Auto Added by WPeMatico

On balance, the cloud has been a huge boon to startups

Today’s startups have a distinct advantage when it comes to launching a company because of the public cloud. You don’t have to build infrastructure or worry about what happens when you scale too quickly. The cloud vendors take care of all that for you.

But last month when Pinterest announced its IPO, the company’s cloud spend raised eyebrows. You see, the company is spending $750 million a year on cloud services, more specifically for AWS. When your business is primarily focused on photos and video, and needs to scale at a regular basis, that bill is going to be high.

That price tag prompted Erica Joy, a Microsoft engineer, to publish this tweet and start a little internal debate here at TechCrunch. Startups, after all, have a dog in this fight, and it’s worth exploring if the cloud is helping feed the startup ecosystem, or sending your bills soaring, as they have with Pinterest.

after discussion with some folks about this article and the generally ridiculous amount of money startups pay for aws, i am wondering if there is an effective, easy to use, open source tool that helps startups reduce aws spend. https://t.co/GBh40b4UOH

— EricaJoy (@EricaJoy) March 25, 2019

For starters, it’s worth pointing out that Ms. Joy works for Microsoft, which just happens to be a primary competitor of Amazon’s in the cloud business. Regardless of her personal feelings on the matter, I’m sure Microsoft would be more than happy to take over that $750 million bill from Amazon. It’s a nice chunk of business; but all that aside, do startups benefit from having access to cloud vendors?

Powered by WPeMatico

Equity Shot: Lyft is public — what does that mean for other IPO-ready unicorns?

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

Sure, we just aired a new episode, but things keep happening, and after talking about this crop of IPOs for so long, we can’t help ourselves. (You can follow us on Twitter, here and here, by the way, if Equity isn’t enough for you.)

Lyft, as you know, started trading today, closing the loop on a long saga that brought the smaller of the two domestic ride-hailing unicorns to the public markets.

After so much speculation about which of the two would get out the door first, Lyft did, and now we get to see what sort of pricing shenanigans happen next. Does Uber drop rates and punish Lyft? Or does Uber work to cut its losses, lowering its expenses and providing a clearer path toward profitability before its April IPO roadshow kicks off? (Not a path to profitability, mind; Uber and Lyft need to show a path to the direction of profitability first.)

We hit all the bases, going over the company’s pricing path, its varying share figures, final raise metrics and more. If you want the hard stuff, we’ve got a shot for you.

Now that the Lyft IPO has wrapped, we’ll be shifting our focus to Pinterest, Zoom and, of course, Uber. Stay tuned.

OK, now we’re done. Until next Friday. Unless something else happens.

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

Unicorns aren’t profitable, and Wall Street doesn’t care

In Silicon Valley, investors don’t expect their portfolio companies to be profitable. “Blitzscaling: The Lightning-Fast Path to Building Massively Valuable Companies,” a bible for founders, instead calls for heavy spending on growth to scale in an Amazon -like fashion.

As for Wall Street, it’s shown an affinity for stock in Jeff Bezos’ business, despite the many years it spent navigating a path to profitability, as well as other money-losing endeavors. Why? Because it too is far less concerned with profitability than market opportunity.

Lyft, a ride-hailing company expected to go public this week, is not profitable. It posted losses of $911 million in 2018, a statistic that will make it the biggest loser amongst U.S. startups to have gone public, according to data collected by The Wall Street Journal. On the other hand, Lyft’s $2.2 billion in 2018 revenue places it atop the list of largest annual revenues for a pre-IPO business, trailing behind only Facebook and Google in that category.

Wall Street, in short, is betting on Lyft’s revenue growth, assuming it will narrow its loses and reach profitability… eventually.

