Silicon Valley

Auto Added by WPeMatico

Auto Added by WPeMatico

Nearly 40 million Americans are unemployed, and a recent study that examined more than 66,000 tech job layoffs found that sales and customer success roles are most vulnerable amid COVID-19. In response, some quarters of Silicon Valley are abuzz about a long-standing technology: reskilling, or training individuals to adopt an entirely new skillset or career for employment.

As millions look for a way to reenter the workforce, the question arises: Who really benefits from reskilling technology?

That depends on how you look at it, said Jomayra Herrera, a senior associate at Cowboy Ventures. Reskilling for a well-networked manager looks a lot different than it does for someone who doesn’t have as much leverage, and the vast majority of people fall into the latter. Not everyone has a friend at Google or Twitter to help them skip the online application and get right to the decision-makers.

Beyond the accessibility offered by live online classes, she pointed to the difference between assets and opportunities.

“You can give someone access to something, but it’s not true access unless they have the tools and structure to really engage with it,” Herrera said. In other words, how useful is content around reskilling if the company doesn’t support job placement post-training.

Herrera said companies must give individuals opportunities to test skills with real work and navigate the career path. Her mother, who did not go to college and speaks English as a second language, is looking to pursue training online. Before she can proceed, however, she has to surmount hurdles like language support, resume creation, job search and other challenges.

All of a sudden, content feels like a commodity, regardless of if it has active and social learning components. It’s part of the reason that MOOCs (massive open online courses) feel so stale.

Udacity, for example, was almost out of cash in 2018 and laid off more than half of its team in the past two years, according to The New York Times. Now, like other edtech companies, it is facing surges in usage.

Powered by WPeMatico

Global trade watchers breathed a sigh of relief on January 15, 2020.

After two years of threats, tariffs and tweets, there was finally a truce in the trade war between the U.S. and China. The agreement signed by President Trump and Chinese Vice Premier Liu He in the Oval Office didn’t resolve all trade tensions and maintained most of the $360 billion in tariffs the administration had put on Chinese goods. But for the first time in months, it looked like manufacturers, importers and shippers could start to put two difficult years behind them.

Then came COVID-19, at first a local disruption in Wuhan, China. Then it spread throughout Hubei province, causing havoc in a concentric circle that eventually engulfed the rest of China, where industrial production fell by more than 13.5% in the first two months of the year. When the virus spread everywhere, chaos ensued: Factories shuttered. Borders closed. Supply chains crumbled.

“It has had a cascading effect through the entire world’s economy,” says Anja Manuel, co-founder and managing partner of Rice, Hadley, Gates & Manuel LLC, an international strategic consulting firm based in Silicon Valley.

The crisis has caused a drastic contraction in global trade; the World Trade Organization estimates trade volumes will fall 13-20% in 2020. And spinning activity back up could be tricky: Even as China starts to get back online, the slowdown there could reduce worldwide exports by $50 billion this year. When factories do reopen, there’s no guarantee whether they will have parts available or empty warehouses, says Manuel, who also serves on the advisory board of Flexport, a shipping logistics startup. “Our supply chains are so tightly-knit and so just-in-time that throw a few wrenches in it like we’ve just done, and it’s going to be really hard to stand it back up again. The idea that we go back to normal the moment we lift restrictions is unlikely, fanciful, even.”

Getting to that new normal, though, is a job that a number of logistics startups are embracing. Already on the rise, companies like Flexport, Haven and Factiv see a global trade crisis as a setback, but also an opportunity to demonstrate the value of their digital platforms in a very much analog industry.

Powered by WPeMatico

Customs is the sieve of international supply chains. And yet despite its critical role, clearing customs for freight brokers can be a slow and opaque process reliant on manual data entry and prone to errors.

Silicon Valley-based KlearNow has developed a platform that aims to bring customs clearance into the digital age. Now, with $16 million new funding, KlearNow aims to expand its geographic reach and improve its product to cover increasingly complex export-import verticals and time-sensitive shipments.

The company has certification to handle any import into the U.S., no matter what the commodity is. KlearNow is close to getting certified in Canada and the U.K., and plans to expand to Netherlands, Belgium, Spain and Germany. KlearNow has about two dozen customers.

