Silicon Valley

Auto Added by WPeMatico

Auto Added by WPeMatico

There comes a time for many startup companies where they either realize they need to do a nationwide rollout, or they need to actively target buyers in the middle of the country. If you are a startup on either the East or the West Coasts, it’s worth thinking about how this market might present its own set of unique challenges, and how you plan to overcome them.

There are a lot of misconceptions about what some people call “flyover country,” and as a San Francisco native who spent two decades in New York, Washington DC, and Boston before moving to Pittsburgh, I can assure you they are almost all wrong. Without getting into specifics, the reality of “middle America” is that it’s the same as anywhere else.

Income, education, world view, and waistlines are all varied. It’s pretty accurate that San Francisco possesses a culture obsessed with fitness and entrepreneurship, but California isn’t necessarily all like that, and if you think it is, I encourage you to go to Bakersfield, the Central Valley, or Eureka sometime.

In addition, just because the stereotypes are wrong doesn’t mean there’s nothing different about doing business here. As you think about how to conduct your rollout, here are some things you should consider:

As with any market, research is key since it informs every other aspect of the rollout. Start by looking into who your competition is.

Since there are fewer VC-backed startups in middle America, and smaller companies tend to get less press, the research may be harder. However, there are some major universities that are actively putting money into their own Entrepreneurship programs and those spinoffs often do very well.

Powered by WPeMatico

Our 14th Annual TechCrunch Summer Party is a mere two weeks away, and we’re serving up a fresh new batch of tickets to this popular Silicon Valley tradition. Jump on this opportunity, folks, because our previous releases sold out in a flash — and these babies won’t last long, either. Buy your ticket today.

Our summer soiree takes place on July 25 at Park Chalet, San Francisco’s coastal beer garden. Picture it: A cold brew, an ocean view, tasty food and relaxed conversations with other amazing members of the early-startup tech community.

TechCrunch parties have a reputation as a place where startup magic happens. And there will be plenty of magical opportunity afoot this year as heavy-hitter VCs from Merus Capital, August Capital, Battery Ventures, Cowboy Ventures, Data Collective, General Catalyst and Uncork Capital join the party.

There’s more than one way to make magic at our summer fete. If you’re serious about catching the eye of these major VCs, consider buying a Startup Demo Package, which includes four attendee tickets.

Fun fact: Box founders Aaron Levie and Dylan Smith met one of their first investors, DFJ, at a party hosted by TechCrunch founder Michael Arrington. It’s one of our favorite success stories.

Check out the party details:

No TechCrunch party is complete without a chance to win great door prizes, including TechCrunch swag, Amazon Echos and tickets to Disrupt San Francisco 2019.

Buy your ticket today and enjoy a convivial evening of connection and community in a beautiful setting. Opportunity happens, and it’s waiting for you at the TechCrunch Summer Party.

Pro Tip: If you miss out this time, sign up here and we’ll let you know when we release the next group of tickets.

Is your company interested in sponsoring or exhibiting at the TechCrunch 14th Annual Summer Party? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico

After a decade in the peculiar world of venture capital, Andreessen Horowitz managing director Scott Kupor has seen it all when it comes to the dos and don’ts for dealing with Valley VCs and company building. In his new book Secrets of Sand Hill Road (available on June 3), Scott offers up an updated guide on what VCs actually do, how they think and how founders should engage with them.

TechCrunch’s Silicon Valley editor Connie Loizos will be sitting down with Scott for an exclusive conversation on Tuesday, June 4 at 11:00 am PT. Scott, Connie and Extra Crunch members will be digging into the key takeaways from Scott’s book, his experience in the Valley and the opportunities that excite him most today.

Tune in to join the conversation and for the opportunity to ask Scott and Connie any and all things venture.

To listen to this and all future conference calls, become a member of Extra Crunch. Learn more and try it for free.

Powered by WPeMatico

The San Francisco Bay Area is a global powerhouse at launching startups that go on to dominate their industries. For locals, this has long been a blessing and a curse.

On the bright side, the tech startup machine produces well-paid tech jobs and dollars flowing into local economies. On the flip side, it also exacerbates housing scarcity and sky-high living costs.

These issues were top-of-mind long before the unicorn boom: After all, tech giants from Intel to Google to Facebook have been scaling up in Northern California for over four decades. Lately however, the question of how many tech giants the region can sustainably support is getting fresh attention, as Pinterest, Uber and other super-valuable local companies embark on the IPO path.

The worries of techie oversaturation led us at Crunchbase News to take a look at the question: To what extent do tech companies launched and based in the Bay Area continue to grow here? And what portion of employees work elsewhere?

For those agonizing about the inflationary impact of the local unicorn boom, the data offers a bit of reassurance. While companies founded in the Bay Area rarely move their headquarters, their workforces tend to become much more geographically dispersed as they grow.

Just because a company is based in Northern California doesn’t mean most workers are there also. Headquarters, our survey shows, does not always translate into headcount.

“Headquarters location can often be the wrong benchmark to use to identify where employees are located,” said Steve Cadigan, founder of Cadigan Talent Ventures, a Silicon Valley-based talent consultancy. That’s particularly the case for large tech companies.

Among the largest technology employers in Northern California, Crunchbase News found most have fewer than 25 percent of their full-time employees working in the city where they’re headquartered. We lay out the details for 10 of the most valuable regional tech companies in the chart below.

With the exception of Intel, all of these companies have a double-digit percentage of employees at headquarters, so it’s not as if they’re leaving town. However, if you’re a new hire at Silicon Valley’s most valuable companies, it appears chances are greater that you’ll be based outside of headquarters.

Tesla, meanwhile, is somewhat of a unique case. The company is based in Palo Alto, but doesn’t crack the city’s list of top 10 employers. In nearby Fremont, Calif., however, Tesla is the largest city employer, with roughly 10,000 reportedly working at its auto plant there.(Tesla has about 49,000 employees globally.)

High-valuation private and recently public tech companies can also be pretty dispersed.

Although they tend to have a larger percentage of employees at headquarters than more-established technology giants, the unicorn crowd does like to spread its wings.

