Series A

Auto Added by WPeMatico

Auto Added by WPeMatico

ULesson, an edtech startup based in Nigeria that sells digital curriculum to students through SD cards, has raised $7.5 million in Series A funding. The round is led by Owl Ventures, which closed over half a billion in new fund money just months ago. Other participants include LocalGlobe and existing investors, including TLcom Capital and Founder Collective.

The financing comes a little over a year since uLesson closed its $3.1 million seed round in November 2019. The startup’s biggest difference between now and then isn’t simply the millions it has in the bank, it’s the impact of the coronavirus pandemic on its entire value proposition.

ULesson launched into the market just weeks before the World Health Organization declared the coronavirus a pandemic. The startup, which uses SD cards as a low-bandwidth way to deliver content, saw a wave of smart devices enter homes across Africa as students adapted to remote education.

“The ground became wet in a way we didn’t see before,” founder and CEO Sim Shagaya said. “It opens up the world for us to do all kinds of really amazing things we’ve wanted to do in the world of edtech that you can’t do in a strictly offline sense,” the founder added.

Similar to many edtech startups, uLesson has benefited from the overnight adoption of remote education. Its positioning as a supplementary education tool helped it surface 70% month over month growth, said Shagaya. The founder says that the digital infrastructure gains will allow them to “go online entirely by Q2 this year.”

It costs an annual fee of $50, and the app has been downloaded more than 1 million times.

With fresh demand, Shagaya sees uLesson evolving into a live, online platform instead of an offline, asynchronous content play. The startup is already experimenting with live tutoring: it tested a feature that allowed students to ask questions while going through pre-recorded material. The startup got more than 3,000 questions each day, with demand so high they had to pause the test feature.

“We want you to be able to push a button and get immediate support from a college student sitting somewhere in the continent who is basically a master in what you’re studying,” he said. The trend of content-focused startups adding on a live tutoring layer continues when you look at Chegg, Quizlet, Brainly and others.

E-learning startups have been booming in the wake of the coronavirus. It’s led to an influx of tutoring marketplaces and content that promises to serve students. One of the most valuable startups in edtech is Byju’s, which offers online learning services and prepares students for tests.

But Shagaya doesn’t think any competitors, even Byju’s, have cracked the nut on how to do so in a digital way for African markets. There are placement agencies in South Africa and Kenya and offline tutoring marketplaces that send people to student homes, but no clear leader from a digital curriculum perspective.

“Everybody sees that Africa is a big opportunity,” Shagaya said. “But everybody also sees that you need a local team to execute on this.”

Shagaya thinks the opportunity in African edtech is huge because of two reasons: a young population, and a deep penetration of private school-going students. Combined, those facts could create troves of students who have the cash and are willing to pay for supplementary education.

The biggest hurdle ahead for uLesson, and any edtech startup that benefitted from pandemic gains, is distribution and outcomes. ULesson didn’t share any data on effectiveness and outcomes, but says it’s in the process of conducting a study with the University of Georgia to track mastery.

“Content efforts and products [will] live or die at the altar of distribution,” Shagaya said. The founder noted that in India, for example, pre-recorded videos do well due to social nuances and culture. ULesson is trying to find the perfect sauce for videos in markets around Africa and embed that into the product.

Powered by WPeMatico

DoNotPay, the consumer advice company that started out helping people easily challenge parking tickets, has come a long way since it launched. It’s expanded to help consumers cancel memberships, claim compensation for missed flights and even sue companies for small claims. In the early days of the pandemic, the startup helped its users file for unemployment, where many state benefit sites crashed.

Now the so-called “robot lawyer” has a new trick. The startup now lets you request information from U.S. federal and state government agencies under the Freedom of Information Act.

FOIA allows anyone to request information from the government, with some exceptions. But ask anyone with experience in filing FOIAs (hello!) and they can tell you that requesting data requires skill and practice to avoid having the request thrown out for being too broad, or not being specific enough. And when you do eventually get something back, it might not be what you expect.

That’s where DoNotPay wants to help. The new feature guides you through how to file a request for information, as well as wrangle the fee waivers and option to expedite processing — which is up to you to convince the government department why you should get the information for free and faster than regular FOIA requests. (In reality, the FOIA system is massively under-resourced, and responses can take months or years to get back.) After asking you a series of questions and what you want to request, DoNotPay generates a formal FOIA request letter using your answers and files it to the government agency on your behalf.

Do Not Pay’s website. (Screenshot: TechCrunch)

DoNotPay’s founder and chief executive Joshua Browder said he’s hoping the new feature can help consumers “beat bureaucracy.”

“Hundreds of users have requested a FOIA product, because the government makes it deliberately difficult and bureaucratic to exercise these rights,” Browder told TechCrunch.