Wall Street’s hungry for unicorns

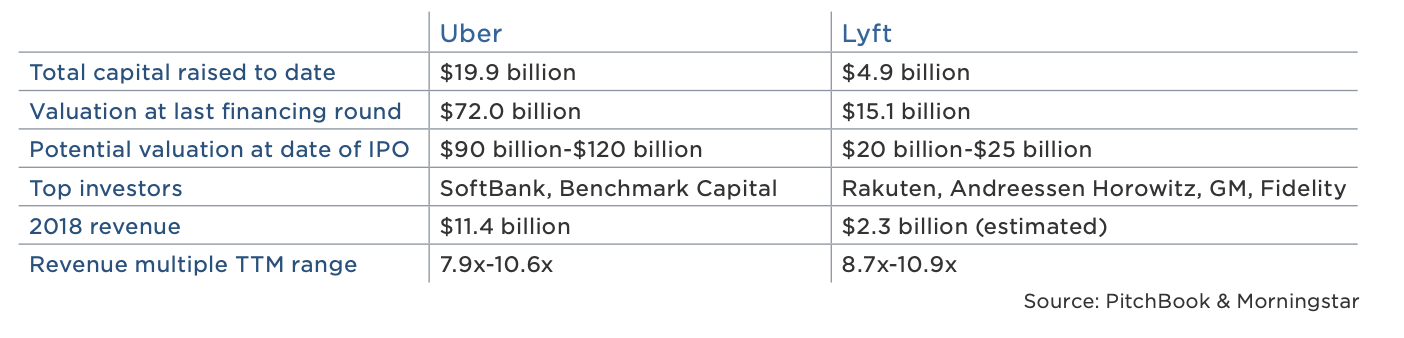

Lyft, losses notwithstanding, is growing rapidly and Wall Street is paying attention. On the second day of its road show, reports emerged that its IPO was already oversubscribed. As a result, Lyft is said to have upped the cost of its stock, with new plans to raise more than $2 billion at a valuation upwards of $25 billion. That represents a revenue multiple of more than 11x, a step up multiple of more than 1.6x from its most recent private valuation of $15.1 billion and, of course, Wall Street’s insatiable desire for unicorns, profitable or not.

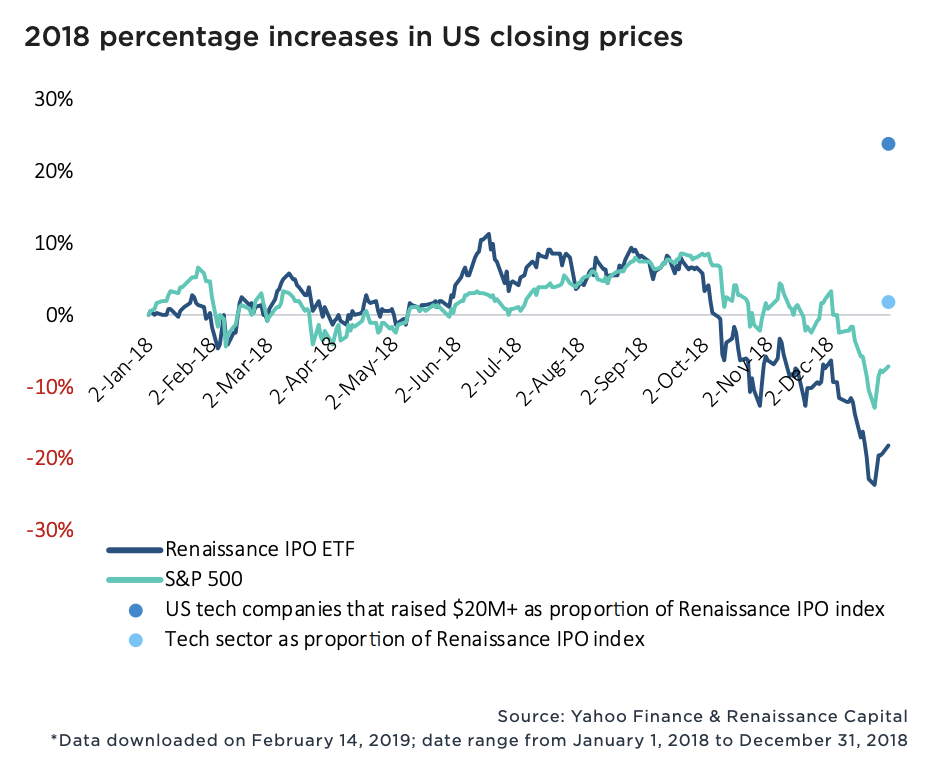

New data from PitchBook exploring the performance of billion-dollar-plus VC exits confirms Wall Street’s leniency toward unprofitable tech companies. Sixty-four percent of the 100+ companies valued at more than $1 billion to complete a VC-backed IPO since 2010 were unprofitable, and in 2018, money-losing startups actually fared better on the stock exchange than money-earning businesses. Moreover, U.S. tech companies that had raised more than $20 million traded up nearly 25 percent of 2018, while the S&P 500 technology sector posted flat returns.

Wall Street is still adapting to the rapid growth of the tech industry; public markets investors, therefore, are willing to deal with negative to minimal cash flows for, well, a very long time.

A tolerance for outsized exits

There’s no doubt Lyft and its much larger competitor, Uber, will go public at monstrous valuations. The two IPOs, set to create a whole bunch of millionaires and return a number of venture capital funds, will provide Silicon Valley a lesson in Wall Street’s tolerance for outsized exits.