Take Uber, the poster child for this trend. Although based in San Francisco, the ride-hailing giant has fewer than one-fourth of its employees there. Out of a global workforce of around 22,300, only about 5,000 are SF-based.

It’s unclear if that kind of breakdown is typical. We had trouble assembling similar geographic employee counts at other Bay Area unicorns, mainly because cities break out numbers only for their 10 largest employers. The lion’s share of regional unicorns are San Francisco-based, and of them only Uber made the Top 10.

That said, there is another, rougher methodology for assessing who works at headquarters: job postings. At a number of the most valuable Bay Area-based unicorns — including Airbnb, Juul, Lime, Instacart, Stripe and the now-public Lyft — a high number of open positions are far from the home office. And as we wrote last year, private companies have been actively seeking out cities to set up secondary hubs.

Even for earlier-stage startups, it’s not uncommon to set up headquarters in the San Francisco area for access to financing and networking, while doing the bulk of hiring in another location, Cadigan said. The evolution of collaborative work tools has also enabled more companies to add staff working remotely or in secondary offices.

Plus, of course, unicorn startups tend to be national or global in focus, and that necessitates hiring where their customers are located.

As we wrap up, it’s worth bringing up how unusual it once was for denizens of a metro area to oppose a big influx of high-skill jobs. In the past couple of years, however, these attitudes have become more common. Witness Queens residents’ mixed reactions to Amazon’s HQ2 plans. And in San Francisco, a potential surge of newly minted IPO millionaires is causing some consternation among locals, along with jubilation among the realtor crowd.

Just as college towns retain room for new students by graduating older ones, however, it seems reasonable that sustaining Northern California’s strength as a startup hub requires locating jobs out-of-area as companies scale. That could be good news for other cities, including Austin, Phoenix, Nashville, Portland and others, which have emerged as popular secondary locations for fast-growing unicorns.

That said, we’re not predicting near-term contraction in Bay Area tech employment, particularly of the startup variety. The region’s massive entrepreneurial and venture ecosystem keeps on producing valuable newcomers well-capitalized to keep hiring.

Methodology

We looked only at employment at company headquarters (except for Apple) . Companies on the list may have additional employees based in other Northern California cities. For Apple, we included all Silicon Valley employees, per estimates by the Silicon Valley Business Journal.

Numbers are rounded to the nearest hundred for the largest employers. Most of the data is for full-time employees only. Large tech employers hire predominantly full-time for staff positions, so part-time, whether included or not, is expected to reflect only a very small percentage of employment.

Cities list their 10 largest employers in annual reports. We used either the annual reports themselves or data excerpted in Wikipedia, using calendar year 2017 or 2018.

Powered by WPeMatico

For a long time, it was the norm for founders to haul their hardware to the 3000 block of Sand Hill Road, where the venture capitalists of “Silicon Valley” would be awaiting their pitches. Today, many of the investors that touted the exclusivity of “The Valley” have moved north to San Francisco, where they have better access to top entrepreneurs.

Y Combinator, a Silicon Valley institution and to many the lifeblood of the startups and venture capital ecosystem, is the latest to pack up shop. YC, which invests $150,000 for 7 percent equity in a few hundred startups per year, is currently searching for a space in SF to operate its accelerator program, sources close to YC confirm to TechCrunch, because the majority of YC’s employees and its portfolio founders reside in the city.

Founded in 2005, YC’s roots are in Mountain View, California. In its first four years, YC offered programs in Cambridge, Massachusetts and Mountain View before opting in 2009 to focus exclusively on The Valley. In late 2013, as more and more of its partners and portfolio companies were establishing themselves in SF, YC opened a satellite office in the city in what would be the beginning of its journey northbound.

The small satellite office, used to support SF-based staff and provide portfolio companies resources and workspace, is located in Union Square. The fate of YC’s Mountain View office is unclear.

YC’s move north will be the latest in a series of small changes that, together, point to a new era for the accelerator. Approaching its 15th birthday, YC announced in September it was changing up the way it invests. No longer would it seed startups with $120,000 for 7 percent equity, it would give startups an additional 30,000 to cover the expenses of getting a business off the ground and it would admit a whole lot more companies.

YC began mentoring its largest cohort of companies to date in late 2018. The astonishing 200-plus group in its winter 2019 batch is more than 50 percent larger than the 132-team cohort that graduated in spring 2018. To accommodate the truly gigantic group at YC Demo Days later this month (March 18 and 19), YC has moved to a new venue, SF’s Pier 48. Historically, YC Demo Days were hosted at the Computer History Museum near its home in Mountain View.

YC has also ditched “Investor Day,” which is typically an opportunity for investors to schedule meetings with startups that just completed the accelerator program. YC writes that the decision came “after analyzing its effectiveness.” On top of that, rumors suggest YC is planning to put an end to Demo Days. Other accelerators, AngelPad for example, put a stop to the tradition last year after realizing demo day was more of a stress to startup founders than a resource. Sources close to YC, however, tell TechCrunch these rumors are categorically false.

YC isn’t the first accelerator to ditch its Silicon Valley digs. 500 Startups, a smaller yet still prolific accelerator, opened an SF satellite office the same year as YC, and in 2018, the nine-year-old program made the decision to permanently relocate to SF. Venture capital firms, too, have realized the opportunities are larger in SF than on Sand Hill Road.

The transition from the peninsula to the city began around 2012, when VC heavyweights like Uber and Twitter-backer Benchmark opened an office in SF’s mid-market neighborhood. Months later, 47-year-old Kleiner Perkins, an investor in Stripe and DoorDash, opened the doors to its new workplace in SF’s South Park neighborhood.

Around that same time a whole bunch of firms followed suit: Shasta Ventures, Norwest Venture Partners, Accel, GV, General Catalyst and NEA opened SF shops, to name a few. Many of these firms, Benchmark, Kleiner and Accel, for example, held onto their Silicon Valley locations. Firms like True Ventures and Peter Thiel’s Founders Fund planted stakes in SF years prior. Both firms have operated SF offices since 2005; True Ventures, for its part, has managed a Palo Alto office from the get-go, as well.

