Private Equity

Auto Added by WPeMatico

Auto Added by WPeMatico

Major gains in online advertising have boosted valuations for adtech startups since the pandemic began, but one insider says investors are missing the party.

“Adtech is having a moment,” writes industry veteran Casey Saran.

“And while much of the oxygen has been soaked up by large legacy companies hitting the public market, there have been smaller deals that indicate a hunger for better creative adtech.”

Saran shares five reasons “why VCs should consider ratcheting up their investment into adtech startups building the next generation of creative tools.”

Full Extra Crunch articles are only available to members

Use discount code ECFriday to save 20% off a one- or two-year subscription

On Wednesday, September 22 at 9:05 a.m PT, I’m moderating “The Path for Underrepresented Entrepreneurs,” a panel discussion at Disrupt 2021.

Our conversation will examine some of the unique challenges facing founders from historically marginalized groups, the strategies they used along the way, and the disruptive changes we need to consider if we want to see fundamental change.

I’ll be speaking with:

I hope you’ll attend; we’ll take audience questions after our discussion concludes. Thanks very much for reading Extra Crunch this week, and have a great weekend.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Image Credits: AndrewLilley (opens in a new window) / Getty Images

Congratulations on shipping your product, but how much do you know about your target customers?

Companies that haven’t created an ideal customer profile and performed a SWOT analysis are making big bets on guesswork and intuition. Sometimes that works out, but more frequently, it leads to tears.

In a guest post that walks readers through the fundamentals of creating customer personas that map to your company’s goals, Grammarly product marketing lead Bryan Dsouza shares five basic requirements for customer acquisition.

“Understanding and executing on these things can guarantee you that first customer win, provided you do them well and with sincerity,” he says.

“Your investors will also see the fruits of your labor and be comforted knowing their dollars are at good work.”

Image Credits: joshblake (opens in a new window) / Getty Images

In school, it’s highly unethical to copy someone else’s work and pass it off as your own. In business, however, it is expected.

Xiaoyun TU, global director of demand generation at Brightpearl, wrote a comprehensive guide for how to use the key metric of return on advertising spend (ROAS) to triple your company’s lead generation.

“A ‘good’ ROAS score is different for each company and campaign,” she says. “If your figure isn’t where you’d like it to be, you can leverage ROAS data to create targeted campaigns and personalized experiences.”

Image Credits: porcorex (opens in a new window) / Getty Images

Most of us prefer to trust our instincts instead of letting automated tools help us make decisions, particularly when it comes to hiring. But that’s not smart.

If your startup relies on an ad hoc hiring process, you’re probably not tracking candidates properly, there’s likely little consistency regarding how they’re treated, and bias can play a major role in who gets hired.

It’s fine to be skeptical of automated hiring tools — but not ignorant.

Image Credits: Nigel Sussman (opens in a new window)

In yesterday’s edition of The Exchange, Anna Heim and Alex Wilhelm speculated about the conditions that could combine to cool off a hot startup market currently fueled by low interest rates and a sweeping digital transformation.

“From where we stand, the factors underpinning the startup fundraising boom appear solid and unlikely to unwind overnight. Still, no golden period shines forever, and even today’s luster will eventually tarnish.”

Image Credits: Smith Collection/Gado / Getty Images

Before news broke this week that Intuit was acquiring Mailchimp for $12 billion, the ’80s-born fintech giant’s biggest buy was spending $7.1 billion last year for Credit Karma.

In the last few years, Mailchimp “has been expanding upon its core email marketing functionality” with offerings like web design and CRM, writes enterprise reporter Ron Miller.

The industry watchers he interviewed said the move signals Intuit’s interest in acquiring and serving more SMB customers with a variety of tools:

Image Credits: Nigel Sussman (opens in a new window)

“One of my favorite long-term issues with the late-stage startup market is that it is far better at creating value than it is at finding an exit point for that accreted value,” Alex Wilhelm writes for The Exchange. “More simply, the startup market is excellent at creating unicorns but somewhat poor at taking them public.”

That’s good news for Forge Global, a technology startup that operates a market for secondary transactions in private companies, with Alex dubbing its plans to go public via a SPAC combination “perfectly reasonable.”

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie,

At Burning Man a few years ago, I was arrested and charged with a misdemeanor for smoking marijuana in public (in my car) and driving under the influence.

I currently have a green card and want to apply for U.S. citizenship next year.

Can I? If so, how should I handle my criminal record?

— Remorseful About the Reefer

Image Credits: Nigel Sussman (opens in a new window)

Alex Wilhelm and Anna Heim continued their tour of U.S. cities after hitting up Chicago and Boston in recent weeks.

This time, they dug into Atlanta’s booming startup scene, which is seeing record capital inflows.

“The picture that forms is one of a city enjoying a rising tide of venture activity, boosted by some local dynamics that may have helped some of its earlier-stage companies scale for cheaper than they might have in other markets,” they write.

Powered by WPeMatico

Startups are raising record sums around the world, thanks to several contributing factors. As The Exchange explored yesterday, historically low interest rates have helped venture capitalists raise more capital than ever, to pick an example.

Low rates have helped startups in another manner: As yields fell for certain assets, investors chased returns by betting on growth. And in recent years, the investing classes turned their attention to public software companies, bidding up the value of their revenue to record highs.

This raised the worth of startups in general terms, and private tech companies’ comps enjoyed a steady, upward climb in the value of their revenues. If the value of a dollar of SaaS revenue was worth $1 one year and $2 the next, the repricing was good for private companies even if we were tracking the metrics from the perspective of public companies.

The free ride could be ending.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

I’ve held back from covering the value of software (SaaS, largely) revenues for a few months after spending a bit too much time on it in preceding quarters — when VCs begin to point out that you could just swap out numbers quarter to quarter and write the same post, it’s time for a break. But the value of software revenues posted a simply incredible run, and I can’t say “no” to a chart.