Much like a seed-stage investor must bet on a founder’s vision, Wall Street, given a choice of several unprofitable businesses, has to bet on potential market value. Fortunately, this strategy can work quite well. Take Floodgate, for example. The seed fund invested a small amount of capital in Lyft when it was still a quirky idea for ridesharing called Zimride. Now, it boasts shares worth more than $100 million. I’m sure early shareholders in Amazon — which went public as a money-losing company in 1997 — are pretty happy, too.

Ultimately, Wall Street’s appetite for unicorns like Lyft is a result of the shortage of VC-backed IPOs. In 2006, it was the norm for a company to make its stock market debut at 7.9 years old, per PitchBook. In 2018, companies waited until the ripe age of 10.9 years, causing a significant slowdown in big liquidity events and stock sales.

Fund sizes, however, have grown larger and the proliferation of unicorns continues at unforeseen rates. That may mean, eventually, an influx of publicly shared unicorn stock. If that’s the case, might Wall Street start asking more of these startups? At the very least, public market investors, please don’t be swayed by WeWork‘s eventual stock offering and its “community adjusted EBITDA.” Silicon Valley’s pixie dust can’t be that potent.

Powered by WPeMatico

Startups Weekly: A much-needed unicorn IPO update

As I’m sure everyone reading this knows, female-founded businesses receive just over 2 percent of venture capital on an annual basis. Most of those checks are written to early-stage startups. It’s extremely difficult for female founders to garner late-stage support, let alone cash $100 million checks.

Maybe that’s finally changing. This week, not one but two female-founded and led companies, Glossier and Rent The Runway, raised nine-figure rounds and cemented their status as unicorn companies. According to PitchBook data from 2018, there are only about 15 unicorn startups with female founders. Though I’m sure that number has increased in the last year, you get the point: There are hundreds of privately held billion-dollar companies and shockingly few of those have women founders (even fewer have female CEOs)…

Moving on…

I spent a good part of the week at San Francisco’s Pier 48 in a room full of vest-wearing investors. We listened to some 200 YC companies make their 120-second pitch and though it was a bit of a whirlwind, there were definitely some standouts. ICYMI: We wrote about each and every company that pitched on day 1 and day 2. If you’re looking for the inside scoop on the companies that forwent demo day and raised rounds, or were acquired, before hitting the stage, we’ve got that too.

Lyft: This week, Lyft set the terms for its highly-anticipated initial public offering, expected to be completed next week. The company will charge between $62 and $68 per share, raising more than $2 billion at a valuation of ~$23 billion. We previously reported its initial market cap would be around $18.5 billion, but that was before we knew that Lyft’s IPO was already oversubscribed. Here’s a little more background on the Lyft IPO for those interested.

Uber: The global ride-hailing business flew a little more under the radar this week than last week, but still managed to grab a few headlines. The company has decided to sell its stock on the New York Stock Exchange, which is the least surprising IPO development of 2019, considering its key U.S. competitor, Lyft, has been working with the Nasdaq on its IPO. Uber is expected to unveil its S-1 in April.

Ben Silbermann, co-founder and CEO of Pinterest, at TechCrunch Disrupt SF 2017.

Pinterest: Pinterest, the nearly decade-old visual search engine, unveiled its S-1 on Friday, one of the final steps ahead of its NYSE IPO, expected in April. The $12.3 billion company, which will trade under the ticker symbol “PINS,” posted revenue of $755.9 million in the year ending December 31, 2018, up from $472.8 million in 2017. It has roughly doubled its monthly active user count since early 2016, hitting 265 million last year. The company’s net loss, meanwhile, shrank to $62.9 million in 2018 from $130 million in 2017.

Zoom: Not necessarily the buzziest of companies, but its S-1 filing, published Friday, stands out for one important reason: Zoom is profitable! I know, what insanity! Anyway, the startup is going public on the Nasdaq as soon as next month after raising about $150 million in venture capital funding. The full deets are here.

General Catalyst, a well-known venture capital firm, is diving more seriously into the business of funding seed-stage business. The firm, which has investments in Warby Parker, Oscar and Stripe, announced earlier this week its plan to invest at least $25 million each year in nascent teams.

Earlier this week, Opendoor, the SoftBank -backed real estate startup, filed paperwork to raise even more money. According to TechCrunch’s Ingrid Lunden, the business is planning to raise up to $200 million at a valuation of roughly $3.7 billion. It’s possible this is a Series E extension; after all, the company raised its $400 million Series E only six months ago. Backers of OpenDoor include the usual suspects: Andreessen Horowitz, Coatue, General Atlantic, GV, Initialized Capital, Khosla Ventures, NEA and Norwest Venture Partners.