“When we first started, it was [expected] that it would be maybe 60-40 Peninsula to the city; it’s actually turned out to be 80-20 SF to The Valley,” True Ventures co-founder Phil Black told TechCrunch. “For us, it was important to be near our customer: the founder. It’s important for us to be in and around where founders are doing their things.”

The transition out of The Valley is ongoing. Other VC funds are still in the process of opening their first SF offices as more partners beg for shorter commutes. Khosla Ventures, for example, is currently searching for an SF headquarters.

Silicon Valley real estate will likely remain a hot — or warm, at least — commodity, however. Why? Because long-time investors have lives established in that part of the bay, where they’ve built homes in well-kept, affluent cities like Woodside, Atherton and Los Altos.

Still, Y Combinator’s move highlights an increasingly adopted mantra: Silicon Valley isn’t the goldmine it used to be. For the best deals and greatest access to entrepreneurs, SF takes the cake — for now, that is. But with rising rents and a changing attitude toward geographically diverse founders, how long SF will remain the destination for top talent is an entirely different question.

Powered by WPeMatico

In the days leading up to TechCrunch Disrupt SF 2018, The Economist published the cover story, ‘Why Startups Are Leaving Silicon Valley.’

The author outlined reasons why the Valley has “peaked.” Venture capital investors are deploying capital outside the Bay Area more than ever before. High-profile entrepreneurs and investors, Peter Thiel, for example, have left. Rising rents are making it impossible for new blood to make a living, let alone build businesses. And according to a recent survey, 46 percent of Bay Area residents want to get the hell out, an increase from 34 percent two years ago.

Needless to say, the future of Silicon Valley was top of mind on stage at Disrupt.

“It’s hard to make a difference in San Francisco as a single entrepreneur,” said J.D. Vance, the author of ‘Hillbilly Elegy’ and a managing partner at Revolution’s Rise of the Rest Fund, which backs seed-stage companies based outside Silicon Valley. “It’s not as a hard to make a difference as a successful entrepreneur in Columbus, Ohio.”

In conversation with Vance, Revolution CEO Steve Case said he’s noticed a “mega-trend” emerging. Founders from cities like Pittsburgh, Detroit or Portland are opting to stay in their hometowns instead of moving to U.S. innovation hubs like San Francisco.

“The sense that you have to be here or you can’t play is going to start diminishing.”

“We are seeing the beginnings of a slowing of what has been a brain drain the last 20 years,” Case said. “It’s not just watching where the capital flows, it’s watching where the talent flows. And the sense that you have to be here or you can’t play is going to start diminishing.”

J.D. Vance says that most entrepreneurs don’t need to move to Silicon Valley.

Here’s why. #TCDisrupt pic.twitter.com/0mFPeTuHLe

— TechCrunch (@TechCrunch) September 6, 2018

Farewell, San Francisco

“It’s too expensive to live here,” said Aileen Lee, the founder of seed-stage VC firm Cowboy Ventures, amid a conversation with leading venture capitalists Spark Capital general partner Megan Quinn and Benchmark general partner Sarah Tavel .

“I know that there are a lot of people in the Bay Area that are trying to work on that problem and I hope that they are successful,” Lee added. “It’s an amazing place to live and we’ve made it really challenging for people to live here and not worry about making ends meet.”

One of Cowboy’s portfolio companies opted to relocate from Silicon Valley to Colorado when it came time to scale their business. That kind of move would’ve historically been seen as a failure. Today, it may be a sign of strong business acumen.

Quinn said that of all 28 of Spark’s growth-stage portfolio companies, Raleigh, North Carolina-based Pendo has the easiest time recruiting folks locally and from the Bay Area.

She advises her Bay Area-based late-stage companies to open a second office outside of the Valley where lower-cost talent is available.

“We often say go to [flySFO.com], draw a three-hour circle around San Francisco where they have direct flights, find a city that has a university and open up a second office as quickly as possible,” Quinn said.

Still, all three firms invest in a lot of companies based in San Francisco. Of Benchmark’s 10 most recent investments, for example, eight were based in SF, according to Crunchbase.

“I used to believe really strongly if you wanted to build a multi-billion dollar company you had to be based here,” Tavel said. “I’ve stopped giving that soap speech.”

Aileen Lee (Cowboy Ventures), Megan Quinn (Spark Capital), and Sarah Tavel (Benchmark Capital) on whether or not Silicon Valley is on the wane for investors #TCDisrupt pic.twitter.com/SOpn7p0eNQ

— TechCrunch (@TechCrunch) September 5, 2018

Underestimated talent

A lot of Bay Area VCs have been blind to the droves of tech talent located outside the region. Believe it or not, there are great engineers in America’s small- and medium-sized markets too.

At Disrupt, Backstage Capital founder Arlan Hamilton announced the firm would launch an accelerator to further amplify companies led by underestimated founders. The program will have cohorts based in four cities; San Francisco was noticeably absent from that list.

Instead, the firm, which invests in underrepresented founders and recently raised a $36 million fund, will work with companies in Philadelphia, Los Angeles, London and one more city, which will be determined by a public vote. Aniyia Williams, the founder of Tinsel and Black & Brown Founders, will spearhead the Philadelphia effort.

“For us, it’s about closing that wealth gap to address inequity in tech,” Williams said. “There needs to be more active participation from everyone.”

Hamilton added that for her, the tech talent in LA and London is undeniable.

“There is a lot of money and a lot of investors … it reminds me of three years ago in Silicon Valley,” Hamilton said.

Silicon Valley vs. China

Silicon Valley’s demise may not be just as a result of increased costs of living or investors overlooking talent in other geographies. It may be because of heightened competition abroad.

Doug Leone, an early- and growth-stage investor at Sequoia Capital, said at Disrupt that he’s noticed a very different work ethic in China.

Chinese entrepreneurs, he explained, are more ruthless than their American counterparts and they’re putting in a whole lot more hours.

Doug Leone of Sequoia Capital says founders in the US and China both want to change the world, but Chinese founders are a little more desperate (and you see it in the crazy work ethic they have).#TCDisrupt pic.twitter.com/dPxsRTbJoq

— TechCrunch (@TechCrunch) September 6, 2018

“I’ve had dinner in China until after 10 p.m. and people go to work after 10 p.m.,” Leone recalled.