The Series A funding round was led by GreatPoint Ventures, with additional participation from Autotech Ventures, Argean Capital and Monta Vista Capital . Ashok Krishnamurthi, managing partner at GreatPoint Ventures, will join KlearNow’s board. Daniel Hoffer from Autotech Ventures is joining as a board observer.

“This is a significant opportunity to transform an archaic industry that is key to global commerce,” Krishnamurthi said in a statement.

The freight ecosystem is filled with different players from the factories and port authorities to the ship liners and the last-mile delivery companies. Each of them have their own systems.

“There’s no one system that you can transmit the data to,” KlearNow founder and CEO Sam Tyagi said in a recent interview. “So everybody dumps technology down to a PDF or a PNG or some sort of format that everybody can read. The broker gets those documents, and then they print it out — so now they become non-digital.”

If you go to any customs brokers office they look like the old doctor’s office where all those folders are there with nicely arranged, really organized but very manual process,” he added. From here, Tyagi said, a broker will read off from those printed documents and type the information into another system that is communicated to Customs and Border Patrol’s system.

“It is very manual, it’s very small, and they work in a siloed system,” Tyagi said. “There is no visibility for the customer, or the importer, and it’s very costly because of the manual intervention.”

KlearNow developed a digital customs clearance platform that aims to be agnostic. This allows importers, customs brokers and freight forwarders to integrate with local customs authorities and conduct business on a single digital platform remotely and in real time. The platform automates this process to eliminate errors and reduces the time to clear customs. KlearNow says it can slash customs clearance times from hours to minutes.

The startup is also betting that its platform will find new customers in this remote work era that was caused by the COVID-19 pandemic. Custom brokers, who might normally travel into central offices and manage physical paperwork, are now faced with completing that task from home.

“Remote work is impossible for these people,” because they often need to access large-format printers, Tyagi said.

The company said its digital platform can funnel new clients, like these newly remote workers, directly to brokers for global customs clearance.

Tyagi said the company has also added new capabilities in response to COVID-19, such as expediting their FDA module to clear much-needed medical supplies, and is temporarily offering free clearance for nonprofit organizations that are importing masks, hand sanitizers and ventilators.

Powered by WPeMatico

Here’s another edition of “Dear Sophie,” the advice column that answers immigration-related questions about working at technology companies.

“Your questions are vital to the spread of knowledge that allows people all over the world to rise above borders and pursue their dreams,” says Sophie Alcorn, a Silicon Valley immigration attorney. “Whether you’re in people ops, a founder or seeking a job in Silicon Valley, I would love to answer your questions in my next column.”

“Dear Sophie” columns are accessible for Extra Crunch subscribers; use promo code ALCORN to purchase a one or two-year subscription for 50% off.

Dear Sophie: I have an H-4 visa and work authorization. I currently have a job that’s considered nonessential during the coronavirus emergency. If I get laid off, I would need unemployment assistance while I look for another job.

Would getting unemployment benefits hurt my or my spouse’s green card petition under the new public charge rule?

— Nonessential in NorCal

Dear Nonessential:

Thanks for your timely question. The short answer is no, getting unemployment benefits alone right now won’t jeopardize your or your spouse’s green card. This is because receiving unemployment benefits, getting tested for coronavirus and seeking emergency medical treatment (even if it’s covered by Medicaid) are all exempt from consideration as government benefits under the new public charge rule.

Immigration officials have long had the authority to deny individuals a visa or green card if they are likely to be dependent on public benefits. The new public charge rule, which went into effect on February 24, expands the factors immigration officials will consider. An additional form seeking health and financial information must now be submitted with most visa and green card applications. Immigration officials will use that information to determine whether applicants are or are likely to become dependent on government benefits.

If you have received a public benefit in the past, your application won’t necessarily be denied, but given what’s at stake, it’s important to consult an experienced immigration attorney.

Individuals who will be subjected to the increased scrutiny of the expanded public charge rule are:

Powered by WPeMatico

If parties came with an alert system, this post would qualify as Def Con 4. Now hear this — we just released the final batch of tickets to our 3rd Annual Winter Party at Galvanize, which heats up on February 7 in San Francisco. If you want to be there with more than 1,000 of Silicon Valley’s finest, act now with all due haste. Buy your ticket right here.

Hang out with your crowd and enjoy cocktails, craft beer and tempting appetizers. Branch out and meet new people in a relaxed, laid-back setting. Startuppers, you work hard, and now it’s time to let loose a little. Bust out your crazy karaoke skills and get ready for other party games, activities and photo ops.