Startup capital

- UiPath is raising $400M at a more than $7B valuation

- Ola raises $300M as part of a new EV deal with Hyundai and Kia

- Music startup Splice raises $57.5M to sell samples

- Iterable lands $50M to expand its cross-channel marketing platform

- Guesty, meant for property managers on Airbnb, raises $35M

- Travis Kalanick invests in Kargo, the ‘Uber for Trucks’

- Catch emerges from Y Combinator with $5.1M

Backstage Capital founder and managing partner Arlan Hamilton, center.

Axios’ Dan Primack and Kia Kokalitcheva published a report this week revealing Backstage Capital hadn’t raised its debut fund in total. Backstage founder Arlan Hamilton was quick to point out that she had been honest about the challenges of fundraising during various speaking engagements, and even on the Gimlet “Startup” podcast, which featured her in its latest season. A Twitter debate ensued and later, Hamilton announced she was stepping down as CEO of Backstage Studio, the operations arm of the venture fund, to focus on raising capital and amplifying founders. TechCrunch’s Megan Rose Dickey has the full story.

This week, TechCrunch’s Connie Loizos revisited a long-held debate: Pro rata rights, or the right of an earlier investor in a company to maintain the percentage that he or she (or their venture firm) owns as that company matures and takes on more funding. Here’s why pro rata rights matter (at least, to VCs).

If you enjoy this newsletter, be sure to check out TechCrunch’s venture-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I chat about Glossier, Rent The Runway and YC Demo Days. Then, in a special Equity Shot, we unpack the numbers behind the Pinterest and Zoom IPO filings.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

Equity Shot: Pinterest and Zoom file to go public

Hello and welcome back to Equity, TechCrunch’s venture capital-focused podcast, where we unpack the numbers behind the headlines.

What a Friday. This afternoon (mere hours after we released our regularly scheduled episode no less!), both Pinterest and Zoom dropped their public S-1 filings. So we rolled up our proverbial sleeves and ran through the numbers. If you want to follow along, the Pinterest S-1 is here, and the Zoom document is here.

Got it? Great. Pinterest’s long-awaited IPO filing paints a picture of a company cutting its losses while expanding its revenue. That’s the correct direction for both its top and bottom lines.

As Kate points out, it’s not in the same league as Lyft when it comes to scale, but it’s still quite large.

More than big enough to go public, whether it’s big enough to meet, let alone surpass its final private valuation ($12.3 billion) isn’t clear yet. Peeking through the numbers, Pinterest has been improving margins and accelerating growth, a surprisingly winsome brace of metrics for the decacorn.

Pinterest has raised a boatload of venture capital, about $1.5 billion since it was founded in 2010. Its IPO filing lists both early and late-stage investors, like Bessemer Venture Partners, FirstMark Capital, Andreessen Horowitz, Fidelity and Valiant Capital Partners as key stakeholders. Interestingly, it doesn’t state the percent ownership of each of these entities, which isn’t something we’ve ever seen before.

Next, Zoom’s S-1 filing was more dark horse entrance than Katy Perry album drop, but the firm has a history of rapid growth (over 100 percent, yearly) and more recently, profit. Yes, the enterprise-facing video conferencing unicorn actually makes money!

In 2019, the year in which the market is bated on Uber’s debut, profit almost feels out of place. We know Zoom’s CEO Eric Yuan, which helps. As Kate explains, this isn’t his first time as a founder. Nor is it his first major success. Yuan sold his last company, WebEx, for $3.2 billion to Cisco years ago then vowed never to sell Zoom (he wasn’t thrilled with how that WebEx acquisition turned out).

Should we have been that surprised to see a VC-backed tech company post a profit — no. But that tells you a little something about this bubble we live in, doesn’t it?

Equity drops every Friday at 6:00 am PT, so subscribe to us on Apple Podcasts, Overcast, Pocket Casts, Downcast and all the casts.

Powered by WPeMatico

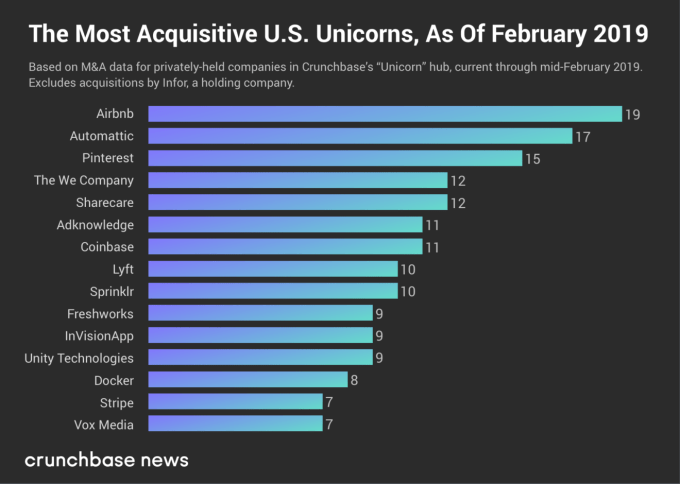

Airbnb, Automattic and Pinterest top rank of most acquisitive unicorns

Jason Rowley

Contributor

Contributor

Jason Rowley is a venture capital and technology reporter for Crunchbase News.