“We don’t see that in the U.S. I’m not saying the U.S. founders oughta do that but those are the differences. They are similar in character. They are similar in dreams. They are similar in how they want to change the world. They are ultra-driven … The Chinese founders have a half other gear because I think they are a little more desperate.”

Much of this, however, has been said before and still, somehow, Silicon Valley remained the place to be for investors and startup entrepreneurs.

The reality is, those engaged in tech culture are always anxiously awaiting for the bubble to pop, the market to crash and for “peak Valley” to finally arrive.

Maybe, just maybe, Silicon Valley is forever.

Here’s more of our coverage of Disrupt 2018.

Powered by WPeMatico

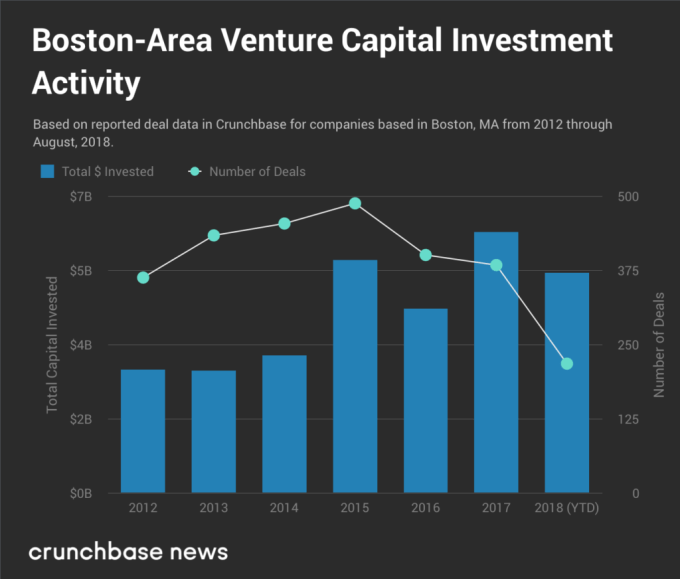

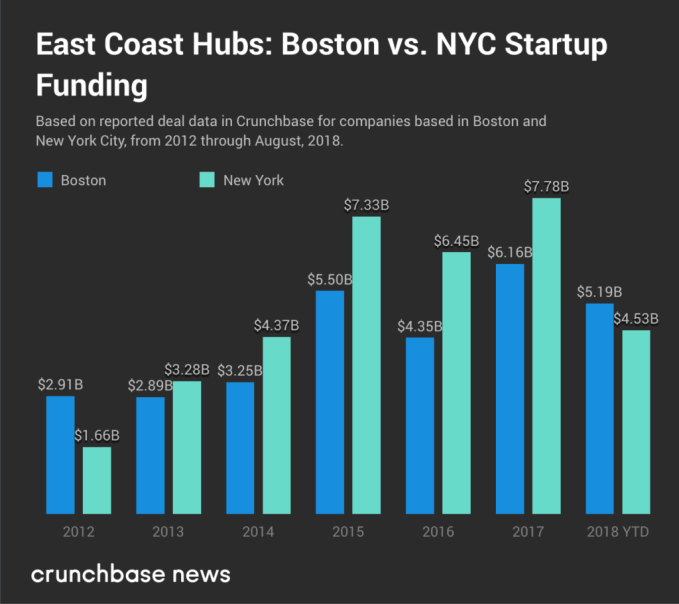

Boston has regained its longstanding place as the second-largest U.S. startup funding hub.

After years of trailing New York City in total annual venture investment, Massachusetts is taking the lead in 2018. Venture investment in the Boston metro area hit $5.2 billion so far this year, on track to be the highest annual total in years.

The Massachusetts numbers year-to-date are about 15 percent higher than the New York City total. That puts Boston’s biotech-heavy venture haul apparently second only to Silicon Valley among domestic locales thus far this year. And for New England VCs, the latest numbers also confirm already well-ingrained opinions about the superior talents of local entrepreneurs.

“Boston often gets dismissed as a has-been startup city. But the successes are often overlooked and don’t get the same attention as less successful, but more hypey companies in San Francisco,” Blake Bartlett, a partner at Boston-based venture firm OpenView, told Crunchbase News. He points to local success stories like online prescription service PillPack, which Amazon just snapped up for $1 billion, and online auto marketplace CarGurus, which went public in October and is now valued around $4.7 billion.

Meanwhile, fresh capital is piling up in the coffers of local startups with all the intensity of a New England snowstorm. In the chart below, we look at funding totals since 2012, along with reported round counts.

In the interest of rivalry, we are also showing how the Massachusetts startup ecosystem compares to New York over the past five years.

So what’s the reason for Boston’s 2018 successes? It’s impossible to pinpoint a single cause. The New England city’s startup scene is broad and has deep pockets of expertise in biotech, enterprise software, AI, consumer apps and other areas.

Still, we’d be remiss not to give biotech the lion’s share of the credit. So far this year, biotech and healthcare have led the New England dealmaking surge, accounting for the majority of invested capital. Once again, local investors are not surprised.

“Boston has been the center of the biotech universe forever,” said Dylan Morris, a partner at Boston and Silicon Valley-based VC firm CRV. That makes the city well-poised to be a leading hub in the sector’s latest funding and exit boom, which is capitalizing on a long-term shift toward more computational approaches to diagnosing and curing disease.

Moreover, it goes without saying that the home city of MIT has a particularly strong reputation for so-called deep tech — using really complicated technology to solve really hard problems. That’s reflected in the big funding rounds.

For instance, the largest Boston-based funding recipient of 2018, Moderna Therapeutics, is a developer of mRNA-based drugs that raised $625 million across two late-stage rounds. Besides Moderna, other big rounds for companies with a deep tech bent went to TCR2, which is focused on engineering T cells for cancer therapy, and Starry (based in both Boston and New York), which is deploying the world’s first millimeter wave band active phased array technology for consumer broadband.

Other sectors saw some jumbo-sized rounds too, including enterprise software, 3D printing and even apparel.

