Paytm

Auto Added by WPeMatico

Auto Added by WPeMatico

The fintech sector has been hugely successful (and hugely profitable) for much of the last decade, and even more so during the pandemic. But it might come as a surprise to learn that many in the industry believe that the story is just beginning and the sector is poised to achieve much more, with fintech’s next decade expected to be radically different from the last 10 years.

Long before the pandemic, the way in which banks were regulated was changing. Initiatives like Open Banking and the Revised Payment Services Directive (PSD2) were being proposed as a way to promote competition in the banking industry — allowing smaller challenger firms to break into a market that has long been dominated by corporate titans.

Now that these initiatives are in place, however, we’re seeing that their effect goes way beyond opening up a gap for challenger banks. Since open banking requires that banks make valuable data available via APIs, it is leading to a revolution in the way that small and mid-size enterprises (SMEs) are funded — one in which data, and not hard capital, is the most important factor driving fintech success.

In order to understand the changes that are sweeping fintech and reconfiguring the way that the industry works with small businesses, it’s important to understand open banking. This is a concept that has really taken hold among governmental and supranational banking regulators over the past decade, and we are now beginning to see its impact across the banking sector.

Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

At its most fundamental level, open banking refers to the process of using APIs to open up consumers’ financial data to third parties. This allows these third parties to design, build and distribute their own financial products. The utility (and, ultimately, the profitability) of these products doesn’t rely on them holding huge amounts of capital — rather, it is the data they harvest and contain that endows them with value.

Open-banking models raise a number of challenges. One is that the banking industry will need to develop much more rigorous systems to continually seek consumer consent for data to be shared in this way. Though the early years of fintech have taught us that consumers are pretty relaxed when it comes to giving up their data — with some studies indicating that almost 60% of Americans choose fintech over privacy — the type and volume shared through open-banking frameworks is much more extensive than the products we have seen up until now.

Despite these concerns, the push toward open banking is progressing around the world. In Europe, the PSD2 (the Payment Services Directive) requires large banks to share financial information with third parties, and in Asia services like Alipay and WeChat in China, and Tez and PayTM in India are already altering the financial services market. The extra capabilities available through these services are already leading to calls for the U.S. banking system to embrace open banking to the same degree.

If the U.S. banking industry can be convinced of the utility of open banking, or if it is forced to do so via legislation, several groups are likely to benefit:

By far the biggest beneficiary of open banking, however, will be SMEs. This is not necessarily because open-banking frameworks offer specific new functionality that will be useful to small and medium-sized businesses. Instead, it is a reflection of the fact that SMEs have historically been so poorly served by traditional banks.

SMEs are underserved in a number of ways. Traditional banks have an extremely limited ability to view the aggregate financial position of an SME that holds capital across multiple institutions and in multiple instruments, which makes securing finance very difficult.

In addition, SMEs often have to deal with dated and time-consuming manual interfaces to upload data to their bank. And (perhaps worst of all) the B2B payment systems in use at most banks provide very limited feedback to the businesses that use them — a lack of information that can cost businesses dearly.

Given these deficiencies, it’s not surprising that fintech startups are keen to lend to small businesses, and that SMEs are actively looking for novel banking products and services. There have, of course, already been some success stories in this space, and the kinds of banking systems available to SMEs today (especially in Europe) are leagues ahead of the services available even 10 years ago.

However, open banking promises to accelerate this transformation and dramatically improve the financial services available to the average SME. It will do this in several ways. Allowing third parties access to the data held at banks will allow the true financial position of SMEs to be assessed, many for the first time.

Via APIs, fintech companies will be able to access information on different types of accounts, insurance, card accounts and leases, and consolidate data from multiple countries into one overall picture.

This, in turn, will have major effects on the way that credit-worthiness is assessed for SMEs. At the moment, there is a funding gap facing many SMEs, largely because banks have been hesitant to move away from the “balance sheet” model of assessing credit risk. By using real-time analytics on an SME’s current business activities, banks will be able to more accurately assess this risk and lend to more businesses.

In fact, this is already happening in countries where open banking is well advanced – in the U.K., Lloyds’ Business ToolBox offers unlimited credit checks on companies and directors in addition to account transaction data.

Open banking will also allow peer comparison analytics far ahead of what we have seen until now. APIs can be used to provide SMEs real-time feedback on how they are performing within their market sector. Again, this ability is already available in the U.K., with Barclays’ SmartBusiness Dashboard offering marketing effectiveness tools as part of a customizable business dashboard.

These capabilities will be so useful to SMEs that they are likely to drive the popularity of any fintech product that offers them. For SMEs, this value will lie mainly in intelligent data-analytics-based insights, recommendations and automatic prompts that can be built on top of account aggregation.

Then, additional insights generated from these same monitoring tools could enable banks and alternative lenders to be more proactive with their lending — offering preapproved lines of credit, in a timely manner, to SMEs that would have previously found it difficult to access funding.

Crucially for the fintech sector, it’s almost a certainty that SMEs will be willing to pay fees for data-analytics-based value-added services that help them grow. This is why some startups in this space are already attracting huge levels of funding, and why open banking is at the heart of the relationship between tech and the economy.

So if fintech has had a good year, this is likely to be just the start of the story. Backed by open-banking initiatives, the sector is now at the forefront of a banking revolution that will finally give SMEs the level of service they deserve and unleash their true potential across the economy at large.

Powered by WPeMatico

In case you’ve not been paying attention, we’ll say it again: The global venture capital industry is on fire. The second quarter of 2021 was the largest single three-month period on record for dollars invested.