More posts by this contributor

It takes a lot more than a good idea and the right timing to build a billion-dollar company. Talent, focus, operational effectiveness and a healthy dose of luck are all components of a successful tech startup. Many of the most successful (or, at least, highest-valued) tech unicorns today didn’t get there alone.

Mergers and acquisitions (M&A) can be a major growth vector for rapidly scaling, highly valued technology companies. It’s a topic that we’ve covered off and on since the very first post on Crunchbase News in March 2017. Nearly two years later, we wanted to revisit that first post because things move quickly, and there is a new crop of companies in the unicorn spotlight these days. Which ones are the most active in the M&A market these days?

The most acquisitive U.S. unicorns today

Before displaying the U.S. unicorns with the most acquisitions to date, we first have to answer the question, “What is a unicorn?” The term is generally applied to venture-backed technology companies that have earned a valuation of $1 billion or more. Crunchbase tracks these companies in its Unicorns hub. The original definition of the term, first applied in a VC setting by Aileen Lee of Cowboy Ventures back in late 2011, specifies that unicorns were founded in or after 2003, following the first tech bubble. That’s the working definition we’ll be using here.

In the chart below, we display the number of known acquisitions made by U.S.-based unicorns that haven’t gone public or gotten acquired (yet). Keep in mind this is based on a snapshot of Crunchbase data, so the numbers and ranking may have changed by the time you read this. To maintain legibility and a reasonable size, we cut off the chart at companies that made seven or more acquisitions.

As one would expect, these rankings are somewhat different from the one we did two years ago. Several companies counted back in early March 2017 have since graduated to public markets or have been acquired.

Who’s gone?

Dropbox, which had acquired 23 companies at the time of our last analysis, went public weeks later and has since acquired two more companies (HelloSign for $230 million in late January 2019 and Verst for an undisclosed sum in November 2017) since doing so. SurveyMonkey, which went public in September 2018, made six known acquisitions before making its exit via IPO.

Who stayed?

Which companies are still in the top ranks? Travel accommodations marketplace giant Airbnb jumped from number four to claim Dropbox’s vacancy as the most acquisitive private U.S. unicorn in the market. Airbnb made six more acquisitions since March 2017, most recently Danish event space and meeting venue marketplace Gaest.com. The still-pending deal was announced in January 2019.

WordPress developer and hosting company Automattic is still ranked number two. Automattic href=”https://www.crunchbase.com/acquisition/automattic-acquires-atavist–912abccd”>acquired one more company — digital publication platform Atavist — since we last profiled unicorn M&A. Open-source software containerization company Docker, photo-sharing and search site Pinterest, enterprise social media management company Sprinklr and venture-backed media company Vox Media remain, as well.

Who’s new?

There are some notable newcomers in these rankings. We’ll focus on the most notable three: The We Company, Coinbase and Lyft. (Honorable mention goes to Stripe and Unity Technologies, which are also new to this list.)

The We Company (the holding entity for WeWork) has made 10 acquisitions over the past two years. Earlier this month, The We Company bought Euclid, a company that analyzes physical space utilization and tracks visitors using Wi-Fi fingerprinting. Other buyouts include Meetup (a story broken by Crunchbase News in November 2017) reportedly for $200 million. Also in late 2017, The We Company acquired coding and design training program Flatiron School, giving the company a permanent tenant in some of its commercial spaces.

In its bid to solidify its position as the dominant consumer cryptocurrency player, Coinbase has been on quite the M&A tear lately. The company recently announced its plans to acquire Neutrino, a blockchain analytics and intelligence platform company based in Italy. As we covered, Coinbase likely made the deal to improve its compliance efforts. In January, Coinbase acquired data analysis company Blockspring, also for an undisclosed sum. The crypto company’s other most notable deal to date was its April 2018 buyout of the bitcoin mining hardware turned cryptocurrency micro-transaction platform Earn.com, which Coinbase acquired for $120 million.

And finally, there’s Lyft, the more exclusively U.S.-focused ride-hailing and transportation service company. Lyft has made 10 known acquisitions since it was founded in 2012. Its latest M&A deal was urban bike service Motivate, which Lyft acquired in June 2018. Lyft’s principal rival, Uber, has acquired six companies at the time of writing. Uber bought a bike company of its own, JUMP Bikes, at a price of $200 million, a couple of months prior to Lyft’s Motivate purchase. Here too, the Lyft-Uber rivalry manifests in structural sameness. Fierce competition drove Uber and Lyft to raise money in lock-step with one another, and drove M&A strategy as well.

