing behavior of people in many Asian and African markets, where they have amassed hundreds of millions of users.

In Pakistan, for instance, most people still run errands to neighborhood stores when they want to top up credit to make phone calls and access the internet.

With China keeping its doors largely closed for foreign firms, India, where many American giants have already poured billions of dollars to find their next billion users, it was a no-brainer call.

“Unlike China, we have given equal opportunities to both small and large domestic and foreign companies,” said Dilip Asbe, chief executive of NPCI, the payments body behind UPI.

And thus began the race to participate in the grand Indian experiment. Investors have followed suit as well. Indian fintech startups raised $2.74 billion last year, compared to 3.66 billion that their counterparts in China secured, according to research firm CBInsights.

And that bet in a market with more than half a billion internet users has already started to pay off.

“If you look at UPI as a platform, we have never seen growth of this kind before,” Nikhil Kumar, who volunteered at a nonprofit organization to help develop the payments infrastructure, said in an interview.

In October, just three years after its inception, UPI had amassed 100 million users and processed over a billion transactions. It has sustained its growth since, clocking 1.25 billion transactions in March — despite one of the nation’s largest banks going through a meltdown last month.

“It all comes down to the problem it is solving. If you look at the western markets, digital payments have largely been focused on a person sending money to a merchant. UPI does that, but it also enables peer-to-peer payments and across a wide-range of apps. It’s interoperable,” said Kumar, who is now working at a startup called Setu to develop APIs to help small businesses easily accept digital payments.

Vice-president of Google’s Next Billion Users Caesar Sengupta speaks during the launch of the Google “Tez” mobile app for digital payments in New Delhi on September 18, 2017 (Photo: Getty Images via AFP PHOTO / SAJJAD HUSSAIN)

The Google Pay app has amassed over 67 million monthly active users. And the company has found the UPI pipeline so fascinating that it has recommended similar infrastructure to be built in the U.S.

In August, the Federal Reserve proposed to develop a new inter-bank 24×7 real-time gross settlement service that would support faster payments in the country. In November, Google recommended (PDF) that the U.S. Federal Reserve implement a real-time payments platform such as UPI.

“After just three years, the annual run rate of transactions flowing through UPI is about 19% of India’s Gross Domestic Product, including 800 million monthly transactions valued at approximately $19 billion,” wrote Mark Isakowitz, Google’s vice president of Government Affairs and Public Policy.

Paytm itself has amassed more than 150 million users who use it every year to make transactions. Overall, the platform has 300 million mobile wallet accounts and 55 million bank accounts, said Sharma.

But despite on-boarding more than a hundred million users on their platform, payment firms are struggling to cut their losses — let alone turn a profit.

At an event in Bangalore late last year, Sajith Sivanandan, managing director and business head of Google Pay and Next Billion User Initiatives, said current local rules have forced Google Pay to operate in India without a clear business model.

Mobile payment firms never levied any fee to users as a strategy to expand their reach in the country. A recent directive from the government has now put an end to the cut they were receiving to facilitate UPI transactions between users and merchants.

Google’s Sivanandan urged the local payment bodies to “find ways for payment players to make money” to ensure every stakeholder had incentives to operate.

Paytm, which has raised more than $3 billion to date, reported a loss of $549 million in the financial year ending in March 2019.

The firm, backed by SoftBank and Alibaba, has expanded to several new businesses in recent years, including Paytm Mall, an e-commerce venture, social commerce, financial services arm Paytm Money and a movies and ticketing category.

This year, Paytm has expanded to serve merchants, launching new gadgets such as a stand that displays QR check-out codes that comes with a calculator and a battery pack, a portable speaker that provides voice confirmations of transactions and a point-of-sale machine with built-in scanner and printer.

In an interview with TechCrunch, Sharma said these devices are already garnering impressive demand from merchants. The company is offering these gadgets to them as part of a subscription service that helps it establish a steady flow of revenue.

The firm’s Money arm, which offers lending, insurance and investing services, has amassed over 3 million users. The head of Paytm Money, Pravin Jadhav, resigned from the company this week, a person familiar with the matter said. A Paytm spokeswoman declined to comment. (Indian news outlet Entrackr first reported the development.)

