Series A

Auto Added by WPeMatico

Auto Added by WPeMatico

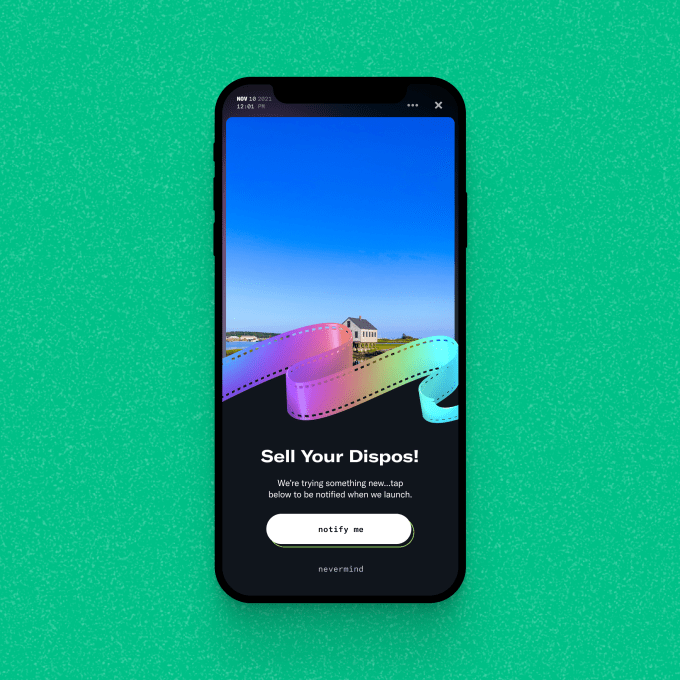

Dispo, the photo-sharing app that emulates disposable cameras, started rolling out a test yesterday that will record user interest in selling photos as NFTs. Some users will now see a sell button on their photos, and when they tap it, they can sign up to be notified when the ability to sell Dispo photos launches.

CEO and co-founder Daniel Liss told TechCrunch that Dispo is still deciding how it will incorporate NFT sales into the app, which is why the platform is piloting a test with its users. Dispo doesn’t know yet what blockchain it would use, if it would partner with an NFT marketplace or what cut of sales Dispo would take.

“I think it’s safe to say from the test that there will be an experience native to the Dispo app,” Liss said. “There are a number of ways it could look — there could be a native experience within Dispo that then connects through an API to another platform, and in turn, they’re our partner, but to the community, it would look native to the Dispo app.”

Image Credits: Dispo

This marks a new direction for the social media app, which seeks to redefine the photo-sharing experience by only letting users see the photos they took at 9 AM the next morning. From Dispo’s perspective, this gimmick helps users share more authentically, since you take one photo and then you’re done — the app isn’t conducive to taking dozens of selfies and posting the “best” image of yourself. But though it only launched in December 2019, Dispo has already faced both buzzy hype and devastating controversy.

Until about a year ago, the app was called David’s Disposables, named after co-founder and YouTuber David Dobrik. The app was downloaded over a million times in the first week after its release and hit No. 1 on the App Store charts. In March 2021, the app dropped its waitlist and relaunched with social network features, but just weeks later, Insider reported sexual assault allegations against a member of Vlog Squad, Dobrik’s YouTube prank ensemble. In response, Spark Capital severed ties with the company, leading to Dobrik’s departure. Other investors like Seven Seven Six and Unshackled Ventures, which contributed to the company’s $20 million Series A round, announced that they would donate any profits from their investments in Dispo to organizations working with survivors of sexual assault.

Liss told TechCrunch in June, when the company confirmed its Series A, that Dobrik’s role with the company was as a marketing partner — Liss has been CEO since the beginning. In light of the controversy, Liss said the app focused on improving the product itself and took a step back from promotion.

According to data from the app analytics firm SensorTower, Dispo has reached an estimated 4.7 million global installs to date since launch. Though the app saw the most downloads in January 2020, when it was installed over 1 million times, the app’s next best month came in March 2021, when it removed its waitlist — that month, about 616,000 people downloaded Dispo. Between March and the end of August, the app was downloaded around 1.4 million times, which is up 118% year over year compared to the same time frame in 2020 — but it should be expected that this year’s numbers would be higher, since last year, the app’s membership was exclusive.

Image Credits: Dispo

Now, with the announcement that Dispo is pursuing NFTs, Liss hopes that his company won’t just change how people post photos, but what the relationship will be between platforms and the content that users create.