What to take away

With long-term business success, it’s often a chicken-and-egg question. Is a company successful because of the startups it bought along the way? Or did it buy companies because it was successful and had an opening to expand? Oftentimes, it’s a little of both.

The unicorn companies that dominate the private funding landscape today (if not in the number of deals, then in dollar volume for sure) continue to raise money in the name of growth. Growth can come the old-fashioned way, by establishing a market position and expanding it. Or, in the name of rapid scaling and ostensibly maximizing investor returns, M&A provides a lateral route into new markets or a way to further entrench the status quo. We’ll see how that strategy pays off when these companies eventually find the exit door .

Powered by WPeMatico

Startups Weekly: Flexport, Clutter and SoftBank’s blood money

The Wall Street Journal published a thought-provoking story this week, highlighting limited partners’ concerns with the SoftBank Vision Fund’s investment strategy. The fund’s “decision-making process is chaotic,” it’s over-paying for equity in top tech startups and it’s encouraging inflated valuations, sources told the WSJ.

The report emerged during a particularly busy time for the Vision Fund, which this week led two notable VC deals in Clutter and Flexport, as well as participated in DoorDash’s $400 million round; more on all those below. So given all this SoftBank news, let us remind you that given its $45 billion commitment, Saudi Arabia’s Public Investment Fund (PIF) is the Vision Fund’s largest investor. Saudi Arabia is responsible for the planned killing of dissident journalist Jamal Khashoggi.

Here’s what I’m wondering this week: Do CEOs of companies like Flexport and Clutter have a responsibility to address the source of their capital? Should they be more transparent to their customers about whose money they are spending to achieve rapid scale? Send me your thoughts. And thanks to those who wrote me last week re: At what point is a Y Combinator cohort too big? The general consensus was this: the size of the cohort is irrelevant, all that matters is the quality. We’ll have more to say on quality soon enough, as YC demo days begin on March 18.

Anyways…

Surprise! Sort of. Not really. Pinterest has joined a growing list of tech unicorns planning to go public in 2019. The visual search engine filed confidentially to go public on Thursday. Reports indicate the business will float at a $12 billion valuation by June. Pinterest’s key backers — which will make lots of money when it goes public — include Bessemer Venture Partners, Andreessen Horowitz, FirstMark Capital, Fidelity and SV Angel.

Ride-hailing company Lyft plans to go public on the Nasdaq in March, likely beating rival Uber to the milestone. Lyft’s S-1 will be made public as soon as next week; its roadshow will begin the week of March 18. The nuts and bolts: JPMorgan Chase has been hired to lead the offering; Lyft was last valued at more than $15 billion, while competitor Uber is valued north of $100 billion.

Despite scrutiny for subsidizing its drivers’ wages with customer tips, venture capitalists plowed another $400 million into food delivery platform DoorDash at a whopping $7.1 billion valuation, up considerably from a previous valuation of $3.75 billion. The round, led by Temasek and Dragoneer Investment Group, with participation from previous investors SoftBank Vision Fund, DST Global, Coatue Management, GIC, Sequoia Capital and Y Combinator, will help DoorDash compete with Uber Eats. The company is currently seeing 325 percent growth, year-over-year.

Here are some more details on those big Vision Fund Deals: Clutter, an LA-based on-demand storage startup, closed a $200 million SoftBank-led round this week at a valuation between $400 million and $500 million, according to TechCrunch’s Ingrid Lunden’s reporting. Meanwhile, Flexport, a five-year-old, San Francisco-based full-service air and ocean freight forwarder, raised $1 billion in fresh funding led by the SoftBank Vision Fund at a $3.2 billion valuation. Earlier backers of the company, including Founders Fund, DST Global, Cherubic Ventures, Susa Ventures and SF Express all participated in the round.

Here’s your weekly reminder to send me tips, suggestions and more to kate.clark@techcrunch.com or @KateClarkTweets.

Menlo Ventures has a new $500 million late-stage fund. Dubbed its “inflection” fund, it will be investing between $20 million and $40 million in companies that are seeing at least $5 million in annual recurring revenue, growth of 100 percent year-over-year, early signs of retention and are operating in areas like cloud infrastructure, fintech, marketplaces, mobility and SaaS. Plus, Allianz X, the venture capital arm attached to German insurance giant Allianz, has increased the size of its fund to $1.1 billion and London’s Entrepreneur First brought in $115 million for what is one of the largest “pre-seed” funds ever raised.