It’s also a chill way to broaden your network, see a handful of exhibiting startups (wow, those demo tables sold out fast) and maybe even meet a future investor, partner or mentor. Startup magic happens at TechCrunch parties. Is this your year for magic?

Wanna know who else will be in the house? Check out some of the companies ready to meet, greet and network in a casual setting.

Here are the party particulars:

It’s just not a TechCrunch party without door prizes, and we will not disappoint. You could win TC swag or win tickets to Disrupt SF, our flagship event coming in September 2020.

Speaking of Disrupt SF 2020, here’s another way to go gratis. It takes a big team to pull off a party of this magnitude. Volunteer to help us throw this party and you’ll earn a pass to our flagship Disrupt event. Pretty sweet.

Startup fans, don’t miss out on one of the great Silicon Valley traditions. Buy your ticket to the 3rd Annual Winter Party at Galvanize, right now before they’re gone for good.

Is your company interested in sponsoring the 3rd Annual Winter Party at Galvanize? Contact our sponsorship sales team by filling out this form.

Powered by WPeMatico

Welcome back to Startups Weekly, a weekend newsletter that dives into the week’s noteworthy startups and venture capital news. Before I jump into today’s topic, let’s catch up a bit. Last week I wrote about the startups we lost in 2019. Before that, I noted the defining moments of VC in 2019.

Unfortunately, this will be my last newsletter, as I am leaving TechCrunch for a new opportunity. Don’t worry, Startups Weekly isn’t going anywhere. We’ll have a new writer taking over the weekly update soon enough; in the meantime, TechCrunch editor Henry Pickavet will be at the helm. You can still get in touch with me on Twitter @KateClarkTweets.

If you’re new here, you can subscribe to Startups Weekly here. Lots of good content will be coming your way in 2020.

TechCrunch reporter Manish Singh penned an interesting piece on the state of Indian startups this week: As Indian startups raise record capital, losses are widening (Extra Crunch membership required). In it, he claims the financial performance of India’s largest startups are cause for concern. Gems like Flipkart, BigBasket and Paytm have lost a collective $3 billion in the last year.

“What is especially troublesome for startups is that there is no clear path for how they would ever generate big profits,” he writes. “Silicon Valley companies, for instance, have entered and expanded into India in recent years, investing billions of dollars in local operations, but yet, India has yet to make any substantial contribution to their bottom lines. If that wasn’t challenging enough, many Indian startups compete directly with Silicon Valley giants, which while impressive, is an expensive endeavor.”

Manish’s story came one day after The New York Times published an in-depth report on Oyo, a tech-enabled budget hotel chain and rising star in the Indian tech community. The NYT wrote that Oyo offers unlicensed rooms and has bribed police officials to deter trouble, among other toxic practices.

Whether Oyo, backed by billions from the SoftBank Vision Fund, will become India’s WeWork is the real cause for concern. India’s startup ecosystem is likely to face a number of barriers as it grows to compete with the likes of Silicon Valley.

Follow Manish here or on Twitter for more of TechCrunch’s growing India coverage.

If you’ve still not subscribed to Extra Crunch, now is the time. Longtime TechCrunch reporter and editor Josh Constine is launching a new series to teach you how to pitch your startup. In it he will examine embargoes, exclusives, press kit visuals, interview questions and more. The first of many, How to find the right reporter to pitch your startup, is online now.

Subscribe to Extra Crunch here.

Another week, another new episode of TechCrunch’s venture capital-focused podcast, Equity. This week, we discussed a few of 2019’s largest scandals, Peloton’s strange holiday ad and the controversy over at the luggage startup Away. Listen here and be sure to subscribe, too.

For anyone wondering about changes at Equity following my departure from TechCrunch, the lovely Alex Wilhelm (founding Equity co-host) will keep the show alive and, soon enough, there will be a brand new co-host in my place. Please keep supporting the show and be sure to recommend it to all your podcast-adoring friends.

Powered by WPeMatico

Spotify did it. Slack did it. Many other late-stage private technology companies are reported to be seriously considering it. Should yours?

If you are a board member of a late-stage, venture-backed company or part of its management team, you likely have heard of the term “direct listing.” Or you may have attended one or all of the slew of recent conferences being hosted by big-name investment banks and others, including tech investor guru Bill Gurley, who recently debated the pros and cons of choosing a direct listing over a traditional IPO.