Browder said that DoNotPay “would not exist” without FOIA laws. “When we got started appealing parking tickets, we used previous requests to see the top reasons why parking tickets were dismissed,” he said. Browder said he’s hoping the feature will help consumers uncover more injustices — just like with parking tickets — to feed his product with more features. “The overall strategy is to use any interesting FOIA data to build great new DoNotPay products,” he said.

DoNotPay raised $12 million in its Series A earlier this year, led by investment firm Coatue Management, with participation from Andreessen Horowitz, Founders Fund and and Felicis Ventures. The startup has 10 employees, including Browder, and is valued at about $80 million, the company confirmed.

The FOIA filing feature is free for academics and journalists, and is included as part of the company’s subscription service of $3 per month for everyone else.

Powered by WPeMatico

Jio Platforms, the biggest telecom operator in India and which has raised over $20 billion from Facebook, Google and other high-profile investors this year, is leading a financing round of a San Francisco-based startup that develops augmented reality mobile games.

Jio has led the Series A fundraise of Krikey, founded by sisters Jhanvi and Ketaki Shriram, the Indian firm said on Wednesday. They did not disclose the size of Krikey’s Series A round, but Jio said Krikey has raised $22 million to date.

Krikey has previously not disclosed any financing rounds, according to their listings on Crunchbase, CBInsights and Tracxn. Jio also did not share who else participated in Krikey’s new round.

As part of the announcement, Krikey has launched Yaatra, a new AR game that invites users to step in an action-adventure story to defeat a monster army. “Using weapons such as the bow and arrow, chakra, lightning and fire bolts, players can battle through different levels of combat and puzzle games,” Krikey said.

Jio subscribers in India will get exclusive access to a range of features in Krikey, available on Android and iOS, including a 3D avatar, and entry to some game levels and weapons. Jio said Yaatra game would also be made available to JioPhone feature-phone users.

Krikey has developed two additional games, including Gorillas, a game the startup developed in partnership with Ellen DeGeneres’s wildlife foundation.

“We believe AR has a huge potential in not just gaming but in many other industries to disrupt the way people interact with the world around them. We are very excited to use the phone as the window back into the natural world and hope that people’s experiences in empathising with birds and guerrillas and different ecosystems will encourage them to start to take real-world conservation behaviour changes,” said Jhanvi in an interview with Cheddar last year.

“Our vision with Krikey is to bring together inspiration and reality in an immersive way. With augmented reality, we are able to bring fantasy worlds into your home, straight through the window of your mobile phone,” said Jhanvi and Ketaki Shriram in a joint statement today. They have previously participated in Apple’s female entrepreneur camp.

In a statement, Akash Ambani, director of Jio, said, “Krikey will inspire a generation of Indians to embrace Augmented Reality. Our vision is to bring the best experiences from across the world to India and the introduction of Yaatra is a step in that direction. Augmented Reality gaming takes the user into a world of its own, and we invite every Jio and non-Jio user to experience AR through Yaatra.”

Jio has previously acquired music streaming service Saavn (which has since been rebranded to JioSaavn), and Haptik, a startup that develops conversational platforms and virtual assistants.

We have reached out to Jio and Krikey for more details.

Powered by WPeMatico

South Africa-based renewable energy startup Sun Exchange has raised $3 million to close its Series A funding round totaling $4 million.

The company operates a peer-to-peer, crypto-enabled business that allows individuals anywhere in the world to invest in solar infrastructure in Africa.

How’s that all work?

“You as an individual are selling electricity to a school in South Africa, via a solar panel you bought through the Sun Exchange,” explained Abe Cambridge, the startup’s founder and CEO.

“Our platform meters the electricity production of your solar panel. Arranges for the purchasing of that electricity with your chosen energy consumer, collects that money and then returns it to your Sun Exchange wallet.”

It costs roughly $5 a solar cell to get in and transactions occur in South African Rand or Bitcoin.

“The reason why we chose Bitcoin is we needed one universal payment system that enables micro transactions down to a millionth of a U.S. cent,” Cambridge told TechCrunch on a call.

He co-founded the Cape Town-headquartered startup in 2015 to advance renewable energy infrastructure in Africa. “I realized the opportunity for solar was enormous, not just for South Africa, but for the whole of the African continent,” said Cambridge.

“What was required was a new mechanism to get Africa solar powered.”

Sub-Saharan Africa has a population of roughly 1 billion people across a massive landmass and only about half of that population has access to electricity, according to the International Energy Agency.

Recently, Sun Exchange’s main market South Africa — which boasts some of the best infrastructure in the region — has suffered from blackouts and power outages.

Image Credits: Sun Exchange

Sun Exchange has members in 162 countries who have invested in solar power projects for schools, businesses and organizations throughout South Africa, according to company data.