Flipkart co-founder invests $92M in Ola

Redis Labs raises a $60M Series E round

Chinese startup Panda Selected nabs $50M from Tiger Global

Image recognition startup ViSenze raises $20M Series C

Circle raises $20M Series B to help even more parents limit screen time

Showfields announces $9M seed funding for a flexible approach to brick-and-mortar retail

Podcasting startup WaitWhat raises $4.3M

Zoba raises $3M to help mobility companies predict demand

Indian delivery men working with the food delivery apps Uber Eats and Swiggy wait to pick up an order outside a restaurant in Mumbai. ( INDRANIL MUKHERJEE/AFP/Getty Images)

According to Indian media reports, Uber is in the final stages of selling its Indian food delivery business to local player Swiggy, a food delivery service that recently raised $1 billion in venture capital funding. Uber Eats plans to sell its Indian food delivery unit in exchange for a 10 percent share of Swiggy’s business. Swiggy was most recently said to be valued at $3.3 billion following that billion-dollar round, which was led by Naspers and included new backers Tencent and Uber investor Coatue.

Lalamove, a Hong Kong-based on-demand logistics startup, is the latest venture-backed business to enter the unicorn club with the close of a $300 million Series D round this week. The latest round is split into two, with Hillhouse Capital leading the “D1” tranche and Sequoia China heading up the “D2” portion. New backers Eastern Bell Venture Capital and PV Capital and returning investors ShunWei Capital, Xiang He Capital and MindWorks Ventures also participated.

Longtime investor Keith Rabois is joining Founders Fund as a general partner. Here’s more from TechCrunch’s Connie Loizos: “The move is wholly unsurprising in ways, though the timing seems to suggest that another big fund from Founders Fund is around the corner, as the firm is also bringing aboard a new principal at the same time — Delian Asparouhov — and firms tend to bulk up as they’re meeting with investors. It’s also kind of time, as these things go. Founders Fund closed its last flagship fund with $1.3 billion in 2016.”

If you enjoy this newsletter, be sure to check out TechCrunch’s venture capital-focused podcast, Equity. In this week’s episode, available here, Crunchbase News editor-in-chief Alex Wilhelm and I discuss Pinterest’s IPO, DoorDash’s big round and SoftBank’s upset LPs.

Want more TechCrunch newsletters? Sign up here.

Powered by WPeMatico

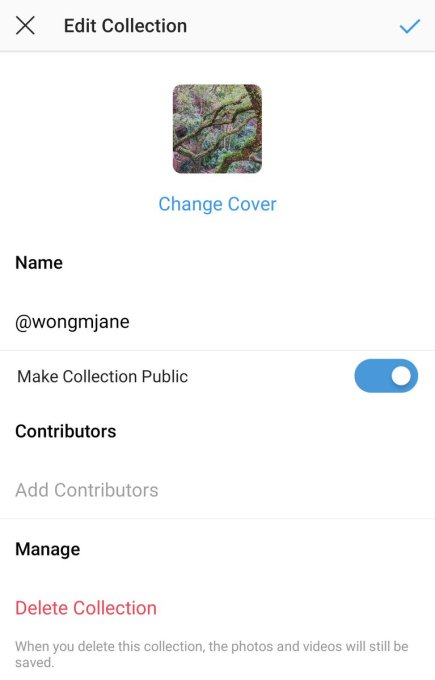

Pinstagram? Instagram code reveals Public Collections feature

Instagram is threatening to attack Pinterest just as it files to go public the same way the Facebook-owned app did to Snapchat. Code buried in Instagram for Android shows the company has prototyped an option to create public “Collections” to which multiple users can contribute. Instagram launched private Collections two years ago to let you Save and organize your favorite feed posts. But by allowing users to make Collections public, Instagram would become a direct competitor to Pinterest.

Instagram public Collections could spark a new medium of content curation. People could use the feature to bundle together their favorite memes, travel destinations, fashion items or art. That could cut down on unconsented content stealing that’s caused backlash against meme “curators” like F*ckJerry by giving an alternative to screenshotting and reposting other people’s stuff. Instead of just representing yourself with your own content, you could express your identity through the things you love — even if you didn’t photograph them yourself. And if that sounds familiar, you’ll understand why this could be problematic for Pinterest’s upcoming $12 billion IPO.

The “Make Collection Public” option was discovered by frequent TechCrunch tipster and reverse engineering specialist Jane Manchun Wong. It’s not available to the public, but from the Instagram for Android code, she was able to generate a screenshot of the prototype. It shows the ability to toggle on public visibility for a Collection, and tag contributors who can also add to the Collection. Previously, Collections was always a private, solo feature for organizing your bookmarks gathered through the Instagram Save feature Instagram launched in late 2016.