The pace at which software revenues were repriced upwards in the last few years is simply astounding. Per the Bessemer Cloud Index, back in 2016, the median revenue multiple for public SaaS companies was around 5x. When 2018 began, median SaaS multiples had expanded to around 7x.

The pace at which software revenues were repriced upwards in the last few years is simply astounding. Per the Bessemer Cloud Index, back in 2016, the median revenue multiple for public SaaS companies was around 5x. When 2018 began, median SaaS multiples had expanded to around 7x.

That’s a 40% climb in pricing, but it proved to be just a foretaste of the feast to come.

By the end of 2019, the median figure had appreciated to around the 9x mark. And today it has shot to just under 18x. That is why software companies have been able to raise so much money, earlier, and in larger chunks. Every dollar of recurring revenue they sold was worth $5 in market cap in mid-2016. At the end of 2019, that same dollar of revenue was worth $9. And today, for the median public software company, it’s valued at around $18.

There are nuances to the data, but we care less about exacting definitions than the directional change it describes: The median value of SaaS revenues more than tripled from 2016 to 2021. That’s an insane amount of growth.

Powered by WPeMatico

Investors in AI-first technology companies serving the defense industry, such as Palantir, Primer and Anduril, are doing well. Anduril, for one, reached a valuation of over $4 billion in less than four years. Many other companies that build general-purpose, AI-first technologies — such as image labeling — receive large (undisclosed) portions of their revenue from the defense industry.

Investors in AI-first technology companies that aren’t even intended to serve the defense industry often find that these firms eventually (and sometimes inadvertently) help other powerful institutions, such as police forces, municipal agencies and media companies, prosecute their duties.

Most do a lot of good work, such as DataRobot helping agencies understand the spread of COVID, HASH running simulations of vaccine distribution or Lilt making school communications available to immigrant parents in a U.S. school district.

The first step in taking responsibility is knowing what on earth is going on. It’s easy for startup investors to shrug off the need to know what’s going on inside AI-based models.

However, there are also some less positive examples — technology made by Israeli cyber-intelligence firm NSO was used to hack 37 smartphones belonging to journalists, human-rights activists, business executives and the fiancée of murdered Saudi journalist Jamal Khashoggi, according to a report by The Washington Post and 16 media partners. The report claims the phones were on a list of over 50,000 numbers based in countries that surveil their citizens and are known to have hired the services of the Israeli firm.

Investors in these companies may now be asked challenging questions by other founders, limited partners and governments about whether the technology is too powerful, enables too much or is applied too broadly. These are questions of degree, but are sometimes not even asked upon making an investment.

I’ve had the privilege of talking to a lot of people with lots of perspectives — CEOs of big companies, founders of (currently!) small companies and politicians — since publishing “The AI-First Company” and investing in such firms for the better part of a decade. I’ve been getting one important question over and over again: How do investors ensure that the startups in which they invest responsibly apply AI?

Let’s be frank: It’s easy for startup investors to hand-wave away such an important question by saying something like, “It’s so hard to tell when we invest.” Startups are nascent forms of something to come. However, AI-first startups are working with something powerful from day one: Tools that allow leverage far beyond our physical, intellectual and temporal reach.

AI not only gives people the ability to put their hands around heavier objects (robots) or get their heads around more data (analytics), it also gives them the ability to bend their minds around time (predictions). When people can make predictions and learn as they play out, they can learn fast. When people can learn fast, they can act fast.

Like any tool, one can use these tools for good or for bad. You can use a rock to build a house or you can throw it at someone. You can use gunpowder for beautiful fireworks or firing bullets.

Substantially similar, AI-based computer vision models can be used to figure out the moves of a dance group or a terrorist group. AI-powered drones can aim a camera at us while going off ski jumps, but they can also aim a gun at us.

This article covers the basics, metrics and politics of responsibly investing in AI-first companies.

Investors in and board members of AI-first companies must take at least partial responsibility for the decisions of the companies in which they invest.

Investors influence founders, whether they intend to or not. Founders constantly ask investors about what products to build, which customers to approach and which deals to execute. They do this to learn and improve their chances of winning. They also do this, in part, to keep investors engaged and informed because they may be a valuable source of capital.

Powered by WPeMatico

Funding for Black entrepreneurs in the U.S. hit nearly $1.8 billion in the first half of 2021 — a fourfold increase from the previous year. But most venture-backed startups are “still overwhelmingly white, male, Ivy-League-educated and based in Silicon Valley,” according to a study conducted by RateMyInvestor and Diversity VC.

With venture investors committing to funding Black and minority founders, alongside the growing availability of government-backed proposals, such as New Jersey allocating $10 million to a seed fund for Black and Latinx startups, can we expect to see fundamental change? Or will we have to repeat the same conversations about representation failings within VC funds?

Crunchbase examined the access to capital in the venture-backed startup ecosystem and proved that many industry leaders still worry that nothing will drastically shift. As a Black fintech founder, I believe that venture investors are making safe bets and investing in late-stage founders instead of early or even pre-seed stages.

But what about those minority founders who don’t have family, friends or connections to lean on for the first $250,000? Venture funding does remain elusive, but here are some tricks for startup founders to hack the system.

Getting your foot in the door with new venture capitalist partners is challenging, and it is often easy for minority founders to be naive at first. I thought that reading TechCrunch and analyzing other VC deals I saw in the news would help me land multiple responses and speak the language of those who managed to score million-dollar deals for their startups. However, I didn’t receive a single response while other founders received VC investment for basic ideas.

This is something I had to learn the hard way: What you hear in the media or read on a company blog post often simplifies the process, and sometimes fails to cover the trajectory that minority founders, in particular, must follow to secure funding.

I experienced hundreds of rejections before raising $2 million to start a mobile payment platform, Bleu, using beacon technology to drive simple and secure payments. It is a huge mountain to climb and a full-time job to continuously pitch your vision and yourself to reach the first meeting with a VC fund — and that’s still miles away from a funding discussion.