“Why NFTs? The most powerful memories of our lives have value. And they have economic value, because we created them, and the past of social media fails to recognize that,” Liss told TechCrunch. “As a result, the only way that a creator with a big following is compensated is by selling directly to a brand, as opposed to profiting from the content itself.”

Adding NFT sales to the app offers Dispo a way to profit from a cut of user sales, but it stands to question how adding NFT sales could impact the community-focused feel of Dispo.

“I think there is tremendous curiosity and interest,” Liss said. “But these problems and questions are why we need more data.”

Powered by WPeMatico

The manufacturing industry took a hard hit from the Covid-19 pandemic, but there are signs of how it is slowly starting to come back into shape — helped in part by new efforts to make factories more responsive to the fluctuations in demand that come with the ups and downs of grappling with the shifting economy, virus outbreaks and more. Today, a businesses that is positioning itself as part of that new guard of flexible custom manufacturing — a startup called Fractory — is announcing a Series A of $9 million (€7.7 million) that underscores the trend.

The funding is being led by OTB Ventures, a leading European investor focussed on early growth, post-product, high-tech start-ups, with existing investors Trind Ventures, Superhero Capital, United Angels VC, Startup Wise Guys and Verve Ventures also participating.

Founded in Estonia but now based in Manchester, England — historically a strong hub for manufacturing in the country, and close to Fractory’s customers — Fractory has built a platform to make it easier for those that need to get custom metalwork to upload and order it, and for factories to pick up new customers and jobs based on those requests.

Fractory’s Series A will be used to continue expanding its technology, and to bring more partners into its ecosystem.

To date, the company has worked with more than 24,000 customers and hundreds of manufacturers and metal companies, and altogether it has helped crank out more than 2.5 million metal parts.

To be clear, Fractory isn’t a manufacturer itself, nor does it have no plans to get involved in that part of the process. Rather, it is in the business of enterprise software, with a marketplace for those who are able to carry out manufacturing jobs — currently in the area of metalwork — to engage with companies that need metal parts made for them, using intelligent tools to identify what needs to be made and connecting that potential job to the specialist manufacturers that can make it.

The challenge that Fractory is solving is not unlike that faced in a lot of industries that have variable supply and demand, a lot of fragmentation, and generally an inefficient way of sourcing work.

As Martin Vares, Fractory’s founder and MD, described it to me, companies who need metal parts made might have one factory they regularly work with. But if there are any circumstances that might mean that this factory cannot carry out a job, then the customer needs to shop around and find others to do it instead. This can be a time-consuming, and costly process.

“It’s a very fragmented market and there are so many ways to manufacture products, and the connection between those two is complicated,” he said. “In the past, if you wanted to outsource something, it would mean multiple emails to multiple places. But you can’t go to 30 different suppliers like that individually. We make it into a one-stop shop.”

On the other side, factories are always looking for better ways to fill out their roster of work so there is little downtime — factories want to avoid having people paid to work with no work coming in, or machinery that is not being used.

“The average uptime capacity is 50%,” Vares said of the metalwork plants on Fractory’s platform (and in the industry in general). “We have a lot more machines out there than are being used. We really want to solve the issue of leftover capacity and make the market function better and reduce waste. We want to make their factories more efficient and thus sustainable.”

The Fractory approach involves customers — today those customers are typically in construction, or other heavy machinery industries like ship building, aerospace and automotive — uploading CAD files specifying what they need made. These then get sent out to a network of manufacturers to bid for and take on as jobs — a little like a freelance marketplace, but for manufacturing jobs. About 30% of those jobs are then fully automated, while the other 70% might include some involvement from Fractory to help advise customers on their approach, including in the quoting of the work, manufacturing, delivery and more. The plan is to build in more technology to improve the proportion that can be automated, Vares said. That would include further investment in RPA, but also computer vision to better understand what a customer is looking to do, and how best to execute it.

Currently Fractory’s platform can help fill orders for laser cutting and metal folding services, including work like CNC machining, and it’s next looking at industrial additive 3D printing. It will also be looking at other materials like stonework and chip making.

Manufacturing is one of those industries that has in some ways been very slow to modernize, which in a way is not a huge surprise: equipment is heavy and expensive, and generally the maxim of “if it ain’t broke, don’t fix it” applies in this world. That’s why companies that are building more intelligent software to at least run that legacy equipment more efficiently are finding some footing. Xometry, a bigger company out of the U.S. that also has built a bridge between manufacturers and companies that need things custom made, went public earlier this year and now has a market cap of over $3 billion. Others in the same space include Hubs (which is now part of Protolabs) and Qimtek, among others.