The $3 million — which closed Sun Exchange’s $4 million Series A — came from the Africa Renewable Power Fund of London’s ARCH Emerging Markets Partners.

With the capital, the startup plans to enter new markets. “We’re going to expand into other Sub-Saharan African countries. We’ve got some clear opportunities on our roadmap,” Cambridge said, referencing Nigeria as one of the markets Sun Exchange has researched.

There are several well-funded solar energy startups operating in Africa’s top economic and tech hubs, such as Kenya and Nigeria. In East Africa, M-Kopa sells solar hardware kits to households on credit, then allows installment payments via mobile phone using M-Pesa mobile money. The venture is backed by $161 million from investors including Steve Case and Richard Branson.

In Nigeria, Rensource shifted from a residential hardware model to building solar-powered micro utilities for large markets and other commercial structures.

Sun Exchange operates as an asset free model and operates differently than companies that install or manufacture solar panels.

“We’re completely supplier agnostic. We are approached by solar installers who operate on the African continent. And then we partner with the best ones,” said Cambridge — who presented the startup’s model at TechCrunch Startup Battlefield in Berlin in 2017.

“We’re the marketplace that connects together the user of the solar panel to the owner of the solar panel to the installer of the solar panel.”

Abe Cambridge, Image Credits: TechCrunch

Sun Exchange generates revenues by earning margins on sales of solar panels and fees on purchases and kilowatt hours generated, according to Cambridge.

In addition to expanding in Africa, the startup looks to expand in the medium to long-term to Latin America and Southeast Asia.

“Those are also places that would really benefit from from solar energy, from the speed in which it could be deployed and the environmental improvements that going solar leads to,” said Cambridge.

Powered by WPeMatico

Juro, a UK startup that’s using machine learning tech and user-centric design to do for contracts what Typeform does for online forms, has caught the eye of Union Square Ventures. The New York-based fund leads a $5 million Series A investment that’s being announced this morning.

Also participating in the Series A are existing investors Point Nine Capital, Taavet Hinrikus (co-founder of TransferWise) and Paul Forster (co-founder of Indeed). The round takes Juro’s total raised to-date to $8M, including a $2M seed which we covered back in 2018.

London is turning into a bit of a hub for legal tech, per Juro CEO and co-founder Richard Mabey — who cites “strong legal services industry” and “strong engineering talent” as explainers for that.

It was also, he reckons, “a bit of a draw” for Union Square Ventures — making what Juro couches as a “rare” US-to-Europe investment in legal tech in the city via the startup.

“Having brand name customers in the US certainly helped. But ultimately, they look for product-led companies with strong cross-functional teams wherever they find them,” he adds.