Flipkart’s PhonePe, another major player in India’s payments market, today serves more than 175 million users, and over 8 million merchants. Its app serves as a platform for other businesses to reach users, explained Rahul Chari, co-founder and CTO of the firm, in an interview with TechCrunch. The company is currently not taking a cut for the real estate on its app, he added.

But these startups’ expansion into new categories means that they now have to face off even more rivals, and spend more money to gain a foothold. In the social commerce category, for instance, Paytm is competing with Naspers-backed Meesho and a handful of new entrants; and heavily-backed OkCredit and KhataBook today lead the bookkeeping market.

BharatPe, which raised $75 million two months ago, is digitizing mom and pop stores and granting them working capital. And PineLabs, which has already become a unicorn, and MSwipe have flooded the market with their point-of-sale machines.

A vendor holds an Mswipe terminal, operated by M-Swipe Technologies Pvt Ltd., in an arranged photograph at a roadside stall in Bengaluru, India, on Saturday, Feb. 4, 2017. (Photographer: Dhiraj Singh/Bloomberg via Getty Images)

“They have no choice. Payment is the gateway to businesses such as e-commerce and lending that you can monetize. In Paytm’s case, their earlier bet was Paytm Mall,” said Jayanth Kolla, founder and chief analyst at research firm Convergence Catalyst.

But Paytm Mall has struggled to compete with giants Amazon India and Walmart’s Flipkart. Last year, Mall pivoted to offline-to-online and online-to-offline models, wherein orders placed by customers are serviced from local stores. The company also secured about $160 million from eBay last year.

An executive who previously worked at Paytm Mall said the venture has struggled to grow because its goal-post has constantly shifted over the years. It has recently started to focus on selling fastags, a system that allows vehicle owners to swiftly pay toll fees. At least two more executives at the firm are on their way out, a person familiar with the matter said.

Kolla said the current dynamics of India’s mobile payments market, where more than 100 firms are chasing the same set of audience, is reminiscent of the telecom market in the country from more than a decade ago.

“When there were just four to five players in the telecom market, the prospect of them becoming profitable was much higher. They were scaling like crazy. They grew with the lowest ARPU in the world (at about $2) and were still profitable.

“But the moment that number grew to more than a dozen overnight, and the new players started offering more affordable plans to subscribers, that’s when profitability started to become elusive,” he said.

To top that off, the arrival of Reliance Jio, a telecom operator run by India’s richest man, in 2016 in the country with the cheapest tariff plans in the world, upended the market once again, forcing several players to leave the market, or declare bankruptcies, or consolidate.

India’s mobile payments market is now heading to a similar path, said Kolla.

If there were not enough players fighting for a slice of India’s mobile payments market that Credit Suisse estimate could reach $1 trillion by 2023, WhatsApp, the most popular app in the country with more that 400 million users, is set to roll out its mobile payments service in the country in a couple of months.

At the aforementioned press conference, Nilekani advised Sharma and other players to focus on financial services such as lending.

Unfortunately, the coronavirus outbreak that promoted New Delhi to order a three-week lockdown last month is likely going to impact the ability of millions of people to use such services.

“India has more than 100 million microfinance accounts, serviced in cash every week by gig-economy workers, who hawk vegetables on street corners or embroider saris sold in malls, among other things. Three out of four workers make a living by working casually for others or at their family firms and farms. Prolonged shutdowns will impair their ability to repay loans of 2.1 trillion rupees ($28.5 billion), putting the world’s largest microfinance industry at risk,” wrote Bloomberg columnist Andy Mukherjee.

Powered by WPeMatico

Earlier today, during an eye-popping market selloff, DoorDash announced that it has privately filed to go public. The decision to file privately will allow the high-valued startup to get its S-1 documents in good order with the SEC before showing the rest of us what it has up its sleeve.

The move to announce its private filing is more interesting and could be related to prepping demand for its shares, providing some PR-cover for backer SoftBank, which could use the assist, or, perhaps, to dampen investor excitement for rival companies, in the face of DoorDash’s implied success and maturity.

Whatever the reasons behind the timing — some of which must deal with the capital requirements of long-running cash burn — the filing is a new milestone for the on-demand and gig economies. And how well DoorDash’s filing is received, predicated in no small part on its recent financial performance, will help set sentiment for a number of other, richly backed startups.