The data coming in points to a worldwide boom. The United States’ startup market had a huge Q2, and investors don’t expect the pace to slow in the country. Europe is also having one hell of a year. Around the world, 2021 is shaping up to be a breakout year for venture investment into startups. And that’s after several years of growing, record-breaking results.

The Exchange explores startups, markets and money.

Read it every morning on Extra Crunch or get The Exchange newsletter every Saturday.

India is another good example of this trend. The country’s venture capital haul thus far in 2021 has nearly matched its 2020 total and is on pace for a record year. But as the third quarter gets underway, something perhaps even more important is going on: public-market liquidity.

The new trend is being spearheaded by Zomato, an Indian food delivery giant that could be valued at $8.6 billion in its public debut. Other major Indian unicorns are following it to the public markets, including fintech players like MobiKwik and Paytm, which is backed by Alibaba and its affiliate Ant Financial. The trio of companies could herald a rush of public offerings from Indian companies if their debuts prove lucrative and stable.

Today, The Exchange is taking a look at India’s recent venture capital results and digging more deeply into the country’s IPO pipeline, with help from VCs Kunal Bajaj of Blume Ventures and Manish Singhal of pi Ventures. We’ll also read the tea leaves when it comes to how Zomato’s IPO is performing thus far, and what we can learn from its early data. This will be fun!

Powered by WPeMatico

Paytm, India’s most valuable startup, confirmed to its shareholders and employees on Monday that it plans to file for an IPO.

In a letter to shareholders and employees, Paytm said that it plans to raise money by issuing fresh equity in the IPO, and also sell existing shareholders’ shares at the event. The startup has offered its employees the option to sell their stakes in the firm.

This is the first time the Noida-headquartered firm, which is valued at $16 billion and has raised over $3 billion to date, has commented on its plans about the IPO. The startup said in the letter that it has received an in-principle approval from the board of directors to pursue the public market.

Paytm, which is backed by Alibaba and SoftBank, hasn’t shared when it plans to file for the IPO, but has sought shareholders’ response to their intention to sell stakes by the end of the month.

Two sources familiar with the matter told TechCrunch that Paytm plans to raise about $3 billion and is targeting a valuation of up to $30 billion in the IPO. Paytm declined to comment.

Paytm’s letter — obtained by TechCrunch — to shareholders on Monday.

This isn’t the first time Paytm has planned to explore the public route. Exactly 10 years ago, long before Paytm established itself as the largest mobile wallet firm and expanded to several financial and commerce services, the startup had filed with the regulator with intentions to become public. The startup at the time cancelled the IPO plan and instead raised money from VCs to explore new avenues for growth.

A lot is riding on a successful IPO of Paytm — which reported a consolidated loss of $233.6 million for the financial year that ended in March this year, down from $404 million a year ago. (The startup’s revenue fell 10% during this period to $437.6 million.) India’s stock markets are yet to be fully tested for tech startups’ stocks in the country — though retail investors have shown good signs in recent years.

The startup, which competes with Google Pay and Flipkart-backed PhonePe, has realigned its payments strategy in recent years to assume a leadership position in the merchant payments market.

In a report to its clients late last month, analysts at Bernstein said the startup’s credit tech vertical is likely to lead the next wave of its revenue growth.