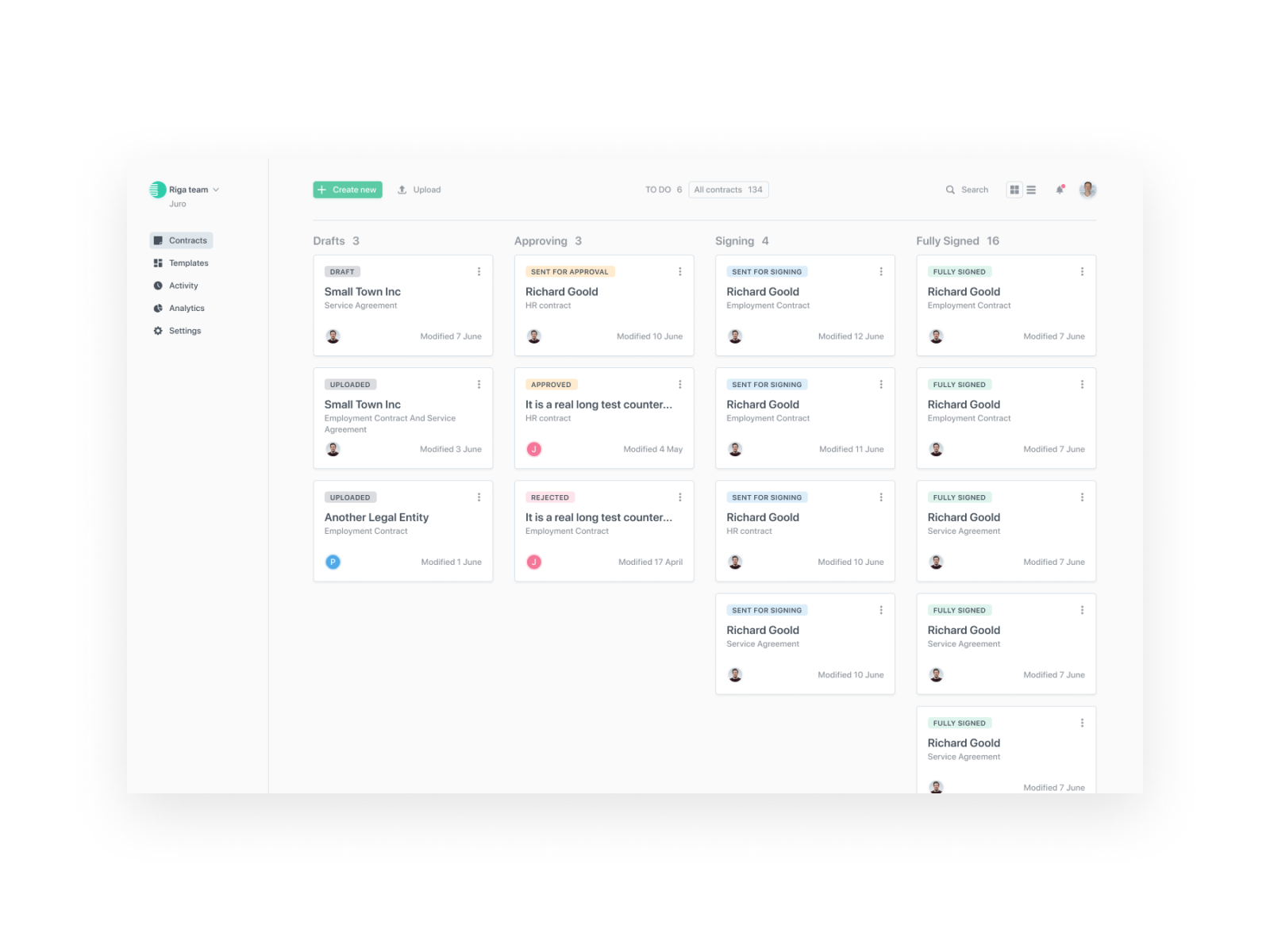

Juro’s business is focused on taking the tedium out of negotiating and drawing up contracts by making contract-building more interactive and trackable. It also handles e-signing, and follows on with contract management services, using machine learning tech to power features such as automatic contract tagging and for flagging up unusual language.

All of that sums to being a “contract collaboration platform”, as Juro’s marketing puts it. Think of it like Google Docs but with baked in legal smarts. There’s also support for visual garnish like animated GIFs to spice up offer letters and engage new hires.

“We have a data model underlying our editor that transforms every contract into actionable data,” says Mabey. “Juro contracts look like contracts, smell like contracts but ultimately they are written in code. And that code structures the data within them. This makes a contract manager’s life 10x easier than using an unstructured format like Word/pdf.”

“Still our main competitor is MS Word,” he adds. “Our challenge is to bring lawyers (and other users of contracts) out of Word, which is a significant task. Fortunately, Word was never designed for legal workflows, so we can add lots of value through our custom-built editor.”

Part of Juro’s Series A funds will be put towards beefing up its machine learning/data science capabilities, per Mabey — who says the overall plan at this point is to “double down on product”, including by tripling the size of the product team.

“That means hiring more designers, data scientists and engineers — building our engineering team in the Baltics,” he tells us. “There’s so much more we are excited to do, especially on the ML/data side and the funding unlocks our ability to do this. We will also be building our commercial team (marketing, sales, cs) in London to serve the EU market and expand further into the US, where we already have some customers on the ground.”

The 2016-founded startup still isn’t breaking out customer numbers but says it’s processed more than 50,000 contracts for its clients so far, noting too that those contracts have been agreed in 50+ countries. (“Everywhere from Estonia to Japan to Kazakhstan,” as Mabey puts it.)

In terms of who Juro users are, it’s still mostly “mid-market tech companies” — with Mabey citing the likes of marketplaces (Deliveroo), SaaS (Envoy) and fintechs (Luno), saying it’s especially companies processing “high volumes of contracts”.

Another vertical it’s recently expanded into is media, he notes.

“E-signature giants have grown massively in the last few years, and some are gradually encroaching into the contract lifecycle — but again, they deal with files (pdfs mostly) rather than dynamic, browser-based documentation,” he argues, adding: “In terms of new legal tech entrants — I’m excited by Kira Systems especially, who are working on unpicking pdf contracts post-signature.”

As part of the Series A, Union Square Ventures parter, John Buttrick, is joining Juro’s board.

Commenting in a supporting statement, Buttrick said: “We look for founders with products equipped to change an industry. While contract management might not be new, Juro’s transformative vision for it certainly is. There’s no greater proof of the product’s ease of use than the fact that we negotiated and closed the funding round in it. We’re delighted to support Juro’s team in making their vision a reality.”