So let’s remind ourselves of what we know about DoorDash’s financial history. This will give us a workable foundation heading into its eventual S-1, and, we presume, old-fashioned IPO. (It’s hard to imagine the cash-fired engine that is DoorDash looking toward a direct listing.) We’ll dig through its fundraising, unearth what we know about its revenue over time and turn over some data concerning its hiring efforts in recent months to better understand its IPO prep.

DoorDash’s fundraising history is well-known but worth recalling sequentially.

Powered by WPeMatico

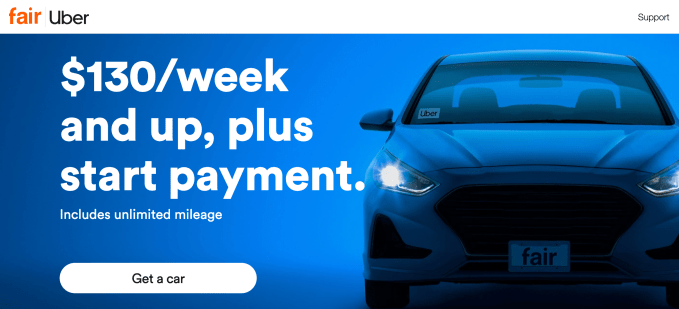

When Fair laid off 40% of its staff in October, CEO Scott Painter promised it wasn’t shuttering leasing services to on-demand fleets. But just one week later, Painter was removed as CEO and replaced in the interim with Adam Hieber, a CFA from Fair investor SoftBank. Today, according to two sources, Fair announced at an all-hands meeting that it would end its Fair Go program that helped Uber drivers lease cars. The program will cease in April. Uber now confirms the news to TechCrunch, and now Fair has directly confirmed the news to us as well.

“Due to an unexpected increase in insurance premiums that would have significantly raised prices for Fair’s rideshare drivers, we will wind down our weekly rideshare service over the coming months,” a spokesperson said. “We are working to minimize the disruption for Fair’s rideshare drivers, including notifying these customers of the status of their subscription in the coming weeks. We are working closely with Uber and exploring options with third parties to provide alternative customer mobility options to ensure a seamless transition for them, as well as continuity in Uber’s vehicle supply. We are thankful for our loyal Fair rideshare drivers and are disappointed we can no longer operate the business in a cost-effective way for our customers.”

Formerly valued at $1.2 billion after raising over $2 billion in equity and debt financing from SoftBank and Lightspeed, Fair laid off 40% of its staff in October. It had bought Uber’s XChange leasing program in early 2018. The deal lets drivers lease an Uber-eligible car with subscriptions to roadside assistance and maintenance for as low as $130 per week with a $500 start fee.

But Uber had sold the leasing program because it was unprofitable and adding to its losses at a tough time for the rideshare giant. As additional fees stacked up, Fair didn’t fare much better operating it.

A source tells us Fair Go was profitable. It was an important focus for the company as it retooled its subscription services for traditional drivers. Another source says at one point Fair Go was adding about 250 to 300 car leases per day and had thousands of active leases.

But Fair Go was facing higher insurance rates from carriers, which make sense since Uber drivers can be on the road far, far longer than traditional car owners.

Rather than trying to pass those fees along to drivers — many of whom are already cash-strapped — Fair told employees it would cease to lease to Uber drivers. That’s a respectable choice, since it could have pushed Uber drivers into debt if they didn’t fully comprehend what their total costs would be.

Attempts to reach Fair for comment were complicated by many of its in-house PR team being hit with October’s layoffs. An agency representative provided the statement above after publishing time.

An Uber spokesperson confirmed the shut down of Fair Go and their partnership, telling TechCrunch that “Unlocking options for vehicle access so drivers can earn with Uber remains a top priority. We’re thankful for Fair’s collaboration, and their contributions to our vehicle rental program. We’re continuing to invest in rental partnerships, and building more flexibility beyond hourly, weekly, and monthly options available today.”

Uber tells me it remains committed to offering rental options to drivers through partnerships with Hertz, Avis, ZipCar and Getaround, and they may be able to work with Uber drivers formerly leasing from Fair.

Painter kept a role as chairman of Fair.com when he stepped away from the CEO position at the end of October — a change we are still confirming is in place today. At the time of the layoffs in October, he maintained that the action was proactive, and not in response to SoftBank pressure.