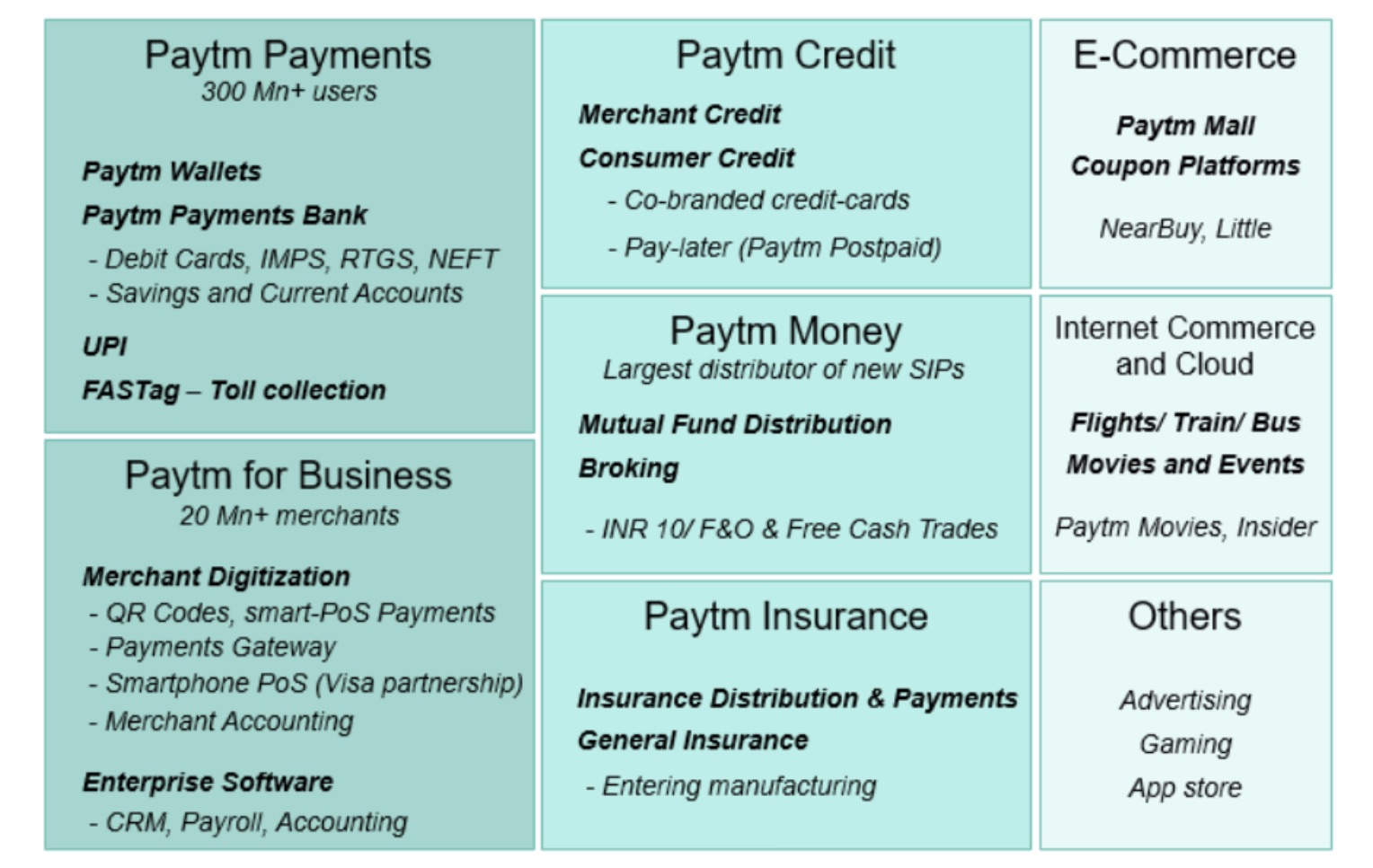

An overview of Paytm’s financial services ecosystem (Bernstein)

“With the advent of UPI, there has been a rising narrative that questioned Paytm’s market leadership,” the analysts wrote, referring to the exponential growth of payments stack developed by retail banks in India that has been adopted by several firms, including Google and PhonePe (as well as Paytm), and which has somewhat lowered the appeal of mobile wallets in India.

“However, under the hood, Paytm leads on merchant payments and has built an ecosystem of synergistic fintech verticals around its ‘super-app.’ The ecosystem spans payments (wallet/UPI), full-suite merchant acquiring, credit tech, digital bank, wealth, and insurance tech. We believe the super-app battle in India is not a ‘winner takes all’ but a game of execution, business building, and creating a superior customer experience with ecosystem integration,” Bernstein analysts added.

Paytm is the latest Indian giant startup that has expressed an interest in becoming public in recent months. Earlier this year, food delivery startup Zomato said it plans to raise $1.1 billion through an initial public offering. TechCrunch reported last month that Flipkart was in talks to raise over $1 billion in what is expected to be its financial fundraise ahead of an IPO.

Powered by WPeMatico

Policybazaar has raised $75 million as the Indian online insurance platform looks to expand its presence in UAE and Middle East.

Sarbvir Singh, chief executive of Policybazaar, told TechCrunch that the startup had raised $75 million, but didn’t elaborate. Falcon Edge Capital led the new tranche of investment in the Indian startup, which has raised about $630 million to date, according to research firm Tracxn.

The 12-year-old startup, which counts SoftBank Group’s Vision Fund and Tiger Global among its investors, is among a handful of startups that is attempting to upend India’s insurance market, which is largely commanded by state and bank-backed insurers.