Juro’s contract management platform — dashboard view

Powered by WPeMatico

The increase in activity in the pre-IPO secondary market means that founders, early employees, and investors are receiving liquidity much sooner in a company’s lifecycle than ever before. For most startups and privately-held companies, liquidity is often an issue for stockholders, as no market exists for selling shares and/or transfer restrictions can prevent their sale. Secondary stock transactions, however, are a way to work around this problem.

Here’s a quick look at how they work and what to keep in mind, especially if you’re going through the process for the first time. (If you’re not familiar, secondaries are transactions in which an existing stockholder sells their stock for cash to third parties or back to the company itself before the company undergoes an exit; traditionally, an exit refers to an M&A or an IPO.)

Offering secondary transactions to founders is a tool VCs have been using to win deals. For example, if a VC promises that the founders will receive $1,000,000 in cash through a secondary sale from a $15,000,000 venture financing round, the founders will likely prefer that VC’s term sheet to a term sheet from a VC that does not offer that deal.

Powered by WPeMatico

Extra Crunch offers members the opportunity to tune into conference calls led and moderated by the TechCrunch writers you read every day. This week, TechCrunch’s Connie Loizos hopped on the line with prominent investor, entrepreneur, thought leader, and Techstars co-founder Brad Feld to chat about the latest edition of his book “Venture Deals,” his advice to founders and investors, and his take on hot-button issues of the day.

In their conversation, Brad and Connie discuss the need to know information when it comes to preparing for, structuring and executing venture deals, and how that information has changed over the past several decades. Feld walks through the major topics that have been added in the latest edition of the book, such as how to handle venture debt, along with tactical attributes that aren’t currently in the book, such as secondary market trading.

Brad also shares his take on the most effective fundraising tactics for founders, and which common pieces of advice might be overblown.

Brad Feld: “I think the approach to the amount of money that you’re raising is both nuanced and evolves based on what financing round you’re at. So if you’re in an early round, some of the characteristics are different than if you’re in a later round. But I think the general truism… that I like to use when people say, ‘Well, how much money should I raise?’

I start with two variables and you the entrepreneur get to define those two variables. The two variables are: the amount of money you raise and what getting to the next level means. The amount of money you should raise is the amount of money that you need to get your business to the next level. There are lots of different ways to define what next level is and by forcing yourself internally to define next level and then define what you need in terms of capital to get to that next level… when you’re raising that first round of financing or even the second or third round of financing, it helps you size rationally what you need versus reactively to whatever the market characteristics are.

I actually encourage entrepreneurs to raise the least amount of money they need to get to the next level, or at least that’s the number that they go out to market with. Not a range, not a big number because you’re trying to drive some kind of valuation characteristic off a big number, but the amount of money that you actually think you need to get to the next level. Then if you can be oversubscribed, that’s an awesome situation.”

Feld and Connie dive deeper into current issues in the startup and venture landscape, including Brad’s take on the impact of the SoftBank Vision Fund, what went down internally and externally at both WeWork and Uber, as well as how boards, executives and founders can manage cult of personality and static company cultures.

For access to the full transcription and the call audio — and for the opportunity to participate in future conference calls — become a member of Extra Crunch. Learn more and try it for free.

Connie Loizos: I think the last time I saw you in person was out here in San Francisco at an event I was hosting and that was maybe two years ago?

Brad Feld: Yup, that’s right. That was at the Autodesk Lab if I remember correctly.

Loizos: Yes. It’s good to hear your voice, and thank you for joining us on this call. We have a lot of readers who are big fans of yours that are on the line and are eager to learn about your book “Venture Deals” and your broader thoughts about the current state of the market. That said — and I know you only have so much time — let’s dive first into the book. So Wiley, your publisher has just put out the fourth edition of this book “Venture Deals,” and it’s really easy to appreciate why. I was looking through it and it’s so incredibly instructive how venture deals come together and possible pitfalls to avoid. And given there are always new entrepreneurs emerging, it continues to be highly relevant.

How do you go about updating a book like this, given that some things change and some things stay the same?

Powered by WPeMatico

Maveron, Slow Ventures and Female Founders Fund have invested $10 million in a startup that claims it’s carving a new path to sobriety.

Tempest offers a $647 eight-week virtual “sobriety school” to help people, particularly women and “historically oppressed individuals,” get sober. The program is led by the company’s founder and chief executive officer Holly Whitaker, who conducts weekly video lectures and Q+As for participants. Offering their expertise as part of the package is marriage and family therapist Kim Kokoska; Valerie (Vimalasara) Mason-John, the co-founder of Eight Step Recovery; and wellness coach Mary Vance, among others.

Tempest teaches the underlying causes of addiction and the “importance of purpose, meaning and creativity in breaking addiction,” as well as how to manage cravings, how to navigate social situations as a non-drinker, how to develop a mindfulness practice and more. At the end of the program, participants can pay a $127 fee for an annual membership to the Tempest online community, where one can communicate with others who’ve completed the program.