Boston also benefits from the rise of supergiant funding rounds. A plethora of rounds raised at $100 million or more fueled the city’s rise in the venture funding rankings. So far this year, at least 15 Massachusetts companies have raised rounds of that magnitude or more, compared to 12 in all of 2017.

Boston companies are going public and getting acquired at a brisk pace too this year, and often for big sums.

At least seven metro-area startups have sold for $100 million or more in disclosed-price acquisitions this year, according to Crunchbase data. In the lead is online prescription drug service PillPack . The second-biggest deal was Kensho, a provider of analytics for big financial institutions that sold to S&P Global for $550 million.

IPOs are huge, too. A total of 17 Boston-area venture-backed companies have gone public so far this year, of which 15 are life science startups. The largest offering was for Rubius Therapeutics, a developer of red cell therapeutics, followed by cybersecurity provider Carbon Black.

Meanwhile, many local companies that went public in the past few years have since seen their values skyrocket. Bartlett points to examples including online retailer Wayfair (market cap of $10 billion), marketing platform HubSpot (market cap $4.8 billion) and enterprise software provider Demandware (sold to Salesforce for $2.8 billion).

Recollections of a frigid April sojourn in Massachusetts are too fresh for me to comfortably utter the phrase “Boston is hot.” However, speaking purely about startup funding, and putting weather aside, the Boston scene does appear to be seeing some real escalation in temperature.

Of course, it’s not just Boston. Supergiant venture funds are surging all over the place this year. Morris is even bullish on the arch-rival a few hours south: “New York and Boston love to hate each other. But New York’s doing some amazing things too,” he said, pointing to efforts to invigorate the biotech startup ecosystem.

Still, so far, it seems safe to say 2018 is shaping up as Boston’s year for startups.

Powered by WPeMatico

Silicon Valley, for better and oftentimes worse, provides an uncanny valley view of the ups and downs of IRL Silicon Valley.

The HBO series has shown what it’s like to deal with an incumbent who steals an idea or IP, the humiliation of saving the day, only to be fired as CEO by your VC, or the fear and exhilaration of competing on the Startup Battlefield stage — a familiar spot for those who have been to Disrupt.

TechCrunch is helping create another Silicon Valley meta moment. Silicon Valley co-creator Mike Judge will join us on stage at TC Disrupt SF.

Interestingly, Judge joined a team from HBO at Disrupt well before Silicon Valley ever aired, doing research for the then-forthcoming series. And, of course, Season 1 ended with the Startup Battlefield stage.

The cycle continued in 2016, when Judge came on stage to discuss what it’s like to parody Silicon Valley culture.

And round and round we go.

Judge has been in the entertainment industry for a long time, creating Beavis and Butt-head, co-creating King of the Hill, and serving as writer and director for classic films like Office Space and Idiocracy.

As Silicon Valley heads into its sixth season, we’re excited to chat with Judge about the direction of the show and the evolution of the media industry as a whole.

And hey, maybe we’ll hear a few spoilers for the upcoming season.

Tickets to the Disrupt SF 2018 are available right here.

Powered by WPeMatico

America’s mayors have spent the past nine months tripping over each other to curry favor with Amazon.com in its high-profile search for a second headquarters.

More quietly, however, a similar story has been playing out in startup-land. Many of the most valuable venture-backed companies are venturing outside their high-cost headquarters and setting up secondary hubs in smaller cities.

Where are they going? Nashville is pretty popular. So is Phoenix. Portland and Raleigh also are seeing some jobs. A number of companies also have a high number of remote offerings, seeking candidates with coveted skills who don’t want to relocate.

Those are some of the findings from a Crunchbase News analysis of the geographic hiring practices of U.S. unicorns. Since most of these companies are based in high-cost locations, like the San Francisco Bay Area, Boston and New York, we were looking to see if there is a pattern of setting up offices in smaller, cheaper cities. (For more on survey technique, see Methodology section below.)

Here is a look at some of the hotspots.

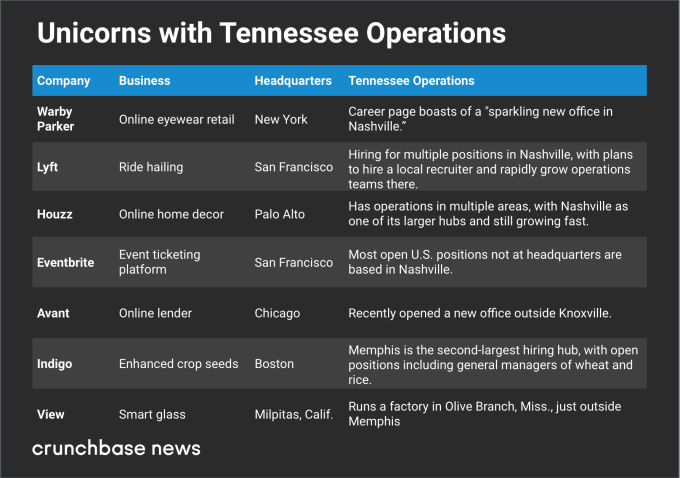

One surprise finding was the prominence of Nashville among secondary locations for startup offices.

We found at least four unicorns scaling up Nashville offices, plus another three with growing operations in or around other Tennessee cities. Here are some of the Tennessee-loving startups:

When we referred to Nashville’s popularity with unicorns as surprising, that was largely because the city isn’t known as a major hub for tech startups or venture funding. That said, it has a lot of attributes that make for a practical and desirable location for a secondary office.

Nashville’s attractions include high quality of life ratings, a growing population and economy, mild climate and lots of live music. Home prices and overall cost of living are also still far below Silicon Valley and New York, even though the Nashville real estate market has been on a tear for the past several years. An added perk for workers: Tennessee has no income tax on wages.