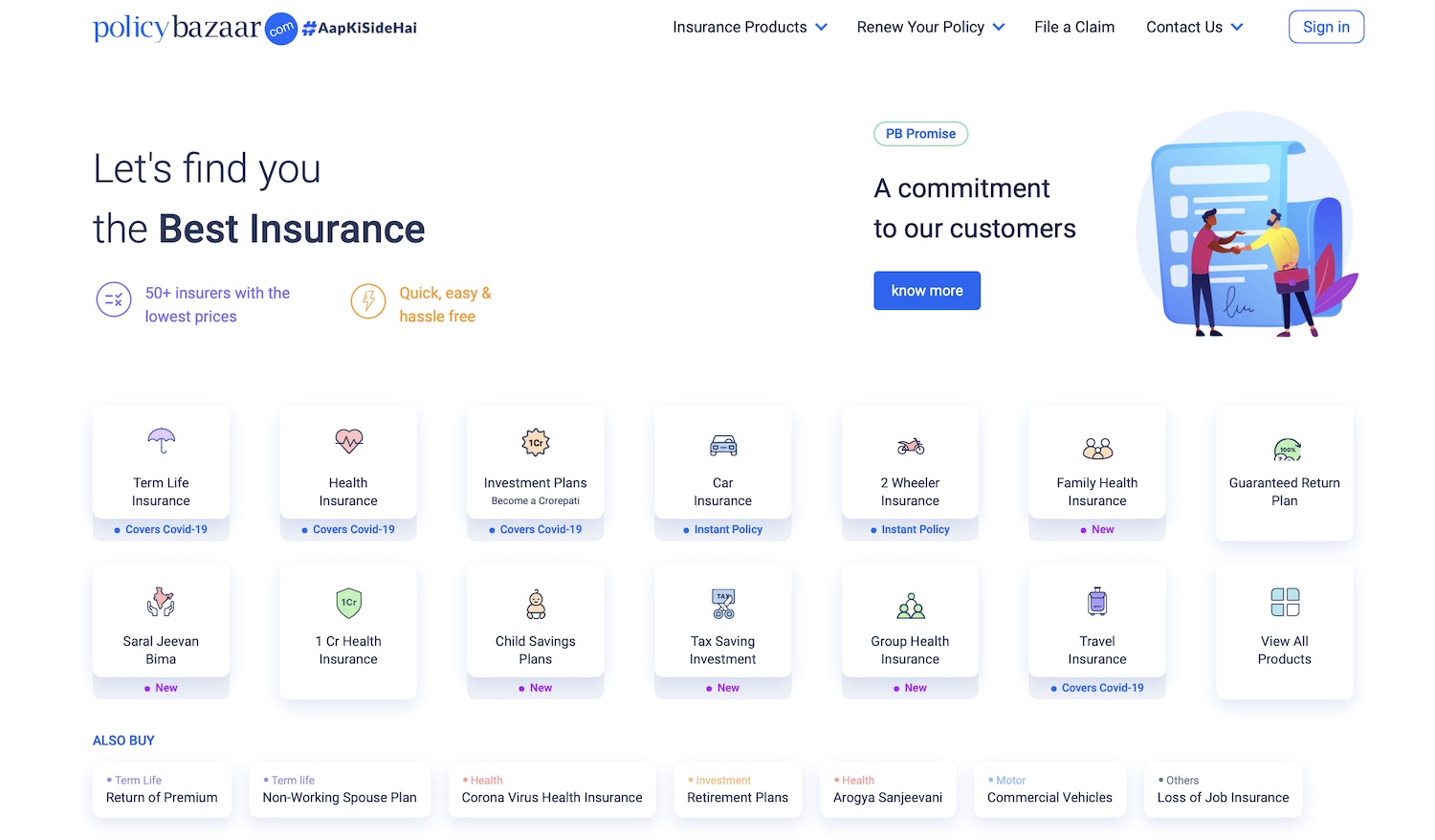

Policybazaar serves as an aggregator that allows users to compare and buy policies — across categories including life, health, travel, auto and property — from dozens of insurers on its website without having to go through conventional agents.

A screengrab of Policybazaar website

In India only a fraction of the nation’s 1.3 billion people currently have access to insurance and some analysts say that digital firms could prove crucial in bringing these services to the masses. According to rating agency ICRA, insurance products had reached less than 3% of the population as of 2017.

An average Indian makes about $2,100 in a year, according to World Bank. ICRA estimated that of those Indians who had purchased an insurance product, they were spending less than $50 on it in 2017.

In a recent report, analysts at Bernstein estimated that Policybazaar commands 90% of share in the online insurance distribution market. The platform also sells loans, credit cards and mutual funds. The startup says it sells over a million policies a month.

“India has an under-penetrated insurance market. Within the under-penetrated landscape, digital distribution through web-aggregators like Policybazaar forms <1% of the industry. This offers a large headroom for growth,” Bernstein analysts wrote to clients.

The startup, which is working on an initial public offering slated for next year, said it will use the fresh investment to expand its presence across the UAE and Middle East regions.

“PolicyBazaar has shown stellar innovation, execution, and relentlessness in establishing itself as the market leader in online insurance aggregation in India. We believe the playbook it has established over the last 10 years in being the most efficient sales channel for insurance manufacturers, can act as a catalyst to gain market leadership in the GCC,” said Navroz Udwadia, co-founder of Falcon Edge Capital, in a statement.

Early Stage is the premier “how-to” event for startup entrepreneurs and investors. You’ll hear firsthand how some of the most successful founders and VCs build their businesses, raise money and manage their portfolios. We’ll cover every aspect of company building: Fundraising, recruiting, sales, product-market fit, PR, marketing and brand building. Each session also has audience participation built-in — there’s ample time included for audience questions and discussion. Use code “TCARTICLE at checkout to get 20% off tickets right here.

Powered by WPeMatico

After spending more than a decade disrupting the neighborhood stores in the U.S. and several other markets, Amazon and Walmart are employing an unusual strategy in India to face off this competitor: Friending them.

Walmart and Amazon, both of which face restrictions from New Delhi on what all they could do in India, have partnered with tens of thousands of neighborhood stores in the world’s second-largest internet market this year to leverage the vast presence of these mom and pop stores.

In June this year, at the height of the pandemic, Amazon announced “Smart Stores.” Through this India-specific program, for instance, Amazon is providing physical stores with software to maintain a digital log of the inventory they have in the shop and supplying them with a QR code.

When consumers walk to the store and scan this QR code with the Amazon app, they see everything the shop has to offer, in addition to any discounts and past reviews from customers. They can select the items and pay for it using Amazon Pay. Amazon Pay in India supports a range of payments services, including the popular UPI, and debit and credit cards.

The world’s largest e-commerce giant also maintains partnerships that allow it to turn tens of thousands of neighborhood stores as its delivery point for customers — and sometimes even rely on them for inventory.

India has over 60 million small businesses that dot the thousands of cities, towns and villages across the country. These mom and pop stores offer all kinds of items, are family run, and pay low wages and little to no rent.

This has enabled them to operate at an economics that is better than most — if not all — of their digital counterparts, and their scale allows them to offer unmatched fast delivery.

Krishna Shah, a New Delhi-based doctor, on paper is one of the perfect customers of e-commerce services. She lives in an urban city, uses digital payments apps and her earnings put her in the top 5% income level in the country. Yet, when she needed to buy food for her cats and needed it as soon as possible, she realized the major giants would take hours, if not longer. She ended up placing a call to a neighborhood store, which delivered the item within 10 minutes.

That neighborhood store, which employs fewer than half a dozen people, was competing with over a dozen giants and heavily funded startups including Grofers and BigBasket — and it won.

At stake is India’s retail market, which is estimated to be worth $1.3 trillion by 2025, from about $700 billion last year, according to Boston Consulting Group and the Retailers’ Association India. E-commerce, by several estimates, accounts for just 3% of the retail market in the country.