Tempest Syllabus

Week 1: Recovery Maps + Toolkits

Week 2: Addiction & The Brain

Week 3: Habit and Night Ritual

Week 4: Yoga, Meditation and Breath

Week 5: Nutrition & Lifestyle

Week 6: Relationships & Community

Week7: Trauma & Therapy

Week 8: Purpose & Creativity

Week 8+ Wrapping Up + Next Steps

A snapshot of Tempest’s weekly coursework.

Founded in 2014, New York-based Tempest has raised about $14.3 million in total VC funding. Whitaker previously spent five years at One Medical, where she was the director of revenue cycle operations. Since founding Tempest, which has enrolled 4,000 participants to date, Whitaker received a two-book deal from Random House to document her methodologies and path to sobriety. Her first book, ‘Quit Like a Woman: The Radical Choice to Not Drink in a Culture Obsessed with Alcohol,’ will be released on December 31.

Today, her business has 28 employees and plans to build out its team, invest in marketing — where it’s historically had very low spend — and explore business opportunities within the enterprise using cash from the $10 million Series A.

“Sobriety, and the refusal to partake in alcogenic culture, is subversive, rebellious, and edgy.” – Tempest

The company is careful to clarify it’s not a detox or 12-step program, like Alcoholics Anonymous, which is structured around the Twelve Steps to recovery. Rather, Tempest can be used in combination with other programs or therapies, or as a first step down the path to recovery. Whitaker explains Tempest isn’t only for the clinically addicted or those who consider themselves addicts or alcoholics. The company welcomes people who have rejected these labels or simply want to cut alcohol out of their life.

“Tempest grew out of my own experience,” Whitaker, who has previously struggled with alcoholism and an eating disorder, tells TechCrunch. “It was a response to the lack of desirable and accessible options to address problematic drinking, the lack of options available for people who don’t identify as alcoholics but struggle with alcohol and the lack of options that have been created for women and other individuals. Everything had been created for men.”

Tempest is tailored to the needs of women and historically oppressed individuals, says Whitaker, though all genders are welcome to complete its course. Taking a holistic approach to recovery, participants are encouraged to address the factors that led them to drink in the first place, including “love lives, poor nutrition, stress, anxiety, crap friendships, consumerism, lack of purpose, unresolved family of origin issues, disenfranchisement, poverty, tight or unmanageable finances, lack of connection, fear, shitty jobs we hate, depression, unprocessed trauma, lack of meaning, unfulfilled dreams, never-ending to-do lists, never-measuring-upness,” the company writes.

Tempest’s website

I had the same question.

Alcoholics Anonymous (A.A.), the most popular and accessible approach to recovery, is free and open to anyone willing to acknowledge they have a drinking problem. A nonprofit organization, A.A. has more than 115,000 groups worldwide. The 84-year-old program is built on peer-support groups that gather regularly for discussion meetings. Over time, more seasoned members can become “sponsors,” helping newer entrants work through the Twelve Steps.

Tempest, alternatively, is taking a for-profit approach, charging for its tech-infused method. And where A.A. emphasizes in-person support groups, Tempest relies on video streams. Increasingly, telemedicine startups are enticing customers with convenient options for health and wellness care but whether people will truly pivot to telemedicine, tele-therapy or virtual sobriety schools is still up for debate. As for Tempest’s similarities to A.A., Whitaker says: “The only thing they have in common is that they are working to help people quit alcohol.”

“By just trying on sobriety or questioning our drink-centric culture, you are profoundly ahead of the pack.” – Tempest

In selling its sobriety school, Tempest evokes a sense of coolness, with phrases like “Sober is the new black” and “Your hangover goes away. Your social life doesn’t,” plastered on its website. In providing a priced and more exclusive route to sobriety, one might question Tempest’s ethics and motivations as it builds a business that capitalizes off of substance abuse. Whitaker, in defense, explains a virtual school fit for the historically powerless is a necessary addition to existing options: “Our program is centered on individuals who have been held out of power, who have been told to shut up and listen,” she said. “We aren’t looking at white, upper-class men. We are looking at a queer person from 2019.”

According to survey data published by Recovery.org, 89% of A.A. attendees are white, while 38% are female.

Tempest’s branding takes a cue from the D2C playbook. The company, led by women, has the opportunity to become the brand that represents sobriety, and it’s taking it. Tempest’s Series A, coupled with the influx of new-age non-alcoholic beverage brands backed by VCs, is representative of the perceived shift away from alcohol among the younger generations.

Millennials are drinking less alcohol and, according to the World Health Organization, there are 5% fewer alcohol drinkers in the world today than in 2000. Tempest’s school seems to cater more to the cohort of people who view ditching alcohol as a lifestyle perk, not those who stop drinking due to addiction.