One selling point that Fractory has been pushing is that it generally aims to keep manufacturing local to the customer to reduce the logistics component of the work to reduce carbon emissions, although as the company grows it will be interesting to see how and if it adheres to that commitment.

In the meantime, investors believe that Fractory’s approach and fast growth are strong signs that it’s here to stay and make an impact in the industry.

“Fractory has created an enterprise software platform like no other in the manufacturing setting. Its rapid customer adoption is clear demonstrable feedback of the value that Fractory brings to manufacturing supply chains with technology to automate and digitise an ecosystem poised for innovation,” said Marcin Hejka in a statement. “We have invested in a great product and a talented group of software engineers, committed to developing a product and continuing with their formidable track record of rapid international growth

Powered by WPeMatico

Canopy Servicing announced this morning it recently closed a $15 million Series A. The startup sells software to fintechs and others, allowing customers to create loan programs and service the resulting products.

The company raised a $3.5 million seed round in 2020. Canaan led its Series A, with participation from Homebrew, Foundation and BoxGroup, among others. Per Canopy, its valuation grew by 5x from its seed round to its Series A.

The company has raised $18.5 million to date.

So far this reads much like any other post announcing a new startup funding round, kicking off with an array of information concerning the round and who chipped into the transaction. Next, we’d probably note the competitors, growth and what investors in the company in question have to say about their recent purchase. This morning, however, I want to riff a bit on the future of fintech and how the financial tech stack of the future may be built.

TechCrunch chatted with Canopy CEO Matt Bivons last week. He has an interesting take on where fintech is headed. Let’s discuss it and work through what Canopy does.

As with many startups, Canopy was built to scratch an itch. Bivons had run into issues regarding loan servicing in prior jobs. He went on to found a startup that aimed to build a student credit card. But after working on that project, Bivons and co-founder Will Hanson pivoted the company to a B2B-focused concern building loan servicing technology.

Behind the decision was market research undertaken by the Canopy crew that uncovered that a great number of fintech startups wanted to get into the credit market. That makes sense; credit products can provide far more attractive economics to fintech startups than, say, checking and savings accounts. Knowing that loan servicing was a bear and a half to manage, Canopy decided to focus on it.

Bivons framed Canopy as a modern API for loan servicing that can be used to create and manage loans at any point in their lifecycle. He noted that what the startup is doing is akin to what several successful fintech companies have done, namely taking a piece of the fintech world and making it better for developers.

This is where Bivons’ view of the future of fintech products comes into play. According to the CEO, in the future, companies will not buy a monolithic financial technology stack. Instead, he thinks, they will buy the best API for each slice of the fintech world that they need to implement. This matters because we could argue that Canopy is targeting too small a product space. Not that its market isn’t large — debt and its servicing are massive problem spaces — but seeing a company find a niche to focus on makes more sense when its leaders expect focused fintech products to win out over large bundles of services.

Bivons added that much of the fintech focus of the last five years has been on debit, citing Chime, Step and Greenlight as examples. The next decade, he said, is going to focus on credit products. That would be good news for Canopy.

Canopy co-founders via the company. CTO Will Hanson (left) and CEO Matt Bivons (right).

Critically, and for the finance nerds out there, Bivons told TechCrunch that its loan servicing technology does not require the company to take on any credit risk, and that it has gross margins of around 90%. I never trust a too-round number, but the figure indicates that what Canopy has built could grow into an attractive business.

Today, Canopy is a traditional SaaS, though Bivons said that it wants to move toward usage-based pricing in time. Its service costs around 50 cents per account per month, or around $6 per year in its current form. Today, around 40% of Canopy’s customers are seed and Series A-scale startups, though Bivons noted that it is moving up the customer size chart over time.

The resulting growth is impressive. Canopy’s customer count grew 4.5x from February to May of 2021. Of course, Canopy is a young company, so its overall customer base could not have been massive at the start of the year. Still, that’s the sort of growth that makes investors sit up and pay attention, making the Canopy Series A somewhat unsurprising.

Fintech growth doesn’t seem to be slackening much, meaning that the market for what Canopy is selling should expand. Provided that its view that best-of-breed, more particular fintech products will beat larger stacks in the market, it could have an interesting trajectory ahead of it. And now that it has raised its Series A, we can start to annoy it with more concrete questions about its growth from here on out.

Powered by WPeMatico

Capping off our dig into the early-stage venture capital market, we’re taking a quick look at Europe this morning. Previously, The Exchange tucked into the United States’ early-stage market for startup capital, uncovering startups using abundant seed capital to get more done before raising a Series A, while others were using pedigree, team and market size to accelerate their first lettered raise.