These discussions then bring further biases to the surface. If you sat in the conference rooms or on those Zoom calls and heard the types of deals proposed to minority founders, you’d see how offensive they can be. Often, these founders are offered all the money they have requested — but don’t be fooled. It is usually not given all at once due to what I consider to be a lack of trust. Essentially, interval funding equates to being babysat.

Therefore, as a minority founder, you have to realize that it will be a long ride, and you will face rejections because you are at a disadvantage before even opening your mouth to pitch your idea. It is all possible, but patience is key.

Once I figured out how complicated the funding process was, my coping mechanism was to figure out how to capitalize on the business ideas I already had in place in case I never received any VC funding.

Think: How could you make money without an institutional investor, friends, family or internal networks? You’ll be surprised by your entrepreneurial thirst for success when you’ve experienced 100 rejections. This is why minority businesses caught in these testing situations can quickly gain the upper hand, whether through ancillary and side businesses or crowdfunding over GoFundMe and Kickstarter.

Although generally considered non-essential, ancillary companies do provide a regular flow of income and services to assist your core business idea. Most importantly, a recurring revenue stream outside your core business demonstrates to investors that you can create valuable products and acquire loyal customers.

Make sure to find a niche market and carry out surveys with potential clients to find out what specific needs they have. Then, build a product with their feedback in mind and launch it to beta clients. When you publicly release the product, find resellers to keep internal headcount low and generate recurring revenue.

Don’t take ancillaries lightly, though; they are not just a side business. There can be payment issues if you get hooked on them for revenue, distractions from clients or partners wanting custom requests, and supply chain problems.

In my case, I built a point-of-sale (POS) software platform to sell to merchants, which gave me a different revenue stream that could integrate with Bleu’s payment technology. These ancillary businesses can help fund your core business until you manage to plan how to launch fully or source further funding.

In 2019, The New York Times published an article headlined “More Start-Ups Have an Unfamiliar Message for Venture Capitalists: Get Lost.” It highlights how more and more entrepreneurs shunned by the VC funding route are turning to alternatives and forming counter-movements. There are always alternatives to look at if the fundraising process is proving to be too arduous.

Accelerators allow ventures to define their products or services, quickly build networks and, most importantly, sit at tables they wouldn’t be able to on their own. Applying to accelerators as a minority founder was the real turning point for me because I met a crucial investor who allowed us to build credibility and open up to new networks, investors and clients.

I would suggest looking out for accelerators explicitly searching for minority founders by using platforms such as F6S. They match you with accelerators and early growth programs committed to innovation in various global industries, like financial technology. That’s how I found the VC FinTech Accelerator in 2016, where one-third of founders were from minority backgrounds.

Then, Bleu earned a spot in the 2020 class of the IBM Hyper Protect Accelerator dedicated to supporting innovative startups in fintech and health tech industries. These types of accelerators offer startups workshops, technical and business mentorship, and access to a network of partners, customers and stakeholders.

You can impress accelerators by creating a pitch deck and a company video less than two minutes long that shows your founder and the product, and engaging with the fintech community to spread the news.

The other alternative to accelerators is government funds, but they have had little success investing in startups for myriad reasons. It tends to be a more hands-off approach as government funds are not under significant pressure from limited partners (LPs, either institutional or individual investors) to perform.

What you need as a minority founder is an investor who is an active partner but, with government-backed funds, there is less demand to return the capital. We have to ask ourselves whether governments are really searching for the best minority-owned startups to help them get sufficient returns.

There are many unconscious social stigmas, stereotypes and unseen biases that exist in the U.S. And you’ll find those cultural dynamics are radically different in other countries that don’t have the same history of discrimination, especially when looking at a team or assessing founders.

I also noticed that, as well as reduced bias, investors out of Southeast Asia, Nordic countries and Australia seemed far more likely to take risks on new contactless payment technology as cash use decreased across their regions. Take Klarna and Afterpay as examples of fintech success stories.

First, I engaged in market research and pored over annual reports to decide whether I should look abroad for funding, instead of applying to funds closer to home. I looked at Nielsen reports, payment publications, PaymentSource and numerous government documents or white papers to figure out the cash usage globally.

My investigations revealed that fintech in Australia was far ahead of the curve, with four-fifths of the population using contactless payments. The financial services sector is also the largest contributor to the national economy, contributing around $140 billion to GDP a year. Therefore, I spoke to the Australian Department of Foreign Affairs and Trade in the U.S., and they recommended some regulatory payment groups.

I immediately flew to Australia to meet with the banking community, and I was able to find an Australian investor by word of mouth who was surrounded by the demand for mobile payment solutions.

In contrast, an investor in the U.S. still using cash and card had no interest in what I had to say. This highlights the importance of market research and seeking out investors rather than waiting for them to come to you. There is no science to it; leverage your network and reach out to people over LinkedIn, too.

VC funding needs to become more inclusive for women and minority groups by tackling the pipeline problem and addressing the level of diversity within VC funds. All of the networks that VCs reach out to first tend to come from university programs at Stanford, MIT and Harvard. These more privileged and wealthy students are able to easily leverage the traditional and outdated networks built to benefit them.

The number of venture dollars flowing to Black and Latinx founders is dismally low partly due to this knowledge gap; many female and minority founders don’t even know that VC funding is an option for them. Therefore, if you do receive seed funding, spread the news about it within your networks to help others.

Inclusion starts at the educational level but, when the percentage of Black and minority students at these elite colleges are still low, you can see why minority representation is needed in the VC ranks. Even if representation rises by a percent, that would be a significant change.

There are increasing numbers of VC funds announcing initiatives and interest in investing in minority businesses, and I would recommend looking at these in-depth. But what about the demographics of the VC firms? How many ethnicities are present in the executive ranks?

To change the venture-backed startup ecosystem, we need to start at the top and diversify those signing the checks. Looking toward the future, it is Black-led funds, like Sequoia, or others that focus on diversity, like Women’s Venture Fund, BackStage Capital and Elevate Capital Inclusive Fund, that are lighting the way to solutions that will reflect the diversity of the U.S.