Tempest founder and CEO Holly Whitaker

Seedlip, a non-alcoholic spirits company, and India’s Coolberg Beverages, which makes non-alcoholic beer, recently raised VC to cater to a similar demographic. Meanwhile, CBD-infused beverage brands like Sweet Reason, Cann and Recess are trendy and raising venture money. None of these, of course, are solutions for someone struggling with alcohol. Capital flowing into these brands merely indicates venture capitalists’ belief that consumers are steering away from traditional liquor and toward new products fit for a generation that is drinking less alcohol.

“By just trying on sobriety or questioning our drink-centric culture, you are profoundly ahead of the pack and among good company,” Tempest writes on its website. “Remember: 70-80% of adults drink depending on where you live; drinking is basic. Sobriety, and the refusal to partake in alcogenic culture, is subversive, rebellious, and edgy.”

Tempest says it has completed an efficacy study performed in consultation with researchers affiliated with the University of Buffalo and Syracuse University. In several years’ time, we’ll know whether the countless think pieces claiming millennials are done with alcohol were indeed true and whether the VC money into these upstarts was wasted or pure genius. As for Tempest, even if just providing a designated place on the internet for discussions around the struggles or benefits of sobriety, it has the potential to make a big impact on those in recovery or those seeking a lifestyle change.

“Alcohol is very similar to cigarettes,” Whitaker said. “We are in a time that we think drinking alcohol is natural, that we are supposed to do it. I thought that would change because to me, alcohol is entirely toxic. We are approaching this tipping point of realizing how toxic and unnecessary it is.”

Tempest is also backed by AlleyCorp, Refactor and Green D Ventures. Maveron’s Anarghya Vardhana has joined the startup’s board of directors as part of the latest deal.

Powered by WPeMatico

Fyle, a Bangalore-headquartered startup that operates an expense management platform, has extended its previous financing round to add $4.5 million of new investment as it looks to court more clients in overseas markets.

The additional $4.5 million tranche of investment was led by U.S.-based hedge fund Steadview Capital, the startup said. Tiger Global, Freshworks and Pravega Ventures also participated in the round. The new tranche of investment, dubbed Series A1, means that the three-and-a-half-year-old startup has raised $8.7 million as part of its Series A financing round, and $10.5 million to date.

The SaaS startup offers an expense management platform that makes it easier for employees of a firm to report their business expenses. The eponymous service supports a range of popular email providers, including G Suite and Office 365, and uses a proprietary technology to scan and fetch details from emails, Yash Madhusudhan, co-founder and CEO of Fyle, demonstrated to TechCrunch last week.

A user, for instance, could open a flight ticket email and click on Fyle’s Chrome extension to fetch all details and report the expense in a single click in real-time. As part of today’s announcement, Madhusudhan unveiled an integration with WhatsApp . Users will now be able to take pictures of their tickets and other things and forward it to Fyle, which will quickly scan and report expense filings for them.

These integrations come in handy to users. “Eighty percent to ninety percent of a user’s spending patterns land on their email and messaging clients. And traditionally it has been a pain point for them to get done with their expense filings. So we built a platform that looks at the challenges faced by them. At the same time, our platform understands frauds and works with a company’s compliances and policies to ensure that the filings are legitimate,” he said.

“Every company today could make use of an intelligent expense platform like Fyle. Major giants already subscribe to ERP services that offer similar capabilities as part of their offerings. But as a company or startup grows beyond 50 to 100 people, it becomes tedious to manage expense filings,” he added.

Fyle maintains a web application and a mobile app, and users are free to use them. But the rationale behind introducing integrations with popular services is to make it easier than ever for them to report filings. The startup retains its algorithms each month to improve their scanning abilities. “The idea is to extend expense filing to a service that people already use,” he said.

Until late last year, Fyle was serving customers in India. Earlier this year, it began searching for clients outside the nation. “Our philosophy was if we are able to sell in India remotely and get people to use the product without any training, we should be able to replicate this in any part of the world,” he said.

And that bet has worked. Fyle has amassed more than 300 clients, more than 250 of which are from outside of India. Today, the startup says it has customers in 17 nations, including the U.S. and the U.K. Furthermore, Fyle’s revenue has grown by five times in the last five months, said Madhusudhan, without disclosing the exact figures.

To accelerate its momentum, the startup is today also launching an enterprise version of Fyle that will serve the needs of major companies. The enterprise version supports a range of additional security features, such as IP restriction and a single sign-in option.

Fyle will use the new capital to develop more product solutions and integrations and expand its footprint in international markets, Madhusudhan said. The startup, which just recently set up its sales and marketing team, will also expand the headcount, he said.