For both cohorts, it appeared that a rapid-fire Series B could be in the offing, with VCs looking to get capital into winners early.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

The Latin American venture capital market for early-stage startups had a number of similar hallmarks. That shouldn’t have been surprising. According to Seth Pierrepont, a partner at London-based Accel, “fundraising dynamics are now no longer U.S.- or European-specific — they’re global.” Fundraising over videoconferencing services like Zoom has done more than make geographical distances less impactful inside of countries — it’s even made national borders and even oceans less meaningful.

Is the European startup market similar to what we’ve seen in Latin America and the United States — a cognate for the North American venture capital scene, given its outsized global weight by round count and amount invested?

Largely, yes, a trend that appears to be shaking up prices and the talent wars. This morning, we’re taking a final look at the early-stage venture capital market, this time through a European lens, with an assist from a few investors from the continent.

Broadly, early-stage venture capital rounds in Europe are happening “earlier and are larger in size,” according to Draper Esprit’s Vinoth Jayakumar, an investor based in London. The correlate of larger rounds being raised while startups are younger is valuation expansion, according to Jayakumar, who said that prices are going up “because larger rounds are very dilutive to founders if done at normal — or in this case too low — valuations.”

Powered by WPeMatico

Earlier this week, The Exchange wrote about the early-stage venture capital market, with the goal of understanding how some startups are raising more seed capital before they work on their Series A, while other startups are seemingly raising their first lettered round while in the nascent stages of scaling.

The expedition was rooted in commentary from Rudina Seseri of Glasswing Ventures, who said abundant seed capital in the United States allows founders to get a lot done before they raise a Series A, effectively delaying these rounds. But after those founders did raise that A, their Series B round could rapidly follow thanks to later-stage money showing up in earlier-stage deals in hopes of snagging ownership in hot companies.

The idea? Slow As, fast Bs.

After chatting with Seseri more and a number of other venture capitalists about the concept, a second dynamic emerged. Namely that the “typical” early-stage funding round, as Seseri described it, was “becoming atypical because of the rise of preemptive rounds [in which] typical expectations on metrics go out the window.”

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

Series As, she said, could come mere months after a seed deal, and Series B rounds were seeing expected revenue thresholds tumble in part to “large, multiasset players that have come down market and are offering a different product than typical VCs — very fast term sheets, no active involvement post-investment, large investments amounts and high valuations.”

Focusing on just the Series A dynamic, the old rule of thumb that a startup would need to reach $1 million in annual recurring revenue (ARR) is now often moot. Some startups are delaying their A rounds until they reach $2 million in ARR thanks to ample seed capital.

While some startups delay their A rounds, others raise the critical investment earlier and earlier, perhaps with even a few hundred thousand in ARR.

While some startups delay their A rounds, others raise the critical investment earlier and earlier, perhaps with even a few hundred thousand in ARR.

What’s different between the two groups? Startups with “elite status” are able to jump ahead to their Series A, while other founders spend more time cobbling together adequate seed capital to get to sufficient scale to attract an A.

The dynamic is not merely a United States phenomenon. The two-tier venture capital market is also showing up in Latin America, a globally important and rapidly expanding startup region. (Brazilian fintech startup Nubank, for example, just closed a $750 million round.)

This morning, we’re diving into the Latin American venture capital market and its early-stage dynamics. We also have notes on the European scene, so expect more on the topic next week. Let’s go!

Mega-rounds are no longer an exception in Latin America; in fact, they have become a trend, with ever-larger rounds being announced over the last few months.

The announcements themselves often emphasize round size: For instance, the recent $100 million Series B round into Colombian proptech startup Habi was touted as “the largest Series B for a startup headquartered in Colombia.” This follows other 2021 records such as “the largest Series A for Mexico ” — $65 million for online grocer Jüsto — and “the largest Series A ever raised by a Latin American fintech” — $43 million for “Plaid for Latin America” Belvo.

Powered by WPeMatico

Mercuryo, a startup that has built a cross-border payments network, has raised $7.5 million in a Series A round of funding.

The London-based company describes itself as “a crypto infrastructure company” that aims to make blockchain useful for businesses via its “digital asset payment gateway.” Specifically, it aggregates various payment solutions and provides fiat and crypto payments and payouts for businesses.

Put more simply, Mercuryo aims to use cryptocurrencies as a tool for putting in motion next-gen, cross-border transfers or, as it puts it, “to allow any business to become a fintech company without the need to keep up with its complications.”