Before you decide what’s right for your company, here are a few things you need to know about direct listings.

For people not familiar with the term, a direct listing is an alternative way for a private company to “go public,” but without selling its shares directly to the public and without the traditional underwriting assistance of investment bankers.

In a traditional IPO, a company raises money and creates a public market for its shares by selling newly created stock to investors. In some instances, a select number of pre-IPO investors, usually very large stockholders or management, may also sell a portion of their holdings in the IPO. In an IPO, the company engages investment bankers to help promote, price and sell the stock to investors. The investment bankers are paid a commission for their work that is based on the size of the IPO—usually seven percent for a traditional technology company IPO.

In a direct listing, a company does not sell stock directly to investors and does not receive any new capital. Instead, it facilitates the re-sale of shares held by company insiders such as employees, executives and pre-IPO investors. Investors in a direct listing buy shares directly from these company insiders.

Does this mean that a company doing a direct listing doesn’t need investment banks? Not quite. Companies still engage investment banks to assist with a direct listing and those banks still get paid quite well (to the tune of $35 million in Spotify and $22 million in Slack).

However, the investment banks play a very different role in a direct listing. Unlike a traditional IPO, in a direct listing, investment banks are prohibited under current law from organizing or attending investor meetings and they do not sell stock to investors. Instead, they act purely in an advisory capacity helping a company to position its story to investors, draft its IPO disclosures, educate a company’s insiders on process and strategize on investor outreach and liquidity.

The concept of a direct listing is actually not a new one. Companies in a variety of industries have used similar structures for years. However, the structure has only recently received a lot of investor and media attention because high-profile technology companies have started to use it to go public. But why have technology companies only recently started to consider direct listings?

The rise of massive pre-IPO fundraising rounds

With an abundance of investor capital, especially from institutional investors that historically hadn’t invested in private technology companies, massive pre-IPO fundraising rounds have become the norm. Slack raised over $400 million in August 2018—just over a year prior to its direct listing. Because of this widespread availability of capital, some technology companies are now able to raise sufficient capital before their actual IPO to either become profitable or put them on a path to profitability.

Criticism of current IPO process

There has been increasing negative sentiment, especially amongst well-known venture capitalists, about certain aspects of the traditional IPO process—namely IPO lock-up agreements and the pricing and allocation process.

IPO lock-up agreements. In a traditional IPO, investment bankers require pre-IPO investors, employees and the company to sign a “lock-up agreement” restricting them from selling or distributing shares for a specified period of time following the IPO—usually 180 days. The bankers put these agreements in place in order to stabilize the stock immediately after the IPO. While the merits of a lock-up agreement can certainly be debated, by the time VCs (and other insiders) are allowed to sell following an IPO, oftentimes the stock price has fallen significantly from its highs (sometimes to below the IPO price) or the post lock-up flood of selling can have an immediate negative impact on the trading price.

In a direct listing, there is no lock-up agreement, which allows for equal access to the offering to all of the company’s pre-IPO investors, including rank-and-file employees and smaller pre-IPO stockholders.

IPO pricing and allocation: In a traditional IPO, shares are often allocated directly by a company (with the assistance of its underwriters) to a small number of large, institutional investors. Traditional IPOs are often underpriced by design to provide large institutional investors the benefit of an immediate 10-15% “pop” in the stock price. Over the last few years, some of these “pops” have become more pronounced. For example, Beyond Meat’s stock soared from $25 to $73 on its first day of trading, a 163% gain. This has fueled a concern, particularly shared amongst the VC community, that investment banks improperly price and allocate shares in an IPO in order to benefit these institutional investors, which are also clients of the same investment banks that are underwriting the IPO. While the merits of this concern can also be debated, in instances where there is a large price discrepancy between the trading price of the stock following the IPO and the price of the IPO, there is often a sense that companies have left money on the table and that pre-IPO investors have suffered unnecessary dilution. If the IPO had been priced “correctly,” the company would have had to sell fewer shares to raise the same amount of proceeds.

Because a company is not selling stock in a direct listing, the trading price after listing is purely market driven and is not “set” by the company and its investment bankers. Moreover, since no new shares are issued in a direct listing, insiders do not suffer any dilution.