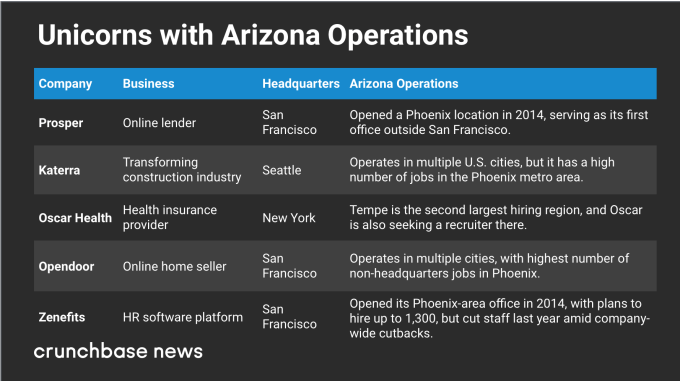

Phoenix is another popular pick for startup offices, particularly West Coast companies seeking a lower-cost hub for customer service and other operations that require a large staff.

In the chart below, we look at five unicorns with significant staffing in the desert city:

Affordability, ease of expansion and a large employable population look like big factors in Phoenix’s appeal. Homes and overall cost of living are a lot cheaper than the big coastal cities. And there’s plenty of room to sprawl.

One article about a new office opening also cited low job turnover rates as an attractive Phoenix-area attribute, which is an interesting notion. Startup hubs like San Francisco and New York see a lot of job-hopping, particularly for people with in-demand skill sets. Scaling companies may be looking for people who measure their job tenure in years rather than months.

Nashville and Phoenix aren’t the only hotspots for unicorns setting up secondary offices. Many other cities are also seeing some scaling startup activity.

Let’s start with North Carolina. The Research Triangle region is known for having a lot of STEM grads, so it makes sense that deep tech companies headquartered elsewhere might still want a local base. One such company is cybersecurity unicorn Tanium, which has a lot of technical job openings in the area. Another is Docker, developer of software containerization technology, which has open positions in Raleigh.

The Orlando metro area stood out mostly due to Robinhood, the zero-fee stock and crypto trading platform that recently hit the $5 billion valuation mark. The Silicon Valley-based company has a significant number of open positions in Lake Mary, an Orlando suburb, including HR and compliance jobs.

Portland, meanwhile, just drew another crypto-loving unicorn, digital currency transaction platform Coinbase. The San Francisco-based company recently opened an office in the Oregon city and is currently in hiring mode.

But you don’t have to be anywhere in particular to score jobs at many fast-growing startups. A lot of unicorns have a high number of remote positions, including specialized technical roles that may be hard to fill locally.

GitHub, which makes tools developers can use to collaborate remotely on projects, does a particularly good job of practicing what it codes. A notable number of engineering jobs open at the San Francisco-based company are available to remote workers, and other departments also have some openings for telecommuters.

Others with a smattering of remote openings include Silicon Valley-based cybersecurity provider CrowdStrike, enterprise software developer Apttus and also Docker.

Of course, not every unicorn is opening large secondary offices. Many prefer to keep staff closer to home base, seeking to lure employees with chic workplaces and lavish perks. Other companies find that when they do expand, it makes strategic sense to go to another high-cost location.

Still, the secondary hub phenomenon may offer a partial antidote to complaints that a few regions are hogging too much of the venture capital pie. While unicorns still overwhelmingly headquarter in a handful of cities, at least they’re spreading their wings and providing more jobs in other places, too.

For this analysis, we were looking at U.S. unicorns with secondary offices in other North American cities. We began with a list of 125 U.S.-based companies and looked at open positions advertised on their websites, focusing on job location.

We excluded job offerings related to representing a local market. For instance, a San Francisco company seeking a sales rep in Chicago to sell to Chicago customers doesn’t count. Instead, we looked for openings for team members handling core operations, including engineering, finances and company-wide customer support. We also excluded secondary offices outside of North America.

Additionally, we were looking principally for companies expanding into lower-cost areas. In many cases, we did see companies strategically adding staff in other high-cost locations, such as New York and Silicon Valley.

A final note pertains to Austin, Texas. We did see several unicorns based elsewhere with job openings in Austin. However, we did not include the city in the sections above because Austin, although a lower-cost location than Silicon Valley, may also be characterized as a large, mature technology and startup hub in its own right.

Powered by WPeMatico

New York City is a marvel of infrastructure planning and engineering. There are the visible landmarks — the Brooklyn Bridge, the Lincoln Tunnel, the Empire State Building — and also the invisible ones that run the city beneath its crowded streets, such as one of the world’s most complex water tunneling and reservoir systems. That infrastructure was built for the economy of the 20th century, a market that emphasized the manufacturing and trading of goods.

Infrastructure though has a very different meaning in the 21st century. The digital economy means we no longer measure the movement of products simply as tonnage on freight ships and trucks, but rather as bits and bytes flowing from data centers to devices. The shipping container once revolutionized 20th century global trade, and now containerization is revolutionizing the way we think about delivering applications to end users.

While New York has more Fortune 500 companies than any other state, to date it hasn’t been a global leader in startups compared to hotspots like the Bay Area, particularly in the sorts of enterprise and data infrastructure startups that undergird the internet revolution.

That situation is rapidly changing. Today, New York City has numerous unicorns targeting the enterprise, and a large number of up-and-coming winners like Datadog that are commanding substantial market share. But what is truly exciting — and different from past prognostications about the success of enterprise in New York — is that we are now seeing the rise of a generation of hundreds of startups that are deeply technical and deeply committed to building the future of enterprise infrastructure and applications.

Today, TechCrunch presents a special report on the state of enterprise startups in New York City. My colleague Ron Miller and I interviewed dozens of people, and we boiled down their thoughts and insights into this series of articles. We purposely brought out focus away from the pure SaaS application world, and instead tried to go deeper into the infrastructure and security startups that are increasingly powering and protecting our internet services.

This article provides an overview of the changing exit environment for startups in NYC, the rise of a set of mafias which are incubating startups, and the changing culture of customers and how that is assisting NYC startups with their competition out west.

We then have a series of profile pieces on early but burgeoning startups: DNS provider NS1, time series database Timescale, bare metal cloud Packet, data privacy BigID, cloud monitoring Datadog, and a trio of security startups: cybersecurity analytics Security Scorecard, graph-based security ops Uplevel Security, and decentralized authentication HYPR. Finally, we put together a gallery of enterprise startups we think are going to be making waves in the coming years.