“SoftBank is a big shareholder and supporting my focus, and that is the reality right now,” Painter said at the time. “Leaning on us is not the term,” he added in response to our questions of whether SoftBank pressured it to make these changes. “They are supporting us — there is a big difference,” he stressed.

The CEO change one week later, and today’s news about Fair Go, points to a different unfolding of events that speaks to the pressure SoftBank itself is under.

The news is the latest low point for the SoftBank portfolio in the wake of the WeWork implosion. That’s caused potential repeat LPs for SoftBank’s massive Vision Fund to tighten their purse strings and other late stage investors to focus on sustainable unit economics. Late-stage startups have been left scrambling to cut their burn rates, often through layoffs.

SoftBank’s portfolio, which may have trouble raising on good terms after what many saw as inflated valuations propped up by the megafund, has been hit the hardest. This week TechCrunch broke the news that Flexport was laying off 3% of staff, or 50 employees.

Other SoftBank-funded company layoffs include Zume Pizza (80% of staff laid off), Wag (80%), Getaround (25%), Rappi (6%), and Oyo (5%). There may be more to come: activist investor Elliott Management, which now owns more than $2.5 billion of SoftBank shares, has reportedly been in talks with the company over a range of issues including better corporate governance and more transparency and management around investments.

Updated with confirmation from Fair, and a correction that Uber will continue offering car rentals through partners but not leasing as we originally printed.

Powered by WPeMatico

Fearing weak fundraising options in the wake of the WeWork implosion, late stage startups are tightening their belts. The latest is another Softbank-funded company, joining Zume Pizza (80% of staff laid off), Wag (80%+), Fair (40%), Getaround (25%), Rappi (6%), and Oyo (5%) that have all cut staff to slow their burn rate and reduce their funding needs. Freight forwarding startup Flexport that is laying off 3% of its global staff.

“We’re restructuring some parts of our organization to move faster and with greater clarity and purpose. With that came the difficult decision to part ways with around 50 employees” a Flexport spokesperson tells TechCrunch after we asked today if it had seen layoffs like its peers.