The Spotify effect

Before Spotify’s direct listing, technology companies hadn’t used the direct listing structure to go public. Spotify was, in many ways, the perfect test case for a direct listing. It was well known, didn’t need any additional capital and was cash flow positive. In addition, prior to its direct listing, Spotify had entered into a debt instrument that penalized the company so long as it remained private. As a result, it just needed to go public. After clearing some regulatory hurdles, Spotify successfully executed its direct listing in April 2018. After Spotify’s direct listing, Slack (relatively) quickly followed suit. Slack’s direct listing was notable because it represented the first traditional Silicon Valley-based VC-backed company to use the structure. It was also an enterprise software company, albeit one with a consumer cult following.

While a direct listing offers many benefits, the structure does not make sense for every company. Below is a list of key benefits and drawbacks:

Powered by WPeMatico

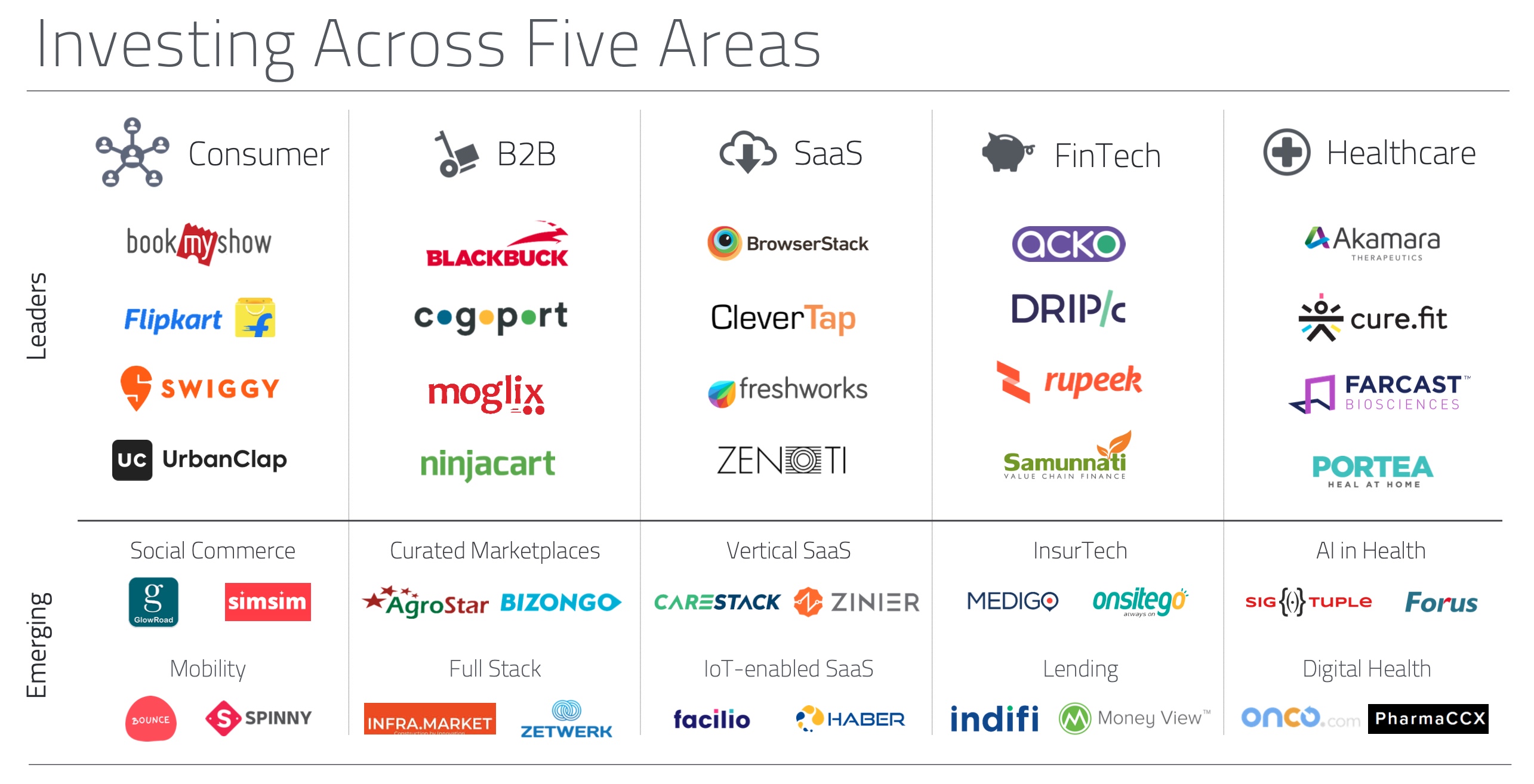

Accel, one of the world’s most influential venture capitalist firms, is getting more bullish on India.