It’s up to the investor community at large to be intentional about building relationships with, and ultimately providing funding to, more women and minority-led startups.

Despite the barriers and hurdles minority founders face when searching for VC funding, more and more avenues for acquiring funding are appearing as the disparities are brought to the media’s attention.

As the outdated system adjusts, the key is to continue preparing yourself for rejections and searching for appropriate accelerators to build vital networks. Then, if you aren’t having any luck, consider what you could do with your business idea without the VC funding or turn to foreign markets, which may have a different setup and varied opportunities.

Powered by WPeMatico

China is becoming a superpower in the tech industry. According to Straits Times, China is the only place in the world where it takes less than six years for a startup to become a unicorn — it takes seven years in the U.S., eight years in the U.K. and 11 years in Germany. Despite geopolitical tensions and recent amendments in CFIUS, it is hard to ignore China.

When I joined Runa Capital almost a year ago, my task was to help our portfolio companies enter the Chinese market, find the right partners and raise funding from Chinese investors. And almost on every call with our startups, colleagues from Runa or other global VCs, I heard: Is it a good idea to raise from a Chinese VC? Is it OK to co-invest with Chinese investors? I was surprised to learn that there is little research answering such questions, as there is a lack of adequate information in English about Chinese investments.

Access to the Chinese market seems to be an obvious reason to invite Chinese funds aboard, but only about 20% of Western startups with Chinese capital have operations in China.

So as a Mandarin-speaking specialist, I decided to fill this gap by conducting a study based on Chinese VC database ITjuzi (the Chinese version of Crunchbase) with the help of our powerful data science resources developed by Danil Okhlopkov.

Below, I will try to answer the following questions using statistics and a case-based approach:

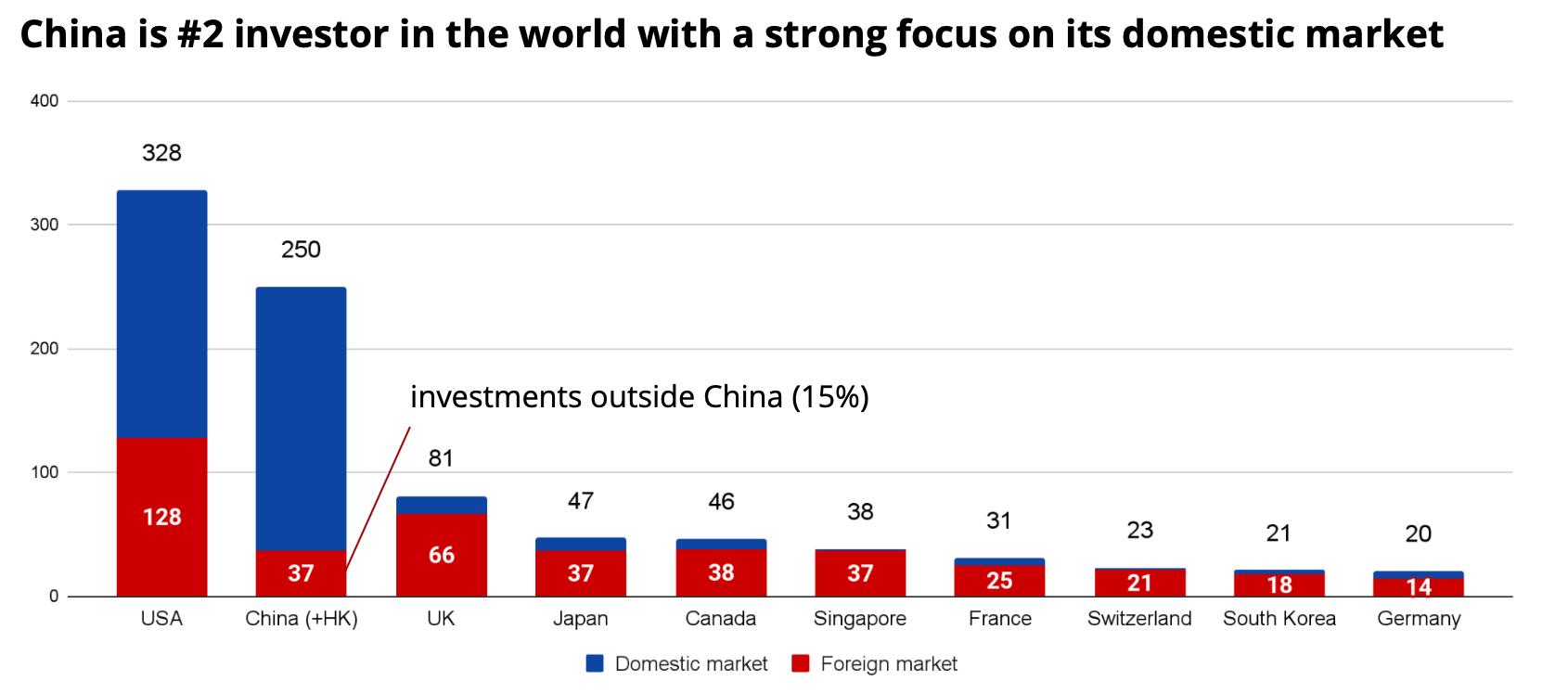

After studying data from ITjuzi, we estimated that Chinese funds invested around $250 billion in 2020 (three times higher than the figure reported in Crunchbase). This figure puts Chinese VC investments only 30% lower than investments by U.S. funds, but three times that of U.K. funds and 12.5 times more than German funds.