If that figure wasn’t small enough already, consider this: Some of the biggest customers of Flipkart and Amazon are these small retail stores. An executive with direct knowledge of the matter told TechCrunch that during some sales, as high as 40% of all smartphone units are bought by physical stores. The idea is, the executive said, to buy the devices at a discounted price, sit on them for a few days and when Amazon and Flipkart are done with their sales, sell the same phones at their standard prices.

Sujeet Kumar, co-founder of Udaan, a Bangalore-based startup that works with merchants, said that even as smartphones and the internet have reached all corners of India, e-commerce hasn’t been able to disrupt the retail market.

“The problem is that it is very difficult for e-commerce companies to build a supply chain and distribution network that is more efficient than those established by neighborhood stores. These mom and pop stores operate on an insanely different kind of cost economics. E-commerce companies are not able to match it,” he said.

Powered by WPeMatico

Mobile Premier League (MPL) has raised $90 million in a new financing round as the two-year-old Bangalore-based esports and mobile gaming platform demonstrates fast-growth and looks to expand outside of India.

SIG, early-stage tech investor RTP Global and MDI Ventures led MPL’s $90 million Series C financing round, with participation from existing investors Sequoia India, Go-Ventures and Base Partners. Times Internet is also an early investor in MPL. The new investment brings MPL’s to-date raise to $130.5 million. It was valued between $375 million to $400 million pre-money, according to a person familiar with the matter.

MPL operates a pure-play gaming platform that hosts a range of tournaments. The app, which has amassed more than 60 million users, also serves as a publishing platform for other gaming firms. MPL, which does not develop games of its own, hosts about 70 games across multiple sports on the app today.

It’s a heist! And it has gone rogue! Can you beat the others to win the game? Rogue Heist, India’s very own multi-player shooter game, coming soon on MPL! Here’s a sneak peek 😉 pic.twitter.com/PkVAjN2b4O

— Mobile Premier League (@PlayMPL) April 20, 2020

The Bangalore-based startup also offers fantasy sports, a segment that has taken off in many parts of India in recent years.

Because fantasy sports is only one part of the business, the coronavirus outbreak that has shut most real-world matches has not impeded the startup’s growth in recent months. The startup claimed it has grown four times since March this year, and more than 2 billion cash transactions have been recorded on the app to date.

“We’re competing with battle-hardened, decade old companies with much, much deeper pockets but it’s incredible what the young team has achieved over the past couple of years. When we were on the Play Store, a couple of years back, MPL was the fastest app to reach a 1M DAU ever in India!” tweeted Abhishek Madhavan, SVP of Marketing at MPL. “We signed Virat Kohli (pictured above), when we were a 3-month old company! When we got out of the Play Store, we were told growth will be very very hard to come by, every single marketing metric would fall.”

Sai Srinivas, co-founder and chief executive of Mobile Premier League, told TechCrunch in an interview that the new financing round validates that esports is here to stay and it is beginning to see its e-commerce moment.

“I believe that esports will be inducted by the Olympics way before than cricket does. And the market cap of esports will most probably will exceed those of all physical sports combined in the next 10 years,” he said.

“Even in an environment as challenging as the current one, we are impressed with the success and accessibility of the platform concept – giving users a unique variety of experiences and social interaction. MPL’s track record speaks for itself, so we’re excited to support the team as they grow and expand,” said Galina Chifina, managing partner at RTP Global, in a statement.

But since an aspect of MPL is about fantasy sports, its app is not available on the Google Play Store. Google Play Store prohibits online casinos, and other kinds of betting, a guideline Google reiterated last week as it pulled Indian financial services platform Paytm from the app store for eight hours. Srinivas declined to comment on Google and Paytm’s episode.

The startup plans to expand outside of India in the following months, said Srinivas. He did not name the new markets, but suggested that India’s neighboring countries as well as Japan and South Korea will likely be part of it.

The startup also plans to expand its gaming catalog and offer more marketing support to third-party developers, who currently either sell licenses to MPL or work through a revenue-sharing agreement with the Indian startup.

Powered by WPeMatico

Khatabook, a startup that is helping small businesses in India record financial transactions digitally and accept payments online with an app, has raised $60 million in a new financing round as it looks to gain more ground in the world’s second most populous nation.

The new financing round, Series B, was led by Facebook co-founder Eduardo Saverin’s B Capital. A range of other new and existing investors, including Sequoia India, Partners of DST Global, Tencent, GGV Capital, RTP Global, Hummingbird Ventures, Falcon Edge Capital, Rocketship.vc and Unilever Ventures, also participated in the round, as did Facebook’s Kevin Weil, Calm’s Alexander Will, CRED’s Kunal Shah and Snapdeal co-founders Kunal Bahl and Rohit Bansal.

The one-and-a-half-year-old startup, which closed its Series A financing round in October last year and has raised $87 million to date, is now valued between $275 million to $300 million, a person familiar with the matter told TechCrunch.

Hundreds of millions of Indians came online in the last decade, but most merchants — think of neighborhood stores — are still offline in the country. They continue to rely on long notebooks to keep a log of their financial transactions. The process is also time-consuming and prone to errors, which could result in substantial losses.

Khatabook, as well as a handful of young and established players in the country, is attempting to change that by using apps to allow merchants to digitize their bookkeeping and also accept payments.

Today more than 8 million merchants from over 700 districts actively use Khatabook, its co-founder and chief executive Ravish Naresh told TechCrunch in an interview.

“We spent most of last year growing our user base,” said Naresh. And that bet has worked for Khatabook, which today competes with Lightspeed -backed OkCredit, Ribbit Capital-backed BharatPe, Walmart’s PhonePe and Paytm, all of which have raised more money than Khatabook.