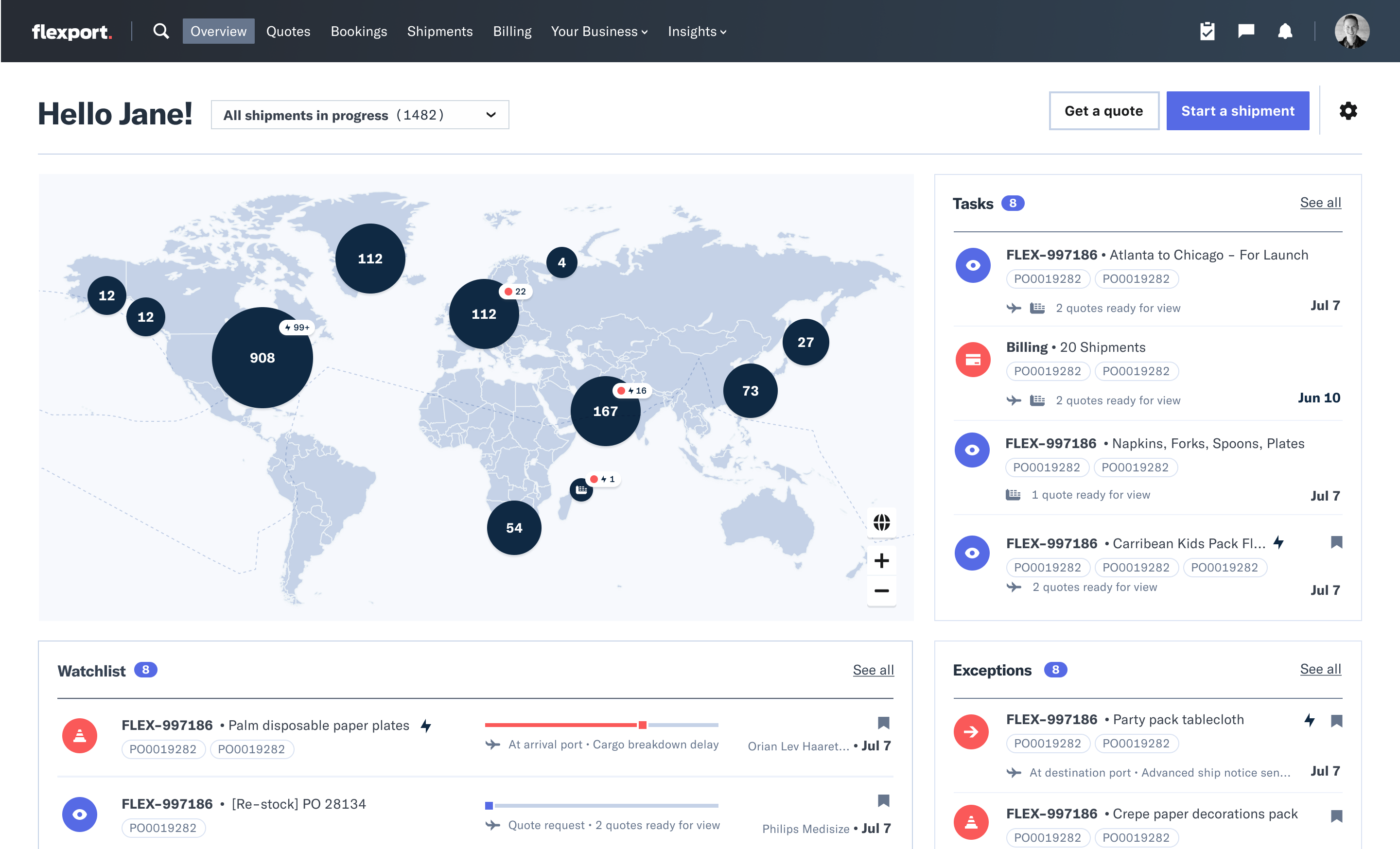

Flexport CEO Ryan Petersen

Flexport had raised a $1 billion Series D led by SoftBank at a $3.2 billion valuation a year ago, bringing it to $1.3 billion in funding. The company helps move shipping containers full of goods between manufacturers and retailers using digital tools unlike its old-school competitors.

“We underinvested in areas that help us serve clients efficiently, and we over-invested in scaling our existing process, when we actually needed to be agile and adaptable to best serve our clients, especially in a year of unprecedented volatility in global trade” the spokesperson explained.

Flexport still had a record year, working with 10,000 clients to finance and transport goods. The shipping industry is so huge that it’s still only the seventh largest freight forwarder on its top Trans-Pacific Eastbound leg. The massive headroom for growth plus its use of software to coordinate supply chains and optimize routing is what attracted SoftBank.

The Flexboard Platform dashboard offers maps, notifications, task lists, and chat for Flexport clients and their factory suppliers.

But many late-stage startups are worried about where they’ll get their next round after taking huge sums of cash from SoftBank at tall valuations. As of November, SoftBank had only managed to raise about $2 billion for its Vision Fund 2 despite plans for a total of $108 billion, Bloomberg reported. LPs were partially spooked by SoftBank’s reckless investment in WeWork. Further layoffs at its portfolio companies could further stoke concerns about entrusting it with more cash.

Unless growth stage startups can cobble together enough institutional investors to build big rounds, or other huge capital sources like sovereign wealth funds materialize for them, they might not be able to raise enough to keep rapidly burning. Those that can’t reach profitability or find an exit may face down-rounds that can come with onerous terms, trigger talent exodus death spirals, or just not provide enough money.

Flexport has managed to escape with just 3% layoffs for now. Being proactive about cuts to reach sustainability may be smarter than gambling that one’s business or the funding climate with suddenly improve. But while other SoftBank startups had to spend tons to edge out direct competitors or make up for weak on-demand service margins, Flexport at least has a tried and true business where incumbents have been asleep at the wheel.

Powered by WPeMatico

SoftBank wants its competing portfolio companies to stop losing so much money and, in some cases, to merge.

That’s the news out from Financial Times today, which reported that Uber and DoorDash discussed merging last year. The talks didn’t wind up in a deal.

The two companies, each heavily backed by SoftBank and its formerly active Vision Fund, compete in the food delivery space at great expense. Uber’s Eats business turned $392 million in adjusted net revenue in Q3 2019 into $316 million adjusted loss. That ocean of red ink actually makes DoorDash’s reported, projected $450 million 2019 operating loss look modest.