“The need for fast and efficient international payments, especially for businesses, is as relevant as ever,” said Petr Kozyakov, Mercuryo’s co-founder and CEO. While there is no shortage of companies enabling cross-border payments, the startup’s emphasis on crypto is a differentiator.

“Our team has a clear plan on making crypto universally available by enabling cheap and straightforward transactions,” Kozyakov said. “Cryptocurrency assets can then be used to process global money transfers, mass payouts and facilitate acquiring services, among other things.”

Image Credits: Left to right: Alexander Vasiliev, Greg Waisman, Petr Kozyakov / MercuryO

Mercuryo began onboarding customers at the beginning of 2019, and has seen impressive growth since with annual recurring revenue (ARR) in April surpassing over $50 million. Its customer base is approaching 1 million, and the company has partnerships with a number of large crypto players including Binance, Bitfinex, Trezor, Trust Wallet, Bithumb and Bybit. In 2020, the company said its turnover spiked by 50 times while run-rate turnover crossed $2.5 billion in April 2021.

To build on that momentum, Mercuryo has begun expanding to new markets, including the United States, where it launched its crypto payments offering for B2B customers in all states earlier this year. It also plans to “gradually” expand to Africa, South America and Southeast Asia.

Target Global led Mercuryo’s Series A, which also included participation from a group of angel investors and brings the startup’s total raised since its 2018 inception to over $10 million.

The company plans to use its new capital to launch a cryptocurrency debit card (spending globally directly from the crypto balance in the wallet) and continuing to expand to new markets, such as Latin America and Asia-Pacific.

Mercuryo’s various products include a multicurrency wallet with a built-in crypto exchange and digital asset purchasing functionality, a widget and high-volume cryptocurrency acquiring and OTC services.

Kozyakov says the company doesn’t charge for currency conversion and has no other “hidden fees.”

“We enable instant and easy cross-border transactions for our partners and their customers,” he said. “Also, the money transfer services lack intermediaries and require no additional steps to finalize transactions. Instead, the process narrows down to only two operations: a fiat-to-crypto exchange when sending a transfer and a crypto-to-fiat conversion when receiving funds.”

Mercuryo also offers crypto SaaS products, giving customers a way to buy crypto via their fiat accounts while delegating digital asset management to the company.

“Whether it be virtual accounts or third-party customer wallets, the company handles most cryptocurrency-related processes for banks, so they can focus more on their core operations,” Kozyakov said.

Mike Lobanov, Target Global’s co-founder, said that as an experiment, his firm tested numerous solutions to buy Bitcoin.

“Doing our diligence, we measured ‘time to crypto’ – how long it takes from going to the App Store and downloading the app until the digital assets arrive in the wallet,” he said.

Mercuryo came first with 6 minutes, including everything from KYC and funding to getting the cryptocurrency, according to Lobanov.

“The second-best result was 20 minutes, while some apps took forever to process our transaction,” he added. “This company is a game-changer in the field, and we are delighted to have been their supporters since the early days.”

Looking ahead, the startup plans to release a product that will give businesses a way to send instant mass payments to multiple customers and gig workers simultaneously, no matter where the receiver is located.

Powered by WPeMatico

Mobile commerce is where it’s at, and rising investment in so-called conversational commerce startups underscores the opportunity.

Via, a two-year-old, Bay Area-based startup, is among those riding the wave, having identified some trends that are becoming clearer by the month. First, more e-commerce sales will be on mobile phones this year than desktops (as much as 70% by some estimates), people tend to read text messages almost immediately and consumers spend upwards of 30 minutes a day engaging with mobile messaging apps.

Via also insists that unlike an expanding pool of startups that are focused on helping retailers and others broadcast their marketing messages in SMS, there’s room for a player to better address the many other pieces that add up to a happy consumer experience, from delivering coupon codes to starting the returns process.

Indeed, according to co-founder and CEO Tejas Konduru — a Brigham Young grad whose parents immigrated to the U.S. from India and who have themselves worked at tech startups — one insight his now 50-person company had early on was that despite that so many of their customers now use the mobile browser to visit and shop from their stores, many retailers use website builders like Shopify or BigCommerce to “cram everything everything into mobile, leaving only enough space for, like, one picture and a Buy button.” Konduru figured there must be a way to take the shopping experience that all these customers have with brands on their website and make them happen in a quick, mobile-native way.