Fig. 1 — Comparison of investment from different countries in 2020, $bn. Source: Crunchbase, ITjuzi. Image Credits: Denis Kalinin

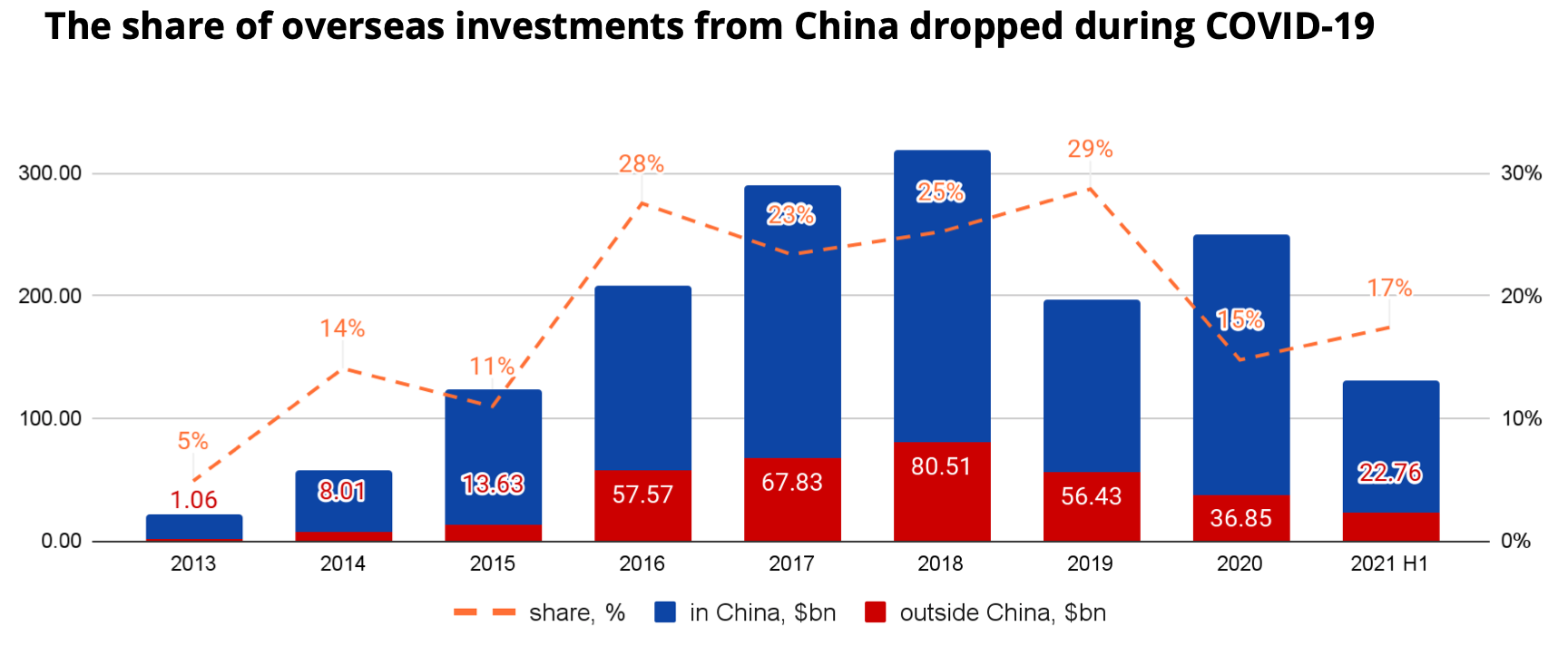

However, only 15% of investments in 2020 and 17% of investments in the first half of 2021 were in companies outside China, significantly lower than in 2019. This appears to be because during COVID, China’s economy recovered much faster than other countries’, so many Chinese investors preferred to redirect their capital flows to the domestic market.

On the other hand, there is great potential for overseas investments to rebound as soon as the borders reopen and the global economy starts to recover.

Fig. 2 — Dynamics of Chinese investments. $bn. Source: Crunchbase, ITjuzi. Image Credits: Denis Kalinin

We can also see that Chinese investors are eyeing European startups favorably, which is related to U.S.-China geopolitical tensions as well as the fact that the European VC market is becoming mature.

Powered by WPeMatico

Southeast Asian tech companies are drawing the attention of investors around the world. In 2020, startups in the region raised over $8.2 billion, about four times more than they did in 2015. This trend continued in 2021, with regional M&A hitting a record high of $124.8 billion in the first half of 2021, up 83% from a year earlier.

This begs the question: Who exactly is investing in Southeast Asia?

Let’s explore the three key types of investors pouring money into and driving the growth of Southeast Asia’s tech ecosystem.

Over 229 family offices have been registered in Singapore since 2020, with total assets under management of an estimated $20 billion.

Southeast Asia has become an attractive market for U.S. and Chinese tech firms. Internet penetration here stands at 70%, higher than the global average, and digital adoption in the region remains nascent — it wasn’t until the pandemic that adoption of digital services such as e-wallets and online shopping took off.

China’s tech giants Tencent and Alibaba were among the first to support early e-commerce growth in Southeast Asia with investments in Sea Limited and Lazada, and have since expanded their footprint into other internet verticals. Alibaba has backed Akulaku, M-Pay (eMonkey), DANA, Wave Money and Mynt (GCash), while Tencent has invested in Voyager Innovations (PayMaya), SHAREit, iflix, Ookbee and Sanook.

U.S. tech firms have also recently entered the scene. In June 2020, Gojek closed a $3 billion Series F round from Google, Facebook, Tencent and Visa. Google, together with Singapore’s Temasek Holdings, invested some $350 million in Tokopedia in October. Meanwhile, Microsoft invested an undisclosed amount in Grab in 2018 and has invested $100 million in Indonesian e-commerce firm Bukalapak.

In Q1 2021, Southeast Asian startups raised $6 billion, according to DealStreetAsia, positioning 2021 as another record year for VC investment in the region.