One of the on-going criticisms of the New York City startup ecosystem has been its lack of exits. Despite being a technology epicenter and a hub for some of the world’s largest and richest companies, the actual track record of startups in the city has never measured up. That’s a massive problem, since exits aren’t just trophies to put on the wall. Rather, they’re the generators of wealth which can be transformed into the lifeblood for the next generation of startups.

The exit environment in New York has started to look much better in recent years though, particularly in the enterprise space over the past year. Yext, which manages online reputation for brands, debuted on the NYSE last year and now sits at a $1.28 billion market cap. MongoDB went public late last year, and is just shy of a $2 billion valuation. Flatiron Health, which applies data analytics to cancer research, was acquired by Roche for $1.9 billion two months ago. Moat, an ad measurement company, was purchased by Oracle for $850 million last year.

Those are some hefty exits over just a couple of months, but the real depth of the NYC ecosystem can be witnessed in the startups right behind them that are becoming market leaders. Those companies include AppNexus, Datadog, UiPath, Dataminr, Sprinklr, InVision, Digital Ocean, Percolate, Namely, Compass, Infor, Zeta Global, Greenhouse, WeWork and the list continues. Together, these companies have raised billion of dollars in venture capital funding according to Crunchbase.

What’s different for New York than in the past is that the city is no longer relying on one company as the leading light that will prove the worth of the rest of the ecosystem. As we interviewed investors and founders about what companies they thought were going to be the most notable in the years ahead, what was illuminating was just how little overlap there existed between their answers. There is truly a cohort of strong startups coming of age in the city, and that gives the ecosystem much more vitality than it has ever seen before.

New York is increasingly a mafia town, and that’s a good thing.

One of Silicon Valley’s biggest advantages has been the constant renewal of its startup talent. People join startups, learn the ropes from experienced founders, meet other talented employees, and eventually decide to spin out on their own and build their startup dreams. Some companies have become so well known for this pattern that the networks they have formed are known as mafias. The PayPal mafia is perhaps the most famous example, but there are many other companies in the Valley that have become boot camps for the next generation of founders.

New York may be more notorious for its occasionally violent, often Italian mafias, but today the city is also home to a growing network of startup mafias who are building companies and firms and powering the ecosystem.

Take Voxel. The company, which was formed in New York City in 1999, built enterprise hosting solutions for customers around the world. It was acquired by Internap in 2012, in an all-cash transaction valued at $30 million.

That’s a pretty small exit by startup standards, but despite its small size, it has created an entire generation of NYC enterprise startup founders. Voxel CEO and founder Raj Dutt ended up starting Grafana, an open source time series analytics platform. Voxel COO Zac Smith left to start Packet, and Voxel principal software architect Kris Beevers started NS1.

Another stylized example is Gilt Groupe. Security Scorecard founders Sam Kassoumeh and Aleksandr Yampolskiy met at Gilt when they became the first two hires for the security team there. Yampolskiy had never heard of the company before, but “my wife was apparently a customer, so maybe I would get some clothes discounts.” When Sam showed up at noon in a sweatshirt on his first day, “I was like, I am going to fire this guy,” he said.

In the end, the two got along, and they eventually left to found Security Scorecard, which has raised more than $62 million in venture capital according to Crunchbase from a long list of luminary Valley-based investors.

The examples are endless. Edward Chiu, the founder of Catalyst, learned customer success at Digital Ocean, and ended up realizing that the company’s internal tooling could be externalized as a startup. Liz Maida, the founder of Uplevel Security, learned her trade at internet traffic juggernaut Akamai, and has taken several of the product lessons she learned there to heart. Timber.io founders Zach Sherman and Ben Johnson met at SeatGeek, where they realized that logging could be made significantly better. The networks each of these bought along helped in building their startups.

Of course, all of these are anecdotes, and it is next to impossible to systematically analyze these movements. Yet, these patterns of entrepreneurs and investors have become much more visible in the ecosystem. Startup talent is increasingly begetting startup talent, spinning out and circulating their knowledge.

But beyond these clusters of individuals lie the glue that is holding the ecosystem together: Jonathan Lehr and his team at Work-Bench and Ed Sim and Eliot Durbin at Boldstart. All three of them made the bet years ago that New York City would become an epicenter of the enterprise infrastructure software industry. Now they are reaping the rewards of those bets.

Work-Bench is both a workspace and a fund, but its core value is the community that’s been built around it. Lehr founded the New York Enterprise Tech Meetup, which hosts at Work-Bench a monthly gathering of hundreds of participants in the enterprise space, from founders to customers.

He has also built up a wide network of potential customers across industries to accelerate the early sales of his startups. “We are not just sending intros, we can backchannel which can save a lot of time” for founders, Lehr said. For instance, if a customer can’t deploy an application for another year because of internal politics, Lehr can figure that out and tell his founders that information, saving them time on a sale that might not come to fruition.

For Sim at Boldstart, the message is much the same. When he first launched the seed fund with Durbin in 2010, people thought that “there aren’t going to be enough deals to be done,” he said. “We thought of it as an experiment,” and the two raised only $1 million to get started. Now the fund has raised its third vehicle of $47 million, and plays a convening in engaging West Coast VCs. “On the West Coast, what [founders] really want is access to customers,” Sim explained “and on the East Coast, they want access to West Coast VCs.” Those West Coast VCs are showing up in New York these days more and more. “Every week there are five different firms sitting in our office trying to figure out what is happening in New York.”

Startup ecosystems take off when there is a sufficient density of talent, a strong desire to help one another, and an open ambition to compete. New York City has never lacked the latter, but it has been missing out on a dense network of helpful and experienced startup hands. The rise of mafias centered on some of the city’s leading companies as well as the development of community hubs for support are adding the final ingredients for a world-class ecosystem.

In the classic text Regional Advantage, AnnaLee Saxenian analyzed the cultural differences between innovation on the East Coast, epitomized by Boston’s Route 128, and the culture of Silicon Valley. She found that the East Coast was stodgy, hierarchical, and centralized around large corporate behemoths like DEC and EMC. In contrast, the West Coast was nimble, networked, and decentralized, with little social hierarchy.