Via’s solution, he says, is to help those businesses interact with customers on the devices and apps they use most often. “When someone uses Shopify or BigCommerce or any of those platforms,” says Konduru, “we also connect it to Via, and it basically takes the entire shopping experience and allows [customers] to quickly swipe right through a menu or like through a catalog on, for example, Facebook Messenger. Via will also create like a native iOS Android app by taking a website, cloning it into a native iOS Android app, then sell the push notification in-app chat layer. Essentially,” he adds, “anytime someone shops on the phone and they’re not using the browser is what Via is handling.”

The “message” seems to be getting through to the right people. Via, which launched last year, says it now employs 54 people on a full-time basis, has 190 brands as customers and just secured $15 million in Series A funding led by Footwork, the new venture firm co-founded by former Stitch Fix COO Mike Smith and former Shasta Ventures investor Nikhil Basu Trivedi.

Other participants in the round include Peterson Ventures, where Konduru once interned; famed founder Josh James of Domo, where Konduru also once interned; and a long list of other notable individual investors, including Ryan Smith of Qualtrics and Lattice co-founder and CEO Jack Altman.

As for how the company charges, it doesn’t ask for a monthly or yearly fee, as per traditional SaaS companies, but instead charges per interaction, whether that’s an SMS or a voice minute or video or a GIF.

It’s starting to add up, according to Konduru, who says that Via’s average customer is seeing 15 times return on its investment and that from May of 2020 — when the company’s service went live — through December, the company generated $51 million in sales. Konduru declined to say exactly how much Via saw from those transactions, but says the company is on track to reach $10 million in annual recurring revenue this year.

As for how brands get started with Via, it’s pretty simple, by the company’s telling. As long as a company is using a commerce platform — from Shopfiy to WooCommerce to Salesforce — it takes just five minutes or so to produce a mobile app with a menu featuring the types of interactions the brand can enable via Via’s platform, says Konduru.

Konduru, who dabbled in investment banking before deciding to launch Via, says he isn’t surprised by the startup’s fast traction, though he says he has been taken aback by the breadth of conversations the company sees. While he imagined Via would be a strong marketing channel for brands that use the platform to push out notifications about abandoned shopping carts and upcoming deliveries, it’s more of a two-way street than he’d imagined.

“Every month, there are maybe 15,000 people who start the returns process through Via and will get a notification from a channel that Via supports. But suddenly — let’s say the customer gets the wrong T-shirt size — people start communicating with the brand. You see everything from fan appreciation to address changes to messaging about bad discount codes to where’s-my-order type exchanges. That’s something I didn’t expect,” says Konduru, who says that before raising its Series A round, Via raised $4.2 million in seed funding led by Peterson Ventures.

“I thought that people would just look at the notification and, like, move it into the abyss somewhere. Instead, people start interacting with the brand.”

Powered by WPeMatico

Despite hundreds of billions of dollars’ worth of goods flowing across the U.S.-Mexican border each year, the freight industry has remained analog — each side of the border offering up its own maze of bureaucracy.

Nuvocargo, a digital logistics platform for cross-border trade, is trying to modernize the process. The company offers an all-in-one service that rolls freight forwarding, customs brokerage, cargo insurance and even trade financing into one UI-friendly software and app. Housing all of these services under one app makes it easier for companies to track their supply chain and gives customs and logistics teams access to more centralized information, according to Nuvocargo CEO Deepak Chhugani.

“And you just have one single audit trail in case something goes wrong,” Chhugani told TechCrunch, adding that the process helps reduce or eliminate the extra costs that come with a high administrative overhead. It also lets customers take a high-level look at their operations from within a single interface, he said.

Chhugani likened the experience to something like Uber Eats, which offers customers the ability to easily track food orders from restaurant to home.

“Just imagine, because you are dealing with so many different parties, you lose visibility on what’s going on. If you want a snapshot of — what did I spend end-to-end? — you actually have to go through all these email chains or faxes or texts with different providers,” Chhugani explained. “Some of them might be in another country. So [Nuvocargo] just creates more visibility throughout the process, from where the goods literally are to visibility around your finances.”

But Nuvocargo is thinking beyond the actual movement of goods. The company is also starting to offer customs brokerage, comprehensive cross-border cargo insurance and factoring, or short-term account receivable finance. The last of these solves an especially difficult pain point for trucking companies, which sometimes must wait up to net-90 days to be paid.

The approach has caught investors’ eyes: Nearly one year after announcing it had raised a $5.3 million seed round, the company has closed on a $12 million Series A funding led by QED Investors and with injections from David Velez, Michael Ronen, Raymond Tonsing, FJ Labs and Clocktower. Investors NFX and ALLVP, which participated in the previous round, also participated.