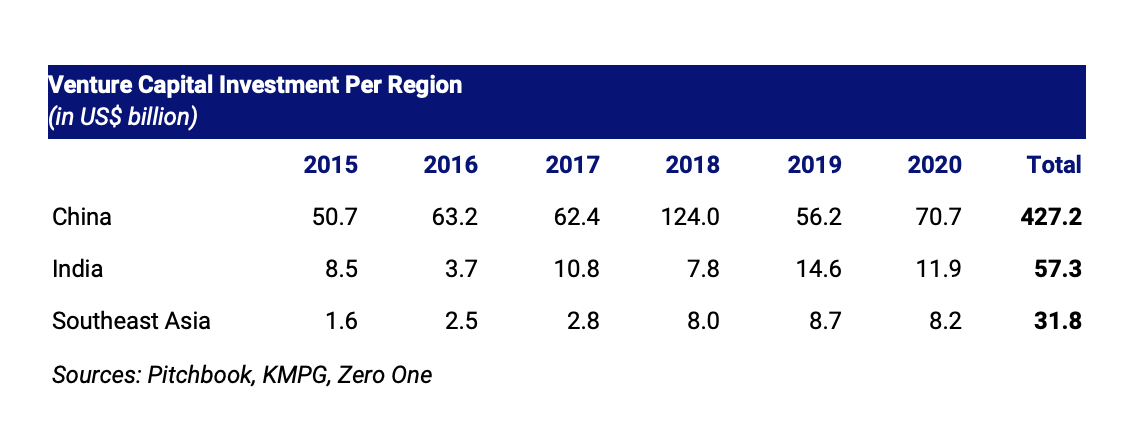

The region is also rising in prominence as a destination for investment capital relative to the rest of Asia. Regional VC investment grew 5.2 times to $8.2 billion in 2020 from $1.6 billion in 2015, as we can see in the table below.

Image Credits: Jungle VC

Southeast Asia also has many opportunities for VC investment relative to its market size. From 2015 to 2020, China saw VC investment of nearly $300 per person; for Southeast Asia — despite a recent investment boom — this metric sits at just $47.50 per person, or just a sixth of that in China. This implies a substantial opportunity for investments to develop the region’s digital economy.

The region’s rising population and growth prospects are higher due to China’s population growth challenges, alongside the latter’s higher digital economy market saturation and maturity.

Powered by WPeMatico

Marshmallow — a U.K.-based car insurance provider that has made a name for itself in the market by providing a new approach to car insurance aimed at using a wider set of data points and clever algorithms to net a more diverse set of customers and provide more competitive rates — is announcing a milestone today in its life as a startup, as well as in the bigger U.K. tech world.

The London company — co-founded by identical twins Oliver and Alexander Kent-Braham and David Goaté — has raised $85 million in a new round of funding. The Series B valuation is significant on two counts: it catapults Marshmallow to a “unicorn” valuation above $1 billion — specifically, $1.25 billion; and Marshmallow itself becomes one of a very small group of U.K. startups founded by Black people — Oliver and Alexander — to reach that figure.

(To be clear, Marshmallow describes itself as “the first UK unicorn to be founded by individuals that are Black or have Black heritage”, although I can think of at least one that preceded it: WorldRemit, which last month rebranded to Zepz, and is currently valued at $5 billion; co-founder and chairman Ismail Ahmed has been described as the most influential Black Briton.)

Regardless of whether Marshmallow is the first or one of the first, given the dearth of diversity in the U.K. technology industry, in particular in the upper ranks of it, it’s a notable detail worth pointing out, even as I hope that one day it will be less of a rarity.

Meanwhile, Marshmallow’s novel, big-data approach and successful traction in the market speak for themselves. When we covered the company’s most recent funding round before this — a $30 million raise in November 2020 — the startup was valued at $310 million. Now less than a year later, Marshmallow’s valuation has nearly quadrupled, and it has passed 100,000 policies sold in its home country, growing 100% over the last six months.

The plan now, Oliver told me in an interview, will be to deepen its relationships with customers, in part by providing more engagement to make them better drivers, but also potentially selling more services to them, too.

In this, the startup will be tapping into a new approach that other insurtech startups are taking as they rethink traditional insurance models, much like YuLife is positioning its life insurance products within a bigger wellness and personal improvement business. Currently, the average age of Marshmallow’s customers is 20 to 40, Oliver said — and there are thoughts of potentially new products aimed at even younger users. That means there is long-term value in improving loyalty and keeping those customers for many years to come.

Alongside that, Marshmallow will also use the funding to inch closer to its plan to expand to markets outside of the U.K. — a strategy that has been in the works for a while. Marshmallow talked up international expansion in its last round but has yet to announce which markets it will seek to tackle first.

Insurance — and in particular insurance startups — are often thought of together with fintech startups, not least because the two industries have a lot in common: they both operate in areas of assessing and mitigating risk and fraud; they are in many cases discretionary investments on the part of the customers; and they are both highly regulated and require watertight data protection for their users.

Perhaps because so much of the hard work is the same for both, it’s not uncommon to see services built to serve both sectors (FintechOS and Shift Technology being two examples), for fintech companies to dabble in insurance services, and so on.

But in reality, insurance — and specifically car insurance — has seen a massive impact from COVID-19 unique to that industry. Separate reports from EY and the Association of British Insurers noted that 2020 actually saw a lift for many car insurance companies: lockdowns meant that fewer people were driving, and therefore fewer were getting into accidents and making fewer claims.

2021, however, has been a different story: new pricing rules being put into place will likely see a number of providers tip into the red for the year. And the Chartered Insurance Institute points out that it will also be worth watching to see how the low use of cars in one year will impact use going forward: some car owners, especially in urban areas where keeping a car is expensive, will inevitably start to question whether they need to own and insure a car at all.

All of this, ironically, actually plays into the hand of a company like Marshmallow, which is providing a more flexible approach to customers who might otherwise be rejected by more traditional companies, or might be priced out of offerings from them. Interestingly, while neobanks have definitely spurred more traditional institutions to try to update their products to compete, the same hasn’t really happened in insurance — not yet, at least.

“We started with the idea of the power of data and using a wider range of resources [than incumbents], and using that in our pricing led us to be able to offer better rates to more people,” Oliver said, but that hasn’t led to Marshmallow seeing sharper competition from older incumbents. “They are big companies and stuck in their ways. These companies have been around for decades, some for centuries. Change is not happening quickly.”