Perhaps by bringing the two companies together they would lose less money, and thus be in a better place to either return to their original IPO valuation or defend their existing private valuation.

Uber has famously struggled to retain value after its IPO, shedding worth during its public offering and since its debut. DoorDash, relatedly, was said to be in the market recently, but unable to close a new, large funding round. And as the two companies compete, a combination makes sense. Even more so when you consider their shared shareholder.

Uber and DoorDash aren’t the only examples of SoftBank-backed companies beating each other up with bricks of Vision Fund cash.

According to a report today in The Wall Street Journal, a fight in Latin America between several SoftBank-backed companies is raging:

Uber is under siege in Latin America amid a bruising price war where its ostensible rivals are Rappi and China’s Didi Chuxing Technology Co. But here’s the twist. All the combatants have as their biggest owner the same tech investor, Japan’s SoftBank Group Corp., which has injected a total of $20 billion into the three.

In the pre-unicorn era, you’ll recall the old venture maxim that no single group should invest in competing players. After all, why pay for one portfolio company to beat on another startup that you already helped finance? SoftBank, with its own investments and the Vision Fund, ignored that rule, and now it’s financing a fustercluck across the various American continents. (Though, there are some examples of other firms doing this, like Sequoia putting money into Uber and Didi.)

Which is why it might want DoorDash and Uber to link up. It might lessen one headache. Then SoftBank could work on figuring out how to keep Uber and Didi from beating each other up on rides in other markets, while disentangling Uber Eats and Rappi from a delivery scrap in yet more.

Perhaps SoftBank wants all the players to merge into a single, mega-delivery and ride corp. That would never pass regulatory oversight, of course, but at least it would centralize the losses and cash burn into a single income statement.

Think of the time it would save!

Powered by WPeMatico

Layoffs in the technology and venture-backed worlds continued today, as 23andMe confirmed to CNBC that it laid off around 100 people, or about 14% of its formerly 700-person staff. The cuts would be notable by themselves, but given how many other reductions have recently been announced, they indicate that a rolling round of belt-tightening amongst well-funded private companies continues. (TechCrunch confirmed the numbers with the company.)

Mozilla, for example, cut 70 staffers earlier this year. As TechCrunch’s Frederic Lardinois reported earlier in January, the company’s revenue-generating products were taking longer to reach market than expected. And with less revenue coming in than expected, its human footprint had to be reduced.

23andMe and Mozilla are not alone, however. Playful Studios cut staff just this week, 2019 itself saw more than 300% more tech layoffs than in the preceding year and TechCrunch has covered a litany of layoffs at Vision Fund-backed companies over the past few months, including:

Scooter unicorns Lime and Bird have also reduced staff this year. The for-profit drive is firing on all cylinders in the wake of the failed WeWork IPO attempt. WeWork was an outlier in terms of how bad its financial results were, but the fear it introduced to the market appears pretty damn mainstream by this point. (Forsake hope, alle ye whoe require a Series H.)

The money at risk, let alone the human cost, is high. Zume has raised more than $400 million. 23andMe has raised an even sharper $786.1 million. Rappi? How about $1.4 billion. And Oyo? $3.2 billion so far. Every company that loses money eventually dies. And every company that always makes money lives forever. It seems that lots of companies want to jump over the fence, make some money and rebuild investor confidence in their shares.

It’s just too bad that the rank-and-file are taking the brunt of the correction.

Powered by WPeMatico

As the global cybersecurity market becomes increasingly crowded, the Start Up Nation remains a bulwark of innovation and opportunity generation for investors and global cyber companies alike. It achieved this chiefly in 2019 by adapting to the industry’s competitive developments and pushing forward its most accomplished entrepreneurs in larger numbers to meet them.

New data illustrates how Israeli entrepreneurs have seized on the country’s reputation for building radically cutting-edge technologies as the number of new Israeli cybersecurity startups addressing nascent sectors eclipses its more traditional counterparts. Moreover, related findings highlight how cybersecurity companies looking to expand beyond their traditional offerings are entering Israel’s cybersecurity ecosystem in larger numbers through highly strategic acquisitions.

Broadly, new findings also reveal the Israeli cybersecurity market’s overall coming of age, seasoned entrepreneurial dominance and greater appetite for longer-term visions and strategies — the latter of which received record-breaking investor backing in 2019.

Powered by WPeMatico