Instagram told TechCrunch “we’re not testing this,” which is its standard response to press inquiries about products that aren’t available to public users, but that are in internal development. It could be a while until Instagram does start experimenting publicly with the feature and longer before a launch, and the company could always scrap the option. But it’s a sensible way to give users more to do and share on Instagram, and the prototype gives insight into the app’s strategy. Facebook launched its own Pinterest -style shareable Sets in 2017 and launched sharable Collections in December.

Currently there’s nothing in the Instagram code about users being able to follow each other’s Collections, but that would seem like a logical and powerful next step. Instagrammers can already follow hashtags to see new posts with them routed to their feed. Offering a similar way to follow Collections could turn people into star curators rather than star creators without the need to rip off anyone’s content. Speaking of infuencers, Wong also spotted Instagram prototyping IGTV picture-in-picture, so you could keep watching a long-form video after closing the app and navigating the rest of your phone.

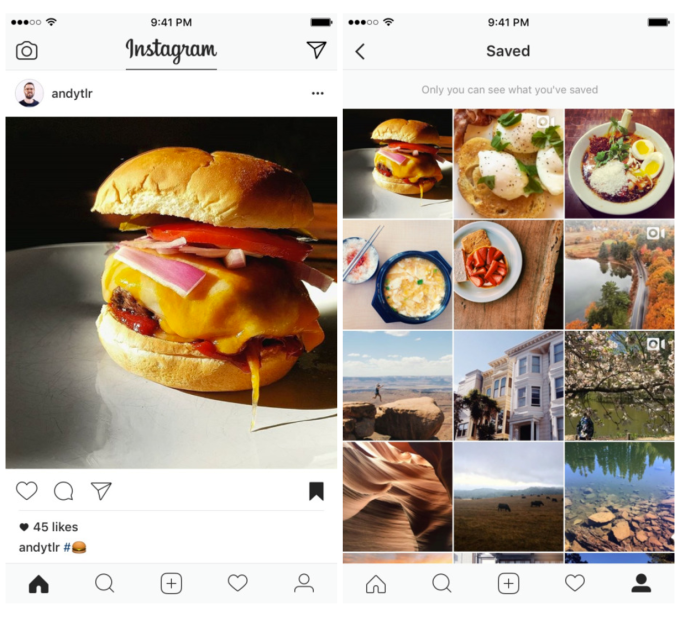

Instagram lets users Save posts, which can then be organized into Collections

Public Collections could fuel Instagram’s commerce strategy that Mark Zuckerberg recently said would be a big part of the road map. Instagram already has a personalized Shopping feed in Explore, and The Verge’s Casey Newton reported last year that Instagram was working on a dedicated shopping app. It’s easy to imagine fashionistas, magazines and brands sharing Collections of their favorite buyable items.

It’s worth remembering that Instagram launched its copycat of Snapchat Stories just six months before Snap went public. As we predicted, that reduced Snapchat’s growth rate by 88 percent. Two years later, Snapchat isn’t growing at all, and its share price is at just a third of its peak. With more than 1 billion monthly and 500 million daily users, Instagram is four times the size of Pinterest. Instagram loyalists might find it’s easier to use the “good enough” public Collections feature where they already have a social graph than try to build a following from scratch on Pinterest.

Powered by WPeMatico

Pinterest files confidentially to go public

Visual search engine Pinterest has joined a long list of high-flying technology companies planning to go public in 2019. The business has confidentially submitted paperwork to the Securities and Exchange Commission for an initial public offering slated for later this year, according to a report from The Wall Street Journal.

Pinterest declined to comment.

Founded in 2008 by Ben Silbermann, earlier reports indicated the company was planning to debut on the stock market in April. In late January, Pinterest took its first official step toward a 2019 IPO, hiring Goldman Sachs and JPMorgan Chase as lead underwriters for its offering.

The company garnered a $12.3 billion valuation in 2017 with a $150 million financing.

Touting 250 million monthly active users, Pinterest has raised nearly $1.5 billion in venture capital funding from key stakeholders Bessemer Venture Partners, Andreessen Horowitz, FirstMark Capital, Fidelity and SV Angel. The business brought in some $700 million in ad revenue in 2018, per reports, a 50 percent increase year-over-year.

Pinterest employs 1,600 people across 13 cities, including Chicago, London, Paris, São Paulo, Berlin and Tokyo. The company says half its users live outside the U.S.

Pinterest will likely follow Lyft, Uber and Slack to the public markets, which have all filed confidential paperwork for IPOs or, in Slack’s case, a reported direct listing, expected in the coming months.

Powered by WPeMatico