That leaves a big opportunity for companies like Marshmallow and other newer players like Lemonade, Hippo and Jerry (not an insurance startup per se but also dabbling in the space), and a big opening for investors to back new ideas in an industry estimated to be worth $5 trillion.

“The traction the team has achieved demonstrates the demand for a new kind of insurance provider, one that focuses more on consumer experience and uses the latest technology and data to give fair prices,” said Eileen Burbidge, a partner at Passion Capital, in a statement. “We’ve been proud to support the team’s ambitions since the start, and now look forward to its next chapter in Europe as it continues its mission to change the industry for the better.”

Powered by WPeMatico

In the United States, a 401(k) plan is an employer-sponsored defined-contribution pension account. However, with legacy institutional investing, most of these have at least some level of fossil fuel involvement, and, let’s face it, very few of us really know. Now a startup plans to change that.

California-based startup Sphere wants to get employees to ask their employers for investment options that are not invested in fossil fuels. To do that it’s offering financial products that make it easier — it says — for employers to offer fossil-free investment options in their 401(k) plans. This could be quite a big movement. Sphere says there are more than $35 trillion in assets in retirement savings in the U.S. as of Q1 2021.

It’s now raised a $2 million funding round led by climate tech-focused VC Pale Blue Dot. Also participating were climate-focused investors including Sundeep Ahuja of Climate Capital. Sphere is also a registered “Public Benefit Corporation,” allowing it to campaign in public about climate change.

Alex Wright-Gladstein, CEO and founder of Sphere said: “We are proud to be partnering with Pale Blue Dot on our mission to reverse climate change by making our money talk. Heidi, Hampus, and Joel have the experience and drive to help us make big changes on the short seven-year time scale that we have to limit warming to 1.5°C.” Wright-Gladstein has also teamed up with sustainable investing veteran Jason Britton of Reflection Asset Management and BITA custom indexes.

Wright-Gladstein said she learned the difficulty of offering fossil-free options in 401(k) plans when running her previous startup, Ayar Labs. She tried to offer a fossil-free option for employees, but found out it took would take three years to get a single fossil-free option in the plan.

Heidi Lindvall, general partner at Pale Blue Dot, said: “We are big believers in Sphere’s unique approach of raising awareness through a social movement while offering a range of low-cost products that address the structural issues in fossil-free 401(k) investing.”

Powered by WPeMatico

There has been significant hype around Latin America’s startup success. For good reason, too: Startups have raised $9.3 billion in just the first half of 2021, almost double the amount in all of 2020, and mega-rounds are a growing trend.

But while the industry hails the rise of the region’s ecosystem and its growing fleet of unicorns, Latin America’s startup story has a far longer past. And it’s one we should keep in mind as entrepreneurs and investors around the world forge the region’s future.

People often ask me: How are consumers different in Brazil? How does the Peruvian market behave compared to the United States? These questions don’t really see each country for its inherent value, but instead gear people up to expect the unexpected from a historically economically disadvantaged region.

In fact, the evolution of business shares far more similarities across countries than we might expect. Latin America’s market has evolved over a very long time — as long as Silicon Valley and any other hub. This region has a global outlook, spectacular universities, a diverse population and an army of entrepreneurs.

It’s important for investors outside of Latin America to get involved in fundraising at earlier stages, when founders need extra support from everyone around.

That’s why the unicorns and megadeals should come as no surprise: They’re the natural evolution of the ecosystem, of more capital generating more success after years of hard work.

As Latin America has grown, competition has grown even more intense in the United States. VCs have more money than ever, and it’s getting increasingly expensive to invest in North America. So they’re looking to diversify their investments with high-potential opportunities abroad. Big funds are now dedicating resources to exclusively targeting Latin America, from SoftBank creating a region-specific fund, to Sequoia saying it will pay more attention to the region.

These incoming investors must bring more than money to ensure that entrepreneurship continues to grow in a healthy manner, rather than set it off balance. Investors should bring a local strategy that makes them an asset to Latin America’s startup ecosystem.

Most Latin American companies reaching unicorn status and going public now were started around 2012. This is not very different from the timeline of businesses in other markets such as the United States. For instance, e-commerce giant MercadoLibre launched in Argentina around the time eBay was emerging.

What this tells us is that foreign investors would do well to keep a sharp eye on emerging opportunities beyond heavily covered markets like Brazil and Mexico. There is a huge opportunity to do what local investors did in Brazil and Mexico years ago, and play a significant role in the next chapter of countries with blossoming markets like Colombia, Peru or Uruguay.

The amount of VC capital being funneled into Latin American startups has surged since 2017, with angel investment close behind. However, much of this investment comes from local and regional investors. Every top university in Brazil has a pool of angels. Investors in the Andean region cover Peru, Chile and Colombia. If today’s ecosystem is flourishing, it’s largely because native investors are lighting the spark.

Meanwhile, U.S. investor presence at the early stages is still low and risk averse. It’s much harder for a pre-seed or seed startup to get foreign investor interest than when they’ve already reached Series A or B. Investors also tend to come in on an ad hoc basis or as outliers brought about by a mutual contact. Foreign investors are the exception, not the rule.

It’s important for investors outside of Latin America to get involved in fundraising at earlier stages, when founders need extra support from everyone around. Investors should be pursuing a long-term strategy that will bring more consistency to the local ecosystem as a whole.

Your contribution as an investor is largely about the resources you can offer. That’s especially challenging for a foreigner who has less of an understanding of the local industry and lacks a network and people on the ground.

While investors may say their your regular value offering is enough — network and U.S. customers — in truth, this won’t necessarily be of much use. Your hiring network might not be ideal for a Latin American company, and your thorough understanding of the U.S. market might not reflect developments in Latin America.

Remember that the region has a plethora of VC organizations who have worked with local startups over the course of a decade. Latin America is a very welcoming and open market, and local investors and accelerators will happily work with foreign investors, including in deal-sharing opportunities.