The “holy grail” of their new offerings, as Chhugani called it, is trade financing. Because Nuvocargo will already have a relationship with companies, including an understanding of credit and fraud risk, its hope is that it can offer financial products at a competitive rate.

This is what attracted QED Investors, a firm that typically focuses on financial technology rather than logistics and trucking.

“After speaking with [Deepak] and seeing the connection points and parallels between what we were looking at in e-commerce and the challenges of actually getting goods across border, the fintech spark went off in my own head,” Lauren Connolley Morton, a partner at QED, said in an interview with TechCrunch. “The opportunities for factoring, for lending, for insuring goods are all very much right up our alley.”

Although Chhugani declined to disclose Nuvocargo’s valuation after this most recent round of funding, it’s clear there is plenty of room to grow into the logistics industry’s huge and seemingly disaggregated value chain.

Powered by WPeMatico

OctoML, a Seattle-based startup that offers a machine learning acceleration platform built on top of the open-source Apache TVM compiler framework project, today announced that it has raised a $28 million Series B funding round led by Addition. Previous investors Madrona Venture Group and Amplify Partners also participated in this round, which brings the company’s total funding to $47 million. The company last raised in April 2020, when it announced its $15 million Series A round led by Amplify.

The promise of OctoML, which was founded by the team that also created TVM, is that developers can bring their models to its platform and the service will automatically optimize that model’s performance for any given cloud or edge device.

As Brazil-born OctoML co-founder and CEO Luis Ceze told me, since raising its Series A round, the company started onboarding some early adopters to its “Octomizer” SaaS platform.

Image Credits: OctoML

“It’s still in early access, but we are we have close to 1,000 early access sign-ups on the waitlist,” Ceze said. “That was a pretty strong signal for us to end up taking this [funding]. The Series B was pre-emptive. We were planning on starting to raise money right about now. We had barely started spending our Series A money — we still had a lot of that left. But since we saw this growth and we had more paying customers than we anticipated, there were a lot of signals like, ‘hey, now we can accelerate the go-to-market machinery, build a customer success team and continue expanding the engineering team to build new features.’ ”

Ceze tells me that the team also saw strong growth signals in the overall community around the TVM project (with about 1,000 people attending its virtual conference last year). As for its customer base (and companies on its waitlist), Ceze says it represents a wide range of verticals that range from defense contractors to financial services and life science companies, automotive firms and startups in a variety of fields.

Recently, OctoML also launched support for the Apple M1 chip — and saw very good performance from that.

The company has also formed partnerships with industry heavyweights like Microsoft (which is also a customer), Qualcomm and AMD to build out the open-source components and optimize its service for an even wider range of models (and larger ones, too).

On the engineering side, Ceze tells me that the team is looking at not just optimizing and tuning models but also the training process. Training ML models can quickly become costly and any service that can speed up that process leads to direct savings for its users — which in turn makes OctoML an easier sell. The plan here, Ceze tells me, is to offer an end-to-end solution where people can optimize their ML training and the resulting models and then push their models out to their preferred platform. Right now, its users still have to take the artifact that the Octomizer creates and deploy that themselves, but deployment support is on OctoML’s roadmap.

“When we first met Luis and the OctoML team, we knew they were poised to transform the way ML teams deploy their machine learning models,” said Lee Fixel, founder of Addition. “They have the vision, the talent and the technology to drive ML transformation across every major enterprise. They launched Octomizer six months ago and it’s already becoming the go-to solution developers and data scientists use to maximize ML model performance. We look forward to supporting the company’s continued growth.”

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion. Use code “TCARTICLE at checkout to get 20% off tickets right here.

Powered by WPeMatico

German drone technology startup Wingcopter has raised a $22 million Series A – its first significant venture capital raise after mostly bootstrapping. The company, which focuses on drone delivery, has come a long way since its founding in 2017, having developed, built and flown its Wingcopter 178 heavy-lift cargo delivery drone using its proprietary and patented tilt-rotor propellant mechanism, which combines all the benefits of vertical take-off and landing with the advantages of fixed-wing aircraft for longer distance horizontal flight.

This new Series A round was led by Silicon Valley VC Xplorer Capital, as well as German growth fund Futury Regio Growth. Wingcopter CEO and founder Tom Plümmer explained to the in an interview that the addition of an SV-based investor is particularly important to the startup, since it’s in the process of preparing its entry into the U.S., with plans for an American facility, both for flight testing to satisfy FAA requirements for operational certification, as well as eventually for U.S.-based drone production.