The Khatabook team poses for a picture (Khatabook)

According to mobile insight firm AppAnnie, Khatabook had more than 910,000 daily active users as of earlier this month, ahead of Paytm’s merchant app, which is used each day by about 520,000 users, OkCredit with 352,000 users, PhonePe with 231,000 users and BharatPe, with some 120,000 users.

All of these firms have seen a decline in their daily active users base in recent months as India enforced a stay-at-home order for all its citizens and shut most stores and public places. But most of the aforementioned firms have only seen about 10-20% decline in their usage, according to AppAnnie.

Because most of Khatabook’s merchants stay in smaller cities and towns that are away from large cities and operate in grocery stores or work in agritech — areas that are exempted from New Delhi’s stay-at-home orders, they have been less impacted by the coronavirus outbreak, said Naresh.

Naresh declined to comment on AppAnnie’s data, but said merchants on the platform were adding $200 million worth of transactions on the Khatabook app each day.

In a statement, Kabir Narang, a general partner at B Capital who also co-heads the firm’s Asia business, said, “we expect the number of digitally sophisticated MSMEs to double over the next three to five years. Small and medium-sized businesses will drive the Indian economy in the era of COVID-19 and they need digital tools to make their businesses efficient and to grow.”

Khatabook will deploy the new capital to expand the size of its technology team as it looks to build more products. One such product could be online lending for these merchants, Naresh said, with some others exploring to solve other challenges these small businesses face.

Amit Jain, former head of Uber in India and now a partner at Sequoia Capital, said more than 50% of these small businesses are yet to get online. According to government data, there are more than 60 million small and micro-sized businesses in India.

India’s payments market could reach $1 trillion by 2023, according to a report by Credit Suisse .

Powered by WPeMatico

WhatsApp, which began testing its mobile payments feature in India two years ago, could offer at least one more financial service to people in its biggest market.

In a filing with the local regulator in India, the company has listed credit as one of the areas it will pursue in the country. The Facebook -owned service declared with the local regulator earlier this month providing credit or loans as one of the “main objects to be pursued by it in the country.” No other financial service is listed in the filing.

At an event in Bangalore late last year, Abhijit Bose, WhatsApp’s head in India, said he believed that the mobile payments market in India, which has attracted dozens of local and international firms in recent years, is still at a very early stage in the country and may eventually see firms move beyond just offering a way for people to send money to one another.

WhatsApp has yet to receive approval from New Delhi for a nationwide rollout of Pay in India. Local media reports claimed earlier this year that WhatsApp had started to expand Pay’s reach in the country in various phases.

Ajit Mohan, a Facebook VP and India head, told TechCrunch in an interview last week that only 1 million WhatsApp users in India, same as before, have access to its mobile payment service.

Dozens of payment services in India have expanded to credit, or online lending, in recent quarters as they search for a business model in the country. A number of firms, including Paytm, India’s most-valued startup, and MobiKwik today offer small ticket credit to millions of users in India.

Tens of millions of users have started to digitally transact money in India in recent years. But the local payments body has removed most of the fees they could levy on banks and merchants to make money. The move has resulted in firms exploring other financial services, such as credit and insurance and target merchants to make money.

This year, Paytm has expanded to serve merchants, launching new gadgets such as a stand that displays QR check-out codes that comes with a calculator and a battery pack, a portable speaker that provides voice confirmations of transactions and a point-of-sale machine with built-in scanner and printer.

The Alibaba and SoftBank-backed company is offering these gadgets as part of a subscription service that helps it establish a steady flow of revenue. Paytm’s Money arm, which offers lending, insurance and investing services, has amassed more than 3 million users.

Flipkart’s PhonePe, another major player in India’s payments market, today serves more than 175 million users and over 8 million merchants. Its app serves as a platform for other businesses to reach users. The company is currently not taking a cut for the real estate on its app.

WhatsApp’s expansion in mobile payments in India, estimated to grow to $1 trillion by 2023 (according to Credit Suisse), could create new challenges for the aforementioned players.

Facebook, which like other American tech giants counts India as one of its biggest markets but makes considerably less revenue in the world’s second largest market, “reaffirmed” its commitment to India this month.

The social giant invested $5.7 billion in Reliance Jio Platforms this month to acquire a 9.99% stake in the Indian telecom giant. Over the weekend, JioMart, an e-commerce venture run by Jio’s parent firm, began testing an “ordering system” on WhatsApp, teasing the first peek at the collaboration between Facebook and Indian telecom giant Reliance Jio Platforms.

Powered by WPeMatico

More than six dozen startup founders, venture capitalists and lobby groups in India have requested the government to grant them a “robust relief package” to help combat severe disruptions their businesses face due to the coronavirus outbreak.

In a joint letter to India’s Prime Minister Narendra Modi, startups requested the government to bankroll 50% of their workforce’s salaries for six months, provide interest-free loans from banks, waive rent for three months and offer tax benefits among other things.

“Unfortunately, our startup companies across the nation are inherently young, less resilient and most vulnerable. Many of them face likely devastation during this extraordinary economic downturn. At this dire moment, Indian startups need a robust relief package from the government, lest all our collective efforts of the past few years are in vain,” they wrote.

Among those who have signed the letter include Mohit Bhatnagar, a managing director at Sequoia Capital, which is in advanced stages to close a fresh $1.3 billion fund for India and Southeast Asia, Gaurav Agarwal of online medicine store 1mg, Debjani Ghosh of industry body Nasscom, Karthik Reddy of Blume Ventures, Anand Lunia of India Quotient, Deepinder Goyal of Zomato, and Sriharsha Majety of Swiggy.