Silicon Valley was believed to be dead in the early 1990s, outcompeted by Asian tigers like Singapore, Taiwan, and Korea in manufacturing the chips that gave the region its name. The Valley was saved in just the nick of time by the opening of the internet to commercial activity, and the culture of the West Coast would prove perfectly attuned to the frenetic pace of innovation that followed. The Valley swept the internet economy, and many of the world’s most important tech companies are now located in the Bay Area.

That Silicon Valley innovation culture is now been exported around the world, and that is no less true walking around New York City startup neighborhoods like the Flatiron and Union Square. It’s not just the obvious sartorial changes that have made the city more relaxed and creative. It’s also the changing personality of the people who are successful here — the finance major is now the computer science graduate.

New York’s startup culture isn’t just a transplant of the Valley’s however, but rather an evolution of it. The pure excitement of tech that can be found at San Francisco meetups is much more muted here. Instead, there is a greater focus on investing in product design by listening to customers earlier and much more closely.

That’s only possible though because customers actually want to talk. The success of New York City’s enterprise startups rests in large part on the changing nature of purchasing at Fortune 500 companies.

Lehr of Work-Bench should know. Prior to starting the fund, he evaluated potential technology vendors at Morgan Stanley. “The adage that you don’t get fired for buying IBM had longed passed,” Lehr explained. Companies have vexing problems, and they are increasingly willing to experiment with startup technology if it has the potential to solve those issues.

The West Coast culture of flexible decision-making has entered the corporate world. CIOs used to have a vice grip on technology purchasing, but now leaders across the enterprise increasingly make their own independent decisions. Lehr said that “you now need to know, as a startup, nuanced different people in enterprise, and as a VC, to stay relevant, you don’t just want to know the CIO or CTO, but the 30 other people who have pain points” across a company.

Sim at Boldstart noted “The last thing heads of IT want is salespeople in front of them. You are not selling anything because they don’t want to buy anything.” Instead, “they are willing to work with startups if you have the right … service partnership mentality,” he said.

With customers increasingly engaged, proximity has become a major boon for startups in NYC. “In the early days before you are ready to scale, it is all about relationships in the enterprise,” Lehr explained. He described the thinking of customers today looking at buying from startups. “I can trust these people to get me promoted, and they are in New York, and they can give me feedback.”

I heard this point made from nearly every person I talked to. Roman Chwyl, a sales executive with experience at AWS, Google, and IBM, noted that when it comes to customers, “We can probably do six meetings a day up and down a subway line.” That thinking was mirrored by George Avetisov, the CEO of HYPR, who said that “All of our customers are in a 10 mile radius” because of the company’s focus on financial institutions.

That customer-centric view is what has made Datadog, which is now north of $100 million in annual recurring revenue, so competitive. Olivier Pomel, the CEO and founder, said that “Mostly what is interesting is that we’re not overwhelmed by the 5,000 startups around us” like in the Valley, and “what we hear is more clearly the message from the customers and the market.” He noted that “For most of the people at Datadog, their significant others are not in tech,” and that means reality doesn’t get distorted in the way it can on the West Coast.

While East Coast customers seem to have become more aggressive early-adopters, that view is not held universally. Kris Beevers, the founder and CEO of NS1, said that “the reality of our business through 2014 and 2015 is that I flew to California twice a month for sales meetings, and that is where the bulk of our customers come from.” As major West Coast companies signed on though, they ended up acting as lighthouse customers for more conservative companies on the East Coast.

Intense pain points can solve that hesitation. Ajay Kulkarni, the founder and CEO of time series database Timescale, noted that the company has customers in conservative industries because the database solves a critical production challenge for those businesses, namely the real-time processing of internet of things data. He also noted that selling to the West Coast is not necessarily easier. “I think the Bay Area is great for open source adoption, but a lot of Bay Area companies, they develop their own database tech, or they use an open source project and never pay for it,” he said.

Lehr also pointed to tech for tech’s sake as one of the increasing challenges for Silicon Valley-based enterprise companies. “In Silicon Valley, too many people start with the whiz bang tech, rather than the dirty word of use cases,” he said.

Some technology purists may complain that customers don’t know what they want until they see it. That may be true, and there is something to be said for disruptive innovation like Docker’s containers, which no one wanted for years and now everyone is excited about. But ultimately, customers buy software because it solves their problems, and they know those problems intimately. Mixing the nimble culture of Silicon Valley with a customer focus has allowed New York to start competing far more aggressively in enterprise infrastructure, and create a leading set of successful companies.

New York has come a long way, but it does still have challenges. Unlike venture capitalists on the West Coast, VCs in NYC often face significantly less competition for deals, and that means they can take significantly longer to make a decision. Almost all founders I talked to griped that — with a handful of exceptions — local VCs just aren’t willing to write the first check into their companies. In fact, for Sim at Boldstart, that has become a rallying cry. He bought firstcheck.vc, which redirects to Boldstart’s domain.

Another challenge that is a bit more peculiar to the geography of the city is just how many sub-ecosystems exist. There are distinct Manhattan and Brooklyn startup communities that overlap far less than some might expect. While there are exceptions, the fintech, biotech, and adtech worlds also keep much to themselves. University ecosystems around Columbia, NYU, Cornell Tech, and Princeton also similarly stay in their own space. These fractures are not apparent at first glance, but few leaders in the community have been able to blur these demarcations.

Ironically, New York also has a lack of showmanship. To put it frankly, there is no Elon Musk or SpaceX that is a paragon of ambition and aspiration that drives the rest of the ecosystem to (literally) shoot for the stars. The city’s strength in enterprise tech is a strong bedrock for a durable startup ecosystem, but it is hard to turn the success of, say, an advertising analytics platform into a beacon for others to try their own fortunes in the startup world.

That’s a loss for the city today, but also the opening for the enterprising individual who wants to make it big. Sim at Boldstart said that “I feel like Rodney Dangerfield: we get no respect, and over the next few years, we will get the respect we deserve.” Ultimately, that’s the story of New York: scrappiness and hustle, and trying to build the future one piece of infrastructure at a time.

Powered by WPeMatico