Moving forward, Madhusudhan said the startup would also explore tie-ups with ERP providers and other ways to extend the reach of Fyle.

In a statement, Ravi Mehta, MD at Steadview Capital, said, “intelligent and automated systems will empower businesses to be more efficient in the coming decade. We are excited to partner with Fyle to transform one of the core business processes of expense management through intelligence and automation.”

Powered by WPeMatico

Silicon Valley has many dreams. One dream — the Hollywood version anyway — is for a down-and-out founder to begin tinkering and coding in their proverbial garage, eventually building a product that is loved by humans the world over and becoming a startup billionaire in the process.

The more prosaic and common version of that Valley dream though is to join an early-stage company right before its growth kicks into high gear. Sure, those early employees might only have a smidgen of equity, but that equity could be worth a whole heck of a lot if they join the right startup.

Every startup has a window of opportunity, a timeframe in which early employees can join while the stock option strike prices are low and the equity grants are high. Join before the big uptick in valuation, and suddenly what might have been an otherwise nice couple of hundred K dollars in the coming years becomes actually, well, in the Bay Area, a reasonably-sized domicile.

Yet, that opportune window seems to be shrinking in size, making it harder for potential startup employees to nail the timing necessary to garner their own best financial return.

For every Roblox, which as we profiled in-depth this week, took almost two decades to reach its current apotheosis, there is a Brex, which seems to reach unicorn status in no time at all. And such stories — while certainly anecdotal — seem to be more commonplace than ever.

Part of the reason for that fast early valuation growth is that Silicon Valley has simply learned how to grow even faster, even earlier. As venture capitalist Reid Hoffman and Chris Yeh discuss in their book Blitzscaling, there are now frameworks and tried-and-true techniques to not just grow a startup, but to grow it at a dizzying rate. Through better marketing channels, growth strategies, and product development, we have indeed made progress at cutting at least some of the time to better valuations.

That rapid transformation from nothing to everything though gives very little time for early employees to discover a startup through the grapevine when the financial conditions are still interesting.

Half a decade ago, I wrote about the plight of early employees in an article I entitled “The Problem with Founders.” I wrote then that:

The secret of Silicon Valley is that the benefits of working at a startup accrues almost entirely to the founders, and that’s why people repeat the advice to just go start a business. There is a reason it is hard to hire in Silicon Valley today, and it isn’t just that there are a lot of startups. It’s because engineers and other creators are realizing that the cards are stacked against them unless they are the ones in charge.

My reasoning then was simple: early employees take on pretty much just as much risk as their founders do, but for a fraction of the equity. Now, with startups jumping to unicorn status in sometimes as short as a handful of months, that risk-reward ratio seems to be even more off-kilter for those early employees.

And it doesn’t just have to be a Brex -scale transformation either. The rapid increase in the size and valuation of series A rounds of financing the past three years means that engineers and salespeople who might have an employee number in the low double digits are suddenly seeing their options struck at a couple of hundred million in valuation. Exits, meanwhile, aren’t suddenly getting richer to compensate.

I started to notice this pattern over the past few weeks in the course of several conversations with software engineering friends of mine who had gotten excited about very early-stage companies — say, just a handful of employees — but who walked away from their offer letters due to already sky-high company valuations.

Now, there is an argument to be made that joining these sorts of companies is precisely where the best opportunities lie. Sure, the valuations are already high, but these are startups with the financial resources and the backing that might allow them to compete effectively. So maybe the equity is smaller and more expensive, but ultimately, if the startup is more likely to be successful, the expected value function might actually be favorable.

Maybe. Yet it is also hard to see how these startups, which despite their rich valuations have barely laid any foundation for success, are a safer bet than a similarly-valued startup with years of experience under its belt and a growth strategy based upon dependable results. Even worse, early employees are perhaps taking even more financial risk, since the preference stack of the venture capital could mean that smaller exits are particularly unfavorable to them.

Plus, the shrinking opportunity window for leading startups means that the difference in financial outcome between two early employees — what could be millions of dollars upon an exit — could have been decided based on who joined the week before the other. That doesn’t seem fair or right, but is increasingly widespread in our industry.

As with most macroeconomic structural changes, there’s not much for anyone to do. Founders aren’t going to take lower valuations or less money just to make the lives of their early employees a bit more rosy, and certainly venture capitalists aren’t going to lowball their offers in a hyper-competitive investment environment. Indeed, the very excitement of a sudden unicorn may be the best attraction for candidates to hear a startup’s pitch and ultimately join.

But when it comes to that Silicon Valley dream of a nice house from a decent return on exit, it’s getting narrower and less widely-distributed. Blitzscaling is making a lot of people a lot of wealth, but early employees? Not so much.

Powered by WPeMatico