Some prominent startup founders and VCs including Vijay Shekhar Sharma of Paytm, and Ritesh Agarwal of Oyo, have also held a meeting with Piyush Goyal, the commerce minister in India, for a similar relief.

“We seek your urgent intervention to help ensure India’s startup ecosystem survives this crisis to emerge as a pillar of growth, employment and innovation to help drive India’s recovery. We need the startup ecosystem to survive in order to help the economy bounce back. We have enclosed herewith our submission for your kind consideration and we look forward to your support in this regard,” the joint letter reads.

The request for bailout comes amid a national lockdown in India that has disrupted countless businesses. New Delhi ordered a 21-day lockdown last month in a bid to curtail the spread of Covid-19.

Earlier this month, ten prominent VC and PE funds in India cautioned startups to brace for the “worst” months ahead.

“Assumptions from bull market financings or even from a few weeks ago do not apply. Many investors will move away from thinking about ‘growth at all costs’ to ‘reasonable growth with a path to profitability.’ Adjust your business plan and messaging accordingly,” they said.

As India, where the economy growth has been slowing for several quarters, scrambles to provide for its 1.3 billion citizens, the letter has drawn some criticism from industry figures.

Disappointed to see many startup leaders & investors that I admire add their names to this shameful letter to the govt asking for bailouts – surely at this time the govt has more important things to worry about than pay “50% of salary bills & contract wage bills paid by startups”

— Sumanth Raghavendra (@sumanthr) April 10, 2020

“I can’t fathom how such a list gets made in a country of more than a billion people who are facing a crisis unlike any they’ve seen before. A significant majority of them daily wage earners who have no financial cushion or any idea where their next meal is going to come from. Let’s not even stray into health and the need for medical emergencies; just putting three square meals on the table a day is proving to be impossible for so many,” wrote Ashish K. Mishra in a column on The Morning Context.

“At this very moment, it is they who need the government’s support. Not fat cats with bloated, middling business models and venture capital funds whose begging bowls are now seemingly larger than their risk appetite,” he added.

Companies asking for a bailout is not limited to India. Oil giants have sought similar help from the U.S. President Donald Trump — and VCs and startups are beginning to explore their option. Brent Hoberman, chairman and co-founder of Founders Factory and Firstminute Capital, urged the UK government to provide some relief to startups last month. But the government has yet to do much about it, just ask Deliveroo, Graphcore and other big UK startups.

Powered by WPeMatico

Vijay Shekhar Sharma, founder and chief executive of India’s most valuable startup, Paytm, posed an existential question in a recent press conference.

“What do you think of the commercial model for digital mobile payments. How do we make money?” Sharma asked Nandan Nilekani, one of the key architects of the Universal Payments Infrastructure that created a digital payments revolution in the country.

It’s the multi-billion-dollar question that scores of local startups and international giants have been scrambling to answer as many of them aggressively shift their focus to serving merchants and building lending products and other financial services .

New Delhi’s abrupt move to invalidate much of the paper bills in the cash-dominated nation in late 2016 sent hundreds of millions of people to cash machines for months to follow.

For a handful of startups such as Paytm and MobiKwik, this cash crunch meant netting tens of millions of new users in a span of a few months.

India then moved to work with a coalition of banks to develop the payments infrastructure that, unlike Paytm and MobiKwik’s earlier system, did not act as an intermediary “mobile wallet” to serve as an intermediary between users and their banks, but facilitated direct transaction between two users’ bank accounts.

Silicon Valley companies quickly took notice. For years, Google and the likes have attempted to change the purchasing behavior of people in many Asian and African markets, where they have amassed hundreds of millions of users.

In Pakistan, for instance, most people still run errands to neighborhood stores when they want to top up credit to make phone calls and access the internet.

With China keeping its doors largely closed for foreign firms, India, where many American giants have already poured billions of dollars to find their next billion users, it was a no-brainer call.

“Unlike China, we have given equal opportunities to both small and large domestic and foreign companies,” said Dilip Asbe, chief executive of NPCI, the payments body behind UPI.

And thus began the race to participate in the grand Indian experiment. Investors have followed suit as well. Indian fintech startups raised $2.74 billion last year, compared to 3.66 billion that their counterparts in China secured, according to research firm CBInsights.

And that bet in a market with more than half a billion internet users has already started to pay off.

“If you look at UPI as a platform, we have never seen growth of this kind before,” Nikhil Kumar, who volunteered at a nonprofit organization to help develop the payments infrastructure, said in an interview.

In October, just three years after its inception, UPI had amassed 100 million users and processed over a billion transactions. It has sustained its growth since, clocking 1.25 billion transactions in March — despite one of the nation’s largest banks going through a meltdown last month.

“It all comes down to the problem it is solving. If you look at the western markets, digital payments have largely been focused on a person sending money to a merchant. UPI does that, but it also enables peer-to-peer payments and across a wide-range of apps. It’s interoperable,” said Kumar, who is now working at a startup called Setu to develop APIs to help small businesses easily accept digital payments.

Vice-president of Google’s Next Billion Users Caesar Sengupta speaks during the launch of the Google “Tez” mobile app for digital payments in New Delhi on September 18, 2017 (Photo: Getty Images via AFP PHOTO / SAJJAD HUSSAIN)

The Google Pay app has amassed over 67 million monthly active users. And the company has found the UPI pipeline so fascinating that it has recommended similar infrastructure to be built in the U.S.

In August, the Federal Reserve proposed to develop a new inter-bank 24×7 real-time gross settlement service that would support faster payments in the country. In November, Google recommended (PDF) that the U.S. Federal Reserve implement a real-time payments platform such as UPI.