The Silicon Valley-headquartered firm, which largely focuses on early-stage investments, said today it has closed $550 million for its sixth venture fund in India.

This is a significant amount of capital for Accel’s efforts in the country, where it began investing 15 years ago and has infused roughly $1 billion through all its previous funds.

Anand Daniel, a partner for Accel in India, told TechCrunch in an interview that the VC fund will continue to focus on identifying and investing in seed and early-stage startups.

But the fund realized it needed more money so it could actively participate in follow-on rounds (later-stage financing rounds) of its portfolio startups. The announcement today follows Accel’s similar recent push in Europe and Israel, where it closed a $575 million fund.

“We also selectively do growth investments for companies that are scaling well, such as Swiggy, UrbanClap, BlackStone and Bounce. We have continued to back them through Series B and Series C rounds,” he said.

At the risk of being accused of bias, I’ll say this: Accel India is a rare Indian fund that had credible exits and more promising exits in the pipeline. They’re also some of the nicest people to work with. https://t.co/aZGjDgSQKe

— JPK (@therealjpk) December 2, 2019

Like in many other markets, Accel’s track record in India is quite impressive. It participated in the seed financing round of e-commerce firm Flipkart, which was then valued at $4 million post-money. Walmart bought a majority stake in Flipkart last year for $16 billion. (This helped Accel net more than $1 billion in return from Flipkart.)

Accel, which has nine partners and more than 50 members in total in India, also invested in the seed round of SaaS giant Freshworks, which is now valued at more than $3 billion, food delivery startup Swiggy, also valued at north of $3 billion, and recently turned unicorn BlackBuck. Accel has been the first institutional investor for 85% of startups in its portfolio.

The VC firm says 44 of the 100-odd startups in its India portfolio today are valued at over $100 million each. In total, including Flipkart’s $21 billion market value, Accel’s portfolio firms have created $44 billion in market value.

Some of the investments Accel has made in India

“When we started our first fund in India in 2005, the world was a very different place. Just 1 in 50 Indians had access to the internet and mobile phone ownership was nascent. Yet we firmly believed that India was on the cusp of a big change,” the firm said in a statement.

“Today, the opportunity ahead is significantly bigger than when we started in 2005: India can now digitally identify 1.3 billion people, has 600 million internet users and 150 million online transacting customers with a national payments platform that processes $20 billion a month.”

Daniel said moving forward Accel will continue to focus on consumer, business-to-business, fintech, healthcare and global SaaS categories. “We have nine partners with their own areas of interest. They invest from their own conviction and finance seed rounds. If we see a particular sector evolving, then we do a deeper thesis work,” he said.

“We then develop deeper confidence for the space. For example, back in the day we invested in mobility startup TaxiForSure, long before Uber had arrived in India. That helped us understand mobility well. We have used those learnings to invest in several more mobility startups.”

Accel’s growing interest in India comes at a time when several other giants, including SoftBank and Prosus Ventures, have also become more active in the nation — though they tend to finance later-stage rounds.

For Indian startups that are already having their best year, this can only be good news.

Powered by WPeMatico

Brexit has taken over discourse in the UK and beyond. In the UK alone, it is mentioned over 500 million times a day, in 92 million conversations — and for good reason. While the UK has yet to leave the EU, the impact of Brexit has already rippled through industries all over the world. The UK’s technology sector is no exception. While innovation endures in the midst of Brexit, data reveals that innovative companies are losing the ability to attract people from all over the world and are suffering from a substantial talent leak.

It is no secret that the UK was already experiencing a talent shortage, even without the added pressure created by today’s political landscape. Technology is developing rapidly and demand for tech workers continues to outpace supply, creating a fiercely competitive hiring landscape.