It’s crucial to create incentives within the ecosystem, which — like in the United States — largely means matching founders with unique opportunities. In North America, this often happens organically, because people are on the ground and actively engaged with what’s happening in the region, from networking events, to awards, and grants and partnership opportunities.

To create this in Latin America, foreign investors need to dedicate a team and money to their regional commitments. They will have to understand the local industry and be available to mentor founders with diverse perspectives.

In my experience helping EA, Pinterest and Facebook land in Latin America, we always had someone on the ground or working remotely but fully dedicated to the region. We had people focused on localizing the product, and we had research teams studying similarities and differences in user behavior. That’s how corporations land their products; it’s how VCs should land their money.

The idea is for foreign investors to strike a balance locally while creating disruptions when it helps startups look outward rather than attempting to overhaul steady, positive internal growth. That can mean encouraging companies to incorporate in the United States to make it easier for investors from anywhere to invest or preparing the company to go global. Local investors can help investors new to the region understand the balance of things that should or shouldn’t be disrupted.

Don’t be surprised when Latin America’s apparent “boom” starts happening in other emerging markets like Africa and Asia. This isn’t about a secret hack coming in from the outside. It’s just about creating the right environment for local talent to flourish and ensuring it maintains healthy growth.

Powered by WPeMatico

Inflation may or may not prove transitory when it comes to consumer prices, but startup valuations are definitely rising — and noticeably so — in recent quarters.

That’s the obvious takeaway from a recent PitchBook report digging into valuation data from a host of startup funding events in the United States. While the data covers the U.S. startup market, the general trends included are likely global, given that the same venture rush that has pushed record capital into startups in the U.S. is also occurring in markets like India, Latin America, Europe and Africa.

The rapidly appreciating startup price chart is interesting, and we’ll unpack it. But the data also implies a high bar for future IPOs to not only preserve startup equity valuations at their point of exit, but exceed their private-market prices. A changing regulatory environment regarding antitrust could limit large future deals, leaving a host of startups with rich price tags and only one real path to liquidity.

Investors appear to be implicitly betting that the future IPO market will accelerate for a multiyear period at attractive prices.

That situation should be familiar: It’s the unicorn traffic jam that we’ve covered for years, in which the global startup markets create far more startups worth $1 billion and up than the public markets have historically accepted across the transom.

Let’s talk about some big numbers.

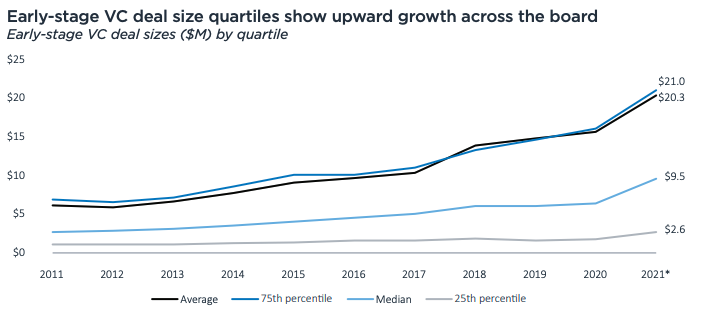

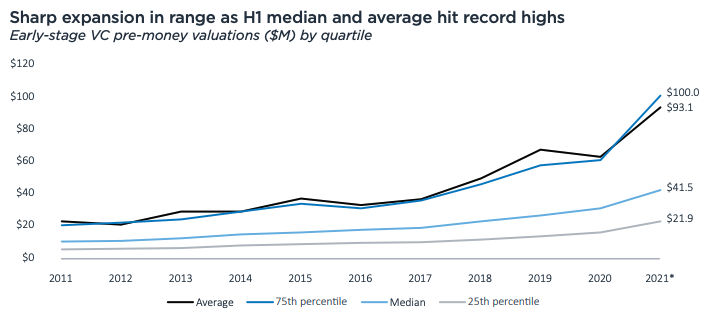

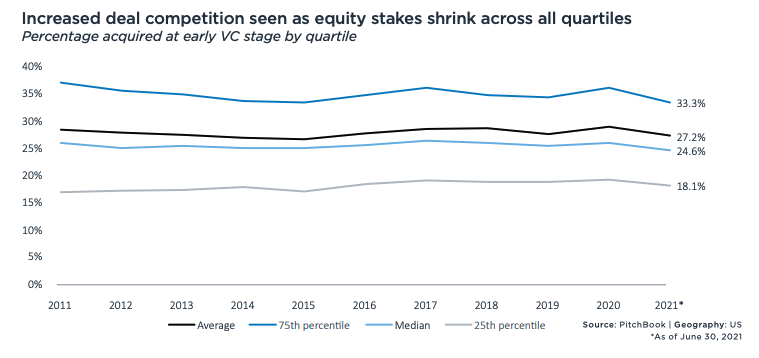

To summarize what PitchBook published: Round sizes are going up as valuations go up, and with the latter rising faster than the former, we’re not seeing investors get more ownership despite them having to spend more for deal access.

In the early-stage market, deal sizes are rising as follows:

Image Credits: PitchBook

Prices are going up as well, as the following chart shows:

Image Credits: PitchBook

Which leads to the following decline in equity take rates:

Image Credits: PitchBook

Those charts belie somewhat how quickly venture capital is changing. For example, in 2020, the median early-stage value created between rounds was $16 million (or a 54% relative velocity, if you prefer). In 2021 thus far, it’s $39.4 million (120% relative velocity). And that 2020 figure was a prior record. It just got smashed.

The PitchBook dataset has other superlatives worth noting. Enterprise-focused seed pre-money valuations hit an average of $11 million in the first half of 2021, an all-time high. Early-stage valuations for enterprise-focused startups also hit fresh records — $92.7 million on average, $43 million median — this year after rising consistently since 2011.

And late-stage valuations for enterprise tech startups have gone vertical (chart on the right):

Powered by WPeMatico

{kind=link}