“After just three years, the annual run rate of transactions flowing through UPI is about 19% of India’s Gross Domestic Product, including 800 million monthly transactions valued at approximately $19 billion,” wrote Mark Isakowitz, Google’s vice president of Government Affairs and Public Policy.

Paytm itself has amassed more than 150 million users who use it every year to make transactions. Overall, the platform has 300 million mobile wallet accounts and 55 million bank accounts, said Sharma.

But despite on-boarding more than a hundred million users on their platform, payment firms are struggling to cut their losses — let alone turn a profit.

At an event in Bangalore late last year, Sajith Sivanandan, managing director and business head of Google Pay and Next Billion User Initiatives, said current local rules have forced Google Pay to operate in India without a clear business model.

Mobile payment firms never levied any fee to users as a strategy to expand their reach in the country. A recent directive from the government has now put an end to the cut they were receiving to facilitate UPI transactions between users and merchants.

Google’s Sivanandan urged the local payment bodies to “find ways for payment players to make money” to ensure every stakeholder had incentives to operate.

Paytm, which has raised more than $3 billion to date, reported a loss of $549 million in the financial year ending in March 2019.

The firm, backed by SoftBank and Alibaba, has expanded to several new businesses in recent years, including Paytm Mall, an e-commerce venture, social commerce, financial services arm Paytm Money and a movies and ticketing category.

This year, Paytm has expanded to serve merchants, launching new gadgets such as a stand that displays QR check-out codes that comes with a calculator and a battery pack, a portable speaker that provides voice confirmations of transactions and a point-of-sale machine with built-in scanner and printer.

In an interview with TechCrunch, Sharma said these devices are already garnering impressive demand from merchants. The company is offering these gadgets to them as part of a subscription service that helps it establish a steady flow of revenue.

The firm’s Money arm, which offers lending, insurance and investing services, has amassed over 3 million users. The head of Paytm Money, Pravin Jadhav, resigned from the company this week, a person familiar with the matter said. A Paytm spokeswoman declined to comment. (Indian news outlet Entrackr first reported the development.)

Flipkart’s PhonePe, another major player in India’s payments market, today serves more than 175 million users, and over 8 million merchants. Its app serves as a platform for other businesses to reach users, explained Rahul Chari, co-founder and CTO of the firm, in an interview with TechCrunch. The company is currently not taking a cut for the real estate on its app, he added.

But these startups’ expansion into new categories means that they now have to face off even more rivals, and spend more money to gain a foothold. In the social commerce category, for instance, Paytm is competing with Naspers-backed Meesho and a handful of new entrants; and heavily-backed OkCredit and KhataBook today lead the bookkeeping market.

BharatPe, which raised $75 million two months ago, is digitizing mom and pop stores and granting them working capital. And PineLabs, which has already become a unicorn, and MSwipe have flooded the market with their point-of-sale machines.

A vendor holds an Mswipe terminal, operated by M-Swipe Technologies Pvt Ltd., in an arranged photograph at a roadside stall in Bengaluru, India, on Saturday, Feb. 4, 2017. (Photographer: Dhiraj Singh/Bloomberg via Getty Images)

“They have no choice. Payment is the gateway to businesses such as e-commerce and lending that you can monetize. In Paytm’s case, their earlier bet was Paytm Mall,” said Jayanth Kolla, founder and chief analyst at research firm Convergence Catalyst.

But Paytm Mall has struggled to compete with giants Amazon India and Walmart’s Flipkart. Last year, Mall pivoted to offline-to-online and online-to-offline models, wherein orders placed by customers are serviced from local stores. The company also secured about $160 million from eBay last year.

An executive who previously worked at Paytm Mall said the venture has struggled to grow because its goal-post has constantly shifted over the years. It has recently started to focus on selling fastags, a system that allows vehicle owners to swiftly pay toll fees. At least two more executives at the firm are on their way out, a person familiar with the matter said.

Kolla said the current dynamics of India’s mobile payments market, where more than 100 firms are chasing the same set of audience, is reminiscent of the telecom market in the country from more than a decade ago.

“When there were just four to five players in the telecom market, the prospect of them becoming profitable was much higher. They were scaling like crazy. They grew with the lowest ARPU in the world (at about $2) and were still profitable.

“But the moment that number grew to more than a dozen overnight, and the new players started offering more affordable plans to subscribers, that’s when profitability started to become elusive,” he said.

To top that off, the arrival of Reliance Jio, a telecom operator run by India’s richest man, in 2016 in the country with the cheapest tariff plans in the world, upended the market once again, forcing several players to leave the market, or declare bankruptcies, or consolidate.

India’s mobile payments market is now heading to a similar path, said Kolla.

If there were not enough players fighting for a slice of India’s mobile payments market that Credit Suisse estimate could reach $1 trillion by 2023, WhatsApp, the most popular app in the country with more that 400 million users, is set to roll out its mobile payments service in the country in a couple of months.

At the aforementioned press conference, Nilekani advised Sharma and other players to focus on financial services such as lending.

Unfortunately, the coronavirus outbreak that promoted New Delhi to order a three-week lockdown last month is likely going to impact the ability of millions of people to use such services.

“India has more than 100 million microfinance accounts, serviced in cash every week by gig-economy workers, who hawk vegetables on street corners or embroider saris sold in malls, among other things. Three out of four workers make a living by working casually for others or at their family firms and farms. Prolonged shutdowns will impair their ability to repay loans of 2.1 trillion rupees ($28.5 billion), putting the world’s largest microfinance industry at risk,” wrote Bloomberg columnist Andy Mukherjee.

Powered by WPeMatico