Wingcopter has already been operating commercially in a few different markets globally, including in Vanuatu in partnership with Unicef for vaccine delivery to remote areas, in Tanzania for two-way medical supply delivery working with Tanzania, and in Ireland where it completed the world’s first delivery of insulin by drone beyond visual line of sight (BVLOS, the industry’s technical term for when a drone flies beyond the visual range of a human operator who has the ability to take control in case of emergencies).

Wingcopter CEO and co-founder Tom Plümmer. Credit: Jonas Wresch

While Wingcopter has so far pursued a business as an OEM manufacturer of drones, and has had paying customers eager to purchase its hardware effectively since day one (Plümmer told me that they had at least one customer wiring them money before they even had a bank account set up for the business), but it’s also now getting into the business of offering drone delivery-as-a-service. After doing the hard work of building its technology from the ground up, and seeking out the necessary regulatory approvals to operate in multiple markets around the world, Plümmer says that he and his co-founders realized that operating a service business not only meant a new source of revenue, but also better-served the needs of many of its potential customers.

“We learned during this process, through applying for permission, receiving these permissions and working now in five continents in multiple countries, flying BVLOS, that actually operating drones is something we are now very good at,” he said. This was actually becoming a really good source of income, and ended up actually making up more than half of our revenue at some point. Also looking at scalability of the business model of being an OEM, it’s kind of […] linear.”

Linear growth with solid revenue and steady demand was fine for Wingcopter as a bootstrapped startup founded by university students supported by a small initial investment from family and friends. But Plümmer says the company say so much potential in the technology it had developed, and the emerging drone delivery market, that the exponential growth curve of its drone delivery-as-a-service model helped make traditional VC backing make sense. In the early days, Plümmer says Wingcopter had been approached by VCs, but at the time it didn’t make sense for what they were trying to do; that’s changed.

“We were really lucky to bootstrap over the last four years,” Plümmer said. “Basically, just by selling drones and creating revenue, we could employ our first 30 employees. But at some point, you realize you want to really plan with that revenue, so you want to have monthly revenues, which generally repeat like a software business – like software as a service.”

Wingcopter 178 cargo drone performing a delivery for Merck.

Wingcopter has also established a useful hedge regarding its service business, not only by being its own hardware supplier, but also by having worked closely with many global flight regulators on their regulatory process through the early days of commercial drone flights. They’re working with the FAA on its certification process now, for instance, with Plümmer saying that they participate in weekly calls with the regulator on its upcoming certification process for BVLOS drone operators. Understanding the regulatory environment, and even helping architect it, is a major selling point for partners who don’t want to have to build out that kind of expertise and regulatory team in-house.

Meanwhile, the company will continue to act as an OEM as well, selling not only its Wingcopter 178 heavy-lift model, which can fly up to 75 miles, at speeds of up to 100 mph, and that can carry payloads up to around 13 lbs. Because of its unique tilt-rotor mechanism, it’s not only more efficient in flight, but it can also fly in much windier conditions – and take-off and land in harsher conditions than most drones, too.

Plümmer tells me that Wingcopter doesn’t intend to rest on its laurels in the hardware department, either; it’s going to be introducing a new model of drone soon, with different capabilities that expand the company’s addressable market, both as an OEM and in its drones-as-a-service business.

With its U.S. expansion, Wingcopter will still look to focus specifically on the delivery market, but Plümmer points out that there’s no reason its unique technology couldn’t also work well to serve markets including observation and inspection, or to address needs in the communication space as well. The one market that Wingcopter doesn’t intend to pursue, however, is military and defense. While these are popular customers in the aerospace and drone industries, Plümmer says that Wingcopter has a mission “to create sustainable and efficient drone solutions for improving and saving lives,” and says the startup looks at every potential customer and ensures that it aligns with its vision – which defense customers do not.

While the company has just announced the close of its Series A round, Plümmer says they’re already in talks with some potential investors to join a Series B. It’s also going to be looking for U.S. based talent in embedded systems software and flight operations testing, to help with the testing process required its certification by the FAA.

Plümmer sees a long tail of value to be built from Wingcopter’s patented tilt-rotor design, with potential applications in a range of industries, and he says that Wingcopter won’t be looking around for any potential via M&A until it has fully realized that value. Meanwhile, the company is also starting to sow the seeds of its own potential future customers, with training programs in drone flights and operations it’s putting on in partnership with UNICEF’s African Drone and Data Academy. Wingcopter clearly envisions a bright future for drone delivery, and its work in focusing its efforts on building differentiating hardware, plus the role it’s playing in setting the regulatory agenda globally, could help position it at the center of that future.

Powered by WPeMatico