The shortage of available tech talent has already created a deficit that could cost the UK £141 billion in GDP growth by 2028, stifling innovation. Now, with Brexit threatening the UK’s cosmopolitan tech landscape — and the economy at large — we may soon see international tech talent moving elsewhere; in fact, 60% of London businesses think they’ll lose access to tech talent once the UK leaves the EU.

So, how can UK-based companies proactively attract and retain top tech talent to prevent a Brexit brain drain? UK businesses must ensure that their hiring funnels are a top priority and focus on understanding what matters most to tech talent beyond salary, so that they don’t lose out to US tech hubs.

Powered by WPeMatico

As I wrote for TechCrunch recently, immigration is not an issue always associated with tech — not even when thinking about the ethics of technology, as I do here.

So when I was moved to tears a few weeks ago, on seeing footage of groups of 18 Jewish protestors link arms to block the entrances to ICE detention facilities, bearing banners reading “Never Again” in reference to the Holocaust — these mostly young women risking their physical freedom and safety to try to help the children this country’s immigration service is placing in concentration camps today, one of my first thoughts was: I can’t cover that for my TechCrunch column. It’s about ethics of course, but not about tech.

It turns out that wasn’t correct. Immigration is a tech issue. In fact, companies such as Wayfair (furniture), Amazon (web services), and Palantir (the software used to track undocumented immigrants) have borne heavy criticism for their support of and partnership with ICE’s efforts under the current administration.

And as I discussed earlier this month with Jaclyn Friedman, a leading sex ethics expert and one of the ICE protestors arrested in a major demonstration in Boston, social media technology has been instrumental in building and amplifying those protests.

But there’s more. IBM, for example, has an unfortunate and dark history of support for Nazi extermination efforts, and many recent commentators have drawn parallels between what IBM did during the Holocaust and what companies like Palantir are beginning to do now.

Dozens of protestors huddle in the rain outside Palantir HQ.

I say “companies,” plural, with intention: immigrant advocacy organization Mijente recently released news that Anduril, the company founded by Palmer Luckey and composed of Palantir veterans, now has a $13.5 million contract with the Marine corps for their autonomous surveillance “Lattice” towers at four different USMC bases, including one border base. Documents procured via the Freedom of Information Act show the Marines mention “the intrusion dilemma” in their justification for choosing Anduril.

So now it seems the kinds of surveillance tech we know are badly biased at best — facial recognition? Panopticon-style observation? Algorithms of various other kinds — will be put to work by the most powerful fighting force ever designed, for expanded intervention into our immigration system.

Will the Silicon Valley elite say “no”? To what extent will new protests emerge, where the sorts of people likely to be reading this writing might draw a line and make work more difficult for their peers at places like Anduril?

Maybe the problem, however, is that most of us think of immigration ethics as an issue that might touch on a small handful of particularly libertarian-leaning tech companies, but surely it doesn’t go beyond that, right? Can’t the average techie in San Francisco or elsewhere safely and accurately say these problems don’t actually implicate them?

Turns out that’s not right either.

Which is why I had to speak this week with Cornell University historian Louis Hyman. Hyman is a Professor at Cornell’s School of Industrial and Labor Relations, and Director of the ILR’s Institute for Workplace Studies, in New York. In our conversation, Hyman and I dig into Silicon Valley’s history with labor rights, startup work structures and the role of immigration in the US tech ecosystem. Beyond that, I’ll let him introduce himself and his extraordinary work, below.

Louis Hyman. (Image by Jesse Winter)

Greg Epstein: I discovered your work via a piece you wrote in the Washington Post, which drew from your 2018 book, Temp: How American Work, American Business, and the American Dream Became Temporary. In it, you wrote, “Undocumented workers have been foundational to the rise of our most vaunted hub of innovative capitalism: Silicon Valley.”

And in the book itself, you write at one point, “To understand the electronics industry is simple: every time someone says “robot,” simply picture a woman of color. Instead of self-aware robots, workers—all women, mostly immigrants, sometimes undocumented—hunched over tables with magnifying glasses assembling parts, sometimes on a factory line and sometimes on a kitchen table. Though it paid a lot of lip service to automation, Silicon Valley truly relied upon a transient workforce of workers outside of traditional labor relations.”

Can you just give us a brief introduction to the historical context behind these kinds of comments?

Louis Hyman: Sure. One of the key questions all of us ask is why is there only one Silicon Valley. There are different answers for that.

Powered by WPeMatico